Abstract

Multiple options for sustainable alternatives to fossil kerosene have been assessed. The route using biomass gasification, hotgas cleaning, hydrogen addition (derived from water electrolysis using renewable power), Fischer-Tropsch synthesis and product upgrading towards ASTM D7566 certified SAF has technical, economic and environmental advantages to be discussed in detail. The technical assessment shows carbon resp. energy efficiency of fuel production at 61% resp. 55%. The economic assessment of brown-field installations in Finland predicts costs in the range of 1.00 €2019/l. For the evaluation of 200 MWth biomass plus 160.2 MWe grid power plant size, an electricity price and biomass price of 42 €2019/t and 51 €2019/MWh were assumed, respectively. The environmental assessment shows a global warming potential reduction of 91% (corresponds to 8.8 gCO2-eq./MJFuel,LHV) compared to fossil fuel using Finnish wind energy and biomass residues, far better than the required 65% GWP reduction of the European RED II regulation. Based on the techno-economic and environmental assessment of the preferred FT route, a European deployment potential between 10 and 60 Mt/a SAF seems achievable in early 2030 years. The authors propose to implement appropriate regulation with high urgency.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

For more than a decade, the aviation sector has been searching for sustainable alternatives to fossil kerosene [1,2,3,4], with the aim to reduce its greenhouse gas (GHG) emissions and ever more requested by increasing policy demand, such as recent EU’s ‘ReFuelEU Aviation’ and U.S. ‘SAF Grand Challenge’ initiatives [5, 6] and the comprehensive net zero carbon strategy [7].

Multiple projects have been announced to introduce sustainable aviation fuels (SAF) globally in growing amounts [8]. All efforts summarized, there still remains a large gap between activities and goals (see Chapter 1.2). The authors are convinced that neither technological gaps nor the feedstock availability are causing the time lag and resistance towards sustainable aviation, but simply the costs of SAF compared to fossil kerosene and the remaining avoidance strategy to pay for this extra cost.

To encourage a much steeper ramp-up of SAF within this decade, the authors want to:

-

Distinguish between long-term promising SAF production pathways and others that are too limited for the required ‘sustainability revolution’, like envisioned and demanded in a recent Roland Berger report [9],

-

Introduce the pathway that promises the highest SAF potential in Europe achievable in the short term regarding local feedstock availability, process maturity and industrial production costs, while quantifying its global warming potential fairly and transparently,

-

Assess production costs and achievable GHG abatement,

-

Provide a fair forecast of possible European SAF production until 2030, if all stakeholders act on their capabilities and their share of fossil fuel consumption.

It will be shown that the technology for the production of SAF is mature and available, and costs and GHG abatement can be seriously predicted. To make sure, the assessment can be verified, a short explanation about the methodology, derived from standard chemical engineering cost estimation and extended towards GHG abatement calculation, is added.

1.1 Certified alternative jet fuels

Sustainable aviation fuels have to go through ASTM's D4054 certification process, which causes already many years of delay [10]. Any defense of that process due to security concerns should be questioned by current knowledge of hydrocarbon analytics according to the authors. As the chemistry and material properties of these drop-in fuels are almost identical compared to fossil kerosene, the certification procedure does not reflect that. Any discussion about non-drop-in fuels is left out of this discussion here, as it requires entirely new airplanes with an undefined year of introduction. Certified routes are subsequently listed in the Annexes of D7566. Since 2009, seven processes have been approved [11]. For all of these routes, multiple references can be found, that are not part of this discussion. A comprehensive summary of the status of each of the certified routes can be found i.a. in [12], hereinafter they are listed just for the sake of completeness.

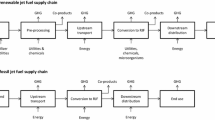

HEFA-SPKFootnote 1 process is currently the least expensive SAF option. In this process, oil is extracted and purified from various lipids that come from plant and animal fats, oils, and greases by chemical and mechanical processes. Subsequently, the lipids are converted into hydrocarbons by the treatment with hydrogen. The hydrocarbons are then cracked and isomerized according to the specifications for jet fuel. Many HEFA feedstocks, such as palm oil and soy, compete directly with food crops for agricultural areas and water. This leads to lower sustainability. However, as the real origin of feedstocks like used cooking oil (UCO) is often hidden, it is claimed as sustainable without any transparent proof [13]. One-third of the UCO used in Europe’s biofuels market was more than likely fraudulent in 2019 according to a source from the biofuel industry cited by EURACTIV.com [14]. It should be mentioned as well that the EU waste-based biodiesel association EWABA “rejects “in the strongest terms” these allegations from an unnamed source”. It cannot be the task of the aviation industry to proof the EU certification system for the sustainability of biofuels, but it has the responsibility of its feedstock supply. Additionally, a CE Delft estimation of the global potential for UCO doesn’t exceed 3.3 Mt/a [15], completely insufficient for the European aviation industry. Non-competing crop options that have a positive impact on sustainability and might increase the production potential are in the early stages of development, for example, algae for HC-HEFA.Footnote 2

Two further certified processes are the HFS-SIPFootnote 3 and the CHJFootnote 4 process. In the HFS-SIP process, sugar, extracted from sugar cane, is fermented with modified yeasts into a single 15-carbon sesquiterpene molecule known as farnesane. This molecule can be further hydrotreated and blended with the jet fuel up to a blending level of 10%. The CHJ process produces synthesized kerosene from lipids (like HEFA) using hydrothermal conversion with subsequent fractionation. Both processes compete with the usage of arable land, fertilizer potential food production, residual water demand, etc. In addition, both pathways are very high dependent on feedstock costs and availability in their production costs.

ATJ-SPKFootnote 5 fuel uses isobutanol or ethanol from the fermentation of starch-/sugar-producing feedstocks or from cellulosic biomass. The alcohol is then converted to jet fuel through dehydration, oligomerization, subsequent hydrogenation and fractionation. The crops used for the production of alcohol have high land and water use requirements, which in turn results in low sustainability and relatively high lifecycle carbon emissions [16].

A promising pathway is the Fischer–Tropsch (FT) process, its advantages are in detail explained later (see chapter 3). The production process requires synthesis gas, a mixture of CO and H2. The syngas can be produced from almost any carbon feedstock. Agricultural and forestry residues have the lowest lifecycle carbon footprint. Waste or industrial waste gases can also be used for syngas production. In the future, it should also be possible to obtain carbon from direct air capture processes. After the gas mixture has been separated and purified as required, long-chain hydrocarbons (up to solid waxes) are produced from the pure syngas by the FT synthesis process, and shorter molecules will be recycled. The wax is then cracked and isomerized to obtain the liquid drop-in fuel. The kerosene from the FT process has quite similar properties as petroleum-based jet fuel. Through the FT-SPK/AFootnote 6 process, a hydrocarbon mixture can be added to the fuel through additional alkylation of light aromatics, which contains the necessary aromatic compounds for jet fuel. Due to the possibility of producing jet fuel in the FT process via a biomass-and-power-to-liquid process (see chapter 4), this pathway can be very sustainable in combination with renewable energy and green hydrogen, as water and land usage, as well as lifecycle emissions are very low. In addition, significant economies of scale effects can be achieved by the future scale-up of the production (see chapter 6). Therefore, this process is preferred here for further analysis.

As all of these SAF have almost identical chemical components and material properties, co-processing in standard refineries is technically feasible and economically attractive; however, it is hindered by regulation and conflicting commercial interests.

1.2 Market activities of SAF

According to the International Air Transport Association (IATA), 65% of kerosene requirements must be provided by SAF to achieve the goal of net zero carbon emissions by 2050. This corresponds to an annual production of about 360 Mt/a, which must be provided till then [7].

In 2021, SAF production worldwide amounted to about 80 kt/a (100m liters [17]). Companies are already increasing their production in 2022, leading to an expected rise of 200% compared to 2021 (300m–450m liters [17]). The world's leading producer of sustainable fuels Neste increased its capacity to 500 kt/a SAF in Rotterdam and 1.3 Mt/a biofuels by the end of 2023 (SAF share not disclosed), the 2026 SAF production capacity is scheduled at 2.2 Mt/a [18]. An important U.S. producer is World Energy with its production site in Paramount. Production is expected to increase from today's 14 kt/a to almost 800 kt/a by 2025 [19]. Other European companies have also entered SAF production. The Italian manufacturer Eni produces 10 kt/a at the Livorno refinery in northwestern Italy. The goal is to reach a production capacity of up to 500 kt/a by 2030 [20]. The French producer TotalEnergies can produce up to 100 kt/a at its refinery in La Mede. In 2024, capacity is to be increased by up to 170 kt/a through the refinery in Grandpuits [21]. The Spanish company Repsol plans to start up the first advanced biofuels plant in Cartagena in 2023 with a total capacity of around 240 kt/a [22]. These examples might show that all activities together amount only a tiny fraction of the European kerosene demand of about 60 Mt/a pre-Corona.

The majority of production processes are based on plant-based lipids or various waste products (HEFA, see above [23]). FT-SPK synthesized from water, CO2 and renewable electricity (Power-to-Liquid, PtL) is currently only produced in initial test plants. These include, for example, the plant in Emsland, which was inaugurated in 2021 and will provide about 20 t/a for Lufthansa Cargo [24]. Some countries are trying to drive SAF production through policy regulations.

Several countries have already stated their blending limit or production capacity goals, respectively. An exemplary list is given in Table 1.

The current maximum blending limit of SAF with conventional kerosene is only 50%, although the chemical properties are similar. Blending is only necessary because some conventional fuel components cause the seals in older engines to swell and prevent fuel leaks [25]. In addition to increasing the blending limit, other policy programs are needed to incentivize increased SAF production. These may include support for investments to build feedstock harvesting and fuel production infrastructure, to reduce the current cost premium of SAF production, and to lower feedstock competition with other sectors [27].

1.3 Assessment of SAF concepts

With many options for SAF production, additional prospects for future certification and the need for accelerated ramp up a merit order of GHG abatement cost and amount would be helpful. A variety of options for large-scale production of kerosene and other fuels with significantly reduced greenhouse gas emissions have been investigated at the Institute of Engineering Thermodynamics (DLR-TT) since 2012 [28,29,30,31]. Based on experimental data received from different research and development projects, process chains have been developed, evaluated and optimized [29]. The standardized methodology, utilized in this study, allows the analysis of system interconnection and process optimization for different production processes and scale-up prediction towards the industrial dimension. It is described in detail in different publications and shortly explained below. Process flow models, validated with experimental project results, are set up with commercial simulation software to map the overall processes as a prerequisite for upscaling of test plants to future commercial plants. Important results of the technical assessment after the best possible process integration are the carbon efficiency (carbon ratio of biomass converted into fuels, Eq. 1), fuel efficiency (ratio of the FT product’s energy content to the energy input, Eq. 2) and process efficiency (ratio of the FT + by-products energy content to the energy input Eq. 3) [32]:

whereas \({\dot{m}}_{C,prod}, {\dot{m}}_{C,biom}\) are the carbon flows of product and feedstock, \({\dot{m}}_{prod}LH{V}_{prod}\), \({\dot{m}}_{biom}LH{V}_{biom}\) are the energy flows (product of mass flow rate and lower heating value) of the product resp. feedstock, and \({P}_{el}\) is the electricity for the process.

An automated link of process simulation and cost estimation in the techno-economic process evaluation tool (TEPET) enables rapid comparison of different plant concepts [30]. [33] The conducted evaluations stand out by their transparency and standardization of the techno-economic analysis (TEA). The economic analysis provides a cost breakdown of the capital expenditure (CAPEX) of a brown-field installation (reduced costs for required infrastructure, such as service, storage, and transportation facilities), based on available feedstock costs and local conditions of the operating costs and finally the net production costs (NPC) in the year of installation. For a detailed description of the applied methodology and cost assumptions, please refer to [31]. The following equations provide the NPC for the base year 2019:

where as FCI is the fixed capital investment, calculated using a reference equipment cost (EC), a reference capacity (D) and specific equipment’s degression factors (d). Feco represents additional factors for installation, and electrical systems (more details are provided in [31]). Based on the interest rate IR (here: 7%) and a defined plant lifetime PL, (here: 20 a) as well as the working capital (which is set to 10% of FCI) the annualized capital costs (AAC) are estimated. NPC add indirect operational costs OPEXind (maintenance, laboratory charges, etc.), direct operational costs OPEXdir (electricity, feedstock costs, etc.) and labor costs (number of employees NP multiplied by their salary clabor), per amount of product, usually per kilogram or per liter, sometimes per energy unit like MJFuel,LHV.

During its continuous development at DLR, the approach and tool have been extended by a life cycle assessment (LCA) based on the same automated process simulation link. LCA results are calculated with the open-source framework brightway2 [34] and evaluate the lump-sum climate impacts (global warming potential over 100-year period, GWP in gCO2-eq./MJ) as well as further environmental impacts, e.g., land use, water use, acidification. Background data are taken from ecoinvent 3.8 database [35]. Environmental impacts are assessed with the Environmental Footprint method EF v3.0 no LT [36]. Detailed information about the methodology, assumptions and input data can be found in [37]. Important results of the combined techno-economic and ecological assessment include the greenhouse gas (GHG) abatement cost:

This factor sets the NPC increase of alternative fuel (AF) compared to fossil fuel (FF) in relation to the global warming potential (GWP) savings. The fossil fuel cost NPCFF is calculated with a crude oil price of 0.48 €2019/l [38, 39] and an additional 0.03 €2019/l for refining [39, 40]. For GWPFF the REDII fossil fuel comparator value of 94 gCO2-eq./MJ is used [41]. The energetic refinery efficiency is accounted for with 93.5% [42] and the lower heating values of fossil diesel and the FT-diesel are 36.1 MJ/l [43] and 32 MJ/l [37], respectively. Since there are more impact categories than just GWP, another metric, the cost-impact factor, was introduced in [37]. The factor considers all environmental impact savings or added burdens in relation to the added cost of alternatives compared with fossil fuel. However, this factor was not included in this publication.

By applying this methodology to a variety of different process concepts, a merit order of a potential roll-out of the production of alternative fuels can be identified.

2 SAF feedstock availability

Looking at all certified processes for the production of SAF (see chapter 1.1) the feedstock availability will define the degree of possible blending ratios, meaning that the remaining rest will sustain fossil. The entire EU-wide wheat, sugar and rapeseed harvest could not even achieve 50% of the EU wide aviation fuel demand [44] while absorbing the European food resources. Hence, the search for widely available sustainable carbon and hydrogen is key for sustainable aviation.

2.1 Carbon sources

Sustainable carbon sources to be considered are forest or agricultural residues or other organic waste streams, but renewables utilization competition might limit its aviation share. European biomass feedstock availability is often questioned despite serious assessments by the European Commission [45], Joint Research Center [46], Imperial College [47] and others. Even if the potential looks sufficient, it still has to be discovered how each supply chain can be established locally in order to feed multiple continuously running fuel production sites. Well-established gasification technologies can be utilized for biomass-based pathways, as gasifier technology derived from coal gasification for different sizes is commercially available [48,49,50]. Additionally, CO2 can be captured from flue gases of industrial plants with washing solutions [51]. Selexol and Rectisol are exemplary certified processes that capture CO2 from gaseous streams in an absorber column. The disadvantage of CO2 as a carbon source is the energy demand for removing two oxygen atoms with hydrogen (2*H2 eq. 3.05 kWhH2.LHV/kgCO2 or 4.75 kWhe/kgCO2, if produced by water electrolysis), producing 2 mols of expensive water for each mol of carbon. The efforts for gaining green carbon are even higher by extracting from the air (direct air capture, DAC), adding an additional 0.25 kWhe/kgCO2 plus 1.75 kWhth/kgCO2 electricity and heat demand [52].

2.2 RE/Hydrogen

Another option to add sustainability to future SAF (beside bimass) is the addition of renewable hydrogen gained from renewable electricity via water/steam electrolysis. In combined Power-and-Biomass-to-liquid (PBtL) processes the carbon efficiency can be increased by hydrogen addition (see chapter 5). The availability question has to be answered here as well, keeping in mind the rather slow replacement velocity of fossil power generation in Europe, if aviation requires additional renewable electricity on top. However, a renewable electricity request in the range of 0.6 PWh/aFootnote 7 for aviation should not be out of range compared with the EU’s “economically competitive wind energy production potential” of 30.4 PWh/a for 2030, envisioned by the European Environment Agency more than a decade ago [53]. A recent study increases that figure stating that “realizable onshore wind power potential throughout Europe is much larger (138 PWh/a)” [54]. It remains questionable, whether the speed of renewable wind (and other) energy capacity installation would be sufficient for aviation needs as well. If Europe increases its wind power capacity up to 427 GW until 2030 (EU-27 according to [55], assuming a power generation of 0.88 PWh/a), only one-third of the current European kerosene requirements could be met. However, aviation can be a strong buyer and promoter, if regulation will be set accordingly.

Based on feedstock availability, as the shortage of renewable electricity in Europe is much more limiting large-scale SAF production than biomass availability, the deployment should start with biomass alone and be supplemented with renewable power according to its expansion speed.

3 Fischer–TROPSCH-based SAF concepts

With the brief review of available SAF options and constraints above, we now focus on a mature, large-scale available process of certified liquid hydrocarbon production for aviation. Almost any source of hydrogen and carbon can be utilized to produce intermediate syngas for FT-SPK production. Coal and natural gas are examples of conventional but ineligible feedstocks, as its kerosene production would cause more GHG emissions (addition rather than abatement) than a crude-oil-based one [56]. As stated above, either biomass or captured CO2 can be utilized as sustainable carbon source together with sustainable hydrogen produced by electrolysis with renewable electricity sources [28, 29] (see chapter 2). Details about what that process might look like, the advantages and drawbacks of adding hydrogen from renewable power, estimated production costs and GHG abatement will be described in the following chapter. We are using publicly available results of the EU project FLEXCHX [31], adapted to the gasification model published in [57]. A switch between the biomass-to-liquid (BtL) and the PBtL operation mode shows the advantages of both concepts.

4 FLEXCHX approach for seasonal market response

The process concept proposed in the EU-project FLEXCHX offers a flexible adaptation of renewable energy conversion in Europe: The fuel process converts biomass to liquid hydrocarbons via the FT route. With heat demand in the winter season, an adjacent combined heat and power (CHP) plant uses the process off-heat to generate district heating and electrical power (biomass alone operation mode, chapter 4.1). Whenever cheap renewable electricity is available, an electrolysis unit is operated to enhance the fuel yield (electrolysis-assisted operation mode, chapter 4.2). Especially in the summer season PV power might be available and no heat is required in Northern Europe [58]. The PBtL mode requires less biomass feedstock to produce an equal amount of FT product compared to the BtL mode. Yet, the higher biomass conversion has to be weighed against the additional cost for the electrolysis power demand.

The two operation modes are shown in Fig. 1.

Operation modes for the hybrid process concept [31]. Operation modes for the hybrid process concept

4.1 Biomass alone (BA) operation mode

The biomass alone mode is depicted in a schematic flow diagram in Fig. 2. In a first step, the biomass moisture content is reduced in the dryer. With the addition of oxygen and steam the dry biomass is converted to raw syngas in a circulating fluidized bed (CFB) gasifier. Besides hydrogen and carbon monoxide, the syngas also contains carbon dioxide, steam, tars, ash and other trace components like ammonia or hydrogen sulfide. Components poisoning the FT catalyst are removed in a gas cleaning process. The auto-thermal tar reformer reduces the tar content while simultaneously increasing the H2/CO ratio of the syngas. Oxygen for gasifier and reformer is produced in a cryogenic air separation unit (ASU).

Schematic flow diagram for the BA mode (top) and EA mode (bottom) [31]

Clean syngas reacts over the FT catalyst to hydrocarbon chains. Here, hydrocarbon chains with a chain length higher than five carbons are considered product and are separated from the shorter hydrocarbons. Further upgrading steps such as cracking of longer chains will lead to FT-SPK according to ASTM D7566 (see chapter 1.1). This upgrading step is not modelled here but is included here with a standard refinery oil processing fee. FT tail gas consisting of short hydrocarbons and unconverted syngas is partly recycled to the reformer or leaves the process (off-gas) to be burned. The energy content of the off-gas is used in the CHP.

4.2 Electrolysis assisted (EA) operation mode

To reach the stoichiometric FT feed ratio of H2/CO ~ 2, hydrogen from the electrolyzer is added. Double carbon recycle A) via CO2 recycle from gas cleaning to the gasifier and B) as tail gas to the reformer leads to a higher carbon efficiency. The electrolyzer byproduct oxygen is sufficient to feed the gasifier and reformer, making the ASU obsolete.

In summary, the hybrid system is a combination of BtL [48] and PBtL [59] processes. Yet, depending on the operation mode, either the ASU (EA mode) or the electrolyzer is inactive (BA mode).

5 Technical assessment of FLEXCHX concept

A process model based on the experimentally confirmed unit performance was built using the commercial software Aspen Plus® (V10). A detailed description of all modeling assumptions is given in [31].

A carbon efficiency of 35.4% (Eq. (1)) was found for the BA mode. As depicted in the Sankey diagram in Fig. 3, the remaining carbon is removed from the process as CO2, off-gas and ash.

Carbon flow Sankey diagram for BA mode (top) and EA mode (bottom) [31]

An advantage of the EA mode is the carbon efficiency of 61.1%. In BA mode, steam addition, needed to reach the defined H2/CO ratio in the autothermal sour shift reactor, causes higher CO2 production. In the EA mode, no additional steam is introduced. Instead, the H2/CO ratio is adjusted with electrolytic H2.

Fuel and process efficiency (Eqs. 1, 2 and 3) are found to be higher in the BA mode compared to the EA mode cf. Table 2. This is mainly due to the additional energy loss in the electrolyzer. The energy streams for BA and EA mode are depicted in Fig. 4 Here, it can be seen that of the 200 MWLHV biomass input in BA mode 57.6% is converted to fuel, 18.8% to district heating and 1.1% to electricity. The bulk of the generated electricity is used for the auxiliary process power requirement. In the EA mode, the remaining electricity is fed to the AEL. Thereby, the electricity demand from the grid can be reduced from 187.9 MWel to 160.2 MWel. With that 55.2% of process power input can be converted to FT fuel, while 18.4% are converted to district heating.

Energy flow Sankey diagram for BA mode (bottom), EA mode (top) (chemical or thermal power in orange, electrical power in red)

6 Economic assessment of FLEXCHX concept

The economic analysis for this hybrid process was conducted with DLR’s software tool TEPET. For a detailed description of the cost calculation, please refer to [31].

NPC of 1.08 and 1.04 €2019/l for continuous operation in BA (biomass price 18.0 €/MWhth) and EA mode (electricity price 55.49 €/MWhe) are found, each one valid for it's own season of the hybrid plant. The BtL and PBtL process (plants for one operation mode build only), in contrast, have NPC of 0.66 and 1.00 €2019/l (cf. Table 3). The difference in NPC for BA and BtL or EA and PBtL is due to the lower investment cost. As the electrolysis unit and CO2 recycle are not implemented in the BtL plant, only 50.9% of the FCI has to be considered relative to the hybrid plant. Similarly, PBtL has 92.2% of the FCI for the hybrid plant.

A sensitivity study for the electricity price is conducted to show under what conditions the hybrid operation would be economically advantageous. Figure 5 displays the production costs for the process in EA and BA mode for an electrical price range from -40 to 80 €/MWh. The resulting production costs of the plant operated half a year in BA and half a year in EA mode are denoted as 50–50. Further, the production costs for a BtL and a PBtL plant of the same size are shown.

Variation of electricity price for EA and BA mode in comparison to BtL and PBtL. The light blue line (50–50) signifies the production costs if the process is operated half a year in BA and EA mode each [31]

The PBtL and BtL comparator production costs stay below those of EA and BA mode, respectively. This is due to the investment costs of temporarily inactive equipment. The inactive electrolyzer accounts for most of the price spread between the BA mode and the BtL comparator.

The EA mode would have to be operated for the entire year at a price of 8 €/MWh to achieve the production costs of a BtL plant. If the EA mode is only operated for half a year electricity prices of below -40 €/MWh would have to be available for the same time period to reach the BtL price level.

7 Ecological assessment of FLEXCHX concept

The LCA for the hybrid process concept was conducted with the extension of DLR’s TEPET tool [37]. The environmental impacts of the FLEXCHX process were distributed between the FT product, district heating and electricity according to energetic allocation. Moreover, not only the production of FT product was included in the LCA but also its refining to FT-diesel, the distribution, and its usage in a medium-sized passenger car. Since this publication focuses on SAF production, it has been assumed as a simplification that the distribution and use phases of FT diesel and FT kerosene do not differ greatly in terms of environmental impacts. There are no differences in assessment up to the refined product. However, for the sake of accuracy, all results are labeled with FT diesel.

Figure 6 shows the GWP of both operation modes in comparison to the renewable energy directive (REDII [41]) 65% limit and fossil fuel comparator value (94 gCO2-eq./MJ) [41] with their main contributors. Additionally, two different energy sources are compared for EA mode. Finnish wind electricity comes with an individual impact of 18 gCO2-eq./kWh while the Finnish grid mix has one of 259 gCO2-eq./kWh in the ecoinvent 3.8 (allocation, cut-off by classification) database [35]. The total GWP amounts to 7.7, 8.8 and 52.2 gCO2-eq./MJFT-diesel for BA mode, EA mode with wind energy and EA mode with grid energy, respectively. When the carbon efficiency is increased in EA compared to BA mode, the GWP contribution from biomass supply and its transport decreases while electricity for the electrolyzer operation becomes a new contributor. Overall, the REDII 65% limit can be achieved for both modes when electricity is provided by wind energy.

Global warming potential of the FLEXCHX process in BA and EA mode using Finnish wind resp. current grid electricity

If the biomass transport distance is not 100 km, like it was assumed in the base case, but closer to 300 km, EA mode can become favorable with respect to the GWP (see Fig. 7). While the GWP increases with longer transport distances, the biomass availability does as well which in turn allows for plants with higher capacity and reduced NPC through economy of scale. Hence, transport distance in dependence on biomass availability is an important but highly variable factor when deciding on the size and mode of the plant.

Sensitivity of the global warming potential to varying biomass transport distances

To assess potential trade-offs in other impact categories when transitioning to the renewable alternative, the environmental impacts of the FLEXCHX FT-diesel are compared with those of fossil diesel. Figure 8 displays the environmental impacts of BA and EA mode normalized to fossil diesel. Out of 16 categories, the comparison with fossil diesel shows a reduction in impact in 11 (BA) or 10 (EA) categories. Additionally, BA has smaller impacts than EA in 7 categories, higher in 5, and roughly equal impacts in 4 categories. Impact increases in the categories of water use and land use are to be expected in comparison with fossil diesel as these ones are minimal during crude oil extraction and refining. Therefore, these categories should only be of concern when local conditions call for it or when different biomass sources are compared with each other.

Environmental impact of the FT-diesel in comparison with fossil diesel for BA and EA mode

The GHG abatement cost is calculated to be 255 €2019/tCO2-eq. (BA mode), 243 €2019/tCO2-eq. (EA mode, wind energy) and 495 €2019/tCO2-eq. (EA mode, grid energy).

8 Development of European SAF installation roadmap

Towards a large-scale production of SAF in Europe, a comprehensive and plausbile prediction of production costs, ecological impact and SAF production volume is of great importance. With DLR’s road mapping approach, a region-specific answer can be provided for a multitude of processes. In [60], the PBtL is compared to the BtL process in terms of aggregated European production volume and national production costs as well as GHG emissions. Further, in [30] a study on the optimal BtL process design depending on the local production conditions entailing biomass price or steam selling price is presented for Central Europe. Here, the study focuses on the production conditions on a regional level (NUTS2 regions, according to the Nomenclature of territorial units for statistics).

In [60], fuel output for BtL and PBtL was calculated on the basis of the EU’s availability for forest (FR) and agricultural residues (AR) (40 and 139 Mtdry/a [61]), as shown in Fig. 9. Here, the possible SAF production is compared to the expected total jet fuel demand of 2030 in the EU [60]. As the higher benchmark, it was assumed that all biomass residue is converted to fuel. As other sectors might compete for the biomass residue in unknown shares, the maximum amount of fuels needs to be adjusted accordingly. The process design details are taken from the unit behavior described in chapter 4.

Maximum fuel production potential using European forestry residue (blue) and agricultural residue (orange) for the PBtL and the BtL process. [60]

With the assumptions made in chapter 4, it can be shown that the PBtL process can produce double the amount of FT syncrude compared to BtL. The PBtL product amount could even cover the EU’s domestic aviation fuel demand of 2030, which is estimated to be about 63 Mt/a [61]. It highlights the advantage of the PBtL process to increase fuel output from the limited biomass resources. However, utilizing the entire EU biomass residue potential for SAF production would be very optimistic. Other means of fuel provision would have to be pursued. If these other means are connected to higher GHG footprints than PBtL fuel, a rapid ramp-up of PBtL production capacity should be prioritized to limit the detrimental effects of air travel on the environment.

However, lump sum figures of potential European SAF production are not reliable, as the local availability of both biomass and renewable electricity has to be considered. According to the Nomenclature of territorial units for statistics (NUTS), minimum and maximum population thresholds for the size of a region are given (NUTS2: between 800′000 and 3′000′000 residents). These conditions include the local availability and costs for straw and forestry residues, electricity costs, biomass transport distances, labor and district heating prices.

As an example, local production costs for different BtL process options are determined in [30], based on results of the EU Horizon 2020 project COMSYN, as shown in Fig. 10. Net Production Cost for BtL production in central Europe, using optimal process design have been adapted to specific local production conditions [30]. When a final upgrading step in the refinery in Litvinov, Czech Rep. (red cross) is assumed, transport efforts of FT product from multiple BtL plants to the refinery have to be considered. As shown in [30], the B-C1-SC2 design option is the most prevalent in Central Europe, where electricity is produced from the BtL process’ off-heat. Contrarily, for regions with low electricity prices, maximizing the steam and district heating production with the off-heat is the more cost-effective solution (case B-C1-SC0 in [30]). Accordingly, a European SAF roadmap for the PBtL pathway described above will be developed shortly.

Net Production Costs for BtL production in central Europe, using optimal process design adapted to specific local production conditions [30]

9 Summary and outlook

This study provides a comprehensive overview of prospective large-scale SAF production routes. Based on a discussion of all currently certified jet fuels and related market activities, this work takes a deeper look at the FT pathway, as both wasted biomass as well as renewable power can be utilized for maximum production rates. A techno-economic analysis reveals production costs of around 1 €2019/l under Finnish market conditions. A corresponding LCA study finds that the same process can produce low-GHG fuel, if Finnish wind power is used for the production of hydrogen. The addition of hydrogen to this process has the benefit of roughly doubling the fuel output from equal biomass input. Thereby, the total biomass residue availability would suffice for the production of more than 60 Mt/a, which equals the jet fuel demand in the EU by 2030. From these findings the following conclusions can be drawn:

-

Current SAF activities concentrate on 1st generation biofuels with limited growth potential and conflict with farmland usage. The short-term production increase is announced, but ambitious long-term aviation goals are not achievable that way. It is questionable, how long this insufficient pathway should be supported.

-

Searching for large-scale SAF production opportunities needs to focus on:

-

o

cheap renewable carbon sources and sufficient renewable electricity,

-

o

market ready conversion technology,

-

o

already certified alternative jet fuels.

-

o

-

The combination of gasification of unused biomass, preferably hotgas cleaning, hydrogen addition (derived from water electrolysis using renewable power), FT synthesis and product upgrading towards ASTM D7566 certified jet fuel seems the most promising pathway regarding deployment speed, cost and GHG abatement. It doesn't mean that this pathway is easily affordable nor sufficient for a net-zero aviation, but viable and proven sustainable.

-

With the process knowledge of former EU projects, a European SAF roadmap for either BtL or PBtL can be developed. With the higher carbon utilization of the PBtL concept, a first rough guess using available waste wood and renewable power of up to 60 Mt/a SAF capacity by 2030 can be strived for. While for the BtL pathway, a first Central European draft was published as shown in Fig. 10 [30], for the PBtL pathway a serious analysis will be published soon. Here a comprehensive insight into the PBtL SAF potential based on the local combined availability of biomass residue and (renewable) power is provided. The economic and ecologic analysis finds regions in Europe which can meet ambitious cost and GHG emission targets. A large-scale deployment of the PBtL concept until 2030 is not hindered by any technological gap according to the author’s findings, the price premium compared to fossil kerosene schould not be expected to decline anytime soon.

-

Only ambitious deployment goals set by European regulation will encourage steep and immediate SAF implementation. It will require a new industry of large-scale green carbon valorization for aviation, despite expected competition of future use, and a massive increase in renewable power generation far beyond current electricity market needs.

-

European refineries will have to adopt the technology to gradually replace fossil crude oil processing in favor of future SAF production. Each refinery will need its own renewable feedstock supply with short transport distances and long-year delivery contracts.

A dedicated European SAF roadmap beyond ReFuelEU Aviation [5] and focusing on the domestic unused biomass and renewable power can guide to meaningful sustainable aviation in a short period of time. That would be in line with the EU’s ambition to limit the rise in global temperature to 1.5 °C and to avoid the most severe consequences of climate change. Regulation will have to request the immediate market transition; individual refinery renovation will make it succeed.

Data availability

All data will be made available on request.

Notes

Hydrotreated Esters and Fatty Acids (HEFA) are chain-length distributed alkanes, building saturated paraffinic kerosene (SPK).

HEFA produced from oils found in a special algae (botryococcus braunii).

Hydroprocessed Fermented Sugars to Synthetic Isoparaffins (HFS-SIP) process utilizes a fermentation process to convert a sugar feed stock.

Catalytic Hydrothermolysis Jet fuel (CHJ, also called hydrothermal liquefaction) uses clean free fatty acid (FFA) oil from the processing of waste oils or energy oils.

Alcohol to jet (ATJ) was certified for isobutanol feedstock first, ethanol feedstock was included later. It produces saturated paraffinic kerosene (SPK) as well.

FT-SPK/A is a variation of the FT process where a fully-synthetic alternative aviation fuel containing produces saturated paraffinic kerosene (SPK) and aromatics is produced.

Assuming a power demand of 0.8 MWe/MWfuel.LHV(cf. Figure 4),

please note: 1 PWh = 109 MWh = 1015 Wh).

References

D. Pham. "American and Alaska Airlines Complete World’s First Commercial Biofuel Flights," 06 February, 2023; https://inhabitat.com/american-and-alaska-airlines-complete-worlds-first-commercial-biofuel-flights/.

Aviation Initiative for Renewable Energy in Germany e.V. (aireg). "Successful launch of aireg with 25 members," 06 February, 2023; https://aireg.de/en/successful-launch-of-aireg-with-25-members/.

IATA. "IATA Sustainable Aviation Fuel Roadmap," 06 February, 2023; https://www.iata.org/contentassets/d13875e9ed784f75bac90f000760e998/safr-1-2015.pdf.

S. v. Dyk, and J. Saddler. "Progress in Commercialization of Biojet/Sustainable Aviation Fuels (SAF)," 06 February, 2023; https://www.ieabioenergy.com/wp-content/uploads/2021/06/IEA-Bioenergy-Task-39-Progress-in-the-commercialisation-of-biojet-fuels-May-2021-1.pdf.

European Union Aviation Safety Agency. "Fit for 55 and ReFuelEU Aviation," 06 February, 2023; https://www.easa.europa.eu/en/light/topics/fit-55-and-refueleu-aviation.

The White House (2021) "Biden Administration Advances the Future of Sustainable Fuels in American Aviation". https://www.whitehouse.gov/briefing-room/statements-releases/2021/09/09/fact-sheet-biden-administration-advances-the-future-of-sustainable-fuels-in-american-aviation/

IATA. "Our Commitment to Fly Net Zero by 2050", 2021, https://www.iata.org/en/programs/environment/flynetzero/

S. Csonka. "Aviation’s Market Pull for SAF," 12 May, 2022; https://www.caafi.org/focus_areas/docs/CAAFI_SAF_Market_Pull_from_Aviation.pdf.

Robert Thomson, and A. Healy. "Sustainable aviation fuels key for the future of air travel," 06 February, 2023; https://www.rolandberger.com/en/Insights/Publications/Sustainable-aviation-fuels-key-for-the-future-of-air-travel.html.

CAAFI. "ASTM D4054 Users Guide," 06 February, 2023; https://caafi.org/information/pdf/D4054_Users_Guide.pdf.

IATA. "Sustainable Aviation Fuel: Technical Certification," 06 February, 2023; https://www.iata.org/contentassets/d13875e9ed784f75bac90f000760e998/saf-technical-certifications.pdf.

J. Holladay (PNNL), Z. Abdullah (NREL), and J. Heyne (U. of Dayton) “Sustainable aviation fuel: review of technical pathways”, U.S. Department of Energy, Office of energy efficiency and renewable energy, 2020. https://www.energy.gov/sites/default/files/2020/09/f78/beto-sust-aviation-fuel-sep-2020.pdf

Moskowitz, E., Asani, M., Sys, M.: How biofuels scams have undermined a flagship EU climate policy, https://www.occrp.org/en/investigations/how-biofuels-scams-have-undermined-a-flagship-eu-climate-policy, 4.7.2023

S. Michalopoulos. "Industry source: one third of used cooking oil in Europe is fraudulent," 20.08.2023; https://www.euractiv.com/section/all/news/industry-source-one-third-of-used-cooking-oil-in-europe-is-fraudulent/?utm_campaign=further_reading.

A. van Grinsven, R. van der Veen, B. Kampman "Used cooking oil (UCO) as biofuel feedstock in the EU", CE Delft, 2020. https://cedelft.eu/wp-content/uploads/sites/2/2021/04/CE_Delft__200247_UCO_as_biofuel_feedstock_in_EU_FINAL-v5.pdf

Geleynse, S., Brandt, K., Garcia-Perez, M., Wolcott, M., Zhang, X.: The Alcohol-to-Jet Conversion Pathway for Drop-In Biofuels: Techno-Economic Evaluation. Chemsuschem 11(21), 3728–3741 (2018)

IATA. "2022 SAF Production Increases 200 %: More Incentives Needed to Reach Net Zero," 19.02., 2023; https://www.iata.org/en/pressroom/2022-releases/2022-12-07-01/.

Neste. "FAQ about SAF," www.nest.com/releases-and-news.

R. Silk. "World Energy is doing a big expansion of its sustainable aviation fuel refinery," 02 February, 2023; https://www.travelweekly.com/Travel-News/Airline-News/World-Energy-expansion-sustainable-aviation-fuel-refinery.

Eni Group. "Eni launches sustainable aviation fuel production " 02 February, 2023; https://www.eni.com/en-IT/media/press-release/2021/10/pr-eni-launches-sustainable-aviation-fuel-production.html.

Argus Media. "Total starts biojet production at La Mede biorefinery," 02 February, 2023; https://www.argusmedia.com/en/news/2203248-total-starts-biojet-production-at-la-mede-biorefinery.

Repsol Global. "Repsol starts construction of Spain's first advanced biofuels plant at its Cartagena refinery," 02 February, 2023; https://www.repsol.com/en/press-room/press-releases/2022/repsol-starts-construction-of-spains-first-advanced-biofuels-plant-at-its-cartagena-refinery/index.cshtml.

SkyNRG. "Technology Basics," 02 February, 2023; https://skynrg.com/sustainable-aviation-fuel/technology-basics/.

Lufthansa Group. "Lufthansa supports world's first production plant for CO2-neutral, synthetic aviation fuels", 2021, https://cleantechhub.lufthansagroup.com/en/focus-areas/alternative-fuels-and-emissions/atmosfair.html

European Commission. "Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on ensuring a level playing field for sustainable air transport," https://ec.europa.eu/info/sites/default/files/refueleu_aviation_-_sustainable_aviation_fuels.pdf.

TotalEnergies. "Total Begins Producing Sustainable Aviation Fuel in France," 2 February, 2023; https://totalenergies.com/media/news/press-releases/total-begins-producing-sustainable-aviation-fuel-in-france.

ICAO. "Guidance on potential policies and coordinated approaches for the development of sustainable aviation fuels," 2 February, 2023; https://www.icao.int/environmental-protection/Documents/SAF/Guidance%20on%20SAF%20policies%20-%20Version%201.pdf.

D. H. König (2016) TÖB der Herstellung synthetischen Flugturbinentreibstoffes aus CO2 und H2,” PhD Thesis

Albrecht, F.G., König, D.H., Baucks, N., Dietrich, R.-U.: A standardized methodology for the techno-economic evaluation of alternative fuels: a case study. Fuel 194, 511–526 (2017)

Maier, S., Tuomi, S., Kihlman, J., Kurkela, E. and Dietrich, R.-U.: Techno-economically-driven identification of ideal plant configurations for a new biomass-to-liquid process – A case study for Central-Europe. Energy Convers. Manag. 247, 114651 (2021). https://doi.org/10.1016/j.enconman.2021.114651

Habermeyer, F., Kurkela, E., Maier, S. and Dietrich, R.-U.: Techno-economic analysis of a flexible process concept for the production of transport fuels and heat from biomass and renewable electricity. Front. Energy Res. 9 (2021). https://www.frontiersin.org/articles/10.3389/fenrg.2021.723774. https://doi.org/10.3389/fenrg.2021.723774

Habermeyer, F., Kurkela, E., Maier, S., Dietrich, R.-U.: Techno-Economic Analysis of a Flexible Process Concept for the Production of Transport Fuels and Heat from Biomass and Renewable Electricity. Front. Energy Res. 9, 684 (2021)

Federal Ministry for Economic Affairs and Energy. "The National Hydrogen Strategy," https://www.bmbf.de/bmbf/shareddocs/downloads/files/bmwi_nationale-wasserstoffstrategie_eng_s01.pdf?__blob=publicationFile&v=2.

Mutel, C.: Brightway: An open source framework for Life Cycle Assessment. J. Open. Sour. Softw. 2(12), 236 (2017)

Wernet, G., Bauer, C., Steubing, B., Reinhard, J., Moreno-Ruiz, E., Weidema, B.: The ecoinvent database version 3 (part I): overview and methodology. Int. J. Life Cycle Assess. 21(9), 1218–1230 (2016)

Fazio, S., Biganzioli, F., De Laurentiis, V., Zampori, L., Sala, S., Diaconu, E.: Supporting information to the characterisation factors of recommended EF Life Cycle Impact Assessment methods: Version 2 from ILCD to EF 3.0, European Commission. https://publications.jrc.ec.europa.eu/repository/bitstream/JRC114822/tr_supportingcf_final_online.pdf (2018)

Weyand, J., Habermeyer, F., Dietrich, R.-U.: Process design analysis of a hybrid Power-and-Biomass-to-Liquid process: An approach combining life cycle and techno-economic assessment, Fuel 342, 127763 (2023). https://doi.org/10.1016/j.fuel.2023.127763

en2x. "Average annual OPEC crude oil price from 1960 to 2022 (in U.S. dollars per barrel)," 20.09.2022; https://www.statista.com/statistics/262858/change-in-opec-crude-oil-prices-since-1960/.

Statista. "Euro (EUR) to U.S. dollar (USD) exchange rate from January 1999 to September 2, 2022," 20.09.2022; https://www.statista.com/statistics/412794/euro-to-u-s-dollar-annual-average-exchange-rate/.

Neste Corporation, Financial Statements Release for 2019. https://www-old.neste.com/sites/neste.com/files/release_attachments/neste_financial_statements_2019.pdf (2020)

European Parliament, "Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the promotion of the use of energy from renewable sources (recast)". https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2018.328.01.0082.01.ENG (2018)

Han, J., Forman, G.S., Elgowainy, A., Cai, H., Wang, M., DiVita, V.B.: A comparative assessment of resource efficiency in petroleum refining. Fuel 157, 292–298 (2015)

Engineering ToolBox. "Fossil and Alternative Fuels - Energy Content," 24.08.2022; https://www.engineeringtoolbox.com/fossil-fuels-energy-content-d_1298.html.

Dietrich, R.-U., Simon, M., Weyand, J., Adelung, S., Habermeyer, F., Raab, M., Rahmat, Y.P.: Advanced biofuels production research and assessment The aviation point of view. Achema Pulse 2021, 15.-18.6.2021, Online Webinar. https://elib.dlr.de/143493/ (2021)

European Commission, DG Research and Innovation, Borzęcka, M., Oberč, B., Haffner, R. et al.: Research and innovation perspective of the mid-and long-term potential for advanced biofuels in Europe—Final report, Publications Office. https://data.europa.eu/doi/10.2777/37969 (2017)

Ruiz, P., Nijs, W., Tarvydas, D., Sgobbi, A., Zucker, A., Pilli, R., Jonsson, R., Camia, A., Thiel, C., Hoyer-Klick, C., Dalla Longa, F., Kober, T., Badger, J., Volker, P., Elbersen, B.S., Brosowski, A., Thrän, D.: “ENSPRESO–an open, EU-28 wide, transparent and coherent database of wind, solar and biomass energy potentials,” Energy Strategy Reviews, vol. 26, 100379, ISSN 2211-467X. https://doi.org/10.1016/j.esr.2019.100379 (2019)

Panoutsou, C., Maniatis, K.: "Sustainable biomass availability in the EU to 2050", Imperial College London. https://www.concawe.eu/wp-content/uploads/Sustainable-Biomass-Availability-in-the-EU-Part-I-and-II-final-version.pdf

Ail, S.S., Dasappa, S.: Biomass to liquid transportation fuel via Fischer Tropsch synthesis–Technology review and current scenario. Renew. Sustain. Energy Rev. 58, 267–286 (2016)

Sikarwar, V.S., Zhao, M., Fennell, P.S., Shah, N., Anthony, E.J.: Progress in biofuel production from gasification. Prog. Energy Combust. Sci. 61, 189–248 (2017)

Kurkela, E., Kurkela, M., Hiltunen, I.: Pilot-scale development of pressurized fixed-bed gasification for synthesis gas production from biomass residues. Biomass Conv. Bioref. 13, 6553–6574. https://doi.org/10.1007/s13399-021-01554-2 (2023)

Albrecht, F.G., Nguyen, T.V.: Prospects of electrofuels to defossilize transportation in Denmark: a techno-economic and ecological analysis. Energy 192, 116511. https://doi.org/10.1016/j.energy.2019.116511 (2020)

Fasihi, M., Efimova, O., Breyer, C.: Techno-economic assessment of CO2 direct air capture plants. J. Clean. Prod. 224, 957–980 (2019)

European Environment Agency (EEA) "Europe's onshore and offshore wind energy potential. An assessment of environmental and economic constraints", Office for Official Publications of the European Communities. https://data.europa.eu/doi/10.2800/11373 (2009)

Enevoldsen, P., Permien, F.-H., Bakhtaoui, I., Krauland, A.-K.V., Jacobson, M.Z., Xydis, G., Sovacool, B.K., Valentine, S.V., Luecht, D., Oxley, G.: How much wind power potential does europe have? Examining european wind power potential with an enhanced socio-technical atlas”. Energy Policy 132, 1092–1100 (2019)

EurObserv'ER Wind Energy Barometer 2022. https://www.eurobserv-er.org/wind-energy-barometer-2022/ (2022)

Davis, B.H., Occelli, M.L. (eds.): Fischer-Tropsch synthesis, catalysts, and catalysis: advances and applications, 1st edn. CRC Press. https://doi.org/10.1201/b19455 (2016)

Hannula, I.: Hydrogen enhancement potential of synthetic biofuels manufacture in the European context: A techno-economic assessment. Energy 104, 199–212 (2016)

Kurkela, E., Kurkela, M., Frilund, C., Hiltunen, I., Rollins, B., Steele, A.: Flexible Hybrid Process for Combined Production of Heat, Power and Renewable Feedstock for Refineries: Managing seasonal energy supply and demand for heat and power in Europe. John. Matth. Technol. Rev. 65(2), 333–345 (2021)

Hillestad, M., Ostadi, M., Serrano, G.A., Rytter, E., Austbø, B., Pharoah, J., Burheim, O.S.: Improving carbon efficiency and profitability of the biomass to liquid process with hydrogen from renewable power. Fuel 234, 1431–1451 (2018)

Habermeyer, F., Weyand, J., Maier, S., Kurkela, E., Dietrich, R.-U.: Power biomass to liquid—an option for Europe’s sustainable and independent aviation fuel production. Biomass Convers Biorefin. 1–19 https://doi.org/10.1007/s13399-022-03671-y (2023)

J. O’malley, N. Pavlenko, and S. Searle (2021) Estimating sustainable aviation fuel feedstock availability to meet growing European Union demand, International Council on Clean Transportation.

Acknowledgements

Some of the process information used in this study is taken from the EU Horizon 2020 projects FLEXCHX and COMSYN. The financial support of the FLEXCHX project, which has received funding from the European Union’s Horizon 2020 research and innovation Programme under Grant Agreement No 763919, is gratefully acknowledged. The financial support of the COMSYN project, which has received funding from the European Union’s Horizon 2020 research and innovation Programme under Grant Agreement No 727476, is gratefully acknowledged.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

A techno-economic and ecological assessment of possible large-scale sustainable aviation fuels production in Europe is provided. Based on that assessment, a production pathway was assessed with maximum energy and carbon usage, moderate costs, meaningful greenhouse gas abatement and large deployment potential. The Fischer-Tropsch based route of kerosene, with gasification of unused biomass, hotgas cleaning, hydrogen addition (derived from water electrolysis using renewable power), FT synthesis and product upgrading towards ASTM D7566 certified SAF promises a cost range of about 1 €2019/l (Finish market conditions), a global warming potential of less than 10 gCO2-eq./MJFuel,LHV, and a European deployment potential between 10 and 60 Mt/a kerosene by 2030.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Dietrich, RU., Adelung, S., Habermeyer, F. et al. Technical, economic and ecological assessment of European sustainable aviation fuels (SAF) production. CEAS Aeronaut J 15, 161–174 (2024). https://doi.org/10.1007/s13272-024-00714-0

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13272-024-00714-0