Abstract

The financial well-being of the charity sector has important social implications. Numerous studies have analysed whether the concentration of income in a few sources increases financial vulnerability. However, few studies have systematically considered whether the type of income (grants, donation, fund-raising activities) affects the survival prospects of the charity. We extend the literature by (a) explicitly modelling the composition of sources of income, (b) allowing for short-term volatility as well as long-term survival and (c) testing alternative specifications in a nested form. We show that the usual association between income concentration per se and financial vulnerability is a specification error. Greater vulnerability is associated with dependence on grant funding, not overall concentration. Previous studies showing that concentration of income per se is problematic are picking up a proxy effect. We also show that the volatility of income streams may be an important factor in the survival of charities, but that this also varies between income sources.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In the UK, the charitable sector generates income of about £40bn per year (2% of GDP; Keen 2015). The UK ‘Big Society’ programme (HM Government 2011) has resulted in the third sector playing a central role in the delivery of particular social and welfare services: one-fifth of UK charities report provision of social services as their primary form of activity income (Keen 2015; NCVO 2017).

Despite the critical role NPOs perform, there are concerns regarding their lack of long-term sustainability (Charities Aid Foundation 2017; Foundation for Social Improvement 2017). Bingham and Walters (2013) note that political support for the third sector does not necessarily translate into increased funding. Moreover, Wilsker and Young (2010) and Bingham and Walters (2013) both argue that the income stream affects the preferred delivery model; increased government support can therefore create an internal tension between the organisation’s mission and its funding source.

Much analysis has been carried out on the role that the revenue streams have on the financial vulnerability or survival prospects of the charity; the meta-analyses of Hung and Hager (2019) and Lu et al. (2019) list some 50 papers on this theme. However, the great majority of these focus on whether the concentration of income from a single type source, per se, creates instability in the organisations.

An important question, rarely tackled in the literature, is whether those different funding streams affect the financial viability of the organisation. Wilsker and Young (2010) argue that a lack of alignment between income and delivery streams increases the inefficiency and vulnerability of the organisation. Frumkin and Keating (2011) argue that concentrating on a small number of income streams increases efficiency. Qualitative analyses (e.g. Bingham and Walters 2013) show an awareness amongst managers of the importance of the social and political environment to funding streams. But while papers such as Myser (2016) and Duquette (2017) consider the type of funding, these are the exception rather than the rule.

This paper directly considers whether the type of funding affects survival prospects. NPOs receive income from three main sources: grants, which are fixed sums to achieve a specific outcome; income arising from the activities of the NPO, such as shop revenue, fees for paid-for services, or fund-raising events; and donations and legacies. These revenue streams have quite different implications for the organisation. For example, an organisation focused on day-to-day fund-raising activities is likely to have quite a different management structure from one that focuses on grant applications as its main income source. Kingston and Bolton (2004) argue that grant income is a poor funding mechanism as it is time-limited and with no guarantee of renewal. A particular interest in the UK is the expressed preference of the UK government 2010–2015 for the increased use of grant funding: did this create a systemic vulnerability in the sector?

There has also been relatively little research on the variability of incoming and expenditure streams, but this is clearly a related issue. As Kingston and Bolton (2004) note, grant income offers very high predictability during the period of the grant but uncertainty outside the grant award. Activity income is variable but predictable and somewhat under the control of the NPO. Donations and legacies are outside the control of the NPO but for long-established organisations can be highly predicable. It may be that the type of activity is itself less important than the effective forecasting of income.

This article seeks to extend understanding of the vulnerability of NPOs by examining the survival prospects of 153 UK charities, focusing particularly on the type and volatility of funding streams. We do this by nesting the concentration measure in a broader regression framework to allow complex factors to be distinguished, and for the different models to be compared for their explanatory power. Key findings are that (1) the type of income is more relevant than the concentration of revenue and (2) volatility of costs and income does indeed matter.

We take an empirical perspective, in line with most of the previous studies (Helmig et al. 2014); as Lu et al. (2019) note, there are good theoretical arguments for revenue concentration either increasing or decreasing survival prospects. Rather than considering all the determinants of financial vulnerability, we focus on testing the dominant finding that concentration of income is itself a risk factor. This is the stylised fact which our results challenge.

Literature Review: Financial Distress and Financial Vulnerability

There is a wide theoretical literature on what makes nonprofits operate in the way that they do; Helmig et al. (2014) provide a survey of how these models of management have been used to analyse financial vulnerability, distress and survival. However, there is a substantial identification problem: the same findings (for example, that nonprofits facing financial distress appear to stay in operation longer than for-profits) can be consistent with many different theories. In addition, many of the papers in this area appear prompted by the desire to give directly applicable advice to nonprofits, at least compared to other social science research articles. As a result, as Helmig et al. (2014) note, most studies ignore the link between theory and hypothesis in favour of identifying associations between nonprofit characteristics and outcomes.

Conceptual Framework

We continue this empirical approach. However, this still entails basic decisions about the concepts being examined. Compared to for-profit organisations, nonprofits have a different legal framework, a different set of motivations, and access to different sources of income. Analysts have therefore had to adapt the for-profit literature to the financial situation of charities and NPOs.

As Myser (2016) discusses, there is a substantial difference between strategic concerns (something in the organisation’s way of working that may lead to a catastrophic failure but which may not be causing current problems) and ‘financial distress’ (an ongoing management problem). Myser (2016) further splits the strategic problem into shorter-term ‘capacity’ and longer-term ‘sustainability’. Financial distress may be experienced by any organisation, but it seems likely that the particular characteristics of NPOs (in particular, the ‘mission’ of Abraham 2003) may lead to them operating with a level of strategic risk that a for-profit firm would not accept. For the purpose of this section, we adopt the term ‘financial vulnerability’ to cover the general prospects for the NPO, aware that its meaning is ambiguous.

Identifying financial distress and vulnerability in an NPO is not straightforward, particularly for charities. As Abraham (2003, p. 1) notes: ‘Once [the mission of the NPO] is defined, an NPO often finds that it is unable to withdraw …Thus, the centrality of mission to the operation of an NPO may expose it to issues of financial sustainability that are not faced by organisations operating in other sectors.’ For example, Arya and Mittendorf (2014) argue that high programme expenditures, rather than administrative efficiency, become performance targets.

Tuckman and Chang’s (1991) framework for financial vulnerability of nonprofit organisations provides the starting point for most quantitative analysis in this field. They argue that four variables (strength of the equity base, concentration of income sources, share of administrative costs and net margin) provide useful indicators of an NPO’s vulnerability; we refer to these as the ‘vulnerability variables’. For 4700 nonprofits, each of these variables was ordered and then split into quintiles, where being in the bottom quintile was defined as being ‘vulnerable’. In their analysis, 42% of the NPOs studied were vulnerable on at least one metric and 1% on all four.

However, these metrics reflect relative performance (being in the bottom quintile) rather than an absolute measure of failure risk; hence, 20% of NPOs are always classed as ‘vulnerable’ even if overflowing with assets and income. In fact, if the four variables were distributed randomly among the NPOs, we would expect 41% to be vulnerable on one measure and 0.1% on all four. This implies very little correlation between metrics in the Tuckman and Chang dataset; indeed, Hager (2001) for the US and Thomas and Trafford (2013) for the UK report negligible bivariate correlation between metrics.

Despite the limited insight in the original paper, the idea that revenue concentration is an important indicator of financial vulnerability has proved popular. Tuckman and Chang’s (1991) proposals have been taken up by three groups of researchers: those who carry out descriptive analyses similar to Tuckman and Chang’s (1991) paper; those who compare the variables and metrics to other predictors of business performance; and those who use the variables in regression models to test the association with vulnerability. We review each of these groups in turn.

The first group, accepting the four rank-based metrics as indicators of relative vulnerability, use them to describe risk in particular sectors or organisations. Omar et al. (2013) and Thomas and Trafford (2013) both consider variations over sectors and time to identify changing vulnerability in particular clusters. Lohmann and Lohmann (2000) urge NPOs to accept the metrics as a measure of risk. Abraham (2003) applies the metrics to a single large charity to argue that, on these measures, the charity in question is unexpectedly vulnerable.

The second group have argued that the usefulness of the vulnerability variables can be tested against the models used to evaluate for-profit businesses. Keating et al. (2005), revised as Gordon et al. (2013), compare the performance of the vulnerability variables against two well-established business models (Altman 1968; Ohlson 1980) and find that no model has much predictive power. They then combine the variables from all models, plus two additional variables; in this model, the vulnerability variables are generally significant and with the expected signs. This suggests that it is the parsimony of the original Tuckman and Chang (1991) model that is at fault (that is, the metrics have too diffuse an impact to be detected in simple models). Tevel et al. (2014) compare the vulnerability variables, Ohlson (1980) and two ‘practitioner’ models. They argue that, if the variables have explanatory power, observing a ‘vulnerable’ NPO should be a good predictor for still finding it vulnerable some time later. On this measure, they find that the vulnerability variables are better predictors of long-term vulnerability. However, it could be argued that this finding merely reflects greater persistence of the vulnerability variables and the metrics based on them: a nonprofit may remain in the bottom quintile even if its absolute performance has improved.

The third, and largest, group of researchers use regression models to test the determinants of ‘financial vulnerability’ (defined in various ways), with the vulnerability variables included alongside others such as size or sector of the nonprofit. In these studies, the focus is usually on the coefficient associated with revenue concentration.

Greenlee and Trussel (2000) appear to be the first paper to do this, finding financial concentration associated with increased vulnerability, as are lower administrative costs and lower margins; equity is found to be insignificant. Hager (2001) applies the model to the arts sector; all four vulnerability variables have the expected signs, but statistical significance varies widely between different types of organisation. Trussel (2002) and Trussel and Greenlee (2004) include size of organisation as well as sector: larger organisations are found less likely to be financially vulnerable. Hu and Kapucu (2015) include management metrics and changes in the sources of funding. Prentice (2015) includes macroeconomic variables (state/national output) as explanatory variables and finds them to be significant. Myser (2016) uses a range of additional variables but not all of the vulnerability variables. Searing (2018) adds the age of the organisation, citing management studies showing both internal experience and external networks improve resilience. Unusually, Searing (2018) models ‘recovery from vulnerability’ rather than vulnerability itself, providing an opportunity to consider whether the routes into and out of vulnerability are the same.

Apart from Prentice (2015), most analysis uses probabilistic modelling of a binary outcome. However, where multiple observations over time on the same organisations are available, alternative specifications are possible; Hager et al. (2004) and Burde et al. (2017) apply survival analysis techniques to generate hazard functions for the probability of failure. Searing (2018) uses a panel data set with repeat periods of vulnerability, but treats the vulnerable periods as independent events rather than multiple events for the same body.

Most authors find that higher equity ratios and higher margins should be associated with higher survival prospects or less distress. There is more debate about the impact of administrative costs as a share of revenue. Tuckman and Chang (1991) proposed low administrative costs as indicators of vulnerability: an organisation with more ‘administrative fat’ to cut should survive any downturn better. Statistical studies generally support this view. However, Ecer et al. (2017) argue that financial efficiency is an indication of good management: resilient organisations adopt the same approach as for-profit firms. Thomas and Trafford (2013) find that administrative costs as a share of income appear to fall during a period of relative prosperity for the UK charity sector, suggesting that those charities do not use good times as a chance to ‘store fat’. This does not directly refute the argument that an ability to cut waste is important for staving off financial problems. Moreover, it is not clear how well the ‘pure’ administrative cost is measured: some activities may be easily allocated to ‘administration’ and ‘programme work’ but others, such as overarching management or estates costs, are much more difficult to allocate. Thomas and Trafford (2013) argue financial regulations give charities an incentive to under-report administrative expenditure.

Choice of Outcome Variable

One difficulty facing the multivariate analyses is the outcome variable. Strategic vulnerability could be approximated by failure, allowing for the fact that strategic vulnerability may not lead to failure, and failure may be due to reasons other than strategic vulnerability. However, the analysis of US NPOs dominates the field, and there is often no direct measure of failure as in the US it is not possible to force charities into bankruptcy or reorganisation. Good datasets on NPO failures are not widely available: four out of five papers with actual failure rates use data collected manually (Hager 2001; Hager et al. 2004; Fernandez 2008; Green et al. 2016).

Research to date therefore usually focuses on indirect measures of ‘distress’. Gilbert et al. (1990) suggest that three years’ worth of net losses indicates distress in for-profits. Greenlee and Trussel (2000) argue that distress in NPOs is better proxied by years of falling service expenditure. Greenlee and Trussel (2000) set the template for most subsequent studies, which tend to use similar measures. Hence, financial ‘vulnerability’ can often mean ongoing financial distress.

Studies with a ‘survival’ variable (Hager 2001; Hager et al. 2004; Fernandez 2008; Burde et al. 2017) argue that survival is the more relevant variable for NPOs. Myser (2016) carried out two separate analyses using ‘distress’ and ‘sustainability’ as outcome variables. Myser argues that the factors that underlie the two outcomes are significantly different, but also indicates that common variables have common impacts. This suggests the distinction between current and strategic problems is important but may not be crucial.

Some authors, rather than committing to a specific measure of financial health, have used multiple measures. Gordon et al. (2013), for example, use four different outcome measures. Searing (2018) compares insolvency and ‘financial disruption’ as alternative measures of vulnerability and finds statistically important differences in outcomes. Prentice (2015) argues that treating vulnerability as dichotomous is unnecessarily restrictive and ignores the interaction of financial indicators which might be in conflict. His analysis using a continuous composite index suggests that this can be a more effective proxy.

Findings on Revenue Concentration

Income concentration in these studies is calculated using a Herfindahl index. For organisation i, let Iis be the income from source s, and Ti total income; then, the concentration ratio ci is calculated as

The value of this ranges from 1/s (income spread equally amongst sources) to 1 (all income from one source). Studies repeatedly show (Greenlee and Trussel 2000; Hager 2001; Hager et al. 2004; Trussel 2002; Trussel and Greenlee 2004; Carroll and Slater 2009; Hu and Kapucu 2015; Prentice 2015) that this is positively related to vulnerability: that is, more concentrated income is associated with the organisation suffering financial or strategic problems. Hung and Hager (2019) carry out a meta-analysis of 40 analyses and report an overall positive and statistically significant effect.

However, Hung and Hager (2019) note that the effect is small, as it is counterbalanced by a number of contrary or insignificant findings. For example, Chikoto and Neely (2014) and von Schnurbein and Fritz (2017) find that revenue concentration is positively associated with growth in funds and revenue, respectively, strengthening the financial base of the charity. Frumkin and Gordon et al. (2013) find that revenue concentration is strongly associated with greater efficiency and, by implication, long-term survival. Berrett and Holliday (2018) show that greater concentration of income is associated with a lower range of output goods and services, and therefore more specialisation, but this is not directly linked to survival. The meta-analysis of 23 papers in Lu et al. (2019) also questions the evidence for any relationship. Their review suggests that concentration has a negligible effect on financial vulnerability, although it does appear to be positively related to financial capability.

Table 1 summarises a selection of regression analyses on nonprofit survival or vulnerability. It highlights significant findings in respect of the four metrics commonly used, which approximate to the original Tuckman and Chang (1991) variables, including financial concentration. ‘+ve’ and ‘−ve’ indicate statistically significant positive or negative findings, respectively; ‘ns’ indicates a variable was included but was not found to be significant. Some articles with very similar models/findings are omitted; for a full review, see Hung and Hager (2019) or Lu et al. (2019).

Compared to the number of papers that include a concentration index in their analysis, very few authors have considered whether studying the components of income is more useful. Hager et al. (2004) find a negative association between the share of income from donations and the failure rate of NPOs. Myser’s (2016) analysis includes grant dependence as a separate explanatory variable and finds it to be insignificant; this contrasts with Green et al. (2016) who found it highly significant. This may reflect a US/UK split in the funding environment. Green et al. (2016) argue that grant funding in the UK is unpredictable, whereas in the USA Myser (2016) proposes that it should be more stable (or at least predictable) than other income sources. However, Hager et al. (2004) find that US government funding is associated with higher failure risk, though access to funding is measured as a simple dummy variable rather than a value. Duquette (2017), while not looking specifically at survival, notes that charities appeared to view grants, activity income and donations as qualitatively different types of revenue.

Apart from these four papers, few works directly analyse the type of funding. Carroll and Slater (2009) discuss it, but only analyse it via the concentration index. Hu and Kapucu (2015), Kim (2014) and Ecer et al. (2017) all analyse components of income, but not as direct indicators of vulnerability.

It is worth considering the mechanism through which different income streams matter. As Wilsker and Young (2010) and Kingston and Bolton (2004) note, different income streams have different predictability, and if one stream is dominant, this is likely to affect the management structure of the nonprofit. It may be that this is the factor which ultimately determines survival prospects. However, structure is hard to identify, although Hu and Kapucu (2015) provide proxies, and as such this is little explored.

This paper will extend this literature in three ways. First, we explicitly study the composition of sources of income. Second, we use a nested specification to allow the explanatory power of revenue concentration and revenue source to be compared. Third, we introduce measures of volatility in income and costs, as a way of exploring organisational flexibility.

Methods and Data

This paper focuses on UK charities using public financial data obtained from the Charities Commission website, where all UK charities must submit financial accounts for each accounting year. ‘Survival’ is determined by whether the charity is reported as operating or closed in 2015, having operated for at least four years previously. There appears to be no up-to-date list of UK charities that have ceased operations and so convenience sampling is used for non-continuing charities, and quota sampling for the matching set of continuing charities.

Charities identified as having ceased operations are identified through recent news articles within the year 2016–2017. Only recent closures could be studied as The Charities Commission stops publishing information for charities that have ceased operating; this leaves a short window between the announced closure of the charity and the removal of its financial information. Thirty ‘small’ charities (average income under £1 m per year) and 20 ‘large’ charities are selected. This oversamples large charities that are much less likely to close.

Continuing charities are selected randomly from the website to provide a quota sample with the same size distribution across surviving and non-continuing charities. With a larger population to choose from, we chose a larger sample size, identifying 52 small charities and 51 large charities.

In theory quota sampling could have used other criteria in addition to size, such as sector and financial status. However, matching samples by more characteristics reduces the opportunity to identify outcomes as a result of those characteristics.

Company accounts for the years 2010–2015 are examined. The start date was chosen to coincide with the new policy regime and to avoid over-sampling of long-lived charities. The end date was chosen as the last full year for which accounts would be reasonably available for all charities. A later start date would have increasing data points for surviving firms, but also increase the chances of a ‘survivor’ sample biased towards well-managed firms with good administrative processes. Table 2 shows the number of observations, whilst Table 3 shows the number of years worth of data available for each charity.

Most charities had either 5 or 6 years of data; for non-continuing charities, the data were most likely to be missing for 2015, the year of closure. It would have been feasible to only select continuing charities with a full 6 years of data. This was not a selection criterion as it was thought likely to bias the continuing sample towards stable charities with good record-keeping.

As noted in the literature review, most authors do not distinguish between financial vulnerability and financial distress. We use vulnerability in Myser’s (2016) definition of ‘strategic risk to operations’, identified through closure of the charity by 2015. The rationale for using this rather than ‘distress’ arises from our interest in income stream dependency as a strategic risk. Charities may close because of an extended period of financial distress, but they may also close because of a catastrophic loss of funding, which may not be preceded by any period of financial distress (for example, the closure of the UK charity Kids Company following withdrawal of its primary source of income, government grants).

The point of evaluation is either the last year before ceasing operations or (in the case of continuing charities) the year before the last observed period. For most charities, this means using the data reported for 2014, so that dead and surviving charities are assessed on the same basis. Four charities closed in 2014 but only accounts for 2010–2013 are available, so 2013 accounts were used.

It could be argued that taking data from the last year of operation misrepresents the true vulnerability of the charity as the event leading to the closure of the charity may already have taken place. If this is the case, the charity’s accounts will reflect an exceptional state, and the estimated coefficients will be biased towards zero. As a robustness check, we tried alternative specifications, including the use of average values over the period, discussed below.

The Basic Model

Our starting point is the standard model involving the four vulnerability variables:

Financial concentration, like the rest of the literature, is measured as a Hirschman–Herfindahl concentration index for income sources. Charity Commission income data is classified under four categories: grant funding, charitable activities, donations and ‘other’ income, which includes money from sources including investment or reimbursements. The latter category is very small, 2% of total income on average, and so this is excluded from the analysis. Grant income includes both government grants and grants from other charitable foundations.

Where no income information is supplied in one of the categories, we set this to zero on the basis that the company does not recognise this form of income. Income data supplied by charities do not equal the sum of the component parts. In 90% of cases, the difference is negligible (under 0.5%) and for 97% of cases under 10%. The larger errors are more likely to occur in live charities and, with one exception, do not appear in the year of closure; this seems to rule out a potential reason for the gap: charities ‘banking’ promised monies but not actually receiving it and so going into liquidation. We therefore recreate the total income for the organisation by summing the relevant components rather than using the reported ‘total’.

Equity is assessed by net asset value. This is assumed to be accurately reported. Three charities show negative net assets, but Framjee (2008) notes that this can occur for a number of reasons and does not necessarily imply anything about the financial state of the charity. It is calculated as a share of total income to normalise it across different-sized operations, in line with previous studies. We multiply by 12 to represent the months of income cover in the case of total loss of income, for ease of presentation in the figures below; this does not affect the estimates.

Margin is defined as income less costs, as a share of income. In our case, we model it equivalently as the total costs as a share of total income, which has the statistical advantage of restricting its range to positive values.

We do not have a direct measure of ‘administrative costs’ from these data. Previous papers assume that ‘administrative costs’ are non-programme costs, i.e. those not directly related to delivery of the service, such as fund-raising. As an attempt to proxy this, we have included staff costs as a percentage of income. The rationale is that organisations may find that staffing costs may give more or less scope for cost cutting in times of financial hardship, compared to other costs.

Costs (annual total and staff expenditure) and reserves are taken as reported, as setting these omitted variables to zero is implausible. One small charity was missing these data and is omitted, leaving 152 valid observations for the multivariate analysis from the original 153 identified.

Table 4 therefore lists our interpretation of the vulnerability variables.

Trussell (2002) was unusual including size as a determinant, but most recent studies (Prentice et al. 2015; Myser 2016; Searing 2018; Burde et al. 2017) include it as a cardinal variable. Discussions with funders and our own experience of working with large and small charities suggested a fundamental difference between large and small charities and therefore the use of a dummy variable approach. The dummy distinguished ‘large’ charities with average income over £1m per annum over the six-year period. Alternative specifications based on maximum or minimum income, or a different threshold value, made little difference, lending support to the idea that this is best treated as a classification issue, rather than a need for a scale variable. There was no a priori expectation on the sign. Carroll and Slater (2009) argue that larger firms should have a higher probability of survival, ceteris paribus, as the same absolute variation in income or costs will have less effect on a big charity compared to a small one. Trussel (2002) finds empirical support for this, although the recent studies find large size is more likely to lead to failure.

Extensions to the Basic Model

We extend the base model with two variations. As noted in the literature review, all models use some form of index for concentration of income sources, but it seems likely that grant funding, self-generated activities and donations have different characteristics.

Accordingly, we include two additional variables.

-

Grant income as a share of total income.

-

Donations as a share of total income.

Activity income is the residual (as grant plus activity plus donation shares must add up to 100%). A priori, we expect an increase in grant income, relative to activity income, to be negatively associated with survival: a higher dependence on successful bids to deliver discrete blocks of money is likely to increase the risk of failure. We have no a priori expectation on the sign of donations.

The second extension is to consider the volatility of the charity’s operating environment, which Carroll and Slater (2009) argue is an important component of overall vulnerability. No authors have included volatility in models based on the vulnerability variables, but Duquette (2017) does include it in his model of revenue allocation. We include volatility as an attempt to see whether structural rigidity is a significant factor in financial vulnerability. If greater income volatility is associated with greater survival probabilities, this would suggest that the variability builds ‘robustness’ in some way. In contrast, more income volatility leading to more failures would suggest that charities are not able to adapt well. Income volatility is negatively correlated with income share for each income type, suggesting it may proxy some form of institutional rigidity around that income stream.

We therefore include five volatility measures: one each for the activity, grant and donation shares of income, and each of the staff and total costs. These are calculated as the coefficient of variation for each measure for each charity, calculated using data for all the years available (5 or 6 years for most charities). We have no a priori view on sign.

Table 5 presents correlations between the income shares of types of income, costs, and assets, as well as the big/small dummy.

Results

In total, data on 153 charities (815 individual observations) were collected. The charities are distributed as in Table 6.

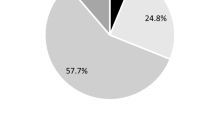

There are substantial differences in sources of income between the surviving and closed charities. Figure 1 shows source of income from 2011 to 2014, the year of analysis before firms closed or survived, by mean and median.

Sources of income: means and medians shares as percentage of total income

The row of means shows that surviving charities depend on grants for less than 25% of their income, on average, with smaller firms likely to have a slightly higher dependence than larger firms; almost 50% of their income comes from donations and a third from revenue-generating activities. In contrast, closed charities depend on grants for 60% of income.

A similar story is told by the medians. In any year, more than half of the closed charities depend on grant funding for over 70% of their income. In contrast, in every year at least half of the surviving firms receive less than 10% of their income from grants.

There does appear to be a difference in 2011 for the ‘live, small’ firms, compared to later years for activity and donated income. It is not clear why this arises. One possibility is that this is a lagged response to the ‘Big Society’ programme introduced in 2010, increasing the proportion of grant income for those charities.

Closed charities are more likely to be dependent on a single source of income. Figure 2 shows the proportion of charities which depend on a single type of income for over 90% of their funding, across all years.

Proportion of charities dependent on a single type of income

Thirty-two percentage of the large charities that had closed by 2015 rely on grant funding for over 90% of income; for small closed charities, the figure is 29%. In contrast, surviving charities are much less likely to be dependent on a single source for over 90% of their funding; where they do, it is activity income or donations.

Figure 3 shows cost ratios for the four types of charity.

Costs and assets

Closed charities show higher staff-cost-to-income ratios across the period than operational charities. For non-staff costs, there is much less difference in the mean share of income accounted for by costs. It is notable that, on average, the closed small charities appear to be living beyond their means with total costs significantly more than 100% of income.

Closed charities have lower assets relative to income across the period on average, but the most striking feature of the data is the very low level of assets amongst the large closed charities. All other groups have assets worth at least 1.5 times annual income, but for the large closed firms, net assets only average 40% of annual income. Figure 4 shows asset cover for income, that is, how long missing income could be funded from assets, assuming all assets are fully liquid.

Months of income cover in assets, all years

Twenty percentage of large closed charities appear to have negligible assets, whereas for the other groups this figure is nearer 5%. Eighty-five percentage of large closed charities and 60% of small closed charities have six months or less asset cover. In contrast, only 45% of charities (large and small) still operational in 2015 have less than 6 months of cover. It could be argued that this is as expected: charities on the brink of collapse would be expected to be running down their assets, particularly liquid ones. However, Fig. 5 shows the mean and median cover for each year 2011–2014, and the pattern is fairly stable.

Number of months income cover, 2011–2014

Not all assets are liquid, and some are required for income-raising (for example, store premises). These figures therefore overstate the ability of charities to cover a significant shortfall in income. Nevertheless, they suggest that the successful charities have greater potential to mitigate the risk of loss of income.

Aside from income and costs, one potential risk factor for charities is the volatility of income and outgoings. Figure 6 shows the volatility of income measured as the absolute coefficient of variation (standard deviation relative to the absolute value of the mean).

Volatility of income

The closed charities have greater volatility in activity and donation income, but in terms of volatility of grant funding, there is a more noticeable difference between large and small charities than between surviving and closed. This may reflect the ability of large charities to have multiple grant funds, whereas small charities are likely to receive grants sequentially: as each grant nears its end, new funding is bid for.

In summary, it appears that closed charities have higher staff costs, greater dependence on grant income, and fewer assets to call upon. The difference between large and small charities is much less notable, except for volatility of income.

These descriptive statistics suggest that there are factors that differentiate surviving and closed charities, but they cannot show how the different factors interact or their importance in determining outcomes. This paper uses a statistical model of the probability of a charity surviving to estimate the relative size of the different effects and the interactions of variables.

As noted above, this paper aims to assess the value of the concentration variable commonly used. Four models are estimated, each with observed survival as the outcome variable:

-

Model 0 survival is associated with the base variables: income concentration, and the other ‘vulnerability variables’ (margin; proxied by total costs; equity proxied by assets; administration costs, proxied by staff costs).

-

Model 1 survival is associated with the base variables and the proportion of income it receives from each type of funding.

-

Model 2 survival is associated with the base variables and the volatility of income and costs.

-

Model 3 survival is associated with the base variables, type of income, and volatility.

The inclusion of both staff and total costs raises the question of multicollinearity. As charities are primarily service organisations, there is a strong link between staff costs and total costs. However, as Fig. 3 shows, this relationship varies over organisation types. We therefore include both variables, as they are proxying different factors, but we note the possibility of multicollinearity in the results.

Size is also included as a control in all models. Results are presented in Table 7.

In terms of the ‘vulnerability’ variables, the income concentration ratio has the expected sign, but is only significant when the actual types of income (grants, donations) are not included. Equity (net assets) is only significant in the simplest model, although it does have the expected sign. Total costs as a share of income (margin) are significant at 10% but only in Model 1. The only ‘vulnerability’ variable that is always significant is the staff-costs-to-income ratio, with a negative sign. This is not easy to interpret. At first glance, it suggests that proportionately lower staff costs increase survival prospects, suggesting that Ecer et al.’s (2017) ‘high costs = organisational failure risk’ argument is correct. However, staff costs are the complement of non-staff costs, and so this could be interpreted as ‘high non-staff costs offer room to “cut the flab”’, as argued by Carroll and Slater (2009).

Distinguishing between sources of income (models 1 and 3) does substantially change the findings. The share of grant and donation income are highly significant, with the expected sign for grant income. (A higher proportion of grant income is associated with a lower probability of survival.) The significant and positive coefficient on donations suggests that a higher dependence on donations rather than one’s own activity is associated with a higher survival probability. This is despite the fact that donations are less likely to be under the control of the charity. However, greater volatility in donations is associated with a higher risk of failure. The implication is that the charity with the greatest probability of survival, ceteris paribus, is one with a large and predictable income from donations. As donation income is likely to be associated with longevity, this appears to contradict Searing’s (2018) finding that older nonprofits find it harder to recover from financial difficulties.

The other volatility measures have value in the basic if revenue concentration is the only measure of financial dependence (Model 2), volatility of grant funding has a positive coefficient, implying that more volatility is associated with a higher probability of success. One possible reason for this is that grant funding is, by its nature, unpredictable, and so greater volatility might help the charity to develop mechanisms for coping with uncertain income streams. However, when types of funding are included (Model 3), only the volatility of donation income remains significant.

Duquette (2017) finds that greater revenue volatility overall is associated with lower savings, in contrast to expectations. Our results suggest that this may be because overall revenue volatility is masking two opposing effects, from grants and donations. This is consistent with Duquette’s (2017) finding that the absolute size of the volatility effect is small.

The variable for whether a charity is large or not has no impact. However, this might be because the differences are more complex than a simple uplift in probability. To evaluate this, we ran separate probability models for large and small charities; see Table 8.

In terms of signs of coefficients, the results are broadly similar, but far fewer of the coefficients are significant; in other words, the model is struggling to identify clear determining factors. Net assets relative to income appear to be much more important for large charities, but staff costs are not; for small charities, the opposite is true. For the full model, the signs are as expected but very little is significant.

This is not surprising: probability models require many degrees of freedom, and the large/small split effectively halves the sample size for each estimate; hence, these results should be treated as indicative and interpreted with caution. A linear probability model, although only able to give indicative results, is less affected by low numbers of observation (although it is more likely to be affected by the multicollinearity between staff and total costs). Running a linear model on this data suggests that for large firms the key story is unchanged: a dependence of grant income lowers the probability of survival, and a high level of donations increases it. For small firms, the linear probability model supports the findings in Table 8: few factors are consistently associated with survival probability.

Finally, it was noted above that using data from the last year before failure might reflect charities in extremis and is therefore unrepresentative of their overall activity. To test this, we ran three alternative specifications:

-

Taking values from 2011, the first year data are available from all charities.

-

Taking values from 2013, the middle year of the period.

-

Averaging values across the three years prior to failure.

The volatility measures, being for the whole period, are unaffected by the choice of year. Table 9 presents the results for the full sample (not split by size), including the original model for comparison.

The findings show considerable robustness to alternative specifications. All coefficient signs are unchanged, and the coefficient values are generally within the same range. There have been some changes in significance: for example, the significance of the share of donations is more variable in the full model. The most notable variation is on costs: in Model 2 the size and significance of the total costs varies considerably; staff costs are highly significant in the final-year model but not others. It is not clear why this is the case. It may be something to do with the imminent failure of charities: staff costs may increase as redundancies are planned, and staff costs may be more difficult to reduce as income decreases. It may also be a result of the multicollinearity between the two costs measures, although this is difficult to determine in a nonlinear model.

When the results are split by large and small charity (not shown here for reasons of space, but available on request), the results are much the same: effect sizes are broadly consistent, although significance is much more variable because of the smaller sample sizes. There is an indication that significance is greater for smaller charities when using early years, suggesting that failure rates for small charities are predictable further in advance.

Discussion

Our model advances the literature in two significant ways.

First, we take the widely reported finding that concentration of income sources per se has a negative effect on a charity’s survival prospects, and we demonstrate that this is not the case. The concentration measure is effectively a poor proxy for specific composition of income; that is, it loses its relevance when more appropriate measures of income dependence are included. In particular, in line with Hager et al (2004), Myser (2016) and Green et al. (2016), we find that dependence on grant funding is a much better explanatory factor. We also find that the share of donations has an even more positive impact on survival than activity income, despite donations being less under the control of the charity then income-generating activities.

Most importantly, we have estimated these variations as part of a nested model, allowing the impact of different specifications to be tested. The literature in this field is mostly composed of independent specifications particular to the paper. While several authors have run non-nested models, very few (Gordon et al. 2013, being a notable exception) have run a hierarchy of models, testing multiple nested specifications on the same data. This provides us with strong evidence that the income concentration effect is a specification error, and not the result of different samples of variable construction.

Our second key contribution is to introduce volatility measures, which Carroll and Slater (2009) and Duquette (2017) argue is important, but which has not been statistically analysed before. Two hypotheses for the effect of volatility are considered: (1) instability in costs and income reduces survival prospects and (2) an unstable environment encourages charities to build in resilience—the ‘what doesn’t kill you makes you stronger’ argument. Our findings offer some support for the latter theory in the case of grant funding, but mostly support the former argument in the case of other income and costs. These results need to be treated with some caution, as the volatility measures are necessarily limited with at most 6 years’ worth of data.

Nevertheless, this does provide a consistent overall message: those charities with the greatest probability of survival have a high level of own-generated activity income and donations, and relative stability in that income and in costs. Charities with a high but stable grant income are more likely to fail.

At first glance, this seems perverse: how can more variation in a source of income improve a charity’s chances of survival? Green et al. (2016) propose that a stable level of grant funding can lead to dependency, so when grant funding is removed the charity is poorly placed to find other income streams. This is most likely to be the case where a charity has received the same or similar grant funding repeatedly, and where the funding counts for a large part of income. In contrast, an organisation that sees a large variation in its grant funding may place more emphasis on securing income from other sources. It may also be better placed to model the risk in its financial forecasts.

This in itself does not fully explain why grant funding volatility should have the opposite effect from activity and donation volatility. The missing part of the explanation may be that grant funding tends to come in large discrete blocks for fixed periods. In contrast, activity and donation income are more likely to be composed of a continuous, and continuously variable, stream of smaller amounts of income. Thus, even though the income stream may not be under the operational control of the charity, there is ample opportunity to observe and react to changing circumstances. Although Wright (2015) argues that only a relatively basic level of accounting knowledge is necessary for effective risk management, Ecer et al. (2017) suggest that the financial resilience of charities is limited by the lack of a for-profit ethos. Without the stimulus of uncertain income, charity management may not develop the necessary risk management skills. This reinforces the view of Hager (2001), Thomas and Trafford (2013) and Prentice (2017), that different indicators do not necessarily all point in the same direction for a charity.

Conclusion

In researching what causes charities to fail, there is one key finding: a diversified revenue stream per se increases financial resilience. By nesting this factor in a broader specification, we show that the basic model does not fully reflect the nuances of charity funding. In particular, we find that a dependence on grant funding is clearly associated with a higher risk of failure. We also argue that analyses that do not allow for the volatility of costs and income may be omitting crucial factors.

There are some limitations to the analysis. Sample sizes were limited by the need to identify closed charities in time for their information to be harvested. We have assumed that the primary reason for charity closure is financial, but we cannot rule out non-financial reasons. Using closure as a post-factum indication of vulnerability may include some charities that have undergone an extended period of financial distress, but it also identifies as ‘non-vulnerable’ charities that experienced financial distress but then recovered. Only three sources of funding were distinguished, whereas the meta-analyses of Lu et al. (2019) and Hung and Hager (2019) both suggested that number of funding sources affects the strength of the concentration effect. However, this may reflect more on the concentration measure, as more funding streams directly affects the variability of the measure; it is not clear that, for example, including multiple types of grant income, or distinguishing between donations and legacies, would necessarily change results significantly. Finally, we assume that the self-reported data are accurate, but there are inconsistencies in the data that suggest accounts are not being filed correctly. Regulators might want to consider the provision of information to the research community; it is noticeable that, with the exception of Burde et al. (2017), all the studies that employ actual survival rates were required to carry out their own data collection.

Despite these limitations, our analysis appears reasonably robust. Alternative specifications, with different variables and using different definitions, produced qualitatively similar results. Our results are not sensitive to the period used for estimation although, like Lu et al. (2019), we find that taking values over a longer period reduces the significance of effects. These findings are also consistent with findings on efficiency and survival from the for-profit sector.

This is an important finding for the UK, where social provision is increasingly tied to the health of the third sector, and vice versa. Chenhall et al. (2013) and Parry and Green (2017) note that there can be resistance to performance measures where this is seen to conflict with the ‘social’ objectives of the charity. However, it appears that a better understanding of cost ratios and of the dependency risk associated with different funding sources may offer trustees and regulators useful guidance on the long-term survival prospects for a charity.

References

Abraham, A. (2003). Financial sustainability and accountability: A model for nonprofit organisations. In AFAANZ 2003 conference proceedings, 6–8 July 2003 (p. 26). Brisbane, Australia: AFAANZ.

Altman, E. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 23, 589–609.

Arya, A., & Mittendorf, B. (2014). Career concerns and accounting performance measures in nonprofit organizations. Accounting, Organizations and Society, 40, 1–12.

Berrett, J., & Holliday, B. (2018). The effect of revenue diversification on output creation in nonprofit organizations: A resource dependence perspective. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, 29, 1190–1201. https://doi.org/10.1007/s11266-018-00049-5.

Bingham, T., & Walters, G. (2013). Financial sustainability within UK Charities: Community sport trusts and corporate social responsibility partnerships. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, 24(3), 606–629.

Burde, G., Rosenfeld, A., & Sheaffer, Z. (2017). Prediction of financial vulnerability to funding instability. Nonprofit and Voluntary Sector Quarterly, 46(2), 280–304.

Carroll, D. A., & Slater, K. J. (2009). Revenue diversification in nonprofit organizations: Does it lead to financial stability? Journal of Public Administration Review and Theory, 19, 947–966.

Charities Aid Foundation. (2017). CAF UK giving report 2017. Retrieved Nov 13, 2017, from https://www.cafonline.org/docs/default-source/about-us-publications/caf-uk-giving-web.pdf.

Chenhall, R., Hall, M., & Smith, D. (2013). Performance measurement, modes of evaluation and the development of compromising accounts. Accounting, Organizations and Society, 38, 268–287.

Chikoto, G., & Neely, D. (2014). Building nonprofit financial capacity: The impact of revenue concentration and overhead costs. Nonprofit and Voluntary Sector Quarterly, 43(3), 570–588.

Duquette, N. (2017). Spend or save? Nonprofits’ use of donations and other revenues. Nonprofit and Voluntary Sector Quarterly, 46(6), 1142–1165.

Ecer, S., Magro, M., & Sarpça, S. (2017). The relationship between nonprofits’ revenue composition and their economic-financial efficiency. Nonprofit and Voluntary Sector Quarterly, 46(1), 141–155.

Fernandez, J. (2008). Causes of dissolution among Spanish nonprofit associations. Nonprofit and Voluntary Sector Quarterly, 37, 113–137.

Foundation for Social Improvement. (2017). Brexit: Implications for small and local charities and community groups. Retrieved Nov 13, 2017, from http://www.thefsi.org/wp-content/uploads/2017/06/Brexit.pdf.

Framjee, P. (2008) Charities and insolvency. Guidance note to the Charity Finance Directors Group. Retrieved Nov 13, 2017, from http://www.cfg.org.uk/~/media/Document%20library/04%20Financial%20Management/04%20Financial%20Difficulties/Charities_and_Insolvency_0812PFIS0001.ashx.

Frumkin, P., & Keating, E. (2011). Diversification reconsidered: The risks and rewards of revenue concentration. Journal of Social Entrepreneurship, 2(2), 151–164.

Gilbert, L. R., Menon, K., & Schwartz, K. B. (1990). Predicting bankruptcy for firms in financial distress. Journal of Business Finance and Accounting, 17(1), 161–171.

Gordon, T., Fischer, M., Greenlee, J., & Keating, E. (2013). Warning signs: Nonprofit insolvency indicators. International Research Journal of Applied Finance, 11(3), 343–378.

Green, E., Ritchie, F., Parry, G., & Bradley, P. (2016) Financial resilience in charities. Project report. University of the West of England. Retrieved Nov 13, 2017, from http://eprints.uwe.ac.uk/30015/1/UWE%20HoL%20Charity%20evidence%20final%20v2.pdf.

Greenlee, J., & Trussel, J. (2000). Estimating the financial vulnerability of charitable organizations. Nonprofit Management and Leadership, 11, 199–210.

Hager, M. (2001). Financial vulnerability among arts organizations: A test of the Tuckman-Chang measures. Nonprofit and Voluntary Sector Quarterly, 30, 376–392.

Hager, M., Galaskiewicz, J., & Larson, J. (2004). Structural embeddedness and the liability of newness among nonprofit organizations. Public Management Review, 6, 159–188.

Helmig, B., Ingerfurth, S., & Pinz, A. (2014). Success and failure of nonprofit organizations: Theoretical foundations, empirical evidence, and future research. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, 25(6), 1509–1538.

HM Government. (2011). Growing the social investment market: A vision and strategy. Cabinet Office. Retrieved Nov 13, 2017, from https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/61185/404970_SocialInvestmentMarket_acc.pdf.

Hung, C., & Hager, M. (2019). The impact of revenue diversification on nonprofit financial health: A meta-analysis. Nonprofit and Voluntary Sector Quarterly, 48(1), 5–27.

Hu, Q., & Kapucu, N. (2015). Can management practices make a difference? Nonprofit organization financial performance during times of economic stress. European Journal of Economic and Political Studies, 8, 1–18.

Keating, E., Fischer, M., Gordon, T., & Greenlee, J. (2005). Assessing financial vulnerability in the nonprofit sector. Cambridge, MA: Harvard University Hauser Center for Nonprofit Organizations.

Keen, R. (2015). Charities and the voluntary sector: Statistics. Briefing paper no. SN05428, House of Commons Library. Retrieved Nov 13, 2017, from http://researchbriefings.files.parliament.uk/documents/SN05428/SN05428.pdf.

Kim, M. (2014). Does revenue diversification really matter? The power of commercial and donative distinction in the nonprofit arts. Mimeo: University of Pennsylvania. Retrieved Nov 13, 2017, from https://www.sp2.upenn.edu/wp-content/uploads/2014/08/Mirae-Kim.pdf.

Kingston, J., & Bolton, M. (2004). New approaches to funding not-for-profit organisations. International Journal of Nonprofit and Voluntary Sector Marketing, 9(2), 112–121.

Lohmann, R. A., & Lohmann, N. (2000). Predicting financial vulnerability in nonprofits. Mimeo: University of West Virginia. Retrieved Nov 13, 2017, from http://community.wvu.edu/~ralohmann/courses/sw656/ratios.ppt.

Lu, J., Lin, W., & Wang, Q. (2019). Does a more diversified revenue structure lead to greater financial capacity and less vulnerability in nonprofit organizations: A bibliometric and meta-analysis. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations. https://doi.org/10.1007/s11266-019-00093-9.

Myser, S. (2016). Financial health of nonprofit organizations. Ph.D. thesis. University of Kansas. Retrieved Nov 13, 2017, from https://kuscholarworks.ku.edu/handle/1808/22474.

NCVO. (2017). The UK Civil Society Almanac 2017. London: National Council for Voluntary Organisations. Retrieved Nov 13, 2017, from https://data.ncvo.org.uk/.

Ohlson, J. A. (1980). Financial ratios and the probabilistic prediction of bankruptcy. Journal of Accounting Research, 18, 109–131.

Omar, N., Arshad, R., & Razali, W. (2013). Assessment of risk using financial ratios in non-profit organisations. Journal of Energy Technologies and Policy, 3(11), 382–389.

Parry, G., & Green, E. (2017). Co-creating value: Through the gate and beyond. Project report. UWE. http://eprints.uwe.ac.uk/30910.

Prentice, C. (2015). Understanding nonprofit financial health: Exploring the effects of organizational and environmental variables. Nonprofit and Voluntary Sector Quarterly, 45(5), 888–909.

Searing, E. (2018). Determinants of the recovery of financially distressed nonprofits. Nonprofit Management and Leadership., 28(3), 313–328.

Tevel, E., Katz, H., & Brock, D. (2014). Nonprofit financial vulnerability: Testing competing models, recommended improvements, and implications. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations. https://doi.org/10.1007/s11266-014-9523-5.

Thomas, R., & Trafford, R. (2013). Were UK culture, sport and recreation charities prepared for the 2008 economic downturn? An application of Tuckman and Chang’s measures of financial vulnerability. VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, 24, 630–648.

Trussel, J. (2002). Revisiting the prediction of financial vulnerability. Nonprofit Management and Leadership, 13, 17–31.

Trussel, J., & Greenlee, J. (2004). A financial rating system for charitable nonprofit organizations. In J. M. Patton, P. A. Copley, & J. L. Chan (Eds.), Research in governmental and nonprofit accounting (Vol. 11, pp. 28–105). Bingley: Emerald Group Publishing Limited.

Tuckman, H., & Chang, C. (1991). A methodology for measuring the financial vulnerability of charitable nonprofit organization. Nonprofit and Voluntary Sector Quarterly, 20, 445–460.

von Schnurbein, G., & Fritz, T. (2017). Benefits and drivers of nonprofit revenue concentration. Nonprofit and Voluntary Sector Quarterly, 46(5), 922–943.

Wilsker, A., & Young, D. (2010). How does program composition affect the revenues of nonprofit organizations? Investigating a benefits theory of nonprofit finance. Public Finance Review, 38(2), 193–216.

Wright, W. (2015). Client business models, process business risks and the risk of material misstatement of revenue. Accounting, Organizations and Society, 48, 43–55.

Acknowledgements

The authors would like to acknowledge the funding that made this work possible from British Academy Leverhulme Small Grant [SG142923], the Cabinet Office, Big Lottery Fund as part of the UWE Linkage project, and from the Faculty of Business and Law at UWE.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Green, E., Ritchie, F., Bradley, P. et al. Financial Resilience, Income Dependence and Organisational Survival in UK Charities. Voluntas 32, 992–1008 (2021). https://doi.org/10.1007/s11266-020-00311-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11266-020-00311-9