Abstract

The aim of this paper is to empirically investigate the potential association between a firm’s cost behavior, characterized as cost stickiness or anti-stickiness, and working capital management (WCM), as measured by the working capital to total assets ratio and the trade cycle measures net trade cycle and cash conversion cycle. We measure cost stickiness using four widely accepted models and a sample of non-financial firms sourced from Compustat. Our findings highlight the significant influence of WCM on cost behavior. Specifically, we observe an inverse relationship between a firm’s WCM aggressiveness and both its cost stickiness and degree of cost adjustment. These relationships are consistent for both operating costs and the costs of goods sold.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Interest in cost behavior has a long history, tracing back a century (Guenther et al., 2014). Recent research within this domain has shown that costs, on average, can exhibit asymmetric behavior. This refers to how organizations adjust their costs in response to changes in activity levels depending on the direction of the change (Banker et al., 2018; Ibrahim et al., 2022). Anderson et al. (2003) was the first to document this phenomenon. They found that costs tend to decrease less in response to a decline in activity than they increase in response to an equivalent rise in activity. This characteristic is defined as cost stickiness. Contrarily, recent research has also identified situations in which costs decrease more in response to a decrease in activity than they increase for a similar upswing. This phenomenon is referred to as cost anti-stickiness (Balakrishnan et al., 2014; Banker et al., 2018). Possible reasons for cost asymmetry when activity levels decrease include firms’ reluctance to lay off redundant employees or their failure to renegotiate contracts with suppliers (Anderson et al., 2004; Banker et al., 2018). Conversely, cost asymmetry when activity levels increase may depend on the ability of firms to negotiate better terms with suppliers as their bargaining leverage increases and the success or failure of inventory management in scaling up appropriately.

Research on cost asymmetry has evolved from merely describing its existence to striving to identify its determinants (Ibrahim et al., 2022; Costa & Habib, 2023). For instance, cost asymmetry has been characterized as a function of factors such as asset intensity (Anderson et al., 2007), employee intensity (Anderson et al., 2003; Chen et al., 2012), debt intensity (Dalla Via & Perego, 2014), working capital intensity (Calleja et al., 2006), stock performance (Chen et al., 2012), industry type (Subramaniam & Watson, 2016), capital structure (Tulcanaza Prieto et al., 2019), capital investments (Shust & Weiss, 2014), CSR activities (Habib & Hasan, 2019), strategic positioning (Ballas et al., 2022), family versus non-family ownership (Siciliano & Weiss, 2023), Artificial Intelligence (AI) adoption (Wang & Qiu, 2023), and digital transformation (Chen & Xu, 2023). Furthermore, the degree of cost asymmetry varies across countries (e.g., Calleja et al., 2006; Banker et al., 2013). However, to the best of our knowledge, little is known about the relationship, if any, between asymmetric cost behavior and Working Capital Management (WCM) (Shin & Soenen, 1998).

In this paper, we contribute to the literature by empirically investigating the relationship between firms’ WCM and their tendency to exhibit asymmetric costs. More specifically, we investigate whether firms inclined towards aggressive WCM - those who possess the skills and willingness to negotiate, write off losses, and make necessary cuts - are better equipped to handle changes in daily operational activities as well as short-term financing issues. Specifically, we examine whether these firms exhibit less cost stickiness. Our study makes several contributions: First, we add knowledge to the literature on cost behavior by providing evidence of determinants of asymmetric cost behavior. In this regard, our study supplements to the literature that investigates the relationships between cost asymmetry and analysts’ earnings forecasts (Weiss, 2010), strategic orientation (Ballas et al., 2022), corporate dividend policy (He et al., 2020), and firm value (Costa & Habib, 2023). Indeed, (Costa & Habib, 2023) call for managers to be more transparent about their resource adjustment decisions. Given the current lack of this transparency, understanding the relationship between WCM and cost behavior could potentially mitigate this issue. While (Anderson & Lanen, 2007) question the appropriateness of standard models used to explain cost asymmetry as a reflection of managerial behavior, we argue that firms experiencing increases or decreases in activity can adjust their costs along a spectrum that ranges from passive to aggressive. Furthermore, we contend that this spectrum will, in many ways, mirror the spectrum of WCM. Consequently, we propose that firms that engage in one type of behavior are likely to engage in the other. Second, we enrich the literature on WCM by demonstrating the operational consequences of its execution. While a strand of the literature focuses on this aspect in terms of time management (Knauer & Wöhrmann, 2013), our study approaches WCM through its influence on cost behavior. Third, our study provides valuable insights for investors evaluating firms, as the primary way investors can discern the consequences of managerial decisions is through accounting figures. Calculating cost asymmetry may be challenging for practitioners. However, the proxies we use for WCM are easily accessible, as accounting data are publicly reported. In conclusion, given that firms emphasize the importance of coordinating financial and operational activities, we contribute to the literature on business controlling by merging financial management and management accounting where we show the relationship between the magnitude of cost stickiness and WCM.

We examine the impact of WCM on the asymmetry of both operating costs and the cost of goods sold. In line with existing literature, we use a firm’s revenues from its profit and loss statements as a proxy for its activity level. Furthermore, since WCM is not a specific management model or framework, but rather encompasses any actions aimed at managing levels of working capital, we operationalize WCM through the use of three proxies. First, we use the two trade cycle measures Cash Conversion Cycle (CCC) and Net Trade Cycle (NTC). The WCM literature employs both these measures as proxies for WCM (Knauer & Wöhrmann, 2013; Wang, 2019; Ujah et al., 2020). Further, using these measures builds on insights from the WCM literature that suggest that the trade cycle can predict profitability (Knauer & Wöhrmann, 2013; Lyngstadaas, 2020). The rationale for using these proxies is that firms with lower CCC and NTC values, indicative of shorter trade cycles, are expansionary and exhibit more aggressive WCM to rely less on external financing for working capital, whereas firms with higher values, representing longer trade cycles, seek greater stability (Smith & Sell, 1980; Raddatz, 2006; Tong & Wei, 2011; Baños-Caballero et al., 2014; Wang 2019). Moreover, the literature infers a connection between the traits of a firm’s managers and their trade cycle time in days (Tauringana & Adjapong Afrifa, 2013). While most of the literature on WCM employs CCC to determine WCM (Singh et al., 2017), we also incorporate NTC. Compared to CCC, NTC does not depend on the cost of goods sold, which we have also used as a dependent variable in our regressions. Additionally, since both CCC and NTC utilize income statement items, including sales which are used in other significant variables in our regressions, we also proxy WCM using a measure based solely on balance sheet items. Specifically, we use the ratio of Working Capital to Total Assets (WCTA), which has also been used for studying WCM (Mättö & Niskanen, 2021). Similar to CCC and NTC, companies with lower WCTA values are in an expansion phase and employ a more aggressive WCM. This reduces their reliance on external financing for working capital, while companies with higher WCTA values aim for increased stability. Furthermore, to test our hypothesis, we utilize established models for asymmetric cost behavior and a sample of non-financial firms from 1983 to 2022 based in the United States and Canada, sourced from Compustat.

Our findings reveal that firms with more aggressive WCM exhibit less cost stickiness, meaning they are more capable of adjusting their operating costs and costs of goods in response to declines in sales, compared to firms with less aggressive WCM. Furthermore, our study reveals that more aggressive WCM is associated with a lower degree of adjustments in operating costs and the cost of goods. Our findings are robust across all our proxies for WCM.

The remainder of this paper is structured as follows: In the next section, we derive our hypothesis. Subsequently, we outline our research design and introduce our sample. After that, we present and discuss our findings. Lastly, we conclude the paper, where we also highlight the limitations of our study and proposing directions for further research based on our findings.

2 Hypothesis development

The cost behavior of firms can be explained by numerous variables (Ibrahim et al., 2022). However, little is known about the relationship, if any, between cost behavior and WCM. On the other hand, WCM research seems to be dominated by its effect on organizational performance, particularly profitability (Singh et al., 2017; Kayani et al., 2019; Prasad et al., 2019).

We propose that a firm’s approach to WCM can offer insights into its operational efficiency (Frankel et al., 2017), thereby revealing distinct aspects of its management style. There are two general approaches to WCM: aggressive and conservative (Etiennot et al., 2012). An aggressive approach seeks to minimize capital binding, while a conservative approach allows for more extensive capital binding. Evidence suggests that aggressive management maximizes profit (Jose et al., 1996).

Tauringana & Adjapong Afrifa, (2013) suggest that firms in different circumstances are better served by adapting their WCM to optimize their profits. For instance, small, newly-started firms should employ aggressive WCM, while larger, established firms should adopt a more passive WCM style. On the other hand, (Singh et al., 2017) find, in their meta-analysis, a generally positive relationship between aggressive WCM and profitability. However, this relationship is more profound for larger firms. A study by (Lyngstadaas, 2020) identifies 11 different configurations of working capital packages contributing to financial performance. As he outlined, there is no one-size-fits-all solution. Nevertheless, there are substantial indications that an optimal working capital level exists concerning profitability (see, e.g., Knauer & Wöhrmann, 2013; Baños-Caballero et al., 2014). We posit that, in aggregate, the WCM style is a function of both conscious decisions and the inherent qualities of managers. Regardless of which aspect dominates from firm to firm, we theorize that firms operating with aggressive WCM do so because their managers accurately appreciate the time value of money. These managers are willing to undertake the challenging task of negotiating terms with suppliers and customers, as well as meticulously managing inventory. Not everyone can comprehend the value of beneficial payment terms and be willing and able to navigate difficult negotiations to obtain them. Additionally, we contend that leaders who manage a business with a relatively short inventory time must be willing to renegotiate orders, quickly identify when goods need to be moved, and be prepared to sell them at a loss. They generally need to be well connected to the other parts of the value chain. These skills involve the ability and willingness to negotiate and the readiness to make cuts and sell at a loss. Our reasoning implies that these qualities are found more often in firms that exhibit more aggressive WCM.

Moreover, financial constraints increase the importance of working capital as a source of corporate funding (Baños-Caballero et al., 2014). Under such circumstances, the firm may accelerate or postpone adjustment decisions, and hence, WCM may affect cost asymmetry. For instance, underutilized working capital may be invested in growth opportunities (Aktas et al., 2015). However, intensive working capital investments may displace necessary investments in technology and work processes (Baños-Caballero et al., 2014).

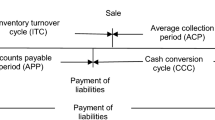

Our study uses the three measures WCTA, CCC, and NTC, as proxies for WCM, where low values are associated with an aggressive WCM strategy. Firms with lower WCTA values employ a more aggressive WCM, reducing their reliance on external financing, compared to firms with higher WCTA values that aim for increased stability. The trade cycle measures CCC and NTC are financial metrics that measure the duration it takes from paying for raw goods to receiving payment from customers. They are calculated by summing up (i) The duration of payment for accounts payable, (ii) The amount of time goods spend in inventory, and (iii) The length of time it takes from making sales until accounts receivables are paid. The three components can give ambiguous signals when acting as a proxy for firm performance. For example, short payment terms for customers might be advantageous as they ensure liquidity. Conversely, longer payment terms could also be beneficial if they attract more customers. Similarly, while it is financially prudent for goods to spend minimal time in inventory to avoid tying up capital and risking product expiration, maintaining a longer inventory period could be advantageous if the firm benefits from offering quick delivery of a wide range of niche goods. The duration of accounts payable can be short if the firm settles debts promptly or longer if the firm leverages its negotiating power to delay repayments. In the former case, the real interest rate on the terms must be considered.

There are two potential reasons why a firm might have an exceedingly long accounts payable duration. One possibility is that the company has successfully negotiated terms with suppliers to its advantage. The other scenario is that the firm is struggling to pay down its debts, thus involuntarily extending its CCC and NTC durations. Firms facing liquidity issues that prevent them from keeping their accounts current are at a heightened risk of bankruptcy. However, these circumstances may paradoxically make their accounts payable duration appear unusually advantageous.

To minimize the CCC and NTC durations, firms must use any leverage to negotiate beneficial payment terms with suppliers and customers. They also need to be vigilant in maintaining lean inventory levels. Thus, managers who succeed in implementing an aggressive WCM style share some common traits: They are shrewd and willing negotiators and are meticulous in inventory management. We assert that managers possessing these underlying characteristics are beneficial to businesses in adapting their costs to changing activity levels.

To sum up, we seek to uncover whether a relationship exists between a firm’s WCM and its cost asymmetry. We underpin this question with the logic we have presented. Imagine, for instance, a firm with an ideal aggressive WCM. They extract every possible advantage in contracting with other firms. They maintain precise and organized warehouses and inventories to minimize the amount of time things spend in their possession. The same business practices that exhibit more aggressive WCM should then benefit the firm in adapting costs to different activity levels. Based on the justification given above, we suggest the following hypothesis:

H1

Firms with more (less) aggressive WCM will exhibit less (more) cost asymmetry.

Even though we propose that there is a relationship between the WCM and cost asymmetry, the literature can be interpreted to suggest the absence of this relationship. For instance, (Calleja et al., 2006) find that different levels of working capital intensity yield different outcomes on cost stickiness. They also explain cost asymmetry as being affected by managerial oversight. The managers influencing WCM as well as cost behavior may be numerous and not coordinated. Sales managers may impact accounts receivable, purchase managers may impact accounts payable, and inventory managers may impact inventories, while different operational managers, be it Production, HR, IT, or the Finance department may impact cost structures. Also when it comes to cost behavior, the picture is not clear: Both stickiness as well as anti-stickiness is shown in the literature (Ibrahim et al., 2022). For instance, (Ballas et al., 2022) find that firms pursuing a prospector strategy, on average, show cost stickiness, while firms pursuing a defender strategy show anti-stickiness. The latter ones were more capital intensive than the first ones, and then we conjecture that there is no relationship between working capital-intensive firms and cost behavior. Also, similar variables can yield different outcomes. (Wang & Qiu, 2023) find evidence for the implementation of AI increasing labor cost stickiness, while (Chen & Xu, 2023) conclude that digital transformation inhibits cost stickiness.

3 Research design

This section details four well-known models in the literature that we employ to test asymmetric cost behavior. Of these, the second model is of particular interest as it is utilized to assess the effect of the NTC. In all models, we control for industry and year fixed effects and cluster all standard errors at the firm level.

We share the code for executing all our analyses and generating results at: https://cost-management-2024.ranik.no. We are unable to share the data due to restrictions imposed by the data provider.

The first model we apply is the baseline model introduced by (Anderson et al., 2003). It is given as follows:

In the above, \(\Delta \ln Cost_{i,t} = \ln {\left[ \frac{Cost_{i,t}}{Cost_{i,t-1}}\right] }\) is the log-change in costs from the previous accounting year \(t-1\) to the current t of firm i; \(\Delta \ln Sales_{i,t} = \ln {\left[ \frac{Sales_{i,t}}{Sales_{i,t-1}}\right] }\) is the log-change in sales; \(D_{i,t}\) is a sales decrease dummy, which is 1 if the sales for period t is less than that in \(t-1\), that is, \(\Delta \ln Sales_{i,t} <0\); \(\epsilon _{i,t}\) is the error term; the coefficient \(\beta _1\) measures the percentage change in costs for a one percent increase in sales; and the coefficient \(\beta _2\) approximates the cost asymmetry in that it measures the additional percentage change in costs in the case of decreasing sales.Footnote 1 In sum, model (1) implies that there is a \(\beta _1\) percentage change in costs when sales increase and a \(\beta _1+\beta _2\) percent change in costs when sales decrease. In other words, since we can assume that \(\beta _1>0\), costs are sticky if \(\beta _2<0\) and anti-sticky if \(\beta _2>0\).

Following (Anderson et al., 2003), we expand model (1) so that the degree of cost asymmetry is given by several explanatory variables. Further, we follow recent studies (e.g., Banker et al., 2013; Banker & Byzalov, 2014; Banker et al., 2014) by letting these explanatory variables also determine the change in costs overall. The general expression of such a model is given as follows:

where \(\textbf{x}^P_{i,t}\) is a vector of P explanatory variables, while \(\mathbf {\delta }_{1}^{P}\) and \(\mathbf {\delta }_{2}^{P}\) are vectors of size P with coefficients to be estimated. Specifically, we test whether the WCM explains the degree of cost asymmetry by using the following model:

where \(AINT_{i,t}=\ln {\left[ \frac{Assets_{i,t}}{Sales_{i,t}}\right] }\) is the asset intensity given by the log-ratio of total assets to sales; \(EINT_{i,t}=\ln {\left[ \frac{Employees_{i,t}}{Assets_{i,t}}\right] }\) is the employee intensity defined as the log-ratio of the number of employees to total assets; and \(\Delta GDP_{t}=\frac{GDP_{t}}{GDP_{t-1}}-1\) is the annual GDP growth rate. Both \(AINT_{i,t}\) and \(EINT_{i,t}\) proxy the magnitude of resource adjustment costs, while \(\Delta GDP_{t}\) proxies managers’ expectations. We use three different proxies for WCM. First, we use WCTA calculated by:

Second, we utilize CCC as a proxy for WCM in model (2). Following (Lyngstadaas & Berg, 2016), we calculate CCC as follows:

where \(INV_{i,t}=365\times \frac{\text {Inventories}_{i,t}}{\text {Cost of goods}_{i,t}}\) is the number of days of inventory; \(ACR_{i,t}=365\times \frac{\text {Accounts receivable}_{i,t}}{\text {Sales}_{i,t}}\) is the number of days of accounts receivable; and \(ACP_{i,t}=365\times \frac{\text {Accounts payable}_{i,t}}{\text {Purchases}_{i,t}}\) is the number of days of accounts payable.Footnote 2. Finally, we employ NTC as proxy for WCM, calculated as follows:

Further, we use an extension of model (1) that (Anderson et al., 2003) introduced to account for any reversion of asymmetry in subsequent periods. It is a two-period model given as follows:

where \(\Delta \ln Sales_{i,t-1}=\ln {\left[ \frac{Sales_{i,t-1}}{Sales_{i,t-2}}\right] }\) is the log-change in costs from accounting year \(t-2\) to \(t-1\); \(D_{i,t-1}\) is a sales decrease dummy, which is 1 if \(\Delta \ln Sales_{i,t-1} <0\); \(\beta _3\) approximates the lagged adjustment of costs for changes in sales; and \(\beta _4\) measures reversal effects of cost asymmetry if \(\beta _2<0<\beta _4\) or \(\beta _4<0<\beta _2\).

Finally, we use a two-period model proposed by (Banker et al., 2014) given by

where \(I_{i,t-1}\) is a dummy which is 1 if the sales increased from \(t-2\) to \(t-1\), that is, \(\Delta \ln Sales_{i,t-1}>0\). The coefficients \(\beta _{1I}\) and \(\beta _{1D}\) measure the percentage change in costs for a one percent increase in sales in the case of increasing and decreasing, respectively, sales in the previous period. Further, \(\beta _{2I}\) and \(\beta _{2D}\) approximate the cost asymmetry in the case of increasing and decreasing, respectively, sales in the previous period. (Banker et al., 2014) predict that \(\beta _{2I}<0\) and \(\beta _{2D}>0\), meaning that costs are sticky following a prior sales increase and anti-sticky following a prior sales decrease. Furthermore, (Banker & Byzalov, 2014) anticipate that in high-growth economies, costs are in both cases sticky but less so following a prior sales decrease compared to a prior sales increase, that is, \(\beta _{2I}<\beta _{2D} \le 0\). Moreover, (Banker et al., 2014) argue for \(\beta _{1I}>\beta _{1D}\), that is, for a given magnitude of current sales increase, costs will increase to a greater extent following a prior sales increase compared to a prior sales decrease.

4 Sample

Our sample includes annual consolidated financial fundamentals for non-financial active and inactive firms based in the United States and Canada, sourced from Compustat. Following (Banker & Byzalov, 2014), we analyze a 40-year period and further use a recent dataset by including annual observations from 1983 to 2022.Footnote 3 We utilize the following Compustat items: SALE for sales, XOPR for operating costs, COGS for the cost of goods, AT for assets, EMP for the number of employees, INVT for inventories, RECTR for trade receivables, AP for trade payables, ACT for current assets, and LTC for current liabilities. Additionally, we incorporate United States GDP data derived from the World Bank Databank.Footnote 4

When estimating coefficients for the models (1) and (2), that have a one-year lag, we include only firm-year observations where fundamentals of the firm are available for the previous accounting year. Moreover, when estimating models (3) and (4) with two-year lags, we include only firm-year observations where the firm’s fundamentals are available from the two previous years. We remove observations with a zero or negative value for accounting items used in each model’s log ratio to avoid numerical issues. Further, when employing model (2), we also avoid numerical issues by excluding observations with missing value for any accounting variables that are used as denominators in any of the ratios for deriving the proxies of WCM. Specifically, when using WCTA and NTC as proxies, we exclude observations with missing values for assets and sales, respectively. Similarly, when employing CCC as the proxy, we exclude observations with missing values in the denominators of any of the three ratios used to derive CCC. Additionally, to mitigate the effect of outliers, we winsorize the WCTA and NTC ratios, as well as the three ratios used to derive CCC, between the 1st and 9th percentiles. To control inflation, we deflate all accounting numbers based on the United States consumer price index, derived from the World Bank Databank.Footnote 5.

Appendix A provides a description of the data employed in our analyses. Specifically, Tables 4 and 5 describe the data when operating costs and cost of goods, respectively, are used for calculating the dependent variable, log-change in costs (\(\Delta \ln Cost_{i,t}\)). In both these tables, data descriptions for model (2) are provided when WCTA is used as the proxy for WCM. Data descriptions for model (2) when CCC and NTC are used as proxies can be found in Tables 6, 7, 8, and 9. In all tables in the Appendix, Panel A outlines the sample selection. As the exclusion of observations varies between the models applied, Panel A provides separate columns for different models. Furthermore, Panel B in all tables provides descriptive statistics for the data utilized in estimating model (2), which is the model of particular interest as it is used for assessing the effects of WCM.

5 Empirical findings

Tables 1 and 2 present the regression results of all our models, where the dependent variable, the log-change in costs (\(\Delta \ln Cost_{i,t}\)), is calculated using operating costs and the cost of goods sold, respectively. In both of these tables, the regression results for model (2) are presented when WCTA is utilized as the proxy for WCM. Additionally, Table 3 exhibits the regression results for model (2) when CCC and NTC are employed as proxies for WCM. All tables provide coefficient estimates, Student’s t-test statistics, and \(R^2\) values as measures of determination. Standard errors are clustered at the firm level. All models control for industry and year fixed effects.Footnote 6 For model (2), we display standardized estimates for the \(\gamma\) coefficients.

The tables provide several interesting insights. Firstly, we observe that \(\beta _1\), including \(\beta _{1I}\) and \(\beta _{1D}\), is consistently positive and statistically significant, as anticipated, since it represents a positive relationship between sales and costs. Further, the coefficient values are in all cases below 1, which suggests, as anticipated, that the firms in our sample do not adjust costs in proportion to shifts in sales. This corresponds to findings in the literature, for instance (Calleja et al., 2006), (Banker & Chen, 2006), and (Dalla Via & Perego, 2014). Nonetheless, we observe higher magnitudes of the estimated \(\beta _1\), \(\beta _{1I}\), and \(\beta _{1D}\) values in Table 2 than in Table 1, indicating a more positive relationship between sales and cost of goods than operating costs. Indeed, for the cost of goods, the \(\beta _1\) coefficient is between 0.589 and 0.661 (see Table 2) as compared to between 0.471 and 0.533 for operating costs (see Table 1). This is as expected, given that accounting rules often necessitate the alignment of goods’ expenses with sales. It also lends credence to our data and findings, as theory predicts that operating costs are harder to change for managers than the cost of goods. For example, operating costs also include investments in machinery and the hiring of employees. Further, we deduce from the negative signs of the \(\gamma _{11}\) and \(\gamma _{12}\) coefficients that an increase in asset intensity and employee intensity, respectively, corresponds to a lower degree of cost adjustment in response to changes in sales. Additionally, the positive signs of the \(\gamma _{13}\) and \(\gamma _{14}\) coefficients indicate a higher degree of cost adjustment with a higher GDP growth rate and higher values of the WCM proxies. That is, we find that more aggressive WCM (lower values of the WCM proxies) is associated with a lower degree of cost adjustment. The positive sign of \(\gamma _{13}\) can be explained by factor prices inclining more than the underlying increase in volume during times of economic growth. These findings are consistent regardless of which proxy we use for WCM and whether we derive our results from operating costs or the cost of goods. The only exception is the positive sign of the \(\gamma _{12}\) coefficient when considering operating costs and using WCTA as the proxy for WCM (see Table 1). Furthermore, all coefficients are statistically significant except for \(\gamma _{12}\) when considering the cost of goods sold and using WCTA as the proxy for WCM (see Table 2). Moreover, the magnitudes of the \(\gamma _{11}\), \(\gamma _{12}\), \(\gamma _{13}\), and \(\gamma _{14}\) coefficients indicate that asset intensity (\(\gamma _{11}\)) has the most significant impact on the degree of cost adjustment in response to changes in sales. While previous research that has investigated variables determining the change in costs in response to changes in sales has used different samples over time periods, they still support our findings (see, e.g., Anderson et al., 2003; Banker et al., 2013). Some studies report effects that deviate from the rest of the literature. For example, (Chen et al., 2012) report a negative coefficient for asset intensity, while they find a positive relationship for employee intensity. They conjecture that these findings depend on different samples.

Secondly, the tables provide evidence of sticky cost behavior among the firms, as the \(\beta _2\) coefficients of models (1) and (3) are negative and statistically significant. Our findings of stickiness are in line with previous literature, for instance, (Anderson et al., 2003), (Banker et al., 2013), and (Banker & Byzalov, 2014). For model (2), the value of the \(\beta _2\) coefficient is positive in all Tables 1, 2, and 3. Nevertheless, the stickiness is also determined by the coefficients \(\gamma _{21}\), \(\gamma _{22}\), \(\gamma _{23}\), and \(\gamma _{24}\) in this model. The \(\gamma _{22}\) coefficient is negative in all cases, and also statistically significant in all cases except for the case when considering costs of goods and using NTC as the proxy for WCM. This testifies to a positive relationship between cost stickiness and employee intensity. Further, the \(\gamma _{21}\) and \(\gamma _{23}\) coefficients are statistically significant and have negative values in all cases when considering operating costs. This provides compelling indications of positive effects of asset intensity and GDP growth rate on stickiness of operating costs. However, when considering costs of goods, the \(\gamma _{21}\) and \(\gamma _{23}\) coefficients are statistically insignificant. When it comes to the relationships between WCM and cost stickiness, we observe that the \(\gamma _{24}\) coefficient is negative and statistically significant when using NTWC and CCC as proxies for WCM, regardless of whether we consider operating costs or the cost of goods. This testifies to positive relationships between cost stickiness and more aggressive WCM. When using NTC as the proxy, the \(\gamma _{24}\) is also negative but statistically insignificant.

Thirdly, the coefficient value of \(\beta _3\) in model (3) is positive in both Tables 1 and 2, indicating a lagged positive relationship between sales and costs, as denoted by \(\beta _1\). However, this effect is minor since the value of \(\beta _3\) is much smaller compared to \(\beta _1\) in both tables. This implies that a change in costs in previous years has a small impact on costs in subsequent years. Furthermore, the \(\beta _4\) coefficient of model (3) is negative, indicating that the cost stickiness, denoted by \(\beta _2\), is not reversed in the subsequent year but persists into the following year. All our findings regarding this two-period model are as expected and in line with the previous literature (see, e.g., Anderson et al., 2003).

Finally, the regression results of model (4) provide evidence of different adjustments to costs among the firms in our sample, depending on whether their sales increased or decreased in the previous accounting years. This follows the reasoning that while some consequences of changes in activity level will take effect immediately, such as buying less raw material and cutting back hours for the employees, others manifest only after some substantial time has passed, for instance, firing or hiring employees, or selling or buying substantial machinery. Specifically, we observe that \(\beta _{1I}\) is higher than \(\beta _{1D}\), which indicates that for a given magnitude of current sales increase, costs will increase to a greater extent following a prior sales increase compared to a prior sales decrease. This corresponds to the findings of (Banker et al., 2014). Furthermore, as predicted by the literature (see, e.g., Banker & Byzalov, 2014; Banker et al., 2014), we find that that \(\beta _{2I}<0\) and \(\beta _{2D}>0\), meaning that costs are sticky following a prior sales increase and anti-sticky following a prior sales decrease. Our findings are consistent and statistically significant, irrespective of whether we apply operating costs or the cost of goods.

6 Discussion and conclusion

This study aimed to investigate whether there exists a relationship between firms’ cost behavior and their WCM, proxied by the trade cycle measures NTC and CCC, as well as NTWC. Our results support our hypothesis by demonstrating a negative relationship between the aggressiveness of a firm’s WCM and its cost stickiness, both when considering operating costs and the costs of goods. This suggests that firms exhibiting more aggressive WCM are better equipped to adjust their operating costs and costs of goods in response to sales declines, compared to firms with less aggressive WCM. This negative relationship between cost stickiness and WCM is present when using NTWC and CCC as the as the proxy for WCM. However, the negative relationship is not statistically significant when using NTC as the proxy. Furthermore, we find a negative relationship between the aggressiveness of a firm’s WCM and its degree of cost adjustment. This finding is statistically significant across all our proxies for WCM, regardless of whether we consider operating costs or the cost of goods. Overall, our study attests to the impact of WCM on cost behavior.

Our study contributes to the cost behavior literature by adding knowledge about the determinants of asymmetric cost behavior as we find that cost stickiness is influenced by firms’ trade cycles. Further, it contributes to the literature on WCM by demonstrating the operational consequences of its execution. Moreover, our study provides implications for practitioners: While cost asymmetry may be challenging to calculate, WCTA, NTC, and CCC are easily accessible through publicly available accounting figures. As firms emphasize the importance of coordinating financial and operational activities, our study contributes to merging financial management and management accounting by showing the relationship between the magnitude of cost stickiness and WCM. Also, our study broadens the insights that different practitioners, such as investors, can gain by combining knowledge from WCM and cost management. As there may be a lack of transparency about firms’ resource adjustment decisions, insight into the relationship between WCM and cost behavior might mitigate this problem. For managers, our study specifically underscores the advantage of reduced cost stickiness when implementing a more aggressive WCM.

However, this article does not exhaust all avenues of research on cost asymmetry. Throughout our work, two areas of inquiry for future research have emerged. The first area pertains to the significance of size and understanding the influence of structural and executional cost drivers on cost management. The second potential area of inquiry for future research concerns the demand side and seeks to determine whether there is a relationship, on an industry average, between price elasticity and cost asymmetry. Further exploration of these topics could provide deeper insights into the complex field of cost management, a necessary skill for firms striving for sustainable competitive advantages. Finally, we suggest that future studies investigate the underlying dynamics of the relationships we found between managerial skills and cost behavior in more depth.

Code and data availability

We share the code for executing all our analyses and generating results at: https://cost-management-2024.ranik.no. We are unable to share the data due to restrictions imposed by the data provider.

Notes

As sales, we focus on the revenue generated from the companies’ operations and exclude other forms of income, such as rental revenue.

Purchases are calculated by taking the cost of goods sold, subtracting the opening inventory balance, and then adding the closing inventory balance

In unreported analyses, we rerun all our analyses with 10-year and 20-year, respectively, periods with annual observations up to 2022. Our findings remain the same, with the same signs of all our coefficient estimates of all our regressions. The Student’s t-test statistics show, however, lower t values with fewer observations. Results are available upon request.

We define industry using the Standard Industry Classification Code, as provided by the Compustat item SIC.

References

Aktas, N., Croci, E., & Petmezas, D. (2015). Is working capital management value-enhancing? Evidence from firm performance and investments. Journal of Corporate Finance, 30, 98–113. https://doi.org/10.1016/j.jcorpfin.2014.12.008

Anderson, M., Banker, R., Chen, L., Janakiraman, S., 2004. Sticky Costs at Service Firms. Working Paper, University of Texas at Dallas.

Anderson, M., Banker, R., Huang, R., & Janakiraman, S. (2007). Cost behavior and fundamental analysis of SG &A costs. Journal of Accounting, Auditing & Finance, 22, 1–28. https://doi.org/10.1177/0148558X0702200103

Anderson, M. C., Banker, R. D., & Janakiraman, S. N. (2003). Are selling, general, and administrative costs “Sticky"? Journal of Accounting Research, 41, 47–63. https://doi.org/10.1111/1475-679X.00095

Anderson, S.W., Lanen, W.N., 2007. Understanding cost management: What can we learn from the evidence on ’Sticky Costs’? Working Paper 10.2139/ssrn.975135.

Baños-Caballero, S., García-Teruel, P. J., & Martínez-Solano, P. (2014). Working capital management, corporate performance, and financial constraints. Journal of Business Research, 67, 332–338. https://doi.org/10.1016/j.jbusres.2013.01.016

Balakrishnan, R., Labro, E., & Soderstrom, N. S. (2014). Cost structure and sticky costs. Journal of Management Accounting Research, 26, 91–116. https://doi.org/10.2308/jmar-50831

Ballas, A., Naoum, V. C., & Vlismas, O. (2022). The effect of strategy on the asymmetric cost behavior of SG &A expenses. European Accounting Review, 31, 409–447. https://doi.org/10.1080/09638180.2020.1813601

Banker, R. D., & Byzalov, D. (2014). Asymmetric cost behavior. Journal of Management Accounting Research, 26, 43–79. https://doi.org/10.2308/jmar-50846

Banker, R. D., Byzalov, D., & Chen, L. T. (2013). Employment protection legislation, adjustment costs and cross-country differences in cost behavior. Journal of Accounting and Economics, 55, 111–127. https://doi.org/10.1016/j.jacceco.2012.08.003

Banker, R. D., Byzalov, D., Ciftci, M., & Mashruwala, R. (2014). The moderating effect of prior sales changes on asymmetric cost behavior. Journal of Management Accounting Research, 26, 221–242. https://doi.org/10.2308/jmar-50726

Banker, R. D., Byzalov, D., Fang, S., & Liang, Y. (2018). Cost Management Research. Journal of Management Accounting Research, 30, 187–209. https://doi.org/10.2308/jmar-51965

Banker, R.D., Chen, T.L., 2006. Labor market characteristics and cross-country differences in cost stickiness. Working Paper 10.2139/ssrn.921419.

Calleja, K., Steliaros, M., & Thomas, D. C. (2006). A note on cost stickiness: Some international comparisons. Management Accounting Research, 17, 127–140. https://doi.org/10.1016/j.mar.2006.02.001

Chen, C. X., Lu, H., & Sougiannis, T. (2012). The agency problem, corporate governance, and the asymmetrical behavior of selling, general, and administrative Costs*. Contemporary Accounting Research, 29, 252–282. https://doi.org/10.1111/j.1911-3846.2011.01094.x

Chen, Y., & Xu, J. (2023). Digital transformation and firm cost stickiness: Evidence from China. Finance Research Letters, 52, 103510. https://doi.org/10.1016/j.frl.2022.103510

Costa, M. D., & Habib, A. (2023). Cost stickiness and firm value. Journal of Management Control, 34, 235–273. https://doi.org/10.1007/s00187-023-00356-z

Dalla Via, N., & Perego, P. (2014). Sticky cost behaviour: Evidence from small and medium sized companies. Accounting & Finance, 54, 753–778. https://doi.org/10.1111/acfi.12020

Etiennot, H., Preve, L. A., & Sarria-Allende, V. (2012). Working capital management: An exploratory study. Journal of Applied Finance, 22(1), 14.

Frankel, R., Levy, H., & Shalev, R. (2017). Factors associated with the year-end decline in working capital. Management Science, 63, 438–458. https://doi.org/10.1287/mnsc.2015.2351

Guenther, T. W., Riehl, A., & Rößler, R. (2014). Cost stickiness: State of the art of research and implications. Journal of Management Control, 24, 301–318. https://doi.org/10.1007/s00187-013-0176-0

Habib, A., & Hasan, M. M. (2019). Corporate social responsibility and cost stickiness. Business & Society, 58, 453–492. https://doi.org/10.1177/0007650316677936

He, J., Tian, X., Yang, H., & Zuo, L. (2020). Asymmetric cost behavior and dividend policy. Journal of Accounting Research, 58, 989–1021. https://doi.org/10.1111/1475-679X.12328

Ibrahim, A. E. A., Ali, H., & Aboelkheir, H. (2022). Cost stickiness: A systematic literature review of 27 years of research and a future research agenda. Journal of International Accounting, Auditing and Taxation, 46, 100439. https://doi.org/10.1016/j.intaccaudtax.2021.100439

Jose, M. L., Lancaster, C., & Stevens, J. L. (1996). Corporate returns and cash conversion cycles. Journal of Economics and Finance, 20, 33–46. https://doi.org/10.1007/BF02920497

Kayani, U. N., De Silva, T. A., & Gan, C. (2019). A systematic literature review on working capital management–An identification of new avenues. Qualitative Research in Financial Markets, 11, 352–366. https://doi.org/10.1108/QRFM-05-2018-0062

Knauer, T., & Wöhrmann, A. (2013). Working capital management and firm profitability. Journal of Management Control, 24, 77–87. https://doi.org/10.1007/s00187-013-0173-3

Lyngstadaas, H. (2020). Packages or systems? Working capital management and financial performance among listed U.S. manufacturing firms. Journal of Management Control, 31, 403–450. https://doi.org/10.1007/s00187-020-00306-z

Lyngstadaas, H., & Berg, T. (2016). Working capital management: Evidence from Norway. International Journal of Managerial Finance, 12, 295–313. https://doi.org/10.1108/IJMF-01-2016-0012

Mättö, M., & Niskanen, M. (2021). Role of the legal and financial environments in determining the efficiency of working capital management in European SMEs. International Journal of Finance & Economics, 26, 5197–5216. https://doi.org/10.1002/ijfe.2061

Prasad, P., Narayanasamy, S., Paul, S., Chattopadhyay, S., & Saravanan, P. (2019). Review of literature on working capital management and future research agenda. Journal of Economic Surveys, 33, 827–861. https://doi.org/10.1111/joes.12299

Raddatz, C. (2006). Liquidity needs and vulnerability to financial underdevelopment. Journal of Financial Economics, 80, 677–722. https://doi.org/10.1016/j.jfineco.2005.03.012

Shin, H. H., & Soenen, L. (1998). Efficiency of working capital management and corporate profitability. Financial Practice and Education, 8, 37–45.

Shust, E., & Weiss, D. (2014). Discussion of asymmetric cost behavior-sticky costs: Expenses versus cash flows. Journal of Management Accounting Research, 26, 81–90. https://doi.org/10.2308/jmar-10406

Siciliano, G., & Weiss, D. (2023). Family ownership influence on cost elasticity. European Accounting Review, 2023, 1–31. https://doi.org/10.1080/09638180.2023.2244016

Singh, H. P., Kumar, S., & Colombage, S. (2017). Working capital management and firm profitability: A meta-analysis. Qualitative Research in Financial Markets, 9, 34–47. https://doi.org/10.1108/QRFM-06-2016-0018

Smith, K.V., Sell, S.B., 1980. Working capital management in practice. Readings on the management of working capital , pp. 51–84.

Subramaniam, C., Watson, M.W., 2016. Additional evidence on the sticky behavior of costs, in: Advances in Management Accounting. Emerald Group Publishing Limited. volume 26 of Advances in Management Accounting, pp. 275–305. 10.1108/S1474-787120150000026006.

Tauringana, V., & Adjapong Afrifa, G. (2013). The relative importance of working capital management and its components to SMEs’ profitability. Journal of Small Business and Enterprise Development, 20, 453–469. https://doi.org/10.1108/JSBED-12-2011-0029

Tong, H., & Wei, S. J. (2011). The composition matters: Capital inflows and liquidity crunch during a global economic crisis. The Review of Financial Studies, 24, 2023–2052. https://doi.org/10.1093/rfs/hhq078

Tulcanaza Prieto, A. B., Koo, J., & Lee, Y. (2019). Does cost stickiness affect capital structure? Evidence from Korea. Korean Journal of Management Accounting Research, 19, 27–57. https://doi.org/10.31507/KJMAR.2019.8.19.2.27

Ujah, N. U., Tarkom, A., & Okafor, C. E. (2020). Working capital management and managerial talent. International Journal of Managerial Finance, 17, 455–477. https://doi.org/10.1108/IJMF-12-2019-0481

Wang, B. (2019). The cash conversion cycle spread. Journal of Financial Economics, 133, 472–497. https://doi.org/10.1016/j.jfineco.2019.02.008

Wang, H., & Qiu, F. (2023). AI adoption and labor cost stickiness: Based on natural language and machine learning. Information Technology and Management. https://doi.org/10.1007/s10799-023-00408-9

Weiss, D. (2010). Cost behavior and analysts’ Earnings forecasts. The Accounting Review, 85, 1441–1471. https://doi.org/10.2308/accr.2010.85.4.1441

Acknowledgements

We appreciate many insightful comments from Hakim Lyngstadaas.

Funding

Open access funding provided by NTNU Norwegian University of Science and Technology (incl St. Olavs Hospital - Trondheim University Hospital).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors have no competing interests to declare.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix 1: Data descriptions

Appendix 1: Data descriptions

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Berg, T., Gustafsson, E. & Wahlstrøm, R.R. Cost management and working capital management: ebony and ivory in perfect harmony?. J Manag Control (2024). https://doi.org/10.1007/s00187-024-00368-3

Accepted:

Published:

DOI: https://doi.org/10.1007/s00187-024-00368-3