Abstract

The sectoral shift hypothesis asserts that sectoral shifts in labor demand can generate a significant unemployment even if the aggregate demand stays the same. Past studies tested the hypothesis using the dispersion of sectoral shocks as a proxy for the size of sectoral shifts and reported contradicting results which are sensitive to the model specification. This paper shows that the dispersion of sectoral shocks alone is insufficient to capture the aggregate layoffs caused by the sectoral shocks and that the shape of the distribution (skewness) of sectoral shocks plays a significant role. The sectoral shift hypothesis is tested as a joint test of the significance of dispersion and skewness. The new test strongly supports the hypothesis, and it is robust to model specifications. Sectoral shifts are also found to be a significant source of cyclical variation in the aggregate unemployment rate.

Similar content being viewed by others

Notes

The idea of sectoral shifts hypothesis has been also used in recent studies to introduce the persistent unemployment in the real business cycle model (Mikhail et al. 2003), to study the macroeconomic effects of reallocation shocks in European countries (Panagiotidis et al. 2003), and to examine the effect of sectoral shifts and employment specialization on the efficiency of the process with which unemployed workers are matched to available job vacancies in the regional labor market in UK (Robson 2004).

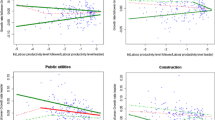

The least improvement of 55 % occurs in the first case of the left panel, but the aggregate layoff rates are extremely small in this case.

Aaronson et al. (2004) and Robson (2004) use the Lilien specification, and Loungani (1986) and Neelin (1987), use a variation of the Abraham and Katz specification. Neelin’s model of sectoral net hiring rates is the same as Abraham and Katz’s first model, but she also estimates the dispersion of aggregate net hiring rates and includes it in the estimation of the aggregate unemployment rate. Loungani’s model does not include the time trend and includes changes in oil prices in his second model.

This interpretation helps to answer the criticism of Gallipoli and Pelloni (2008) who argue that the underlying assumption of time-invariant variance of the purged sectoral shock in the normalization procedure contradicts the main idea of the sectoral shifts hypothesis that the distribution of sectoral shocks varies over time.

Specifically, let \(\hat{\sigma }_1 \)and \(\hat{\sigma }_2\) be the vectors of the estimates of dispersion based on the SICS and NAICS classification codes, respectively, over the overlapping sample period 1990Q1– 2003Q1. Let \(m_i \) and \(s_i\) be the mean and the standard deviation of \(\hat{\sigma }_i \). The adjusted estimate of dispersion based on the NAICS is computed by \(\tilde{\sigma }_{2t} =m_1 +s_1 (\hat{\sigma }_{2t} -m_2 )/s_2 \) for period \(t.\) The estimate of skewness coefficient is adjusted similarly.

As discussed below, this result is not robust to the choice of sample period.

Estimator \(\hbox {g}_{pc} \) gives qualitatively similar results.

Let \(Z_t {\beta }\) denote the right-hand side of (3.2a). We can write \(\hbox {UR}_t =Z_t {\beta }+ \sum _{s=1}^4 r_s (\hbox {UR}_{t-s} -Z_{t-s} {\beta })+{\eta }_t \), which is an autoregressive model with a white noise error term. The nonlinear restrictions are that the coefficient vector of \(Z_{t-s} \) is the product of the coefficient vector of \(Z_t \) and the coefficient of \(\hbox {UR}_{t-s} \).

Their study does not include the skewness in the unemployment rate equation. If the skewness is a significant factor to the expected mean as this paper showed, then it is likely to be a significant factor to quantiles also. Omitting this in their model can bias their estimate of the dispersion coefficient, and the bias depends not only on the relationship between omitted and included variables, but also on the quantile. This is shown by Angrist et al. (2006).

We are grateful to a referee who urged us to consider this new approach to avoid the weakness of the Lilien-type empirical approach.

References

Aaronson D, Rissman ER, Sullivan DG (2004) Can sectoral reallocation explain the jobless recovery? Econ Perspect Fed Reserve Bank Chic 28:36–49

Abraham KG, Katz LF (1984) Cyclical unemployment: sectoral shifts or aggregate disturbances? NBER working paper no. 1410

Abraham KG, Katz LF (1986) Cyclical unemployment: sectoral shifts or aggregate disturbances? J Polit Econ 94:507–522

Angrist J, Chernozhukov V, Fernandez-Val I (2006) Quantile regression under misspecification, with an application to the U.S. wage structure. Econometrica 74:539–563

Barro RJ (1977) Unanticipated money growth and unemployment in the United States. Am Econ Rev 67:101–115

Gallipoli G, Pelloni G (2008) Aggregate shocks vs reallocation shocks: an appraisal of the applied literature. Working paper series 27–08, The Rimini Centre for Economic Analysis

Ghayad R (2013) A decomposition of shifts of the beveridge curve. Public Policy Briefs, Federal Reserve Bank of Boston

Groenewold N, Hagger AJ (1998) The natural unemployment rate in Australia since the seventies. Econ Rec 74:24–35

Groshen EL, Potter S (2003) Has structural change contributed to a jobless recovery? Federal Reserve Bank of New York. Curr Issues Econ Financ 9:1–7

Groshen EL, Potter S, Sela R (2004) Was the 2001 recession different in the labor market? Comparing measures. Federal Reserve Bank of New York working paper

Hobijn B, Aysegeul S (2013) Beveridge curve shifts across countries since the great recession. working paper, Federal Reserve Bank of San Francisco

Hwang H (2009) Two-step estimation of a factor model in the presence of observable factors. Econ Lett 105:247–249

Lilien DM (1982) Sectoral shifts and cyclical unemployment. J Polit Econ 90:777–793

Loungani P (1986) Oil price shocks and the dispersion hypothesis. Rev Econ Stat 68:536–539

Mikhail O, Eberwein CJ, Handa J (2003) Can sectoral shift generate persistent unemployment in real business cycle models? University of Central Florida, Dept of Econ, working paper

Mills TC, Pelloni G, Zervoyianni A (1995) Unemployment fluctuations in the United States: further tests of the sectoral-shifts hypothesis. Rev Econ Stat 77:294–304

Neelin J (1987) Sectoral shifts and Canadian unemployment. Rev Econ Stat 69:718–723

Palley T (1992) Sectoral shifts and cyclical unemployment: a reconsideration. Econ Inq 30:117–133

Panagiotidis T, Pelloni G, Polasek W (2003) Macroeconomic effects of reallocation shocks: a generalised impulse response function analysis for three European countries. J Econ Integr 18:794–816

Panagiotidis T, Pelloni G (2013) Employment reallocation and unemployment revisited: a quantile regression approach. Working paper series 01–13, The Rimini Centre for Economic Analysis

Rissman ER (1993) Wage growth and sectoral shifts. J Monet Econ 31:395–416

Rissman ER (2003) Can sectoral labor reallocation explain the jobless recovery? Chic Fed Lett 197

Robson M (2004) Sectoral shifts, employment specialisation and the efficiency of matching: an analysis using UK regional data. University of Durham, Department of Econ and Finance, working paper

Sakata K (2002) Sectoral shifts and cyclical unemployment in Japan. J Jpn Int Econ 16:227–252

Samson L (1990) Sectoral shifts and aggregate unemployment: additional empirical evidence. Appl Econ 22:331–346

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Byun, Y., Hwang, Hs. Sectoral shifts or aggregate shocks? A new test of sectoral shifts hypothesis. Empir Econ 49, 481–502 (2015). https://doi.org/10.1007/s00181-014-0878-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-014-0878-7