Abstract

This paper investigates the association between real estate demand and the volatility of population changes. In a financial liberalized housing market, the housing mortgage loan implies insurance function to homeowners through the default option. Larger expected volatilities in the population imply a higher value of the default option. When analyzing the impact of the long-term population development on housing prices, the traditional deterministic population forecasting employed by previous research provides limited credibility. By means of the newly developed stochastic population forecasting methodology and counterfactual numerical simulations, we found a huge volatility associated with long-term population forecasting. A positive correlation between the expected volatility of population changes and real estate demand is ascertained.

Similar content being viewed by others

Notes

Hoynes and McFadden (1994)

The Supreme People’s Court of the People’s Republic of China.

Software R has been adopted to generate the multivariate normal distributed variables for changes in population, housing stock, and income. The singular value decomposition method was used in generating the multivariate normal distributed variables.

The data is from the 2009 Shanghai Statistics Yearbook. For the variables of income, population and housing supply, we use the published data on individual average disposable income, residential population and the area of newly constructed residential dwellings as the proxies.

For the minimum age of childbearing, β 4, we found that estimates were invariably equal to 15 years.

17.38, 17.32, and 16.76 million are for 2015, 2030, and 2040, respectively.

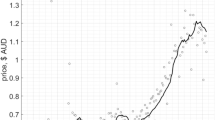

The price is published for January 2007 on http://www.ehomeday.com.

It is obtained by (predicted population mean in Year 2030 – population in Year 2000)/ population in Year 2000.

It is obtained by ((upper bound of 95% confidence interval – population in Year 2000)/ population in Year 2000)^2.

The “equivalent” population concept has been introduced by Mankiw and Weil (1989) and employed extensively afterwards. The core of “equivalent” population is to transform the nominal population number into another population number, which denotes an artificial population size as if all the people are at the same age group.

1.86, 5.03, and 10.08 million are for group younger than 25 years old, middle age group between 25 and 55 years old, and the old group with age above 55 years old, respectively.

\({\rm log}\left( {Y_t } \right)_{\rm adj} = {\rm log}\left( {Y_t } \right)-log\left( {Y_t } \right)_{\rm hat} ,\,\quad {\rm where} \quad {\rm log}\left( {Y_t } \right)_{\rm hat} =\hat {\gamma }_0 +\hat {\gamma }_1 {\rm log}\left( {N_t } \right)+\hat {\gamma }_2 {\rm log}\left( {K_t } \right).\)

\({\rm log}\left( {K_t } \right)_{\rm adj} = {\rm log}\left( {K_t } \right)-{\rm log}\left( {K_t } \right)_{\rm hat} ,\quad {\rm where} \quad {\rm log}\left( {K_t } \right)_{\rm hat} =\hat {\lambda }_0 +\hat {\lambda }_1 \,{\rm log}\left( {N_t } \right).\)

References

Abel AB (2001) Will bequests attenuate the predicted meltdown in stock prices when baby boomers retire? Rev Econ Stat 83(4):589–595

Abel AB (2003) The effects of a baby boom on stock prices and capital accumulation in the presence of social security. Econometrica 71(2):551–578

Ameriks J, Zeldes SP (2000) How do household portfolio shares vary with age? TIAA-CREF Working Paper

Bergantino S (1998) Life cycle investment behavior, demographics, and asset prices. Doctoral Dissertation, Department of Economics, MIT

Brooks RJ (1998) Asset market and saving effects of demographic transitions. Doctoral Dissertation, Department of Economics, Yale University

Cheng Y (2003) The impact of migration to shanghai on the performance of the social pension system. Master Thesis, Department of Economics, University of Oslo

China National Committee on Ageing (2008) The ageing of population and its implications in China. Country Statement. Available at http://en.cncaprc.gov.cn

Crawford GW, Rosenblatt E (1995) Efficient mortgage default option exercise: evidence from the mortgage insurance industry. J Real Estate Res 10(5):543–555

Cunningham D, Hendershott PH (1986) Pricing FHA mortgage default insurance NBER Working Paper No. W1382

Danthine JP, Donaldson JB (2002) Intermediate financial theory. Prentice Hall, Mahwah

Epperson JF, Kau JB, Kennan DC, Muller WJ (1985) Pricing default risk in mortgage. Rev Econ Stat 13(3):261–272

Fortin M, Leclerc A (2000) Demographic changes and real housing prices in Canada. Working Paper 00–06, Economics Department, University of Sherbrook

Foster C, Van Order R (1984) An option-based model of mortgage default. Hous Financ Rev 3(4):351–372

Foster C, Van Order R (1985) FHA terminations: a prelude to rational mortgage pricing. Rev Econ Stat 13(3):273–291

Girouard N, Kennedy M, Noord P, André C (2006) Recent house price developments: the role of fundamentals. OECD Economics Department Working Papers No. 475

Green MH (2003) Econometric analysis. Prentice Hall, NJ

Guiso L, Sapienza P, Zingales L (2009) Moral and social constraints to strategic default on mortgage. NBER Working Paper No. w15145

Han X (2010) Housing demand in Shanghai: a discrete choice approach. China Econ Rev 21(2):355–376

Hoem J, Hansen HO, Madsen D, Løvgreen Nielsen J, Olsen EM, Rennermalm B (1981) Experiments in modeling recent Danish fertility curves. Demography 18(2):231–244

Hoynes HW, McFadden D (1994) The impact of demographic on housing and non-housing wealth in the United States. NBER Working Paper No. w4666

Kau JB, Kim T (1994) Waiting to default: the value of delay. Rev Econ Stat 22(3):539–551

Kau JB, Keenan DC, Smurov AA (2004) Reduced-form mortgage valuation. Working Paper in Department of Insurance, Legal Studies and Real Estate, University of Georgia, Athens, Georgia

Keilman N, Pham D, Hetland A (2001) Norway’s uncertain demographic future. Working Paper in Statistics Norway, Oslo. ISBN 82–537–5002–1

Keilman N (2002) TFR predictions and Brownian motion theory. Yearb Popul Res Fin 38:209–221

Lutkepohl H (2005) New introduction to multiple time series analysis. Springer, Berlin

Mankiw NG, Weil DN (1989) The baby boom, the baby bust, and the housing market. Reg Sci Urban Econ 19(2):235–258

McFadden D (1993) Demographics, the housing market, and the welfare of the elderly. In: Wise D (ed) Studies in the economics of ageing. The University of Chicago Press, Chicago, pp 225–285

Ohtake F, Shintani M (1996) The effect of demographics on japanese housing market. Reg Sci Urban Econ 26(2):189–201

Ortalo-Magne F, Rady S (1999) Boom in, bust out: young household and the housing price cycle. Eur Econ Rev 43(4–6):755–766

Poterba JM (2001) Demographic structure and asset returns. Rev Econ Stat 83(4):565–584

Siegel J (1998) Stocks for the long run. McGraw Hill, New York

Vandell KD (1995) How ruthless is mortgage default? A review and synthesis of the evidence. J Hous Res 6(2):245–264

Yoo PS (1994) Age distributions and returns of financial assets. Federal Reserve Bank of St. Louis Working Paper 1994–002B

Acknowledgements

We would like to thank the anonymous referees, Nico Keilman, James M. Poterba, Olav Bjerkholt, John K. Dagsvik, Erik Biorn, Kaiji Chen, and Ke Wang for their valuable comments. We also gratefully acknowledge the support of National Natural Science Foundation of China (Research Project: #70632002, Fudan University, China) and the sponsor from Shanghai Pujiang Program.

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Alessandro Cigno

Appendix

Appendix

Starting from Eq. 14, we can get

Based on Eq. 29, we can have

The variance of \(\mathop P\limits^\bullet \) can be expressed as

To get the testable empirical counterpart of the Eq. 29, we first transform the variable into logarithm.

Then, we have the empirical regression specification as

If we regress Eq. 32 directly, it is going to be serious multicollinearities between the variables as testified by the correlations in Table 9. Therefore, we use the adjusted income and housing supplyFootnote 13 as the regressor instead. The regression results are presented in Table 10.

New residential land area allocated in Shanghai from 1995 to 2008. Source: 2002 and 2009 Shanghai statistics yearbook. For years before 2000, the new residential land volumes are published by the Statistics Yearbook 2000. For years after 2000, the new residential land areas are not published directly. Rather, the traded land volumes are published, which include both the new and the re-traded land. To proxy the new land volume, we subtract the residential volume of the “movers” from the total number

Age-specific birth rates, empirical values, and gamma curve fit for selected years

Stochastic predictions for TFR for Shanghai, with restriction (0.4–6)

Stochastic predictions for mean age at childbearing for Shanghai

Stochastic prediction for variance at age of childbearing for Shanghai

Stochastic predictions for life expectance at birth, male

Stochastic predictions for life expectance at birth, female

Stochastic population forecasting for 2015

Stochastic populations forecasting for 2030

Population pyramid in 2000

Rights and permissions

About this article

Cite this article

Cheng, Y., Han, X. Does large volatility help?—stochastic population forecasting technology in explaining real estate price process. J Popul Econ 26, 323–356 (2013). https://doi.org/10.1007/s00148-010-0349-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00148-010-0349-1