Abstract

Urban housing markets, along with markets of other assets, universally exhibit periods of strong price increases followed by sharp corrections. The mechanisms generating such non-linearities are not yet well understood. We develop an agent-based model populated by a large number of heterogeneous households. The agents’ behavioral rules are consistent with the concept of bounded rationality. The model is calibrated using several large and distributed datasets of the Greater Sydney region (demographic, economic and financial) across three specific and diverse periods since 2006. The model is not only capable of explaining price dynamics during these periods, but also reproduces the novel behavior actually observed immediately prior to the market peak in 2017, namely a sharp increase in the variability of prices. This novel behavior is related to a combination of trend-following aptitude of the household agents (herding) and their collective propensity to borrow. Trend-following behavior is found to be essential in replicating market dynamics.

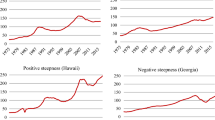

Source: Securities Industry Research Centre of Asia–Pacific on behalf of CoreLogic, Inc

Similar content being viewed by others

Availability of data and materials

All data needed to evaluate the conclusions in the paper are present or referred to in the paper. The reference data for housing transactions are owned by CoreLogic, Inc. Additional information related to this paper may be requested from the authors.

References

Alfarano S, Lux T, Wagner F (2005) Estimation of agent-based models: the case of an asymmetric herding model. Comput Econ 26(1):19–49

Alfarano S, Lux T, Wagner F (2008) Time variation of higher moments in a financial market with heterogeneous agents: an analytical approach. J Econ Dyn Control 32(1):101–136

Arthur BW (2006) Out-of-equilibrium economics and agent-based modeling. In: Tesfatsion L, Judd KL (eds) Handbook of computational economics: agent-based computational economics. Chapter 32, vol 2. Elsevier, pp 1551–1564

Assenza T, Gatti DD, Grazzini J (2015) Emergent dynamics of a macroeconomic agent based model with capital and credit. J Econ Dyn Control 50:5–28

Axtell RL, Epstein JM, Dean JS, Gumerman GJ, Swedlund AC, Harburger J, Chakravarty S, Hammond R, Parker J, Parker M (2002) Population growth and collapse in a multiagent model of the Kayenta Anasazi in Long House Valley. Proc Natl Acad Sci 99:7275–7279

Axtell R et al (2012) Getting at systemic risk via an agent-based model of the housing market. Am Econ Rev 102(3):53–58

Axtell R, Farmer D, Geanakoplos J, Howitt P, Carrella E, Conlee B, Goldstein J, Hendrey M, Kalikman P, Masad D, Palmer N, Yang C-Y (2014) An agent-based model of the housing market bubble in metropolitan Washington, D.C. In: Deutsche Bundesbank’s Spring Conference on “Housing markets and the macroeconomy: Challenges for monetary policy and financial stability”, Deutsche Bundesbank

Bailey MJ, Muth RF, Nourse HO (1963) A regression method for real estate price index construction. J Am Stat Assoc 58:933–942

Banwo O, Harrald P, Medda F (2019) Understanding the consequences of diversification on financial stability. J Econ Interac Coord 14(2):273–292

Baptista R, Farmer JD, Hinterschweiger M, Low K, Tang D, Uluc A (2016) Macroprudential policy in an agent-based model of the UK housing market. Staff Working Paper 619, Bank of England

Barde S (2016) Direct comparison of agent-based models of herding in financial markets. J Econ Dyn Control 73:329–353

Barthelemy M (2016) The structure and dynamics of cities: urban data analysis and theoretical modeling. Cambridge University Press

Bikhchandani S, Welch I, Hirshleifer DA (1992) A theory of fads, fashion, custom, and cultural change as informational cascades. J Polit Econ 100(5):992–1026

Bonabeau E (2002) Agent-based modeling: methods and techniques for simulating human systems. Proc Natl Acad Sci 99:7280–7287

Bouchaud J-P (2013) Crises and collective socio-economic phenomena: simple models and challenges. J Stat Phys 151:567–606

Brock WA, Durlauf SN (2001) Discrete choice with social interactions. Rev Econ Stud 68(2):235–260

Brock WA, Hommes CH (1998) Heterogeneous beliefs and routes to chaos in a simple asset pricing model. J Econ Dyn Control 22(8–9):1235–1274

Cardaci A (2018) Inequality, household debt and financial instability: an agent-based perspective. J Econ Behav Organ 149:434–458

Carro A, Toral R, San MM (2015) Markets, herding and response to external information. PLoS ONE 10(7):e0133287

Case KE, John MQ, Robert JS (2003) Home-buyers, housing and the macroeconomy. In: Anthony R, Tim R (eds) Asset prices and monetary policy. Reserve Bank of Australia, pp 149–188

Chen JJ, Tan L, Zheng B (2015) Agent-based model with multi-level herding for complex financial systems. Sci Rep 5:8399

Cincotti S, Raberto M, Teglio A (2010) Credit money and macroeconomic instability in the agent-based model and simulator eurace. Economics 4:26

Cliff OM, Harding N, Piraveenan M, Erten EY, Gambhir M, Prokopenko M (2018) Investigating spatiotemporal dynamics and synchrony of influenza epidemics in Australia: an agent-based modelling approach. Simul Model Pract Theory 87:412–431

Cont R, Bouchaud JP (2000) Herd behaviour and aggregate fluctuations in financial markets. Macroecon Dyn 4:170–196

Crosato E, Nigmatullin R, Prokopenko M (2018) On critical dynamics and thermodynamic efficiency of urban transformations. Roy Soc Open Sci 5:180863

Dawid H, Gatti DD (2018) Agent-based macroeconomics. In: Cars H, Blake LB (eds) Handbook of computational economics, vol IV. Elsevier

Dosi G, Fagiolo G, Napoletano M, Roventini A (2013) Income distribution, credit and fiscal policies in an agent-based Keynesian model. J Econ Dyn Control 37(8):1598–1625

Erlingsson EJ, Teglio A, Cincotti S, Stefansson H, Sturluson JT, Raberto M (2014) Housing market bubbles and business cycles in an agent-based credit economy. Economics 8(2014-8):1–42. https://doi.org/10.5018/economics-ejournal.ja.2014-8

Evans BP, Glavatskiy K, Harré MS, Prokopenko M (2021) The impact of social influence in Australian real-estate: market forecasting with a spatial agent-based model. J Econ Interact Coord. https://doi.org/10.1007/s11403-021-00324-7

Farmer JD, Foley D (2009) The economy needs agent-based modelling. Nature 460:685–686

Farmer JD, Geanakoplos J (2009) The virtues and vices of equilibrium and the future of financial economics. Complexity 14(3 Special Issue: Econophysics):11–38

Filatova T, Verburg PH, Parker DC, Stannard CA (2013) Spatial agent-based models for socio-ecological systems: challenges and prospects. Environ Model Softw 45:1–7

Ge J (2017) Endogenous rise and collapse of housing price. An agent-based model of the housing market. Comput Environ Urban Syst 62:182–198

Geanakoplos J (2010) The leverage cycle. NBER Macroecon Annu 24(1):1–66

Geanakoplos J, Axtell R, Farmer DJ, Howitt P, Conlee B, Goldstein J, Hendrey M, Palmer NM, Yang C-Y (2012) Getting at systemic risk via an agent-based model of the housing market. Am Econ Rev 102(3):53–58

Germann TC, Kadau K, Longini IM, Macken CA (2006) Mitigation strategies for pandemic influenza in the United States. Proc Natl Acad Sci 103(15):5935–5940

Gilbert N, Hawksworth J, Swinney PA (2009) An agent-based model of the English housing market. In: Papers from the 2009 AAAI Spring Symposium, Technical Report SS-09–09, Stanford, California, USA, March 23–25. AAAI Spring Symposium

Grimm V, Revilla E, Berger U, Jeltsch F, Mooij WM, Railsback SF, Thulke H-H, Weiner J, Wiegand T, De Angelis DL (2005) Pattern-oriented modeling of agent-based complex systems: lessons from ecology. Science 310:987–991

Guilmi CD (2017) The agent-based approach to post Keynesian macro-modeling. J Econ Surv 31(5):1183–1203

Haldane AG, Turrell AE (2017) An interdisciplinary model for macroeconomics. Oxf Rev Econ Policy 34(1–2):219–251

Haldane AG, Turrell AE (2019) Drawing on different disciplines: macroeconomic agent-based models. J Evol Econ 29(1):39–66

Harré MS, Harris A, McCallum S (2019) Singularities and catastrophes in economics: historical perspectives and future directions. Revue Roumaine des Mathematiques Pures et Appliquees 64(4):403–429

Jensen HJ, Arcaute E (2010) Complexity, collective effects, and modeling of ecosystems: formation, function, and stability. Ann NY Acad Sci 1195:E19–E26

Goldstein J, Axtell R, Farmer D, Geanakoplos J, Howitt P, Hendrey M, Palmer N, Conlee B, Yang C-Y, Carrella E, Kalikman P (2017) Rethinking housing with agent-based models: models of the housing bubble and crash in the Washington DC area 1997–2009. PhD Dissertation, George Mason University

Kaplan G, Mitman K, Violante GL (2017) The housing boom and bust: model meets evidence. Tech. rep. National Bureau of Economic Research

Kirman A (1993) Ants, rationality, and recruitment. Q J Econ 108(1):137–156

Kouwenberg R, Zwinkels RCJ (2015) Endogenous Price Bubbles in a Multi-Agent System of the Housing Market. PLoS ONE 10(6):e0129070

Lauretta E (2018) The hidden soul of financial innovation: an agent-based modelling of home mortgage securitization and the finance-growth nexus. Econ Model 68:51–73

Mazzocchetti A, Raberto M, Teglio A, Cincotti S (2018) Securitization and business cycle: an agent-based perspective. Ind Corp Change 27(6):1091–1121

Mérő B (2019) Novel modelling of the operation of the financial intermediary system–agent-based macro models. Fin Econ Rev 8(3):83–113

Pangallo M, Nadal J-P, Vignes A (2019) Residential income segregation: a behavioral model of the housing market. J Econ Behav Organ 159:15–35

Poledna S, Miess MG, Hommes C (2019) Economic Forecasting with an Agent-based Model. SSRN Electron J. https://doi.org/10.2139/ssrn.3484768

Raberto M, Ozel B, Ponta L, Teglio A, Cincotti S (2019) From financial instability to green finance: the role of banking and credit market regulation in the Eurace model. J Evol Econ 29(1):429–465

Randolph B, Pinnegar S, Tice A (2013) The first home owner boost in Australia: a case study of outcomes in the Sydney housing market. Urban Policy Res 31(1):55–73

Reinhart CM, Rogoff KS (2009) This time is different: eight centuries of financial folly. Princeton University Press

Rogers JD, Cegielski WH (2017) Building a better past with the help of agent-based modeling. Proc Natl Acad Sci 114(49):12841–12844

Simon HA (1955) A behavioral model of rational choice. Q J Econ 69(1):99–118

Teglio A, Raberto M, Cincotti S (2012) The impact of banks’ capital adequacy regulation on the economic system: an agent-based approach. Adv Complex Syst 15(supp02):1250040

Tesfatsion L (2006) Agent-based computational economics: a constructive approach to economic theory. In: Tesfatsion L, Judd KL (eds) Handbook of computational economics: agent-based computational economics, vol 2. Elsevier, pp 831–880

Xin C, Huang J-P (2017) Recent progress in econophysics: Chaos, leverage, and business cycles as revealed by agent-based modeling and human experiments. Front Phys 12(6):128910

Yang J, Carro A (2020) Two tales of complex system analysis: MaxEnt and agent-based modelling. Eur Phys J Special Topics 229:1623–1643

Zachreson C, Fair KM, Cliff OM, Harding N, Piraveenan M, Prokopenko M (2018) Urbanization affects peak timing, prevalence, and bimodality of influenza pandemics in Australia: results of a census-calibrated model. Sci Adv 4:eaau5294

Acknowledgements

Authors thank Markus Brede and Doyne J. Farmer for useful comments on the paper draft. Data on housing transactions are supplied by Securities Industry Research Centre of Asia-Pacific (SIRCA) on behalf of CoreLogic, Inc. (Sydney, Australia). We also acknowledge the Australian Bureau of Statistics for the access to Census data and the Melbourne Institute for the access to the “Household, Income and Labour Dynamics in Australia” Survey.

Funding

This work is supported by the Australian Research Council Discovery Project DP170102927 for MH and MP and by University of Sydney Mobility Scheme-2019 for KG.

Author information

Authors and Affiliations

Contributions

KG analyzed the source data, developed the software code, performed and analyzed the simulations, and prepared the manuscript (“Model”, “Implementation”, and “Results” sections, Figures, and Tables); KG, MP, and MH developed the model; AC consulted on agent-based modeling; PO consulted on economic modeling; all authors contributed to “Introduction”, “Related works”, and “Discussion” sections of the manuscript.

Corresponding authors

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interests.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Glavatskiy, K.S., Prokopenko, M., Carro, A. et al. Explaining herding and volatility in the cyclical price dynamics of urban housing markets using a large-scale agent-based model. SN Bus Econ 1, 76 (2021). https://doi.org/10.1007/s43546-021-00077-2

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s43546-021-00077-2