Abstract

In this paper, a fractional-order model of a financial risk dynamical system is proposed and the complex behavior of such a system is presented. The basic dynamical behavior of this financial risk dynamic system, such as chaotic attractor, Lyapunov exponents, and bifurcation analysis, is investigated. We find that numerical results display periodic behavior and chaotic behavior of the system. The results of theoretical models and numerical simulation are helpful for better understanding of other similar nonlinear financial risk dynamic systems. Furthermore, the adaptive fuzzy control for the fractional-order financial risk chaotic system is investigated on the fractional Lyapunov stability criterion. Finally, numerical simulation is given to confirm the effectiveness of the proposed method.

Similar content being viewed by others

1 Introduction

Chaotic systems have received more attention due to their potential applications in economics and management, such as equity market indices: cases from the United Kingdom [1], monetary aggregates [2], business cycle [3], firm growth and R&D investment [4], chaotic behavior in foreign direct investment, and foreign capital investments [5, 6].

Some nonlinear models have been established to investigate the complex economic dynamics such as Goodwin’s accelerate model [7], Van der Pol’s models [8], Duffing–Holmes model [9], Kaldoria model [10], and IS-LM model [11]. In recent years, chaotic economics has obtained intensive attention and has been raised to engineering applications for understanding the complex behavior of the real financial market. In [12], Chen studied the chaos behavior in a financial system with the help of fractional order. In [13], Gao and Ma introduced a new finance chaotic system and exhibited Hopf bifurcation in the qualitative analysis of the finance system. In [14], Wang et al. described a finance chaotic system with delayed fractional order. In [15], Yu et al. used speed feedback control and linear feedback control for stabilizing hyperchaotic finance system to unstable equilibrium. In [16], Wang et al. designed the sliding mode controller (SMC) for an uncertain chaotic fractional-order economic system. In [17], Vaidyanathan et al. devised a new finance chaotic system and discussed its passivity-based synchronization with circuit realization of the system. The study of economic dynamics with the approach fractional order can be seen in references [18, 19].

In this work, a financial risk chaotic system is proposed and its properties are elucidated. In Sect. 2, we present the properties and dynamics of a new fractional-order financial risk chaotic system and investigate the properties numerically via Lyapunov exponents and bifurcation diagram. Section 2 also contains the results of simulation and analysis of the new fractional-order financial risk chaotic system. Section 3 describes the adaptive fuzzy control for the fractional-order financial risk chaotic system. Section 4 contains the conclusions of this work.

2 Model of fractional-order financial risk system

At present, there are many different definitions for the fractional calculus, such as G-L definition, R-L definition, and Caputo definition. The Caputo fractional derivative is widely used in the engineering application fields. The main reason is that this definition is in the order of differential and integral, thus it a clearer physical meaning. In this work, we utilized the Caputo definition, which is defined by [20]

where q is the order of fractional derivative, m is the lowest integer which is not less than q, and Γ is the gamma function

In 2013, Xiao-Dan et al. [21] reported a financial risk chaotic system:

In (3), x, y, z describe occurrence value risk, analysis value risk, and control value risk in the current market, respectively. The parameter δ denotes the analysis risk efficiency, r denotes the transmission rate of previous risk, and b denotes the distortion coefficient of risk control. Three state variables x, y, and z must be positive, because risk in financial markets always exists as the market occurs. The system (3) is chaotic when the parameter values are taken as \(\delta = 10\), \(r = 28\), and \(b = \frac{8}{3}\). We take the initial conditions of system (3) as \((10, 10, 10)\).

The mathematical description of the commensurate fractional-order model of the financial risk chaotic system (3) can be expressed as follows:

In (4), \(q_{1}\), \(q_{2}\), and \(q_{3}\) are the fractional orders of the respective states. a, b, c are constant positive parameters of the system. For numerical simulation of fractional-order model (4) of the financial risk chaotic systems, the Adams–Bashforth–Moulton predictor-corrector scheme is used [22–27].

The dynamic evolution graphs of the system are obtained by means of bifurcation diagram and Lyapunov exponents. They show dynamics of the system with the variation of system parameters. Particularly, Lyapunov exponents in the q-r parameter plane can give us a clear view of the state of the system.

The dynamical behavior of the financial risk chaotic system can be characterized by its Lyapunov exponents which are computed numerically by Wolf algorithm [28]. The Lyapunov exponents of the financial risk chaotic system are obtained as \(L1 = 1.251\), \(L2 = 0\), and \(L3 = -14.9197\), while the Kaplan–Yorke dimension of the financial risk chaotic system is obtained as \(D_{KY} = 3.0839\).

In this study, we analyze bifurcation behavior of the fractional-order financial risk system (4) in many cases.

Case (A)

Here, we fix \(q_{2} = 1\), \(q_{3} = 1\), and \(q_{1}\) varies from 0.4 to 1. The bifurcation diagram is shown in Fig. 1(a). According to Fig. 1(a), chaotic behavior can be seen for \(q_{1} \in [0.63, 1]\) and for \(q_{1}\leq 0.62\), system (4) exhibits periodic motion.

Bifurcation diagrams of the fractional-order financial risk system with derivative order varying (a) \(q_{1}\) varying, \(q_{2} =1\), \(q_{3}=1\) and \(r=28\); (b) \(q_{2}\) varying, \(q_{1}=1\), \(q_{3}=1\) and \(r=28\); (c) \(q_{3}\) varying, \(q_{1}=1\), \(q_{2}=1\) and \(r=28\); (d) \(q_{1}= q_{2}=q_{3}=q\) varying and \(r=28\)

Case (B)

Here, we fix \(q_{1} = 1\), \(q_{3} = 1\), and \(q_{2}\) varies from 0.7 to 1. The system exhibits chaotic behavior for \(q_{1}\in [0.9, 1]\). The system shows periodic behavior for \(q_{1}< 0.9\). This has been confirmed in the bifurcation diagram analysis (see Fig. 1(b)).

Case (C)

Here, we fix \(q_{1} = 1\), \(q_{2} = 1\). Let the derivative order \(q_{3}\) vary from 0.7 to 1. It is shown in Fig. 1(c) that the system is chaotic over the interval \(q_{3}\in [0.9, 1]\) and the system behavior becomes periodic motion for \(q_{3}< 0.9\).

Case (D)

Here, we fix \(q_{1}= q_{2} = q_{3}= q\). The dynamical properties of the system with r and q varying are analyzed. The bifurcation diagram and LEs for derivative order \(q \in [0.9, 1]\) are shown in Figs. 1(d) and 2(a). The chaotic zone covers most of the range \(q \in [0.944, 1]\), excepting a periodic window near \(q \leq 0.943\). In addition, for \(q_{1}=q_{2}=q_{3}=0.98\) and vary the system parameter r from 5 to 30. The resulting bifurcation diagram is shown in Fig. 3(a), and LCE result is presented in Fig. 2(b). The largest increases with the increase of r, and when r is larger than 10.18, the system is chaotic. Also, \(q_{1}=q_{2}=q_{3}=0.95\) and r varying from 5 to 30 are shown in Fig. 3(b).

LEs of the fractional-order financial risk system (a) LEs with q varying; (b) LEs with r varying

Bifurcation diagrams of the fractional-order financial risk system with parameter r varying (a) \(q_{1}=q_{2}=q_{3}=0.98\) and r varying; (b) \(q_{1}=q_{2}=q_{3}=0.95\) and r varying

Complexity of the fractional-order financial risk chaotic system with derivative q and control parameter r varying is analyzed, where the step size of q is 0.001 and in the range of \(q \in [0.9, 1]\). In addition, step size of r is 0.25 and in the range of \(r \in [5, 30]\). LEs in the \(q-r\) plane are shown in Fig. 4(a)–4(d).

\(q-r\) plane of the fractional-order financial risk system (a) LEs 1, r, q plane, (b) r, q plane, (c) LEs 2, r, q plane, and (d) LEs 3, r, q plane

3 Adaptive fuzzy control for the fractional-order financial risk chaotic system

3.1 Fuzzy logic system

Fuzzy logic system includes singleton fuzzification, sum-product inference, and center off-sets defuzzification, which can be expressed by

where x is the input, \(f(x)\) is the output. The membership of jth rule is \(\mu _{F_{i}^{j}}(x_{i})\), and the centroid of the jth consequent set is \(\theta _{j}\). Then (5) can be rewritten as follows:

where \(\theta = [\theta _{1},\ldots,\theta _{N}]\), \(\psi (x)=[p_{1}(x),p_{2}(x),\ldots,p_{N}(x)]^{T}\) and the fuzzy basis function is \(p_{j}(x)= \frac{\prod^{n}_{i=1}\mu _{F_{i}^{j}}(x_{i})}{\sum^{N}_{j=1} [\prod^{n}_{i=1}\mu _{F_{i}^{j}}(x_{i}) ] }\).

Lemma 1

([29])

Suppose that \(f(x)\) is a continuous function and \(x\in \Omega \), where Ω is a compact set. For (6), there exists a fuzzy system such that

where \(\varepsilon >0\).

3.2 Controller design and stability analysis

Adaptive fuzzy control of the commensurate fractional-order model of financial risk chaotic system (4) is as follows:

Let \(f_{1}(x_{1})=\delta y+yz\), \(f_{2}(y_{2})=-xz+rx\), and \(f_{3}(z_{3})=xy\) be unknown as nonlinear functions, respectively. Then system (8) can be rewritten as

Based on Lemma 1, the unknown functions can be respectively approximated by a fuzzy logic system as follows:

Let the optimal parameter estimation of fuzzy systems be \(\theta ^{\ast }_{i}=\min [\sup \vert f_{i}-\hat{f_{i}}(, \theta _{i}) \vert ]\), where \(\theta ^{\ast }_{i}\) is a constant.

Let the parameter error and optimal estimation error of the fuzzy system be respectively

Based on [30], we can suppose that \(\vert \varepsilon _{i} \vert \leq \varepsilon ^{\ast }_{i}\), where \(\varepsilon ^{\ast }_{i}\) is a positive constant.

The estimation error of the unknown nonlinear function can be written as

Based on the above discussion, the controllers can be designed as

where \(k_{i}>0\), \(\hat{\varepsilon }^{\ast }_{i} \) is an estimate of the unknown constant \(\varepsilon ^{\ast }_{i}\) for \(i=1,2,3\).

In this subsection, we propose the fractional-order parameters adaptive laws as follows:

where \(\mu _{i},\sigma _{i}>0\), \(i=1,2,3\).

To check the stability of the controlled system, some results of stability analysis of fractional-order systems are given in advance as follows.

Lemma 2

([30])

Let \(V=\frac{1}{2}x^{2}+\frac{1}{2}y^{2}\), where \(x,y \in R\) and x, y have a continuous first derivative, respectively. If there exists a constant \(h>0\) satisfying

then one has

where \(E^{q}(-2ht^{q})\) is the Mittag-Leffler function.

Lemma 3

([30])

Let \(V=\frac{1}{2}x^{T}x+\frac{1}{2}y^{T}y\), where \(x,y \in R^{n}\) and x, y have a continuous first derivative, respectively. There exists a constant \(k>0\) such that

Then \(\Vert x \Vert \), \(\Vert y \Vert \) are bounded and x asymptotically approaches zero, where \(\Vert \varepsilon \Vert \) represents Euclid from.

Lemma 4

If \(x \in R^{n}\) is a continuous differentiable function, one holds

In order to facilitate, we write the fractional order of system (8) as q. From what has been discussed above we can obtain the following:

where \(a_{1}=\delta +k_{1}\).

Multiply both sides of the equation (26) by \(x^{T}\), one has

Similar, we can obtain

where \(a_{2}=1+k_{2}\), \(a_{3}=b+k_{3}\).

Theorem 1

Under given initial conditions, the variables x, y, and z of fractional-order system (8) converge to zero under the action of adaptive controller (14), (15), (16) and fractional-order parameter adaptive laws (17), (18), (19), (20), (21), (22), and all variables in the closed-loop system are bounded.

Proof

Let the Lyapunov function be

where \(\tilde{\theta }_{1}=\hat{\theta }_{1}-\theta ^{\ast }_{1}\) and \(\tilde{\varepsilon }^{\ast }_{1}=\hat{\varepsilon }^{\ast }_{1}- \varepsilon ^{\ast }_{1}\).

Based on Lemma 4, (17), (18), and (28), we can obtain

where \(a_{1}>0\). We know from Lemma 3 that x asymptotically approaches zero, namely \(\lim_{t\to \infty } \Vert x \Vert =0\).

Choose the Lyapunov function as

where \(\tilde{\theta }_{2}=\hat{\theta }_{2}-\theta ^{\ast }_{2}\) and \(\tilde{\varepsilon }^{\ast }_{2}=\hat{\varepsilon }^{\ast }_{2}- \varepsilon ^{\ast }_{2}\).

Based on Lemma 4, (19), (20), and (29), we can obtain

where \(a_{2}>0\). We know from Lemma 3 that y asymptotically approaches zero, namely \(\lim_{t\to \infty } \Vert y \Vert =0\).

Consider the Lyapunov function

where \(\tilde{\theta }_{3}=\hat{\theta }_{3}-\theta ^{\ast }_{3}\) and \(\tilde{\varepsilon }^{\ast }_{3}=\hat{\varepsilon }^{\ast }_{3}- \varepsilon ^{\ast }_{3}\).

Based on Lemma 4, (21), (22), and (30), we can obtain

where \(a_{3}>0\). We know from Lemma 3 that z asymptotically approaches zero, namely \(\lim_{t\to \infty } \Vert z \Vert =0\). □

Noting that \(\tilde{\varepsilon }^{\ast }_{i} \in R\), \(i=1,2,3\), so it has \(\tilde{\varepsilon }^{\ast }_{i}=\tilde{\varepsilon }^{\ast T}_{i}\).

We know from Lemma 2 that \(\tilde{\theta }_{i}\), \(\tilde{\varepsilon }^{\ast }_{i}\) are bounded, and \(\hat{\theta }_{i}\), \(\hat{\varepsilon }^{\ast }_{i}\) are also bounded. From the above proof, x, y, and z are bounded, and the construction of controllers (14), (15), and (16) shows that \(u_{i}\) is bounded for \(i=1,2,3\). So, all signals in a closed loop system (8) are bounded.

3.3 Simulation studies

In this subsection, we choose fractional-order system (8) as an example.

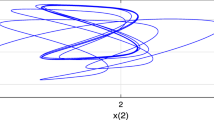

Let the parameters of the financial risk chaotic system (8) be \(\delta =10\), \(r=28\), \(b=\frac{8}{3}\), with the initial conditions of system (8) being \((2.5,0.5,4)\) and \(q=0.95\). In the simulation, x, y, z are the inputs of the fuzzy systems. We choose four Gaussian membership functions on \([-3,3]\). \(k_{1}=15\), \(k_{2}=15\), \(k_{3}=10\) and \(\mu _{i}=700\), \(\sigma _{i}=0.8\) for \(i=1,2,3\). The estimated value of the approximation error of the fuzzy system is \(\hat{\varepsilon }^{\ast }_{1}(0)=1\), \(\hat{\varepsilon }^{\ast }_{2}(0)=1\), \(\hat{\varepsilon }^{\ast }_{3}(0)=1.5\). The simulation results are shown in Fig. 5, Fig. 6, and Fig. 7. In Fig. 5, the system variables have a rapid convergence. Figure 6 shows the smoothness of the control inputs, and Fig. 7 indicates the convergence of the fuzzy parameters under the proposed fractional-order adaptation laws. It has been shown that good control performance has been obtained.

Time response of system variables

Control inputs

Fuzzy parameters

4 Conclusion

In this paper, the numerical solution of a fractional-order financial risk chaotic system was investigated and all parameter values of the system were determined. Dynamical analysis of the new fractional-order financial risk chaotic system was described by the phase portraits, Lyapunov exponents spectrum, and bifurcation diagram. We found that the chaotic behavior exists for the new fractional-order financial risk system in the range \(q_{1}\in [0.63, 1]\), \(q_{2} \in [0.9, 1]\), \(q_{3} \in [0.9, 1]\), and \(q \in [0.944, 1]\). Also, periodic behavior exists for the fractional-order financial risk system in the range of \(q_{1} \leq 0.62\), \(q_{2} < 0.9\), \(q_{3} < 0.9\), and \(q \leq 0.943\). An adaptive fuzzy approach has been presented in this study to handle the control problem for the fractional-order financial risk system. Based on the proposed method, simulation results were given to indicate the effectiveness of the proposed scheme.

Availability of data and materials

Not applicable in our research.

References

Abhyankar, A., Copeland, L.S., Wong, W.: Nonlinear dynamics in real-time equity market indices: evidence from the United Kingdom. Econ. J. 105(431), 864–880 (1995)

Barnett, W., Chen, P.: Deterministic chaos and fractal attractors as tools for nonparametric dynamical econometric inference: with an application to the divisia monetary aggregates. Math. Comput. Model. 10(4), 275–296 (1988)

Hallegatte, S., Ghil, M., Dumas, P., Hourcade, J.C.: Business cycles, bifurcations and chaos in a neo-classical model with investment dynamics. J. Econ. Behav. Organ. 167(1), 57–77 (2008)

Klette, T.J., Griliches, Z.: Empirical patterns of firm growth and R&D investment: a quality ladder model interpretation. Econ. J. 110(463), 363–387 (2000)

Hsiao, F.S., Hsiao, M.C.W.: The chaotic attractor of foreign direct investment—why China?: a panel data analysis. J. Asian Econ. 15(4), 641–670 (2004)

Bouali, S., Buscarino, A., Fortuna, L., Frasca, M., Gambuzza, L.V.: Emulating complex business cycles by using an electronic analogue. Nonlinear Anal., Real World Appl. 13(6), 2459–2465 (2012)

Lorenz, H.W., Nusse, H.E.: Chaotic attractors, chaotic saddles, and fractal basin boundaries: Goodwin’s nonlinear accelerator model reconsidered. Chaos Solitons Fractals 13(5), 957–965 (2002)

Chian, A.C.L., Borotto, F.A., Rempel, E.L., Rogers, C.: Attractor merging crisis in chaotic business cycles. Chaos Solitons Fractals 24(3), 869–875 (2015)

Hosseinnia, S., Ghaderi, R., Mahmoudian, M., Momani, S.: Sliding mode synchronization of an uncertain fractional order chaotic system. Comput. Math. Appl. 59(5), 1637–1643 (2010)

Lorenz, H.W.: Nonlinear Dynamical Economics and Chaotic Motion. Springer, Berlin (1993)

Fanti, L., Manfredi, P.: Chaotic business cycles and fiscal policy: an IS-LM model with distributed tax collection lags. Chaos Solitons Fractals 32(2), 736–744 (2007)

Chen, W.C.: Nonlinear dynamics and chaos in a fractional-order financial system. Chaos Solitons Fractals 36(5), 1305–1314 (2008)

Gao, Q., Ma, J.: Chaos and Hopf bifurcation of a finance system. Nonlinear Dyn. 58(1), 209–216 (2009)

Wang, Z., Huang, X., Shi, G.: Analysis of nonlinear dynamics and chaos in a fractional order financial system with time delay. Comput. Math. Appl. 62(3), 1531–1539 (2011)

Yu, H., Cai, G., Li, Y.: Dynamic analysis and control of a new hyperchaotic finance system. Nonlinear Dyn. 67(3), 2171–2182 (2012)

Wang, Z., Huang, X., Shen, H.: Control of an uncertain fractional order economic system via adaptive sliding mode. Neurocomputing 83, 83–88 (2012)

Vaidyanathan, S., Sambas, A., Kacar, S., Cavusoglu, U.: A new finance chaotic system, its electronic circuit realization, passivity based synchronization and an application to voice encryption. Nonlinear Eng. 8, 193–205 (2019)

Abd-Elouahab, M.S., Hamri, N.E., Wang, J.: Chaos control of a fractional-order financial system. Math. Probl. Eng. 2010, Article ID 270646 (2010)

Hajipour, A., Tavakoli, H.: Analysis and circuit simulation of a novel nonlinear fractional incommensurate order financial system. Optik, Int. J. Light Electron Opt. 127(22), 10643–10652 (2016)

Caputo, M.: Linear models of dissipation whose Q is almost frequency independent—II. Geophys. J. Int. 13(5), 529–539 (1967)

Xiao-Dan, Z., Xiang-Dong, L., Yuan, Z., Cheng, L.: Chaotic dynamic behavior analysis and control for a financial risk system. Chin. Phys. B 22(3), 030509 (2013)

Petráš, I.: Fractional-Order Nonlinear Systems: Modeling, Analysis and Simulation. Springer, Berlin (2011)

Herrmann, R.: Fractional Calculus: An Introduction for Physicists. World Scientific, Singapore (2011)

Caponetto, R., Dongola, G., Fortuna, L., Petráš, I.: Fractional Order Systems: Modeling and Control Applications World Scientific, Singapore (2011)

Yang, X.J.: General Fractional Derivatives: Theory, Methods and Applications. CRC Press, New York (2019)

Yang, X.J., Peng, Y.Y., Cattani, C., Inc, M.: Fundamental solutions of anomalous diffusion equations with the decay exponential kernel. Math. Methods Appl. Sci. 42(11), 4054–4060 (2019)

Liu, J.G., Yang, X.J., Feng, Y.Y., Cui, P.: On group analysis of the time fractional extended \((2+1)\)-dimensional Zakharov–Kuznetsov equation in quantum magneto-plasmas. Math. Comput. Simul. 178, 407–421 (2020)

Wolf, A., Swift, J.B., Swinney, H.L., Vastano, J.A.: Determining Lyapunov exponents from a time series. Phys. D: Nonlinear Phenom. 16(3), 285–317 (1985)

Li-Xin, W.: Adaptive Fuzzy Systems and Control: Design and Stability Analysis. Prentice Hall, New York (1994)

Liu, H., Chen, Y., Li, G., Xiang, W., Xu, G.: Adaptive fuzzy synchronization of fractional-order chaotic (hyperchaotic) systems with input saturation and unknown parameters. Complexity 2017, Article ID 6853826 (2017)

Liu, H., Pan, Y., Li, S., Chen, Y.: Adaptive fuzzy backstepping control of fractional-order nonlinear systems. IEEE Trans. Syst. Man Cybern. Syst. 47(8), 2209–2217 (2017)

Qin, X., Li, S., Liu, H.: Adaptive fuzzy synchronization of uncertain fractional-order chaotic systems with different structures and time-delays. Adv. Differ. Equ. 2019, 174 (2019)

Heydari, Z.R., Karimaghaee, P.: Adaptive fuzzy synchronization of uncertain fractional-order chaotic systems with different structures and time-delays. Adv. Differ. Equ. 2019, 498 (2019)

Zhang, S., Liu, H., Li, S.: Robust adaptive control for fractional-order chaotic systems with system uncertainties and external disturbances. Adv. Differ. Equ. 2018, 412 (2018)

Acknowledgements

The authors are grateful to referees for their careful reading, suggestion, and valuable comments which have improved the paper substantially.

Funding

The author Aceng Sambas was supported by Kementrian Riset dan Teknologi Republik Indonesia/Badan Riset dan Inovasi Nasional (KEMENRISTEKDIKTI-BRIN) through Project No. 2891/L4/PP/2019 (Penelitian Kerja Sama Antar Perguruan Tinggi). Shaobo He is funded by the National Natural Science Foundation of China (Grant No. 61901530) and the Natural Science Foundation of Hunan Province (No. 2020JJ5767). We also would like to thank Universiti Malaysia Terengganu for supporting this research publication and one form of research collaboration with Universitas Padjadjaran and Universitas Muhammadiyah Tasikmalaya.

Author information

Authors and Affiliations

Contributions

All the authors contributed to the writing of the present article. They also read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare that they have no competing interests.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Sukono, Sambas, A., He, S. et al. Dynamical analysis and adaptive fuzzy control for the fractional-order financial risk chaotic system. Adv Differ Equ 2020, 674 (2020). https://doi.org/10.1186/s13662-020-03131-9

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s13662-020-03131-9