Abstract

Our paper investigates how the heterogeneous structure of the middle class in sub-Saharan Africa influences its consumption of financial services, identifying drivers for their selection of these services. Implications for marketing practice are outlined. This research is an across-country city-based exploratory study in ten cities where structured questionnaires were used in interviews to obtain information from respondents over a period of 2 years. Our findings identify the importance of the financial realities of the three middle-class groups of the Accomplished, Comfortable and Vulnerable on their consumption of financial services and answer the question of what drives demand for these services. The three groups have varied spending and saving habits, perceptions of financial services and financial aspirations. We identify six key drivers for selecting services, namely availability, accessibility, affordability, status, security and trust. Technology is a key mediating variable of the marketing mix considerations. Marketing practice implications indicated a need for marketers to recognise the importance of the heterogeneity of the middle class and its influence on segmentation strategies. Opportunities for new approaches to new product development and marketing communication strategies that leverage the heterogeneity of the middle class are outlined. Marketers should also consider the varied influence of the drivers for the choice of financial services among the three groups. Our findings reinforce the need and potential that exist for financial services providers to improve the financial inclusion of previously marginalised consumers.

Similar content being viewed by others

Introduction

The last decade has witnessed significant global growth in middle-class households, making the group a key focus of research in multiple disciplines, such as international business, economics, and international marketing (Bhorat et al. 2021; Kharas 2017; Uner and Gungordu 2016). The middle class in emerging markets, such as China, India, Brazil and some markets in sub-Saharan Africa, has a combined global spending power estimated at more than US$35 trillion (World Bank 2019). The segment’s attractiveness is further reinforced by forecasted growth by the World Bank, which estimates the segment will grow as much as 25% by 2030. Central to this development and growth of spending power has been changed in this class’s consumption and attitudes towards financial services. Sub-Saharan Africa (SSA) has witnessed considerable shifts in the level of financial inclusion of groups such as the middle class, largely due to the rapid growth of mobile-telephone-payment-based services (Chikalipah 2017; Mothobi and Grzybowski 2017). The middle-class consumers in SSA have rising disposable incomes, which have empowered them to afford diverse products and services using emerging financial service innovations. They therefore represent viable and significant target segments for marketers (Kardes 2016; Cavusgil and Kardes 2013). However, although there are significant previous studies on financial inclusion and exclusion in SSA, there have not been many empirical studies that position this discussion in the context of the middle class. In particular, not much emphasis has been made on identifying the impact of the changing and emerging structure of the middle class on its consumption patterns and drivers for the selection of financial services.

The prevailing assumption of the middle class in SSA assumes the segment to be homogenous. Based on an empirical study in nine SSA countries, heterogeneity is increasingly being recorded in marketing and consumer behaviour literature (Lappeman et al. 2021; Chikweche et al. 2021). In this study, we use the model from Lappeman et al. (2021) to observe the financial behaviour three distinct middle class groups in SSA. This segmenting of the middle class has implications for understanding the decision-making process for selecting financial services. This paper addresses a gap in understanding of drivers of middle-class financial service consumption, by using a multi-country and multi-city-based investigation into the middle-class consumption of financial services. Our paper argues that marketers of financial services need to consider the practical implications of the heterogeneity of the middle class in SSA in their strategies. Treating the growing middle class as a homogenous group is likely to provide misleading business insights for marketers looking to provide financial services. Since so much of the focus of financial services research has been on financial inclusion in SSA, research for marketers in this growing sector has been sparse.

Consequently, our paper reinforces calls for a renewed focus on studying the consumption of financial services by the middle class by using a non-aggregate country-based analysis based on cities and towns in Africa (Cavusgil et al. 2018; Lappeman et al. 2021). This approach has the potential for providing more accurate insights into the consumption behaviour of financial services by the middle class in a changing environment, in which consumers now have increasing choices of financial service products (Kardes 2016). In summary, we examine factors that shape and influence their choice and consumption of financial service products and their potential implications for marketers. We also explore the question of what drives demand for financial services in Africa. In so doing, our paper aims to contribute to addressing knowledge gaps in perspectives of the consumption of financial services in SSA beyond the often published issues of financial inclusion and mobile-telephone-based payment systems.

Literature review

Middle class

To date, there is no nationally or globally accepted definition of the middle class, given the different contexts in which the middle-class lives (Bui and Wilkins 2017; Cavusgil et al. 2018; Uner and Gungordu 2016; Lustig 2016; Tschirley et al. 2015). A key weakness of previous literature has been on treating this group as a homogenous cluster of consumers based on common indicators (Bowman 2016; Kharas 2010, 2016; Birdsall 2007; Pressman 2010). Examples of common indicators used include income levels and expenditure patterns with distinct habits that are often associated with conspicuous consumption (Ravallion 2010; Kravets and Sandikci 2014). Both absolute and relative approximation approaches have been used to define the middle-class (Lustig 2016). Although the definition of the middle class is contested, there is some consensus on the need for a more comprehensive conceptualisation that takes into consideration the nuances and interpretation of the different contexts (Cavusgil and Guercini 2014; Uner and Gungordu 2016). This is a gap we partially address in our paper by classifying the middle class in SSA as a heterogeneous group of consumers with varied consumer behaviour. Income or consumption levels are the most common economic indicators used to measure the middle-class. Other scholars have used non-income-based approaches, such as education and wealth levels and sociological focus on ‘class’ (Pressman 2015). Table 1 provides a summary of various income parameters used by different authors who study the middle class across various disciplines.

Based on the various parameters outlined in Table 1, there are indications of potential problems with upper-end maximum bends and lower bends. The global middle class definition that uses an upper-end maximum bend of US$100 per day, for example, has the potential to diminish and ignore the growth of the middle class in regions such as SSA which has a far lower average income. Similar problems or weaknesses apply to industry-based classifications, which tend to use broad income categories like how Goldman Sachs defines the middle-income range as US$16 to US$82 daily and McKinsey uses a range of US$9 to US$77 daily.

A key attempt to define the middle class has been made by the African Development Bank, which uses a threshold gap of US$2 and US$20 per day (Ncube et al. 2011). However, this definition potentially exaggerates the size of the middle class, with the low US$2 bend of consumers and other strata of US$2–US$4 and US$4–US$10, who are more bottom-of-pyramid consumers than middle class. Different definitions argue from different points of departure, and some arguably do not fully recognise the emerging heterogeneity in the middle class. Despite the variations in using lower- and upper-income bends, a practice that is gaining acceptance and is supported by the World Bank is the use of a middle-income threshold of US$10 per day as the minimum bend that should be used to define middle-class.

Financial inclusion and emerging financial services platforms

The concept of financial inclusion faces similar contestation as that of the middle class in terms of having multiple definitions. There is no consensus over the definition of financial inclusion as differences emanate from the context wherein the term is used, the state of economic development and the geographical location of the area (Asuming et al. 2019; Chinoda and Kwenda 2019). Soumare et al. (2016) refer to financial inclusion as the creation of an enabling environment and developing innovative financial solutions to facilitate access to financial services to a bigger part of the population, by lifting the barriers. Others, such as Sarma (2008), define financial inclusion as a process of ensuring easy access to availability and usage of formal financial systems to all members of an economy. While at the other extreme, Amidžić et al. (2014) and Camara et al. (2014) define financial inclusion as the process of maximising access and usage while minimising involuntary financial exclusions. Therefore, they focus more on access, usage, and barriers, which capture both the demand and supply side of financial access.

The World Bank concurred with Sarma (2008) and defined an inclusive financial system as one that ensures easy access to or use of affordable financial services and products (transactions, credit, savings, payments, and insurance) that meets the necessities of businesses and individuals, conveyed in a responsible and viable manner. Chikalipah (2017) examined the determinants of financial inclusion in SSA, focussing on the vulnerable bottom-of-pyramid (BOP) consumers. In SSA, prior to the mobile phone fintech revolution, consumers faced common barriers to accessing formal financial services, such as a lack of innovative financial solutions, high costs of services and a lack of information on these services (Gosavi 2018). Asuming et al. (2019) examined key trends and determinants of financial inclusion in SSA with a focus on why financial inclusion remained low among vulnerable consumers. While these challenges are predominantly faced by BOP consumers, they shaped the overarching environment in which marketers deliver financial services.

The rapid adoption of mobile phones and their role in facilitating mobile-platform-based payments has been one of the biggest game-changers in enhancing financial inclusion in SSA (Abor et al. 2018; Asuming et al. 2019; Liébana-Cabanillas et al. 2015; Kanobe et al. 2017; GSMA 2016; Gosavi 2018). In SSA, mobile phone-based payments originated in Kenya in early 2007 to help urban migrant workers send money back home to their families who reside in rural areas (Hughes and Lonie 2007). The region now commands close to 53% of active global mobile-payment services, due to the huge investment in mobile-telephone infrastructure across the region (PWC 2016; GSMA 2016). The mobile platforms have also created a firm foundation for new diversified financial services innovation (like internet banking and different forms of insurance) that are offered by mainstream providers such as banks (PWC 2016). However, to date, not many studies have investigated middle-class adoption and use of these financial innovations. The focus of previous studies has been on examining limited aspects of consumer behavioural intentions on an individual country basis, primarily focussing on vulnerable bottom-of-pyramid consumers (Chikweche and Fletcher 2014ab). The predominant focus on the BOP misses an opportunity to examine the growing middle class with its increased capacity to consume the different emerging financial services (Narteh et al. 2017).

The growth in the use of mobile payments in SSA has filled a key gap of access and the provision of financial services by the unbanked consumer majority, and a key facet of this challenge has been the role of trust by these consumers in adopting new mobile-related financial innovations (Mothobi and Grzybowski 2017; Xin et al. 2015; Chandra et al. 2010; Bongomin et al. 2018). These studies outline the moderating role of social networks on financial inclusion in SSA, but too often assume homogeneity of a vulnerable group of consumers.

Revisiting the middle-class definition in Africa: our approach

The definition of the middle class after the ADB’s estimates of close to 500 million by 2030 was disputed and has complicated the quantification of the middle class in Africa. A report on the global middle class by Ernst and Young estimated the middle class in SSA to be over 82 million and is forecast to be 107 million by 2030 (Ernst and Young 2013). However, studies by Standard Bank (a South African bank with operations across the region) estimate that the African middle class has tripled in size over the past 14 years (Africa Research Online 2014). Future growth prospects indicate the segment is forecast to grow over the next 15 years, with an estimated extra 25 million households expected to become middle class (Ernst and Young 2013). Part of the challenge in quantifying the segment is the lack of reliable, city-specific, contextually relevant data which profile the African middle class. The segment is regarded as a potential driver of the region’s economic and social development. Research on the middle class in Africa has largely been in the social sciences (Iqani 20152017; Mashaba and Wiese 2016). Further justification of the segment comes from the World Bank’s forecasts, which highlight opportunities for the African middle class from the digital revolution. This has seen increased demand for and support for digital transformation in the provision of financial services through the fintech movement (World Bank 2019).

A key point of difference in our paper, indicated earlier, is the use of a segmented approach to the middle class, as opposed to the more common approach of viewing the group as homogenous. Approaching the financial services behaviour of the middle class through a three segment theoretical framework (Chikweche et al. 2021) forms the basis of our paper as illustrated in Fig. 1. We then adapted Kardes (2016) and Cavusgil et al. (2018), who used a more granular approach of using urban clusters samples. This approach provided a better likelihood of identifying insights into the SSA middle class.

Three middle class segment approach (adapted from Chikweche et al. 2021)

The Accomplished make up 19% of the middle class. They have an average household income of US$19 per day, are largely financially secure and have greater optimism about the future than other segments. The group is more positive about managing the macro-environmental challenges common in SSA, which can impact their livelihoods. They have diverse sources of income, invest in education as a foundation for a better life and, among the three groups, consume the widest range of financial services. The Comfortable make up 26% of the middle class, this is the largest group. It has an average household income per day of just over US$16. The group is also optimistic about the future, although its members use credit as a key basis for up keeping their middle-class status. Their knowledge and use of financial services is not as comprehensive as that of the Accomplished. The Vulnerable is the smallest group of the middle class, making up 15%. It has an average household income per day of US$15.70. The group is the most vulnerable of the middle class and is conscious of the potential to slip out of the middle class if macro-environmental forces change. Their knowledge and use of financial services are not as comprehensive as the other two groups. While the average income difference between the Comfortable and Vulnerable is relatively small, Chikweche et al. (2021) identified a number of behavioural differences such as the Vulnerable being more likely to incur debts to pay for education, clothing, food and their own businesses.

Methodology

The investigation was an exploratory one, which covered ten cities spread across major SSA countries that have experienced population and economic growth over 2 years. A total of 8412 interviews were conducted across the ten cities, which included Accra (Ghana), Addis Ababa (Ethiopia), Douala (Cameroon), Dar es Salaam (Tanzania), Abidjan (Ivory Coast), Kano (Nigeria), Lagos (Nigeria), Luanda (Angola), Lusaka (Zambia) and Nairobi (Kenya) (Chikweche et al. 2021; Lappeman et al. 2021). Structured questionnaires were used to obtain information from respondents. Computer-assisted personal interviews (Malhotra 2010) were administered using a team of 150 fieldworkers sourced through research agency Ipsos. The distribution of the samples is outlined in Table 2.

Using random probability sampling, three starting points were identified per sub-area in the urban areas and four interviews were conducted per starting point for between one and one and a half hours. The data collection method used conforms to those used by other researchers who have conducted research on the middle class in emerging markets (Kravets and Sandikci 2014; Jaiswal and Gupta 2015). As indicated in earlier sections, our focus on urban samples is in line with previous calls for a more focussed granular approach of analysing the middle class, advocated by Kardes (2016) and later reinforced by Cavusgil et al. (2018). This approach has been proven to have a better basis for identifying insights on the middle class, as it considers the diversity that is fostered by nuanced variables that impact the group in its heterogeneity. This heterogeneity can take various forms, among which are ethnicity, language, infrastructure such as mobile phone networks, and other financial service enablers (technology). This more robust methodology has the potential implication of enhancing our understanding of how the middle class in SSA engages with financial services, noting how this might vary among cities within a country. A further rationale for this approach is its potential for minimising methodological nationalism. This refers to over-dependence or a limited focus on the nation state as the only unit of analysis for social research (Wimme and Schiller 2002).

A data analysis protocol was developed to examine the meaning of text utilising condensation, categorisation, narration and interpretation. The data were cleaned and coded using SPSS software. A k-means clustering approach was used to identify the emerging segments from the data as per Wolff et al. (2020) and Mittelmeier et al. (2019). In the analysis, a two-stage clustering approach was used to determine the appropriate number of clusters (using hierarchical analysis). This was then followed by a k-means cluster analysis to segment the data into the number of emerging middle class income groups as described in Chikweche et al. (2021). Multiple cluster options were then reviewed in terms of individual income and variables like financial outlook, aspirations, financial situation, living standards, debt, financial support, money for emergencies, accommodation type, employment, and expenditure. Discriminate analysis was then conducted to confirm group membership results of the k-means clustering. Each cluster was then named (Fig. 1). This was complemented with comparisons with the existing literature, although it is limited.

Findings

Middle-class financial reality

Meeting our objective of examining the consumption behaviour of financial services by the middle class in a changing environment, our findings identified the emerging core factors that shape and influence their choice and consumption of financial service products. Our findings indicate that heterogeneous middle-class consumers’ consumption of financial services is centred around the group’s ‘financial reality’. This is examined below by exploring key sources of income, spending and saving habits, perceptions of financial services and overall aspirations of the middle class. While the nuance between counties is not easily generalisable, some of the nuance between each middle-class segment is explained and visually represents.

-

(1)

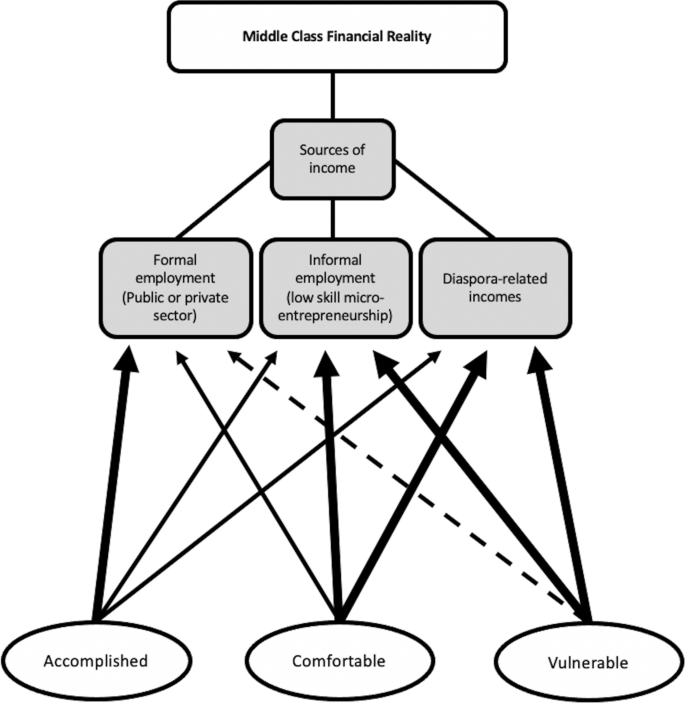

Sources of income

The financial reality of the middle class was predominantly determined by their sources of income, which in turn influenced their behavioural traits regarding financial services. Across all three segments, households often had more than one income earner and each individuals income could have various sources. While the Accomplished group had more disposable income (followed by the Comfortable and then the Vulnerable), they were also most likely to gain their income from formal employment (45%). Formal employment was either from the higher echelons of the civil service or in the private sector. Some were also likely to engage in entrepreneurial activities (27%). The Comfortable and Vulnerable (31% and 35%) had a higher participation in self-employment entrepreneurial activities and relied on diaspora-related income from relatives living overseas.

The sophistication of self-employment activities varied among the three groups. The Accomplished, for example, engaged in more structured service and trade-oriented self-employment activities to leverage their education or training. In comparison, the Vulnerable were likely to engage in what could be termed hustling and the trading of goods, which did not require higher levels of training. Of the ten cities, Luanda, Doula and Nairobi had the highest levels of income across all three segments. Hustling for extra income was more common in Lusaka, Dar es Salaam and Addis Ababa, and this was most common among the Vulnerable group and to some extent the Comfortable. A few members of the Accomplished group in cities such as Doula and Luanda had access to rental income. By virtue of being more active in formal employment, the majority of the Accomplished received more income on a monthly basis from their salaries compared to the Vulnerable and the Comfortable (who often earned inconsistent daily wages/income). This cycle of income payment has implications on how they planned and budgeted their income and the nature of financial services they used. Figure 2 summarises some of the segment differences in sources of income.

Fig. 2

Key sources of income per segment

-

(2)

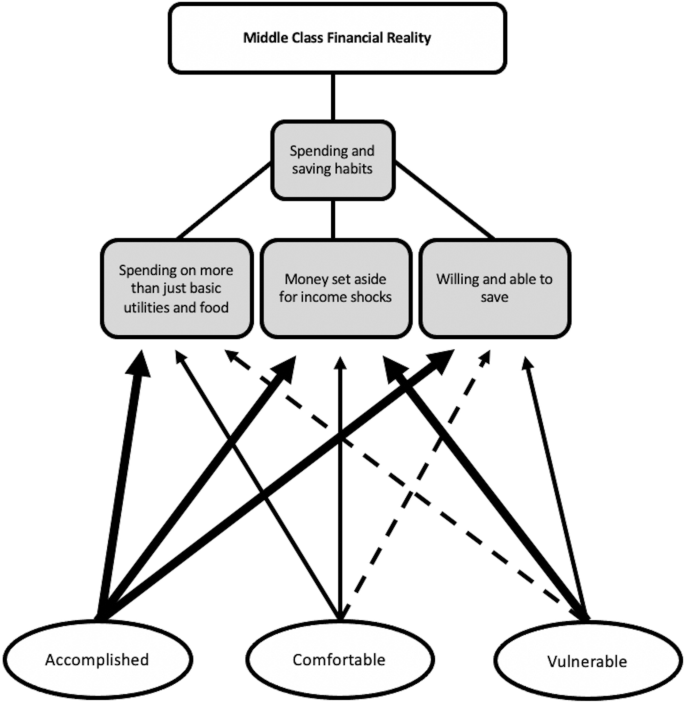

Spending and Saving Habits

Spending and saving habits varied across the three groups and were shaped by the timing and frequency of income as outlined earlier. The Vulnerable prioritised basic foodstuffs, housing, accommodation and utilities. The Accomplished were more likely to spread their expenditure across various expenses above basic needs. These expenses include more regular spending on clothing, personal effects and entertainment. The Comfortable had similar patterns but with less total expenditure on these items. Levels of disposable income also influenced the saving culture of the three groups, which is important in the context of understanding the middle class’s demand for financial services. The vast majority had unexpected expenses at least once a year. The majority of the Accomplished (75%) set money aside for these unforeseen emergencies, compared to 59% for the Comfortable. An interesting observation is that the Vulnerable (66%) were more inclined towards saving for emergencies than the Comfortable. This is partially attributed to the group’s higher levels of caution and income insecurity due to self-employment.

Similar patterns were observed with regard to saving. 30% of the Comfortable often had money left at the end of the month (compared to 36% of the Vulnerable). An important finding relevant to understanding the heterogeneity of the middle class was attitudes towards saving. Both the Accomplished and Comfortable have a significantly higher percentages of members who are likely to set aside money for savings after expenses (67% and 66%), while less of the Vulnerable (60%) would save on a monthly basis. Opportunities exist for marketers of financial services to develop segmented products to meet the needs of these groups. Savings are also sometimes a key source of additional income, along with money received from friends and family. In addition, this evidence of robust saving is crucial to the building up of creditworthiness and bodes well for the future financial market within the African middle class. The spending and savings findings are represented in Fig. 3.

Fig. 3

Spending and savings observations per segment

-

(3)

Perceptions of Financial Services

Although there is evidence of a positive attitude towards saving, as reflected in the generally high numbers of the middle class who set aside extra money for savings after expenses, there is a variation in the perceptions these groups have of financial services. The Accomplished, in particular, were most likely to have had improved access to financial services in recent decades. The Accomplished in Addis Ababa, Luanda, and Dar es Salaam had a particularly robust and positive perception of the various formats of financial services that were emerging in their markets, which embraced the integration of technology. In the Comfortable group, the formally employed members had similar positive perceptions about financial services, although their interactions were not as extensive as those of the Accomplished.

By virtue of their often-limited interactions with diverse financial services, the Vulnerable were likely to have less robust perceptions of financial services. The limited interaction was closely tied to their limited knowledge and confidence in financial services and the feeling that, as a group, they were not targeted by financial services providers.

The Accomplished are the least indebted among the middle-class segments, and significantly so compared to the norm. They are also the least likely to feel trapped by debt. The Comfortable were the most indebted, while the Vulnerable were more cautious about their level of debt, which was also affected by their perception of not being a core target of financial services providers. This was often confirmed by the difficulties this group faced to access financial products when collateral and a credit history were required. Other perceptions for this group related to how they preferred to avoid using credit because they did not understand how credit worked, which could be indicative of a lack of financial literacy initiatives by financial services providers.

-

(4)

Financial Stability and Aspirations

The general view held by all three groups was that living standards and financial situations had improved and were likely to continue to improve in future. The Accomplished were more assured of their financial stability and ability to sustain their middle-class status, largely based on the security of their jobs and investment in education, which provided them with more career options. The Comfortable also had a higher level of assurance and optimism about their future financial stability, although those in the self-employed category were not as optimistic. The Vulnerable group was the least optimistic of the three and this was reflected in their approach to handling their finances and use of financial services. Compared to other cities, the middle class in Addis Ababa, Luanda, and Dar es Salaam were more optimistic and confident about their capacity to meet their needs without much financial stress. Setting up business ventures was identified as a key mechanism for ensuring financial stability, especially by the Vulnerable group and self-employed members of the other two groups. This sentiment was particularly strong in Addis Ababa, Luanda, Dar es Salaam and Nairobi. A summary of the final two financial realities is found in Fig. 4.

Perceptions of financial services, financial stability and aspirations per segment

Drivers of demand for financial services

The three groups used a variety of financial services, but extant literature has thus failed to adequately explore the drivers of demand for such services in a comprehensive way. In this study, we observed that savings accounts were the most often used financial service, followed by debit accounts and electronic money (examples being eWallet and Mpesa). In terms of the product life cycle, the Accomplished are mature consumers; the Comfortable are in the growth phase and the Vulnerable are in the development and introduction phase. This is reflected in the level of sophistication of financial services accessed by each group. The Accomplished were likely to place more value in having a relatively diverse portfolio of financial services inclusive of insurance products, such as medical insurance or investment-related products at entry level. This also extended to internet banking-related solutions being introduced by banks. With the Comfortable group, smaller numbers (usually within the formally employed) showed similar consumption patterns as the Accomplished. Otherwise, as a growth group, the Comfortable were still accessing the entry-level financial services primarily provided by banks and were also reliant on emerging mobile-driven financial products. In contrast to the Vulnerable, they accessed more sophisticated and aspirational financial services such as medical insurance, but they did not have a strong understanding of investment products. The Vulnerable were at the development or introduction stages of consuming mainstream financial products provided by banks, but they were trendsetters in the growing financial services area of mobile banking. Across all ten cities, the financial services sector is growing, which has allowed previously unbanked consumers to now access some form of banking service through their mobile phones.

Debt and demand for financial services were interlinked with the majority of the Accomplished (81%) not having loans or debts to pay off. As they did not generally feel trapped by levels of debt, this segment felt more freedom to make use of various financial services (more so than the other segments). When the Comfortable do need credit, they are more likely to get it from a formal source like a bank as opposed to informal lending. The Comfortable also maintain low levels of indebtedness (12%). In contrast, about 30% of the Vulnerable had debt or loans to pay. Most of this debt was informal lending from friends and family and other small social network-driven financial formats, such as community savings clubs.

In order to examine the behaviour and attitude of middle-class consumers of financial services, it is important to identify the drivers that were considered by the groups in selecting financial services, noting variations in the levels of importance considered by the three groups. These are outlined in Fig. 5 and explained as follows.

Drivers of financial services selection in sub-Saharan Africa

-

(1)

Availability

This driver referred to the availability of the various financial products that meet the needs of the middle-class groups. The importance of this varied among the groups. The Accomplished placed more value in the availability of traditional formal channels of distribution of financial services, such as different formations of banks and insurance companies that offered a variety of products (for example, medical or funeral insurance). For the Comfortable, availability considerations were also similar to the Accomplished but extended to mobile-payment-based services, since this was a channel used by the self-employed. Those in the group with some level of sophistication made similar considerations as the Accomplished but for a limited product portfolio. The Vulnerable’s key driver for availability was predominantly savings account-driven providers, such as savings clubs and low-interest banking products. Mobile-payment-based services availability was by far the dominant concern for this group, since this had opened up avenues for financial inclusion. The convenience of using services was also cited as a key component of availability but this differed among the groups. The Vulnerable assessed the convenience of using mobile-telephone-related financial products as a major aspect of availability. The Accomplished considered convenience from the aspect of availability of internet banking to access their accounts, while the Comfortable still regarded brick-and-mortar financial services as a key requirement.

-

(2)

Accessibility.

Respondents in all three groups indicated that, although financial services were available, this did not translate to them being accessible. Thus, accessibility became a key driver for considering the adoption of these services. This was particularly evident with the Comfortable and Vulnerable groups, which were at different levels of sophistication in terms of understanding the forms of financial services that were predominantly used by the Accomplished. The requirement for collateral limited these two groups’ access to products such as mortgages. Although all three groups were using savings accounts as entry products for banking, the processes that members of each group went through to access the products differed. The majority of the Accomplished and some members of the Comfortable could use their payslips to access financial services such as debit cards and medical insurance. The situation was different for the majority of the Comfortable and the Vulnerable group, who did not have payslips and credit histories thereby disadvantaging them from accessing loans because of the bias for formal forms of income and credit such as payslips and credit histories. Although these groups (majority of the Comfortable and Vulnerable group) applauded the emergence of new forms of financial services, they remained concerned about the difficulties of accessing these products and the lack of information on the products due the bias by financial institutions for formal forms of evidence of income source and savings mentioned above.

-

(3)

Affordability

There were different levels of consideration on the affordability of financial services which the heterogeneous middle class could access. This was closely linked to the groups’ needs and experience with financial services. The Accomplished indicated that affordability was key in their choice of products such as medical, funeral and life insurance because there was a great variety of these products on offer. Thus, their decision-making process when selecting these products involved more detailed comparisons than applicable to products such as savings accounts or personal loans. For the Comfortable, affordability concerns were the key in determining whether in fact they purchased financial products, such as medical, life and funeral insurance, since these were bound to exert some financial pressure on their incomes. Although they saw the need for these products (unlike the Accomplished), they were not necessarily at the top of the list of services to be purchased. Their decision-making process for these products was longer and more comprehensive than that of the Accomplished. Coming from a relatively disadvantaged position in which they had limited access to financial products, the Vulnerable group saw the affordability of any financial services as of paramount importance. Subscription fees, interest rates, and late payment penalties were all material to their decision-making processes, because of their limited resources.

-

(4)

Security

Considerations of the level of security of financial services products were a key driver among the three groups. The Accomplished were at a stage at which internet banking was still relatively new and concerns about the security of this product were raised as key drivers for selecting a service. In terms of the uptake, the Accomplished was the group most likely to use this service instead of mainstream banking services. The Comfortable and Vulnerable had similar concerns around the security of their money and details, although they were unlikely to sign up for the service. The Vulnerable did not share the same level of concern with the mobile-payment services which they predominantly used and were in so many ways integrated with online banking. However, the difference cited was the differences in accessibility between internet banking by banks and mobile-payment services. Mobile phones had become basic tools that were part of their day-to-day lives where there were no restrictions in terms of access. Over time, this built confidence to use them even for financial transactions. Notwithstanding the above, consumers still examined the security features of the different mobile operators who offered financial service platforms.

-

(5)

Status

Attainment and maintenance of middle-class status were highlighted as a key driver of financial services adoption. This was particularly important for financial services because the products that one consumed were indicative of one’s middle-class status, although the triggers for this differed among the three groups. The Accomplished had a selection of financial services, such as investment products and medical insurance. This was an important point of differentiation from the rest of the middle class. Thus, the status that is associated with specific services and brands was an important driver of their decision-making processes. This was also reflected by the Comfortable group, who had aspirations to graduate to the consumption habits of the Accomplished. Therefore, they would consider adopting financial innovations that reflect their acceleration up the social-class ladder. For the Vulnerable group, maintaining middle-class status was a continuous preoccupation, since they were on the borderline. Thus, they were conscious of their vulnerability to losing middle-class status, which in turn motivated them to demonstrate their status through the consumption of financial services.

-

(6)

Trust

The role of trust and its antecedents summed up considerations that members made as part of the process of their intention to adopt new financial service innovations. Members of the Vulnerable group who used savings groups and other forms of social network-driven financial providers considered references from family and friends as a basis for examining the trustworthiness of the provider. This was also evident with both the Accomplished and Comfortable when it came to the adoption of new services such as investment products or medical insurance. Testimonials and word-of-mouth referrals were more important than professional financial planners’ advice. Previous history and experience with the products were important in determining the level of risk that was associated with the decision-making process.

Influence of integrated technology and media

A key trend in all ten cities that made up the sample was the increased use of integrated technology platforms in various aspects of not just the middle class but the whole population. The introduction of mobile phone services has been central in enhancing access to technology through the adoption of various mobile phone-based payment services. In all ten cities, there was evidence of increased access and use of the Internet by the middle class. The Accomplished and part of the Comfortable owned satellite dishes through DSTV/MultiChoice, which has become a regional media entertainment group. The Vulnerable also accessed low-end cheaper satellite services, such as GoTV. Subscription to satellite services was a form of confirmation of one’s middle-class status, although there were variations in the services accessed. Technology was important in facilitating access and the consumption of financial services, as evident in discussions in earlier sections. Across all groups, technology-facilitated communication using various forms of social media, such as Facebook, WhatsApp and, in some cases, local social media platforms were being introduced, targeting the middle class, for example, Sasai. The Accomplished were generally the highest users of Internet services, using a variety of products, such as laptops, tablets and mobile phones.

Discussion

Our paper has developed a framework for examining SSA middle-class consumption behaviour regarding financial services, which considers their financial realities. Figure 6 provides an integrated model summarising the core findings and pointing towards the need for context-based financial services. The framework was derived from the need to integrate a segmented middle class financial reality with the drivers of financial service demand. This context-based perspective on financial services in SSA provides a key point of departure for our study. In part, this supports previous assertions by Kardes (2016) and Cavusgil et al. (2018) who advocated a granular approach of studying the middle class using urban clusters. However, they did not extend this to developing heterogeneous segments, as we do. In so doing, we have been able to examine and demonstrate the implications of consumption behaviour and choices of financial services across the three groups that we identified.

Summary of core findings

A further point of departure of our paper has been positing the discussion on the general challenges of financial inclusion within the domain of the middle class in SSA. The majority of previous studies (Asuming et al. 2019; Tchana and Kengne 2016) in this discussion focussed on the context of a general reference to developing countries. This misses the potential nuances that relate to the middle class, which is an important income-resourced group but which is not necessarily maximising the use of financial services. Our findings are centred on the practical financial realities of the heterogeneous middle class. By outlining a framework that maps drivers for selecting financial services by the heterogeneous middle class, we have been able to articulate the varying levels of importance attributed to these drivers by the three groups. This is different to findings from previous studies that treat the middle class as one homogenous group, thereby generalising the importance of these drivers across the whole segment. While recognising the importance of trust in financial service providers, as outlined by others, such as Xin et al. (2015) and Chikalipah (2017), our study further outlines its varied importance for the three groups and the related products chosen by the groups.

Our framework also makes an important distinction between the three As (availability, affordability and accessibility), which provides a different nuanced perspective on financial inclusion parameters. Previous studies (Amidzic et al. 2014; Abor et al. 2018) recognised some of these variables independently in their discussions of financial exclusion in developing countries. By positing our investigation on the middle class, we have identified gaps and opportunities that exist for financial service providers to accelerate their contributions to financial inclusion in SSA. This is a region that is commonly cited for lacking the financial inclusion of its citizenry. Our findings also reinforce previous findings on the role of mobile-telephone-driven financial platforms in enhancing financial inclusion. However, we go beyond the generalised findings to articulate the different interactions the three middle-class groups have with these platforms. We then cite the resultant implications this has on their consumption of financial services, which reflect each group’s nuances and concerns.

Findings from our study on the behaviour of middle-class consumers in the three groups indicate some divergence from classic theories of consumption, such as Friedman (1957) and Modigliani and Brumberg (1954). These posited that consumers’ spending is driven by anticipated income that is available over a lifetime, thereby negating consumers’ contextual nuances, such as those evident for the three groups in our study. There is evidence of different perceptions of financial stability, financial services used and drivers of selecting services, which was not necessarily influenced by their forecasted or desired future income. Further insights from our study also challenge assertions by Chao and Lyons (2013) and Fornell et al. (2010) of middle-class consumer behaviour of over-indulgence and living beyond one’s means using credit, which is common among middle classes in advanced economies. In SSA’s case, there are distinct patterns of a savings culture among the three groups, with variations in motivation for saving. Our insights on the middle class’s interaction with technology in their consumption of financial services, especially in the context of mobile payments, add to the growing body of literature in this area (Gosavi 2018; Humbani and Wiese 2018).

Implications

Segmentation

Our study has demonstrated how the middle class in SSA is heterogeneous, as evident from the three groups that we identify. This has implications on how financial services providers can revisit their segmentation strategies that recognise the implications of this heterogeneity. As opposed to serving the middle class as one big homogenous group, it is evident that there is scope to divide the segment into three distinct target micro-segments. We then demonstrated how these segments engage in different consumption patterns and have different attitudes to financial services. By revisiting their segmentation approach, providers will be able to tailor-make their services to the distinct groups and, additionally, this will improve their evaluations of their marketing campaigns.

New product development

Our study identified various consumer behaviour traits, in particular regarding the type of financial services and perceptions of these services by the different middle-class groups. From a marketing perspective, the findings provide insights into potential opportunities for the development of products that are responsive to the nuances of the various middle classes. Opportunities for involving middle-class consumers in co-creating products could be useful in addressing some of the concerns reflected in perceptions about security. Social network groups could be engaged in co-creating products, especially for the Vulnerable group, which relies most on these groups as reference points for product selection. Product mix extensions of services such as medical insurance could find traction across the different groups but should be structured to accommodate each group’s needs and capacity. The high rate of ownership of savings accounts indicates traction with banking products but there are a variety of inhibitors to the full adoption of other banking products, which providers could develop considering each group’s nuance. Part of this process could involve an acceleration of establishing partnerships with providers of other complementary financial service products, such as insurance companies and, where possible, mobile phone operators. Although mobile phone operators are indirectly disrupting mainstream financial institutions, such as banks, they have regulatory limitations on the type and depths of products they can offer. Therein lies an opportunity for these institutions to co-create products and co-brand.

Marketing communications strategies

A lack of awareness and knowledge about the financial services available to the middle class in SSA is evident from the perceptions of the different groups. Financial service providers need to revisit their communication strategies for the middle class by moving away from a generic, homogenous approach to one that recognises intra-group heterogeneity. This will be important in identifying specific communication gaps and needs for each group. The Vulnerable could do with more communication aimed at product awareness, which also addresses their fears and uncertainties about some financial products. Brand-loyalty and product-trial focussed communication could be useful for the Accomplished and some of the Comfortable group. Opportunities to leverage potential partnerships with mobile phone operators and social network groups should also be explored in expanding the reach of marketing communications. This could be structured around complementing word-of-mouth communication, which is popular across the three groups. Reinforcing the use of local brand ambassadors who are recognised in the different groups should also be accelerated to enhance brand association.

Social implications

The SSA region is commonly associated with markets in which financial inclusion has been identified as a major concern in as far consumers are excluded from accessing financial services. Our findings highlight the potential that exists for financial services providers to improve the problem of financial inclusion. This could be by having targeted but context-relevant strategies of developing new products for the middle class. In our case, this could be done by identifying the middle-class groups in these markets, noting their concerns about financial services, availability, accessibility and the affordability of these services. Financial institutions can draw on these intra-group insights to address these concerns by developing a responsible framework for serving these groups. This should go beyond the scope of new product development and include a contribution to the development of policies that can safeguard some of these consumers who are in vulnerable positions. Financial service providers should see themselves as key players in a big ecosystem of multiple players, such as the consumers, social network groups, governments and mobile phone operators. Their roles in this ecosystem are central to the efficient and responsible manner in which financial inclusion can be achieved, leveraging the nuances of the environment in SSA. Security concerns were highlighted as a concern across all groups but more prominently with the Vulnerable. There is scope for financial services marketers to ensure they engage with this group responsibly, properly informing them of the security features of the services they provide.

Future research direction and limitations

A key potential area for future research is studies of the current marketing strategies used by financial services marketers in SSA, examining how these are aligned to the three groups. The generalisability of the findings could be extended by expanding the sample to include cities in advanced African economies, such as South Africa, Morocco and Egypt, which are likely to have a more advanced middle class. Social and cultural conditions that influence people’s decisions regarding financial services is another important area for consideration based on the heterogeneity explored in this research. A deeper exploration of socio-cultural influences at a tribal, country level and regional level will further enrich the current literature on SSA. In particular, research should continue to steer towards acknowledgement of the differences in race, religion and culture as these all impact on attitudes and perceptions towards personal finances. As definitions of middle class move beyond purely socio-economic factors and are able to introduce a stronger geo-political perspective, the homogenous picture of the African middle class will persist. Part of the problem with the prior definitions of the middle class in SSA is their failure to keep up with the economic and social changes taking place in the region, thereby not reflecting changes in income levels and consumption behaviour. The changes in mobile-telephone technology, for example, are likely to influence the types of products that financial services marketers develop. There is a constant need to examine these and other consumption-related variables to prevent homogenising the middle class in Africa based on outdated assumptions.

References

Abor, J.Y., M. Amidu, and H. Issahaku. 2018. Mobile telephony, financial inclusion and inclusive growth. Journal of African Business 19 (3): 430–453.

Africa Research Online. 2014. Measuring Africa’s middle class, 15 September 2014. https://africaresearchonline.wordpress.com/2014/09/15/measuring-africas-middle-class/.

Amidzic, G., A. Massara, and A. Mialou. 2014. Assessing countries financial inclusion standing—A new composite index IMF Working Paper WP/14/36.

Asuming, P.O., L.G. Osei-Agyei, and J.I. Mohammed. 2019. Financial inclusion in Sub-Saharan Africa: Recent trends and determinants. Journal of African Business 20 (1): 12–134.

Banerjee, A.V., and E. Duflo. 2008. What is middle class about the middle classes around the world?. Journal of Economic Perspectives 22 (2): 3–28.

Birdsall, N. 2007. Reflections on the macroeconomic foundations of inclusive middle-class growth, center for global development, Working paper 130, Washington DC, October.

Birdsall, N. 2010. The (Indispensable) Middle Class in Developing Countries; or, The Rich and the Rest, Not the poor and the Rest. Center for Global Development Working Papers 207.

Bhorat, H., M.E. Kimani, J. Lappeman, and P. Egan. 2021. Characterisation, definition, and measurement issues of the middle class in sub-Saharan Africa, Development Southern Africa.

Bongomin, G., J. Ntayi, J. Munene, and C. Malinga. 2018. Mobile money and financial inclusion in Sub-Saharan Africa: The moderating role of social networks. Journal of African Business 19 (3): 361–384.

Bowman, S.W. 2016. Who and what you know: Social and human capital in black middle-class economic decision-making. Race and Social Problems 8 (1): 93–102.

Bui, H.T., and H.C. Wilkins. 2017. Young Asians’ imagination of social distinction. Journal of Vacation Marketing 23 (2): 99–113.

Camara, N., X. Pena, and D. Tuesta. 2014. Factors that matter for financial inclusion: Evidence from Peru, No. 1409.

Cavusgil, S.T., S. Deligonul, I. Kardes, and E. Cavusgil. 2018. Middle-class consumers in emerging markets: Conceptualization, propositions, and implications for international marketers. Journal of International Marketing 26 (3): 94–108.

Cavusgil, S.T., and S. Guercini. 2014. Trends in middle class as a driver for strategic marketing. Mercati e Competitiva 3: 7–10.

Cavusgil, S.T. and I. Kardes. 2013. GSU-CIBER middle class scorecard: Quantifying the rise of the middle class in emerging markets, paper presented at Middle Class Phenomenon in Emerging Markets Conference, Atlanta (September 26–28).

Chandra, S., S.C. Srivastava, and Y.L. Theng. 2010. Evaluating the role of trust in consumer adoption of mobile payment systems: An empirical analysis. Communications of the Association for Information Systems 27 (1): 561–588.

Chao, L., and J. Lyons. 2013. Bill comes due for Brazil’s middle class, The Wall Street Journal (October 9), A1–A12.

Chikalipah, S. 2017. What determines financial inclusion in Sub-Saharan Africa? African Journal of Economic and Management Studies 8 (1): 8–18.

Chikweche, T., and R. Fletcher. 2014a. Marketing to the middle of the pyramid in emerging markets using a social network perspective: Evidence from Africa. International Journal of Emerging Markets 9 (3): 400–423.

Chikweche, T., and R. Fletcher. 2014b. Rise of the middle of the pyramid in Africa: Theoretical and practical realities for understanding middle class consumer purchase decision making. Journal of Consumer Marketing 31 (1): 27–38.

Chikweche, T., J. Lappeman, and P. Egan. 2021. Revisiting middle-class consumers in Africa: A cross-country city-based investigation outlining implications for international marketers. Journal of International Marketing. 29 (4): 79–94.

Chinoda, T., and F. Kwenda. 2019. Do mobile phones, economic growth, bank competition and stability matter for financial inclusion in Africa? Cogent Economics & Finance 7 (1): 1622180.

Court, D., and L. Narasimhan. 2010. Capturing the world’ emerging middle-class. McKinsey Quartely 3 : 12–17.

Ernst and Young. 2013. Hitting the sweet spot: The growth of the middle class in emerging markets, report. http://www.ey.com/Publication/vwLUAssets/Hitting_the_sweet_spot/%24FILE/Hitting_the_sweet_spot.pdf.

Ferreira, F., J. Messina, J. Rigolini, L.F. Lopez-Calva, M.A. Lugo, and R. Vakis. 2012. Economic mobility and the Latin American middle-class, The World Bank, Washington.

Fornell, C., R. Rust, and M. Dekimpe. 2010. The effect of customer satisfaction on consumer spending growth. Journal of Marketing Research 47 (1): 28–35.

Friedman, M. 1957. A theory of the consumption function. Princeton, NJ: Princeton University Press.

Gosavi, A. 2018. Can mobile money help firms mitigate the problem of access to finance in Eastern sub-Saharan Africa? Journal of African Business 19 (3): 343–360.

GSMA. 2016. The mobile economy Africa 2016. London, UK.

Hughes, N., and S. Lonie. 2007. M-PESA: Mobile money for the ‘unbanked’ turning cellphones into 24-hour tellers in Kenya. Innovations: Technology Governance, Globalization 2 (1–2): 63–81.

Humbani, M., and M. Wiese. 2018. A cashless society for all: Determining consumers’ readiness to adopt mobile payment services. Journal of African Business 19 (3): 409–429.

International Labour Organization 2013. Global employment trends 2013: Recovering from a second jobs dip. International Labour Organization. Geneva, Switzerland.

Iqani, M. 2015. Agency and affordability: Being black and ‘middle class’ in South Africa in 1989. Critical Arts 29 (2): 126–145.

Iqani, M. 2017. A new class for a new South Africa? The discursive construction of the ‘black middle class’ in post-apartheid media. Journal of Consumer Culture 17 (1): 105–121.

Kanobe, F., P.M. Alexander, and K.J. Bwalya. 2017. Policies, regulations and procedures and their effects on mobile money systems in Uganda. The Electronic Journal of Information Systems in Developing Countries 83 (1): 1–15.

Kardes, I. 2016. Reaching middle class consumers in emerging markets: Unlocking market potential through urban-based analysis. International Business Review 25 (3): 703–710.

Kharas, H. 2010. The emerging middle class in developing countries, working paper no. 285. Paris: OECD Development Centre Paris.

Kharas, H. 2016. How a Growing Global Middle Class Could Save the World’s Economy. Trend Magazine (Summer), http://trend.pewtrusts.org/en/archive/trend-summer-2016/how-a-growing-middle-class-could-save-the-worlds-economy.

Kharas, H. 2017. The unprecedented expansion of the global middle class: An update. Global Economy & Development, working paper no. 100, February.

Kochhar, R. 2017. A global middle-class is more promise than reality: From 2001 to 2011, nearly 700 million step out of poverty, but most only barely, Pew Research Center report (July).

Kravets, O., and O. Sandikci. 2014. Competently ordinary: New middle class consumers in the emerging markets”. Journal of Marketing 78 (4): 25–140.

Jaiswal, A.K., and S. Gupta. 2015. The influence of marketing on consumption behavior at the bottom of the pyramid. Journal of Consumer Marketing 32 (2): 113–124.

Lappeman, J., L. du Plessis, E. Ho, E. Louw, and P. Egan. 2021. Africa’s heterogenous middle class: A 10-city study of consumer lifestyle indicators. International Journal of Market. Research. 63 (1): 58–85.

Lustig, N. 2016. Inequality and fiscal redistribution in middle income countries: Brazil, Chile, Colombia, Indonesia, Mexico, Peru and South Africa. Journal of Globalization and Development 7 (1): 17–26.

Liébana-Cabanillas, F., I.R. De Luna, and F.J. Montoro-Ríos. 2015. User behaviour in QR mobile-payment system: The QR payment acceptance model. Technology Analysis & Strategic Management 27 (9): 1031–1049.

Malhotra, N. 2010. Marketing Research: An Applied Orientation, 6th ed. New York: Pearson.

Mashaba, N., and M. Wiese. 2016. Black middle class township shoppers: A shopper typology. The International Review of Retail, Distribution and Consumer Research 26 (1): 35–54.

Milanovic, B., and S. Yitzhaki. 2002. Decomposing world income distribution: Does the world have a middle-class?. Review of Income and Wealth 48 (2): 155–178.

Mittelmeier, J., R. Jekaterina, D. Long, D. Mwazvita, A. Gunter, and P. Prinsloo. 2019. Understanding the Early Adjustment Experiences of Undergraduate Distance Education Students in South Africa. International Review of Research in Open and Distributed Learning, 20 (3). https://doi.org/10.19173/irrodl.v20i4.4101.

Modigliani, F., and R. Brumberg. 1954. Utility analysis and the consumption function: An interpretation of cross-section data. In Post-Keynesian economics, ed. K. Kurihara, 388–436. New Brunswick, NJ: Rutgers University Press.

Mothobi, O., and L. Grzybowski. 2017. Infrastructure deficiencies and adoption of mobile money in Sub-Saharan Africa. Information Economics and Policy 40: 71–79.

Narteh, B., M.A. Mahmoud, and S. Amoh. 2017. Customer behavioural intentions towards mobile money services adoption in Ghana”. The Service Industries Journal 37 (7–8): 426–447.

Ncube, M., C. Lufumpa, and S. Kayizzi-Mugerwa. 2011. The middle of the pyramid: Dynamics of the middle class in Africa. Tunis: Africa Development Bank.

Pressman, S. 2010. The middle class throughout the world in the mid-2000s. Journal of Economic Issues 44 (1): 243–263.

Pressman, S. 2015. Defining and measuring the middle class. American Institute for Economic Research: 1–27 .

PWC. 2016. Ghana banking survey: How to win in era of mobile money. Retrieved April 13, 2017, from https://www.pwc.com/gh/en/assets/pdf/2016-banking-survey-report.pdf.

Sarma, M. 2008. Index of financial inclusion. IMF Working Paper No. 215.

Ravallion, M. 2010. The developing world’s bulging (but vulnerable) middle class. World Development 38 (4): 445–454.

Tchana, F., and T.M. Kengne. 2016. Analysis of the determinants of financial inclusion in Central and West Africa”. Transnational Corporations Review 8 (4): 231–249.

Tschirley, D., T. Reardon, M. Dolislager, and J. Snyder. 2015. The rise of a middle class in East and Southern Africa: Implications for food system transformation. Journal of International Development 27 (5): 628–646.

Uner, M.M., and A. Gungordu. 2016. The new middle class in Turkey: A qualitative study in a dynamic economy. International Business Review 25 (3): 668–678.

Wilson, D. and R. Dragusanu. 2008. The expanding middle: The exploding world middle-class and falling global in equality global economics Paper No: 170: Goldman Sachs.

Wimmer, A., and N.G. Schiller. 2002. Methodological nationalism and beyond: Nation-state-building and the social sciences. Global Networks 2 (4): 301–334.

Wolff, E., T. Grippa, Y. Forget, S. Georganos, S. Vanhuysse, M. Shimoni, and C. Linard. 2020. Diversity of urban growth patterns in Sub-Saharan Africa in the 1960–2010 period. African Geographical Review 39 (1): 45–57. https://doi.org/10.1080/19376812.2019.1579656.

World Bank. 2019. Taking the Pulse of Africa’s Economy. https://www.worldbank.org/en/region/afr/publication/taking-the-pulse-of-africas-economy.

Xin, H., Techatassanasoontorn, and F.B. Tan. 2015. Antecedents of consumer trust in mobile payment adoption. Journal of Computer Information Systems 55 (4): 1–10.

Funding

Open Access funding enabled and organized by CAUL and its Member Institutions.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Chikweche, T., Lappeman, J. & Egan, P. Marketing financial services in Africa: exploring the heterogeneous middle-class consumer across nine countries. J Financ Serv Mark 29, 1–16 (2024). https://doi.org/10.1057/s41264-022-00179-4

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41264-022-00179-4