Abstract

The phenomenal growth of retail in India is reflected in the rapid increase in number of supermarkets, departmental stores and hypermarkets in the country. However, this unprecented growth trend has been challenged by the shadow of the current economic slowdown, which has raised a fear of dip in consumption and slowdown of growth for Indian organized retailers. At a time when consumer spending is on decline, success will lie with those retailers that can drive customer loyalty by responding to the demands of the discerning consumer. This study is an attempt to address issues related to store attributes and their relevance in the store selection process. Eleven variables (store attributes) have been identified in this article based on theory and judgment. Factor analysis has yielded three factors: Convenience & Merchandise Mix, Store Atmospherics and Services. The factors identified and recommendations made in the article would be of use to retailers in designing their outlets with store attributes that would meet the expectations of shoppers and thus motivate them towards store patronage decisions.

Similar content being viewed by others

INDIAN RETAIL SCENARIO

Shopping in India is witnessing a gradual revolution with the phenomenal rise and exponential growth of the retail industry, which is having employment of around 8 per cent and contributing to over 10 per cent of the country's GDP (Source: www.business.mapsofindia.com). At US$511 billion in 2008, the overall retail industry of the country is expected to rise to US$ 833 billion by 2013 and further to US$ 1.3 trillion by 2018, at a Compound Annual Growth Rate (CAGR) of 10 per cent. Organized retail, which accounts for almost 5 per cent of the market, is expected to grow at a CAGR of 40 per cent from $20 billion in 2007 to $107 billion by 2013. Modernization of the industry is reflected in rapid growth in sales of supermarkets, departmental stores and hypermarkets. Sales from these large-format stores have expanded at commendable growth rates during the period of 2003–2008, ranging from 24 per cent to 49 per cent per year.

Looking at Indian retail in the backdrop of the worldwide economic slowdown, it can be concluded that the current economic environment has raised a fear of dip in consumption and slowdown of growth for Indian organized retailers. According to the Retailers’ Association of India, growth in the Rs 45,000-crore organized retail sector has slowed down to 5 per cent in the fourth quarter of 2008–2009, a far cry from the 35 per cent growth recorded in January–March 2008. A report by KPMG (March 2009) states that the ongoing slowdown in the economy has taken a major toll on the dissemination of India's organized retail. The report also revealed that India's investment flow in organized retailing, which was expected to touch $25 billion over the next 5-year period, is showing signs of slowdown.

Let us see the impact of the slowdown on consumers. At a time when consumer spending is on a decline, households may not be able to altogether prevent a fall in total expenditure; they would rather adjust the basket of goods purchased and shift their consumption towards essentials rather than luxury and high-end products. Another possibility would be switching over to cheaper brands or just eliminating some of the more expensive regular items of consumption. Does this mean doom for retail?

It would be quite obvious that under such taut economic circumstances, customers would congregate around outlets that offer higher value. Outlets that offer not-so-essential items would be the foremost victims; success will lie with those retailers that can drive customer loyalty by responding to the demands of the discerning consumer. Increased scrutiny of product quality and value propositions would be the decisive factors behind retail success amid slowdown. Factors like remixing value propositions, store rationalization, regionalization, working capital management, cost optimization and manpower resizing would thus emerge as the foremost concerns for retailers. They must provide good customer service consistently to enhance customer retention and thus drive profitability.

Retailers can, in fact, cash on the current financial turmoil as a business opportunity. They can take the maximum possible benefit from low rentals available in Tier II and III cities across the country, attracting extended middle-income families and thus expanding their loyalty base.

STORE ATTRIBUTES: RELEVANCE IN ORGANIZED RETAIL

Store attributes related to a retail outlet can be grouped in terms of ‘store atmospherics’ (Kotler, 1973) and store location. Store atmospheric attributes (including color, lighting, sales personnel, music and so on) form the overall context within which shoppers make decisions of store selection and patronage. Past research on retail environment suggests that such attributes affect the image of the store. Retailers realize the importance of such attributes and systematically try to avail of an ambience, including appropriate colors, music and so on that will attract their target customers. Further, purchase decision-making has become complex due to inseparability of product and services offered in retail outlets. As such, understanding the role played by store atmospherics on shoppers’ perceptions is critical to ensure store selection and patronage decisions and makes it an interesting area of research.

RETAIL MARKET CHANGES: DRIVERS FOR THE STUDY

The retail surge in India has percolated to Tier II and III cities. An estimate by Knight Frank indicates that 35 per cent of the total retail space being developed in India is located in 50 such cities. In smaller towns organized retail is growing at a rate of 50–60 per cent annually as compared to 35–40 per cent in metros and Tier I cities. Economic prosperity coupled with fewer spending options in these cities is attracting a number of retailers. Looking at the retail growth and development in Tier II and Tier III cities, researchers in this study have identified two Tier II cities to gain insight into the acceptance of organized retail outlets in smaller cities.

Customer's choice of a particular store depends on shopping orientation as well as satisfying experience. In addition, a customer's attitude towards the store may result from his/her evaluation of the perceived importance of store attributes, molded and remolded by direct experiences with the store's overall offerings. An attempt has been made in this study to analyze purchase patterns of customers towards organized retail outlets in terms of merchandise categories purchased; time spent within the store; number of merchandise purchased on each visit; and store switching behavior. Besides, we have also made an effort to identify store attributes that drive store selection process.

A store intercept survey was planned to obtain responses of shoppers on a structured questionnaire. The questionnaire was divided into two broad sections: the first was on purchase patterns of respondents, and the second on store attributes that influence the store selection process. Eleven variables were identified in the second section on the basis of review of related studies in the past and researchers’ insight, in order to identify important factors that drive store selection. The questions have been deliberately kept closed-ended, in order to facilitate data analysis. The survey was conducted at different times of the day and different days of the week to improve randomness. Total sample size was 520. However, on ignoring non-response, the sample size stood at 490.

Data were analyzed with SPSS version 11.5, using factor analysis, frequency tables and cross tabulation.

RELATED STUDIES

Store atmospheric attributes such as color, lighting, interior decoration or music form the overall context within which shoppers make store selection and patronage decisions, and are likely to have a significant impact on store image. Selection of a specific retail outlet involves a comparison of the available alternative outlets on the evaluative criteria of a consumer. Literature suggests a range of such criteria, which makes it a challenging task from the retailers’ point of view and makes store choice a matter of concern to retailers.

According to Lindquist (1974), store image consists of a combination of tangible (or functional) and intangible (or psychological) factors that consumers perceive to be found in retail stores. Consumers use store image as an evaluative criterion in the decision-making process of selecting a retail outlet (Varley, 2005). Store attributes refer to the underlying components of a store image dimension (like merchandise, physical facilities, services, atmospherics and so on). Research on store image has yielded a large number of attributes (Martineau, 1958; James et al, 1976; Peter and Olson, 1990). Store image has been found to be linked to store loyalty and patronage decisions (Assael, 1992; Wong and Yu, 2003).

Hansen and Deutscher (1978) used a base of 485 consumers in Ohio and examined the relative importance of the various aspects of retail image to different consumer segments. They made comparison of different attributes across departmental and grocery stores to indicate congruence and concluded that the same attributes are important across different types of stores.

Kaul (2005) made a study on which store attributes are appealing for self-image of consumers and their impact on in-store satisfaction and patronage intentions. She concluded that service expressiveness value is distinct from the performance value obtained from service delivery. Consumers satisfied with service quality are most likely to become and remain loyal (Wong and Sohal, 2003). Kaul (2005) further observes that a store having modern equipment, good and clean physical facilities and ease in transactions would be able to yield satisfaction and patronage intentions.

Tripathi and Sinha (2006) have studied retail store choice not from the perspective of an individual but of the family. They argue that it is mostly the family and not the individual who is the consumer of the retail offering.

Visser et al (2006) studied the importance of apparel store image attributes as perceived by female consumers by means of eight focus groups. Results indicated that merchandise and clientele were perceived as the most important dimensions, followed by service; physical facilities were the least important.

Leung and Oppewal (1999) had conducted research on the roles of store and brand names in consumers’ choice of a retail outlet and concluded that a high-quality brand or high-quality store is sufficient to attract the customer to a retail store. The study also revealed that store names have a larger impact on store choice than the brand names of the products that these stores have on offer.

Hedrick et al (2005) propose that store environment and store atmospherics can influence customer's expectations on the retail salesperson. They conducted a study on sales people and store atmosphere, and identified that customer's perceptions of a salesperson's attributes and relationship building behaviors’ were important drivers of customer satisfaction. In retail, intentions are usually determined by a willingness to stay in the store, willingness to repurchase, willingness to purchase more in the future and willingness to recommend the store to others.

Yildirim et al (2007) did a study focusing on determining the effects of a store window type (flat or arcade) on consumers’ perception of store windows (promotion, merchandise and fashion) and shopping attitudes (intentions for store entry and purchase) in the context of retail outlets. To test the assumption that there are relationships between various types of store windows and consumers’ perception of store windows and shopping attitudes, they conducted a study based upon digital pictures of two types of store windows hypothetically located in a big store. Results revealed that consumers seem to have a more positive perception of flat windows than arcade windows with respect to promotion, merchandise and fashion.

Consumers evaluate alternative stores on a set of attributes, and depending on their individual preferences, would patronize the best store (Tripathi and Sinha, 2006). More studies on store attributes are given in Table 1.

SHOPPING PATTERNS AND EXPECTATIONS OF INDIAN CONSUMERS

-

i)

Acceptance of Retail among Different Age Groups: According to an analysis by Ernst & Young, the number of households in the upper middle class and high-income groups in India has increased from 30 million to 81 million, thus growing by 270 per cent. With over 50 per cent of the population under the age of 25 years, the Indian youth is driving the growth in the retail industry (Source: The Economic Times, 9 January 2008). Our survey reveals that of the respondents who visited organized retail outlets, 40 per cent were in the age group of less then 24 years, 27 per cent were between 25–34 years, 18 per cent were in the age group of 35–44 and 15 per cent belonged to the age group of 45 years and above. It thus corroborates the trend that the younger generation has greater tendency to visit organized retail outlets.

-

ii)

Frequency of Visit to an Outlet: Responses reveal that 22 per cent respondents visit a retail outlet once in a week, 7 per cent respondents visit once in 2 weeks, 22 per cent visit once in a month, 34 per cent visit once in 2–3 months, while the remaining 15 per cent visit an outlet once in 6 months.

-

iii)

Time Spent in a Store: Previous researches suggest that store patronage has direct relation with time spent in the store. Our survey reveals that most of the respondents (61 per cent) stay in a retail outlet for 1–2 hours; stay of 22 per cent respondents has lasted for less than 1 hour and 17 per cent respondents have mentioned their stay to be 3–4 hours at an outlet. However, none of the respondents was found to stay at an outlet for more than 4 hours.

-

iv)

Merchandise Purchased: The range of items that shoppers buy from any outlet may give an insight to the retailers about the acceptance of merchandise mix they offer. Responses show that 34 per cent respondents buy grocery, 70 per cent respondents buy garments, 34 per cent buy accessories, 29 per cent buy kids wear, 34 per cent buy household appliances, 59 per cent buy lifestyle products, 31 per cent respondents buy electronic goods and the rest 5 per cent buy other categories. Our survey further revealed that 13 per cent respondents purchase items worth less than Rs 500 in a single visit, 26 per cent respondents purchase goods worth Rs 500–1000, 20 per cent purchase worth Rs1000– 2000, 25 per cent respondents purchase items worth Rs 2000–5000 and the rest 16 per cent respondents shop for more than Rs 5000.

-

v)

Time Spent within Store and Average Number of Items Purchased on a Single Visit: 17 per cent and 16 per cent respondents respectively remained in the store for less than an hour, and purchased upto 10 items on a single visit ( Table 2). 23 per cent of respondents remained in the store for 1–2 hours, and on an average purchased upto 10 items. A small fraction of respondents (nearly 6 per cent) in the same category purchased 10–20 items. Surprisingly, those who remained in the store for 3–4 hours and for more than 4 hours had purchased fewer items (upto 10). This particular finding can be attributed to two facts: one, high involvement products require more time spent on acquiring knowledge and other related matters; and two, such people have a leisure orientation towards shopping. Those who spend less time within the store seem to come on a purposive visit of purchasing predetermined products, and remain averse to any kind of visual cues used by retailers for triggering further purchases.

Table 2 Time spent in a store *average number of items purchased (cross tabulation) -

vi)

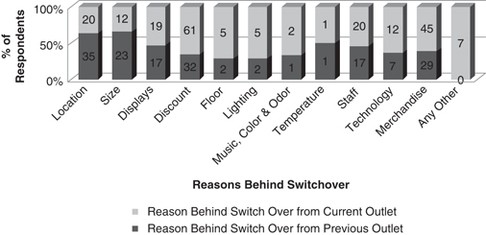

Store-Switching Behavior and Underlying Reasons: An attempt was made to identify store-switching behavior of shoppers, and to determine the reasons for switching from a previous outlet. The most important reasons for switching from previous to new one were Location, Discounts and Merchandise Offered, followed by Displays, Prompt Staff and Size of the Store (Figure 1). Factors like Floor Management, Lighting, Temperature, Light, Odor, Music and Technology remain dormant.

Figure 1:

Reasons behind switchover from outlet.

-

vii)

Store Attributes as Influencers in Store Selection Process: Based on theory and judgment of the researchers, 11 variables (store attributes) were identified, which could influence an individual's decision to visit a retail outlet. Respondents were asked to rank their responses on a five-point Likert Scale ranging from Highly Important (5) to Not at all Important (1). Factor analysis was run using SPSS version 11.5 on the ratings collected from the sample to generate factors that would indicate the most important of the store attributes.

Bartlett's test of sphericity and Kaiser–Meyer–Olkin (KMO) measures of sampling adequacy were used to examine the appropriateness of factor analysis. The approximate chi-square statistic is 367.574 with 55 degrees of freedom, which is significant at 0.05 level. The KMO statistic (0.722) is also large (greater than 0.05). Considering these outcomes, factor analysis is considered as an appropriate technique for further analysis of data.

Three factors have emerged on the basis of Varimax Rotation with Kaiser Normalization, with factor loadings greater than 0.6. 24.203 per cent of variance is explained by Factor 1; 20.904 per cent of variance is explained by Factor 2 and 17.403 per cent of variance is explained by Factor 3. All three factors together contribute to 62.510 per cent of variance (Refer to Table 3).

The researchers have conceptualized the identified factors as: Convenience and Merchandise Mix (Factor 1); Store Atmospherics (Factor 2) and Services (Factor 3). The identified factors with the associated variables and factor loadings are given in Table 4.

-

i)

Convenience and Merchandise Mix (Factor 1): It is evident from the survey that customers in Tier II and III cities tend to evaluate a store on the two facets of convenience and merchandise on offer. Convenience is sought in terms of distance of an outlet from residence or workplace and floor of an outlet for ease of movement within the outlet. Exposure to multiple options to choose from makes customers more demanding while selecting an outlet. They seek variety of products at competitive prices.

-

ii)

Store Atmospherics (Factor 2): Shopping is gradually emerging as a stress releaser (Sinha, 2003). Desire to shop in a pollution-free and comfortable atmosphere is apparent from the responses in the survey. Customers look for hassle-free shopping in an environment that is conducive. Well-lit stores with the right temperature and right kind of music may also reduce stress.

-

iii)

Services (Factor 3): Store selection process is becoming complex due to the ever-increasing needs of shoppers. A customer chooses a store on the basis of parameters like convenience, merchandise mix and atmospherics, as is evident from the previous factors. The services component of an outlet cannot be ignored, as it forms an inseparable part of the store selection decision-making. Our study reveals that customers look for fast and efficient billing systems, visual merchandizing, informative signage within the store and prompt staff.

TARGETED RETAIL STRATEGIES

As is evident from the survey, the ‘older’ generation in the age group of 45 years and above visits retail outlets less frequently. Such findings could be attributed to certain facts like: elder generations are less experimental and wish to remain associated with the stores they have been patronizing for longer duration; they are pragmatic and seek value, whereas a general perception about new retail formats is that these formats offer comparatively higher prices, do not provide personal attention and are inconvenient.

Responses obtained on the merchandise purchased show that the commonly purchased items from a retail outlet are garments, followed by lifestyle products, grocery and household appliances. Kidswear registered a very low purchase rate. A shift from taking shopping as a mundane activity to more towards considering it as a stress releaser and fun has been observed from past researches; this is evident from the responses that shoppers remain within a store for at least 2 hours.

Any decision-making process for retail outlets becomes complex due to the inseparability of goods and multiplicity of services. A customer now appreciates shopping in a pleasant environment at one-stop location with a wider product-portfolio in a speedy manner. Our study reveals that customers in Tier II and III cities evaluate a store based on Convenience and Merchandise Mix, Store Atmospherics and Services.

The following are the recommendations that can be made from the findings:

-

i)

Retailers may adopt cross-merchandising by offering complementary goods and services to encourage shoppers to buy more. They can also aim at infusing newer product lines frequently to improve the turnover of the outlet by targeting the impulsive buying behavior of customers.

-

ii)

Exclusivity and value are desired by shoppers while purchasing. Private labels can play an important role here, in bridging the gaps like special and desired price points, exclusivity and regional tastes. A private label can add significant value when it is well recognized and has built positive association in the mind of the consumer.

-

iii)

Elements of fun and entertainment in a store lead to longer time spent. Retailers may organize small events from time to time. Having exclusive happy hours during lean hours of the day for older generations may attract them to visit outlets more frequently and thus cement their relationship with the store.

-

iv)

Outlets must ensure that sales personnel must have sufficient knowledge of the products offered, and also must be capable of handling complaints. They must also exhibit willingness to handle returns, and should be available for advice or clarification. Overall, retail outlets must ensure courteous behavior of sales personnel. Well-mannered and helpful staff can always lead to store patronage decisions.

-

v)

Retailers can reduce the perception of waiting, without necessarily reducing the actual wait. They can make outlets more entertaining by utilizing the layout or methods of displaying merchandise to alter customers’ perceptions of waiting. Additionally, they can enhance the store atmospherics through visual communications (signs and graphics), lighting, colors and even odors.

-

vi)

Store space utilization and layout affect traffic patterns inside the store. Store entrance, aisles and lighting should enhance the image of the store to encourage customers to wander around and be stimulated. Special zones could be created to appeal to the shoppers to stay longer and explore the shopping experience further.

-

vii)

In an age of quick services, technology is a necessary ingredient for success of any retail outlet. Consumers would prefer to visit such outlets that would provide prompt and error-free billing services. Retailers may adopt different technologies to manage faster billing. They should also work on having multiple payment options like cash, credit cards and debit cards and so on to facilitate customers.

All these, and more, can surely meet the expectations of shoppers from an outlet and thus motivate them towards store patronage decisions.

References

Assael, H. (1992) Consumer Behavior and Marketing Action, 4th edn. Boston, MA: PWS-KENT Publishing Company.

Bawa, K. and Ghosh, A. (1999) A model of grocery shopping behavior. Marketing Letters 10 (2): 149–160.

Bell, D.R. and Lattin, J.M. (1998) Shopping behavior and consumer preference for store price format: Why ‘large basket’ shoppers prefer EDLP. Marketing Science 17 (1): 66–88.

Berman, B. and Evans, J.R. (2007) Retailing Management: A Strategic Approach, 8th edn. New Delhi: Pearson Education.

Desai, K. and Talukdar, D. (2003) Relationship between category price perceptions, shopper's basket size, and overall store price image: An analysis of the grocery market. Psychology & Marketing 20 (10): 903–933.

Donovan, R.J., Rossiter, J.R., Marcoolyn, G. and Nesdale, A. (1994) Store atmospherics and purchasing behavior. Journal of Retailing 70 (3): 283–294.

Ehrenberg, A., Hammond, K. and Goodhardt, G. (1994) The after-effects of price-related consumer promotions. Journal of Advertising Research 34 (4): 11–21.

Engel, J.F., Blackwell, R.D. and Miniard, P.W. (1995) Consumer Behavior, 8th edn. Forth Worth, TX: The Dryden Press.

Grewal, D., Krishnan, R., Baker, J. and Borin, N. (1998) The effect of store name, brand name and price discounts on consumers’ evaluations and purchase intentions. Journal of Retailing 74 (3): 331–352.

Hansen, R. and Deutscher, T. (1978) An empirical investigation of attribute importance in retail store selection. Journal of Retailing 53 (4): 59–95.

Hawkins, D.I., Best, R.J. and Coney, K.A. (2004) Consumer Behavior: Building Marketing Strategy, 9th edn. New York: McGraw-Hill.

Hedrick, N., Beverland, M. and Oppewal, H. (2005) The impact of retail salespeople and store atmospherics on patronage intentions, http://www.conferences.anzmac.org/ANZMAC2004/CDsite/papers/Hedrick1.PDF.

Herrington, J.D. and Capella, L.M. (1994) Practical applications of music in retail and service settings. Journal of Services Marketing 8 (4): 50–65.

Hui, M.K., Dube, L. and Chebat, J.-C. (1997) The impact of consumers’ reaction to waiting for services. Journal of Retailing 73: 87–104.

James, D.L., Du Rand, R.M. and Dreeves, R.A. (1976) The use of a multi-attribute model in a store image study. Journal of Retailing 52 (2): 23–32.

Kaul, S. (2005) Impact of performance and expressiveness value of store service quality on the mediating role of satisfaction. WP No. 3 October 2005, IIMA.

Kotler, P. (1973) Atmospherics as a marketing tool. Journal of Retailing 49: 48–64.

Leung, V. and Oppewal, H. (1999) Effects of brand and store names on consumer store choice, http://smib.vuw.ac.nz:8081/www/ANZMAC1999/Site/L/Leung.pdf.

Levy, M. and Weitz, B. (1998) Retailing Management, 3rd edn. New York: McGraw Hill.

Lindquist, J.D. (1974) Meaning of image. Journal of Retailing 50 (4): 29–38.

Martineau, P. (1958) The personality of the retail store. Harvard Business Review 36: 47–55.

Mattila, A.S. and Wirtz, J. (2001) Congruency of scent and music as a driver of instore evaluations and behavior. Journal of Retailing 77 (3): 273–289.

McGoldrick, P. (2002) Retail Marketing, 2nd edn. London: McGraw-Hill.

Mendes, A. and Themido, I. (2004) Multi outlet retail site location assessment. International Transactions in Operational Research 11 (1): 1–18.

Peter, J.P. and Olson, J.C. (1990) Consumer Behavior and Marketing Strategy, 2nd edn. Boston, MA: Irwin.

Reynolds, K.E. and Arnold, M.J. (2000) Customer loyalty to the salesperson and the store: Examining relationship customers in an upscale retail context. Journal of Personal Selling & Sales Management 20 (2): 89–98.

Schiffman, L. and Kanuk, L. (2008) Consumer Behavior, 9th edn. New Delhi: PHI.

Simonson, I. (1999) The effect of product assortment on buyer preferences. Journal of Retailing 75 (3): 347–370.

Sinha, P.K. (2003) Shopping orientation in the evolving Indian market. Vikalpa 28 (2): 13–22.

Tripathi, S. and Sinha, P.K. (2006) Family and store choice – A conceptual framework. WP No. 3 November 2006, IIMA.

Varley, R. (2005) Store image as the key differentiator. European Retail Digest 46: 18–21.

Visser, E., Preez, R. and Noordwyk, H. (2006) Importance of apparel store image attributes: Perceptions of female consumers. South African Journal of Industrial Psychology 32 (3): 49–62.

Wong, G.K.M. and Yu, L. (2003) Consumers’ perception of store image of joint venture shopping centres: First-tier versus second-tier cities in China. Journal of Retailing and Consumer Services 10: 61–70.

Wong, A. and Sohal, A. (2003) Service quality and customer loyalty perspectives on two levels of retail relationships. Journal of Services Marketing 17 (5): 495–513.

Yildirim, K., Akalin-Baskaya, A. and Hidayetoglu, M. (2007) The effects of the store window type on consumers’ perception and shopping attitudes through the use of digital pictures. G.U. Journal of Science 20 (2): 33–40.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Ghosh, P., Tripathi, V. & Kumar, A. Customer expectations of store attributes: A study of organized retail outlets in India. J Retail Leisure Property 9, 75–87 (2010). https://doi.org/10.1057/rlp.2009.27

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/rlp.2009.27