Abstract

This article studies the valuation of multivariate equity options by determining the joint risk-neutral distribution of the underlying stock prices by means of copulas. In contrast to previous work that concentrates on two underlyings this study considers the general multivariate case. In particular, tri-variate and six-variate elliptical and Archimedean copula families are calibrated empirically in order to find the copula that best fits the observed dependence structure. In addition, based on price data from single underlying options traded at the European Exchange (Eurex) the valuation of typical multivariate options is compared between Black–Scholes-like and alternative copula-based valuation models. Remarkable differences and thus a high model risk become evident, accompanied by a distinct parameter sensitivity in the copula models.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

INTRODUCTION

The importance of multivariate equity options in the international financial markets is increasing steadily. Well suited for portfolio hedging purposes and active market strategies these derivatives have experienced rapid growth in recent years. This holds true for both the over the counter (OTC) and the retail markets where these days multivariate equity options are often found to be embedded components of structured financial products. For instance, the gross market values of outstanding equity-linked options in the OTC market amounted to US$876 billion by mid-2007, with an annual growth rate of 67 per cent (source: Bank for International Settlements). The trading volume of exchange-tradable structured products in Germany as the largest European retail market reached nearly €200 billion in 2007, which constitutes about a 50 per cent increase compared to 2006 (source: Deutsches Derivate Institut). The standard valuation models for multi-underlying contingent claims are based on the assumption of a multivariate geometric Brownian motion for the price process of the underlying securities,1, 2 which implies that the underlying prices (returns) are jointly log-normally (normally) distributed. Empirically, however, it is a well-known stylized fact that stock return distributions usually depart from the assumption of normality. Furthermore, the risk-neutral return distribution induced by standard option pricing models is not compatible with the normality dogma against the background of proven phenomena such as a volatility smile or skew and a non-flat term structure of volatility. This suggests that, by using the standard (log-)normal distribution, multivariate options can be misvalued significantly, which motivates the search for alternatives.

In the literature, many recent models for valuing multivariate options rely on the theory of copulas. Copulas allow the separate modeling of the marginal distributions and the dependence structure of the variables. Rosenberg,3 for example, uses a Plackett copula to couple the risk-neutral marginal distributions extracted from univariate options data. Cherubini and Luciano4 also link risk-neutral marginals with various Archimedean copula families. While these two studies estimate the copulas statically, Van den Goorbergh et al5 employ a dynamic approach with the copula parameter depending on conditional volatility, a technique that was recently extended further by the work of Zhang and Guegan.6 All of these papers study options on equity indices. Rosenberg7 proposes non-parametric modeling and applies it to bivariate currency options. Saita et al8 compare the prices of five-variate equity options produced under the multivariate normal assumption with those generated by t-copulas with arbitrary degrees of freedom. However, a thorough calibration of the copulas and marginal distributions to market data is missing.

This article studies the valuation of a range of multivariate equity options by determining the joint risk-neutral distribution of the underlying stock prices using copulas. By considering the general multivariate case it extends previous work, which concentrates mainly on two underlying options. A range of elliptical and Archimedean copulas is calibrated empirically to stock returns in order to find the best fit to the observed dependence structure, while stock option data are used to extract marginal distributions. Based on this setting, which largely extends the former setup chosen by Saita et al,8 the valuation of several types of multivariate options is assessed and compared. A parameter sensitivity analysis is conducted in order to shed further light on the mechanics of the copula-based valuation approaches. The results suggest a high degree of model risk inherent in the option valuation as well as pronounced parameter sensitivity in the models themselves.

The article is organized as follows. The next section provides a brief introduction to the theory of copulas. The subsequent section outlines the copula-based valuation approach for multivariate options. The methodology and results of the empirical application are described in the following section. The last section summarizes and provides an outlook for further research.

ESSENTIALS ON COPULAS

Definition and main characteristics

Starting with a brief introduction to the theory of copulas (see, for example, Nelsen9 as a standard reference) elementary terms and results are outlined first. A copula is a multivariate distribution function C defined on [0, 1]d with uniformly distributed margins,

where U1, …, U d ∼U(0, 1).

The fundamental result of the copula theory is the well-known Sklar10 theorem. It states that for any real-valued random variables X1, …, X d with joint distribution function F and univariate marginal distribution functions F1, …, F d there exists a copula C such that

Conversely, given a copula C and univariate distribution functions F1, …, F d , the function F defined by (1) is a d-dimensional distribution function with univariate margins F1, …, F d . Furthermore, if F1, …, F d are all continuous C is unique and referred to as the copula of X1, …, X d . It follows that, in the case of continuous margins, the joint distribution function can be decomposed into the margins and the functional dependence of the random variables represented by their unique copula. For practical purposes, the marginal distributions can thus be modeled separately from the dependence structure. The combination of arbitrary margins and copulas yields a flexible approach to the construction of multivariate distributions. In the other direction, knowledge of the joint distribution function and the margins determine the copula by

where ui, …, u d ∈[0, 1] and F i −1(u i )= inf{x i ∈ℝ:F i (x i )⩾u i } denotes the pseudo-inverse of F i . This technique for the construction of copulas is known as the inversion method.

If a copula is absolutely continuous it has a density, which then equals the d-th mixed partial derivative of C with respect to u1, …, u d . Furthermore, it follows from (1) that the copula density can be expressed as the quotient between the joint density f of X1, …, X d and the product of the marginal densities f i , i=1, …, d:

A useful property of copulas for modeling stochastic dependence is their invariance under strictly monotone transformations of the random variables (Embrechts et al.11 p. 337). Formally, let X1, …, X d be continuous random variables with (unique) copula C. If α1, …, α d are strictly increasing functions the transformed random variables α1(X1), …, α d (X d ) have the same copula C. This invariance is particularly useful for financial applications in which logarithmic transformations are used frequently.

Important copulas for financial applications

Elliptical copulas

Elliptical copulas are commonly used in financial applications. They describe the dependence structure of elliptical distributions and can be derived using (2) (for further details see Embrechts et al,11 pp. 357 ff.). Elliptical copulas are characterized by a range of parameters and can be fitted flexibly to data, although all of these copulas are radially symmetric. Their major disadvantage is the absence of closed-form expressions. The most prominent elliptical copulas are the Normal and the t-copulas.

The Normal copula, also known as the Gaussian copula, is defined as

where Φ∑ denotes the multivariate normal distribution function with correlation matrix ∑ and Φ−1 as the quantile function of the univariate standard normal distribution. Following (3) the density of the Normal copula reads as follows:

with ς=(Φ−1(u1), …, Φ−1(u d ))′ and I as the d-dimensional identity matrix. The Normal copula is the copula of the multivariate Gaussian distribution and is thus inherent in many standard models in finance.

Another prominent elliptical copula is the t-copula. Compared to the Normal copula it can model stronger dependencies in the distribution tails (for details on tail dependence see, for example, Embrechts et al,11 pp. 348 ff.). The t-copula is defined via (2) as

where tν,∑ stands for the distribution function of the multivariate t-distribution with ν>0 degrees of freedom and correlation matrix ∑. t ν −1 represents the quantile function of the univariate t-distribution with ν degrees of freedom and Γ refers to the gamma function. The density of the t-copula is given by

with ς i =t ν −1(u i ), i=1, …, d, and ς= (t ν −1(u1), …, t ν −1(u d ))′. In comparison to the Normal copula the t-copula has one additional parameter – the degrees of freedom ν, which controls the dependence in the tails. This dependence increases for decreasing values of ν. The t-copula converges to the Normal copula for ν → ∞.

Archimedean copulas

Another important class of copulas is given by the Archimedean copulas, which are easily constructed by means of univariate generator functions and possess closed forms. Archimedean copulas can model a variety of dependence structures. In particular, unlike elliptical copulas, they can reflect asymmetrical dependence patterns. Their drawback is the small number of parameters, which reduces the flexibility. Formally, let φ:[0, 1] → [0, ∞] be a continuous, strictly decreasing function with φ(1)=0 and φ(0)=∞ and let φ−1 be its inverse function with φ−1(0)=1 and φ−1(∞)=0. Then the function C:[0, 1]d → [0, 1] defined as

is a d-dimensional copula if and only if φ−1 is d-monotone on [0, ∞).12 The function C is referred to as an Archimedean copula and φ as the corresponding generator function. The density of the Archimedean copulas is given by

where φ−1(d)=∂dφ−1/∂u1 … ∂u d is d-th mixed partial derivative of the inverse generator.

For dimensions d⩾3 Archimedean copulas (in their commonly used form with completely monotone generators) can represent only positive dependencies (see Embrechts et al.11, p. 374). This constraint is of less concern for practical applications in equity markets as negative dependencies are usually rare in that context. A more important property of the Archimedean copulas is that all their k-dimensional margins, k=2, …, d−1, are identical. This property suggests that each two variables have the same ‘degree’ of dependence, which turns out to be very restrictive for more than two dimensions.

There are three Archimedean families that are most commonly used in the financial context and that have multivariate extensions for dimensions greater than two – the Gumbel, Clayton and Frank family. The Gumbel copula is able to model dependencies in the right tails of the variables. The Gumbel family given by

is generated by φ θ (t)=(−lnt)θ, for θ⩾1. For modeling dependencies in the left tails, an appropriate family is the Clayton one, which has the form

It is generated by φ

θ

(t)=1/θ(t−θ−1) with θ>0. The Frank copula is the only radially symmetric Archimedean copula. Like the Normal copula, the Frank copula cannot model dependencies in the tails. Its generator is  with θ>0, and the family has the form

with θ>0, and the family has the form

For all these Archimedean families an increase in the parameter θ implies a stronger dependence.

VALUATION APPROACH FOR MULTIVARIATE EQUITY OPTIONS

Building on the property of copulas to bind the univariate marginal distributions to the joint distribution this section presents a valuation model for multivariate equity derivatives. A multivariate option is a financial instrument whose payoff depends on the prices of several underlying securities. Generally, in the equity case let h(S1, …, S d ) be a function of d stock prices S i at the option's maturity and g(x) be a univariate payoff function. Accordingly, a multivariate, non-path-dependent and European-style equity option can be represented as g(h(S1, …, S d )) (see also Cherubini and Luciano,4 p. 70).

A variety of option types can be constructed by combining different functions g and h. It is well known that the option value can be expressed as the discounted risk-neutral expected value of the payoff. Thus, the first step in valuing a multivariate option consists in determining the joint risk-neutral distribution. Sklar's theorem allows a simplification of this task by separately modeling the univariate risk-neutral margins and the risk-neutral copula. In the following analysis, the univariate risk-neutral margins are extracted by means of Shimko's method.13 The volatility smile is thereby assumed to be a quadratic function, σ(K)=a0+a1K+a2K2, where K denotes the strike price. Using this representation a differentiation of the seminal Black and Scholes14 formula with respect to the strike yields the risk-neutral distribution function F i ℚ of the stock price S i at maturity:

with

where φ(x) and Φ(x) represent the density and the distribution function of the standard normal distribution at the point x, respectively. Si,0 stands for the current underlying price, r the (continuously compounded) risk-free interest rate and τ the time-to-maturity.

After extracting the risk-neutral margins the dependence structure must be identified. As multivariate equity options are usually traded over the counter one cannot easily obtain option prices in order to extract the risk-neutral copula from market prices. Owing to this lack of data it is assumed that the risk-neutral and the real-world copulas are identical. Rosenberg,7 for instance, argues that under general conditions this is a reasonable assumption. Relying on historical (continuous) asset returns different copula families can then be fitted to the data (refer to Cherubini and Luciano4 for a similar calibration to historical returns). As the returns are strictly monotone transformations of asset prices both have identical copulas.

The option values can be determined by simulation15 through repeating the following three steps M times:

-

1

Simulation of one vector from the d-variate copula,16 (u1*, …, u d *)∼C θ .

-

2

Transformation of (u1*, …, u d *) to (x1*, …, x d *) via the univariate inverse risk-neutral distributions x1*=F i ℚ(−1)(u i *), i=1, …, d.

-

3

Evaluation of the discounted payoff O m *=e−rτg(h(x1*, …, x d *)).

The option value is then approximated by the mean of the discounted payoffs:

EMPIRICAL APPLICATION

Methodology and data

The following empirical investigation aims at assessing the valuation of multivariate equity options based on real-world data from the European derivatives market. The study searches to reveal valuation implications arising from the use of dependence structures that differ from the Normal copula, the implicit assumption in Black–Scholes-like option valuation models. Henceforth, the focus lies on European-style calls on the maximum of several assets (call-on-maximum), puts on the minimum of several assets (put-on-minimum) and multivariate digital put options. The former two types only make sense when the underlying prices are close to each other at inception. Therefore, the asset prices, Si,0, are normalized to the common level S by scaling them with the factors, a i =S/Si,0, i=1, …, d, so that the payoff functions read as follows:

for the call-on-maximum and

for the put-on-minimum option, with S i as the spot price of stock i at maturity and K as the strike price. The digital put should pay D if all underlying options fall below their strikes. Hence, the payoff is formalized as D∏i=1d 1(S i ⩽K i ).

The empirical application refers to multivariate call-on-maximum, put-on-minimum and digital options on three different stock baskets. The first basket consists of six companies from the Dow Jones Euro Stoxx 50 with liquid single stock options, the other two each comprise a sub-selection of three of these titles – Allianz, Münchener Rück and AXA (‘insurance basket’) and SAP, Nokia and Alcatel-Lucent (‘technology basket’).

In order to extract the risk-neutral distributions for the six underlying options, corresponding option data from the Eurex, provided by Deutsche Börse, Frankfurt/Main, is used. Option settlement prices that refer to the close of the trading day at 17:30 are collected. All single stock options at the Eurex are American-style (for details on Eurex products see Eurex17). The reference date is chosen as 16 June 2005, although additional calculations are conducted for the period from 1 June through 15 June 2005 in order to enable stability and sensitivity studies. All available options with maturities in September and December 200518 are considered, leading to times-to maturity of approximately 3 and 6 months. Synchronized stock prices are obtained from the electronic XETRA trading system at the Frankfurt Stock Exchange. The underlying options do not exhibit dividend payments in the relevant time period. 3-month and 6-month Euribor rates serve as proxies for the risk-free interest rates and are obtained from Bloomberg.

The first step to deriving univariate risk-neutral distributions consists in extracting the volatility smile from the option prices. As common practice the analysis refers to generally more liquid out-of-the-money calls and puts, that is, implied volatilities for strikes below (above) the current stock price are calculated from puts (calls).19 The option data are cleaned as follows. Options with no open interest are removed from the database because missing open positions render settlement prices, set by the exchange, artificial and usually non-tradeable. Furthermore, options with prices below 10 times the minimum tick size, that is, 10 euro cents, are excluded in order to avoid bias associated with very small option (time) values. Both criteria mainly affect deep out-of-the-money options. The remaining options are checked for potential violations of distribution-free arbitrage boundaries and the fulfillment of the put-call inequality for otherwise identical American-style options (Hull20, p. 211). Except from rounding differences the latter conditions are fulfilled throughout the option data set.

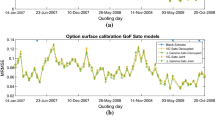

Implied volatilities are calculated via binomial trees and then used to estimate the coefficients in Shimko's quadratic regression.13 Figure 1 displays the regression results for options on Allianz with maturity in September (left) and December (right) on 1, 8 and 15 June. The typical volatility skew is modeled perfectly by the quadratic function, the adjusted R2 amount to more than 0.99. Similar results are obtained for all 144 regressions over the six underlying options, 12 valuation days and two maturities. As depicted the volatility skews in the Allianz example are quite stable over time in both maturity buckets.

Volatility skews of Allianz options on several trading days, fitted to quadratic functions; (a) Maturity: September 2005; (b) Maturity: December 2005.

With the help of the estimated regression coefficients formula (13) provides the corresponding implied univariate risk-neutral distribution functions.21 A volatility skew, for instance, is thus translated into a density that is more left-skewed and exhibits fatter left tails compared to a log-normal distribution.

Risk-neutral copulas

As discussed there are no direct means of estimating risk-neutral copulas in the absence of liquid tradeable prices for multivariate options. In the following analysis, the copulas under the real measure are referred to as adequate proxies. In theory, copulas for the 3- and 6-month returns are required. Following the simplified assumption that copulas for different time horizons are identical, that is, the copulas for returns and their respective sums must be equal, the copula inference is based on the weekly (continuously compounded) stock returns for the 3 years preceding the reference date.22 Descriptive statistics of the return series as well as the standard (Pearson) correlations of the six companies are shown in Table 1. All series exhibit rather high volatility, caused mainly by the hectic price movements in the first 1.5 years of the period July 2002 through June 2005. The correlation between all stocks is found to be positive, although correlations within the insurance basket are much higher than those within the technology basket.

The two elliptical copulas – Normal and t – as well as the three Archimedean copulas – Gumbel, Clayton, and Frank – are fitted to the historical time series. As the univariate distributions are given exogenously, the appropriate estimation technique is the canonical maximum likelihood (CML) method, which estimates only the copula.23, 24 The results of the estimation including values for the log-likelihood and Akaike's criterion (AIC) are shown in Table 2.

On the basis of the AIC values the t-copula exhibits clearly the best fit for all baskets. For the three-dimensional cases the second-best fit is observed for the Frank copula, whereas for the six-assets basket the Normal copula has the second-lowest AIC value.

Simulation of option values

On the basis of the univariate risk-neutral distributions and the calibrated copulas, theoretical values of non-path-dependent multivariate options are derived by simulating the joint risk-neutral distribution, with 100 000 simulation runs. The value of a multivariate digital option equals the discounted value of the copula at the strikes and can thus be calculated directly. The values of the underlying options for the call-on-maximum and put-on-minimum option are normalized to a level of S=100 for all baskets. Values of at-the-money options with a strike of K=100, out-of-the-money options with a strike at K=110 for calls (K=90 for puts) as well as in-the-money options with a strike at K=90 for calls (K=110 for puts) are calculated. The payout of the digital options is set to D=100. The out-of-the-money and in-the-money strikes for the digitals are selected at 10 per cent above and 10 per cent below the current stock price.

In standard models for valuing multivariate derivatives a multivariate normal distribution for the return distribution is assumed, thus implying a Gaussian copula as the ‘link’ between the marginal distributions. Below, the option values based on the two elliptical and the three Archimedean copulas are compared. Tables 3 and 4 display all option values with maturity in 3 and 6 months, respectively.

Some elementary plausibility checks are fulfilled. For instance, the value of the call-on-maximum and the put-on-minimum options for the single sectors must be lower than or equal to those on the entire basket. The opposite holds in the case of the multivariate digital puts. The options on the basket of six underlying options must be worth less than those on the compilation of three titles. In general, the values of the call-on-maximum and put-on-minimum derivatives should be the higher the weaker the dependence between the underlying options. Likewise, for multivariate digital options, the opposite should hold. For instance, the correlations of the elliptical copulas and the θ̂s of the Archimedean copulas are higher for the insurance basket compared to the technology basket. Hence, call-on maximum and put-on-minimum derivatives on the technology basket are more valuable than those on the insurance basket for all copulas. The opposite is true for the digital options.

From Tables 3 and 4 one can indeed see that large valuation discrepancies are evident. The relative differences range from approximately 1.2 per cent to a remarkable 75.2 per cent for the digital derivatives. For the other option types, valuation differences amount to 2.7 per cent through 15.3 per cent. The percentage differences vary with the moneyness. Not surprisingly, relative discrepancies are highest (lowest) for out-of-the-money (in-the-money) options owing to their low (high) values.

Sensitivity analysis

In order to gain further insight into the copula-based valuation of multivariate options, a sensitivity analysis based on at-the-money options is conducted. Two aspects are analyzed – the effect of changes (i) in the ‘degree’ of dependence and (ii) in the risk-neutral marginal distributions. Accordingly, the t-copula with the best fitting dependence structure is chosen as a basis.

First, the correlation coefficients (Σ in (6)) are varied simultaneously by ±0.1, while the degrees of freedom ν and the marginal distributions are held constant.25 Second, the margins are replaced consecutively by those from the previous two trading weeks while leaving the dependence structure of 16 June 2005 unchanged.26 The results are provided in Tables 5 and 6. It becomes evident that changes in the correlations imply substantial valuation differences. In particular, the relative differences range from approximately 2.5 per cent to 16.0 per cent for options with 3 months to maturity and from 2.4 per cent to 16.7 per cent for those expiring in 6 months. As found in the previous valuation analysis, the digital options again exhibit the largest ‘gaps’. The change in the margins causes day-to-day valuation differences in absolute terms between approximately 0.3 per cent and 14.0 per cent for the 3-month options and between 0.2 per cent and 10.7 per cent for the 6-month options. This is, of course, driven by changes in the volatility skew structures of the basket constituents. For example, all stocks in the technology basket exhibit shifts in their 3-month volatility skews on 10 June, which lead to a 14.0 per cent difference in the value of the put-on-minimum option.

In summary, the analysis has shown that – based on typical historical return data and empirical volatility skew structures – the choice of the copula has a substantial effect on the valuation of multivariate equity options. In particular, option values derived from the standard assumptions on correlation structures differ substantially from those considering a ‘true’ reflection of dependencies. The implications of such model risk for real-world applications as trading and risk management are evident. Furthermore, a brief sensitivity study showed that even moderate variations in the model parameters such as the ‘degree’ of dependence and the empirical marginal distributions of the baskets’ constituents may also cause significant valuation differences.

SUMMARY AND OUTLOOK

This article analyzes the valuation of multivariate equity options. Accordingly, the multivariate normality assumption for the underlying options’ returns is dropped and copula functions are applied instead, so as to bundle the univariate risk-neutral marginal distributions to the joint distribution function from which option prices are obtained by simulation. This approach enables the separate modeling of marginals and dependence structure so that the procedure for identifying the joint distribution becomes more tractable. The method thus allows the construction of multivariate distributions that better reflect market conditions and that also provide more accurate, market-consistent values of multivariate options.

In an empirical study, risk-neutral marginals are extracted from univariate options traded at the Eurex, while the dependence structure is estimated from historical stock returns. Various copula families are calibrated. It emerges that Archimedean copulas are not well suited to modeling the dependence in more than two dimensions because of their restrictive characteristics, whereas elliptical t-copulas provide the best data fit. When valuing multivariate equity options substantial differences result from assumptions about the underlying copula. Parameter sensitivity in the copula models is of concern as well.

The applied approach is very flexible and can be extended in numerous ways. First, other copula families could be considered such as hierarchical Archimedean copulas, which are much less restrictive than the simple Archimedean copulas. A better fit that takes into account asymmetrical dependencies could be achieved and lead to a more accurate valuation. Second, another promising direction is the consideration of dynamic dependence. Allowing the copula parameters to be time-varying (see Van den Goorbergh et al5 for such an approach in two dimensions) should further improve the performance of the model. Finally, the collection of a range of OTC market prices for multivariate equity options from market participants such as banks could yield more valuable insights into the empirical pricing mechanism and ‘market-implied copulas’.

REFERENCES AND NOTES

Stulz, R.M. (1982) Options on the minimum or the maximum of two risky assets: Analysis and applications. Journal of Financial Economics 10: 161–185.

Johnson, H. (1987) Options on the minimum or the maximum of several assets. Journal of Financial and Quantitative Analysis 22: 277–283.

Rosenberg, J.V. (1999) Semiparametric Pricing of Multivariate Contingent Claims. Working Paper, New York University, New York, August 1999.

Cherubini, U. and Luciano, E. (2002) Bivariate option pricing with copulas. Applied Mathematical Finance 9: 69–85.

Van den Goorbergh, R.W.J., Genest, C. and Werker, B.J.M. (2005) Bivariate option pricing using dynamic copula models. Insurance: Mathematics and Economics 37: 101–114.

Zhang, J. and Guegan, D. (2008) Pricing bivariate option under GARCH processes with time varying copula. Insurance: Mathematics and Economics 42: 1095–1103.

Rosenberg, J.V. (2003) Nonparametric pricing of multivariate contingent claims. The Journal of Derivatives 10 (Spring): 9–26.

Saita, F., Romano, M.E., Joossens, E. and Campolongo, F. (2005) Pricing Multiasset Equity Options with Copulas: An Empirical Test. Working Paper, Università Bocconi, Milan, June 2005.

Nelsen, R. (2006) An Introduction to Copulas, 2nd edn. New York: Springer.

Sklar, A. (1959) Fonctions de répartition à n dimensions et Leurs Marges. Publications de l’Institut de Statistique de l’Université de Paris 8: 229–231.

Embrechts, P., Lindskog, F. and McNeil, A. (2003) Modelling dependence with copulas and applications to risk management. In: S.T. Rachev (ed.) Handbook of Heavy Tailed Distributions in Finance. Amsterdam: Elsevier/North-Holland.

The function φ is referred to as a strict generator if φ(0)=∞ holds. For φ(0)<∞ it is also possible to define a copula function (for details see Embrechts et al,11 p. 373).

Shimko, D.C. (1993) Bounds of probability. Risk 6 (April): 33–37.

Black, F. and Scholes, M. (1973) The pricing of options and corporate liabilities. Journal of Political Economy 81: 637–654.

Cherubini and Luciano4 (p. 74) provide some closed-form expressions for bivariate options. Such expressions, however, are usually difficult or even impossible to derive in the multivariate case.

For simulation algorithms for elliptical copulas see Embrechts et al11 (p. 361) and for Archimedean copulas see Cherubini, U. Luciano, E. and Vecchiato, W. (2004) Copula Methods in Finance. West Sussex, UK: John Wiley & Sons, p. 188.

Eurex (2007) Products. Frankfurt/Main, March 2007.

Eurex stock option contracts expire on the third Friday of the maturity month.

Moneyness is defined as M=S/K for call and put options, that is, the study employs call (put) prices for M<1 (M>1).

Hull, J.C. (2008) Options, Futures and Other Derivatives, 7th edn. Upper Saddle River, NJ: Prentice Hall.

The formula for the marginal risk-neutral distribution holds only in the strike price range of the options from which it has been extracted. As a simplification it is assumed that it is also valid outside that range.

Compared to daily returns, weekly returns usually show less pronounced time dependence. A 3-year period provides sufficient observations for the estimation.

Genest, C., Ghoudi, K. and Rivest, L.-P. (1995) A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika 82: 543–552.

While the Archimedean copulas simply require a maximisation, the application of the CML estimation for the elliptical copulas is slightly more involved. See Bouyé, E., Durrleman, V., Nikeghbali, A., Riboulet, G. and Roncalli, T. (2000) Copulas for Finance: A Reading Guide and Some Applications. Working Paper, Crédit Lyonnais, Paris, July 2000, p. 27 for the Gaussian copula and the algorithm of Mashal, R. and Zeevi, A. (2002) Beyond Correlation: Extreme Co-movements Between Financial Assets. Working Paper, Columbia University, New York, October 2002 for the t-copula.

An increase in the degrees of freedom will lead to option values between those for the Normal and t-copulas in Tables 3 and 4.

Changes in the risk-neutral marginal distributions are reflected in volatility variations as well as in time-to-maturity effects. Given that maturities are identical for all options, the two influences cannot be separated from one another.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Slavchev, I., Wilkens, S. The valuation of multivariate equity options by means of copulas: Theory and application to the European derivatives market. J Deriv Hedge Funds 16, 303–318 (2011). https://doi.org/10.1057/jdhf.2010.5

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jdhf.2010.5