Abstract

This article examines, through a Monte Carlo simulation study, the impact of considering different Loss Given Default (LGD) definitions, as allowed by the regulation, in the accuracy of LGD calculation at portfolio level. The article suggests that the way the regulation is interpreted can have dramatic effects on LGD measurement and, consequently, on the capital that banks are required to hold for regulatory purposes. The findings herewith can be deemed quite robust given that they are observed under different Monte Carlo simulation settings – for Retail and Corporate portfolios, as well as for different phases of the economic cycle. The effect of introducing correlation between LGD and EAD is also analyzed. The implications of the findings presented in this article range from policy actions to the practical way banks determine LGD, encompassing also issues of level playing field and financial stability. Future research along the lines presented here can be extended to understand and, eventually, shed some additional light on the cyclicality of Basel II.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

INTRODUCTION

The first Basel Accord was a relatively rudimentary method of assigning risk weights (RW) to assets with an exaggerated emphasis on balance-sheet risks, whereas Basel II is much more focused on risk sensitiveness, hence being an important enhancement vis-à-vis the previous framework. As such, Basel II is also much more demanding in its implementation than the previous framework. Furthermore, there are still many issues around the correct implementation of the internal ratings-based (IRB) approach. This article examines the potential effects of distinct interpretations of the current EU regulatory framework (CRD)Footnote 1 under different assumptions with regard to the Loss Given Default (LGD) measurement and also the correlation between Exposure at Default (EAD) and LGD.

We demonstrate that the different ways of determining LGD can cause large deviations in the regulatory capital requirements calculated by financial institutions under certain interpretations and correlation specifications (see Schuermann2 for a comprehensive survey on LGD). This is because loss distributions for credit risk are very sensitive to correlation assumptions. Moreover and to complicate, the EU regulatory framework (CRD) allows two different interpretations of ‘default weighted average’ in the LGD definition, namely, count-weighted average or value-weighted average.

Count-weighted average refers to determining LGD by considering the total loss divided by the number of defaults, which implies that each default is given the same weight (1/n, where n is the total number of defaults) in the LGD calculation. By contrast, when value-weighted average is used, each default is given a weight equal to its EAD divided by total EAD in the LGD calculation. As shown in this article, this can lead to quite different LGD calculations.Footnote 2

The EU regulatory Directive 2006/48/EC, in its Annexure VII, Part 4, paragraph 73 refers to the fact that, for retail exposures, ‘(…) institutions shall estimate LGDs by facility grade or pool on the basis of the average realised LGDs by facility grade or pool using all observed defaults within the data sources (default weighted average)’. That is, it refers clearly to the default-weighted average but is ambiguous as to whether it means count-weighted average or value-weighted average. Nothing is said with regard to corporate exposures.

In practice, because of potentially distinct interpretations of the regulatory framework, expected losses may be determined differently by financial institutions in different jurisdictions, which can undermine the level playing field envisaged by the CRD. Curiously, some supervisory authorities tried to ‘compensate’ this lack of regulatory orientation when transposing CRD to their national framework (for example, UK-Financial Services Authority (FSA)4 and Banco de España5).Footnote 3

The different possible interpretations of ‘default weighted average’ do not have a significant impact if, indeed, LGD and EAD are uncorrelated. However, existing research and empirical evidence are equivocal with respect to the existence of correlation between EAD and LGD. Some former papers7, 8, 9 suggest that EAD and LGD are to a large extent uncorrelated, whereas more recent research,10, 11 based on better quality data, points to the existence of different degrees of correlation. Recall that the assumptions and tests conducted by the Banking Committee on Banking Supervision for Basel II calibration were produced with data from years before 2005, a period for which data quality can be challenged.

In this article, both possibilities (correlated and uncorrelated EAD and LGD) were considered in the Monte Carlo simulations as there are good arguments for both cases. One possible explanation for the mixed evidence regarding the correlation between EAD and LGD is that the relation between the two can be non linear, namely in the Retail portfolio. This could be the case if there is a high LGD for both low and high EAD (and a low LGD for intermediate EAD) as is often observed in practice. The underpinnings of this behaviour may well lie in the obligor assuming that, if the EAD is low, there will be no serious consequences in defaulting, whereas if the EAD is high, the obligor may feel that he will not be able to pay off his debt. If this last effect prevails, then a positive correlation between EAD and LGD will be observed.

In order to understand the significance of this subject in terms of regulatory capital requirements, the simulations presented in this article are quite comprehensive comprising different portfolios, macroeconomic conditions and degrees of correlation between EAD and LGD. A further note to clarify that the findings herewith are independent of the model used to determine LGD as the simulations are not built around any specific model. Instead, the simulations consider the observed losses for the obligors in a portfolio. The assumption being that irrespective of the model used by the bank it will give accurate LGD estimates. Under this assumption, it suffices to look at the observed LGD in a portfolio as any model that has been approved by the supervision authority is expected to track well the observed LGD. This fosters the generality of the findings in that they carry on irrespective of the type of model used by the financial institution to determine LGD.

The remainder of the article is structured as follows. ‘Methodology’ section puts forth the methodology by explaining the different Monte Carlo simulations and lays down the rationale for constructing them. ‘Results’ section presents the main results obtained and highlights the impact of the different assumptions on loss calculation and regulatory capital requirements. Finally, ‘Conclusion’ section summarizes the main findings and discusses policy implications and possible solutions to the issues identified.

METHODOLOGY

This part of the article presents a set of Monte Carlo simulations designed to understand the impact on loss calculation and RW, and consequently, on the regulatory capital requirements by considering different interpretations of ‘default weighted average’. Recall from ‘Introduction’ section that the CRD wording permits that ‘default weighted average’ be interpreted as both count-weighted average or value-weighted average.

The simulations have been structured so that they replicate observed characteristics of Retail and Corporate portfolios in terms of EAD distribution as well as its average, maximum and minimum values.Footnote 4 In addition, two different macroeconomic scenarios were assumed – the first corresponding to an economic downturn; and the second representing ‘normal’ economic conditions. The change in the number of defaults for each of the different economic scenarios was also taken into account in the simulations.

In terms of LGD, empirical evidence suggests that its distribution is bimodal, that is, recoveries are either quite high or very low.2 This empirical evidence is captured in the simulations by assuming that LGD follows a ‘mixed’ distribution implying that the loss amount can result from a LGD distribution with a high mode (distribution 1) or from a LGD distribution with a low mode (distribution 2). The ‘mixing’ proportions (that is, the percentage of defaults that follow distribution 1 or 2 in each of the economic backgrounds) are also parameterized so that they approximate reasonably actual LGD distributions.2, 13

Putting all of the above together shows that the simulations presented in this article are quite comprehensive in that they comprise different portfolios, macroeconomic conditions and degrees of correlation between EAD and LGD. All in all, the simulations cover eight scenarios (see Figure 1).

Scenarios considered in the simulations.

Overall, assumptions considered both for the portfolio characteristics and for LGD seem reasonable and are representative of a number of ‘real life’ portfolios that can be found in banks. However, as the simulations are fully parameterized, other sets of assumptions can also be tested, if need be, which will allow an understanding of the issue at hand in settings different from the ones foreseen in this article. Moreover, this methodology also allows for testing many types of scenarios and stress-testing bank capital requirements, subjects of the utmost importance in an economic downturn period.

The characteristics assumed for the EAD distribution for both portfolios (Retail and Corporate) are summarized in Table 1. This table also contains the number of defaults in each of the portfolios, for the different economic settings.

EAD figures have been generated from a lognormal distribution14, Footnote 5 with quantiles limited to the interval [0.0001; 0.9999] to avoid extreme values that could blur the simulation's results by introducing outliers in the analysis. Figures 2 and 3 depict the empirical distribution of EAD based on the abovementioned assumptions.

EAD empirical distribution for Retail portfolio.

EAD empirical distribution for Corporate portfolio.

Table 2 presents the main inputs used to obtain LGD values. These values have been generated from Beta distributions with the approximate modal values shown in the top panel and the ‘mixing’ proportions put forth in the bottom panel.Footnote 6

For example, the Retail portfolio in this experiment is expected to have, in a downturn, either 90 per cent (distribution 1) or 11 per cent (distribution 2) loss and there is a 45 per cent probability that a given obligor will follow distribution 1 and, conversely, a 55 per cent probability that it will follow distribution 2. Figure 4 shows the empirical distribution of LGD for both portfolios (Retail and Corporate), considering the abovementioned assumptions.

LGD empirical distribution (no correlation with EAD).

The economic downturn scenario is based on a deterioration of the portfolio characteristics, although this means different things for the two portfolios considered. For the Retail portfolio, it is assumed that a downturn will lead to a slight increase in the number of defaults (11 per cent in absolute terms) and a reduction in the maximum and average EAD. The rationale for this is that, in an economic downturn, banks will shy away from large exposures in the retail segment especially when they tend to be unsecured, which is often the case in this segment (or when the collateral's value tends to decrease as is the case with the housing market in a downturn).

For the Corporate portfolio, it can be expected that an economic downturn will generate a larger increase in the number of defaults (20 per cent in absolute terms) and an increase in the minimum and average EAD. The reasoning for this is that an economic downturn usually impacts more strongly smaller and younger companies, which tend to have smaller exposures. Hence, in an economic downturn, banks can be expected to be stricter in operations involving those companies than in operations with larger and well-established companies.

With regard to the correlation between EAD and LGD, there is less consensus about its existence, let alone the intensity of the relationship between the two variables. This being the case, it was deemed necessary to allow for both possibilities in the simulations. First, because there are sound arguments for both cases and, second, to understand how introducing correlation between EAD and LGD would impact the results. As no LGD model is considered in the simulations (given that they refer to the observed LGD as explained in the ‘Introduction’ section), we assume that a correctly specified (and approved by the supervision authority) LGD model will yield correlation between EAD and LGD if it exists.Footnote 7 For the ‘correlated’ scenario, it was assumed that the intensity of the correlation was mildly strong (0.5) and that the sign of the correlation was positive for the Retail portfolioFootnote 8 and negative for the Corporate portfolio.Footnote 9

In Figures 5 and 6, it is possible to see the impact of the introduction of correlation between LGD and EAD on LGD distribution. When LGD and EAD are uncorrelated (Figure 5), the bimodality is clear in that the LGD distribution is determined essentially by the ‘mixing’ proportion (for example, the higher the ‘mixing’ proportion associated with LGD distribution 1 – high mode, see Table 2 – the higher the concentration around that point). When LGD and EAD are correlated (Figure 6), the bimodality is somewhat smothered given that the LGD distribution is driven to a large extent by the degree of correlation.

LGD empirical distribution (correlation with EAD).

Loss difference for alternative LGD definitions (no correlation between LGD and EAD).

RESULTS

Given the assumptions abovementioned, a set of 1000 simulations were generated in order to understand the differences induced by the two LGD definitions (that is, by the two different interpretations of ‘default weighted average’ – count-weighted or value-weighted) allowed for in the CRD in terms of loss estimate and regulatory capital requirements.

Figures 7 and 8 show the difference in the loss for the eight scenarios considered. The first noteworthy result is that (both for Retail and Corporate portfolios) if LGD is uncorrelated with EAD, both interpretations of ‘default weighted average’ lead to approximately the same results. This is seen in Figure 6, where the distributions are centred approximately at zero and have a small standard deviation (note that the scale ranges from −2 to 2 per cent). These findings may explain the lack of orientation presented by Basel II.

Loss difference for alternative LGD definitions (LGD correlated with EAD, Retail).

Loss difference for alternative LGD definitions (LGD correlated with EAD, Corporate).

However, when LGD is mildly correlated with EAD, the two possible interpretations of ‘default weighted average’ lead to quite different results. For the Retail portfolio (Figure 7), if count-weighted LGD is considered, it can lead to significant loss underestimation of Circa 25 per cent, but can be as large as 34 per cent. For the Corporate portfolio (Figure 8), count-weighted LGD seems to be slightly more conservative than value-weighted LGD, in that, it results in loss overestimation of approximately 6–7 per cent.Footnote 10 Thus, in terms of regulatory capital requirements, when EAD and LGD are correlated, significant loss underestimation or overestimation can be observed, depending on the interpretation of the ‘default weighted average’ being considered. Evidence supporting the possibility of a correlation between EAD and LGD increasing the effect of the business cycle on regulatory capital requirements has also been found by Altman21 through Monte Carlo simulations.Footnote 11

In comparison, the value-weighted average seems to lead to more accurate loss quantification because of lower LGD underestimation and overestimation.

Another interesting point can be observed in Figures 7 and 8 (for the scenarios in which LGD is correlated with EAD, and maintaining the level of correlation equal to the normal economic scenario): in an economic downturn, the distribution of the difference in loss between count-weighted and value-weighted LGD shifts slightly towards zero, which suggests that in an economic downturn the differences between the two LGD definitions decrease. This is because of the fact that in an economic downturn, the average value of the individual exposures tends to decrease in Retail portfolios (higher unsecured exposures) and increase in Corporate portfolios (less loans to small- and medium-sized enterprises).

These findings suggest the existence of a somewhat ‘counter-cyclical’ factor in the loss calculation and in the regulatory capital requirements, independently of the interpretation of ‘default weighted average’, when constant correlation (between LGD and EAD) throughout the economic cycle is assumed. However, correlation tends to be different according to the phase of the macroeconomic cycle hence the differences in the loss calculation may even increase generating higher loss underestimations or overestimations. Given the complexity of this matter, further investigation would be warranted in order to determine the robustness of this finding.

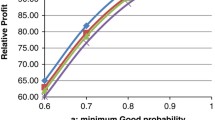

Figures 9, 10, 11 and 12 depict the RW for the ‘average’ exposure in each of the scenarios considered in the simulations for different Probability of Default (PD) levels, considering a broad enough PD range to be relevant to most ‘real life’ portfolios. The RW curve is determined according to Basel II formulas.Footnote 12 As those figures show, considerable differences exist in the RW for the different macroeconomic conditions and portfolios. As expected, different LGD figures shift the RW curve, for different PD levels, up or down. Given the extent of the LGD values resulting from different interpretations of ‘default weighted average’, the differences in RW can be up to fourfold.

Impact in RW for different PD levels (Retail, no downturn).

Impact in RW for different PD levels (Retail, downturn).

Impact in RW for different PD levels (Corporate, no downturn).

Impact in RW for different PD levels (Corporate, downturn).

CONCLUSION

The Monte Carlo simulation exercise herewith shows that the way ‘default weighted average’, in the LGD regulatory definition, is interpreted can lead to significantly different results in terms of LGD calculation and regulatory capital requirements. In fact, if it is interpreted as count-weighted average, and if LGD is correlated with EAD, the simulations show, for different scenarios, that the resulting LGD does not lead to accurate loss quantification.

This makes a strong case for interpreting ‘default weighted average’ as value-weighted average instead of count-weighted average since the former always leads to accurate loss quantification. However, the EU supervisory rules are not clear. As banks can consider different interpretations, a case could be made for the need to clarify that count-weighted average can only be used if the bank can demonstrate to the banking supervisor's satisfaction that LGD is uncorrelated with EAD. In order to increase the transparency of the assumptions, the type of default-weighted average used in the LGDs should also be publicly disclosed by banks for each of the portfolios.

In terms of practical LGD quantification, the findings presented in this article suggest that value-weighted LGD should be preferred by banks when determining LGD. Furthermore, given that correlation between LGD and EAD can bias LGD, a case could also be made in favour of the need to segment LGD by EAD (as a practical way to eliminate or, at least, strongly reduce, correlation, hence increasing LGD and loss calculation accuracy). Again, the generality of the findings presented in this article should be highlighted in that no specific LGD model is assumed in the simulations.

With regard to policy actions, it can be argued based on these findings that the precise interpretation of ‘default weighted average’ should be further clarified in the regulatory framework as well as the conditions in which count-weighted average can be used. In addition, given that LGD segmentation (by EAD) can be an efficient practical way to reduce potential correlation with EAD, further guidance could be issued to encourage banks to segment their portfolios, for LGD calculation purposes, thus improving the accuracy of the models. This is something that regulators should bear in mind when conducting the validation of LGD estimations to be used by financial institutions for regulatory capital calculation under the IRB approach.

Moreover, the potential overestimation or underestimation of the regulatory capital requirements, considering different interpretations of the regulatory framework and the phase of the business cycle, undermines the desired level playing field and increases the difficulty of distinguishing structural from idiosyncratic shifts in key risk variables such as LGD and EAD. This situation introduces a greater risk that authorities miscalculate the evolution of the early warning risk indicators and aggregated risks within the financial system with negative consequences in terms of financial stability.

Notes

Directive 2006/48/EC (banking book) and Directive 2006/49/EC (trading book), commonly referred to as Capital Requirements Directive (CRD).

Besides count-weighted and value-weighted averages, the EU-regulatory framework could also be interpreted as meaning time-weighted average although this possibility has been dismissed since it would ‘smooth out’ good and bad years, which is something definitely not intended by the regulation. For a more in-depth discussion of the possible interpretations of ‘default weighted average’ see Schuermann2 and FSA4.

The FSA determines, in its regulation (BIPRU), that LGD has to be calculated using count-weighted average, even though in one of its papers (see FSA4) it allows LGD to be calculated using value-weighted average. In Spain, Banco de España has eliminated from its CRD transposition the reference to ‘default weighted average’ which arguably gives Spanish banks even more leeway to determine LGD as they see fit (see Moral5 for a study on different ways of determining loss for a mortgage portfolio).

In the absence of detailed and thorough studies on EAD distribution, fairly conservative and generic assumptions have been assumed so that the simulations can be representative for most ‘real life’ Corporate and Retail portfolios. The assumptions comprise a level of concentration around small values and the possibility of a few large values existing in the portfolio.

For alternative – Gamma and Inverse Gaussian – EAD distributions see Jimenez14.

Other studies also consider the Beta distribution to approximate the distribution of LGD – see Jimenez,14 for example.

Even though, as noted below, if the model used by the financial institution is adequately segmented, the degree of correlation may be mitigated, especially within each of the segments.

The rationale being that unsecured exposures comprise the most part of the obligors in the Retail portfolio and as such the larger the exposure amount the harder it will be for the bank to recover the whole defaulted amount. For secured exposures it can be argued that this reasoning is not so clear cut; nevertheless, it will be retained to simplify the analysis.

The reasoning for a negative correlation between LGD and EAD in the Corporate portfolio rests on two underlying stylized facts that can be observed in many banks. First, that corporate exposures tend to have larger values than retail ones implying that they are more closely monitored by the bank. Second, that the higher the corporate exposure the more collateral will be required by the bank hence making large recoveries more likely in this portfolio.

Other simulations conducted (not shown) suggest that the stronger the degree of correlation between LGD and EAD, the larger will be the difference between loss estimates based on count-weighted LGD or on value-weighted LGD.

Altman21 also conduct a set of Monte Carlo simulations that show that if default rates and recovery rates are correlated, across the business cycle, both expected and unexpected loss can be vastly understated. Note that the focus of that paper is on the need for models to carefully factor in the correlation between default rates and recovery rates across the business cycle.

Corporate portfolio: See PDF version for display of equation

For more information on the regulatory formulas see Directive 2006/48/EC, Annexure VII, Part 1.

References

Schuermann, T. (2004) What do we know about loss given default? In: D. Shimko (ed.) Credit Risk Models and Management, 2nd edn. London, UK: Risk Books.

FSA – Financial Services Authority-UK. (2005) Own estimates of loss given default. Expert Group paper on Loss Given Default.

Moral Turiel, G. and García Baena, R. (2003) Estimación de la severidad de una cartera de prestamos hipotecarios. Banco de España Estabilidad financiera 3: 127–164.

Asarnow, E. and Edwards, D. (1995) Measuring loss on defaulted bank loans: A 24-year study. The Journal of Commercial Lending 77 (7): 11–23.

Carty, L. and Lieberman, D. (1996) Defaulted Bank Loan Recoveries. Moody's Special Report 20641 : 1–12.

Thornburn, K.S. (2000) Bankruptcy auctions: costs, debt recovery, and firm survival. The Journal of Financial Economics 58: 337–368.

Dermine, J. and Neto de Carvalho, C. (2008) Bank loan-loss provisioning, central bank rules vs. estimation: The case of Portugal. Journal of Financial Stability 4 (1): 1–22.

Grunert, J. and Weber, M. (2009) Recovery rates of commercial lending: Empirical evidence for Germany. Journal of Banking & Finance 33 (3): 505–513.

Dermine, J. and Neto de Carvalho, C. (2006) Bank loan losses given default – A case study. Journal of Banking & Finance 30: 1219–1243.

Jimenez, G. and Mencia, J. (2007) Modelling the Distribution of Credit Losses with Observable and Latent Factors. Documentos de trabajo no. 0709, Banco de España.

Altman, E.I., Brady, B., Resti, A. and Sironi, A. (2004) The link between default and recovery rates: Theory, empirical evidence, and implications. The Journal of Business 78 (6): 2203–2228.

Acknowledgements

We are grateful for the comments made by Alnoor Bhimani, (LSE-London School of Economics), Mohamed Azzim Gulamhussen, (ISCTE-Lisbon University Institute) and Francisco Covas (Fed). We are also grateful to some colleagues for their comments and suggestions. The views stated herein are those of the authors and are not necessarily the views of the European Central Bank or of Barclays Bank, plc.

Author information

Authors and Affiliations

Corresponding author

Additional information

2has an extensive experience in modelling with a particular focus on Probability of Default, Loss Given Default and Exposure at Default models and an in-depth knowledge of Basel II acquired both as a banking supervisor (at Bank of Portugal) and as a modeller (in Barclays Bank, plc, Portfolio Predictive Modelling Team). He received his master's degree in Applied Econometrics and Forecasting from the ISEG-University Institute in Lisbon.

Rights and permissions

About this article

Cite this article

Lopes, SR., Nunes, T. A simulation study on the impact of correlation between LGD and EAD on loss calculation when different LGD definitions are considered. J Bank Regul 11, 156–167 (2010). https://doi.org/10.1057/jbr.2010.7

Published:

Issue Date:

DOI: https://doi.org/10.1057/jbr.2010.7