Abstract

Does transnational anti-bribery enforcement affect the risk-mitigation strategies of firms? This paper uses an original dataset on the enforcement actions of the Foreign Corrupt Practices Act (FCPA) to examine the law’s impact on corporate behavior and political risks for multinational corporations (MNCs). I argue that corrupt institutions are not necessarily undesirable for foreign investors. Foreign firms seek above-normal returns in high-risk markets through informal exchanges with the host government. FCPA enforcement provides a “fire alarm” that affects firms differently given their sensitivity to corruption concerns. FCPA enforcement has unequal deterrence against corporate misconduct, encouraging some firms to adopt transparency norms while incentivizing other firms to be more insidious in their corrupt business practices. I use a partial observability bivariate probit model to estimate the unobservable propensity of firms to engage in corrupt exchanges. Then I examine the impact of FCPA enforcement on Chinese FDI, and find that Chinese investments are deterred from markets with robust legal institutions. The FCPA’s deterrence effects against corrupt competitors is a positive outcome for U.S. MNCs. However, American companies experience diminished returns in countries with strong investor protection regimes. External legal interventions under the FCPA generate regulatory burdens on U.S. that limit their business opportunities.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Multinational corporations (MNCs) are usually confronted with two types of institutional risks when operating abroad. First, there are potential risks of expropriation by local state and non-state actors, especially in countries that lack strong legal protection of investor rights. Second, host country governments impose strict regulatory requirements over certain industries, creating obstacles for MNCs to enter and operate in those industries.

The prevailing view in the international political economy literature is that investors are deterred from entering markets with high expropriation risks and weak judicial institutions (Li and Resnick 2003; Jensen 2003, 2008; Moon 2015; Wellhausen 2015; Allee and Peinhardt 2011). The assumption is that when investor rights protections are weak, foreign firms expect to receive only discounted (if not negative) investment returns on their assets, which creates the needs for other substitutive rights protection mechanisms such as bilateral investment treaties (Jensen 2003; Büthe and Milner 2014; Arias et al. 2017; Tobin and Rose-Ackerman 2011). It is also the common view that when the host government institutes regulatory restrictions and market entry barriers against foreign firms, it creates unnatural monopoly rents for local producers and disincentivizes foreign firms to engage in local operations (Boddewyn 2015; Rowley et al. 2013; Hillman 2013; Boldrin and Levine 2013; Aligica and Tarko 2012). Such policies are expected to reduce financial returns to investors by denying them access to profitable opportunities, and thus the benefits of remaining in the market are insufficient to justify and compensate for potential expropriation risks.

However, we still observe large amounts of foreign investments flowing into high-risk countries that lack a rule of law and tolerate rampant predations against foreign enterprises. The industries MNCs operate in are often characterized by high barriers to entry, substantial risks of illegal takings, discriminatory and arbitrary enforcement of regulations, and myriad contractual uncertainties. Hajzler (2012) documents expropriation of foreign direct investment (FDI) across all developing countries from 1993 to 2006. He compares the sectoral distribution of FDI of recent expropriating countries to that of non-expropriating countries, and finds a puzzling fact that average resource-based FDI shares are higher in expropriating countries. It means that, compared with countries that do not expropriate, countries which are more likely to expropriate attract a larger proportion of FDI in historically high-risk industries such as resource-based sectors (particularly in mining and petroleum). Another example is the heavily regulated financial industries in China.Footnote 1 The Chinese government limits the share of foreign ownership of financial institutions, asset managers, and security brokerages, and frequently imposes restrictions on foreign firms’ profits repatriations and currency exchanges.Footnote 2 Nevertheless, in spite of the recent slowdown of the Chinese economy and trade tensions between investors’ host and home countries, foreign corporations such as JP Morgan and Goldman Sachs keep expanding their business presence in the Chinese market.Footnote 3

This leads to a puzzle that has not been addressed by the existing literature: why do MNCs have incentives to invest in business environments with significant threats of expropriations, especially in industries featuring high regulatory barriers? I argue that corrupt institutions in host countries work both ways: on one hand, they incentivize opportunistic behavior such as predations against investors and generate monopoly rents enjoyed by vested interests and regime insiders; on the other hand, the arbitrariness in such institutions make them malleable and vulnerable to influences of informal exchanges. By exploiting the dual nature of weak institutional environments, MNCs are able to profitably navigate political risks in countries that are traditionally viewed as unsafe for foreign investment.

One observable implication of MNCs adopting informal risk-mitigation strategy is the rise of transnational corruption. In Brazil, MNCs make illicit payments to officials of the government and political parties in order to evade taxes and to influence the enactment of legislation that would negatively impact firms’ business.Footnote 4 In Nicaragua, the American telecommunications company BellSouth Corporation made improper payments to the wife of the Nicaraguan legislator who was the chairman of the Nicaraguan legislative committee with oversight of Nicaraguan telecommunications. BellSouth retained her in 1998 to lobby for the repeal of the foreign ownership restriction, and in 1999 the Nicaraguan National Assembly voted to repeal the foreign ownership restriction.Footnote 5 In Nigeria, Willbros Group made corrupt payments to officials of the Nigerian judicial system in exchange for favorable action on pending cases, including in some instances dismissal of a case affecting the business of the Willbros Nigerian subsidiaries.Footnote 6 In Uzbekistan, Telia Company paid bribes to an Uzbek government official who exercised influence over Uzbek telecommunications industry regulators in order to enter the Uzbek telecommunications market, gain valuable telecom assets, and continue operating in Uzbekistan.Footnote 7 In India, Pride Forasol made payments to a judge with India’s Customs, Excise, and Gold Appellate Tribunal (“CEGAT”) to secure a favorable judicial decision for Pride India relating to a litigation matter pending before the official involving the payment of customs duties and penalties assessed for importing a rig.Footnote 8 However, navigating the political risk landscape in the host market through informal dealings with officials engenders another source of legal hazard: the risk of transnational anti-bribery sanctions. A host of national, regional, and international anti-corruption legal mechanisms have been set up to combat transnational bribery activities (De Sousa 2010). Several prominent initiatives are the United States Foreign Corrupt Practices Act (FCPA), the OECD Anti-Bribery Convention (OECD Convention), the United Nations Convention Against Corruption (UNCAC), the Inter-American Convention Against Corruption (IACAC), and the African Union Convention on Preventing and Combating Corruption (AU Convention).

By many measures, the United States has been an exceptionally diligent participant in international anticorruption efforts through its robust enforcement of the FCPA (Davis 2009). Transparency International has classified U.S. enforcement actions against foreign bribery as “active enforcement” (the highest category) since the beginning of the records (International 2016; OECD 2014). Data from the OECD Working Group on Bribery also shows that the U.S. leads the rest of the Parties to the OECD Convention in the number of investigations, legal dispositions, and sanctions against both individuals and legal persons.Footnote 9

The FCPA criminalizes the payment of bribes to foreign officials or any government instrumentalities for the purpose of obtaining or retaining business. The existing literatures focuses on two interrelated questions in assessing the law’s effectiveness (Krever 2007). First, has the FCPA deterred U.S. corporations from making corrupt foreign payments? Second, has active enforcement of the FCPA hurt American firms’ investment and competitiveness in foreign markets where bribery is a common practice (Salbu 1997; Cuervo-Cazurra 2008; Smarzynska et al. 2000)? I argue that the existing literature on the impact of the FCPA has suffered from two limitations. First, given the secretive nature of corrupt exchanges, it is difficult to empirically examine changes in corrupt behavior after external legal interventions. Second, given that corrupt institutions can work both ways for MNCs, anti-bribery enforcement may increase as well as decrease investment risks for MNCs at the same time. On the one hand, firms benefit from anti-corruption deterrence when they regain market shares lost previously to competitors offering higher bribes. On the other hand, firms suffer from anti-corruption deterrence when they are no longer able to maintain market advantages and mitigate expropriation risks by using illegal side payments.

This paper tries to address these methodological and theoretical limitations. Firstly, I use the partial observability bivariate probit model to estimate the effects of FCPA enforcement on firms’ likelihood of paying bribes (Poirier 1980), taking into account that firms generally refuse to disclose their illicit activities in answering surveys. Second, I examine the FCPA’s impact on foreign direct investment flows from China, a major exporter of under-regulated cross-border business activities. I show that transnational anti-bribery enforcement discourages Chinese FDI from flowing to countries with low levels of corruption and high levels of judicial independence. Third, I investigate whether FCPA enforcement benefits or hurts American companies’ performance in the global market. I find that FCPA enforcement improves the operating outcomes for US multinational enterprises in countries with high risks of expropriations and intellectual property theft. However, in markets with strong legal protections of investor rights, US firms are more sensitive to potential risks of transnational liabilities, which ties the hands of US firms in seeking restrictive business opportunities and makes their business operations less profitable than without FCPA scrutiny.

The paper is organized as follows. The next section lays out my argument that corrupt institutions can present themselves as both risks and opportunities for foreign investors. Then I propose my hypotheses on the FCPA’s “fire alarm” effect and its uneven impact on MNC activities, conditional on the legal-institutional constraints of MNCs’ home and host countries. Notably, U.S. firms can benefit from FCPA enforcement but can also be put into a situation of double jeopardy. The empirical analysis provides support for my hypotheses. The robustness checks further demonstrates how the FCPA disrupts the underlying dynamics of corruption and risk-mitigation strategies. The final section concludes.

Theory

Corrupt institutions as a curse and a boon

MNCs face a variety of institutional risks when investing in foreign markets, especially in jurisdictions with weak institutional protections of investors’ rights. Kesternich and Schnitzer (2010) examines different types of political risks faced by MNCs, including outright expropriation or nationalization, creeping expropriation such as a lack of protection for intellectual property rights, unreliable contract enforcement, or particular regulatory requirements directed at foreign multinationals, and policies that directly affect investment profits, such as discriminatory and confiscatory taxation, demands for bribery, and blocking of profit repatriation.

When host country institutions are not able or willing to protect investor rights and enforce contracts, MNCs face significant ex post investment risks because of the hold-up problem and their “obsolescing bargain” with host governments (Vadlamannati 2012; Brouthers and Brouthers 2003; Eden et al. 2005). The government can easily expropriate immobilize assets without adequate compensations (Konrad and Kovenock 2009; Andonova and Diaz-Serrano 2009; Vahabi 2016). MNCs may also lose their proprietary technologies or other knowledge-based assets and competencies through imitations or outright theft (Luo 2001; Chiao et al. 2010; Chang et al. 2013; Brouthers and Brouthers 2003; Liebeskind 1999). A large body of evidence has shown that foreign companies are oftentimes victims of their local business partners’ opportunistic behavior that deprives MNCs’ of their competitive advantage in technology, R&D capabilities, or other firm-specific assets (Roy and Oliver 2009; Hennart et al. 1999; Case et al. 2007; Delios and Henisz 2000; Luo 2005; Guillén 2003; Osland and Cavusgil 1996; Zhang et al. 2007; Chew 1993).

Moreover, corrupt institutions establish unnatural barriers to market entry. Discriminatory regulations that discourage the entry of new firms create industrial concentration, which in turn stimulates long term profitability for established crony firms (Luo 2001; Morschett et al. 2010). In developing countries, the degree of entry barriers is shown to be associated with the amount of monopoly rents available in that industry (Zhu and Deng 2018; Malesky et al. 2015). It is common among developed economies as well that the government can create rents by cartelizing private producers (Stigler 1971; Acemoglu 2008), especially when the institutions are weak (Mitton 2008). It has been shown that when government uses regulatory policies to create market entry barriers, competition is decreased and the amount of profits to be shared among market incumbents increases (Djankov 2009; Blanchard and Giavazzi 2003; Hillman 2013; Alder et al. 2014; Maijoor and Van Witteloostuijn 1996; Rose 1987; Djankov et al. 2002; Degryse and Ongena 2008; Black and Strahan 2001; McChesney 1987).

The resource-based view of investment strategies often points to the mode of market entry as a means of overcoming institutional inefficiencies. It is found that joint venture (JV) partnerships provide useful resources for foreign investors to navigate high environmental uncertainties. The JV local partner can help MNCs increase market access, obtain country- specific knowledge and resources, overcome government restrictions, and mitigate operational and political risks (Meyer et al. 2009a; Chen and Xu 2023; Lu and Beamish 2006; Pan and David 2000), especially when the cultural distance between FDI home and host countries is high (David et al. 1997). Chen and Hennart (2002) find that Japanese investors facing high market barriers in the target industry are more likely to choose joint ventures than wholly owned subsidiaries. When the local institutional framework is weak, resources held by the local firm such as permits and licenses for operation are especially valuable for foreign investors facing idiosyncratic regulatory restrictions (Meyer et al. 2009b). The local partner’s operating privileges help MNCs gain legitimate rights to conduct business in restrictive regulatory environments (Yiu and Makino 2002). Puck et al. (2009) find that when the perceived external uncertainty (including political and legal risks) or the complexity of government regulations for foreign firms is high, MNCs were less likely to convert from JV to WOE even if they had the choice. Luo (2001) also finds that the level of governmental intervention and environmental uncertainty as perceived by MNC managers are positively associated with the probability of choosing the joint venture mode. Morschett et al. (2010) similarly show that country risk is positively associated with cooperative entry modes, such as JV, rather than wholly owned subsidiaries.

The essence of the resource-based argument is that the source of competitive advantages of JV over WOE derives from the fact that local linkages and personal connections are very important in FDI activities (Chen et al. 2004; Davies et al. 1995). A major motivation for establishing JV is to utilize the political influence and support of domestic firms (Henisz 2002). More broadly, we can infer that when firms are not able to establish political ties with local authorities via certain corporate structures, they may adopt other informal risk-mitigating strategies to obtain and retain businesses. One of such alternatives is bribery.

It is commonly found that multinational enterprises offer things of personal value to local officials in exchange for favorable policies or administrations thereof. Considering that the legal systems in emerging economies are generally more susceptible to undue influence and manipulation than in developed markets, absent external legal constraints, MNCs should prefer informal channels to resolve their claims with government officials over pursing costly and cumbersome formal actions such as litigation.

Malesky et al. (2015) argue that foreign firms use bribes to enter protected industries in search of rents, and show that bribe propensity varies across sectors according to expected profitability. They find that in restricted sectors that require special licensing procedures, foreign firms contribute to further corruption. Zhu and Deng (2018) argue that firms in fixed-asset intensive industries have strong incentives to bribe government officials in exchange for property rights protections. This is because high fixed asset intensity creates natural entry barriers, thereby giving rise to market concentration and opportunities for MNCs to extract monopoly rents. Furthermore, high fixed assets reduce firms’ ex post mobility, increasing foreign firms’ vulnerability to government officials’ predation and thus the need to build strong political ties. Wright and Zhu (2018) finds that, in the past two decades, much of foreign direct investment in the primary sector has flowed to unconventional, politically-risky destinations. They argue that personalist dictatorships provide an attractive institutional environment for fixed asset investors because the lack of institutional constraints over the dictator enables the leader, who controls key economic sectors, to facilitate rent-seeking activities for foreign investors. They show evidence that personalist dictatorships have significantly more foreign investment in the primary sector than other regimes.

In summary, a corrupt legal and regulatory system can imply greater investments risks for MNCs, in terms of expropriations, access restrictions, and unfair regulatory treatments, as well as greater investment opportunities, in terms of the malleability of government policy and administrations. In the next section, I propose several ways that FCPA enforcement can disrupt the dynamics of transnational corruption.

FCPA enforcement as a fire alarm

The U.S. is by far the most active country in enforcing its law against transnational corruption. U.S. authorities are also increasingly cooperating with their counterparts in developed countries to prosecute such offenses. In order to level the playing field for law- abiding MNCs,Footnote 10 the DOJ and SEC have started to more aggressively target non-US firms’ bribery behavior since the 2010s,Footnote 11 and have shown no sign of abating.Footnote 12 However, there is significant variations in the willingness and capacity of foreign governments to either cooperate with U.S. authorities or to initiate their own legal actions against multinational businesses’ malfeasance. Non-US firms are subject to uneven pressures from legal scrutiny over their business practices (Perlman and Sykes 2018).Footnote 13

The FCPA applies to three types of entities: issuers, domestic concerns, and persons other than issuers or domestic concerns (Guide 2012). An “issuer” is a U.S. or foreign company that has a class of securities traded on a U.S. exchange or an entity required to file reports with the SEC. A “domestic concern” is any business form (or a U.S. citizen or resident) with a principal place of business in the U.S. or organized under U.S. law. A legal or natural person other than an “issuer” or “domestic concern” is subject to the FCPA if the person makes use of any means or instrumentality of interstate commerce in furtherance of an improper payment scheme while in the territory of the U.S. The MNCs not under the jurisdictions of FCPA or other foreign anti-bribery regulations are obviously less constrained from paying bribes. Among the 539 FCPA enforcement actions up till 2017, 390 are against companies headquartered or incorporated in the U.S., 45 are targeting Chinese firms, 37 are against German companies, 35 are against French companies, 42 are against UK companies, 9 are against Japanese companies, 4 are against South Korean companies, and 15 are against Dutch companies. According to a survey of legal and compliance specialists in 824 companies worldwide conducted by the consulting firm Control Risks in 2015/2016, 64 percent of the respondents agreed that international anti-corruption laws serve as a deterrent for corrupt competitors, while 30 percent disagreed.Footnote 14 Recent surveys indicate heightened awareness of the FCPA and other anti-bribery laws among Latin American businesses,Footnote 15 whether the respondents are large corporations operating in high-risk industries or small and medium-sized international enterprises.Footnote 16

I argue that FCPA enforcement has significant deterrent effects on firms’ bribery behavior. FCPA deterrence helps expose the extent of corruption problems in the local business environment, and facilitates greater transparency of corporate misconduct. For some firms, they are encouraged to be more open about unethical business norms in the host market. However, FCPA probes also act as fire alarms that alert some firms to cover up their corrupt practices. Therefore, firms’ perceptions of the level of integrity of the investment environment in the aftermath of FCPA scandals provide nuanced information about the impact of FCPA enforcement. Some companies are more willing to expose corrupt behavior after FCPA interventions, while other companies become more secretive in hiding their illegal dealings. Firms are not incentivized to the same extent to improve transparency and business ethics.

-

Hypothesis 1: FCPA enforcement increases firms’ sensitivity to issues of corruption in the host country and changes the observable patterns of corrupt behavior.

FCPA enforcement as a risk and an opportunity

Many major players in the global investment and trade landscape do not have robustly enforced anti-bribery laws. For instance, China has been accused of being too inactive in transnational enforcement (Lang 2017). From 2014 to 2017, China on average accounts for 10.8% of total global exports. Meanwhile, it has been ranked as”Little or No Enforcement” (the lowest category) in sanctioning its own firms’ overseas bribery by Transparency International.Footnote 17 From 2014 to 2017, China initiated zero investigations or prosecutions of its firms, while the U.S. commenced 32 investigations and concluded 66 major cases with substantial sanctions.

U.S. MNCs have long complained that compliance obligations with the FCPA put them at a competitive disadvantage vis-`a-vis the under-regulated firms. Scholars have also found evidence suggesting that the FCPA will reduce American exports to corrupt jurisdictions and discourage American business activities in bribery-prone markets (Beck et al. 1991; Hines Jr 1995; Graham and Stroup 2016). But the existing literature relies mostly on descriptive statistics and lacks a rigorous empirical methodology. The empirical evidence is also fairly mixed regarding the impact of FCPA on US trade and investments with corrupt countries (Geo-JaJa and Mangum 1999; Borgman and Datar 2012; Graham 1984; Cragg and Woof 2002).

I argue that the inconsistent findings can be explained by the heterogeneous and nuanced responses of firms, which will determine whether the law’s outcomes are positive or negative for MNCs. Firms that are less constrained by their domestic anti-bribery obligations may be able to adjust their investment strategies in response to heightened enforcement risks. Meanwhile, firms constrained by stronger anti-bribery regulations are benefiting from the sanctions imposed on other bribe-payers and, at the same time, suffering from the higher risk of being sanctioned themselves.

U.S. authorities have kept expanding multi-jurisdictional anti-corruption collaboration and coordination with their foreign counterparts (Willborn 2013). Attorneys from the DOJ and the SEC have been building an aligned multinational network of law enforcers with sophisticated legal tools to make it increasingly difficult to engage in foreign bribery with impunity.Footnote 18 The SEC has always been negotiating Memorandums of Understanding (MOUs) with foreign governments in order to establish official channels of cooperation to facilitate obtaining documents from foreign companies (Bencivenga 1997). The DOJ has also signed Mutual Legal Assistance Treaties (MLATs) with foreign law enforcement agencies in order to facilitate its investigation, e.g. to obtain employee testimony.Footnote 19 The Deputy Attorney General Rod Rosenstein recently emphasized the DOJ’s commitment to international cooperation with foreign partners to combat international corruption.Footnote 20

The implication is that in U.S. authorities should find it easier to prosecute and sanction transnational offenders in countries with stronger legal systems due to their greater willingness and capability for inter-jurisdictional cooperation. In contrast, U.S. agencies face greater difficulties in seeking legal assistance from regimes with corrupt judicial systems. Jensen and Malesky (2018) have shown that the peer review procedure implemented by the OECD Anti-bribery Convention generates pressures on OECD member states to discipline corporate misconduct. There is significant variations in the level of enforcement efforts even among OECD member states. Therefore, the U.S.-led initiative may only have limited impact in countries that condone such behavior.

Emergent market MNCs from non-OECD countries, such as Chinese firms, have been frequent perpetrators of transnational corruption schemes (Cuervo-Cazurra 2006). Such bribe-payers should face higher risks of sanctions in countries with robust legal institutions to cooperate with U.S. authorities than in countries that lack a rule of law. As an observable implication, Chinese MNEs should divest from markets with highly independent judicial systems. Meanwhile, the comparative advantages of Chinese MNCs vis-`a-vis their more regulated peers, in terms of the unfettered ability to adapt to corrupt norms (Beazer and Blake 2018), should be diminished by FCPA deterrence. Nevertheless, in countries without strong judicial institutions, FCPA deterrence would still be less costly to their investments given a lack of strong judicial systems to cooperate with U.S. law enforcement in tackling corruption. In such cases, FCPA actions are still able to sanction targets in corrupt jurisdictions and reduce their investment incentives. But greater logistical obstacles imply that the negative impact will be more limited.

-

Hypothesis 2a: FCPA enforcement decreases Chinese FDI into countries with strong legal systems, and the negative impact is smaller in countries with weaker judicial systems and more pervasive corruption.

For the more scrutinized U.S. firms, they benefit from stronger transnational legal deterrence against the dishonest behavior of their competitors. All else equal, FCPA interventions should improve the performances of American companies in markets characterized by pervasive corruption. Meanwhile, although less routinized, U.S. MNCs are also reported to have engaged in bribery activities themselves. Evidence suggests that U.S. firms are not always adopting higher ethical standards of business practices in transition economies (Hellman et al. 2002; Sheffet 1995). Optimists believe that the internationalization of anti-corruption efforts will raise the potential costs of bribery for all businesses and add new momentum to the FCPA’s effectiveness (Krever 2007).

I argue that stronger legal collaborations between US authorities and local law enforcement in developed jurisdictions discourage corrupt business dealings and illegally-obtained investment opportunities of U.S. MNEs. In industries characterized by high technological barriers and significant asset-specific investments, some incumbent American companies need to engage in corrupt regulatory capture to build and sustain rent-seeking capabilities in the market (Boldrin and Levine 2002, 2013; Sell et al. 2003; Kirkpatrick et al. 2006; Hanna 2010). FCPA enforcement disrupts the profitable yet illegitimate models of business practices when US firms are under dual legal pressures from home and host country governments. Therefore, I expect that FCPA enforcement will, on the margin, negatively impact the performances of U.S. MNCs in countries with strong property rights regimes. Compared with the generally negative impact on Chinese investors (H2a), the key difference is that US MNCs can enjoy positive boost to their performances from FCPA interventions in countries with weak investor protection institutions that would have advantaged unregulated firms.

-

Hypothesis 2b: FCPA enforcement improves the performances U.S. MNCs in countries with weak legal systems and hurts the performances of U.S. MNCs in countries with strong legal systems.

Methodology

Data

The DOJ and SEC publicize all of their FCPA enforcement actions on the government websites.Footnote 21 The Foreign Corrupt Practices Act Clearinghouse (FCPAC) at the Stanford Law School maintains a database of all SEC and DOJ enforcement actions related to the FCPA and is publicly available.Footnote 22 The information for each enforcement action is scraped from the FCPAC website and hand-coded for analysis.

I merged the FCPA enforcement dataset with the World Bank Enterprise Surveys datasetFootnote 23 to examine the effects of FCPA actions on firm behavior. The Enterprise Surveys were administrated to business owners and top executives from a representative sample of firms across all geographic regions, covering small, medium, and large companies. The respondents were asked questions about characteristics of the business environment including topics on corruption, regulations, and licensing. The dataset is a cross-sectional survey with firm as the unit of analysis, covering over 13,000 firms across 139 host countries. It has adopted a uniform global methodology for survey implementation since 2006.Footnote 24 Therefore, survey results after 2006 are comparable.

Data on bilateral investment flows is obtained from the United Nations Conference on Trade And Development (UNCTAD) website.Footnote 25 Information on outward activities of American MNCs is obtained from the Activity of Multinational Enterprises (AMNE) database maintained by the Organization for Economic Co-operation and Development (OECD).Footnote 26 For the country-level control variables, I merged other datasets with the World Economics and Politics (WEP) Dataverse which offers 87 most commonly used data sources in the field of international and comparative political economy (Graham and Tucker 2017).

Dependent variables

To test the first hypothesis, the first set of dependent variables try to measure the impact of the FCPA on businesses’ sensitivity to issues of corruption. The Enterprise Surveys include the following questions:

-

(1)

When establishments like this one do business with the government, what percent of the contract value would be typically paid in informal payments or gifts to secure the contract?

-

(2)

In reference to that application for an operating license, was an informal gift or payment expected or requested?

I also converted responses to the first question to a binary variable which indicates whether any positive value of corrupt payments would be paid. It is shown that 22% of respondents reported positive amounts of informal payments or gifts. To examine the effects of the FCPA on response rates, I created a new binary indicator for whether respondents answered the second question. The result shows that 87% of the surveyed firms directly answered the question instead of refusing to answer or answering “don’t know.”

The second dependent variable is the amount of bilateral Chinese foreign direct investment flows into its partner countries, which is obtained from the UNCTAD database. The third dependent variable is an indicator of the performance of U.S. multinational enterprises. I use two different measurements provided by the AMNE database: gross operating surplus and value added at factor cost.Footnote 27

Independent variables

The primary independent variable is a binary indicator of whether any FCPA enforcement action occurred in a country-year unit of observation. I lag the independent variable by 1 year to take into account the time for the effects of an enforcement action to materialize. The result shows that 27% of the surveyed firms were located in a country in a given year where at least one enforcement action occurred. FCPA probes can be targeting either corporate, personal, or both types of offender(s) of a given country in a given year, and not necessarily against the surveyed firms. The surveyed firms are assumed to be receiving the deterrence signal from FCPA interventions into their own markets. For robustness checks, I also use the total number of enforcement actions for the entire year in a given country as the independent variable, and the results are not affected by using the count measurement.

Control variables

I take into account a wide set of potentially confounding variables to examine the effects of FCPA enforcement on the outcomes of interest. The existing level of corruption in a country is correlated with both the likelihood of receiving FCPA prosecutions and the dependent variables, and therefore must be controlled for to ensure unbiasedness. Corruption is measured by the Political Corruption index from the Varieties of Democracy Dataset.Footnote 28 In the WEP Dataverse, GDP per capita, GDP growth rate, and Population are obtained from the World Bank World Development Indicators; The Level of democracy variable is measured by the Polity IV scores (Marshall et al. 2016). These potential confounders might also be correlated with both the propensity to be targeted in FCPA sanctions and the outcomes of interest on corruption sensitivity, investment flows, and firm performance. For robustness checks, I also control for a country’s total natural resource rents as a percentage of GDP and FDI net inflows as a percentage of GDP, both obtained from the World Bank.Footnote 29

Model

To test the first hypothesis, I firstly run three separate binomial logistic models to examine firms’ responses to sensitive questions on corrupt behavior after FCPA interventions. The models include two-way fixed effects to account for time-invariant country-specific characteristics and also for country-invariant time period effects. This is to ensure that particular features of a country or of a certain year do not bias the estimates of the effects of FCPA enforcement. Considering that responses of firms within the same country are likely to be correlated, I use country-clustered robust standard errors for all models.

Firms’ responses to questions of corrupt payments provide direct information about their behavior, although they suffer from social desirability bias. Given the voluntary nature of the survey, we also want to know the potential responses of firms who chose NOT to answer the surveys. In the aftermath of an FCPA action, the responses of firms who choose to answer sensitive questions and the potential responses of firms who choose not to answer should be systematically different. Therefore, the FCPA’s impact can also be gauged by examining how the external legal intervention changes the potential reactions of those firms who have refused to answer the sensitive questions. However, the obvious methodological challenge is that we cannot obtain the counter-factual knowledge of what the answers of the non-responsive firms would have been if they had chosen to answer the questions.

To address this problem, I use the partial observability bivariate probit (POBP) model to estimate the potential outcomes for those firms who did not answer the sensitive questions (Poirier 1980). The POBP model defines two binary dependent variables Y1 and Y2, each of which take the value of either 0 or 1. I model the joint outcome (Y1, Y2) using two marginal probabilities for each dependent variable, and the correlation parameter, which describes how the two dependent variables are related. The two unobserved latent variables are characterized as:

where E1 and E2 follow a bivariate normal distribution with a correlation parameter ρ. The outcomes for the model are defined as \({Y}_{i}=\left\{\begin{array}{cc}1& \mathrm{if\, }{Y}_{i}^{*}>0\\ 0& {\text{otherwise}}\end{array}\right.\), where i ∈ {1, 2}. In my model, Y1 is the firm’s response to Question (2) and Y2 is whether the firm answered Question (2) at all. A firm’s decisions of whether and how to answer the sensitive question should be correlated and therefore modeled together to examine the underlying causes. Using this approach, I can estimate the effects of FCPA enforcement on the unobservable outcome of (Y1 = 1, Y2 = 0), that is, the likelihood that the firm who did not respond to the question actually made corrupt payments to apply for an license.

To test Hypothesis 2(a), I run two interactive models to examine the conditional effects of FCPA actions on Chinese FDI net inflows into the targeted countries. The first model interacts the independent variable with the degree of judicial independence of the host country, as measured by the latent score of de facto judicial independence constructed by Linzer and Staton (2015). A high level of judicial independence also implies a low degree of corruption because of the ability of strong legal institutions to sanction and prevent corruption. Therefore, if Hypothesis 2(a) is correct, I should be able to see that the responses of Chinese FDI to FCPA enforcement are also conditional on the extent of corruption in the host country. The second model thus interacts the FCPA intervention with the level of corruption in the host country, as an alternative test.

To test Hypothesis 2(b), I use different measurements of the host country’s institutional quality as the conditioning variable to examine the heterogeneous effects of FCPA enforcement on U.S. firms’ performance. I disentangle different aspects of the legal-institutional environment and show how they mediate the impact of FCPA enforcement. Developed economy MNEs often face high risks of intellectual property theft and expropriations without adequate compensation in emerging markets. In the meantime, foreign firms can bribe the predatory officials to mitigate such political risks. Therefore, I examine how the level of corruption, the strength of intellectual property rights protections, and the adequacy of compensation for expropriations affect whether U.S. MNCs benefit or suffer from FCPA prosecutions in the host country. I also explore potential nonlinear dynamics between the independent variable and the conditioning variables.

Results

The fire alarm mechanism

In Table 1, Models (1) and (2) show that, among the firms surveyed in the World Bank Enterprise Survey who chose to answer the questions on corrupt payments, FCPA enforcement in their countries make these firms more likely to confirm illegal practices of their own. In percentage terms, FCPA enforcement causes such firms to be 18 percentage points more likely to disclose bribery behavior for obtaining government contracts, and 12 percentage points more likely to disclose bribery behavior for obtaining operating licenses. Meanwhile, however, the transformed logit coefficient in Model (3) indicates that FCPA enforcement makes surveyed firms to be 9 percentage points less likely to answer the sensitive questions on bribery activities. The results imply that the FCPA is changing the patterns of firms’ observable behavior: it reveals more dishonest behavior among responsive firms who are willing to disclose it, while discouraging other firms to be responsive at all to such sensitive questions. Given the secretive nature of corruption schemes and social desirability biases, we still need to ascertain the actual impact of the FCPA on firms’ potential behavioral patterns that are unobservable.

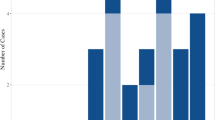

To overcome this methodological challenge, I use the partial observability bivariate probit model to estimate the probability of engaging in illegal exchanges for firms who did not answer the questions. Table 2 and Fig. 1 present the average treatment effects (ATEs) of FCPA enforcement on four potential outcomes. The first potential outcome (Y1 = 1, Y2 = 1) is the scenario where the firm provided a positive answer to the question on informal payments for licensing. The second potential outcome (Y1 = 1, Y2 = 0) is the counter-factual scenario where the firm did not answer the question, but would have provided a positive answer. The third potential outcome (Y1 = 0, Y2 = 1) is when the firm provided a negative answer to the question on informal payments for licensing. The fourth potential outcome (Y1 = 0, Y2 = 0) is the second counter-factual scenario where the firm did not answer the question and would have provided a negative answer. It is used as the baseline group.

Average treatment effects of FCPA enforcement

The results show that FCPA enforcement causes firms to be more likely to admit to their informal business practices. Moreover, in the aftermath of FCPA interventions, those firms that refused to answer the question are even more likely to report having engaged in bribery than firms that answered the question. This indicates that FCPA exposures of individual incidents help reveal the wider phenomenon of insidious corruption schemes in the host country. However, FCPA enforcement also creates a more sensitive anti-bribery environment because the legal alert makes firms who have engaged in misconduct more likely to refuse to report unethical corporate behavior. Interestingly, the effects on the third potential outcome shows that FCPA prosecutions make it less likely (−12.4 percentage points) for firms not to report malfeasance when they choose to answer the survey. It indicates that some firms are more willing to voluntarily disclose their misconduct in surveys because of the FCPA’s exposures. All of the evidence shows that firms have different responses to the FCPA. While some firms are encouraged by FCPA revelations to become more transparent in business practices, other firms become more alarmed and start to engage in more secretive, low-profile forms of corrupt dealings. The findings support Hypothesis 1.

Opportunities and risks

Table 3 shows how FCPA enforcement has greater deterrent effects on Chinese investments in countries with stronger institutional integrity, as measured by the pervasiveness of corruption and the level of judicial independence. Model (1) interacts the FCPA treatment variable with the level of corruption in the host country; Model (2) interacts the FCPA treatment variable with the level of judicial independence in the host country. The coefficients of direct effect and the interactive effect of the two models are expected to be in opposite directions, as higher degrees of judicial independence are usually associated with lower levels of corruption. However, judicial independence is still a relatively noisy proxy of corruption and expropriation risks faced by firms. Therefore, we also explore other measurements of institutional integrity in additional tests.

Table 3 shows that the coefficients of both models are in the expected directions, although we only find significant results for Model (1). The results imply that FCPA enforcement reduces Chinese FDI inflows into the targeted countries with lower levels of corruption, and the negative effects are smaller in more corrupt markets. They imply that FCPA deterrence causes Chinese investors to retreat from markets with robust legal institutions because of stronger legal scrutiny by U.S. and host country authorities. Meanwhile, Chinese investments are less affected by the FCPA when the host economy is characterized by pervasive corruption or weak rule of law institutions that diminish the efficacy of FCPA deterrence.

Next, it is possible that there could be a nonlinear relationship regarding the conditional effects of FCPA enforcement given the underlying institutional environment. Chinese investments are expected to decrease more in countries with stronger institutional control over corruption. Meanwhile, Chinese investments should be less deterred in countries with more pervasive corruption problems where local law enforcement support is weak. Yet, if the corruption problems are so severe that even well-adapted firms find it challenging to operate, FCPA scrutiny should be more effective in deterrence under such high-risk market conditions. The extremely high frequencies of corruption incidents and likelihood of exposure of misconduct will discourage investors who are vulnerable to external legal sanctions.

To examine the potential non-linear relationship, I include a quadratic term of the conditional variable in the regression to estimate the conditional effects of FCPA enforcement. Then, I use LOESS regression to fit a smooth curve through all estimated effects of the FCPA at each value of the conditional variable. In Fig. 2, I present the fitted marginal effects of FCPA enforcement conditional on a set of political risk factors with quadratic relationships. The results suggest that FCPA probes significantly decrease Chinese investments in countries with strong institutions to safeguard governance integrity. Meanwhile, consistent with the expectation, the deterrent effecrts of the FCPA against Chinese FDI are smaller in countries with high levels of corruption or weak judicial systems, although the marginal effects remain below zero. However, Chinese investments are still deterred by the FCPA in jurisdictions with extremely high institutional risks, more so than in the moderately corrupt countries. Overall, the results provide evidence for the limited deterrence with uneven impact regarding FCPA enforcement in weak institutional environments, and lends support to Hypothesis 2a.

The conditional effects of FCPA enforcement on Chinese FDI

The uneven impact of FCPA enforcement on Chinese FDI flows also have important implications for the performances of American businesses. On one hand, the withdrawal of bribe-paying competitors should lead to more business opportunities for law-abiding firms in corrupt markets; on the other hand, given that U.S. firms are already subject to higher compliance requirements in countries with strong legal regimes, the marginal outcome of FCPA scrutiny is additional regulatory oversight that creates more burdens than necessary. Therefore, while FCPA deterrence benefits American businesses in weak institutional environments, it creates unnecessary institutional constraints in countries with high levels of status quo legal compliance. In addition, as mentioned above, it is common practice for firms to pay bribes to circumvent political risks, more enforcement pressure makes it more costly for U.S. firms to navigate risky political and regulatory landscapes through informal channels. Therefore, when the host legal regimes are actively cooperating with U.S. authorities against transnational bribery, American business interests will be negatively affected by the heightened constraints. In such instances, U.S. firms should experience worsened performance.

In Table 4, I examine the conditional effects of FCPA enforcement on the performances of American MNCs, as measured by gross operating surplus and value added at factor cost. I use two indicators from the WEP Dataverse to capture the extent of property rights protection of foreign investors in the host countries: protection of intellectual property rights (IP Protection) and compensation for expropriation (Expropriation Compensation). The coefficients in Table 4 suggest that FCPA enforcement increases US MNC performance in countries with weak property rights protection regimes. Meanwhile, the positive effects turn negative in countries with strong preexisting institutions.

I also explore potential non-linear relationships in the interactive models. Figure 3 visualizes the conditional marginal effects of the FCPA on Gross Operating Surplus of U.S. MNCs, using LOESS regressions. The figures show how the competing effects of FCPA enforcement are manifested out across countries with varying degrees of institutional integrity. The first two graphs show that in countries with inadequate compensations for state expropriations or weak protection of intellectual property rights, U.S. firms are benefiting from transnational legal interventions. This is because the FCPA discourages market competitors from adopting illegal practices to obtain unfair regulatory advantages vis-a-vis American firms. However, in countries with robust legal institutions to protect investor rights, transnational legal scrutiny and requirements create additional regulatory burdens on U.S. firms that are already complying with demanding legal standards. In addition, U.S. firms will not be able to maintain their market privileges and rent-seeking status obtained through informal exchanges. They face heightened legal pressure from joint enforcement efforts by the host and home governments, which disrupts their once profitable modes of businesses. The mechanism is also supported by the third graph using judicial independence as the conditional variable.Footnote 30 The evidence lends support to Hypothesis 2b. Overall, the results suggest that the marginal effects of FCPA interventions are conditional on the different regulatory and legal dynamics and the political risk mechanisms at play across jurisdictions.

The conditional effects of FCPA enforcement on U.S. firm performance

Conclusion

This paper examines the impact of the FCPA on corporate behavior and political risks for multinational enterprises. I argue that corrupt institutions are not necessarily undesirable for foreign investors. Foreign firms are able to gain above-normal returns in high-risk markets when they engage in informal exchanges with the host government. External FCPA enforcement rings the alarm for corrupt actors, causing them to be more sensitive to issues of corruption. Some firms become more willing to expose norms of corrupt business practices in the host country, while other firms become less transparent in their corporate behavior and more reluctant to disclose misconduct. Firms that are benefiting from lucrative opportunities obtained through illegitimate means seem less likely to perceive corruption and regulatory restrictions as business obstacles. FCPA enforcement has unequal deterrent effects on firm behavior, encouraging some firms to adopt norms of transparency while incentivizing other firms to be more insidious in their corrupt business practices.

I use a partial observability bivariate probit model to estimate the underlying propensity of firms to make informal payments for licenses and permits. I find that FCPA interventions reveal that firms that refuse to answer sensitive questions on informal payments are more likely to have engaged in misconduct than firms who choose to answer the questions. Then I examine the impact of FCPA enforcement on Chinese FDI, considering that Chinese firms have been found by U.S. authorities to be frequently participating in transnational corruption. Chinese investments are shown to be more deterred from markets with robust legal institutions that can collaborate with U.S. authorities. The FCPA’s deterrence effects against corrupt competitors is a positive outcome for U.S. MNCs. However, American companies see diminished gains in countries with strong investor protection regimes. FCPA prosecutions generate additional regulatory burdens for U.S. firms that are complying with high legal standards of host countries, and U.S. firms may suffer from significant loss of business opportunities. In this sense, good law does not necessarily mean good business. Cross-jurisdictional legal cooperation between assertive judicial systems may, on the margin, hurt business incentives.

The implication of the paper is that the more regulated and scrutinized MNCs could be subject to a double jeopardy where they face the dual hazards of host government expropriation and home government anti-bribery enforcement. In jurisdictions with weak institutional oversight, these firms lose business opportunities to unconstrained competitors who outbid American firms through bribery. Meanwhile, such firms cannot adopt similar risk-mitigation strategies as they are under intensive anti-bribery scrutiny of the FCPA. In markets with more reliable judicial systems to cooperate with U.S. authorities, FCPA interventions are more likely to generate unnecessary legal burdens and disrupt these MNCs’ status quo business models used to navigate local regulatory landscapes. In the global market place, such firms will be placed in a competitive disadvantage until better coordinated transnational anti-bribery enforcement creates a level playing field for MNCs of different national origins.

Availability of data and materials

The replication dataset and code will be made available upon request.

Notes

See the OECD FDI Regulatory Restrictive Index for financial services, banking, and insurance industries at https://stats.oecd.org/Index.aspx?datasetcode=FDIINDEX#.

See reports on “window guidance” and other capital control measures at https://www.ft.com/content/c9f7d320-dee7-11e6-9d7c-be108f1c1dce and https://www.ft.com/stream/06c60680-8dc7-4bc5-8311-251b82a477b5.

Activities include Increased employment, investment, and joint venture establishments. See reports at https://www.scmp.com/business/companies/article/2152620/jpmorgan-goes-hiring-spree-retool-its-china-banking-team-serving, https://www.scmp.com/tech/start-ups/article/2143474/goldman-sachs-leads-us300-million-investment-chinas-second-hand-car, https://www.ft.com/content/1835404e-54c2-11e8-b3ee-41e0209208ec, and https://www.bloomberg.com/news/articles/2017-11-13/goldman-lays-groundwork-for-china-future-without-ownership-curb

See case information at http://fcpa.stanford.edu/fcpac/documents/5000/003625.pdf and http://fcpa.stanford.edu/fcpac/documents/4000/003405.pdf.

See case information at http://fcpa.stanford.edu/fcpac/documents/4000/002817.pdf.

See case information at http://fcpa.stanford.edu/fcpac/documents/2000/000502.pdf.

See case information at http://fcpa.stanford.edu/fcpac/documents/5000/003568.pdf.

See case information at http://fcpa.stanford.edu/fcpac/documents/3000/001586.pdf.

See the remarks by Deputy Attorney General Rod Rosenstein at https://www.justice.gov/opa/speech/deputy-attorney-general-rosenstein-delivers-remarks-34th-international-conference-foreign.

See the remarks by Attorney General Jeff Sessions at https://www.justice.gov/opa/speech/attorney-general-jeff-sessions-delivers-remarks-ethics-and-compliance-initiative-annual. Also see a related commentary at http://www.fcpablog.com/blog/2018/6/11/bill-steinman-the-fcpa-is-not-dead-redux.html.

Among the top ten FCPA enforcement actions based on the amount of monetary penalties, only two are U.S. companies and the rest are all from developed economies. See http://www.fcpablog.com/blog/2018/6/7/socgen-replaces-total-sa-on-the-top-ten-list.html.

https://wislawjournal.com/2015/03/17/global-market-requires-heightened-awareness-of-fcpa-enforcement/. On the latest trend of global enforcement and compliance, see https://www.opus.com/growing-force-anti-bribery-and-corruption-compliance/. See also https://www.forbes.com/2009/12/08/foreign-corrupt-practices-act-opinions-contributors-michael-perlis-wrenn-chais.html#11722d24e81c.

See the 2018 Progress Report at https://www.transparency.org/whatwedo/publication/exporting_corruption_2018. Including major non-OECD corruption exporters such as China is a major change from Transparency International’s 2015 Progress Report.

See the official websites at https://www.sec.gov/spotlight/fcpa/fcpa-cases.shtml and https://www.justice.gov/criminal-fraud/related-enforcement-actions.

Data on enforcement actions is obtained from http://fcpa.stanford.edu/enforcement-actions.html.

See the dataset at http://www.enterprisesurveys.org.

For detailed descriptions of the methodology, see http://www.enterprisesurveys.org/methodology.

The data is available for download at https://unctad.org/en/Pages/DIAE/FDI%20Statistics/FDI-Statistics-Bilateral.aspx.

The data is available for download at http://www.oecd.org/sti/ind/amne.htm.

I also use total turnover as the DV for robustness checks, and the results are very similar.

For more details on this index, see the V-Dem codebook available at https://www.v-dem.net/en/data/data-version-7-1/.

Additional robustness checks using different measurements of the control variables and including more controls are available upon request.

There is also a nonlinear relationship regarding corruption levels, where FCPA enforcement boots corporate performance in moderately corrupt countries, while hurting corporate performance in countries with extremely high or low levels of corruption.

References

Acemoglu, Daron. 2008. Oligarchic versus democratic societies. Journal of the European Economic Association 6 (1): 1–44.

Alder, Simeon, David Lagakos, and Lee Ohanian. 2014. Competitive pressure and the decline of the Rust Belt: A macroeconomic analysis. Technical report National Bureau of Economic Research.

Aligica, Paul Dragos, and Vlad Tarko. 2012. State capitalism and the rent-seeking conjecture. Constitutional Political Economy 23 (4): 357–379.

Allee, Todd, and Clint Peinhardt. 2011. Contingent credibility: The impact of investment treaty violations on foreign direct investment. International Organization 65 (03): 401–432.

Andonova, Veneta, and Luis Diaz-Serrano. 2009. Political institutions and telecommunications. Journal of Development Economics 89 (1): 77–83.

Arias, Eric, James R. Hollyer, and B. Peter Rosendorff. 2017. Cooperative autocracies: Leader survival, creditworthiness and bilateral investment treaties. Technical report Working Paper. Google Scholar.

Beazer, Quintin H., and Daniel J. Blake. 2018. The conditional nature of political risk: How home institutions influence the location of foreign direct investment. American Journal of Political Science 62 (2): 470–85.

Beck, Paul J., Michael W. Maher, and Adrian E. Tschoegl. 1991. The impact of the Foreign Corrupt Practices Act on US exports. Managerial and Decision Economics 12 (4): 295–303.

Bencivenga, Dominic. 1997. Anti-bribery campaign: SEC cracks down on illegal payments abroad. New York Law Journal 110 (10): 5–6.

Black, Sandra E., and Philip E. Strahan. 2001. The division of spoils: Rent-sharing and discrimination in a regulated industry. American Economic Review 91 (4): 814–831.

Blanchard, Olivier, and Francesco Giavazzi. 2003. Macroeconomic effects of regulation and deregulation in goods and labor markets. The Quarterly Journal of Economics 118 (3): 879–907.

Boddewyn, Jean J. 2015. Political Aspects of MNE Theory. In The Eclectic Paradigm, ed. J. Cantwell, 85–110. London: Springer, Palgrave Macmillan. https://doi.org/10.1007/978-1-137-54471-1_4.

Boldrin, Michele, and David Levine. 2002. The case against intellectual property. American Economic Review 92 (2): 209–212.

Boldrin, Michele, and David K. Levine. 2013. The case against patents. Journal of Economic Perspectives 27 (1): 3–22.

Borgman, Richard H., and Vinay Datar. 2012. The foreign corrupt practices act: Regulatory burden and response. International research. Journal of Applied Finance 3(1): 3–19.

Brouthers, Keith D., and Lance Eliot Brouthers. 2003. Why service and manufacturing entry mode choices differ: The influence of transaction cost factors, risk and trust. Journal of Management Studies 40 (5): 1179–1204.

Büthe, Tim, and Helen V. Milner. 2014. Foreign direct investment and institutional diversity in trade agreements: Credibility, commitment, and economic flows in the developing world, 1971–2007. World Politics 66 (01): 88–122.

Case, Spencer A., D. Scott Lee, and John D. Martin. 2007. The potential for expropriation through joint ventures. Review of Financial Economics 16 (1): 111–126.

Chang, Sea-Jin, Jaiho Chung, and Jon Jungbien Moon. 2013. When do wholly owned subsidiaries perform better than joint ventures? Strategic Management Journal 34 (3): 317–337.

Chen, Shih-Fen S., and Jean-Francois Hennart. 2002. Japanese investors’ choice of joint ventures versus wholly-owned subsidiaries in the US: The role of market barriers and firm capabilities. Journal of International Business Studies 33 (1): 1–18.

Chen, Frederick R., and Jian Xu. 2023. Partners with benefits: When multinational corporations succeed in authoritarian courts. International Organization 77 (1): 144–178.

Chen, Tain-Jy, Homin Chen, and Ying-Hua Ku. 2004. Foreign direct investment and local linkages. Journal of International Business Studies 35 (4): 320–333.

Chew, Pat K. 1993. Political risk and US investments in China: Chimera of protection and predictability. Virginia Journal of International Law 34: 615.

Chiao, Yu-Ching, Fang-Yi Lo, and Chow-Ming Yu. 2010. Choosing between wholly-owned subsidiaries and joint ventures of MNCs from an emerging market. International Marketing Review 27 (3): 338–365.

Cragg, Wesley, and William Woof. 2002. The US Foreign Corrupt Practices Act: A study of its effectiveness. Business and Society Review 107 (1): 98–144.

Cuervo-Cazurra, Alvaro. 2006. Who cares about corruption? Journal of International Business Studies 37 (6): 807–822.

Cuervo-Cazurra, Alvaro. 2008. The effectiveness of laws against bribery abroad. Journal of International Business Studies 39 (4): 634–651.

David, K. Tse, Yigang Pan, and Kevin Y. Au. 1997. How MNCs choose entry modes and form alliances: The China experience. Journal of International Business Studies 28 (4): 779–805.

Davies, Howard, Thomas K.P. Leung, Sherriff T.K. Luk, and Yiu-hing Wong. 1995. The benefits of “Guanxi”: The value of relationships in developing the Chinese market. Industrial Marketing Management 24 (3): 207–214.

Davis, Kevin E. 2009. Does the globalization of anti-corruption law help developing countries? SSRN working paper.

De Luís, Sousa. 2010. Anti-corruption agencies: Between empowerment and irrelevance. Crime, Law and Social Change 53 (1): 5–22.

Degryse, Hans, and Steven Ongena. 2008. Competition and regulation in the banking sector: A review of the empirical evidence on the sources of bank rents. Handbook of Financial Intermediation and Banking 2008: 483–554.

Delios, Andrew, and Witold I. Henisz. 2000. Japanese firms’ investment strategies in emerging economies. Academy of Management Journal 43 (3): 305–323.

Djankov, Simeon. 2009. The regulation of entry: A survey. The World Bank Research Observer 24 (2): 183–203.

Djankov, Simeon, Rafael La Porta, Florencio Lopez-de Silanes, and Andrei Shleifer. 2002. The regulation of entry. The Quarterly Journal of Economics 117 (1): 1–37.

Eden, Lorraine, Stefanie Lenway, and Douglas A. Schuler. 2005. From the obsolescing bargain to the political bargaining model. In International business and government relations in the 21st century, 251–272. Cambridge University Press.

Geo-JaJa, Macleans A., and Garth Mangum. 1999. Donor aid and human-capital formation: A neglected priority in Africa’s development. In Making aid work: Innovative approaches for Africa at the turn of the century. Lanham: Rowman and Littlefield Publishers.

Graham, John L. 1984. The foreign corrupt practices act: A new perspective. Journal of International Business Studies 15 (3): 107–121.

Graham, Brad, and Caleb Stroup. 2016. Does anti-bribery enforcement deter foreign investment? Applied Economics Letters 23 (1): 63–67.

Graham, Benjamin A.T., and Jacob R. Tucker. 2017. The international political economy data resource. Review of International Organizations. Online First.

Guide, FCPA. 2012. A resource guide to the US Foreign Corrupt Practices Act. By the Criminal Division of the US Department of Justice and the Enforcement Division of the US Securities and Exchange Commission.

Guillén, Mauro F. 2003. Experience, imitation, and the sequence of foreign entry: Wholly owned and joint-venture manufacturing by South Korean firms and business groups in China, 1987–1995. Journal of International Business Studies 34 (2): 185–198.

Hajzler, Christopher. 2012. Expropriation of foreign direct investments: Sectoral patterns from 1993 to 2006. Review of World Economics 148 (1): 119–149.

Hanna, Rema. 2010. US environmental regulation and FDI: Evidence from a panel of US-based multinational firms. American Economic Journal: Applied Economics 2 (3): 158–189.

Hellman, Joel S., Geraint Jones, and Daniel Kaufmann. 2002. Far from home: Do foreign investors import higher standards of governance in transition economies?

Henisz, Witold J. 2002. The institutional environment for infrastructure investment. Industrial and Corporate Change 11 (2): 355–389.

Hennart, Jean-Francois, Thomas Roehl, and Dixie S. Zietlow. 1999. ‘Trojan horse’ or ‘workhorse’? The evolution of US-Japanese joint ventures in the United States. Strategic Management Journal 20 (1): 15–29.

Hillman, Arye L. 2013. The political economy of protection. Taylor & Francis.

Hines Jr, James R. 1995. Forbidden payment: Foreign bribery and American business after 1977. Technical report National Bureau of Economic Research.

International, Transparency. 2016. Global corruption report: Sport. Routledge.

Jensen, Nathan M. 2003. Democratic governance and multinational corporations: Political regimes and inflows of foreign direct investment. International Organization 57 (03): 587–616.

Jensen, Nathan. 2008. Political risk, democratic institutions, and foreign direct investment. The Journal of Politics 70 (4): 1040–1052.

Jensen, Nathan M., and Edmund J. Malesky. 2018. Nonstate actors and compliance with international agreements: An empirical analysis of the OECD anti-bribery convention. International Organization 72 (1): 33–69.

Kesternich, Iris, and Monika Schnitzer. 2010. Who is afraid of political risk? Multinational firms and their choice of capital structure. Journal of International Economics 82 (2): 208–218.

Kirkpatrick, Colin, David Parker, and Yin-Fang Zhang. 2006. Foreign direct investment in infrastructure in developing countries: Does regulation make a difference? Transnational Corporations 15 (1): 143–172.

Konrad, Kai A., and Dan Kovenock. 2009. Competition for FDI with vintage investment and agglomeration advantages. Journal of International Economics 79 (2): 230–237.

Krever, Tor. 2007. Curbing corruption-The efficacy of the Foreign Corrupt Practice Act. North Carolina Journal of International Law and Commercial Regulation 33: 83.

Lang, Bertram. 2017. Engaging China in the fight against transnational bribery: ‘Operation Skynet’ as a new opportunity for OECD countries. 2017 OECD Global Anti-Corruption and Integrity Forum. http://www.oecd.org/cleangovbiz/Integrity-Forum-2017-Lang-China-transnational-bribery.pdf.

Li, Quan, and Adam Resnick. 2003. Reversal of fortunes: Democratic institutions and foreign direct investment inflows to developing countries. International Organization 57 (01): 175–211.

Liebeskind, Julia Porter. 1999. Knowledge, strategy, and the theory of the firm. In Knowledge and strategy, 197–219. Elsevier.

Linzer, Drew A., and Jeffrey K. Staton. 2015. A global measure of judicial independence, 1948–2012. Journal of Law and Courts 3 (2): 223–256.

Lu, Jane W., and Paul W. Beamish. 2006. Partnering strategies and performance of SMEs’ international joint ventures. Journal of Business Venturing 21 (4): 461–486.

Luo, Yadong. 2001. Determinants of entry in an emerging economy: A multilevel approach. Journal of Management Studies 38 (3): 443–472.

Luo, Yadong. 2005. Transactional characteristics, institutional environment and joint venture contracts. Journal of International Business Studies 36 (2): 209–230.

Maijoor, Steven, and Arjen Van Witteloostuijn. 1996. An empirical test of the resource-based theory: Strategic regulation in the Dutch audit industry. Strategic Management Journal 17 (7): 549–569.

Malesky, Edmund J., Dimitar D. Gueorguiev, and Nathan M. Jensen. 2015. Monopoly money: Foreign investment and bribery in Vietnam, a survey experiment. American Journal of Political Science 59 (2): 419–439.

Marshall, Monty G., T.D. Gurr, and K. Jaggers. 2016. Polity IV project. Political regime characteristics and transitions, 1800–2015. Dataset users’ manual. Center for Systemic Peace.

McChesney, Fred S. 1987. Rent extraction and rent creation in the economic theory of regulation. The Journal of Legal Studies 16 (1): 101–118.

Meyer, Klaus E., Mike Wright, and Sarika Pruthi. 2009a. Managing knowledge in foreign entry strategies: A resource-based analysis. Strategic Management Journal 30 (5): 557–574.

Meyer, Klaus E., Saul Estrin, Sumon Kumar Bhaumik, and Mike W. Peng. 2009b. Institutions, resources, and entry strategies in emerging economies. Strategic Management Journal 30 (1): 61–80.

Mitton, Todd. 2008. Institutions and concentration. Journal of Development Economics 86 (2): 367–394.

Moon, Chungshik. 2015. Foreign direct investment, commitment institutions, and time horizon: How some autocrats do better than others. International Studies Quarterly 59 (2): 344–356.

Morschett, Dirk, Hanna Schramm-Klein, and Bernhard Swoboda. 2010. Decades of research on market entry modes: What do we really know about external antecedents of entry mode choice? Journal of International Management 16 (1): 60–77.

OECD. 2014. OECD foreign bribery report: An analysis of the crime of bribery of foreign public officials. OECD Publishing.

Osland, Gregory E., and S. Tamer Cavusgil. 1996. Performance issues in US—China joint ventures. California Management Review 38 (2): 106–130.

Pan, Yigang, and K. Tse David. 2000. The hierarchical model of market entry modes. Journal of International Business Studies 31 (4): 535–554.

Perlman, Rebecca L., and Alan O. Sykes. 2018. The political economy of the foreign corrupt practices act: An exploratory analysis. Journal of Legal Analysis 9 (2): 153–182.

Poirier, Dale J. 1980. Partial observability in bivariate probit models. Journal of Econometrics 12 (2): 209–217.

Puck, Jonas F., Dirk Holtbrügge, and Alexander T. Mohr. 2009. Beyond entry mode choice: Explaining the conversion of joint ventures into wholly owned subsidiaries in the People’s Republic of China. Journal of International Business Studies 40 (3): 388–404.

Rose, Nancy L. 1987. Labor rent sharing and regulation: Evidence from the trucking industry. Journal of Political Economy 95 (6): 1146–1178.

Rowley, Charles, Robert D. Tollison, and Gordon Tullock. 2013. The political economy of rent-seeking. Vol. 1 Springer Science & Business Media.

Roy, Jean-Paul, and Christine Oliver. 2009. International joint venture partner selection: The role of the host-country legal environment. Journal of International Business Studies 40 (5): 779–801.

Salbu, Steven R. 1997. Bribery in the global market: A critical analysis of the Foreign Corrupt Practices Act. Washington and Lee Law Review 54: 229.

Sell, Susan K., et al. 2003. Private power, public law: The globalization of intellectual property rights. Vol. 88 Cambridge University Press.

Sheffet, Mary Jane. 1995. The Foreign Corrupt Practices Act and the Omnibus Trade and Competitiveness Act of 1988: Did they change corporate behavior? Journal of Public Policy & Marketing 14 (2): 290–300.

Smarzynska, Beata K., Shang-Jin Wei, et al. 2000. Corruption and composition of foreign direct investment: Firm-level evidence, vol. 7969. Cambridge: National Bureau of Economic Research.

Stigler, George J. 1971. The theory of economic regulation. The Bell Journal of Economics and Management Science 3–21.

Tobin, Jennifer L., and Susan Rose-Ackerman. 2011. When BITs have some bite: The political-economic environment for bilateral investment treaties. The Review of International Organizations 6 (1): 1–32.

Vadlamannati, Krishna Chaitanya. 2012. Impact of political risk on FDI revisited—An aggregate firm-level analysis. International Interactions 38 (1): 111–139.

Vahabi, Mehrdad. 2016. A positive theory of the predatory state. Public Choice 168 (3–4): 153–175.

Wellhausen, Rachel L. 2015. Investor–state disputes: When can governments break contracts? Journal of Conflict Resolution 59 (2): 239–261.

Willborn, Emily. 2013. Extraterritorial enforcement and prosecutorial discretion in the FCPA: A call for international prosecutorial factors. Minnesota Journal of International Law 22: 422.

Wright, Joseph, and Boliang Zhu. 2018. Monopoly rents and foreign direct investment in fixed assets. International Studies Quarterly 2: 341–356.

Yiu, Daphne, and Shige Makino. 2002. The choice between joint venture and wholly owned subsidiary: An institutional perspective. Organization Science 13 (6): 667–683.

Zhang, Yan, Haiyang Li, Michael A. Hitt, and Geng Cui. 2007. R&D intensity and international joint venture performance in an emerging market: moderating effects of market focus and ownership structure. Journal of International Business Studies 38 (6): 944–960.

Zhu, Boliang, and Qing Deng. 2018. Monopoly rents, institutions, and bribery. SSRN working paper.

Funding

The project received funding from Emory University Professional Development Support fund for PhD students.

Author information

Authors and Affiliations

Contributions

It is a single author project. All author(s) read and approved the final manuscript.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

The project does not involve human subjects and does not need IRB approval.

Competing interests

There are no competing interests to be disclosed.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Xu, J. Double jeopardy: FCPA enforcement and MNC risk-mitigation strategies. ARPE 3, 1 (2024). https://doi.org/10.1007/s44216-023-00021-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s44216-023-00021-1