Abstract

Tech-based SMEs are important subjects for achieving national innovation-driven development, and it is crucial to study whether and how changes in the macro-institutional environment affect their innovation efficiency. New Asset Management Regulation (NAMR) is a policy promulgated by the Chinese government to address the chaotic expansion of shadow banking in China, and this study treats it as a quasi-natural experiment, selecting a sample of Chinese GEM-listed firms from 2015 to 2019, adopting the event study method and the generalized double difference method, and empirically testing the impact of shadow banking contraction on the innovation efficiency of Chinese tech-based SMEs and its mechanism. This study finds that shadow banking contraction under the NAMR significantly improves innovation efficiency of tech-based SMEs. The mechanism test finds that the NAMR can optimize the debt financing structure of tech-based SMEs, reduce their financing costs and financing risks, and ultimately accelerate their innovation efficiency by improving their financing efficiency, which supports the hypothesis of “financing efficiency view”; it is further found that, to tech-based SMEs, the more they rely on shadow banking and the severer financing constraints they endure, the more obvious NAMR’s effect is on improving innovation efficiency. The findings not only provide some empirical evidence to clarify the controversy of shadow banking in China from the perspective of firm innovation, but also have some implications for the subsequent financial regulatory reform.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Tech-based SMEs are important subjects for practicing innovation-driven development in China. To tech-based SMEs, high innovation efficiency means better innovation input–output ratio (Cruz-Cázares et al., 2013; Manzaneque et al., 2020). Meanwhile, the characteristics of high risk, long cycle time, and uncertainty of innovation (Crick & Jones, 2000) make tech-based SMEs demand for sustained and large external financial investment to maintain high quality innovation efficiency. However, the high operational risk (Zhu et al., 2012), weak risk prevention (Pederzoli et al., 2013), and severe information asymmetry (Chen et al., 2019; Hoffman et al., 1998) of tech-based SMEs make it difficult for them to obtain large-scale financing from formal channels such as banks. Therefore, in order to obtain adequate innovation funding, tech-based SMEs are forced to turn to informal channels such as shadow banks for financing (Allen et al., 2019).

In China, SMEs are the main force of shadow bank borrowing (Lu et al., 2015). Among them, tech-based SMEs are more liable to be involved in long-term investment activities such as innovation which demand sufficient financing to sustain. Thus, it is important to investigate the impact of the change in the size of shadow banks on the innovation efficiency of tech-based SMEs from the perspective of financing. The Chinese Growth Enterprise Market (GEM) is a securities market that provides financing opportunities for tech-based SMEs that are temporarily unable to list on the Chinese Main Board. Therefore, this study chooses Chinese GEM-listed firms as the proxy research sample of tech-based SMEs due to two reasons, which are the difficulty of data acquisition on one hand, and most Chinese GEM-listed firms, with technical innovativeness and small size as a common typical feature, reflecting the overall picture of Chinese tech-based SMEs on the other.

Compared to other developed countries, Chinese shadow banking is a product of off-balance-sheeting of domestic assets in the context of restricted bank credit impulses and less securitization of assets (Agnello et al., 2020; Allen et al., 2019; Irani et al., 2021). This kind of unofficial banking agencies manifest themselves mainly as “shadow of banks”, which essentially as a partial replacement for commercial bank credit driven by SMEs’ financing needs (Guo & Xia, 2014). Since their sources of funding are mainly savings funds of firms and residents, they are not subject to the regulatory capital requirement framework and central bank supervision (Lu et al., 2015). In recent years, driven by the high financing demand of SMEs and the high return motive of large firms (Allen & Gu, 2021), the scale of shadow banking in China has expanded significantly, which not only exacerbates the rising cost of social financing, but also amplifies systemic financial risks through multi-layer nesting (An & Yu, 2018).

In November 2017, the People’s Bank of China, together with various ministries and commissions, issued a draft of the New Asset Management Regulation (NAMR) for public comment back, which laid the basic policy guidance for governing shadow banking and preventing financial risks. On April 27, 2018, the NAMR was officially promulgated and implemented, to regulate qualified investors identification, break rigid exchange and resolve multi-layer nesting, which is of great significance for preventing and controlling financial risks. Since the release of the NAMR for public comment back, the scale of shadow banking in China has indeed witnessed a substantial decline.

However, at the micro enterprise level, has the shadow banking contraction changed the original financing model of tech-based SMEs, thus affecting the efficiency of innovation? To answer the question, this study empirically examines the impact of shadow banking contraction on the innovation efficiency of tech-based SMEs and its mechanism of action from the “financing constraint view” hypotheses and the “financing efficiency view” hypotheses. We use the NAMR as a quasi-natural experiment, adopting the event study method and the generalized double difference method, and selecting a sample of Chinese GEM-listed firms from 2015 to 2019. It is found that the contraction of shadow banks under the NAMR significantly improves the innovation efficiency of tech-based SMEs; the mechanism test finds that the NAMR can optimize the debt financing structure of tech-based SMEs, reduce their financing cost and financing risk, and ultimately accelerate their innovation efficiency by improving the financing efficiency, which supports the “financing constraint view” hypothesis. It is further found that, to the tech-based SMEs, there is a positive relationship between the effect of the NAMR on improving innovation efficiency and the degree of their reliance on shadow banking as well as the extent of financing constraints on them.

This study makes the following important contributions: (1) It is the first to expand the research on the factors influencing innovation efficiency of tech-based SMEs from the macro policy perspective of shadow banking contraction. Although it has been found in previous studies that firm innovation efficiency is mostly influenced by the micro level (Qiao & Fung, 2016; Xie et al., 2020), few studies have addressed this topic from a macro policy perspective. (2) It enriches the research on the economic consequences of shadow banking contraction from the perspective of firm innovation. Among the existing literature studying the economic consequences of shadow banking expansion (Chernenko & Sunderam, 2014; Gong et al., 2021; Grochulski & Zhang, 2019; Lu et al., 2015; Yang et al., 2019), there is almost no research on shadow banking contraction. (3) It provides some basis for the formation of a dialectical view of the shadow banking problem in China. Regarding the impact of shadow banking expansion in China, opposing views have emerged in academia: one is that shadow banking expansion promotes credit development in capital markets (Chernenko & Sunderam, 2014; Duca, 2016); whereas the other is that shadow banking expansion amplifies systemic financial risks (Gong et al., 2021; Le et al., 2020; Yang et al., 2019). And this study presents empirical evidence on new aspects from the perspective of the relationship between shadow banking contraction and innovation efficiency.

The rest of the study is composed of realistic background, literature review and research hypothesis, study design, empirical results, mechanism testing, further testing, as well as research conclusions and implications.

2 Realistic background

The implementation of the NAMRFootnote 1 marks the formal formation of a new regulatory framework that mainly regulates and shrinks shadow banking: firstly, to exclude most SMEs and guiding most of them to focus on their main business and move away from the virtual to the real world, the NAMR identifies qualified firm investors as legal entities with net assets of not less than 10 million at the end of the previous year; secondly, a series of provisions in the NAMR, such as regulating capital pools, breaking rigid exchange, eliminating multi-layer nesting, and restricting channel business, have greatly improved market resource allocation; thirdly, the NAMR emphasizes the combination of institutional and functional regulation to achieve penetrating regulation, which brings participating entities and operating assets into the scope of regulation to prevent multiple arbitrages, enhance the efficiency of capital use, reduce transaction costs and prevent financial risks brought by shadow banking.

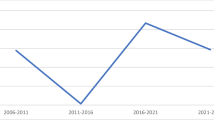

In practice, the implementation of the NAMR has indeed achieved the objective of shrinking the size of shadow banking. Figure 1Footnote 2 shows the trend of the average size of shadow banking in China by province from 2015 to 2019. With the release of the NAMR for public comment back in November 2017, the growing scale of the new shadow banking scale began to show a downward trend after peaking in January 2018. Especially after the official introduction of the NAMR in April 2018, the scale of shadow banking grew negatively, directly falling from 88,683 billion to − 66,380 billion, a decrease of 174.85%, and then showing a negative range of low fluctuations. This reflects the effectiveness of the implementation of the macro policy of the NAMR.

Trend of the average size of shadow banking in China by province. Data source: China CEInet Statistics Database

3 Literature review and research hypothesis

3.1 Literature review

3.1.1 Economic consequences of shadow banking

Academically, two opposing views have emerged from studies on the expansion of shadow banking in China: one is that shadow banks act as a complement and alternative to formal banks, and their expansion promotes credit development in capital markets. Shadow banks tend to provide short-term loans due to the absorption of short-term idle funds (Duca, 2016), which improves the replenishment of firm liquidity (Chernenko & Sunderam, 2014). Another opinion holds that the expansion of shadow banking amplifies systemic financial risks due to unregulated and multiple nesting. At the financial market level, the rapid expansion of shadow banking reduces the proportion of liquidity per unit of social financing, increases the vulnerability of the financial system (Gong et al., 2021), and makes credit financing more accessible to large firms, consequently creating financing mismatches (Grochulski & Zhang, 2019). At the firm level, in the environment of insufficient supply of long-term funds, firms are prone to the maturity mismatch of “short loans and long investment” in shadow bank financing, which aggravates the financial risks of economic entities (An & Yu, 2018; Le et al., 2020).

3.1.2 Debt financing impact mechanism of innovation efficiency

It has been argued that for SMEs, in addition to equity financing as the external source of innovation funding, debt financing can also promote innovation (Cornaggia et al., 2015; Madrid-Guijarro et al., 2016; Xin et al., 2017). And the mechanism of debt financing affecting innovation efficiency can be divided into the “financing constraint view” hypothesis and the “financing efficiency view” hypothesis. The “financing constraint view” hypothesis suggests that debt financing can alleviate the financing constraint of firms and promote R&D investment to improve innovation efficiency (Benfratello et al., 2008). While, the “financing efficiency view” hypothesis suggests that the improvement of debt financing efficiency can reduce the chances of firms investing inefficient funds, and the efficiency of firms’ innovation will be improved with the same innovation output (Gomariz & Ballesta, 2014).

Taken together, international research on the consequences of shadow banking contraction has not yet received attention, and there are fewer studies on the impact on the innovation efficiency of tech-based SMEs. This study examines the impact of shadow banking contraction on the innovation efficiency of tech-based SMEs and the mechanism of action by using the NAMR as a quasi-natural experiment, and tries to explain and supplement the connotation of the macro policy NAMR on micro tech-based SMEs from the perspective of different financing needs.

3.2 Research hypothesis

3.2.1 Based on the “financing constraint view”

According to the “financing constraint view”, shadow banks can provide credit support to tech-based SMEs that cannot be financed through formal channels, while the impact of the contraction of shadow banks under the NAMR has undoubtedly cut some of their financing channels, aggravated the financing constraint, made it difficult to meet the demand for innovation, and ultimately reduced the efficiency of innovation.

The financing needs of firms can be divided into two categories: investment financing needs and financing needs to alleviate liquidity constraints (Tse & Wong, 2011). Due to innovation activities, tech-based SMEs often have more eager investment financing needs (Zhou et al., 2021). The theory of financing priority (Myers & Majluf, 1984) suggests that firm financing tends to follow the sequence of endogenous financing over exogenous financing. However, since endogenous financing can hardly meet the innovation needs of tech-based SMEs, it becomes an indispensable source of funding (Carbo-Valverde et al., 2009; Cressy & Olofsson, 1997; Petersen & Rajan, 1994). In the current environment of imperfect capital market and low stock market in China, debt financing is still one of the channels for most Chinese tech-based SMEs to meet their investment financing needs (Maes et al., 2019). Based on the difference in credit sources, debt financing can be divided into formal financing channels represented by banks, and informal channels represented by shadow banks. Due to the severe information asymmetry (Chen et al., 2019), high operational risk (Zhu et al., 2012), and weak risk prevention ability (Pederzoli et al., 2013) of tech-based SMEs, formal institutions like banks have difficulties in accurately assessing the development trend of firms and set credit quotas based on the prudence of innate risk control threshold such as restrictions to constrain their financing.

To obtain adequate innovation funding, tech-based SMEs are forced to turn to informal channels like as shadow banks for financing (Allen et al., 2019). The implementation of the NAMR has led to the contraction of shadow banks, which may exacerbate the financing constraints of tech-based SMEs and reduce innovation efficiency. In terms of financing channels, the NAMR disrupts the relationship between supply and demand of funds in the original capital market, limits the external sources of funds for tech-based SMEs, and weakens the alternative and complementary functions of shadow banks to formal credit. Meanwhile, in terms of financing costs, the contraction of shadow banks reduces the supply of capital in the capital market, and due to the limitation of the total amount of formal financial loans, the cost of future borrowing from both shadow banks and formal channels is raised substantially for tech-based SMEs, making financing “more difficult”. It has been found that financing constraints reduce the investment efficiency (Borisova & Brown, 2013; Efthyvoulou & Vahter, 2016; Silva & Carreira, 2012).

The investment efficiency of tech-based SMEs is mainly reflected in the innovation efficiency. Under the contraction of shadow banking caused by the NAMR, the financing constraint of tech-based SMEs is more serious and they have to cut down the relevant innovation investment (Yu et al., 2021), and undoubtedly leading to the low innovation efficiency. Accordingly, this study proposes hypothesis H1a.

H1a: Tech-based SMEs’ innovation efficiency decreases under the impact of the contraction of shadow banking due to the NAMR.

3.2.2 Based on the “financing efficiency view”

The “financing efficiency view” argues that shadow banking does not fundamentally solve the innovation needs of tech-based SMEs, but rather greatly increases their original financing costs and risks, and present inefficient financing instead, which leads to more challenges for their future operation and development. The NAMR, however, restricting the development of shadow banks and allowing capital to be concentrated in high-quality firms, improves the financing efficiency of tech-based SMEs by enhancing the allocation of social resources, and consequently drives their innovation efficiency.

Firstly, the funds provided by shadow banks are mostly short-term loans, which makes it difficult to meet the long-term innovation financing needs of tech-based SMEs. Shadow banks tend to provide short-term loans because they can reduce the risk of firm default (Wu & Shen, 2019) and rely on short-term credit instruments for wholesale funding (Duca, 2016). If tech-based SMEs “lend short and invest long”, this can lead to maturity mismatches and increased financial risk (Bleakley & Cowan, 2010).

Secondly, shadow banking invariably raises the original financing costs of tech-based SMEs. Under China’s credit crunch policy, banks tend to choose large firms as lending targets, but large firms prefer to use most of their funds for subsidiaries or affiliated firms. As a result, only a small portion is lent in the form of entrusted loans, constituting the interest chain of “large firms-commercial banks-shadow banks”, which indirectly raises the original financing cost of tech-based SMEs (Lu et al., 2015). Meanwhile, high returns drive more commercial banks to be willing to invest funds from formal channels into shadow banks, and the scarcity of resources from formal channels raises financing costs (Wang et al., 2021). In order to meet the long-term demand for innovative financing, tech-based SMEs have to frequently raise funds from shadow banks and are forced to pay additional interest and operating costs, forming a vicious circle of “the more they borrow, the poorer they become”.

Finally, shadow banking aggravates the financing risk of tech-based SMEs. Under the financing term mismatch, once they are in poor condition and the overall performance is not good, the high leverage generated by the shadow bank financing will aggravate their innovation burden and lead to “borrowing new for interest” and “deterioration of assets and liabilities”, and even bankruptcy (Gopalan et al., 2014). Therefore, to avoid the unwelcomed dilemma, tech-based SMEs prefer to operate conservatively when the operational risk is high, for example, using the financing for business management rather than technological innovation (Harford et al., 2009), to avoid more risk from innovative activities.

In a comprehensive view, the NAMR enhances the financing efficiency of tech-based SMEs in three aspects: optimizing financing structure, reducing financing cost, decreasing financing risk, and thus enhancing innovation efficiency through the regulation of shadow banks. Accordingly, this study proposes hypothesis H1b.

H1b: Tech-based SMEs’ innovation efficiency rises under the impact of the contraction of shadow banking due to the NAMR.

4 Study design

4.1 Sample and data sources

Tech-based SMEs mainly focus on technological innovation, operate on a small scale and have high potential for innovation and development. Most of the listed firms in China GEM are technically innovative and generally small, which represent the overall picture of tech-based SMEs. This study selects GEM-listed firms from 2015 to 2019Footnote 3 as the research samples. The sample data are processed as follows: (1) delete the samples of financial industry firms; (2) delete the samples of firms listed after the release of the NAMR for public comment back; (3) delete the samples of firms that cannot satisfy the estimation window period and event window period in the event study method; (4) delete the samples of ST and PT firms; (5) delete the samples of firms with missing data. The final samples of 3353 observations were obtained. To control for outliers, continuous variables were Winsorized treated at 1% and 99% levels. The event study method selects daily data for the corresponding window period, and the regression analysis uses annual data. The micro data, such as innovation efficiency, financial data and related firm governance, are obtained from Chinese CSMAR and WIND databases, while macro data, such as shadow banking and social financing scale are obtained from China CEInet statistical database.

4.2 Identification strategy and model setting

The double difference model (DID) is a classic method to verify the effect of exogenous policies. However, since the NAMR is issued by the state, and all firms will be affected at the same point in time, it is difficult to distinguish the “treatment group” and “control group” in a strict sense. Therefore, this study draws on the study of Greenland et al. (2020) to construct a generalized double difference model (GDD) based on the conventional double difference method. The GDD is applicable to the situation where all individual firms are exposed to policy shocks, but each individual firm is affected to a different extent. The steps are as follows: firstly, the event study method is used to calculate the cumulative abnormal returns (CAR) of tech-based SMEs after the policy release to determine their different degrees of response to the contraction of shadow banking; and then the GDD is applied to measure the change in their innovation efficiency.

4.2.1 Event study method

The event study method can accurately and intuitively capture the impact of the contraction shock of shadow banking on micro firms due to the NAMR. The first is the selection of the event date. This study takes place on November 17, 2017, which is the release date of the NAMR for public comment back, as the event date. The reason is that, since the release of the NAMR for public comment back, the number of news media reports has surged and the policy has gained widespread attention; moreover, the formal introduction of the policy has been expected by the market, and various financial institutions have adjusted their related businesses accordingly; most importantly, such non-predetermined chain-reactive events can better highlight the validity of the event research method. Second, the CAR is calculated using the capital asset pricing model constructed by Sharpe (1964), which can reflect the abnormal fluctuation of firm stock returns during the event window, and also the different reactions of tech-based SMEs to the promulgation of the NAMR. The CAR is calculated as follows.

where \({R}_{i,t}\) is the tech-based SME’s stock return, \({R}_{f,t}\) is the risk-free rate of return, \({R}_{m,t}\) is the market rate of return, and \({\varepsilon }_{i,t}\) is the disturbance term.

4.2.2 Generalized double difference method

This study constructs the following GDD model and controls for firm and year fixed effects.

In model (2), IE is the innovation efficiency; POST is a dummy variable for whether or not the NAMR for public comment back is released, taking the value of 0 before release and 1 after release; CAR_ad is the value of the CAR after the event study method is calculated to be positive; CONTROL is a set of control variables, with \(\sum FIRM\) and \(\sum YEAR\) indicating that the model controls for firm and year fixed effects. In addition, the regression results were corrected for firm-level clustering. In addition, to mitigate the effect of policy occurrence on the control variables in the model, the data of control variables are all initial values for a period of time.

4.2.3 Variable definition

The core variable of interest in this study is innovation efficiency (IE), and a data envelopment analysis (DEA) model is constructed to measure it. Two indicators, R&D personnel input and R&D capital input, are selected as the innovation input of firms in terms of human and material resources; two indicators, number of patent applications and operating income, are selected to reflect the innovation output of firms in terms of quantity and amount. Among them, the number of patent applications is obtained by calculating the weighted average after assigning weights of 0.5, 0.3 and 0.2 to invention, utility model and design patents, respectively. Meanwhile, this study constructs the policy variable (CAR_ad), the time variable (POST), and also selects the firm size (SIZE), intangible assets (IA), gearing ratio (LEV), return on assets (ROA), earnings before interest and tax (EBIT), the shareholding ratio of the first largest shareholder (LSSR), government subsidy (GS), and ownership nature (OWN) as control variables with reference to relevant studies. In addition, financing structure (FS), financing cost (FC), financing risk (FR), and financing efficiency (FE) are added as mediating variables in the mechanism test below. The specific variables are defined in Table 1.

5 Empirical results

5.1 Descriptive statistics

Table 2 shows the results of descriptive statistics of the variables. It can be seen that IE of the sample firms has a maximum value of 1, a minimum value of 0, and a mean value of 0.207, indicating that the overall innovation efficiency of tech-based SMEs is low; CAR_ad has a maximum value of 244.684, a minimum value of 82.617, a mean value of 175.785, and a median value of 139.268, reflecting that most tech-based SMEs are affected by the NAMR, and the number of those significantly affected is high; the mean value of the POST is 0.507 and the standard deviation is 0.268, implying a more balanced selection of sample periods. Further, the IE is grouped into descriptive analysis by the year of the release of the NAMR for public comment back, and it is found that the innovation efficiency differences of tech-based SMEs are narrowed and improved overall after the event of the NAMR, which initially verifies the hypothesis H1b.

5.2 Event validity test and market reaction analysis

5.2.1 Event validity test

In order to test whether the release of the NAMR for public comment back receives wide market attention, this study, using the Baidu index,Footnote 4 referring to what Lin et al. (2016) have done in their research, analyzes the search situation before and after the release of the NAMR for public comment back. In order to make the search more precise, this study identifies the keywords as “NAMR” and the full name of the policy. The release date of the NAMR for public comment back was November 17, 2017, and Fig. 2Footnote 5 shows the Baidu index for each 15 days before and after the release. It can be seen that the search volume of web users soars after the release date of the NAMR for public comment back, and all of them reach the peak on the 3rd day after the release. This can indicate that the release of the NAMR for public comment back is an unexpected event with strong exogenous nature, which verifies the validity of designating November 17, 2017 as the event date.

Baidu index before and after the release of the NAMR for public comment back. Data source: China Baidu Index Database

5.2.2 Market response analysis

The capital asset pricing model is used to analyze the market reactions during the window period before and after the release of the NAMR for public comment back to capture the value impact of tech-based SMEs’ short-term exposure to the contraction of shadow banking under the NAMR. While testing the statistical significance, the model is set to estimate the window period of 180 days, and the CAR of tech-based SMEs is calculated by using 2 days before and after the event date as the event window period. From Table 3, it can be seen that the CAR shows a strong negative significance during the event window period. It indicates that the event of the NAMR has a significant negative impact on the stock price volatility of tech-based SMEs in the short term, which can intuitively reflect the extent to which they are impacted by the NAMR.

5.3 Regression results

This study calculates CAR of tech-based SMEs after the policy release by the event study method, and the CAR is positively processed to obtain CAR_ad to reflect the impact of tech-based SMEs affected by the contraction of shadow banking under the NAMR, and we find the larger the value is, the more severe the impact manifests. Table 4 presents the regression results between the contraction of shadow banking and the innovation efficiency of tech-based SMEs under the NAMR. It can be seen that the regression coefficient of the interaction term POST × CAR_ad and IE is significantly positive at the 1% level, indicating that tech-based SMEs, which are more affected by the contraction of shadow banking, have improved their innovation efficiency instead. Therefore, the hypothesis H1b is verified.

5.4 Robustness tests

5.4.1 Parallel trend test

The differences in policy catering, firm governance, and especially financing sources between SOEs and private firms lead to different motivations for innovation, which may affect significant differences in innovation efficiency between the two types of firms. Therefore, this study suspects that tech-based SMEs with different ownership nature are most likely to violate the parallel trend hypothesis. OWN is used as the independent variable and IE is used as the dependent variable for the regression test, with other control variables held constant. Column (1) of Table 5 shows the test results, and the regression coefficients of OWN and IE are not significant, which indicates that the development trend of innovation efficiency of tech-based SMEs with different ownership nature does not differ systematically and passes the parallel trend test.

5.4.2 Placebo test

To remove the interference of stochastic factors to conclusions, this study conducts a placebo test by flattening the time of policy implementation forward. Therefore, this study selects 2015 and 2016 as the year of the dummy event respectively, and re-runs the GDD test. The corresponding test results are shown in columns (2) and (3) of Table 5. It can be seen that the regression coefficient of the interaction term POST × CAR_ad and IE is not significant in both columns, implying that it is indeed the contraction of shadow banking under the NAMR in 2017 that led to the improvement of innovation efficiency.

5.4.3 Excluding other major events in the same period

In the event study test, this study also uses the Hang Seng Index in Hong Kong, China (excluding Mainland Chinese firms) as the benchmark market return. This is because the Hang Seng Index, with the exclusion of mainland-listed Chinese firms, is not only insulated from the impact of the NAMR, but also circumvents the possible disruptions caused by other contemporaneous events in the China mainland. Column (4) of Table 5 presents the corresponding results, and the regression coefficient of the interaction term POST × CAR_ad and IE remains significant at the 1% level after excluding the interference of other major events in the same period, hence strengthening the robustness of the results.

5.4.4 Other robustness tests

On the event interval, 5 days before and after the event are selected as the new event interval, and the CAR is recalculated. The conclusions remain robust after testing.

6 Mechanism testing

This study then examines the “financing efficiency view” mechanism between the NAMR and the innovation efficiency. Specifically, if the “financing efficiency view” hypothesis is valid, it will lead to the decrease in both the proportion of short-term borrowing in the debt financing structure and the cost of debt financing, and the reduction in financing risk as well, which will ultimately lead to the increase of financing efficiency of tech-based SMEs and improve their innovation efficiency. Next, this study constructs the following mediating effect test model based on model (2).

In the above model, MEDs are added as mediating variables, representing financing structure (FS), financing cost (FC), financing risk (FR) and financing efficiency (FE), respectively.

6.1 Financing structure

Financing structure (FS) is defined as the ratio of firm short-term borrowings to all borrowings, and the corresponding regression results are presented in columns (1), (2) and (3) of Table 6. It can be seen that the regression coefficient between the interaction term POST × CAR_ad and FS in column (2) of Table 6 is significantly negative at the 1% level. In column (3), the regression coefficients of the interaction terms POST × CAR_ad and POST × FS with IE are both significant, verifying the mediation effect of financing structure. For robustness, the Sobel test was also conducted, and the p-value obtained was 0. The proportion of mediating effects to the total effect was 35%.

6.2 Financing cost

This study measures financing cost (FC) as the ratio of interest expense on debt to total debt. Columns (1), (4) and (5) of Table 6 report the test results, and it can be seen that the mediation mechanism of financing cost holds. In addition, the p-value of Sobel test is 0, and the proportion of mediating effect to the total effect is 32%.

6.3 Financing risk

This study uses the net debt ratio to measure financing risk (FR), which is the ratio of the difference between interest-bearing debt and money capital to the difference between shareholders’ equity and perpetual debt, and the larger the net debt size of the firm, the greater the financing risk. Columns (1), (6) and (7) of Table 6 show the regression results, indicating that financing cost as a mediating variable is significant. In addition, the p-value of Sobel test is 0, and the proportion of mediating effect to the total effect is 26%.

6.4 Financing efficiency

The DEA model is constructed to measure debt financing efficiency (FE). Considering the characteristics of high input, high risk and high growth of tech-based SMEs, and at the same time to avoid the high covariance among indicators, this study selects the inverse of FS, FC and FR as input indicators; the total asset turnover rate, operating income growth rate and return on net assets represent the operating capacity, development capacity and profitability of tech-based SMEs respectively as output indicators. Columns (1), (8) and (9) of Table 6 show the results of the mediation test for financing efficiency. It can be seen that financing efficiency plays a mediating role. In addition, the p-value of Sobel test is 0, and the proportion of intermediation effect to the total effect is 87%. This fully confirms the hypothesis of “financing efficiency view”.

7 Further testing

Next, this study conducts heterogeneity tests based on the shadow banking dependence and financing constraints of tech-based SMEs respectively.

7.1 Shadow banking dependence

From the perspective of financing efficiency, tech-based SMEs, which are highly dependent on shadow banks, have low financing efficiency all year round, making it difficult to drive innovation efficiency. Now, with the NAMR reducing the original financing cost and financing risk by limiting the scale of shadow banks, their financing efficiency can be improved and innovation efficiency can be promoted. Trust loans and entrusted loans in the Statistical Table of Social Financing Scale issued by the People’s Bank of China are selected to be divided by the total scale of social financing as proxy variables for firms’ shadow banking dependence (SBD). The samples are grouped by the annual median of the industry, and when the shadow banking dependence is higher than the median, they are divided into a group with high shadow banking dependence, otherwise a group with low dependence.

Columns (1) and (2) of Table 7 shows that the regression coefficient of the interaction term POST × CAR_ad and IE is significantly positive at the 1% level in the shadow banking high dependence group, while in the low shadow banking dependence group, the corresponding regression coefficient is significant at the 10% level and the between-group difference test suest coefficient is significant at the 1% level. It shows that the higher the reliance on shadow banking financing under the NAMR is, the more efficient the innovation will be.

7.2 Financing constraints

This study explores whether the NAMR promotes or inhibits the innovation efficiency of tech-based SMEs with severe financing constraints. The SA index is chosen as a proxy variable for financing constraint (FFC), and the larger the value is, the more serious the degree of financing constraint will be. The same grouping is performed: when the SA index is higher than the median of the sample industry year, it is divided into the high financing constraint group, otherwise it is divided into the low financing constraint group. Columns (3) and (4) of Table 7 show that the regression coefficient of the interaction term POST × CAR_ad and IE in the high financing constraint group is significantly positive at the 1% level; while the low financing constraint group is significant at the 5% level, and the between-group difference test suest coefficient is significant at the 5% level. It implies that the contraction of shadow banking under the NAMR is more likely to enhance the innovation efficiency of tech-based SMEs with severe financing constraints. It further verifies the hypothesis of “financing efficiency view”.

8 Research conclusions and implications

8.1 Research conclusions

This study explores the impact of shadow banking contraction on the innovation efficiency of tech-based SMEs and its mechanism of action, based on the NAMR for public comment back issued in 2017. The study finds that the innovation efficiency of tech-based SMEs is improved under the impact of shadow banking contraction caused by the NAMR; the mechanism test finds that the contraction of shadow banks under the NAMR can optimize the debt financing structure of tech-based SMEs, reduce their financing costs and financing risks, and ultimately accelerate their innovation efficiency by improving financing efficiency, which supports the hypothesis of “financing efficiency view”; further tests find that for tech-based SMEs with higher reliance on shadow banks and more severe financing constraints, the contraction of shadow banks under the NAMR improves their innovation efficiency.

8.2 Implications

This study has important insights: firstly, the role of the NAMR policy under the new situation needs to be deeply understood from multiple perspectives. On the one hand, for non-tech SMEs, it is likely to restrict some of their financing channels, resulting in insufficient daily liquidity. However, on the other hand, the findings exclude the “financing constraint view” hypothesis and support the “financing efficiency view” hypothesis, indicating that the NAMR improves the financing efficiency of tech-based SMEs and accelerates the innovation efficiency. Therefore, in the long term, the NAMR has more advantages for tech-based SMEs, and its prevention of systemic risks, promotion of financing balance, and superior innovation efficiency can better contribute to national innovation activities and support the development of the real economy.

Secondly, how China will follow up on the steady progress of the policy implementation of the NAMR. At this stage, under the severe impact of the COVID-19 on the global economy, the extension of the transition period of the NAMR to the end of 2021 is conducive to relieving the pressure of financial institutions to rectify the situation. The subsequent steady implementation of the NAMR requires policy coordination between the capital market and the insurance market, and efforts to achieve a dynamic balance between financial risk prevention and control to and serve the real economy and go hand in hand with the interest rate market reform.

Finally, in the future, China needs to explore and develop more ways to broaden the financing channels of tech-based SMEs. At this stage, the scale of bank credit to undertake off-balance sheet financing contraction is still limited, the vigorous development of multi-level financial markets is on high demand for the future, more policies need to be formulated to expand the financing channels of tech-based SMEs. Only when all these demands are met, can the function of financial services entities be strengthened and the sustainable development of national innovation be promoted.

Notes

Announcement of the People’s Bank of China on the New Asset Management Regulation policy for public comment back (Draft for Comments). http://www.pbc.gov.cn/rmyh/105208/3420439/index.html.

The data are obtained from the China CEInet Statistics Database, which is a huge economic statistical database group organized by China National Information Center through specialized processing by virtue of its good cooperation with national government departments. In Fig. 1, the vertical axis represents the average growth scale in the size of shadow banking (the size of shadow banking in the current period minus the size of shadow banking in the previous period), and the horizontal axis reflects the time in semi-annual basis.

The reason for using 2019 as the final year is that Chinese firms’ business conditions continue to fluctuate in the context of the COVID-19 that started to emerge in China at the end of 2019, which means that the relevant firm data become abnormal from 2020 onwards, and therefore, we need to exclude the special samples after 2019. The reason for using 2015 as the starting year of the study is that on November 17, 2017, the NAMR for public comment back was released, and since 2019 is the final year of the study, in order to avoid interference from other events due to the long duration of the previous data, 2015 is chosen as the starting year to achieve a symmetrical and balanced sample period centered on the time of the event.

China Baidu index reflects the search scale of a keyword in China Baidu website, which is calculated by weighting the searched frequency of each webpage keyword, the higher the index, the higher the attention of netizens.

In Fig. 2, the horizontal axis represents the number of days from the event date, and the vertical axis reflects the Baidu index.

References

Agnello, L., Castro, V., Jawadi, F., & Sousa, R. M. (2020). How does monetary policy respond to the dynamics of the shadow banking sector? International Journal of Finance & Economics, 25(2), 228–247. https://doi.org/10.1002/ijfe.1748.

Allen, F., & Gu, X. (2021). Shadow banking in China compared to other countries. The Manchester School, 89(5), 407–419. https://doi.org/10.1111/manc.12331.

Allen, F., Qian, Y., Tu, G., & Yu, F. (2019). Entrusted loans: a close look at China’s shadow banking system. Journal of Financial Economics, 133(1), 18–41. https://doi.org/10.1016/j.jfineco.2019.01.006.

An, P., & Yu, M. (2018). Neglected part of shadow banking in China. International Review of Economics & Finance, 57, 211–236. https://doi.org/10.1016/j.iref.2018.01.005.

Benfratello, L., Schiantarelli, F., & Sembenelli, A. (2008). Banks and innovation: microeconometric evidence on Italian firms. Journal of Financial Economics, 90(2), 197–217. https://doi.org/10.1016/j.jfineco.2008.01.001.

Bleakley, H., & Cowan, K. (2010). Maturity mismatch and financial crises: evidence from emerging market corporations. Journal of Development Economics, 93(2), 189–205. https://doi.org/10.1016/j.jdeveco.2009.09.007.

Borisova, G., & Brown, J. R. (2013). R&D sensitivity to asset sale proceeds: new evidence on financing constraints and intangible investment. Journal of Banking & Finance, 37(1), 159–173. https://doi.org/10.1016/j.jbankfin.2012.08.024.

Carbo-Valverde, S., Rodriguez-Fernandez, F., & Udell, G. F. (2009). Bank market power and SME financing constraints. Review of Finance, 13(2), 309–340. https://doi.org/10.1093/rof/rfp003.

Chen, L., Chen, Z., & Li, J. (2019). Can trade credit maintain sustainable R&D investment of SMEs? —Evidence from China. Sustainability, 11(3), 843. https://doi.org/10.3390/su11030843.

Chernenko, S., & Sunderam, A. (2014). Frictions in shadow banking: evidence from the lending behavior of money market mutual funds. The Review of Financial Studies, 27(6), 1717–1750. https://doi.org/10.1093/rfs/hhu025.

Cornaggia, J., Mao, Y., Tian, X., & Wolfe, X. (2015). Does banking competition affect innovation? Journal of Financial Economics, 115(1), 189–209. https://doi.org/10.1016/j.jfineco.2014.09.001.

Cressy, R., & Olofsson, C. (1997). European SME financing: an overview. Small Business Economics, 9(2), 87–96. https://www.jstor.org/stable/40228632.

Crick, D., & Jones, M. V. (2000). Small high-technology firms and international high-technology markets. Journal of International Marketing, 8(2), 63–85. https://doi.org/10.1509/jimk.8.2.63.19623.

Cruz-Cázares, C., Bayona-Sáez, C., & García-Marco, T. (2013). You can’t manage right what you can’t measure well: technological innovation efficiency. Research Policy, 42(6–7), 1239–1250. https://doi.org/10.1016/j.respol.2013.03.012.

Duca, J. V. (2016). How capital regulation and other factors drive the role of shadow banking in funding short-term business credit. Journal of Banking & Finance, 69, S10–S24. https://doi.org/10.1016/j.jbankfin.2015.06.016.

Efthyvoulou, G., & Vahter, P. (2016). Financial constraints, innovation performance and sectoral disaggregation. The Manchester School, 84(2), 125–158. https://doi.org/10.1111/manc.12089.

Gomariz, M. F. C., & Ballesta, J. P. S. (2014). Financial reporting quality, debt maturity and investment efficiency. Journal of Banking & Finance, 40, 494–506. https://doi.org/10.1016/j.jbankfin.2013.07.013.

Gong, X. L., Xiong, X., & Zhang, W. (2021). Shadow banking, monetary policy and systemic risk. Applied Economics, 53(14), 1672–1693. https://doi.org/10.1080/00036846.2020.1841088.

Gopalan, R., Song, F., & Yerramilli, V. (2014). Debt maturity structure and credit quality. Journal of Financial and Quantitative Analysis, 49(4), 817–842. https://doi.org/10.1017/S0022109014000520.

Greenland, A. N., Ion, M., Lopresti, J. W., & Schott, P. (2020). Using equity market reactions to infer exposure to trade liberalization. National Bureau of Economic Research. https://doi.org/10.2139/ssrn.3640803.

Grochulski, B., & Zhang, Y. (2019). Optimal liquidity policy with shadow banking. Economic Theory, 68(4), 967–1015. https://doi.org/10.1007/s00199-018-1152-6.

Guo, L., & Xia, D. (2014). In search of a place in the sun: the shadow banking system with Chinese characteristics. European Business Organization Law Review, 15(3), 387–418. https://doi.org/10.1017/S1566752914001189.

Harford, J., Klasa, S., & Walcott, N. (2009). Do firms have leverage targets? Evidence from acquisitions. Journal of Financial Economics, 93(1), 1–14. https://doi.org/10.1016/j.jfineco.2008.07.006.

Hoffman, K., Parejo, M., Bessant, J., & Perren, L. (1998). Small firms, R&D, technology and innovation in the UK: a literature review. Technovation, 18(1), 39–55. https://doi.org/10.1016/S0166-4972(97)00102-8.

Irani, R. M., Iyer, R., Meisenzahl, R. R., & Peydró, J. (2021). The rise of shadow banking: evidence from capital regulation. The Review of Financial Studies, 34(5), 2181–2235. https://doi.org/10.1093/rfs/hhaa106.

Le, V. P. M., Matthews, K., Meenagh, D., Minford, P., & Xiao, Z. (2020). China’s market economy, shadow banking and the frequency of growth slowdown. The Manchester School, 89(5), 420–444. https://doi.org/10.1111/manc.12318.

Lin, C., Morck, R., Yeung, B. Y., & Zhao, X. (2016). Anti-corruption reforms and shareholder valuations: event study evidence from China. SSRN. https://doi.org/10.2139/ssrn.2729087.

Lu, Y., Guo, H., Kao, E. H., & Fung, H. (2015). Shadow banking and firm financing in China. International Review of Economics & Finance, 36, 40–53. https://doi.org/10.1016/j.iref.2014.11.006.

Madrid-Guijarro, A., García-Pérez-de-Lema, D., & Auken, H. V. (2016). Financing constraints and SME innovation during economic crises. Academia Revista Latinoamericana De Administracin, 29(1), 84–106. https://doi.org/10.1108/ARLA-04-2015-0067.

Maes, E., Dewaelheyns, N., Fuss, C., & Hulle, C. V. (2019). The impact of exporting on financial debt choices of SMEs. Journal of Business Research, 102, 56–73. https://doi.org/10.1016/j.jbusres.2019.05.008.

Manzaneque, M., Rojo-Ramírez, A. A., Diéguez-Soto, J., & Martínez-Romero, M. J. (2020). How negative aspiration performance gaps affect innovation efficiency. Small Business Economics, 54(1), 209–233. https://doi.org/10.1007/s11187-018-0091-8.

Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. https://doi.org/10.1016/0304-405X(84)90023-0.

Pederzoli, C., Thoma, G., & Torricelli, C. (2013). Modelling credit risk for innovative SMEs: the role of innovation measures. Journal of Financial Services Research, 44(1), 111–129. https://doi.org/10.1007/s10693-012-0152-0.

Petersen, M. A., & Rajan, R. G. (1994). The benefits of lending relationships: evidence from small business data. The Journal of Finance, 49(1), 3–37. https://doi.org/10.1111/j.1540-6261.1994.tb04418.x.

Qiao, P., & Fung, A. (2016). How does CEO power affect innovation efficiency? The Chinese Economy, 49(4), 231–238. https://doi.org/10.1080/10971475.2016.1179017.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The journal of finance, 19(3), 425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x.

Silva, F., & Carreira, C. (2012). Do financial constraints threat the innovation process? Evidence from Portuguese firms. Economics of Innovation and New Technology, 21(8), 701–736. https://doi.org/10.1080/10438599.2011.639979.

Tse, M. K. S., & Wong, K. P. (2011). Liquidity risk and corporate hedging with futures. Pacific Economic Review, 16(2), 229–235. https://doi.org/10.1111/j.1468-0106.2011.00544.x.

Wang, C., Le, V. P. M., Matthews, K., & Zhou, P. (2021). Shadow banking activity and entrusted loans in a DSGE model of China. The Manchester School, 89(5), 445–469. https://doi.org/10.1111/manc.12319.

Wu, M. W., & Shen, C. H. (2019). Effects of shadow banking on bank risks from the view of capital adequacy. International Review of Economics & Finance, 63, 176–197. https://doi.org/10.1016/j.iref.2018.09.004.

Xie, L., Zhou, J., Zong, Q., & Lu, Q. (2020). Gender diversity in R&D teams and innovation efficiency: role of the innovation context. Research Policy, 49(1), 103885. https://doi.org/10.1016/j.respol.2019.103885.

Xin, F., Zhang, J., & Zheng, W. (2017). Does credit market impede innovation? Based on the banking structure analysis. International Review of Economics & Finance, 52, 268–288. https://doi.org/10.1016/j.iref.2017.01.014.

Yang, L., Wijnbergen, S. V., Qi, X., & Yi, Y. (2019). Chinese shadow banking, financial regulation and effectiveness of monetary policy. Pacific-Basin Finance Journal, 57, 101169. https://doi.org/10.1016/j.pacfin.2019.06.016.

Yu, C. H., Wu, X., Zhang, D., Chen, S., & Zhao, J. (2021). Demand for green finance: resolving financing constraints on green innovation in China. Energy Policy, 153, 112255. https://doi.org/10.1016/j.enpol.2021.112255.

Zhou, L. J., Zhang, X., & Sha, Y. (2021). The role of angel investment for technology-based SMEs: evidence from China. Pacific-Basin Finance Journal, 67, 101540. https://doi.org/10.1016/j.pacfin.2021.101540.

Zhu, Y., Wittmann, X., & Peng, M. W. (2012). Institution-based barriers to innovation in SMEs in China. Asia Pacific Journal of Management, 29(4), 1131–1142. https://doi.org/10.1007/s10490-011-9263-7.

Funding

This work was Funded by the Fundamental Research Funds for the Central Universities [2020YJS061] (China); The National Social Science Foundation of China [19BGJ001].

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Yu, Z., Xiao, X. Shadow banking contraction and innovation efficiency of tech-based SMEs-based on the implementation of China’s New Asset Management Regulation. Eurasian Bus Rev 12, 251–275 (2022). https://doi.org/10.1007/s40821-021-00201-0

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40821-021-00201-0

Keywords

- New Asset Management Regulation

- Shadow banking contraction

- Innovation efficiency

- Financing constraints

- Financing efficiency