Abstract

In the age of rapid technological advancement and digitization, coordination strategy remains an important issue for the supply chain. Additionally, the uncertainty caused by the disruption often induces the risk aversion in the supply chain members. Motivated by this issue, here we propose a coordination mechanism for a risk-averse supply chain using mean–variance approach. Here, we consider both centralized and decentralized cases and show that our analysis holds good for a central planner as well as for a decentralized supply chain under channel coordinating contracts such as buyback and revenue-sharing schemes. With the help of theoretical and numerical analysis, we exhibit how an individual supply chain agent’s risk aversion behavior can impact the contracts selection mechanism - from the profitability perspective. We extend our analysis to a dyadic setting to a single-supplier multiple-retailer network and confirm that pure strategy Nash equilibrium exists when all the retailers are risk-averse with varying risk attitude.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction and literature review

Global supply chains are complex multi-echelon systems consisting of numerous agents. Due to rapid technological advancements, digitization, and a strive to improve operational efficiency, supply chains are increasingly becoming decentralized in nature. Firms are often relying on decentralization-enabling technologies such as blockchains to manage their decentralized supply chains (Catalini and Gans 2016; Alzahrani and Bulusu 2018). However, these global supply chains often become vulnerable as they face different kinds of uncertainties and risks. For example, if a supplier firm employs a direct sales channel with traditional retailers, it exposes her to risk due to conflict from vertical as well as horizontal competition (Tsay and Agrawal 2004; Yao and Liu 2005). The political instability of a region (Peck 2005), natural disasters (Tomlin 2006) are other primary sources of supply chain risk because of their disruptive effects. As the uncertainties and the risks associated with supply chain decisions are increasing day by day, the risk-neutrality assumption seems to be inadequate (Wu et al. 2009; Katariya et al. 2013; Zhuo et al. 2018) from the perspective of supply chain coordination. In this context application of predictive analytics and associated models become crucial for devising optimal results for a firm. Predictive analytics enables supply chain managers to arrive at optimal decisions based on external market conditions. During the recent outbreak of the COVID-19 pandemic, supply chains are facing liquidity crunchFootnote 1 coupled with reduced demand in the markets Footnote 2. As a result, businesses are increasingly turning risk-averseFootnote 3. Modelling the channel coordination mechanism for a risk-averse firm using predictive analytics is typically based on game-theoretical techniques (Souza 2014). In this paper, we focus on such a modeling technique for a risk-averse dyadic supply chain.

In supply chain management, the classical newsvendor problem-solving approach is employed to design channel coordinating supply contracts. Buyback contracts (Pasternack 2008; Cachon 2003); revenue-sharing contract (Pasternack 2005; Cachon and Lariviere 2005; Giri and Bardhan 2012), and quantity discount contract (Huang et al. 2011) are some instances of channel coordination mechanisms. However, these mechanisms do not consider the risk attitude of the agent and focus on the objective of either maximizing the expected profit or minimizing the expected cost.

Scholars have adopted a multitude of approaches to incorporate the risk-averse nature of the members of a supply chain. Examples include mean–variance (MV) analysis (Lau 1980; Choi et al. 2008a, b; Wu et al. 2009; Wei and Choi 2010; Katariya et al. 2013), conditional value-at-risk (CVaR) minimization (Gotoh and Takano 2007; Chen et al. 2009; Li et al. 2014; Soleimani et al. 2014), and expected-utility (EU) maximization (Horowitz 1970; Eeckhoudt et al. 1995; Keren and Pliskin 2006). The MV framework enables investors to analyze risk diversification of assets and helps them to design an optimal portfolio (Markowitz 1959). This framework has been explored extensively by scholars within the realm of supply chain management to address supply chain risks, particularly those arising from uncertain market demand (Chiu and Choi 2016; Choi and Chiu 2012; Liu et al. 2016). We further observe that in supply chain management both MV approach and von Neumann–Morgenstern utility (VNMU) approach are employed by scholars for studying optimal supply chain decisions under risk. In spite of being a precise approach, usage of VNMU approach is limited due to the difficulty in estimating an individual’s utility function in practice (Choi et al. 2008a, b). On the other hand, the MV approach aims at providing an implementable, useful, and approximate solution (Van Mieghem 2003; Buzacott et al. 2003).

In the context of MV analysis, there are three distinct ways to compute the objective(s) of a supply chain agent: (i) she tries to maximize the difference between the expected profit and a product multiplier of the variance of the profit (Wu et al. 2009; Katariya et al. 2013), (ii) she tries to maximize the expected profit while restricting its variance within a pre-defined level (Wei and Choi 2010), (iii) she attempts to minimize the variance of the profit, thereby ensuring her expected profit to exceed a pre-defined minimum threshold (Choi et al. 2008a, b; Choi and Chiu 2012). Choi et al. (2008a, b) show that the channel coordination in a two-tier supply-chain structure is a function of the net difference between the risk preferences of the supplier and the retailer. They conclude that coordination in the supply chain is not achievable in the presence of a highly risk-averse retailer. Wei and Choi (2010) propose a wholesale price and a profit-sharing mechanism that coordinates the supply chain, depending on the risk-aversion threshold of the retailer.

While MV analysis follows the maximization of the difference between expected profit and risk-attitude multiplier of the variance of profit, Lau (1980) have established that the optimal order quantity for a risk-averse agent would be less than that for a risk-neutral one without considering the shortage cost. Wu et al. (2009) have demonstrated that a risk-averse newsvendor can order more than a risk-neutral one by incorporating stock-out costs in their analysis. Katariya et al. (2013) show that under the MV criterion, a comparison between the optimal order quantities of the risk-neutral and risk-averse newsvendors depends solely on the model parameters and the nature of demand distribution chosen. As a result, channel coordination exercises under the MV criterion becomes parameter-dependent exclusively.

In this paper, we attempt to answer the following questions:

-

1.

Is channel coordination in a risk-averse supply chain dependent on parameters (or preferences) of individual supply chain agents?

-

2.

Is it possible for a supplier to coordinate a supply chain network consisting of a single supplier and multiple retailers where the retailers are all risk-averse?

In this paper, we derive the general condition for MV objective-maximization of a risk-averse supply chain. We consider both centralized and decentralized cases and show that our analysis holds good for a central planner as well as for a decentralized supply chain under channel coordinating contracts such as buyback and revenue-sharing schemes. Existing studies by Choi et al. (2008a, b) and Wei and Choi (2010) demonstrate that specially-designed contracts can achieve coordination in a risk-averse supply chain. We show that conventional contract forms, such as buyback and revenue-sharing schemes, can also lead to channel coordination. In the context of a two-tier supply chain structure, we first analyze the optimality conditions of a centralized risk-averse supply chain, which subsequently serves as a benchmark in our study. We further establish that an agent’s MV optimization is dependent solely on the prior demand distribution. We prove that the maximizing condition is independent of the model parameters—a finding hitherto unreported in the extant literature. As a consequence of this novel finding, we successfully propose a relatively simplified technique to calculate the optimal order quantity compared to the existing mechanisms. Supported by extensive numerical analysis, we report interesting insights on how the risk aversion behavior of an individual supply chain agent can impact the contract selection mechanism, especially from the profitability perspective. We extend our analysis to a dyadic setting with a single-supplier multiple-retailer network and confirm that a pure-strategy Nash equilibrium exists when all the retailers are risk-averse with varying risk attitudes. We also establish the range of values for the risk-aversion parameter within which this pure Nash solution holds. Such analysis can assist supply-chain managers in designing their optimal supply contract forms in the context of a supply chain network.

The rest of the paper is organized as follows. In Sect. 2, we analyze the centralized supply chain under mean–variance approach with three contract forms, compare between risk shares, and develop the criterion to achieve channel coordination. In Sect. 3, we extend our analysis to a single-supplier multiple-retailers supply chain network when all the retailers are risk-averse and possess different risk attitude. We analytically investigate the condition(s) under which a pure-strategy Nash equilibrium may exist for such a game. In Sect. 4, we conclude our study by discussing our key findings and future research avenues.

Mean–variance model of a risk-averse supply chain

We consider a dyadic supply chain comprising one supplier and one retailer. The retailer experiences stochastic demand \(x\) during the selling season. Let \(F\) represent the cumulative distribution of that demand and \(f\) is its density function. We assume that \(F\) is differentiable and strictly increasing. Let the retail price be \(p\), and at this price, the retailer’s order quantity be \(q\). The supplier’s unit production cost is \(s\) and the retailer’s marginal cost per unit is \(c\). The retailer sells her season-end left-over inventory at per unit salvage price \(v\;\left( { < c} \right){\kern 1pt} \,\). For expositional simplicity, both retail price (\(p\)) and salvage price (\(v\)) are exogenous to our model. To avoid triviality, we assume: \(0 < v < c < p\). Therefore, the expected sales \(S\left( q \right)\) and the expected left-over inventory \(I\left( q \right)\) can be expressed as,

where \(T\left( \cdot \right)\) is the expected transfer payment that the retailer pays to the supplier. A transfer payment is a function of the order quantity, left-over inventory, and the contract offered by the supplier. Let \(E\left[ {\pi_{R} \left( q \right)} \right]\) and \(E\left[ {\pi_{S} \left( q \right)} \right]\) denote the expected profits of the retailer and the supplier, given by Eqs. (1) and (2) respectively.

First, we analyze the optimality condition(s) for the centralized supply chain. Subsequently, we study the decentralized supply chain and compute the expected profit and variance of the individual supply chain agents.

Centralized supply chain

In the case of a centralized supply chain, the supplier and the retailer are vertically integrated. The expected profit \(E\left[ {\pi_{C} \left( q \right)} \right]\) of such a centralized system can be easily computed by adding Eqs. (1) and (2) to get (3), so that

where \(\pi_{C} \left( q \right)\) designates the randomized profit of the centralized supply chain, represented by (3) and is given by

Mean–Variance (MV) analysis employs a risk-aversion parameter \(\alpha \;\left( { \ge 0} \right)\) to characterize the risk aversion attitude of a supply chain agent (Wu et al. 2009). It signifies a quantitative balance between the expected profit and the risk associated with its variance. For a risk-neutral agent, \(\alpha\) is zero, while it is positive-valued for a risk-averse agent (Wu et al. 2009). An increase in \(\alpha\) indicates a rise in the agent’s willingness to forego her expected profit and avoid the associated risks. Under the MV framework, Eq. (5) represents the objective of the central planner.

where \(\alpha_{C}\) denotes the risk aversion attitude of the overall centralized supply chain. Now, the variance of the centralized supply chain profit can be defined as:

Using Eqs. (3) and (4), \(Var\left[ {\pi_{C} \left( q \right)} \right]\) can be represented as

From (3), it is evident that the expected profit \(E\left[ {\pi_{C} \left( q \right)} \right]\) is concave in \(q\), although the variance may be unbounded. For such reasons, the presence of a unique optimum is not always guaranteed (Wu et al. 2009). We apply the change in the order of integration and the properties of truncated distribution, to arrive at the following maximizing criterion from the first- and second-order conditions of Eq. (5).

Theorem 1

The order quantity decision ( \(q^{*}\) ) of the central planner can be calculated as:

which maximizes her objective function if and only if it additionally satisfies \(q.\,r\left( q \right) \le \frac{1}{1 - E\left( \xi \right)}\) , where \(r\left( \cdot \right) = \frac{f\left( \cdot \right)}{{1 - F\left( \cdot \right)}}\) is the failure rate of the demand distribution \(x\) , \(\xi = {Y \mathord{\left/ {\vphantom {Y q}} \right. \kern-\nulldelimiterspace} q}\) , and \(Y\) is a random variable that corresponds to the truncated distribution of demand \(x\) over \(\left[ {0,\,\,q} \right]\) .

Proof

The proof is provided in Appendix.

From Theorem 1, we observe that the optimality of ordering decisions relies only on the prior demand distribution. This result marks a significant improvement over existing works of Choi et al. (2008a, b), and Katariya et al. (2013), because it concludes that the optimality of the ordering decision depends both on the model parameter and the demand distribution. The closed-form solution of the optimal order quantity is straightforward and can be obtained from Eq. (7), and holds for different distributions. Otherwise, the optimal order quantity can be easily determined by employing a suitable one-dimensional search algorithm with a risk-neutral central planner’s order quantity decision as an initial solution. Also, we need to calculate only one expression, \(\int\nolimits_{0}^{q} {F\left( x \right)dx}\)-which we can compute with the help of the numerical integration method, and which has a closed-form solution for many distributions. Our technique poses significant computational simplicity over the method proposed by Lau (1980). Additionally, we report a significant improvement over Wu et al. (2009), that required the computation of both \(\int\nolimits_{0}^{q} {F\left( x \right)dx}\) and \(\int\nolimits_{0}^{q} {xF\left( x \right)dx}\). From Eq. (7) we also observe that the optimal order quantity (\(q^{*}\)) is decreasing in the central planner’s risk attitude (\(\alpha_{C}\)).

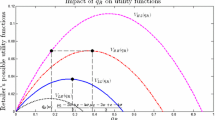

Through a numerical example, we demonstrate the implications of Theorem 1. For this purpose, we consider the following parametric values for our dyadic supply chain: (i) demand is discrete ~ U[0, 20]; (ii) per unit retail price, p = 10, (iii) per unit production cost, c = 5, (iv) per unit salvage price, s = 2. The risk aversion attitude, \(\alpha_{C}\) of the central planner, varies between 0.01 and 0.02. Figure 1 presents the effect of order quantity and risk-aversion attitude on the mean–variance payoff for a central planner.

Mean–Variance payoff v/s Order quantity and Risk Aversion Attitude of a central planner

From Fig. 1, we observe the following:

-

i.

For a given value of risk aversion attitude \(\alpha_{C}\), the mean–variance payoff for the central planner first increases and subsequently decreases.

-

ii.

For a given value of order quantity \(q^{*}\), the mean–variance payoff decreases with an increase in the value of risk aversion attitude \(\alpha_{C}\).

-

iii.

This aforementioned decrease is higher when the order quantity is large, and it is lower when the order quantity is small.

Therefore, from Fig. 1, we can easily infer that the optimal order quantity of a risk-averse central planner decreases in its risk aversion attitude. For example, at \(\alpha_{C} = 0.011\), the optimal order quantity is: \(q^{*} = 9\), and at \(\alpha_{C} = 0.019\), optimal order quantity is: \(q^{*} = 7\), whereas the optimal order quantity for a risk-neutral central planner is \(q^{*} = 13\) with the same parametric value of the supply chain.

Decentralized supply chain and discussion on channel coordinating contracts

Next, we consider a decentralized supply chain. Here, the supplier offers contractual terms to the retailer, and accordingly, they decide the transfer payment options. We study the MV criterion in a decentralized supply chain under three types of contract: (i) wholesale price, (ii) buyback, and (iii) revenue-sharing. These contracts have been extensively discussed in the extant literature in the context of supply chain coordination involving risk-neutral agents. Cachon (2003) provides a comprehensive survey of this relevant literature.

We compare expected profit levels and associated risks for both supplier and retailer for all three contracts. The expected transfer payment functions and description of contract parameters are presented in Table 1.

Using the transfer payment functions in Eqs. (1) and (2), we calculate the expected profit-levels and associated risks for the supplier and retailer. The optimization problem of a decentralization supply chain is given by the following equations:

In the aforementioned equation, \((w,b = 0,\phi = 0)\) represents wholesale price contract, \((w,b,\phi = 0)\) represents buyback contract, and \((w,b = 0,\phi )\) represents revenue-sharing contract. Then, we compare the variance of profits from the centralized and the centralized cases and present the results in Table 2. The associated calculations are presented in Appendix.

From Table 2, we observe the following about the three types of supply contracts considered in our study.

Observation 1

-

i.

In the case of a wholesale price contract, the retailer bears the entire risk of the supply chain.

-

ii.

For the buyback contract, the supplier’s risk \(\left[ {Var\left\{ {\pi_{S,BB} \left( q \right)} \right\}} \right]\) is more than that of the retailer \(\left[ {Var\left\{ {\pi_{R,BB} \left( q \right)} \right\}} \right]\) iff \(b > {p \mathord{\left/ {\vphantom {p 2}} \right. \kern-\nulldelimiterspace} 2}\), i.e., the buyback price is more than half of the retail price. At \(b = {p \mathord{\left/ {\vphantom {p 2}} \right. \kern-\nulldelimiterspace} 2}\), the risk shares of the supplier and the retailer are equal. The retailer bears more risk than the supplier when \(b < {p \mathord{\left/ {\vphantom {p 2}} \right. \kern-\nulldelimiterspace} 2}\).

-

iii.

In the context of a revenue-sharing contract, the supplier’s risk \(\left[ {Var\left\{ {\pi_{S,RS} \left( q \right)} \right\}} \right]\) is more than that of the retailer \(\left[ {Var\left\{ {\pi_{R,RS} \left( q \right)} \right\}} \right]\) iff \(\phi < {1 \mathord{\left/ {\vphantom {1 2}} \right. \kern-\nulldelimiterspace} 2}\), i.e., the supplier allows the retailer to retain less than 50% of the total revenue. Otherwise, the retailer bears more risk than the supplier. At \(\phi = {1 \mathord{\left/ {\vphantom {1 2}} \right. \kern-\nulldelimiterspace} 2}\) the supplier and the retailer share equal risk.

From Observation 1, it is evident that in the case of buyback and revenue-sharing contracts, risk-sharing by supply chain agents is dependent on the model parameters. However, in the case of a wholesale price contract, the risk-sharing is independent of the model parameters.

Since full information is available with all the agents, the supplier knows whether the retailer is risk-averse as well as the value of the retailer’s risk attitude (\(\alpha_{R}\)); she can further anticipate that a risk-averse retailer’s order quantity would be less than that of a risk-neutral one. Under such circumstances, as a second-best strategy, the supplier can employ a buyback contract to coordinate the supply chain with a risk-averse retailer if the risk-averse centralized supply chain is considered as a benchmark. Wei and Choi (2010) adopted a similar approach for deciding a coordination strategy for a risk-averse supply chain.

Proposition 1

The following two parameters define the channel coordinating buyback contract:

-

(i)

the price charged per unit: \(w_{b} = \left( {1 - \lambda } \right)\left( {p - c} \right) + \lambda s\)

-

(ii)

the buyback price: \(b = \left( {1 - \lambda } \right)p + \lambda v\)

where \(\lambda\) is the proportion of centralized supply chain profit that the supplier allows the retailer to retain. The retailer’s order quantity is equal to that of a central planner with a risk attitude \(\alpha_{C} = \lambda \alpha_{R}\) and as \(\alpha_{C} < \alpha_{R}\) , optimal ordering decision \(q_{BB}^{*} \left( {\lambda \alpha_{R} } \right) > q_{BB}^{*} \left( {\alpha_{R} } \right)\) .

Proof:

The proof is provided in Appendix.

Under a coordinating buyback contract, the retailer’s order quantity \(\left( {q_{BB}^{*} } \right)\) is equal to that of the centralized supply chain with risk attitude \(\alpha_{C} = \lambda \alpha_{R}\). As \(0 < \lambda < 1\), we have: \(\alpha_{C} < \alpha_{R}\). Following the argument presented in Theorem 1, we observe that the retailer’s order quantity is decreasing in \(\alpha_{R}\). Therefore, intuitively we can comprehend that under the coordinating buyback contract, the retailer orders more than what she would have ordered otherwise. The retailer’s order quantity also maximizes her mean–variance objective if it satisfies the following: \(q.\,r\left( q \right) \le \frac{1}{1 - E\left( \xi \right)}\). Defining the salvage price as \(v = \beta {\kern 1pt} p\;\left( {0 < \beta < 1} \right)\) we further observe that the risk-share of the supplier would be less than that of the retailer for \(\lambda < {1 \mathord{\left/ {\vphantom {1 {\left( {2 + \beta } \right)}}} \right. \kern-\nulldelimiterspace} {\left( {2 + \beta } \right)}}\).

Similarly, the supplier can also coordinate the supply chain with a risk-averse retailer by employing a revenue-sharing contract, if the risk-averse centralized supply chain is considered as a benchmark. The channel coordinating revenue-sharing contract then takes the following form:

Proposition 2

In the case of a revenue-sharing contract, if the sharing parameter \(\phi\) also designates the proportion of a centralized supply chain profit that the supplier allows the retailer to retain, then the supplier can coordinate the supply chain by setting the per-unit price as \(w_{r} = \phi \,s - \left( {1 - \phi } \right)\,c\) . The retailer’s order quantity is equal to that of a central planner with a risk attitude \(\alpha_{C} = \phi \alpha_{R}\) and as \(\alpha_{C} < \alpha_{R}\) , the optimal ordering decision follows: \(q_{RS}^{*} \left( {\phi \alpha_{R} } \right) > q_{RS}^{*} \left( {\alpha_{R} } \right)\) .

Proof

The proof is provided in Appendix.

In the case of a revenue-sharing contract, we observe that if the retailer’s order quantity satisfies: \(q.\,r\left( q \right) \le \frac{1}{1 - E\left( \xi \right)}\) , it would maximize her mean–variance objective. Therefore, the optimality criterion for the order quantity decision, as presented in Theorem 1, holds not only for the centralized but also for decentralized decision-making under coordination mechanism. Theorem 1 provides us with a generalized framework to evaluate the mean–variance objective of a risk-averse supply chain agent for both centralized and decentralized supply chain. The optimality criterion of ordering decision is independent of the model parameter. Instead, it depends only on the demand distribution.

Extension of mean–variance (MV) analysis for a risk-averse supply chain network

We consider a supply chain network with one supplier and N risk-averse retailers. The retailers sell substitutable products in the same market. The ith retailer faces a market demand \(L_{i} \left( {\vec{p}} \right) + \varepsilon_{i}\) during a single selling season, where \(\vec{p} = \left( {p_{1} ,p_{2} ,..,p_{N} } \right)\). \(L_{i} \left( {\vec{p}} \right)\) considers the deterministic component of the demand and follows the economics of price-based competition: (i) \({{\partial L_{i} \left( {\vec{p}} \right)} \mathord{\left/ {\vphantom {{\partial L_{i} \left( {\vec{p}} \right)} {\partial p_{i} }}} \right. \kern-\nulldelimiterspace} {\partial p_{i} }} < 0\) and (ii) \({{\partial L_{i} \left( {\vec{p}} \right)} \mathord{\left/ {\vphantom {{\partial L_{i} \left( {\vec{p}} \right)} {\partial p_{j} }}} \right. \kern-\nulldelimiterspace} {\partial p_{j} }} > 0\). The conditions (i) and (ii) demonstrate own-price and cross-price elasticity of the demand, respectively, whereas \(\varepsilon_{i}\) represents the stochastic component of the demand. \(\left( {\varepsilon_{1} ,\varepsilon_{2} ,..,\varepsilon_{N} } \right)\) follow independent and previously known continuous distributions on the positive real axis.

At the beginning of the selling season, each retailer makes two decisions: (i) retail price,\(p_{i}\), and (ii) safety stock, \(y_{i}\). The safety stock helps the retailer to cater to the uncertain demand. The total order quantity of the ith retailer is: \(Y_{i} = L_{i} \left( {\vec{p}} \right) + y_{i}\). We also assume that a fixed proportion of the jth retailer’s lost sale switches to the ith retailer. Such demand switching activity is independent of the retail price. Therefore, the effective total demand faced by the ith retailer is given as: \(q_{i} \left( {\vec{p}} \right) = L_{i} \left( {\vec{p}} \right) + \varepsilon_{i} + \sum\nolimits_{j \ne i} {\gamma_{ji} \left( {\varepsilon_{j} - y_{j} } \right)}^{ + }\), where \(\gamma_{ji}\) designates the spill-rate received by the jth retailer lost from the ith retailer. The effective stochastic part of the demand of retailer i is given by: \(x_{i} = \varepsilon_{i} + \sum\nolimits_{j \ne i} {\gamma_{ji} \left( {\varepsilon_{j} - y_{j} } \right)}^{ + }\); where \(x_{i}\) is a non-negative random variable. Let \(F_{i} \left( \cdot \right)\) be the cumulative distribution of \(x_{i}\) and \(f_{i} \left( \cdot \right)\) be its density function. We assume that, \(F\) is differentiable and strictly increasing. We further assume that the failure rate of \(x_{i}\), defined as: \(h\left( \cdot \right) = \frac{f\left( \cdot \right)}{{1 - F\left( \cdot \right)}}\), is a weakly increasing function over the entire range of \(x_{i}\), indicating that \(x_{i}\) has an increasing failure rate (IFR). The supplier’s per-unit production cost to cater to the order quantity of the ith retailer is \(s_{i}\) and the retailer i’s marginal cost per unit is \(c_{i}\). Each retailer’s marginal cost is inclusive of her production, transportation, and other per-unit costs incurred. The supplier charges each retailer through a wholesale price contract, implemented through a per-unit price \(w_{i}\) for the ith retailer. For expositional simplicity, we consider the salvage price of excess quantity for each retailer to be zero. To avoid triviality, we assume: \(0 < c_{i} < w_{i} < p_{i}\).

Retailer i chooses \(p_{i}\) and \(y_{i}\) in order to maximize her mean–variance objective, such that:

The following set of equations gives the expected profit function of the ith retailer:

where, \(\pi_{i}^{d} \left( {\vec{p}} \right) = \left\{ {p_{i} - \left( {w_{i} + c_{i} } \right)} \right\}L_{i} \left( {\vec{p}} \right)\) is the profit generated due to the deterministic part of the demand. The firmness of the strategy is ensured by assuming the following:

The following equation gives the variance of profit:

Each retailer’s optimal decision for her retail price and order quantity is given by \(\left( {p_{i}^{*} ,Y_{i}^{*} } \right)\) and is otherwise represented as \(\left( {p_{i}^{*} ,y_{i}^{*} } \right)\), because \(Y_{i}^{*} = L_{i} \left( {\vec{p}^{*} } \right) + y_{i}^{*}\). The optimization problem of the decentralized supply chain network is described below.

Equation (13) represents the supplier’s optimization problem and equation (14) represents the optimization problem of retailer i.

Analysis of the Nash Equilibrium

Since every concave game has a Nash equilibrium (Geanakoplos 2003), we need to prove that the function \(MV_{i} \left( {p_{i} ,y_{i} } \right)\) is concave in \(\left( {p_{i} ,y_{i} } \right)\) to show that Nash equilibrium exists for our N risk-averse retailers’ game. We need the following two additional conditions to hold for establishing the existence of a pure-strategy Nash equilibrium:

-

(A)

\({{\partial^{2} \left\{ {\pi_{i}^{d} \left( {\vec{p}} \right)} \right\}} \mathord{\left/ {\vphantom {{\partial^{2} \left\{ {\pi_{i}^{d} \left( {\vec{p}} \right)} \right\}} {\partial p_{i}^{2} }}} \right. \kern-\nulldelimiterspace} {\partial p_{i}^{2} }} < 0\) and \({{\partial^{3} \left\{ {\pi_{i}^{d} \left( {\vec{p}} \right)} \right\}} \mathord{\left/ {\vphantom {{\partial^{3} \left\{ {\pi_{i}^{d} \left( {\vec{p}} \right)} \right\}} {\partial p_{i}^{3} }}} \right. \kern-\nulldelimiterspace} {\partial p_{i}^{3} }} \le 0\).

-

(B)

The distribution \(x_{i} = \varepsilon_{i} + \sum\nolimits_{j \ne i} {\gamma_{ji} \left( {\varepsilon_{j} - y_{j} } \right)}^{ + }\) has an increased failure rate (IFR).

Theorem 2

We assume that the conditions (A) and (B) hold. Then we have the following results for N risk-averse retailers’ game:

-

(i)

The MV objective of the i th retailer \(MV_{i} \left( {p_{i} ,y_{i} } \right)\) is jointly quasi-concave in \(\left( {p_{i} ,y_{i} } \right)\) iff the following condition is satisfied: \(1 - y_{i} r_{i} \left( {y_{i} } \right)\left[ {\frac{1}{{F_{i} \left( {y_{i} } \right)}} - E\left( {1 - \xi_{i} } \right)} \right] < 0\) , where \(\xi_{i} = {{\Psi_{i} } \mathord{\left/ {\vphantom {{\Psi_{i} } {y_{i} }}} \right. \kern-\nulldelimiterspace} {y_{i} }}\) and \(\Psi_{i}\) is a random variable that corresponds to the truncated distribution of demand \(x_{i}\) over \(\left[ {0,\,\,y_{i} } \right]\) .

-

(ii)

A pure-strategy Nash equilibrium exists for the game.

-

(iii)

The solution of Eqs. (11) – (12) gives the best response of the ith retailer.

$$\frac{{\partial \pi_{i}^{d} \left( {\vec{p}} \right)}}{{\partial p_{i} }} + E\left[ {\min \left( {x_{i} ,y_{i} } \right)} \right] - 2\alpha_{i} p_{i} \left[ {E\left[ {\min \left( {x_{i}^{2} ,y_{i}^{2} } \right)} \right] - \left\{ {E\left[ {\min \left( {x_{i} ,y_{i} } \right)} \right]} \right\}^{2} } \right] = 0$$(15)$$- \left( {w_{i} + c_{i} } \right) + p_{i} \Pr \left( {x_{i} > y_{i} } \right) - 2\alpha_{i} p_{i}^{2} \left\{ {y_{i} - E\left[ {\min \left( {x_{i} ,y_{i} } \right)} \right]} \right\}\Pr \left( {x_{i} > y_{i} } \right) = 0$$(16)

Proof

The proof is provided in Appendix.

From Theorem 2, we observe that the maximizing condition is dependent only on the safety stock of the retailer and not on the retail price. Theorem 2 also signifies that a pure-strategy Nash equilibrium can exist in the single-supplier multiple-retailer game when all the retailers are risk-averse with varying degrees of risk-aversion attitude. From Eqs. (15) to (16) we further observe that the interiority of the Nash solution would be dependent on the risk attitude (\(\alpha_{i}\)) for the ith retailer. If the risk attitude(s) satisfy the condition enumerated by Proposition 3, then we can conclude that the Nash solution would always be an interior solution.

Proposition 3

The maximizer of the MV objective function of the i th retailer is in the interior of the strategy set: \(\left( {p_{i} ,y_{i} } \right) \in \left\{ {\left( {w_{i} + c_{i} } \right) \le p_{i} \le p_{i}^{\max } \;and\;0 \le y_{i} \le y_{i}^{\max } } \right\}\) , when all the retailers are risk-averse with risk-aversion parameter satisfying the condition: \(\alpha_{i} < \min \left( {{\rm A}_{i} ,\,{\rm B}_{i} } \right)\) , where \({\rm A}_{i} = \frac{{p_{i} - \left( {w_{i} + c_{i} } \right)}}{{2p_{i}^{2} \left\{ {y_{i} - E\left[ {\min \left( {x_{i} ,y_{i} } \right)} \right]} \right\}}}\) and \({\rm B}_{i} = \frac{{\left. {L_{i} \left( {\vec{p}} \right)} \right|_{{p_{i} = \left( {w_{i} + c_{i} } \right)}} + E\left[ {\min \left( {x_{i} ,y_{i} } \right)} \right]}}{{2\left( {w_{i} + c_{i} } \right)\left[ {E\left[ {\min \left( {x_{i}^{2} ,y_{i}^{2} } \right)} \right] - \left\{ {E\left[ {\min \left( {x_{i} ,y_{i} } \right)} \right]} \right\}^{2} } \right]}}\) .

Proof

The proof is provided in Appendix.

Proposition 3 provides us with the boundary condition of the risk attitude of the retailers, which, in turn, ensures the existence of a pure-strategy Nash equilibrium for the single-supplier multiple-retailer game. However, the supplier cannot guarantee that the risk attitudes of the retailers would always exist within this specified range. Therefore, it is not possible to analytically prove that the maximizer would always be unique. The MV objective maximizer can be found with the help of a search algorithm. The solutions of Eqs. (15)–(16), along with the maximizing condition, form the bounds of the strategy space within which the maximizer exists.

Conclusion

In this paper, we study a risk-averse supply chain with a mean–variance objective. The theoretical contributions of the study are twofold. First, in the context of a dyadic supply chain comprising of a single supplier and single retailer, we show that a single condition can define the optimality criterion of the ordering decision in both centralized and decentralized supply chains. Such optimality is independent of the model parameters and solely relies on the nature of the demand distribution. Second, we demonstrate that the proposed ordering decision is computationally more straightforward than the methods available in extant literature. The optimal ordering decision is therefore represented as a mathematical function of the final demand distribution that the retailer experiences. This result marks an improvement over existing techniques of computing optimal ordering quantity decisions, as presented by Choi et al. (2008a, b) and Katariya et al. (2013) in the context of a dyadic supply chain. Our proposed method has a significant computational simplicity over Lau (1980) and Wu et al. (2009). The managerial implications and research findings are summarized in Table 3 below. We also establish that the risk of an individual agent is a mathematical function of the model parameter(s).

In the context of a supply chain network comprising of a single supplier and multiple retailers, we demonstrate that a pure-strategy Nash equilibrium exists when all the retailers are risk-averse with varying risk attitudes. We also establish the boundary condition of the risk-aversion parameter within which this pure Nash solution would hold. This analysis can be extended in the context of a supply chain network and that we leave for future research.

Notes

Economic Times Retail Report (June 10, 2020), “Driving demand to drive economy”, Retrieved from: https://retail.economictimes.indiatimes.com/news/industry/driving-demand-to-drive-economy/76298362, Accessed on: June, 10, 2020.

Ibid.

Mason, B. (May 14, 2020), “Risk Aversion Sweeps across the Markets as COVID-19 Realities Sink In”, Retrieved from: https://www.fxempire.com/news/article/risk-aversion-sweeps-across-the-markets-as-covid-19-realities-sink-in-649266, Accessed on: June 01, 2020.

References

Alzahrani N, Bulusu N (2018).Towards true decentralization: a blockchain consensus protocol based on game theory and randomness. In: International conference on decision and game theory for security. Springer, Cham, pp 465–485.

Buzacott J, Yan H, Zhang H (2003) Risk analysis of commitment-option contracts with forecast updates. Working paper, York University.

Cachon GP (2003) Supply chain coordination with contracts. Handbook in operations research and management science, Volume on Supply Chain Management: Design, Coordination and Operation. North Holland, Amsterdam, pp 229–339.

Cachon GP, Lariviere MA (2005) Supply chain coordination with revenue-sharing contracts: strengths and limitations. Manag Sci 51(1):30–44

Catalini C, Gans JS (2016) Some simple economics of the blockchain (No. w22952). National Bureau of Economic Research.

Chen Y, Xu M, Zhang ZG (2009) Technical note-a risk-averse newsvendor model under the CVaR criterion. Oper Res 57(4):1040–1044

Chiu CH, Choi TM (2016) Supply chain risk analysis with mean-variance models: a technical review. Ann Oper Res 240:489–507

Choi TM, Chiu CH (2012) Mean-downside-risk and mean-variance newsvendor models: implications for sustainable fashion retailing. Int J Prod Econ 135(2):552–560

Choi TM, Li D, Yan H, Chiu CH (2008) Channel coordination in supply chains with agents having mean-variance objectives. Omega 36(4):565–576

Choi TM, Li D, Yan H (2008) Mean–variance analysis of a single supplier and retailer supply chain under a returns policy. European Journal of Operational Research 184(1):356–376

Eeckhoudt L, Gollier C, Schlesinger H (1995) The risk-averse (and prudent) newsboy. Manag Sci 41(5):786–794

Geanakoplos J (2003) Nash and Walras equilibrium via Brouwer. Econ Theory 21(2):585–603

Giri BC, Bardhan S (2012) Supply chain coordination for a deteriorating item with stock and price-dependent demand under revenue sharing contract. Int Trans Oper Res 19(5):753–768

Gotoh J, Takano Y (2007) Newsvendor solutions via conditional value-at-risk minimization. Eur J Oper Res 179(1):80–96

Horowitz I (1970) Decision Making and the theory of the firm. Holt, Rine-hart & Winston, New York.

Huang X, Choi SM, Ching WK, Siu TK, Huang M (2011) On supply chain coordination for false failure returns: a quantity discount contract approach. Int J Prod Econ 133(2):634–644

Katariya AP, Cetinkaya S, Tekin E (2013) On the comparison of risk-neutral and risk-averse newsvendor problems. J Oper Res Soc 65(7):1090–1107

Keren B, Pliskin JS (2006) A benchmark solution for the risk-averse newsvendor problem. Eur J Oper Res 174(3):1643–1650

Lau HS (1980) The newsboy problem under alternative optimization objectives. J Oper Res Soc 31(6):525–535

Li B, Chen P, Li Q, Wang W (2014) Dual-channel supply chain pricing decisions with a risk-averse retailer. Int J Prod Res 52(23):7132–7147

Liu M, Cao E, Salifou CK (2016) Pricing strategies of a dual-channel supply chain with risk aversion. Transportation Res E Logistics Transportation Rev 90:108–120

Markowitz HM (1959) Portfolio selection: efficient diversification of investment. Wiley, New York

Pasternack BA (2005) Using revenue sharing to achieve channel coordination for a newsboy type inventory model. Models, Applications, and Research Directions. Springer, US, Supply Chain Management, pp 117–136

Pasternack BA (2008) Optimal pricing and return policies for perishable commodities. Market Sci 27(1):133–140

Peck H (2005) Drivers of supply chain vulnerability: an integrated framework. Int J Phys Distribut Logistics Manag 35(4):210–232

Soleimani H, Seyyed-Esfahani M, Kannan G (2014) Incorporating risk measures in closed-loop supply chain network design. Int J Prod Res 52(6):1843–1867

Souza GC (2014) Supply chain analytics. Business Horizons 57(5):595–605

Tsay AA, Agrawal N (2004) Channel conflict and coordination in the E-commerce age. Prod Oper Manag 13(1):93–110

Tomlin B (2006) On the value of mitigation and contingency strategies for managing supply chain disruption risks. Manag Sci 52(5):639–657

Van Mieghem JA (2003) Capacity management, investment, and hedging: Review and recent developments. Manufact Service Oper Manag 5:269–301

Wu J, Li J, Wang S, Cheng TCE (2009) Mean–variance analysis of the newsvendor model with stockout cost. Omega 37(3):724–730

Wei Y, Choi TM (2010) Mean–variance analysis of supply chains under wholesale pricing and profit sharing schemes. Eur J Oper Res 204(2):255–262

Yao DQ, Liu JJ (2005) Competitive pricing of mixed retail and E-tail distribution channels. Omega 33(3):235–247

Zhao X (2008) Coordinating a supply chain system with retailers under both price and inventory competition. Prod Oper Manag 17(5):532–542

Zhao X, Atkins DR (2008) Newsvendors under simultaneous price and inventory competition. Manufact Service Oper Manag 10(3):539–546

Zhuo W, Shao L, Yang H (2018) Mean–variance analysis of option contracts in a two-echelon supply chain. Euro J Oper Res 271(2):535–547

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: Channel coordination of a risk averse supply chain

Appendix: Channel coordination of a risk averse supply chain

Proofs and Calculations

Proof of Theorem 1

The central planner’s optimization problem is presented by (5). The first- and second-order derivatives of the objective function are given below

Equating (17) to zero, we calculate an order quantity decision \(q^{*}\). This order quantity satisfies FOC, but that does not signify maximization of the objective function. From (18), we can say that \(q^{*}\) would maximize the objective function if and only if the following condition is satisfied

To simplify (19), we change the order of integration for the right-hand-side expression and define \(Y\) as a random variable that corresponds to the truncated distribution of demand \(x\) over \(\left[ {0,\,\,q^{*} } \right]\). Thus, we obtain:

By writing \(\xi = Y/q*\), we can observe that, \(\xi \in [0,1]\) and (20) takes the following form: \(E(q* - Y) = q*E(1 - \xi ) = q*\{ 1 - E(\xi )\}\). Using this simplified form in (19) we get:

\(r\left( \cdot \right) = {{f\left( \cdot \right)} \mathord{\left/ {\vphantom {{f\left( \cdot \right)} {\left\{ {1 - F\left( \cdot \right)} \right\}}}} \right. \kern-\nulldelimiterspace} {\left\{ {1 - F\left( \cdot \right)} \right\}}}\) is the failure rate of the demand distribution. Theorem 1 follows from (17) and (21).□

Calculations related to Table 2

-

(A)

Wholesale price contract: In this case, the random profit of the supplier and the retailer are presented by the following two equation

$${\pi _{S,WP}}(q) = (w - s)q\quad \forall x$$(22)$${\pi _{R,WP}}\left( q \right) = \left\{ {\begin{array}{l}{\left\{ {p - \left( {w + c} \right)q} \right\}\quad \quad \quad \quad \quad \quad \quad\; \forall x \geqslant q} \\ {\left\{ {p - \left( {w + c} \right)q} \right\} - \left( {p - v} \right)\left( {q - x} \right)\quad \forall x < q} \\ \end{array} } \right.$$(23)The expected profit and variance are calculated from (22) and (23).

-

(B)

Buyback contract: The expected transfer payment is given by:

$${T_{BB}}\left( {w,b,q} \right) = {w_b}q - bI\left( q \right) = {w_b}q - b\int\limits_0^q {F\left( x \right)dx}$$The random profit of the supplier and the retailer are presented by the following two equations

$$\pi _{{S,BB}} \left( q \right) = \left\{ {\begin{array}{ll} {\left( {w_{b} - s} \right)q\quad \quad \quad \quad \,\,\;\,\;\forall x \ge q} \\ {\left( {w_{b} - s} \right)q - b\left( {q - x} \right)\quad \forall x < q} \\ \end{array} } \right.$$(24)$$\pi _{{R,BB}} \left( q \right) = \left\{ {\begin{array}{*{20}c} {\left\{ {p - \left( {w_{b} + c} \right)q} \right\}\quad \quad \quad \quad \quad \quad \quad \;\forall x \ge q} \\ {\left\{ {p - \left( {w_{b} + c} \right)q} \right\} - \left( {p - b} \right)\left( {q - x} \right)\quad \forall x < q} \\ \end{array} } \right.$$(25)From (24) and (25), the expected profit and variance of profit are calculated as follows:

$$E\{\pi_{S,BB}(q)\}=(w_{b}-s)q-b \int\limits_{0}^{q} F(x)dx$$$${\text{Var}}\left[ {{\pi _{S,BB}}\left( q \right)} \right] = - {b^2}\left\{ {{{\left[ {\int\limits_0^q {F(x)dx} } \right]}^2} - 2\int\limits_0^q {\left( {q - x} \right)F\left( x \right)dx} } \right\}$$$$E\left\{ {{\pi _{R,BB}}\left( q \right)} \right\} = \left\{ {p - \left( {{w_b} + c} \right)} \right\}q - \left( {p - b} \right)\int\limits_0^q {F\left( x \right)dx}$$$${\text{Var}}\left[ {{\pi _{R,BB}}\left( q \right)} \right] = - {\left( {p - b} \right)^2}\left\{ {{{\left[ {\int\limits_0^q {F(x)dx} } \right]}^2} - 2\int\limits_0^q {\left( {q - x} \right)F\left( x \right)dx} } \right\}$$ -

(C)

Revenue-sharing contract: In this case the expected transfer payment is:

$${T_{RS}}\left( {w,\phi ,q} \right) = {w_r}q + \left( {1 - \phi } \right)\left\{ {pS\left( q \right) + vI\left( q \right)} \right\} = \left\{ {{w_r} + \left( {1 - \phi } \right)p} \right\}q - \left( {1 - \phi } \right)\left( {p - v} \right)\int\limits_0^q {F\left( x \right)dx}$$The random profit of the supplier and the retailer are given by the following two equations

$${\pi _{S,RS}}\left( q \right) = \left\{ \begin{array}{ll} \left( {{w_r} - s} \right)q+(1-\phi)pq& \forall x \geqslant q \\ \left( {{w_r} - s} \right)q +\left( {1 -\phi}\right)pq -(1-\phi)(p-v)(q-x)& \forall x < q \\ \end{array} \right.$$(26)$${\pi _{R,RS}}\left( q \right) = \left\{ \begin{array}{ll} \left\{\phi p - \left( {{w_r} + c} \right) \right\}q&\forall x \geqslant q \\ \left\{\phi p - \left( {{w_r} + c} \right) \right\}q - \phi\left( {p - v} \right)\left( {q - x} \right)& \forall x < q \\ \end{array} \right.$$(27)

From (24) and (25), the expected profit and variance of profit are calculated as follows:

Proof of Proposition 1

In the case of buyback contract if the per unit price and buyback price are given by:\({w_b} = \left( {1 - \lambda } \right)\left( {p - c} \right) + \lambda s\) and \(b = \left( {1 - \lambda } \right)p + \lambda v\), then the retailer’s expected profit and variance of profit takes the form:

Using (28) and (29), the retailer’s mean–variance objective can be written as:

The retailer’s objective function is equivalent to that of a central planner’s problem where the central planner’s risk attitude is given by: \({\alpha _C} = \lambda {\alpha _R}\). Since, 0< λ <1, we have: αc < αR and it implies: \(q_{BB}^*\left( {{\alpha _C} = \lambda {\alpha _R}} \right) > q_{BB}^*\left( {{\alpha _R}} \right)\), as from Theorem 1 we know, the order quantity decision is decreasing in α.□

Proof of Proposition 2

In the case of revenue-sharing contract if the per unit price is given by: \({w_r} = \phi \,s - \left( {1 - \phi } \right)\,c\), then the retailer’s expected profit and variance of profit takes the following form:

Using (31) and (32), the retailer’s mean–variance objective can be written as:

The retailer’s objective function is equivalent to that of a central planner’s problem where the central planner’s risk attitude is given by: \({\alpha _C} = \phi {\alpha _R}\). Since, 0 < λ < 1, we have: αc < αR and it implies: \(q_{RS}^*\left( {{\alpha _C} = \phi {\alpha _R}} \right) > q_{RS}^*\left( {{\alpha _R}} \right)\), as from Theorem 1 we know, the order quantity decision is decreasing in αÖ.□

Proof of Theorem 2

The MV objective of retailer i is: \(\mathop {\max }\limits_{{p_i},{y_i}} M{V_i}\left( {{p_i},{y_i}} \right) = \left\{ {E\left[ {{\pi _i}\left( {{p_i},{y_i}} \right)} \right] - {\alpha _i}Var\left[ {{\pi _i}\left( {{p_i},{y_i}} \right)} \right]} \right\}\). \(E\left[ {{\pi _i}\left( {{p_i},{y_i}} \right)} \right]\) is jointly quasi-concave in (pi, Yi) when conditions (A) and (B) hold (for detailed proof refer to Zhao and Atkins 2008; Zhao 2008). Therefore if \(\left\{ { - {\text{Var}}\left[ {{\pi _i}\left( {{p_i},{y_i}} \right)} \right]} \right\}\) is concave in (pi, Yi), then from the properties of concavity we can conclude that MVi(pi, Yi) is concave in (pi, Yi). From (3) we can write the Hessian Matrix of \(\left\{ { - {\text{Var}}\left[ {{\pi _i}\left( {{p_i},{y_i}} \right)} \right]} \right\}\), which is a bivariate function of (pi, Yi), as follows:

\(\left\{ { - {\text{Var}}\left[ {{\pi _i}\left( {{p_i},{y_i}} \right)} \right]} \right\}\) is concave if and only if the matrix H(pi, Yi) is negative semi-definite, in other words all the principal minors of H(pi, Yi) are positive. Negative semi-definite property of the matrix ensures under the condition:

We define ψi as a random variable that corresponds to the truncated distribution of demand xi over [0, yi]. Using the properties of the order of integration and truncated distribution (A18) can be written as follows:

where \({\xi _i} = {{{\Psi _i}} \mathord{\left/ {\vphantom {{{\Psi _i}} {{y_i}}}} \right. \kern-\nulldelimiterspace} {{y_i}}}\) and \({\xi _i} \in \left[ {0,1} \right]\). If retailer i’s safety stock decision follows (35), the N retailers’ game becomes a concave one and therefore pure-strategy Nash equilibrium exists for such a game, and the best response of an individual player is given by her first-order condition.

Proof of Proposition 3

From the expression of \(\pi _i^d\left( {\vec p} \right)\), we obtain: \(\frac{{\partial \pi _i^d\left( {\vec p} \right)}}{{\partial {p_i}}} = {L_i}\left( {\vec p} \right) + \left\{ {{p_i} - \left( {{w_i} + {c_i}} \right)} \right\}\frac{{\partial {L_i}\left( {\vec p} \right)}}{{\partial {p_i}}}\). By assumption (A), \(\frac{{{\partial ^2}\pi _i^d\left( {\vec p} \right)}}{{\partial p_i^2}} < 0\), i.e., the deterministic profit part is concave and decreasing in pi. \(p_i^{\max }\) is sufficiently large and arbitrarily chosen such that: \({\left. {\frac{{\partial \pi _i^d\left( {\vec p} \right)}}{{\partial {p_i}}}} \right|_{{p_i} = p_i^{\max }}} < 0\). We also have: \({\left. {\frac{{\partial \pi _i^d\left( {\vec p} \right)}}{{\partial {p_i}}}} \right|_{{p_i} = \left( {{w_i} + {c_i}} \right)}} = {\left. {{L_i}\left( {\vec p} \right)} \right|_{{p_i} = \left( {{w_i} + {c_i}} \right)}} > 0\). The range of pi and yi are given by: \({p_i} \in \left[ {\left( {{w_i} + {c_i}} \right),p_i^{\max }} \right]\) and \({y_i} \in \left[ {0,y_i^{\max }} \right]\). At the boundary points we have the following:

\(p_i^{\max }\) is chosen in such a way that: \(\left| {{{\left. {\frac{{\partial \pi _i^d\left( {\vec p} \right)}}{{\partial {p_i}}}} \right|}_{{p_i} = p_i^{\max }}}} \right| > \left| {E\left[ {\min \left( {{x_i},{y_i}} \right)} \right]} \right|\) and (19) holds.

In the safety stock strategy set, we have the following: \(\mathop {\lim }\nolimits_{{y_i} \to 0} \Pr \left( {{x_i} > {y_i}} \right) \to 1\) and \(\mathop {\lim }\nolimits_{{y_i} \to y_i^{\max }} \Pr \left( {{x_i} > y_i^{\max }} \right) \to 0\). Therefore at the boundary points, we can observe

If both (36) and (37) are positive then we can conclude that the maximizer of the MV objective function is an interior point in the defined strategy set. We can observe that for small αi values,

In other words, we can say that when the retailers are slightly risk-averse then the maximizer of the MV objective function is an interior solution to the defined strategy set.

Rights and permissions

About this article

Cite this article

Biswas, I., Adhikari, A. & Biswas, B. Channel coordination of a risk-averse supply chain: a mean–variance approach. Decision 47, 415–429 (2020). https://doi.org/10.1007/s40622-020-00267-1

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40622-020-00267-1