Abstract

Global mine production of copper has risen more than 80 times over the last 135 years. What were the main drivers? I examine this question based on copper market data from 1880 to 2020. I employ a structural time series model with sign restrictions to identify demand and supply shocks. I find that a deterministic trend drives most of the output growth. At the same time, unpredictable demand and supply shocks caused substantial fluctuations around the trend. A global commodity demand shock that is, for example, linked to a 3% unexpected expansion of the global economy due to rapid industrialization causes a 10% rise in the real copper price, incentivizing a 5% increase in global copper production. This provides empirical evidence for the feedback control cycle of mineral supply.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The long-run supply of non-renewable resources and its drivers has been a recurrent topic in economics and geology. Hotelling (1931) and extensions such as Dasgupta and Heal (1974), Nordhaus et al. (1992), and Weitzman (1999) suggest that the production from a non-renewable resource would decline at the rate of interest as its deposits get exhausted.

However, Wellmer and Hagelüken (2015), Wellmer et al. (2019), and Wellmer and Dahlheimer (2020), and others argue that supply is driven by the so called feedback control cycle of mineral supply. If there is a shortage in the market, prices will rise, and encourage investment and innovation in mining, recycling, and processing of minerals. Schwerhoff et al. (2019) provide a formal general equilibrium growth model, where a rise in resource demand incentivizes firms to invest into new extraction technology and to expand production.

This paper is to my knowledge the first to examine empirically the long-run drivers of non-renewable resource production. Stuermer and Von Hagen (2012) and Stuermer (2017) find that periods of industrialization are a major driver of the demand for copper and other minerals, while a broad literature has established that such global commodity demand shocks are a major driver of various commodity prices (see, e.g., Kilian 2009; Stuermer 2018; Jacks and Stuermer 2020; Baumeister and Hamilton 2021 and others). This paper goes one step further and shows how global commodity demand shocks drive global copper production.

I use a standard structural Bayesian VAR model for commodity markets to decompose global copper production into a predictable trend component and unpredictable fluctuations driven by three different types of shocks (e.g., Kilian 2009; Baumeister and Peersman 2013; Jacks and Stuermer 2020; Boer et al. 2021 and many others). We use global copper market data from 1880 to 2020. In line with the literature, I define shocks as changes in the variables that are unpredictable based on the model. I include three endogenous variables, namely the percentage change in global real GDP, the percentage change in global copper mine production, and the real price of copper.

Sign restrictions based on standard economic theory allow me to distinguish three different shocks that I interpret as follows: first, a global commodity demand shock driven by the global business cycle. This type of shock captures an unexpected shift in the demand curve for all commodities, e.g., an unexpected strong increase in the consumption of all commodities due to rapid industrialization in Asia. As markets adjust, this type of shock leads to a global supply response and hence drives copper production up. Second, I define a copper supply shock as an unexpected shift in the supply curve. Examples include strikes, natural disasters that affect mines, or the earlier than expected opening of a major mine. Finally, I assume a copper-specific demand shock that shifts the demand curve due to unexpected changes in consumption that are specific to the copper market.

I find that most of the rise in copper production is driven by a deterministic constant and a linear trend in the annual average growth rate of copper production. The linear trend declines, implying that the growth rate of output decreases from roughly 9% at the beginning to about 2% at the end of our sample. This result shows that mining firms base their investment decisions on predictable long-term trends unaffected by price shocks.

At the same time, there are substantial medium- and long-term fluctuations in global output around the constant and the long-term trend. These fluctuations are driven by demand and supply shocks in roughly similar proportions. Global commodity demand shocks that are, for example, linked to fast industrialization and an expansion of the world economy drive up prices and lead to an increase in mine production. An unexpected expansion of the global economy by 3% causes a 10% rise in real copper prices, incentivizing a 5% increase in global copper production. This paper hence provides empirical evidence for the feedback control cycle of mineral supply.

The methodology also allows to zoom-in on different sub-periods. For example, a series of subsequent negative demand shocks drove down copper production during the 1980s and early 1990s. A mix of positive demand and supply shocks led to increasing production since the late 1990s. Since 2013, copper-specific demand shocks and positive supply shocks led to strong production increases. These were interrupted by strong negative demand shocks due to the Great Recession and the COVID-19 pandemic.

Our analysis is subject to three major limitations. First, I find a relatively short-cycled but persistent supply response peaking in the second year after the shock. Data limitation does not allow the model to disentangle the different factors that may drive this, including expansions of existing mines, higher capacity utilization of existing mines, and the building of new mines. These factors could also play varying roles at different time horizons, offsetting each other at the aggregate.

Furthermore, the model is a global model over a long sample period. Controlling for the world war periods, the long sample period is a sensible assumption as copper has mostly been traded in relatively integrated global markets, where the law of one price holds approximately. Historical data issues may still bias results. Finally, I assume no structural break or shift over the long-time horizon. It follows that estimated coefficients are presumed to be constant. Major changes are interpreted as shocks in our framework.

The remainder of the paper is structured as follows. The “Data” section provides a description of the data. The “Econometric model” section lays out the econometric model including the identification strategy, and the “Empirical results” section presents the results. Finally, the “Conclusion” section concludes.

Data

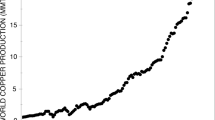

I use historical annual data for global real GDP, global copper production, and the real copper price, as depicted in Fig. 1. I build on Pescatori et al. (2021), Stuermer (2018), Jacks and Stuermer (2020), and Schwerhoff et al. (2019) in assembling the data-set.

Historical copper market data from 1880 to 2020 used in the regression model. GDP: global real GDP (percentage change); PROD: global copper output (percentage change); PRICE: real price of copper (log)

I construct a series for global real GDP by using data for 1880 to 2007 from Schwerhoff et al. (2019) who build on Maddison (2010). I expand the data to 2020 based on growth rates of global real GDP from the International Monetary Fund’s World Economic Outlook database. The data follows the global business cycle in line with narrative evidence from economic history.

I employ global copper production data from Schwerhoff et al. (2019) for the period 1880 to 2020. These data include mine production only. The series shows higher volatility during the world war periods and their direct aftermath when converting it to percentage change. I control for the two world war periods and the respective 3 consecutive years by using annual time dummies.

Annual price data is sourced from Boer et al. (2021) for the sample period of 1880 to 2020. I employ the US all urban consumers price index to adjust prices for inflation. I take logs of the price series to make it more symmetric.

Econometric model

I set up a VAR model with three endogenous variables \(\mathbf {y}_{t}=(\boldsymbol {\Delta GDP}_{t}, \boldsymbol {\Delta Q}_{t}, \mathbf {P}_{t})^{\prime }\), namely the percent change of global real GDP, the percentage change of global copper production ΔQt, and the log of the real price of copper Pt.Footnote 1 I estimate

with a lag length of p = 4, where Ai are the reduced-form VAR coefficients and ut the reduced-form forecast errors. These errors have no economic interpretation. The matrix of deterministic terms Dt consists of a constant, a linear trend, annual dummies during the two world war periods, and the 3 respective following years.

The reduced-form VAR in Eq. 1 can be expressed in a structural form given by

where εt are independent structural shocks with an economic interpretation. These are related to the reduced-form errors via the linear transformation \(\mathbf {u}_{t} = \mathbf {B}_{0}^{-1} \boldsymbol {\varepsilon }_{t}\). Thus, \(\mathbf {B}_{0}^{-1}\) contains the impact effects of the structural shocks on the three endogenous variables in yt. By assuming a unit variance for the uncorrelated structural shocks, i.e., \(\mathbb {E}(\boldsymbol {\varepsilon }_{t} \boldsymbol {\varepsilon }_{t}^{\prime } )= \mathbf {I}_{n}\) (an identity matrix), the reduced-form covariance matrix Σu is related to the structural impact multiplier matrix as \(\boldsymbol {\Sigma }_{u} = \mathbb {E}(\mathbf {u}_{t} \mathbf {u}_{t}^{\prime }) = \mathbf {B}_{0}^{-1} \mathbb {E}(\boldsymbol {\varepsilon }_{t} \boldsymbol {\varepsilon }_{t}^{\prime }) { \mathbf {B}_{0}^{-1}}^{\prime }= \mathbf {B}_{0}^{-1} { \mathbf {B}_{0}^{-1}}^{\prime }\).

Identification

Without further information, it is not possible to identify \(\mathbf {B}_{0}^{-1}\) and thereby the structural form in Eq. 2. The literature has come up with different restrictions placed directly on \(\mathbf {B}_{0}^{-1}\) to solve this identification problem. I apply conventional sign restrictions (e.g., Faust 1998; Canova and Nicolo 2002, and Uhlig 2005) on the elements in \(\mathbf {B}_{0}^{-1}\), i.e., I assume that the structural shocks have either a positive or negative effect on the endogenous variables on impact. I base these impact restrictions on economic intuition as specified in Table 1 following Pescatori et al. (2021) and others.

I interpret the first shock as a global commodity demand shock that is related to the global business cycle, shifting the demand curve for all commodities simultaneously. The assumed sign restrictions imply that a positive shock increases global economic activity, global copper production, and its real price on impact during the first year. As we assume that the effects of the shocks are symmetric, the reverse effects hold as well, meaning that a negative global commodity demand shock decreases global economic activity, global copper production, and the real copper price.

I label the second shock as a copper supply shock, capturing unexpected shifts in the supply curve, for example, production outages, or a stronger than expected increase in production. A positive shock that increases global copper production is assumed to have a positive impact on global economic activityFootnote 2 and to decrease the real copper price on impact (or vice versa).

I interpret the third shock as a copper-specific demand shock. This shock represents a shift in the demand curve due to factors that affect the demand for only copper. Note that this shock may also capture precautionary demand shocks, namely shifts in the demand for inventory due to forward-looking behavior. I assume that a positive shock increases the production and price on impact (or vice versa). I also presume that a positive shock decreases global economic output on impact as a result of the higher copper price and hence higher costs of copper as an input (see also Kilian 2009; Baumeister and Peersman 2013) (or vice versa). I recognize that this effect is likely close to zero, as copper inputs into manufacturing are relatively small compared to global aggregate output.

Historical decomposition

Based on the structural model, a historical decomposition allows me to decompose the global copper production variable into the contributions of the deterministic trend and the world war dummies as well as the three identified shocks. To explain it differently, we basically compute what the counter-factual global copper production would have looked like when removing the effects of the deterministic components or each of the shocks.

The historical decomposition is used in the literature on commodities markets in different contexts. Examples include among others Kilian (2009), Kilian and Murphy (2014), Stuermer (2018), Baumeister and Hamilton (2019), and Rausser and Stuermer (2020), and Jacks and Stuermer (2021).

Employing the historical decomposition can decompose each of the three endogenous variables according to:

where the matrix \(B_{0}^{-1}\) is the estimated structural multiplier matrix of the endogenous variables, \({\Pi}^{\star}\) is the structural form matrix for the deterministic terms, the upper tilde denotes variables that are derived from the historical, and ϕi are the estimated reduced-form impulse responses that capture the responses of the endogenous variables to one unit shocks i periods ago. They are computed from \(\phi _{i}=J\boldsymbol {A}^{i} J^{\prime }\) and \(\left [A_{1}^{(t)},\cdots ,A_{p}^{(t)}\right ]=J A^{t}\), with (K × Kp) matrix \(J = \left [I_{K}, 0_{(K\times K)}, \cdots , 0_{(K\times K)}\right ]\). The companion matrix A is defined as a (pK × pK) matrix:

The first term on the right-hand side of Eq. 3 contains the sum of the cumulative contributions of the three structural shocks to each of the endogenous variables. The second term contains the contributions of the deterministic terms to the endogenous variables. The last term on the right hand includes the cumulative effect of the initial states on the endogenous variables, which become negligible for stationary processes as \(t \rightarrow \infty\).Footnote 3

Estimation and inference

Estimation and inference are based on standard Bayesian techniques laid out in Waggoner and Zha (1999), Rubio-Ramirez et al. (2010), and Antolín-Díaz et al. (2021). To draw candidate models, I use the algorithm from Antolín-Díaz et al. (2021) that builds on Waggoner and Zha (1999).Footnote 4 The algorithm uses a Gibbs sampler procedure that iterates between draws from the conditional distributions of the structural parameters.

Hence, I pick a random draw of structural parameters out of 25,000 potential draws that rely both on actual data. I use a Minnesota-type prior with standard shrinkage parameters (see Giannone et al. 2015) in combination with a sum-of-coefficients prior (Doan et al. 1984) and a dummy-initial-observation prior (Sims 1993) to estimate Eq. 1.

Identification via sign restrictions does not yield point estimates but instead sets of possible parameter intervals for the different elements in \(\mathbf {B}_{0}^{-1}\). For each model, a set of 1000 admissible draws is obtained, where each draw consists of a conditional forecast, future shocks, and an associated \(\mathbf {B}_{0}^{-1}\) matrix that satisfies the identifying restrictions. These draws are also used for inference, i.e., they yield an indication of the uncertainty around the pointwise median estimates. Following Antolín-Díaz and Rubio-Ramírez (2018) and Antolín-Díaz et al. (2021), we report pointwise median and percentiles of impulse responses for set-identified structural VAR models, as it is common in the literature.

The literature has made substantial recent progress on inference in Bayesian models, which is important to take into account when interpreting our results. First, Baumeister and Hamilton (2015) and Baumeister and Hamilton (2020) and Watson (2019) remark that readers are used to associating error bands with sampling uncertainty, but in large-sample sign-restricted SVARs these error bands only result from the prior for the rotation matrix Q, not sampling uncertainty. Inoue and Kilian (2020) point out that the share of uncertainty resulting from the prior on Q tends to be rather small in most applications, in particular, when assuming several sign restrictions. For our model with three variables, the Haar prior placed on the rotation matrix Q is uninformative about the structural impulse responses (a special case as Baumeister and Hamilton 2015 show).

Empirical results

How do shocks affect global copper output?

In a first step, the econometric model allows us to show how each shock affects the three different endogenous variables in the impulse response functions (see Fig. 2).

Impulse responses of three endogenous variables to the three identified shocks. The responses are based on 1000 draws showing the pointwise median (blue solid line) with 68% pointwise credible sets (blue shaded areas). The shocks refer to one standard deviation shock. GDP: global real GDP; PROD: global copper output; PRICE: real price of copper. AD: global commodity shock; MS: copper supply shock; MD: copper-specific demand shock

The upper left panel illustrates that a one standard deviation global commodity demand shock (AD) is associated with a roughly 3% increase in global real GDP. The lower left panel shows that this 3% positive shock to global real GDP causes a roughly 10% increase in the copper price. Considering the middle left panel, this implies that supply responds with a persistent 5% increase in global copper production.

The panel in the middle depicts how a one standard deviation copper supply shock (MS) is associated with a roughly 7% persistent increase in global copper output. Such an increase leads to a roughly 3% decline in the copper price that dissipates over time. The effects of this shock on global real GDP are close to zero.

A one standard deviation copper-specific demand shock (MD) is associated with a 13% increase in price (see lower right panel). It does not exert a clear effect on copper output. It is positive during the first year and then turns negative, but is overall indistinguishable from zero. The effect on real global GDP is slightly negative. The effects seem not be estimated with a high precision.

Overall, the impulse response functions show that global commodity demand shocks have a substantial impact on global copper mining output.

To what extent is global copper output predictable?

In a second step, I use a historical decomposition to disentangle the deterministic trend component from the unpredictable fluctuations that are driven by the three different types of shocks. To do so, I transform the global copper output variable from percent changes back to levels.

Figure 3 shows how the deterministic trend and the world war dummies contribute to the evolution of global copper production in levels. They explain a large portion of it. The world war periods led to substantial increases in production, followed by a period with lower production. Note that the linear trend turns into a non-linear trend when converting the percentage changes to levels. There is actually a predictable decline in the annual average growth rate of copper production from 9% at the beginning to about 2% at the end of the sample.

Global copper output explained by the constant, trend, and world war dummies

Figure 4 shows the joint contribution of the three different shocks to the fluctuations of global copper production around the deterministic trend using the historical decomposition again. The trend component is shut-off. One can see that the three shocks drove global copper production above its long-run trend during the 1930s, which then got suddenly reversed in a steep drop during the 1929–1930 Great Depression. There is another brief upward movement right before the outbreak of World War II.

Fluctuations in the level of global copper output. Note: The fluctuations in copper output become larger over time because they move around an increasing deterministic trend as shown in Fig. 3

After World War II, output fluctuated mostly below its long-run trend. However, there were strong upward movements in the 1960s and in the early 1970s. Afterwards the joint three shocks drove global copper output sharply down in the 1980s and 1990s.

Starting in the mid-1990s, the shocks drove global copper output sharply up. There is another sharp decline during the Great Recession in 2008–2009, which is followed by steep increases in global copper output. Finally, during the 2020 pandemic, output declined steeply.

Overall, the predictable, deterministic terms drove most of the level of global copper output. However, unexpected shocks to copper markets caused large fluctuations around the trend.

What drives fluctuations in global copper output?

As a final step, I disentangle the contribution of each of the three types of shock to explain the fluctuations in global copper output.

Figure 5 shows the contribution of each type of shock to the level of global copper output. For example, the blue line illustrates how the global copper mine output would have evolved if there had been only global commodity demand shocks. Subsequent positive demand shocks first drove up global output in the 1920s. Afterwards negative global commodity demand shocks during the Great Depression drove copper output sharply down. During the 1960s and 1970s, subsequent demand shocks put upward pressure on copper production mostly in line with the global business cycles.

Accumulated contribution of the three shocks to the fluctuations in global copper output. Note: The fluctuations in copper output become larger over time because they move around an increasing deterministic trend as shown in Fig. 3

In the late 1990s and 2000s, a series of massive subsequent positive demand shocks — most likely due to the economic boom in parts of Asia — led to strong positive supply responses. During the Great Recession, negative commodity demand shocks caused a strong decline in copper output. After some upward pressure in the mid-2010s, the pandemic triggered another strong negative demand shock that led to a negative response of global copper output.

Copper supply shocks mostly exerted negative pressures on global copper output. This is particularly the case during the 1980s and 1990s when the Soviet Union broke up. They are about just as important in driving output fluctuations like global commodity demand shocks.

Copper-specific demand shocks led to a positive impact on output in the interwar period. The impact also spikes in 2009 and 2020. This could be driven by the service sector shrinking more during periods of recessions than mining output and copper consumption, driving up the copper intensity of the global economy. However, as the impulse response functions are not clear-cut for this type of shock, the results for copper-specific demand shocks should be taken with a grain of salt.

Conclusion

This paper is the first to empirically examine the long-run drivers of non-renewable resource output. It does so at the example of the copper market, based on annual data on global mine production, real copper price, and global real GDP from 1880 to 2020. I employ a structural time series model to identify demand and supply shocks based on standard sign restrictions.

I show that there is no empirical evidence for the hypothesis that copper mine production is declining at the rate of interest due to a limited stock of resources in line with Hotelling (1931). At the same time, I find evidence that the feedback control cycle of mineral supply (see Wellmer and Dahlheimer (2020), Wellmer and Hagelüken (2015), and Wellmer et al. (2019), and others) is an important contributor to long-run fluctuations in global copper output. Global commodity demand shocks drive up prices incentivize the expansion of global copper mine production, or vice versa.

I also find that most of the rise in production is driven by a predictable constant and trend in the growth rate of copper production, which declines from 9% of annual growth in production at the beginning to about 2% at the end of the sample.

Global commodity demand shocks were an equally important contributor to fluctuations around this trend like copper supply shocks. A series of subsequent negative demand shocks drove down copper production during the 1980s and early 1990s, and positive demand and supply shocks have led to increasing production since the late 1990s. Since 2013, a combination of demand shocks and supply shocks has driven up production with strong declines due to the Great Recession and the COVID-19 pandemic.

The results open a puzzle for future research. I find that the impact of the global commodity demand shocks on global copper mine production is at its peak 2 years after the demand shock. However, the control cycle duration typically assumes lead times between deposit discovery and start of operations of about 5 to 10 years. It is therefore not clear how the observed relations between price and production relate to the feedback control cycle. Future research with more granular data could disentangle the different factors that may drive this, including expansions of existing mines, higher capacity utilization of existing mines, and the building of new mines. These factors could also play varying roles at different time horizons, offsetting each other at the aggregate level and leading to the empirical results presented here.

Finally, it also remains to be seen if possible positive demand shocks due to the energy transition will trigger strong increases in global copper mining over the next two decades, more than offsetting the slowly moderating long-term trend.

Data availability

Data and materials are available from the author upon request.

Notes

Note that the methodological section leans heavily on Boer et al. (2021).

I recognize that this effect is likely very minor and could go close to zero due to the small share of the copper industry in global aggregate output.

For more methodological background on historical decompositions, see Kilian and Lütkepohl (2017, p. 116–120).

The algorithm by Antolín-Díaz et al. (2021) was written to derive structural scenarios. Here it is used only for identification of the shocks and to derive the structural vector auto-regressive model output.

References

Antolín-Díaz J, Petrella I, Rubio-Ramírez JF (2021) Structural scenario analysis with SVARs. J Monet Econ 117(C):798–815

Antolín-Díaz J, Rubio-Ramírez JF (2018) Narrative sign restrictions for SVARs. Am Econ Rev 108(10):2802–2829

Baumeister C, Hamilton JD (2015) Sign restrictions, structural vector autoregressions, and useful prior information. Econometrica 83(5):1963–1999

Baumeister C, Hamilton JD (2019) Structural interpretation of vector autoregressions with incomplete identification: revisiting the role of oil supply and demand shocks. Am Econ Rev 109(5):1873–1910. https://doi.org/10.1257/aer.20151569

Baumeister C, Hamilton JD (2020) Drawing conclusions from structural vector autoregressions identified on the basis of sign restrictions. J Int Money Financ 109:102405

Baumeister C, Hamilton JD (2021) Estimating structural parameters using vector autoregressions. Manuscript, University of California, San Diego

Baumeister C, Peersman G (2013) The role of time-varying price elasticities in accounting for volatility changes in the crude oil market. J Appl Econ 28(7):1087–1109

Boer L, Pescatori A, Stuermer M (2021) Energy transition metals. IMF Working Paper, No 2021–243

Canova F, Nicolo GD (2002) Monetary disturbances matter for business fluctuations in the G-7. J Monet Econ 49(6):1131–1159

Dasgupta P, Heal G (1974) The optimal depletion of exhaustible resources. Rev Econ Stud 41:3–28

Doan T, Litterman R, Sims C (1984) Forecasting and conditional projection using realistic prior distributions. Econ Rev 3(1):1–100

Faust J (1998) The robustness of identified VAR conclusions about money. Carnegie-Rochester Conference Series on Public Policy 49:207–244. https://doi.org/10.1016/S0167-2231(99)00009-3

Giannone D, Lenza M, Primiceri G (2015) Prior selection for vector autoregressions. Rev Econ Stat 97(2):436–451

Hotelling H (1931) The economics of exhaustible resources. J Polit Econ 39(2):137–175

Inoue A, Kilian L (2020) The role of the prior in estimating VAR models with sign restrictions. Dallas Fed Working Paper, No. 2030

Jacks DS, Stuermer M (2020) What drives commodity price booms and busts? Energy Econ 85:104035

Jacks DS, Stuermer M (2021) Dry bulk shipping and the evolution of maritime transport costs, 1850–2020. Aust Econ Hist Rev 61(2):204–227

Kilian L (2009) Not all oil price shocks are alike: disentangling demand and supply shocks in the crude oil market. Am Econ Rev 99(3):1053–1069

Kilian L, Lütkepohl H. (2017) Structural vector autoregressive analysis. Cambridge University Press, Cambridge, U.K. https://doi.org/10.1017/9781108164818

Kilian L, Murphy DP (2014) The role of inventories and speculative trading in the global market for crude oil. J Appl Econ 29(3):454–478

Maddison A (2010) Historical statistics of the world economy: 1-2008 AD. http://www.ggdc.net/maddison/. Accessed 13 June 2011

Nordhaus WD, Stavins RN, Weitzman ML (1992) Lethal model 2: the limits to growth revisited. Brook Papers on Econ Act 1992(2):1–59

Rausser G, Stuermer M (2020) A dynamic analysis of collusive action: the case of the world, 1882-2016. MPRA Working Paper, No. 104708

Rubio-Ramirez JF, Waggoner DF, Zha T (2010) Structural vector autoregressions: theory of identification and algorithms for inference. Rev Econ Stud 77(2):665–696

Schwerhoff G, Stuermer M et al (2019) Non-renewable resources, extraction technology and endogenous growth. Dallas Fed Working Paper, No. 1506 (Updated: 2019)

Sims CA (1993) A nine-variable probabilistic macroeconomic forecasting model. In: Stock JH, Watson MW (eds) Business cycles, indicators and forecasting. NBER Studies in Business Cycles. University of Chicago, pp 179–212

Stuermer M (2017) Industrialization and the demand for mineral commodities. J Int Money Financ 76:16–27

Stuermer M. (2018) 150 years of boom and bust: what drives mineral commodity prices? Macroecon Dyn 22(3):702–717

Stuermer M, Von Hagen J (2012) Der Einfluss des Wirtschaftswachstums aufstrebender Industrienationen auf die Märkte mineralischer Rohstoffe. Deutsche Rohstoffagentur (DERA) in der Bundesanstalt für Geowissenschaften und Rohstoffe, Hanover, Germany

Uhlig H (2005) What are the effects of monetary policy on output? Results from an agnostic identification procedure. J Monet Econ 52(2):381–419

Waggoner D, Zha T (1999) Conditional forecasts in dynamic multivariate models. Rev Econ Stat 81(4):639–651

Watson M (2019) Comment on “The empirical (ir) relevance of the zero lower bound constraint”. NBER Macroeconomic Annual, 34

Weitzman ML (1999) Pricing the limits to growth from minerals depletion. Q J Econ 114 (2):691–706

Wellmer F, Dahlheimer M (2020) The feedback control cycle as regulator of past and future mineral supply. Miner Deposita 47(7):713–729

Wellmer F-W, Buchholz P, Gutzmer J, Hagelüken C, Herzig P, Littke R, Thauer RK (2019) Raw materials for future energy supply. Springer, New York

Wellmer F-W, Hagelüken C (2015) The feedback control cycle of mineral supply, increase of raw material efficiency, and sustainable development. Minerals 5(4):815–836

Acknowledgements

I thank Juan Antolin-Diaz, Juan Rubio-Ramirez and Ivan Petrella for sharing their code with me. I am grateful to Lukas Boer for suggestions as well as to two anonymous referees for their highly valuable comments. The views expressed in this paper do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

Author information

Authors and Affiliations

Contributions

I am the sole contributor to this paper.

Corresponding author

Ethics declarations

Ethics approval

I have reviewed the ethics guidelines and confirm that I comply with all of them.

Consent for publication

I approve the manuscript for submission. The content of the manuscript has not been published, or submitted for publication elsewhere.

Competing interests

The author declares no competing interests.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Stuermer, M. Non-renewable resource extraction over the long term: empirical evidence from global copper production. Miner Econ 35, 617–625 (2022). https://doi.org/10.1007/s13563-022-00352-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13563-022-00352-0