Abstract

Following geographically concentrated changes in housing markets, real estate prices have skyrocketed in many cities and metropolitan areas across Germany. These developments have not only shifted the macro-level distribution of asset wealth among homeowners but have also resulted in price spikes in rental markets, which in turn have intensified social and economic risks among renters. This preregistered study aims to provide a theoretical rationale for, and first-time insights into, the determinants of individual preferences for rent control. It argues that policy preferences are shaped by individuals’ economic and geographic positions in the housing market. It not only explores differences between homeowners and renters but also considers how heterogeneity in exposure to the burden of rental costs—structured by local rents and disposable income—explains differences within the group of renters. The results reveal the precedence of egotropic considerations over geotropic effects of common market exposures. Homeowners oppose rent control far more strongly than renters do, whose support for rent control is primarily a function of income. Market rents, in contrast, only heighten support for rent control among low-income renters. These findings deepen our understanding of the politicization of housing policy in Germany and advance important debates on political reactions to housing markets.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Real estate prices have skyrocketed in many cities and metropolitan areas across Germany (Baldenius et al. 2020). This has not only shifted the macro-level distribution of asset wealth to the benefit of homeowners but has also resulted in price spikes in rental markets, which in turn have intensified social and economic risks among renters. As a result, rent and housing policy has become a focal point of political contestation: The introduction of the (now defunct) Berlin rent freeze prompted large-scale demonstrations both in support of and opposition to the policy, and citizens’ initiatives have recently initiated a referendum calling for the expropriation of the housing stock of large private real estate firms.

Political science scholarship is only slowly starting to catch up with this sudden burst in the real-world importance of rent and housing policy in Germany and elsewhere. Existing work in comparative political economy has mostly focused on the effects of house price appreciation rates on individuals’ general preferences for taxation and redistribution (Ansell 2009, 2014) and voting behavior (André and Dewilde 2016; Larsen et al. 2019; Adler and Ansell 2019; Ansell et al. 2022). In doing so, existing research has, both theoretically and empirically, adopted a stringent focus on the role of homeowners. While this focus is plausible given the high ownership rates in most Western countries (e.g., Kohl 2017, 2018), the neglect of the situation of renters in today’s rapidly changing housing markets paints an incomplete picture of the political economy of housing. This is particularly true when studying the German-speaking countries in Central Europe, where ownership rates have been historically low. In 2018, a mere 46.5% of residences in Germany were owner-occupied. In urban areas such as Hamburg and Berlin, the ownership rates were even lower, at 24% and 17%, respectively.Footnote 1

In renter-majority countries, the dynamics of local housing markets affect large parts of the population in fundamentally different ways than as parts of the “ownership game”. Once individuals buy a home—a decision that often involves the biggest financial investment of their lives—they become asset owners. As a result, their asset wealth depends on local house prices. Thus, the geographic heterogeneity in house price appreciation rates determines relative winners and losers: Homeowners in static or stagnant housing markets do not experience increases in their asset wealth, whereas homeowners in booming localities benefit decisively (e.g., Ansell 2019). For renters, in contrast, exposure to local housing market dynamics comes with structurally different implications. Rather than a matter of the long-term payoffs of an investment in an asset, increasing rents imply an immediate threat of reductions in discretionary incomes. While this threat may not materialize immediately—as increases in current market rents may not directly translate into rent increases in existing contracts—it signals an increased risk of looming economic burdens and residential displacement (Abou-Chadi et al. 2021).

Existing work in comparative political economy has provided ample evidence on the relationship between house price appreciation rates and owners’ political behavior. Ansell (2009, 2014) shows that house appreciation rates, over and beyond income, predict more conservative preferences for funding social security and taxation among homeowners. The underlying rationale is that house price appreciation generates additional income streams through rents and serves as a self-supplied social insurance mechanism, thus undermining individual support for public redistribution and insurance. In a comparative study of 24 countries, André and Dewilde (2016) explore whether this effect is contingent on age, income, and national housing financialization schemes, though the evidence is inconclusive. In support of economic voting and context priming theories, Larsen et al. (2019) show that increases in house prices lead to support for both left-wing and right-wing incumbent governments, particularly in localities with high housing market activity rates. Adler and Ansell (2019) and Ansell et al. (2022), lastly, link higher local house prices to lower support for populism. Studies on renters’ political reaction to local rental markets, however, are only starting to enter the debate (Hankinson 2018; Marble and Nall 2021; Abou-Chadi et al. 2021).

Aside from the lack of focus on the distinct market position of renters in both theoretical and empirical approaches to the political economy of housing, existing work faces another limitation. In linking markets to general socioeconomic policy preferences or party support, it skips an equally important and obvious question: If housing markets trigger political reactions among voters, then what do voters want? More specifically, given the increasing evidence on the political relevance of individuals’ economic and geographic positions in the housing market, which policies do voters demand in response to the market situation they face? With the exception of two recent studies on housing policy and land use preferences in the United States (Hankinson 2018; Marble and Nall 2021), this question has so far remained understudied.

To overcome these limitations and to advance the debate in comparative political economy—all while providing specific insights on the demand side of one of the most highly politicized socioeconomic issues in the 2021 German Federal Election campaign—this preregistered studyFootnote 2 sets out to analyze individual preferences for rent control with a particular focus on renters. My argument emphasizes individuals’ economic and geographic positions in the housing market. First, renters should support the policy more strongly than owners. This is because renters can be immediate beneficiaries of rent caps, whereas for owners whose homes are in the regulated market, rent caps imply a (temporary) reduction in asset wealth. Moving beyond this simple renter–owner dichotomy, I then focus on the group of renters and emphasize two important sources of geoeconomic heterogeneity within this group: market rents at their place of residence and their disposable income. Focusing on the interplay of these two variables, I argue that renters are most likely to demand policies protecting them against increasing rents where rents are high. This effect, in turn, will most likely materialize among renters in low-income households, for whom the threat of rental cost overburden is particularly high.

To test the proposed argument, I make use of the German Longitudinal Election Study Pre-Election Cross-Section (GLES 2022), which features a novel item measuring respondents’ support for the highly politicized issue of a nationwide rent cap. My findings show a precedence of egotropic considerations over geotropic effects of common market exposures. Homeowners oppose rent control far more strongly than renters do, whose support for rent control is primarily a function of income. Market rents, in contrast, only heighten support for rent control among low-income renters. These findings not only deepen our understanding of the politicization of one of the most fiercely politicized socioeconomic issues in the 2021 German Federal Election campaign but also advance the broader debate in comparative political economy on the political effects of housing markets.

2 Theoretical Framework

2.1 Rent Control as a Focal Point of Political Conflict in the 2021 German Federal Election

Housing markets have undergone drastic changes. Since the late 1990s, national house prices have soared across the Western world, crashed in many countries in the wake of the 2007–2008 financial crisis, and rapidly increased again in recent years (Ansell 2019). These dynamics have had major repercussions on wealth inequality. In Germany, 60% of wealth increases due to real estate appreciation have been concentrated in the top decile of the wealth distribution, compared to only 3% in the bottom half. This has been accompanied by major shifts in the rental market: Rents have increased drastically in many cities and metropolitan areas, often fundamentally changing the composition of urban neighborhoods (Baldenius et al. 2020).

It is thus not surprising that rent and housing policy has become a focal point of political competition. Horst Seehofer (Christian Social Union [CSU]), Federal Minister of the Interior, Building and Community from 2018 to 2021, has repeatedly referred to housing as the “great social question of our time” (Seehofer 2018). The increasing politicization of rent and housing policy has engaged voters and parties alike. Legislative proposals like the (now defunct) 5‑year rent freeze have brought large numbers of citizens to the streets both in support of and opposition to the policy. On the other hand, the bottom-up citizens’ initiative Deutsche Wohnen & Co. enteignen has successfully initiated a public referendum on the expropriation of large private real estate, thus forcing parties to position themselves on the issue. Rent and housing policy is thus unquestionably a “hot issue” and was arguably one of the most fiercely contested socioeconomic issues during the 2021 Federal Election campaign.

Like many issue domains, rent and housing policy is a hotchpotch of different policies. In the context of the 2021 German Federal Election, for instance, parties campaigned on five major subdomains directly related to rent and housing policy. Two of these subdomains were targeted at increasing the housing stock: incentivization of private construction by developers and facilitation of the acquisitions of private homes. Specific policies within the former subdomain include, for instance, the simplification of bureaucratic procedures for the designation of new building land and tax amortizations for the construction of rental homes; policies in the latter subdomain include the expansion of financing schemes for aspiring homeowners and exemption from the land transfer tax of property for personal use. Three other subdomains focused on state intervention and market control: the curbing of realty sector speculation (e.g., increasing taxes on capital gains from real estate purchases), the promotion of public and nonprofit housing (e.g., purchasing privately owned building land and real estate for conversion into public property), and rent control and tenant protection (including the introduction of federal caps on rents and rent price increases). In addition, parties also campaigned on specific residual policy proposals, including measures to fight homelessness or the expropriation of large real estate firms.

Figure 1 shows the results of original codings of parties’ policy proposals based on their 2021 election manifestos. For these codings, specific policy proposals mentioned in parties’ election manifestos were assigned to each of the five subdomains (residual policies not shown). I then classified each mention as positive (i.e., in support of the general target of the subdomain), neutral, or negative. Figure 1 shows the net sum of positive and negative policy mentions for each of the five sub-domains. As none of the parties took ambiguous stances within any of the five subdomains (e.g., none of the parties concurrently support a policy in favor of incentivizing private construction and a different policy in opposition of this target), positive and negative mentions do not cancel out in aggregation, such that the counts shown in the figure give valid indications of both salience and positions.

Party positions on multidimensional rent and housing policies. Own codings based on parties’ 2021 federal election manifestos

Figure 1 reveals a few important insights. First, and perhaps unsurprisingly, there is a clear left–right divide in terms of salience. The right-wing parties (Alternative for Germany [AfD], Christian Democratic Union [CDU/CSU], and Free Democratic Party [FDP]) clearly emphasize measures that target market-based expansions of the housing stock. While they share with the Social Democratic Party [SPD] and Greens their appeals for facilitation of the acquisition of private homes for personal use, they are the only parties to talk about policies that incentivize private development. Left-wing parties (Greens, Left, and SPD), on the other hand, tend to emphasize policies that advocate different forms of state intervention. Secondly and relatedly, we see that parties’ positions are mostly a function of the issues they talk about. On most subdomains, parties hardly address policies they oppose. Instead, they focus on proposing policies in support of their overall targets—and mostly remain silent on the rest. There is one clear exception to this rule: policies targeting rent control and tenant protection. Here, we see a clear contrast between left-wing and right-wing parties: Left-wing parties endorse numerous policies in support of the target, whereas right-wing parties oppose them. This is particularly true for caps on rent prices (Mietendeckel) and rent price increases (Mietpreisbremse), which are explicitly opposed by nearly all right-wing parties (with CDU/CSU referring to only one of the two policies) but are supported by all left-wing parties.

2.2 A Theory of Individual Preferences for Rent Control

As detailed in the previous section, the issue domain of rent and housing policy has become one of the most fiercely politicized subdimensions of socioeconomic political conflict. Albeit a multidimensional policy domain, policies targeting rent control and tenant protection have a special standing within this broader policy domain: The political debate about these policies not only receives exceptional attention but is also polarized like few other subdomains.

This exceptional politicization of policies targeting rent control and tenant protection begs the question of whose interests parties cater to (reject) when endorsing (opposing) these policies. Leaving aside the questions of if, how, or under which conditions preferences for rent control affected vote choice in the context of the 2021 German Federal Election (all of which are best addressed using postelection survey data), I propose a theoretical argument to explain why—and where—individuals are most likely to support rent-control policies. My argument emphasizes the interplay of individuals’ economic and geographic positions in the housing market by focusing on three central characteristics: homeownership, local rent levels, and disposable income.Footnote 3

2.2.1 Renters vs. Owners

The first part of my argument emphasizes the different market positions of renters and owners. For renters, booming local housing markets pose an immediate economic threat. Increases in customary local comparative rents not only systematically result in actual increases in household rents, but even before resulting in adjustments to existing rental contracts, they may signal that such rent increases are imminent (Abou-Chadi et al. 2021). As such, booming rental markets imply that renters can expect reductions in discretionary incomes sooner rather than later. Their pocketbooks are thus vastly exposed to sudden shocks in household rents. Unless they can bear the brunt of these shocks, either by relying on assets or by matching increasing rents by equally increasing household incomes, renters will experience a decrease in discretionary incomes. In severe instances, this may result in an overburden of rental costs—which, in turn, often results in involuntary moves. While renters in these situations may be able to stay in their current neighborhood, e.g., by moving to a smaller home or a home of lesser quality, they may also be forced to look for housing far from their old place of residence altogether. This illustrates how exposure to housing markets can quickly and severely disrupt the lives of renters, with implications not only for their finances but possibly also for their social integration.

By owning their homes, owners face a fundamentally different dependence on housing markets. Even when still servicing a mortgage, owners will not face additional monthly expenditures when the local house and rent prices around them increase. Developments in local housing markets, thus, do not affect owners’ short-term discretionary incomes. Instead, they contribute to the payoffs of a long-term investment. Buying a home—arguably the biggest investment most families make in a lifetime—means that owners have acquired an asset whose value depends on local housing markets (Ansell 2019). Homeowners thus benefit from booming markets that promise to increase their asset wealth. Rent market control, however, tends to decelerate these developments and to lower house prices of regulated units (Mense et al. 2018).

As this discussion shows, rent control can clearly benefit renters by protecting them from shocks to their pocketbooks—shocks that not all renters can easily compensate for. On the other hand, rent control not only offers no such benefit to owners but also undermines their long-term economic interests. This yields the following hypothesis:

H1: Renters are more likely than owners to support rent control.

2.2.2 Geoeconomic Differences in Renters’ Preferences: Market Rents and Disposable Income

Although renters are in a drastically different market position than owners, not all renters’ market positions are alike. Focusing exclusively on the subgroup of renters, I argue that two important characteristics condition how strongly renters will support rent control: their place in the rental geography of Germany and their place in the income distribution.

From a sociotropic renter’s perspective, there is no apparent reason not to support rent control. Even when renters live in an area where rents are structurally low and the policy would have little to no effect, supporting the policy would ultimately come without costs, albeit also with little to no expected benefit. Yet, given that rent levels are highly geographically stratified (for empirical evidence, see Fig. 2), I expect that renters in high-rent areas will more uniformly support rent-control policies than renters in low-rent areas. This is because rent-control policies come with different priorities for renters in different places. First, renters in high-rent areas are more likely to experience the material problems that rent-control policies seek to tackle firsthand. This is a perspective that renters in low-rent areas lack. Second, and perhaps more important, renters in high-rent areas are also more likely to be confronted with debates surrounding the policy in both the political and social contexts that surround them. As a result, these egotropic considerations and local context effects should result in a greater sense of urgency among renters in high-rent areas, which, in turn, should result in firm and solidified views in favor of rent control.

Geographic distribution of 2020/2021 median market rents across 299 electoral districts

H2: Renters in high-rent areas are more likely to support rent control than renters in low-rent areas.

Geographic variation in rent levels is likely to affect the priorities that individuals assign to rent control and, as a result, is likely to affect their average levels of support for the policy. However, this sense of urgency does not necessarily affect all renters alike. While protecting current renters from rapid increases in their rent loads, rent-control policies may discourage investments in the regulated stock of rental housing, result in a reduction of available housing supply, and halt processes of local development and neighborhood upvaluation—at least when the regulated local sector is large (see, e.g., Mense et al. 2018). Thus, rent control may have different appeals to different groups of renters. On the one hand, it shields low-income renter households against sharp increases in rent loads and thereby protects against reductions in discretionary income that may push households toward housing cost overburden and residential displacement. High-income renter households, on the other hand, are less likely to be existentially threatened by increasing rent levels and may instead fear the possible negative externalities of rent-control policies. Thus, instead of favoring policies that protect low-income renters, high-income renters in high-rent areas may favor the (costly, but affordable) positive externalities of gentrification (also cf. Hankinson 2018).

H3: The effect of local rents on support for rent control is stronger among renters in low-income households than among renters in high-income households.

3 Empirical Strategy

3.1 Data

To test my theoretical expectations, I used data from the GLES. Specifically, I used the initial release of the GLES Cross-Section 2021 Pre-Election Survey (GLES 2022).

3.1.1 Outcome Variable: Individual Preferences for Rent Control

For a long time, measures on specific preferences on the issue domain of rent and housing policy were unavailable for social science research, arguably due to a lack in societal and academic relevance that justified their inclusion in general social and election surveys. With the inclusion of an item prompting respondents to disclose their preferences for the highly politicized issue of a nationwide rent cap, the GLES Pre-Election Cross-Section 2021 has overcome this limitation at last. As part of a broader item battery on political attitudes and preferences, respondents are asked to indicate their views on the statement that “[t]he government should implement a nationwide rent cap.” Respondents’ preferences are measured on a five-point Likert scale ranging from (1) “strongly agree” to (5) “strongly disagree,” with a neutral intermediate category (3) “neither agree nor disagree” (q27i). The item does not specify the specifics of the policy (e.g., if and how subnational variation in rental markets would determine the applicability or the different levels of a nationwide rent cap). Therefore, it is best understood as a statement of general support for stricter rental market regulation by the federal government.

3.1.2 Main Predictors

Homeownership: To distinguish individuals’ position in the housing market, I generated a trichotomous indicator (based on GLES item wum8). The first category is homeowners, i.e., individuals who live in a house or apartment owned personally or by members of their family. The second category is renters, i.e., individuals who live in a temporarily (sublet) or permanently rented house or apartment at market rent. The third, residual category is comprised of individuals living in service and work apartments or in social housing. Because individuals in these housing arrangements are, to a certain degree, exempt from the hypothesized market mechanisms, I excluded them from all analyses. As a result, we are left with a binary indicator distinguishing renters from owners.Footnote 4 This binary indicator constitutes the main predictor of interest in assessing H1 and defines the renter subset for the subgroup-specific tests of H2 and H3.

District-level rental markets: To capture market rents at the level of the 299 federal electoral districts, I used original aggregations of rental market statistics from the RWI-GEO-RED: Real Estate Data Scientific Use File (RWI; ImmobilienScout24 25,26,a, b).Footnote 5 This data collection provides detailed information on millions of rental objects (apartments and houses) advertised on ImmobilienScout24 since 2007. Roughly 96% of the objects are georeferenced, among others, at the levels of INSPIRE 1‑km2 grids and municipalities (Gemeinden). I used this information to link ads to electoral districts. The data management procedure is detailed in the online Appendix.

Focusing on ads for both rental apartments and rental houses posted between January 2020 and June 2021 (the most recent month included in the data), I retained all objects that could be linked to an electoral district and for which information on the base rent per square meter was available (i.e., all ads with complete information on both the total base rent and the area of the living space). This yielded a total of 2,284,595 advertised objects from 8760 municipalities. I then aggregated the square-meter rents of the rental objects within the 299 federal electoral districts to obtain a measure of district-level 2020/2021 market rents. Specifically, I took the district-level median, which is more robust to high-priced outliers than the mean.

Figure 2 shows the geographic distribution of these rent levels across Germany. As we can see, there is considerable variation in local rents, which range from 4.66 €/sqm to as much as 21.82 €/sqm, with a national district-level average of 8.84 €/sqm. The map displays high face validity. High rents in metropolitan areas in and around Munich, Berlin, Hamburg, Frankfurt/Main, Stuttgart, and the Rhineland around Cologne, Bonn, and Dusseldorf are contrasted by low rents in the rural periphery, such as most parts of Rhineland-Palatine, Lower Saxony, and eastern Germany. These external data are then joined with the GLES survey data using the IDs of respondents’ electoral districts (wknr).Footnote 6

Lastly, I measured respondents’ monthly equivalized net household income as a function of the GLES household income categories (d63) and household size (d3). I first mapped the income categories onto an approximate continuous scale by setting the first K−1 income bins to their midpoints and modeling the final top-coded category (“10,000 € or more”) based on the assumption that the upper end of the income distribution follows a Pareto distribution (see Hout 2004).Footnote 7 I then adjusted for household size by dividing monthly net household income by the square root of the number of household members. Given that income distributions tend to be heavily skewed, I applied a log transformation, \(\log (\cdot +1)\).

3.1.3 Background Covariates

Background covariates include a list of likely confounders, i.e., variables that are possible joint causes of the outcome and the main predictors. I first included basic demographics. I operationalized gender as a binary variable, distinguishing male and nonmale respondents (d1). An approximate measure of age was constructed as the difference of the survey year, 2021, and respondents’ year of birth (d2a). To account for systematic differences in preferences toward state intervention in the economy across eastern and western Germany, I included a binary measure of respondents’ East/West residence (ostwest2).

I measured respondents’ current labor market status by collapsing the detailed information from the GLES (d9) into four broader categories. These distinguish (1) economically active (full-time or part-time employment, apprenticeships, short-time working, marginally employed, or on parental leave), (2) unemployed, and (3) permanently inactive respondents (retired, working in the household), with an additional category capturing (4) individuals who have not yet entered the labor market (school and university students, those in retraining, or those in community service).

To construct a measure of respondents’ education, I used information on their highest level of general education (d7) and their professional training degrees (d8a–d8m). From these variables, I constructed a categorical indicator that yields a collapsed version of ISCED 2011. It distinguishes respondents with (1) lower secondary education or less, (2) upper secondary education, (3) postsecondary nontertiary training, (4) higher vocational training, and (5) tertiary polytechnic or university degrees.Footnote 8

3.1.4 Handling of Missing Data

Survey data are generally prone to item nonresponse. This phenomenon occurs when respondents do not provide valid information in response to a given question, e.g., because they do not know the answer or prefer not to disclose the information to the interviewer. I addressed missingness via multiple imputation using the Expectation Maximization Bootstrap algorithm implemented in AMELIA II (Honaker et al. 2011) to generate \(M=25\) imputed versions of the data. The imputation model contains all right-hand side and left-hand side variables included in the analysis, including additional covariates used as part of the robustness checks. All variables are supplied according to their level of measurement (e.g., continuous, bounded continuous, or categorical).

3.2 Models

3.2.1 Statistical Models

Because the outcome variable, support for rent control, is an ordered categorical variable, I used an ordered logistic model. Ordered logistic regression models the probability that an individual i chooses a category \(k\in \{1,2,3,4,5\}\) on the rent cap policy item as a function of K−1 ordered threshold parameters κ and a latent linear predictor ηi such that

where \(\text{logit}^{-1}(\cdot )\) is the inverse logistic cumulative distribution function.

The latent linear predictor ηi is modeled as a function of individuals’ values on the main predictors, denoted by the vector xi, and the background covariates denoted by the vector zi, with corresponding coefficient vectors β and γ, respectively.

Given that one of the main predictors, median market rents, is measured at the level of J electoral districts, I used a hierarchical specification with district-level random effects, νj, to account for the geographic clustering of multiple respondents in the same electoral district. These random effects are assumed to follow a normal distribution with mean zero and variance \({\sigma }_{\nu }^{2}\), i.e., \(\nu _{j}\sim \mathrm{N}(0,{\sigma }_{\nu }^{2})\).

I implemented and estimated this model in a Bayesian framework using Stan via the R package brms.Footnote 9 I ran the sampler in sets of two chains across each of the M multiply imputed versions of the data. Initially, each sampler collects 1000 warm-up samples (to be discarded) and 1000 post–warm-up samples, which I thinned by a factor of five to preserve memory.Footnote 10 I assessed convergence within each pair of chains by checking that the Gelman–Rubin diagnostic did not exceed a value of 1.1 on any of the model parameters.Footnote 11 I pooled the posterior samples across all imputations to obtain a mixture of the M posterior distributions (e.g., Gelman et al. 2004) and subsequently processed the pooled posterior samples into substantively meaningful quantities of interest. I used the GLES’ adjustment weights (rescaled for each subset of the data such that they had unit mean and sum to N) to multiply each entry in the model log-likelihood.

3.2.2 Quantities of Interest and Inference Criteria

Because my empirical interest lies with support for rent control, my predictive quantities of interest are conditional expected values. In the context of the hierarchical ordered logistic models, these are given by predicted probabilities of supporting a nationwide rent cap as a function of individual values on the main predictors, xi, and the background covariates, zi. As individual support, yi, is measured on a five-point scale with agreement captured by values \(y_{i}\in \{1,2\}\), this quantity can be calculated as \(\Pr (y_{i}\leq 2| \boldsymbol{x}_{i},\boldsymbol{z}_{i})=\text{logit}^{-1}(\kappa _{2}-\eta _{i})\).

To assess the effects stipulated by my hypotheses, I focused on associational quantities of interest derived as a function of all unit-level predicted probabilities. Specifically, I assessed H1 on renter–owner differences using average first differences between renters and owners, holding equivalized household income, average market rents, and all background covariates constant at their observed values. I assessed H2 on the effect of market rents on renters’ preferences for rent control based on the average marginal effect of a counterfactual 1 €/sqm increase in market rents, holding household income and all background covariates constant at their observed values. Lastly, I scrutinized H3 using the conditional marginal effect of a counterfactual 1 €/sqm increase in market rents conditional on various levels of log equivalized household income. Following Hainmueller, Mummolo, and Xu (2019), I supplemented results based on a linear interaction effect with results based on a tertile-binned version of the moderator.

For inference, I presented the full posterior probability distribution of each associational quantity of interest. Contrary to the null hypothesis significance testing (NHST) paradigm of statistical inference, Bayesian inference based on full posteriors presents the exact probability of support for a given directional hypothesis in light of the data. As such, it overcomes the binary conceptualization of statistical significance characteristic of the NHST approach, in which one either rejects or fails to reject a null hypothesis given an arbitrarily chosen significance level (e.g., Gill 1999; McShane et al. 2019). Instead, posterior probability distributions provide a continuous measure of statistical support of variable baseline hypotheses.

3.2.3 Robustness Checks

In order to assess the sensitivity of my findings to alternative model specifications, I conducted three types of robustness checks:

-

To assess the sensitivity of my findings to the choice of the statistical model, I replicated the analyses using two alternative model specifications: a hierarchical linear model and a hierarchical logistic model (distinguishing supporters of rent control from nonsupporters).

-

Next to respondents’ East/West residence, I included an indicator on whether respondents lived in an urban, suburban, or rural (towns, village, and single homesteads) environment (wum6). Jointly, these variables are likely to absorb much of the geographic variation in district-level rents. Given that rents are measured at a fairly coarse geographic level, testing to which extent the hypothesized effects hold within different types of localities constitutes a very hard test of the theoretical argument.

-

As discussed above, generalized political orientations can be conceived of as mediators through which the effects of economic self-interest on policy preferences unfold. To assess whether the hypothesized mechanisms were distinct from mechanisms that operate through generalized political orientations, I estimated the direct effects of homeownership, market rents, and household income, blocking indirect effects that may unfold via generalized ideological self-placement (q37; measured on an 11-point scale from 1 “left” to 11 “right”), generalized economic preferences (q40; measured on an 11-point scale from 1 “lower taxes and fewer social services” to 11 “more social services and higher taxes”), and leaning toward a political party (q75a; a multicategorical indicator that distinguishes the six parliamentary groups represented in the Bundestag as well as the residual category “Others” and those who do not lean toward any political party).

3.2.4 Additional Preregistered Descriptive and Exploratory Analyses

To allow for further contextualizations of my analyses, I supplemented the preregistered confirmatory tests (and corresponding robustness checks) of my hypotheses with additional exploratory analyses (reported in the online Appendix). I reported descriptive (i.e., unadjusted) estimates of the relationship between preferences for rent control on the one hand and renter/owner status, local market rents, equivalized household income, as well as the tendency to lean toward a political party and vote intention (q8bb) on the other. Additionally, I replicated the tests of the renter-specific H2 and H3 for the subgroup of homeowners. This allowed me to explore whether and how the interplay of rental markets and household incomes affected owners’ preferences for rent control.

4 Results

4.1 Descriptive Evidence

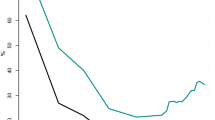

Given the novelty of analyzing preferences for rent control in empirical political science research, this section presents some descriptive information on the popularity of the introduction of a hypothetical nationwide rent cap in Germany. Figure 3 shows the expected values (i.e., predicted probabilities) from a hierarchical ordered logistic null model of respondents’ support for the policy in the GLES 2021 Pre-Election Cross-Section. As we can see, rent control enjoys widespread popularity, with roughly 61% of respondents (strongly) supporting the policy. In contrast, only 20% of respondents (strongly) oppose the policy. The remaining 19% are neither in support of, nor in opposition to, the introduction of a rent cap.

Expected values (predicted probabilities) from a hierarchical ordered logistic null model. Posterior medians and 95% credible intervals

Bivariate descriptive analyses (cf. Figs. 12.1–12.5, online Appendix) explore the associations between preferences for rent control and individuals’ position in the housing market. First, with a predicted support of 73.6% (71.6%, 75.7%) vs. 53.0% (51.0%, 54.9%), a rent cap is decisively more popular among renters than among owners. Second, I found a weakly negative association between district-level market rents and respondents’ support for rent control. Third, I found a strong and negative association between equivalized household income and preferences for rent control. Whereas the predicted support for a nationwide rent cap ranges between 71% and 92% in households with a monthly equivalized income of less than 1100 €, the prediction falls below 50% for households with a monthly equivalized income of 3700 € or more. Lastly, individual support for a nationwide rent cap has clear partisan underpinnings. Conditioned on either partisanship or vote intentions, the predicted support for the rent cap is between 40% and 50% among FDP and CDU/CSU supporters and slightly greater than 50% among AfD supporters. In contrast, supporters of left-wing parties overwhelmingly support the policy, with roughly 70% in favor among supporters of the SPD and the Greens, and greater than 80% among supporters of the Left.

4.2 Confirmatory Evidence

4.2.1 Main Analyses

The first theoretical expectation, H1, argues that renters should support rent control more strongly than homeowners do. While the descriptive evidence discussed above supports this expectation, this finding may, in part or in whole, be a spurious reflection of structural compositional differences between the group of renters, e.g., with respect to sociodemographic characteristics, income, or residence in specific housing market segments. Therefore, the first main analysis reassesses the average difference in support for rent control between renters and homeowners while adjusting for the background covariates introduced above. Ceteris paribus, 52.0% (50.0%, 54.0%) of homeowners and 71.0% (68.8%, 73.1%) of renters support the policy. This vastly reflects the unadjusted probability difference from the descriptive analyses presented above. Thus, in support of H1, even after adjusting for sociostructural, socioeconomic, and geoeconomic differences between renters and owners, renters support the introduction of a nationwide rent cap far more strongly than homeowners do.

Figure 4 presents a targeted assessment of H1 using the preregistered quantities of interest and inference criteria. The upper part of the figure plots the cumulative posterior probability (y-axis) along various potential values of the quantity of interest (x-axis), i.e., the average first difference in support for a national rent cap between renters and homeowners. This quantity reflects the probability of observing an effect at least as large as a given value on the x-axis, given the model and the data. Conversely, we can use the complementary probability to infer the probability of observing an effect larger than a given value on the x-axis. We, thus, find near-zero probabilities of observing an average first difference of less than 14 percentage points or more than 24 percentage points between renters and owners. The 95% credible interval, shown in the lower part of the figure, indicates 2.5% probabilities of finding an average first difference of less than 16.4 percentage points and of more than 21.6 percentage points, respectively, with a posterior median of 19 percentage points.

Average first difference in support of a national rent cap between renters and owners. Upper: cumulative posterior probability. Lower: posterior median and 95% credible interval

The second theoretical expectation, H2, stipulates a positive effect of local market rents on renters’ support for rent control. This expectation stands in contrast to the descriptive evidence presented above, which shows a negative relationship between rents and residents’ support for rent control. However, this association reflects an average of renters’ and homeowners’ preferences for rent control. Furthermore, it does not account for potential confounders. For instance, structural differences on variables such as income may codetermine residential self-selection into high-rent areas and opposition to rent control. Therefore, I assessed the average marginal effect of a counterfactual € 1/sqm increase in district-level market rents on the probability of supporting the introduction of a nationwide rent cap in the subsample for renters, adjusting for all preregistered background covariates.

Figure 5 shows the corresponding evidence. As Fig. 4 above, the upper part of the plots shows the cumulative posterior probability along a sequence of values for the estimated quantity of interest, whereas the lower part compactly summarizes the posterior distribution through the posterior median and the 95% credible interval. As we can see, with a 34.9% probability of a negative effect and a complementary 65.1% probability of a positive effect, there is no conclusive support for a positive effect of district-level market rents on renters’ support for a national rent cap. The posterior median and 95% credible interval of a predicted 0.1 (−0.5, 0.8) percentage point increase in support for rent control for each € 1/sqm increase in market rents reflect this uncertainty about the directionality of the effect. Thus, the analysis does not lend support to H2: There is no conclusive evidence that renters in high-rent areas are generally more supportive of rent control than renters in low-rent areas.

Average marginal effect of district-level market rents on renters’ support for a national rent cap. Upper: cumulative posterior probability. Lower: posterior median and 95% credible interval

While H2 stipulated a general positive effect of market rents on renters’ support for rent control, H3 specified a conditionality in this effect: We should primarily expect such a positive effect among low-income renters who are particularly vulnerable to the economic burden of high rents. Thus, in spite of the absence of an unconditional effect of market rents on renters’ support of rent-control policies, we may expect a positive conditional effect among low-income renters.

To assess this hypothesis, Fig. 6 displays the average marginal effect of a counterfactual € 1/sqm increase in district-level market rents, conditional on equivalized household income.Footnote 12 For a compact display, the figure shows posterior medians (solid line) along with the 95% credible interval (shaded area). As we can see, the overall pattern of effect heterogeneity is in line with H3: The effect is positive and most pronounced among low-income renters and turns negative as equivalized household incomes exceed approximately 2500 € This shows that high local rents do, indeed, prompt higher support for rent control among respondents from economically vulnerable households. Albeit in line with H3, support for the hypothesis is relatively weak. While the posterior probability of a positive effect exceeds 98% at the lowest values of equivalized household income, the substantive magnitude of this effect is modest at a predicted 0.96 (0.01, 2.22) percentage point increase in the probability of supporting rent control per € 1/sqm increase in market rents.

Conditional average marginal effect of district-level market rents on renters’ support for a national rent cap by equivalized household income. Posterior median and 95% credible interval

4.2.2 Robustness Checks

All robustness checks, preregistered above and reported in the online Appendix, produced findings that are substantively consistent with those from the main analyses. The robustness checks that test the sensitivity of the findings to different models confirm the original conclusions, albeit with some nuances. Whereas the moderation pattern in H3 is marginally weaker in the hierarchical logistic model (cf. Fig. 11.6, online Appendix), which sacrifices some information on the outcome variable by collapsing the five-point Likert scale into a binary variable, it is more prominently pronounced in the hierarchical linear model (cf. Fig. 11.3, online Appendix), which treats the outcome variable as a five-point continuous measure. The use of the binned moderator (cf. Fig. 11.19, online Appendix) confirms a positive effect of local market rents in the lowest tertile of household income, though the evidence is weaker than in the models using the continuous version of the moderator.

Those robustness checks that extend the main analyses by adjusting for additional covariates in hierarchical ordered logistic models confirm the findings from the main analyses. They consistently show a sizable gap in support of a national rent cap between renters and owners in accordance with H1, the absence of the unconditional effect of district-level market rents among renters stipulated by H2, and a modest level of heterogeneity in this effect between respondents from low-income and high-income households in weak support of H3.

5 Summary and Discussion

What explains voters’ preferences for rent control? This article has approached this novel question by emphasizing the interplay of individuals’ economic and geographic positions in the housing market. Departing from the differential egotropic economic effects of rent control for renters and homeowners, it has analyzed the interplay of individual economic resources and geotropic exposure to district-level rental markets among the group of renters. Taken together, the empirical results presented in this article highlight the precedence of egotropic considerations over geotropic effects that emanate from common exposure to similar market contexts. This is evidenced not only by two of the main findings—the differential support for rent control between renters and homeowners, and the differential effects of market rents between high-income and low-income renters—but also by two important insights from additional preregistered exploratory analyses.

First, I found a pronounced negative effect of market rents on homeowners’ support for rent control (cf. Fig. 12.6, online Appendix). This is consistent with the egotropic hypothesis that homeowners seek to avert policies that diminish the value of their assets. It contradicts geotropic accounts that predict homogeneous reactions of renters and homeowners due to shared exposure to similar residential contexts. Second, I found a strong and negative effect of equivalized household income on renters’ support for rent control, which was particularly pronounced in high-rent areas (cf. Figs. 12.8 and 12.9, online Appendix). Unlike shared exposure to local rental markets, individual financial resources thus strongly condition renters’ policy preferences.

It thus seems that individuals’ economic position in the housing market—defined by homeownership and financial resources—predicts preferences for rent control more consistently than their geographic position in the housing market. Given the robustness of these findings to voter ideology, socioeconomic preferences, and partisanship, this suggests that support for rent control is primarily determined by egotropic considerations. However, even though rent-control policies have clear economic beneficiaries, different egotropic mechanisms seem to underlie preferences for rent control. The strong support for rent control among low-income renters, whose discretionary incomes strongly depend on protection from increasing rents, reflects a classic economic pocketbook calculus. In contrast, the preferences of high-income renters are much less homogeneous. This indicates a greater willingness to accept the costs of living in booming regions in exchange for the positive externalities that come with it.

Although the evidence presented in this paper suggests that rental markets are of subordinate importance for preferences for rent control, this should not lead us to reject the general relevance of housing markets for individuals’ preferences on the issue domain of housing policy. First, owing to data restrictions, the analyses used median market rents in electoral districts. Electoral districts typically cover large areas and display significant internal market heterogeneity. Future research on this topic would, thus, benefit from using more fine-grained georeferencing to test the effects of local market contexts.Footnote 13 On the other hand, tests of pocketbook effects would drastically benefit from knowledge of respondents’ actual household rents and the size of their homes. Given the increasing importance of housing for individuals’ socioeconomic situations, such variables would be valuable additions to existing background covariates in general social and election surveys.

Second, market contexts may well affect housing policy preferences in ways that are not reflected by overall effects on voter positions on specific policies. As the “social question of our times,” the increase of affordable housing is a valence issue on which parties compete by proposing multidimensional policy packages. The rent cap is the most vividly debated, yet also the most polarizing, policy instrument proposed toward this end. Thus, soaring local rents may heighten the general importance that voters attribute to the issue domain while concurrently activating support for and opposition to any specific policy. A differentiated inquiry into voters’ housing policy preferences thus requires a more nuanced approach. Therefore, future research can benefit from extending the focus of inquiry from positions toward single specific policies to a comprehensive analysis of individuals’ salience attributions to housing policy on the one hand and their positional preferences for competing policies on the other.

Finally, over and beyond substantive insights into the determinants of preferences for rent control and implications for future research, this article yields a simple yet important take-away message: The introduction of a nationwide rent cap enjoys widespread popularity in the German electorate. Supporters of left-wing parties, perhaps unsurprisingly, firmly support this policy. But also among supporters of right-wing parties—all of whom have taken clear stances against rent caps in their manifestos—there are more voters who support the introduction of a rent cap than voters who oppose it. This implies that parties—and especially those who have so far campaigned against rent control—may benefit electorally from embracing the policy. Future programmatic competition over rent and housing policy could then revolve around the question of which policies should be implemented along with—not instead of—rent control.

Notes

See DESTATIS: Von Eigentümern bewohnte Wohnungen (Eigentümerquote) 2018. https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Wohnen/_Grafik/_Interaktiv/eigentuemerquote.html.

The theoretical argument, hypotheses, and research design were preregistered at the Open Science Framework (OSF) prior to the data release of the GLES 2021 Pre-Election Cross-Section. Technical choices, such as the selection and coding of variables, were informed by the prereleased questionnaire (GLES 2021).

With this emphasis on individuals’ geographic and economic market positions, my argument stipulates that economic self-interest determines individual support for rent control. A lively debate surrounds the question of whether self-interest affects issue-specific policy preferences in general (e.g., Weeden and Kurzban 2017) and housing policy preferences in particular (Hankinson 2018; Marble and Nall 2021). A frequent caveat against such arguments is that general ideological orientations—not economic self-interest—drive policy preferences. Rather than being joint causes of individuals’ economic position and their policy preferences or independent drivers of political preferences, however, individuals’ revealed ideological leanings may be the outcome of economic self-interest (e.g., Margalit 2013) or even aggregations of their policy preferences across multiple issues (Hinich and Pollard 1981). Thus, unless strictly conceptualized as an exogenous trait that predates both policy preferences and their presumed economic drivers, ideology should be thought of as an outcome of the hypothesized mechanisms rather than as an alternative or competing explanation to economic self-interest.

The binary indicator is based on information concerning individuals’ primary residence. As a result, it cannot identify, e.g., individuals who are owners of their primary residence but renters at their secondary residence or individuals who rent their primary residence while owning property elsewhere. Such individuals are not only cross-pressured by being renters and owners at the same time but are also affected by different local market contexts. As a result of this imperfect measurement, the hypothesized effects of ownership and market rents may be biased toward zero.

The scientific use files are free for academic use and made available by the data provider upon signing a data use agreement. For details, visit the web site of the FDZ Ruhr am RWI.

Although the smallest geographic unit available in the initial release of the GLES Cross-Section 2021 Pre-Election Survey, the electoral districts shown in Fig. 2 are fairly large. Consequently, there may be considerable heterogeneity in market rents between localities or neighborhoods within a given district. These small-scale nuances are clearly relevant for the hypothesized relationships between local market rents and renters’ support for rent control but will unavoidably be lost upon aggregation. This may bias the hypothesized effect of market rents toward zero.

This function uses the number of observations in the final two categories, NK−1 and NK, as well as the lower bounds of the respective income bins, \({X}_{K-1}^{\min }=7500\) and \({X}_{K}^{\min }=10000\), to model the mean value of the final category as \({X}_{K}^{\text{mean}}={X}_{K}^{\min }\times \left(1+\frac{V}{V-1}\right)\), where \(V=\frac{\log (N_{K-1}+N_{K})-\log (N_{K})}{\log ({X}_{K}^{\min })-\log ({X}_{K-1}^{\min })}\).

Specifically: 1. No school degree, Hauptschulabschluss, or Realschulabschluss; 2. Fachhochschulreife or Hochschulreife; 3. completed trades/crafts, agricultural, commercial, compact, or other vocational training; 4. completed technical, vocational, or specialized college certificate; 5. polytechnic or university degree.

I specified weakly informative normal priors for all regression coefficients, \(\beta \sim \mathrm{N}(0,5)\), \(\gamma \sim \mathrm{N}(0,5)\), and a weakly informative half-Cauchy prior for the standard deviation of the varying intercepts, \(\sigma _{\nu }\sim \text{Cauchy}^{+}(0,5)\).

The number of \(M=25\) imputations was not initially preregistered. As a result of choosing a large number of imputations, I increased the thinning factor post hoc from 2 to 5 to preserve memory.

Figures 10.1–10.3 in the online Appendix do not show any signs of nonconvergence. Otherwise, per my preregistration, I would have iteratively increased the length of warm-up and post–warm-up sampling periods until the model passed the convergence checks.

The corresponding model was estimated using a log-transformed version of equivalized household income, \(\log (\cdot +1)\). For an intuitive interpretation, the conditional average marginal effects were first calculated along a sequence of values on the log-scale, which were subsequently mapped back onto the original scale using the inverse transformation, \(\exp (\cdot )-1\), for visualization.

Ideally, local contexts should be defined such that they capture the relevant spheres of social and economic life that inform individuals’ perceptions and expectations. The specific size of these geographic frames of reference may, of course, differ across individuals, localities, and context characteristics. Future research on residential context effects should explore these questions in greater detail.

References

Abou-Chadi, Tarik, Denis Cohen, and Thomas Kurer. 2021. The political economy of rental housing. Conference Paper (SVPW 2021, EPSA 2021).

Adler, David, and Ben Ansell. 2019. Housing and populism. West European Politics 43(2):344–365. https://doi.org/10.1080/01402382.2019.1615322.

André, Stéfanie, and Caroline Dewilde. 2016. Home ownership and support for government redistribution. Comparative European Politics 14(3):319–348.

Ansell, Ben. 2014. The political economy of ownership: housing markets and the welfare state. American Political Science Review 108(2):383–402.

Ansell, Ben. 2019. The politics of housing. Annual Review of Political Science 22:165–185.

Ansell, Ben W. 2009. The “Nest egg” effect? Housing, the welfare state, and political incentives. Midwest Political Science Association Annual Conference, University of Minnesota.

Ansell, Ben, Frederik Hjorth, Jacob Nyrup, and Martin Vinæs. 2022. Sheltering populists? House prices and the support for populist parties. Journal of Politics https://doi.org/10.1086/718354 .

Baldenius, Till, Sebastian Kohl, and Moritz Schularick. 2020. Die Neue Wohnungsfrage: Gewinner Und Verlierer Des Deutschen Immobilienbooms. Leviathan 48(2):195–236.

Gelman, Andrew, John B. Carlin, Hal S. Stern, and Donald B. Rubin. 2004. Bayesian data analysis, 2nd edn., Vol. 40. Boca Raton, London, New York, Washington, DC: Chapman & Hall/CRC.

Gill, Jeff. 1999. The insignificance of null hypothesis significance testing. Political Research Quarterly 52(3):647–674.

GLES. 2021. GLES cross-section 2021, pre-election (ZA7700): pre-release of questionnaire documentation. Cologne: GESIS. Version 0.2, 2021-08-26.

GLES. 2022. GLES cross-section 2021, pre-election (ZA7700): data file version 2.0.0. Cologne: GESIS.

Hainmueller, Jens, Jonathan Mummolo, and Yiqing Xu. 2019. How much should we trust estimates from Multiplicative interaction models? Simple tools to improve empirical practice. Political Analysis 27(2):163–192.

Hankinson, Michael. 2018. When do renters behave like homeowners? High rent, price anxiety, and Nimbyism. American Political Science Review 112(3):473–493.

Hinich, Melvin J., and Walker Pollard. 1981. A new approach to the spatial theory of electoral competition. American Journal of Political Science 25(2):323–341.

Honaker, James, Gary King, and Matthew Blackwell. 2011. Amelia II: A Program for Missing Data. Journal of Statistical Software, 45(7):1–47. https://doi.org/10.18637/jss.v045.i07.

Hout, Michael. 2004. Getting the most out of the Gss income measures. Berkeley: University of California.

Kohl, Sebastian. 2017. Homeownership, renting and society. London, New York: Routledge.

Kohl, Sebastian. 2018. The political economy of homeownership: a comparative analysis of homeownership ideology through party manifestos. Socio-Economic Review 00(0):1–28.

Larsen, Martin Vinæs, Frederik Hjorth, Peter Thisted Dinesen, and Kim Mannemar Sonderskov. 2019. When do citizens respond politically to the local economy? Evidence from registry data on local housing markets. American Political Science Review 113(2):499–516.

Marble, William, and Clayton Nall. 2021. Where self-interest trumps ideology: liberal homeowners and local opposition to housing development. Journal of Politics 83(4):1747–1763.

Margalit, Yotam. 2013. Explaining social policy preferences: evidence from the great recession. American Political Science Review 107(01):80–103.

McShane, Blakeley B., David Gal, Andrew Gelman, Christian Robert, and Jennifer L. Tackett. 2019. Abandon statistical significance. American Statistician 73(sup1):235–245.

Mense, Andreas, Claus Michelsen, and Konstantin A. Cholodilin. 2018. Empirics on the causal effects of rent control in Germany. In Beiträge zur Jahrestagung des Vereins für Socialpolitik 2018. https://www.econstor.eu/handle/10419/181625.

RWI, and ImmobilienScout24. 2021a. RWI real estate data—apartments for rent—SUF. RWI-GEO-RED. Version: 1. Essen: RWI—Leibniz Institute for Economic Research.

RWI, and ImmobilienScout24. 2021b. RWI real estate data—houses for rent—SUF. RWI-GEO-RED. Version: 1. Essen: RWI—Leibniz Institute for Economic Research.

Seehofer, Horst. 2018. Wohnraumoffensive: Die Soziale Frage Unserer Zeit. BBB: BundesBauBlatt Online 11/2018. https://www.bundesbaublatt.de/artikel/bbb_Die_soziale_Frage_unserer_Zeit_3251898.html.

Weeden, Jason, and Robert Kurzban. 2017. Self-interest is often a major determinant of issue attitudes. Political Psychology 38:67–90.

Acknowledgements

I thank Tim Allinger, Nick Baumann, and Andreas Küpfer for their excellent research assistance. This article has benefited from the use of high-performance computing services provided by the state of Baden-Württemberg through bwHPC, which is funded by the German Research Foundation (DFG) through grant INST 35/1134‑1 FUGG.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

D. Cohen declares that he has no competing interests.

Additional information

Registration: https://osf.io/gwz4f

OSF Repository: https://osf.io/yxfp5/?view_only=9a88319188c94bcd9314ca466b11f3de

Supplementary Information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Cohen, D. Preferences for Rent Control: Between Political Geography and Political Economy. Polit Vierteljahresschr 64, 183–205 (2023). https://doi.org/10.1007/s11615-022-00404-8

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11615-022-00404-8