Abstract

Countries prohibit firms’ transnational financial crime by coordinating their regulations under international organizations (IOs). Under these IOs, states threaten to prosecute firms’ foreign misconduct at home. Such threats can help conscript companies to diffuse sustainable business models abroad. This paper studies the effect of corporate criminal regulations on firms’ foreign direct investment (FDI). Critics of these policies claim they push firms’ investment away from host economies where financial crime is more likely to happen. Yet, regulations should also cut informal costs of crime and favor investment. I reconcile these opposed expectations and show they are special cases of the same argument. I claim that the effect of multilateral anti-bribery policies on FDI depends on the level of corruption of the host economy. It is null in non-corrupt countries. It is positive where corruption is moderate: here, laws provide legal leverage to refuse paying bribes and cut corruption costs. The effect is negative where corruption is endemic: here, anti-bribery laws expose firms to additional regulatory costs. I support the argument with multiple evidence. Company-level data on investment by 3871 firms between 2006 and 2011 show that regulated corporations have a \(27\%\) higher probability of investing in moderately corrupt economies than unregulated firms, which plummets to \(-52\%\) in extremely corrupt countries. A synthetic counterfactual design using country-dyadic FDI flows corroborates this finding. Results show that regulatory policies harmonized by IOs change international competition for FDI in ways that do not necessarily harm regulated firms.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

F21 , F23 , D73 , G38

1 Introduction

Corporate crime is made of complex cross-border transactions. For instance, a multinational company (MNC) can bribe in a foreign market to circumvent local competition and extract rents (Malesky et al., 2015). Bribe payments can be paid through bank accounts located in several countries (Cooley & Sharman, 2017) and recipients of bribes can conceal illicit funds in jurisdictions with poor money-laundering standards (Sharman, 2011).

Countries coordinate the regulation of such complex transnational flows by adopting common rules under international organizations (IOs) (Keohane, 1984). Members of the Organization for Economic Cooperation and Development (OECD), for instance, agreed on common anti-bribery policies in 1997 (Abbott & Snidal, 2002). Similarly, the Financial Action Task Force coordinates anti-money laundering efforts. Finally, in 2013 the OECD and G20 started a joint framework aimed at combating corporate tax evasion in the form of base erosion and profit shifting (BEPS). By creating these IOs, states extend the arm of their laws beyond borders (Kaczmarek & Newman, 2011) to prohibit foreign misconduct by companies incorporated in their jurisdictions. They conscript firms under their regulatory umbrella to diffuse sustainable corporate standards, often by threatening prosecution at home.

How do corporate criminal regulations affect firms’ legitimate activity such as foreign direct investment (FDI)? This question remains unanswered. Political economy expectations are twofold. First, policies would raise additional costs for regulated companies—i.e., firms whose home countries impose regulations against foreign crime—thus deterring investment. For instance, home countries’ anti-bribery laws would increase risk of investing into corrupt host countries where exposure to bureaucrats’ bribe requests is higher (Gueorguiev & Malesky, 2012) and so is the risk of prosecution (Cuervo-Cazurra, 2008). Yet, an opposite hypothesis expects that corporate criminal regulations empower firms’ foreign investment. They would force companies to keep business above board thus cutting costs induced by uncertainty of criminal practices in countries that otherwise lack regulatory standards. For instance, anti-bribery provisions can tie companies’ hands and force them to refuse bribe requests, cut down costs of corruption, and operate more efficiently (Perlman & Sykes, 2017). IO-sponsored regulations would thus offer companies an advantage when investing into countries with lax business standards.

In this paper I propose a single argument to unify these two expectations which I label, respectively, deterrence and empowerment. I study the effects of anti-bribery regulations on FDI. I argue that deterrence and empowerment are observable when considering investment into host countries at different corruption levels. Deterrence is observable in extremely corrupt hosts and empowerment dominates in moderately corrupt ones. Anti-bribery policies reduce firms’ incentives to participate in bribery deals (Jensen & Malesky, 2018) by adding regulatory costs to such exchanges. In doing so, regulations tie firms’ hands and incentivize them to secure business opportunities legally at lower costs (Davis, 2011). This effect modifies regulated firms’ expected utility in a potential host country—thus, the probability of an investment—in a direction that depends on its corruption level. This is so because bribery provides firms with greater rents in more corrupt economies (Ades & Di Tella, 1999). In moderately corrupt hosts, bribery offers no more lucrative perks than legal opportunities. Here regulation binds firms to refuse bribe requests, and operate more efficiently, without losing business. In very corrupt hosts, instead, bribery is frequent (Zhu, 2017) and refusing to take part in it implies the loss of access to exclusive rents (Malesky et al., 2015). Here, regulated firms expect a lower utility and are less likely to invest.

Empirically, I study laws under the 1997 OECD Anti-Bribery Convention that criminalized foreign bribe payments by companies headquartered in 44 ratifier countries. Two exercises support my argument. First, I leverage data from Beazer and Blake (2018) and model individual decisions by 3871 firms to invest in a foreign location between 2006 and 2011. I show that firms under the OECD Convention make investment decisions that depend non-linearly on the level of corruption of the host economy. Firms from ratifiers are no more likely than their unregulated competitors to invest in non-corrupt economies. They are up to \(27\%\) more likely to invest in moderately corrupt host economies. Instead, they are \(52\%\) less likely to invest in extremely corrupt destinations. This offers evidence in support of my argument at the level of investment decision-makers. Second, I find similar results when employing country-dyadic data in a generalized synthetic control design to identify the proposed effect more credibly.

The paper offers three distinct contributions. First, I show that regulations do not necessarily place a burden on companies’ FDI. I therefore speak to research on the effects of corporate regulations for international business. In the first place, this contributes to studies about the effect of anti-corruption policies on FDI. To the best of my knowledge, I offer the first attempt at reconciling two competing expectations (see Cuervo-Cazurra , 2008; Davis , 2011). I show that home countries’ anti-corruption policies create complex interactions with host markets’ institutional characteristics—as argued by Beazer and Blake (2018)—and alter firms’ business conditions: they can be both a liability and an asset. Beyond anti-corruption, this conclusion contributes to studies of firms’ regulatory preferences (Ahlquist & Mosley, 2021; Genovese, 2020; Kalyanpur & Newman, 2019; Kennard, 2020).

Second, I use the anti-corruption case to show that IOs can alter the behavior of MNCs. This connects the study to a classic international political economy area of research: whether, and by what means, international institutions affect behaviors of private transnational companies (Gray, 2009). A vast scholarship has studied the effectiveness of IOs regulating licit transactions on foreign investment. Studied examples include arbitration in investment disputes or institutions protecting investors’ rights (Allee & Peinhardt, 2011; Betz et al., 2021; Biglaiser & DeRouen, 2010; Neumayer & Spess, 2005; Skovgaard Poulsen, 2014; Tobin & Rose-Ackerman, 2011). I approach this topic from a different angle and study the effect on foreign investment generated by international corporate criminal laws and IOs keeping economic exchanges above board. In doing so, I document a form of policy diffusion where home countries negotiate common corporate standards under an IO umbrella and conscript domestically-incorporated companies to diffuse them abroad. Areas of global governance where states operate similarly include the prevention of money laundering, tax evasion, human rights violation, or environmental degradation (Putnam, 2009).

Finally, I contribute to the literature on IO effectiveness in pursuing global governance goals. I study IO effectiveness by looking at the behavior of firms under their umbrella (see Abbott & Snidal, 2010; Baradaran et al. , 2012; Findley et al. , 2015; Morse , 2019; Thrall , 2021). I offer a faceted perspective on whether anti-corruption IOs can reduce corruption. I find that effectiveness depends on the institutional context of the countries where firms under the IO umbrella operate. Findings that anti-corruption IOs favor companies’ investment into mid-range corrupt economies are good news for ensuring sustainable business models through multilateral negotiations. Because firms under anti-bribery laws are deterred from offering bribes (Jensen & Malesky, 2018), this motivates some optimism for the prospect of curbing (the international supply of) corruption without undermining investment.

However, conclusions are pessimistic for host countries with severe corruption levels which would perhaps need anti-corruption IOs to elicit a positive effect the most. I find that regulated firms tend to invest less here. These countries are left exposed to investments from unregulated firms who can arguably commit felonies, remain unpunished, and reinforce existing levels of corruption. This pessimistic conclusion adds to recent findings on the perverse effects of anti-corruption IOs induced by different standards among firms (Brazys & Kotsadam, 2020; Chapman et al., 2020) or by poor organizational practices (Ferry et al., 2020; Hafner-Burton & Schneider, 2019).

2 The effect of anti-bribery laws on foreign investment

2.1 The effect of foreign bribery on foreign investment

The literature on FDI and political risk assumes that a “parent” firm invests abroad—by establishing ownership of a foreign “subsidiary”—if doing so maximizes its expected utility. Expected utility maximization drives investment choices because an investment is relatively immobile ex-post, thus the firm evaluates expected future benefits against present costs (Dunning, 1980). For this reason, politics and institutions of the host drive firms’ utility expectations (Danzman & Slaski, 2022; Jensen, 2008; Jensen et al., 2012; Pandya, 2016; Pond, 2018). Bribery is among them (Busse & Hefeker, 2007).

BriberyFootnote 1 is an informal exchange between a firm and a public official. In a stylized deal, the public official demands a bribe in exchange for the discretionary award of a service—e.g., a contract in public procurement (Rose-Ackerman, 1975). The firm would leave the deal if it could obtain the same service without bribing. The bureaucrat wants to maximise the fee and would award the service to the firm’s competitors if the offered bribe were too small. Each actor’s power to extort or turn down bribe requests increases if they can leave the deal while still deriving what the counterpart was offering.Footnote 2

Firms’ power to turn down bribe requests decreases with the level of corruption of the host country.Footnote 3 Two factors result in this outcome: (i) the exclusive access to rents and (ii) the number of potential bribers. First, by bribing in corrupt economies firms gain a monopolistic position (Ades & Di Tella, 1999; Malesky et al., 2015) from which they extract rents (Pinto & Zhu, 2016; Zhu, 2017). Bribe-payers can secure the monopolistic access to natural resources (Knutsen et al., 2017) or construction deals.Footnote 4 Second, in more corrupt economies bribery is more frequent (Treisman, 2007). If a firm refused to take part in a corrupt deal, bureaucrats would easily find alternative bribers (Lambsdorff, 2002). Thus, in more corrupt economies firms will find it difficult to turn down bribe requests.

When deciding whether to invest in a corrupt country, a firm evaluates the expected utility deriving from taking part in such deals. A heated debate on whether corruption ultimately favors or harms FDI has found very mixed results (Barassi & Zhou, 2012; Egger & Winner, 2005; Zhu & Shi, 2019). In this paper, I remain agnostic on this relationship. I claim that a firm expects a higher utility if it anticipates that it will manage to turn down bribe requests—and obtain the same service it would have bribed for—or that it will bribe and extract rents larger than what it paid. Rather than discussing the effect of corruption on FDI, my goal is to derive testable implications on how home countries’ anti-bribery laws change firms’ foreign investment choices. I derive these implications in the next section.

2.2 The effect of anti-bribery laws on FDI

With anti-bribery policies, home countries threaten prosecution at home for companies which, under their jurisdiction, engage in foreign bribery. They increase costs of bribing (Cuervo-Cazurra, 2008). Next section describes the large fines and settlements levied by law enforcers since the 2000s. But costs are not limited to penalties.Footnote 5 For instance, authorities mandate that firms restructure their organization and monitor compliance with anti-bribery standardsFootnote 6 (Garrett, 2011).

How do anti-bribery policies affect firms’ investments in a corrupt host? I present my answer here. As argued above, a firm expects a positive utility (thus, it decides to invest) in a corrupt country if it can turn down bribe requests or pay the bribe cost and extract rents. I argue that anti-bribery laws imposed by the home country affect investment decisions by altering expected bribery costs and the power to turn down bribe requests differently in countries with different corruption levels.

In a nutshell, I argue that anti-bribery policies deter firms’ participation to bribery deals by increasing their cost. They tie firms’ hands and incentivize regulated firms to secure business opportunities legally, at lower costs. This leverage improves firms’ expected utility only where bribery offers relatively poorer perks than those that can be achieved legally, i.e., in less-corrupt economies. Here, refusing to bribe does not prevent access to profitable opportunities. The opposite occurs in extremely corrupt hosts, where bribing guarantees exclusive rents. Regulated firms’ foreign investment decisions reflect this differential change in expected utility.

I describe the effect of anti-bribery laws on investment choices in three scenarios. In each scenario a firm evaluates whether to set up a subsidiary in a foreign country. The first scenario considers a highly corrupt economy. The second describes a moderately corrupt economy. The final scenario considers a non-corrupt economy. I theorize the effect of anti-bribery regulations on the probability of an investment by comparing the utility expectation of a regulated firm and that of its unregulated counterfactual.

Scenario 1: Host countries with high corruption levels

The home country’s anti-bribery policies deter the investment choice in case of a highly corrupt host.Footnote 7 The regulated firm would risk anti-bribery prosecution at home if it took part in bribery deals, resulting in costs that it would not have faced without regulation. The expected corruption perks, instead, are the same. In expectation, therefore, bribery is less profitable for a regulated firm. Refusing to bribe would save corruption and regulatory costs. However, doing so would also likely imply the loss of access to the rents offered by corruption (Malesky et al., 2015) which are not easily obtained by legal means. Thus the regulated firm expects either to pay more for the same perks or to lose access to corrupt rents. As such, it expects a significantly lower utility than it would have without regulation when evaluating whether to invest in very corrupt economies. Consequently, a regulated firm will be less likely to invest in countries where bribery is entrenched in the business opportunities.

Scenario 2: Host countries with mid corruption levels

The regulated firm is, instead, more likely to invest in the second scenario—that of a moderately corruptFootnote 8 host—than it would be without regulation. Here, too, a regulated investor expects legal costs at home for partaking in bribery deals. However, because here bribery does not provide significantly more lucrative opportunities than those achieved legally, anti-bribery policies put the regulated firm in a position to resist bribe requests without losing business (Davis, 2011). Home-country regulations thus enhance the expected utility of regulated firms because they remove bribery costs. In the absence of regulation, the firm would not have enjoyed this prerogative and it would have experienced a lower utility.

Perlman and Sykes (2017) studied the US anti-bribery policy—the Foreign Corrupt Practices Act (FCPA)—by conducting interviews with corporate and legal practitioners that offer perhaps the most complete description of how invoking anti-bribery laws can help companies avoid bribe requests. They report that “[foreign] government agents know about the FCPA and know that bribes requested from American companies will not be provided. [...] Similarly, [...] the FCPA made it easier to avoid bribes by explaining to corrupt officials that it would be impossible to withdraw the necessary cash without detection” (Perlman & Sykes, 2017, 170). Thus anti-bribery laws improve firms’ power to turn down bribe requests by making them less frequent and by offering a “my hands are tied” type of argument out of a potential request.

Of course, regulated firms’ expected utility improves only if they do not risk losing business opportunities by refusing to bribe. Public officials can award the corruption perks to alternative bribers, if a regulated firm refuses to pay the bribe. Thus, regulation increases utility only if the size of the exclusive advantages offered by corruption is relatively small. I argue that a similar condition occurs in moderately corrupt economies. Here, corruption offers relatively less lucrative perks than what can be obtained legally (Ades & Di Tella, 1999). Thus, regulated firms expect larger investment benefits than they would have experienced in the absence of regulation: they find it easier to turn down potential bribe requests without losing significant business opportunities.

Scenario 3: Low corruption levels in host countries

Finally, in a scenario where the potential host country is non-corruptFootnote 9 the regulated firm is no more or less likely to invest than its unregulated counterfactual. Here, it is unlikely that local public officials will demand bribe payments at all. Because bribe requests here do not likely occur, the regulated firm would not expect different investment conditions than it would have without regulation.

So far, I have assumed vigorous law enforcement. In fact, some evidence suggests that anti-bribery laws might yield effects on FDI independent of that. Using 1980s data, Hines (1995, 19) found a “relative decline of American business activity in the more corrupt countries” right after the adoption of the US FCPA. As described in the next section, the FCPA was significantly under-enforced in the 1980s: prosecutors brought just 40 cases in the twenty years after its adoption “and settled these charges on sympathetic terms” (Brewster , 2017, 1614). The fact that the FCPA affected US companies’ business into corrupt economies even in a period of “enforcement silence” (Brewster , 2017, 1645) suggests that anti-bribery laws might change companies’ investment decisions regardless of their enforcement. Perhaps, the uncertainty about future levels of law enforcement couples with the long time-horizon entailed by an FDI and changes regulated firms’ investment as if the law were vigorously enforced.

In general, however, expectations of future law enforcement should condition whether policies have an effect on investment. If firms expected lax law enforcement, a regulated firm would not anticipate higher bribery costs. Thus, it would be no more or less likely to engage in bribery than without regulation. Similarly, expectation of lax enforcement would make anti-bribery regulations a weak hand-tying leverage. Thus, expectations of lax (vigorous) enforcement should weaken (strengthen) the effect of anti-bribery on FDI.

Expected effect of anti-bribery laws on investments, conditional on host country corruption

Figure 1 generalizes my expectations beyond the three scenarios. It sketches the effect of anti-bribery policies on the probability of a foreign investment (y-axis) at increasing levels of corruption of the host (x-axis). For low levels of corruption of the host, the effect is null. As the host economy becomes more corrupt, regulation empowers firms and increases their probability to invest. When the level of corruption increases, this effect reaches a maximum, decreases, and reverses. In extremely corrupt host countries, anti-bribery policies deter firms’ investment. Deterrence and empowerment are thus observable at different levels of corruption of the host.

My argument explains firms’ investment location choices, abiding by a tradition in the research on the political economy of FDI (Pandya, 2016). It describes how home corporate regulations interact with host country corruption to determine the decision to invest. To some extent, anti-bribery laws can also similarly affect firms’ decisions on the investment amount. A firm would be willing to invest more, and undertake greater costs, if it expected larger returns (Dunning, 1980). The risk of anti-bribery prosecution increases the expected costs of corruption for regulated companies investing in very corrupt economies, whereas rents offered by corruption likely do not vary with regulations adopted at home. Expected returns, net of investment costs, will thus be lower for regulated firms investing in very corrupt economies and so will be the size of their investment. Conversely, in moderately corrupt economies regulated firms expect larger returns because they can cut down on costs induced by corruption without losing profits. Here, regulated investment should be larger.

This should also hold if firms already have investments in a foreign corrupt country, representing sunk costs. Market exit is costly for firms with existing sunk costs (Barkema et al., 1996; O’Brien & Folta, 2009), so investing larger amounts might be relatively cheaper. This might make these companies relatively indifferent to the presence of home anti-bribery regulations. However, Perlman and Sykes (2017) notice that anti-bribery laws work similarly to investment treaties in that they protect investors who already have sunk costs in a country from opportunistic attempts by host bureaucrats to expropriate bribes. This seems to imply that even firms with existing investment in a country would make decisions on investment amounts that are influenced by anti-bribery laws consistent with my argument.

3 The OECD anti-bribery convention

Although laws against domestic corruption have a long history, policies that forbid companies from paying bribes abroad are more recent. The US was the first country to prohibit foreign bribery when, in 1977, Congress passed the Foreign Corrupt Practices Act (FCPA) as a response to the discovery of bribe payments made by several major US companies abroad.Footnote 10 However, enforcement of the FCPA lagged for two decades because non-US competitors lacked similar regulations (Brewster, 2017). Until 1997, about half of the OECD countries even endorsed such payments by making them tax-deductible (Gutterman, 2015). In this context US administrations feared enforcing the FCPA would have tilted the playing field of international competition against US-based companies.

In the late 1970s and 1980s the US attempted to secure an anti-corruption international treaty in order to level the playing field of international business. Attempts made at the United Nations, the International Chamber of Commerce, the OECD, and the Tokyo Round of the General Agreement on Tariffs and Trade failed to secure anything more than non-binding recommendations (Brewster, 2017): “Because other governments understood that Congress could not undo the FCPA, the United States had no interest-based leverage” (Abbott & Snidal, 2002, 162).

Western countries’ reluctance to adopt anti-bribery rules failed in the 1990s, when a shift in norms and corruption salience made an OECD anti-bribery treaty inevitableFootnote 11 (Abbott & Snidal, 2002). In this decade, scandals of corruption hit Western public opinion (Tarullo, 2004) and “various NGOs [...] demanded that OECD governments confront the consequences of their policies of tolerance of [...] foreign corruption by their multinational corporations” (Brewster , 2017, 1641). The US strategically used issue salience to secure a major international anti-corruption treaty at the OECD by leveraging European officials’ fear of public criticism. Allegedly, the US Assistant Secretary of State for Economic and Business Affairs at the time “carried with him (or told people he did) a list of the 10 largest bribe-paying companies in the world. When officials became recalcitrant, he would tap his jacket pocket, suggesting he could make the list public.” (Abbott & Snidal, 2002, 164).

The OECD Anti-Bribery Convention was ratified in 1997, initially signed by 34 countries including five non-OECD members.Footnote 12 Ten more countries have ratified the treaty since 1997.Footnote 13 Membership covers a disproportionate share of the global economy: MNCs under the regulatory umbrella of the Convention account for more than 80% of global outbound foreign direct investment stocks. They include 95 of the 100 largest non-financial enterprises and the 50 largest financial companies (OECD, 2018).Footnote 14

The Convention is an instrument of hard-law (Abbott & Snidal, 2000). Articles 1 through 4 legally bind ratifiers to adopt policies that prohibit companies, foreign employees, subsidiaries, and individuals under their jurisdiction to pay bribes in international business. To date, all parties have adopted the necessary laws to implement the Convention. Under Article 5, the Convention mandates countries to enforce laws against domestic subjects suspected of foreign bribery.

How have treaty members complied with the OECD Convention over time? Answering this question is important in order to understand companies’ expectations of future law enforcement. During the first decade member countries mostly focused on the adoption of laws required under the Convention. They achieved two crucial goals. First, members harmonized corporate criminal laws (Brewster, 2017; Spahn, 2013). Far from being formal, these achievements included the removal of favorable tax treatments for companies engaging in foreign bribery (Gutterman, 2015). It is likely that companies regarded such legalization process as a credible commitment against corporate corruption (Abbott & Snidal, 2002). Second, in early years member countries developed networks of mutual legal assistance (MLA) and cooperation defined under Article 9.

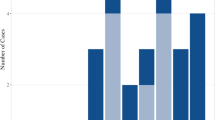

Enforcement of the Convention was mostly done by the US in this first decade. The OECD Convention had “levelled the playing field” of international competition and extended anti-bribery laws to US firms’ competitors. The US Department of Justice (DOJ) and the Securities and Exchange Commission (SEC) could thus significantly fast-track enforcement from the end of the 1990s (Brewster, 2017; Leibold, 2014). Crucially, such significant increase in enforcement did not only target US-based companies. Under the FCPA extraterritorial provisions, the DOJ and the SEC enforce the US anti-bribery law against non-US companies headquartered in OECD Convention signatories by leveraging MLA networks (Spahn, 2013). Figure 2 describes this “international-competition neutral” strategy (Brewster , 2017, 1615). Since the early 2000s, the number of FCPA cases and fines levied from US and non-US firms significantly increased, experiencing a peak in 2010. Importantly, this time of growing enforcement overlaps with the period considered by the analysis in the next section.

FCPA enforcement. Number of cases and fines. Shaded area reports the time-period of the firm-level analysis. Data from the Violation Tracker, Good Jobs First

Such intense US-lead enforcement of the Convention stimulated OECD Convention members to start applying their own anti-bribery policies (Kaczmarek & Newman, 2011). Excluding the US, the median ratifier of the OECD Convention brought its first anti-bribery case in 2005 (earliest enforcement in 1998, latest in 2008).Footnote 15 By 2010, judicial authorities in treaty members like France, Germany, Italy, Norway, Switzerland, the UK, and the US fully cooperated in important and highly publicized cases. They involved US-based companies (e.g., Baker Hughes, Monsanto, Halliburton, and the Titan Corporation), but also large non-US MNCs—including ABB Ltd., BAE Systems, ENI, Innospec, JGC Corp, Siemens, Statoil, and Technip (Spahn, 2012).

Have law enforcement actions been biased against certain countries or industries in a way that might alter firms’ expectations? Scholarly answers are mixed. McLean (2012) finds that FCPA enforcement between 2000 and 2011 was mainly determined by the level of corruption of the host country. Early law enforcement, it seems, just followed the bribes where they were more frequent. However, Tomashevskiy (2021) extends the data to consider more recent FCPA cases and finds that US agencies disproportionately target “unfriendly” countries to the US. Work by Garrett (2020) also suggests that, in recent years, corporate law enforcement might have followed political objectives rather than the occurrence of crime. Choi and Davis (2014) find that US agencies levy disproportionally larger fines from non-US companies, even when holding constant the size of the bribe, perhaps as a way to set an example.

Because studying determinants of enforcement exceeds my scope, I address the issue in two ways. First, I focus on the early years of the Convention when companies likely had limited observations of past law enforcement to expect biases. Second, within this narrow time-frame I investigate whether past enforcement actions by country or sector factor differently into investment choices (Appendix F).

4 Empirical analysis

I propose two empirical exercises to test my argument that anti-bribery policies affect foreign investment decisions non-linearly depending on the level of corruption of host economies. The first one applies a selection on observables design on firm-level data about foreign investment decisions. The second employs a generalized synthetic counterfactual design on dyadic country-level FDI data.

4.1 Firm-level analysis

My firm-level analysis models binary investment choices. A firm f from country i invests in country j if its propensity to invest, \(I^{*}_{fij}\), is greater than 0. In Eq. 1, \(I^{*}_{fij}\) is a function of whether country i is a signatory of the OECD Convention (\(S_i = 1\)), and of a continuous measure for the level of corruption of the host country (\(C_j\)). Corruption also appears as a squared term (\(C^{2}_j\)). Both \(C_j\) and \(C^2_j\) are multiplied by \(S_i\). This represents the statement that the effect of the OECD Convention on the propensity to invest abroad is non-linear in the level of corruption of the host country.Footnote 16 Matrix \(\mathbf {X_{fij}}\) includes covariates and \(u_{fij}\) is the idiosyncratic error term.

The non-linear effect of the OECD Convention on the propensity of a firm to invest abroad, conditional on the level of corruption of the host country, is derived in Eq. 2. It is a parabola with an expected inverted-U shape, as in Fig. 1. Therefore, \(\beta _1\) is expected to be negative, \(\beta _2\) positive, and \(\beta _3\) null.

I estimate Eq. 1 with OrbisFootnote 17 firm-level data retrieved from Beazer and Blake (2018). This dataset reports information on the portfolio of foreign subsidiary incorporations by 3871 parent firms between 2006 and 2011 i.e., in early years of the Convention. It reports the home countryFootnote 18 of the parent (62 in total) and that of the subsidiary (host country, 86 in total) for each incorporation.Footnote 19

The dataset is a cross-section of the investment choices of firms between 2006 and 2011, where each company is paired with each potential host country. Potential host countries are all economies where a subsidiary has been established by at least one firm in the dataset. This is supposed to represent all attractive host countries.Footnote 20 The binary outcome variable (\(\text {Subsidiary}\)) codes whether a firm f is the “ultimate parent” of a subsidiary in host j between 2006 and 2011. Subsidiary incorporations do not include financial investments and small firms are excluded from the sample which thus represents a population composed of large MNCs embarking in long-term foreign productive enterprises, rather than speculative ventures.Footnote 21

Skeptical readers might be concerned that, between 2006 and 2011, the OECD Convention had no dent against foreign bribery because many signatories fast-tracked enforcement in later years. This is a relevant concern: as argued in the previous section, credibility of enforcement is necessary for anti-bribery rules to have an effect on firms’ investment decisions.

However, as argued above, lax enforcement should draw towards the null equally deterrence and empowerment. Any significant finding I observe from a period of lax enforcement should therefore be larger in magnitude in times of stronger enforcement. Moreover, whether the mid-2000s represented a period of enforcement silence can be debated. US authorities vigorously applied the FCPA against non-US companies headquartered in OECD Convention signatories at the time (Fig. 2). Also, as argued above, the 2000s did not represent a period of non-compliance with the OECD Convention by other members: ratifiers signalled commitments to anti-bribery standards by adopting significant legal tools and by beginning to enforce their anti-bribery laws in a series of largely publicized cases (Spahn, 2012).

In Appendix, I propose some tests to probe this concern empirically. I show that results are robust to the extension of data from Beazer and Blake (2018) to consider investments made by these very firms until 2018 thus considering a period of stronger enforcement.Footnote 22 Moreover, a placebo test shows that the effect is detected only for firms in countries and industries that had experienced enforcement by 2005 and that could therefore reasonably expect future actions (Appendix F).

My main explanatory variable is the binary \(\text {OECD Ratifier}\). It codes whether the OECD Anti-Bribery Convention was into force for home country i of a parent firm f by 2005. I consider the 2005 value for all variables on the right-hand side of Eq. 1, for it is the year before the start of my cross-section.

Next, I need a measure of the moderator: host-country level of corruption. Well-known limitations of perception-based measures of corruption (Gueorguiev & Malesky, 2012; Olken, 2009) make them a sub-optimal choice. These measures are built by surveying experts or the general population about perceptions or experiences of corruption. Social desirability biases answers about first-hand experiences (Treisman, 2007). Annual measures, moreover, are subject to confirmation bias if respondents’ answers are informed by previous releases. Finally, these indexes often implicitly adopt a definition of corruption not aligned with that of respondents or researchers (Heywood, 1997). Alternative solutions leverage observable information. Measures like the observed number of bribery cases, however, are no reliable indicators of corruption since effective crime takes place out of sight. In my case they might reflect enforcement of the Convention, rather than levels of corruption of the host.

The Public Administration Corruption Index (PACI), from Escresa and Picci (2017), offers a valid alternative. The index leverages variation in the geographic distribution of observable cases of cross-border corruption to derive a measure of relative corruption among countries. It is based on the following intuition. Suppose we observed that a large share of foreign bribery cases exported from home country i involved host country j but j made up for a relatively modest share of i’s economic outflows. This would be evidence that j is relatively more corrupt than other partners of i because it attracts relatively more bribes. The PACI generalizes this intuition: it measures corruption of each host country as the deviation between the observed geographic distribution of cross-border bribes and the distribution that could be expected if all countries were equally corrupted and bribes followed economic flows.

I adopt this measure of corruption.Footnote 23 I also test robustness of my results to traditional perception-based measures and verify that my results hold.Footnote 24 Escresa and Picci (2017) compute the PACI employing information between 1997 and 2012. For each host country in my dataset, I re-compute the index using software and data provided by the authors. I consider bribes paid between 1997 and 2005 (included). The resulting measure \(\text {Host PACI}\) is my main indicator of corruption of the host economy. It ranges from 0 to 8.90, with higher values indicating more corrupt countries.

I explain my binary outcome variable in a multilevel logit model. This choice allows to specify the cross-level interaction in Eq. 1 (Bell & Jones, 2015). It also models the complex structure of the data (home-, host-, and dyad-level cross-nesting) accounting for unobserved clustering—e.g., companies’ advantage when investing in the same destinations as co-nationals (see Johns & Wellhausen, 2016). All specifications include cross-classified random intercepts at the dyad, home, and host countries-level.

I include covariates to control for potential confounders. I control for economic and institutional features of the host country: its (logged) Gross Domestic Product (GDP), per capita GDP, total trade, and net FDI inflows (both as GDP percentages). I include its Political Constraint (POLCON) III index, a binary indicator for democracy from Cheibub et al. (2010), and a measure for judicial independence (Linzer & Staton, 2015). Next, I control for home country features that could correlate with OECD Ratifier: wealth (logged GDP and GDP growth rate) and level of judicial independence. Then, I control for dyadic covariates. First, a measure of the distance in kilometres between capitals of the home and host. Second, dummies for: whether they signed a bilateral investment treaty (BIT); whether they have a past colonial relationship; and whether they have a common first or official language. Finally, I control for firm-level features: the number of host countries for each firm, its age, and its total assets (all logged).Footnote 25 Summary statistics are reported in Appendix.Footnote 26

4.1.1 Results

Table 1 presents my results relative to the variables of interest only.Footnote 27 In order to prevent suppression effects (Lenz & Sahn, 2021), Table 1 first includes only the variables of interest (1). Then, it adds host and home countries’ controls (2). Then, firm-level covariates (3), dyadic controls (4), and industry-level intercepts (5). Model 6 estimates the full model but updates the dependent variable from Beazer and Blake’s (2018) data with Orbis data on additional investments made by these 3781 companies from 2012 until 2018. Extensive robustness and placebo tests are presented in Appendix E and F.

Results are consistent with expectations. The coefficient of the interaction between OECD Ratifier and squared Host PACI is negative in size. It is distinguishable from zero at the 0.05 level of significance in all specifications but model 3 (p-value: 0.06). Estimates for the coefficient of the interaction with Host PACI are also positive and statistically significant at the 0.05 conventional level, but for Model 3 (p-value: 0.06). Coefficients are estimated with more precision when updating investment data to consider subsidiaries established until 2018.

I compute the marginal effect of anti-bribery policies at given levels of corruption to evaluate if the argument represented by Fig. 1 is supported (Brambor et al., 2006). I compute the percentage change in predicted probability of an investment when OECD Ratifier varies from 0 to 1, for given levels of Host PACI, holding everything else at its mean. I draw 95% confidence intervals from 1000 simulations of the sampling distribution of the estimated effect (King et al., 2000).

The non-linear effect of ratifying the OECD Convention on companies’ subsidiary incorporation, conditional on host-country corruption

Figure 3 shows results obtained when considering model 1 from Table 1. When OECD Ratifier changes from 0 to 1, the predicted probability that a firm will incorporate a subsidiary changes conditionally on the level of corruption of the host economy non-linearly. The effect can be roughly divided in panels (a), (b), and (c). Figure 3 reports the number of host countries included in each panel under the corresponding label. In panel (a) the change in predicted probability is close to zero for least corrupt hosts (e.g.: Canada, Denmark, Sweden). As the host country becomes more corrupt, firms from countries with anti-bribery policies have a higher probability of investing. At its maximum, firms from ratifiers have a 27% higher probability of investing than their competitors (hosts at the peak are Singapore and Taiwan).Footnote 28 As the host country becomes more corrupt (b), the effect of regulation remains positive but declines in size. This indicates that OECD anti-bribery policies still benefit regulated firms investing in economies like Brazil, China, Indonesia, Italy, Mexico, and the United Arab Emirates but to a lesser extent. For extreme levels of corruption—panel (c)—firms from ratifier countries are worse off. They have a lower probability of investing here than their unregulated counterparts, a quantity that reaches a lowest point of \(-52\%\) for host countries at the right-end of the corruption scale like Egypt, India, Kazakhstan, Nigeria, Russia, or Vietnam.Footnote 29

4.2 Country-dyadic analysis

The previous section provides micro-level evidence that firms subject to OECD anti-bribery policies make investment choices non-linear in the level of corruption of the host country. Yet, the analysis has two limitations. First, it cannot study changes in investment behavior, as it focuses on cross-sectional information. Thus, it cannot control for companies’ existing investments into countries with different corruption levels which might subject firms to different investment conditions (Perlman & Sykes, 2017). Second, selection under OECD policies is not random. OECD Convention ratifiers have characteristics that distinguish them from non-ratifiers (Table C.1). If random effects and controls did not account for such differences, the conditional independence assumption would be violated and the previous analysis would wrongly attribute the effect of these idiosyncrasies to anti-bribery policies. Time-varying data would provide a solution to both issues and allow to hold time-invariant characteristics constant.

In order to test internal validity of my estimates, I use country-level FDI data from the United Nations Conference on Trade and Development (UNCTAD). My argument is at the firm-level: it predicts the probability of an investment and, to some extent, its size. When aggregated up to the country-level, individual investment and size choices should still be detected albeit in a noisy manner. I intend this test as a solution of the identification problems highlighted above.

I use UNCTAD country-level data on foreign investment in directed dyads because my theory claims that the effect of a home-country anti-bribery policy is conditional on host-country corruption. I retrieve UNCTAD data, country-, and dyad-level covariates from Beazer and Blake (2018). My dependent variable is the logarithm of dyad-level net FDI flows. Information ranges from 1985 to 2006 included.Footnote 30 It thus covers the period preceding and shortly following the ratification of the OECD Convention. It also spans until the very beginning of my firm-level cross-section, thus offering a snapshot of how investment conditions changed before its onset. Represented home economies are 101 and host countries are 109. Descriptive statistics are in Table G.1.

I test my non-linear conditional argument by adopting a binning approach.Footnote 31 I divide dyads in five subsamples depending on the level of corruption of the host country in the dyad. I measure corruption using the same 2005 Host PACI index computed for the firm-level analysis.Footnote 32 The five subsamples are defined based on quintiles of the Host PACI distribution.Footnote 33 A total of 1765 directed dyads report information for the dependent variable and Host PACI. I estimate the effect of the OECD Convention for dyads in each of the five bins to study the impact of anti-bribery policies conditionally on the level of corruption of the host economy.

I identify the average treatment effect of the treated (ATT) dyads with a generalized synthetic control approach.Footnote 34 A dyad whose home country ratified the Convention is considered treated after the treaty has entered into force. Control dyads are those whose home countries did not ratify the agreement. My identification strategy draws on control dyads to impute one synthetic counterfactual for each treated dyad. It does so by maximizing similarity in pre-treatment trends between treated and synthetic controls. I choose this solution over a standard two-way fixed-effect (2FE) model because the treatment timing (entry into force of the OECD Convention) is staggered over the years 1999-2001 for early signatories and my panel dataset is unbalanced. I adopt the model proposed by Xu (2017), which allows for heterogeneity in treatment effects, staggered treatment timing, and unbalanced data.Footnote 35

Synthetic counterfactuals for treated dyadic FDI flows. Average trends by host corruption level

4.2.1 Results

Figure 4 reports results obtained in each corruption bin. Average pre-treatment trends of the synthetic counterfactuals closely approximate observed average trends of treated dyads in all bins. This lends confidence that synthetic control units were properly imputed. Post-treatment differences in average flows between observed and synthetic controls confirm expectations from the theory. On average, dyads with extremely clean host economies (first bin) saw a small or insignificant increase in their FDI flows in the post-treatment period. A positive effect, instead, is detected for dyads with moderately corrupt hosts (second and third bins). Post-treatment differences between observed and synthetic FDI dyadic flows are not significant for units in the fourth bin. Finally, FDI flows from ratifiers to the Convention were negatively affected for dyads with extremely corrupt host countries (fifth bin).

The effect of the OECD Convention on dyadic FDI flows at given host-country corruption levels. Estimates from synthetic counterfactual designs

Figure 5 reports the aggregated ATT over the entire time period for each of the five bins. It also reports the distribution of the Host PACI variable and the number of dyads in each bin. Estimates across the five bins reproduce the inverted-U pattern seen in the firm-level analysis. The Convention had a small effect on investment for dyads in the first bin (hosts include Australia, Canada, Denmark, and Sweden). As the host economy in a dyad gets moderately corrupt, the estimated effect is positive and statistically significant. This is true for dyads in the second and third bins, whose hosts include Brazil, Italy, Mexico, Singapore, and Taiwan. When converted from the logarithmic scale, estimates inform us that ratification increased net FDI flows from an average treated dyad, on an average post-treatment year, by about 2.01 million constant US dollars (second bin) and 1.83 million (third bin). These effects amount to an increase in FDI flows to dyads in the second and third bin of about 2.11% and 8.83% respectively, over the pre-treatment average. The effect declines in the fourth bin, where it is not statistically significant. It becomes negative and significant for dyads with extremely corrupt host economies like Kazakhstan, Nigeria, and Uzbekistan. In this bin, the estimated ATT is a reduction of about 2.08 million US dollars in net FDI flows, equal to a 22.09% reduction in net FDI flows from the average. Robustness of these results is tested in Appendix H through J.

5 Concluding remarks

This article has studied the effect of multilateral corporate regulations on companies’ foreign investments. I have focused on regulations imposed by firms’ home states that prohibit bribe payments abroad under the 1997 OECD Anti-Bribery Convention. Political economy advances two opposed expectations about the effect of such regulations on FDI. I contributed to the debate by attempting to rejoin them. I argued that the two expectations are observable in host countries with different corruption levels. In moderately corrupt countries, regulated companies can leverage regulations to turn bribe requests down and secure business opportunities by other means than bribing. This favors their investment. In extremely corrupt hosts, instead, regulated companies find it harder to secure business opportunities without bribing and operate at higher costs induced by anti-bribery. Here, laws deter investment. I found empirical support of this argument at the firm- and country-dyad levels.

Limitations of the study open up various possible lines of future inquiry. My argument rests on regulated companies’ leverage to refuse bribe requests, which I claim varies in the host countries’ corruption level. I have not tested this mechanism directly although previous studies lend plausibility to it (Svensson, 2003). It might be possible that anti-bribery policies affect the behavior of public officials, too (Perlman & Sykes, 2017). The overall observed effect on investment might thus be the compounded result of these different mechanisms. Future work could disentangle the role of these regulations in affecting bribery by firms vs foreign public officials.

An important limitation concerns modes of entry in a foreign market. I did not consider other strategies than establishing ownership. Sub-contracting and forming joint ventures, yet, are potential alternatives to invest abroad which cannot be studied with the type of FDI data I used (Kerner, 2014). They can expose firms from ratifiers of the Convention to a lower risk of interaction with corrupt public officials (see Chapman et al. , 2020; Zhu & Shi, 2019). By entering a market using these alternative modes, firms might circumvent anti-bribery policies. Future work could investigate this possibility.

A final limitation concerns the time coverage of the country-level analysis: as UNCTAD data used extend only until 2006, the analysis did not consider more recent time periods when some countries under the OECD Convention reinforced their commitments to enforce anti-bribery standards—roughly since 2010 (Jensen & Malesky, 2018). An example is the UK which, in 2010, passed the Bribery Act, considered by many as an improvement over its previous anti-bribery policy. Future work could extend the time-series considered by the current study and evaluate whether more vigorous enforcement, or the adoption of more recent anti-bribery policies, have produced different or comparable effects on regulated companies’ investments.

My study on the effectiveness of the OECD Convention rests on scope conditions that limit the generalizability of the results to other anti-bribery IOs. An important condition is the role of US prosecutors in sustaining enforcement. The OECD Convention almost represents the extension of the FCPA to OECD partners. A similar outcome would have been more difficult to achieve in larger venues such as the UN Convention Against Corruption (Spahn, 2013). Due to the tight connection between provisions in the OECD Convention and the FCPA, US prosecutors can easily leverage the treaty to prosecute foreign companies for the very type of misconduct prohibited under FCPA terms. This has two effects. First, it compensates for weak levels of compliance by other parties making the US the “global policeman” of the Convention (Choi & Davis, 2014; Crippa, 2021; Tomashevskiy, 2021). Second, it stimulates other treaty members to initiate their own anti-bribery actions (Kaczmarek & Newman, 2011). Future studies could investigate more systematically differences in effectiveness for anti-corruption IOs where there is no leading state de facto in charge of enforcement.

The study shows that a multilateral approach to the diffusion of sustainable business models can facilitate companies in a range of countries where financial crime is common. These findings are good news for the possibility to conjugate corporate regulatory efforts with economic activity. Recent regulatory initiatives, like the OECD/G20 BEPS Inclusive Framework, could learn an encouraging lesson from the study. Implications also travel to areas that include human and labor rights violations, money laundering, and environmental regulation.

A caveat concerns host countries with extremely weak regulatory standards. Here, the strategy backfires. Regulated firms are more likely to abandon these economies. Although a rigorous welfare analysis goes beyond the scope of this article, this might look like a desirable outcome: if not from the perspective of firms, at least from that of extremely corrupt host economies, given that firms from OECD countries are among the main exporters of bribery (Picci, 2018). Cutting down on the supply of bribery, one could argue, is one effective way to reduce corruption in places that need it the most.

However, a reduction in the supply of bribes by regulated companies could be met by an increase in bribe-payments from unregulated competitors (Jensen & Malesky, 2018). To the extent that unregulated firms can violate business standards, bribe in the conduct of business, and remain unpunished by their home economies, bribery standards in economies with already high corruption levels might not improve—or even decline further. This pessimistic conclusion aligns with existing studies on the perverse regulatory effects of corporate policies induced by different standards among competitors (Brazys & Kotsadam, 2020; Chapman et al., 2020) and on the limited effectiveness of anti-corruption IOs (Ferry et al., 2020; Hafner-Burton & Schneider, 2019).

Data availability statement

All datasets analysed in the study and the code used are available in the replication package which can be downloaded at: https://doi.org/10.7910/DVN/JTGGLJ.

Notes

In the article, I consider exclusively foreign bribery, where the bribe payer and payee are of different nationalities.

The actors’ choices to take part in the deal are likely affected by other factors too. The firm might find it easier to turn down bribe requests if they threatened to divest and if the host country’s divestment costs were large. Viceversa, the public official might find it easier to advance bribe requests if the firm could not find comparable alternative hosts. I exclude these elements from my argument in order to focus on my key explanatory variables (home anti-bribery laws and host corruption). This choice also ensures consistency with my analysis. Ultimately, I assume that similar factors do not vary with the home country’s adoption of anti-bribery laws. For a discussion on the effect of anti-bribery regulations that accounts for some of these alternative drivers, see Perlman and Sykes (2017, 166-168).

I adopt a very narrow definition of what constitutes a more or less corrupt country. I define a country’s level of corruption solely in terms of how frequent bribe payments are in its economy.

For instance, the TSKJ joint venture—formed by Technip (French), Snamprogetti (Dutch, but owned by the Italian ENI), KBR (owned by Halliburton, US), and JGC (Japanese)—allegedly paid \( \$180 \) million in bribes between 1995 and 2004 to Nigerian government officials in order to obtain \( \$6 \) billion worth in contracts for the exclusive construction of natural gas facilities on Bonny Island. See: https://fcpaprofessor.com/jgc-of-japan-formally-joins-the-bonny-island-bribery-club/ and https://www.traceinternational.org/TraceCompendium/Detail/192?type=1. Both accessed on May 18, 2023.

For instance, financial markets impose 80% of the costs faced by a firm after an anti-bribery action (Sampath et al., 2018). However, such reputational costs need not vary with whether involved companies’ headquarters have anti-bribery laws: a firm might be exposed to reputational costs for involvement into bribery regardless of its headquarter.

Prosecuted firms usually set up monitoring systems run by third-parties for a probatory period and periodically rotate international offices to avoid managers established personal connections with local authorities. For a textbook example, see the measures implemented by Siemens AG after an infamous worldwide bribery scandal: https://www.complianceweek.com/how-siemens-worked-to-fix-a-culture-of-institutionalized-corruption/14915.article.

According to my data, highly corrupt economies include countries like Kazakhstan, Nigeria, Vietnam, or Russia.

Moderately corrupt economies in my data include Italy, Mexico, Singapore, or Taiwan.

In my data these countries include Canada, Denmark, or Sweden.

Arguably, the most notorious case involved Lockheed: https://www.washingtonpost.com/archive/business/1977/05/27/lockheed-paid-38-million-in-bribes-abroad/800c355c-ddc2-4145-b430-0ae24afd6648/.

Because a change in norms and values was crucial in determining ratification of the Convention, I claim that participation in the treaty can be considered exogenous to considerations related to firms’ international business position, at least for its first ratifiers. To back up this claim, in Appendix B, I investigate determinants of ratification of the OECD Convention. I find no evidence that country-level factors such as the level of outward FDI in more or less corrupt economies delayed or fast-tracked treaty adoption.

Original signatories were: Argentina, Australia, Austria, Belgium, Brazil, Bulgaria, Canada, Chile, Czechia, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Japan, Luxembourg, Mexico, Netherlands, New Zealand, Norway, Poland, Portugal, Slovakia, South Korea, Spain, Sweden, Switzerland, Turkey, the UK, and US.

In chronological order: Slovenia (2001), Estonia (2004), South Africa (2007), Israel (2009), Colombia and Russia (2012), Latvia (2014), Costa Rica and Lithuania (2017), and Peru (2018).

Such disproportion is reflected in my firm-level data, see Appendix C.

My own computation using replication data from Kaczmarek and Newman (2011).

In Appendix E, I show that the effect of the OECD Convention is not significant with a linear interaction with corruption.

Orbis data are provided by Bureau van Dijk (BvD), a Moody’s company that obtains information from compulsory reports that public authorities mandate. Both listed and non-listed firms must disclose information. BvD retrieves and cross-checks it from various country-specific sources.

In Appendix (Table E.2), I show that results are robust when excluding firms from countries that joined the Convention between 2006 and 2011 or from likely outliers.

Appendix C discusses selection into the sample and balance in covariates.

I depart from Beazer and Blake (2018) and impose the condition \(i \ne j\), which I deem appropriate in the case of foreign investment. Results do not change significantly when relaxing this condition.

The “ultimate parent” is defined as the firm owning more than 25% in stakes of the foreign subsidiary. Financial companies, insurance firms, hedge funds, and investment banks are excluded. Small firms have less than one million euros in operating revenues a year, total assets less than two million euros, and less than 15 employees.

Table E.3.

I discuss the measurement and its assumptions in Appendix A. The reader should keep in mind one important assumption that supports the index validity. The PACI assumes that “the probability of observing a corrupt transaction involving firms from country i [...] and public officials in country j does not depend on the identity of country j” (Escresa & Picci, 2017, 211). Thus the PACI assumes that other countries do not discriminate when enforcing anti-corruption cases based on characteristics of country j other than its level of corruption. The index uses only cases of cross-border corruption first-enforced in other countries (meaning, not in country j itself), to mitigate violations of this assumption. The authors draw on results from McLean (2012) to support the validity of a no-discrimination assumption in anti-bribery law enforcement. However, recently Tomashevskiy (2021) argued that US authorities use anti-corruption enforcement as a way to further political goals against specific states. If this were happening, the PACI would return a biased measure of corruption: its score would in part reflect the discriminatory enforcement of anti-bribery cases. Since studying the determinants of enforcement goes beyond the scope of this article, I caution the reader against this potential violation of the index validity. However, results presented in the next section hold when using traditional perception-based measures of corruption that do not assume no discriminatory enforcement. This reassures against such violation of the PACI assumption, at least in this case.

See Table E.1.

Table C.2. In the estimation procedure, I recenter the distribution of all covariates around their means to help convergence. Descriptive statistics are reported before recentering distributions of these variables.

The baseline probability of investment in these countries is 0.02.

The baseline probability of investment in these countries is 0.001.

Attempting to extend this time-series proved surprisingly difficult. At the time of writing, the UNCTAD data portal does not report bilateral FDI statistics anymore. Alternative common sources of FDI bilateral data are not appropriate to the case studied here. OECD statistics only report bilateral FDI data where origin and destinations of investments are OECD countries, thus they would only include information for treated units in the dataset. Moreover the moderator would not have enough variation. A valid alternative would be represented by the IMF Coordinated Direct Investment Survey (CDIS) data. Unfortunately, CDIS time series start only in 2009 and they measure FDI stocks, whereas the UNCTAD time-series consider FDI flows. I return on the issue of time coverage in the conclusion.

In Appendix J, I substitute my binning strategy with a traditional interaction of the treatment variable with the linear and squared measure of Host PACI, in various model specifications.

I choose the 2005 value for consistency with the firm-level analysis. The choice is appropriate given that corruption is a particularly sticky institutional characteristic with little time variation (Treisman, 2007). The relevant variation in levels of corruption most likely takes place between rather than within countries, especially in a short time window as the one of my analysis.

The choice of quintiles is purely empirical, as it guarantees enough observations in each bin. Alternatives (using tertiles and quartiles) provided consistent results, see Appendix H.

In Appendix, I show results are very similar when adopting a 2FE design (Figure I.1). This design includes all dyads, therefore ensuring results do not depend on excluding dyads without enough pre-treatment observations.

In the estimation procedure I impose a 2FE model specification. I employ time-varying covariates at the level of the host country, home country, and dyad that are also adopted in the firm-level analysis. This is done to improve the synthetic counterfactual imputation. I drop all treated dyads without at least five pre-treatment observations. This is a recommended practice to obtain reliable synthetic control units (Xu, 2017). An Expectation Maximization algorithm has been applied to obtain more precise synthetic counterfactuals. A cross-validation procedure has also been applied to estimate the best number of factor loadings between 0 and 3. Non-parametric standard errors are estimated with 1000 bootstrap iterations blocked at the dyad-level.

References

Abbott, K. W., & Snidal, D. (2000). Hard and soft law in international governance. International Organization, 54(3), 421–456.

Abbott, K. W., & Snidal, D. (2002). Values and interests: International legalization in the fight against corruption. The Journal of Legal Studies, 31(S1), S141–S177.

Abbott, K. W., & Snidal, D. (2010). International regulation without international government: Improving IO performance through orchestration. The Review of International Organizations, 5, 315–344.

Ades, A., & Di Tella, R. (1999). Rents, competition, and corruption. American Economic Review, 89(4), 982–993.

Ahlquist, J. S., & Mosley, L. (2021). Firm participation in voluntary regulatory initiatives: The accord, alliance, and US garment importers from Bangladesh. The Review of International Organizations, 16(2), 317–343.

Allee, T., & Peinhardt, C. (2011). Contingent credibility: The impact of investment treaty violations on foreign direct investment. International Organization, 65(3), 401–432.

Baradaran, S., Findley, M. G., Nielson, D., & Sharman, J. C. (2012). Does international law matter? Minnesota Law Review, 97, 743.

Barassi, M. R., & Zhou, Y. (2012). The effect of corruption on FDI: A parametric and non-parametric analysis. European Journal of Political Economy, 28(3), 302–312.

Barkema, H. G., Bell, J. H., & Pennings, J. M. (1996). Foreign entry, cultural barriers, and learning. Strategic Management Journal, 17(2), 151–166.

Beazer, Q. H., & Blake, D. J. (2018). The conditional nature of political risk: How home institutions influence the location of foreign direct investment. American Journal of Political Science, 62(2), 470–485.

Bell, A., & Jones, K. (2015). Explaining fixed effects: Random effects modeling of time-series cross-sectional and panel data. Political Science Research and Methods, 3(1), 133–153.

Betz, T., Pond, A., & Yin, W. (2021). Investment agreements and the fragmentation of firms across countries. The Review of International Organizations, 16, 755–791.

Biglaiser, G., & DeRouen, K. (2010). The effects of IMF programs on US foreign direct investment in the developing world. The Review of International Organizations, 5(1), 73–95.

Brambor, T., Clark, W. R., & Golder, M. (2006). Understanding interaction models: Improving empirical analyses. Political Analysis, 14(1), 63–82.

Brazys, S., & Kotsadam, A. (2020). Sunshine or curse? Foreign direct investment, the OECD anti-bribery convention, and individual corruption experiences in Africa. International Studies Quarterly

Brewster, R. (2017). Enforcing the FCPA: International resonance and domestic strategy. Virginia Law Review pp. 1611–1682

Busse, M., & Hefeker, C. (2007). Political risk, institutions and foreign direct investment. European Journal of Political Economy, 23(2), 397–415.

Chapman, T. L., Jensen, N. M., Malesky, E. J., & Wolford, S. (2020). Leakage in international regulatory regimes: Did the OECD anti-bribery convention increase bribery? Quarterly Journal of Political Science

Cheibub, J. A., Gandhi, J., & Vreeland, J. R. (2010). Democracy and dictatorship revisited. Public choice, 143(1–2), 67–101.

Choi, S. J., & Davis, K. E. (2014). Foreign affairs and enforcement of the foreign corrupt practices act. Journal of Empirical Legal Studies, 11(3), 409–445.

Cooley, A., & Sharman, J. C. (2017). Transnational corruption and the globalized individual. Perspectives on Politics, 15, 732–753.

Crippa, L. (2021). Global firms and global sheriffs? Why territory matters for extraterritorial enforcement of regulatory regimes. APSA Preprints

Cuervo-Cazurra, A. (2008). The effectiveness of laws against bribery abroad. Journal of International Business Studies, 39(4), 634–651.

Danzman, S. B., & Slaski, A. (2022). Incentivizing embedded investment: Evidence from patterns of foreign direct investment in Latin America. The Review of International Organizations pp. 1–25

Davis, K. E. (2011). Why does the United States regulate foreign bribery: Moralism, self-interest, or altruism. NYU Annual Survey of American Law, 67, 497.

Dunning, J. H. (1980). Toward an eclectic theory of international production: Some empirical tests. Journal of International Business Studies, 11(1), 9–31.

Egger, P., & Winner, H. (2005). Evidence on corruption as an incentive for foreign direct investment. European Journal of Political Economy, 21(4), 932–952.

Escresa, L., & Picci, L. (2017). A new cross-national measure of corruption. The World Bank Economic Review, 31(1), 196–219.

Ferry, L. L., Hafner-Burton, E. M., & Schneider, C. J. (2020). Catch me if you care: International development organizations and national corruption. The Review of International Organizations, 15, 767–792.

Findley, M. G., Nielson, D. L., & Sharman, J. C. (2015). Causes of noncompliance with international law: A field experiment on anonymous incorporation. American Journal of Political Science, 59(1), 146–161.

Garrett, B. L. (2011). Globalized corporate prosecutions. Virginia Law Review, 97, 1775.

Garrett, B. L. (2020). Declining corporate prosecutions. American Criminal Law Review, 57, 109.

Genovese, F. (2020). Market responses to global governance: International climate cooperation and Europe’s carbon trading. Business and Politics pp. 1–33

Gray, J. (2009). International organization as a seal of approval: European Union accession and investor risk. American Journal of Political Science, 53(4), 931–949.

Gueorguiev, D., & Malesky, E. (2012). Foreign investment and bribery: A firm-level analysis of corruption in Vietnam. Journal of Asian Economics, 23(2), 111–129.

Gutterman, E. (2015). Easier done than said: Transnational bribery, norm resonance, and the origins of the US foreign corrupt practices act. Foreign Policy Analysis, 11(1), 109–128.

Hafner-Burton, E. M., & Schneider, C. J. (2019). The dark side of cooperation: International organizations and member corruption. International Studies Quarterly, 63(4), 1108–1121.

Heywood, P. M. (1997). Political corruption: Problems and perspectives. Political Studies, 45(3), 417–435.

Hines, J. R. (1995). Forbidden payment: Foreign bribery and American business after 1977. Technical report National Bureau of Economic Research

Jensen, N. M. (2008). Nation-states and the multinational corporation: A political economy of foreign direct investment. Princeton University Press

Jensen, N. M., Biglaiser, G., Li, Q., Malesky, E. J., Pinto, P., & Staats, J. (2012). Politics and foreign direct investment. University of Michigan Press.

Jensen, N. M., & Malesky, E. J. (2018). Nonstate actors and compliance with international agreements: An empirical analysis of the OECD anti-bribery convention. International Organization, 72(1), 33–69.

Johns, L., & Wellhausen, R. L. (2016). Under one roof: Supply chains and the protection of foreign investment. American Political Science Review, 110(1), 31–51.

Kaczmarek, S. C., & Newman, A. L. (2011). The long arm of the law: Extraterritoriality and the national implementation of foreign bribery legislation. International Organization, 65(4), 745–770.

Kalyanpur, N., & Newman, A. L. (2019). Mobilizing market power: Jurisdictional expansion as economic statecraft. International Organization, 73(1), 1–34.

Kennard, A. (2020). The enemy of my enemy: When firms support climate change regulation. International Organization pp. 1–35

Keohane, R. O. (1984). After hegemony: Cooperation and discord in the world political economy. Princeton University Press

Kerner, A. (2014). What we talk about when we talk about foreign direct investment. International Studies Quarterly, 58(4), 804–815.

King, G., Tomz, M., & Wittenberg, J. (2000). Making the most of statistical analyses: Improving interpretation and presentation. American Journal of Political Science, 44(2), 347–361.

Knutsen, C. H., Kotsadam, A., Olsen, E. H., & Wig, T. (2017). Mining and local corruption in Africa. American Journal of Political Science, 61(2), 320–334.

Lambsdorff, J. G. (2002). Making corrupt deals: contracting in the shadow of the law. Journal of Economic Behavior & Organization, 48(3), 221–241.

Leibold, A. (2014). Extraterritorial application of the FCPA under international law. Willamette Law Review, 51, 225.

Lenz, G. S., & Sahn, A. (2021). Achieving statistical significance with control variables and without transparency. Political Analysis, 29(3), 356–369.

Linzer, D. A., & Staton, J. K. (2015). A global measure of judicial independence, 1948–2012. Journal of Law and Courts, 3(2), 223–256.

Malesky, E. J., Gueorguiev, D. D., & Jensen, N. M. (2015). Monopoly money: Foreign investment and bribery in Vietnam, a survey experiment. American Journal of Political Science, 59(2), 419–439.

McLean, N. (2012). Cross-national patterns in FCPA enforcement. Yale Law Journal,121(7)

Morse, J. C. (2019). Blacklists, market enforcement, and the global regime to combat terrorist financing. International Organization, 73(3), 511–545.

Neumayer, E., & Spess, L. (2005). Do bilateral investment treaties increase foreign direct investment to developing countries? World Development, 33(10), 1567–1585.

O’Brien, J., & Folta, T. (2009). Sunk costs, uncertainty and market exit: A real options perspective. Industrial and Corporate Change, 18(5), 807–833.

OECD. (2018). Fighting the crime of foreign bribery. The anti-bribery convention and the OECD working group on bribery. Technical report Organization for the Economic Cooperation and Development.

Olken, B. A. (2009). Corruption perceptions vs. corruption reality. Journal of Public Economics, 93(7–8), 950–964.

Pandya, S. S. (2016). Political economy of foreign direct investment: Globalized production in the twenty-first century. Annual Review of Political Science, 19, 455–475.

Perlman, R. L., & Sykes, A. O. (2017). The political economy of the foreign corrupt practices act: An exploratory analysis. Journal of Legal Analysis, 9(2), 153–182.

Picci, L. (2018). The supply-side of international corruption: A new measure and a critique. European Journal on Criminal Policy and Research, 24(3), 289–313.

Pinto, P. M., & Zhu, B. (2016). Fortune or evil? The effect of inward foreign direct investment on corruption. International Studies Quarterly, 60(4), 693–705.

Pond, A. (2018). Protecting property: The politics of redistribution, expropriation, and market openness. Economics & Politics, 30(2), 181–210.

Putnam, T. L. (2009). Courts without borders: Domestic sources of US extraterritoriality in the regulatory sphere. International Organization, 63(3), 459–490.

Rose-Ackerman, S. (1975). The economics of corruption. Journal of Public Economics, 4(2), 187–203.

Sampath, V. S., Gardberg, N. A., & Rahman, N. (2018). Corporate reputation’s invisible hand: Bribery, rational choice, and market penalties. Journal of Business Ethics, 151(3), 743–760.

Sharman, J. C. (2011). The money laundry: Regulating criminal finance in the global economy. Cornell University Press

Skovgaard Poulsen, L. N. (2014). Bounded rationality and the diffusion of modern investment treaties. International Studies Quarterly, 58(1), 1–14.

Spahn, E. K. (2012). Multijurisdictional bribery law enforcement: The OECD anti-bribery convention. Virginia Journal of International Law, 53, 1.

Spahn, E. K. (2013). Implementing global anti-bribery norms: from the Foreign corrupt practices act to the OECD anti-bribery convention to the UN convention against corruption. Indiana International & Comparative Law Review, 23, 1.

Svensson, J. (2003). Who must pay bribes and how much? Evidence from a cross section of firms. The Quarterly Journal of Economics, 118(1), 207–230.

Tarullo, D. K. (2004). The limits of institutional design: Implementing the OECD anti-bribery convention. Virginia Journal of International Law, 44(3), 665–710.

Thrall, C. (2021). Public-private governance initiatives and corporate responses to stakeholder complaints. International Organization, 75(3), 803–836.

Tobin, J. L., & Rose-Ackerman, S. (2011). When BITs have some bite: The political-economic environment for bilateral investment treaties. The Review of International Organizations, 6(1), 1–32.

Tomashevskiy, A. (2021). Economic statecraft by other means: The use and abuse of anti-bribery prosecution. International Studies Quarterly, 65(2), 387–400.

Treisman, D. (2007). What have we learned about the causes of corruption from ten years of cross-national empirical research? Annual Review of Political Science, 10, 211–244.

Xu, Y. (2017). Generalized synthetic control method: Causal inference with interactive fixed effects models. Political Analysis, 25(1), 57–76.

Zhu, B. (2017). MNCs, rents, and corruption: Evidence from China. American Journal of Political Science, 61(1), 84–99.

Zhu, B., & Shi, W. (2019). Greasing the wheels of commerce? corruption and foreign investment. The Journal of Politics, 81(4), 1311–1327.