Abstract

Because of global lock-downs caused by the unexpected COVID-19, the interactions between emission trading and related markets have changed significantly compared to the pre-COVID-19 period. Considering the pandemic effect, this paper established an integrated system to identify the relationship trajectories between carbon trading market and impact factors. A noise-assisted multivariate empirical mode decomposition (N-A MEMD) method was utilized to simultaneously decompose the original multi-dimensional time series into intrinsic mode functions (IMFs), after which the Lempel-Ziv (LZ) complexity algorithm was applied to reconstruct the IMFs into high-frequency (HF), low-frequency (LF), and trend modules. Vector autoregression (VAR) and vector error correction (VEC) models were then used to systematically simulate the correlations. The time span was split into pre-COVID-19 and post-COVID-19 periods for comparison, and the mobility trends data during the outbreak period released by the Apple company was chosen to reflect the pandemic effects. The empirical analysis results revealed the energy prices, macroeconomic index, and exchange rate are the main external impact factors of carbon price in the short term. Summarizing from the cointegration models over the long term, the market stability reserve (MSR) mechanism was found to have ability on stabilizing the carbon price under the epidemic shock. Furthermore, the COVID-19 was found to complicate the relationships between carbon price and influence factors, which resulted in fluctuating markets.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The worldwide infectious COVID-19 pandemic has significantly affected the global economy around the since late 2019 (Wang and Zhang 2021). The International Energy Agency reported that in 2020, primary energy demand had dropped nearly 4% and global energy-related CO2 emissions had fallen by 5.8%.Footnote 1 These impacts have spread to the emissions trading system (ETS) and relative energy markets (Mintz-Woo et al. 2021). Under the effects of epidemic, the evolutionary of relationship directions between the ETS and potential drivers remains unclear.

To date, many studies have focused on the COVID-19 pandemic effects on global and national economies, such as impacts on air pollution levels and economic loss (Dutheil et al. 2021; Rasheed et al. 2021). In particular, the carbon price has also been heavily affected by COVID-19 (Dong et al. 2020). Although some studies have discussed the pandemic effects on carbon prices, most have only considered a single relationship between the carbon price and a particular commodity market (Tiwari et al. 2021). However, carbon trading market has complicated relationships with many factors, such as energy consumption, macroeconomic status, and the pandemic. Also, correlationships between carbon price and influence factors may be different in short and long terms. To describe these complicated relations, this paper considers a more comprehensive carbon price analysis system in short and long terms that encompasses key related factors including energy markets, macroeconomic indexes, exchange rate, and mobility trends in the epidemic period. The effect of inner market mechanism in the carbon trading market is also discussed.

Contributions of this paper include three distinct aspects. First, differing with existing one-dimensional decomposed method (Yang et al. 2020), the noise-assisted multivariate empirical mode decomposition (N-A MEMD) is introduced into the carbon price analysis, which can simultaneously decompose the multivariate time series and facilitate the further analysis. Second, the pandemic impacts on carbon price fluctuation are verified through the comparison between pre-COVID-19 and post-COVID-19 periods. Unlike qualitative analysis of the epidemic (Bagchi et al. 2020), the mobility trends data are utilized as a meaningful and high relevant indicator to quantitatively measure the pandemic effects. Third, this paper reveals the dominant position of the market stability reserve (MSR) mechanism in European Union emissions trading system (EU ETS) on maintaining carbon price stability. Comparing with previous literature that equally treated all impact factors in different decomposed modules (Zhu et al. 2018), the common determinants are found to be mainly effective in the short term.

The remainder of this paper is organized as follows. “Literature review” introduces the potential determinants and effective models; research gaps are also provided in this section. “Methodology” describes the methods designed and proposed in this paper. “Data description” details the statistical characteristics of the variables. “Empirical analysis and results” discusses the characteristics of HF, LF, and trend modules. “Discussion” summarizes the empirical analysis and results, and “Conclusions” concludes this study.

Literature review

Identifying the potential determinants is the first important topic for the relationships analysis of carbon trading market and related factors. As energy consumption is one of the major sources of carbon emissions, energy prices for crude oil, natural gas, and coal have generally been included when assessing carbon price (Zhao et al. 2018). As for the crude oil, some researchers held the point that a higher crude oil price can stimulate households and industries to seek cleaner, cheaper alternative energy sources, such as natural gas (Ullah et al. 2020). These alternatives may improve environmental quality and reduce carbon emissions, which means lower carbon price. However, other researchers had results that a rise in the crude oil price can lead to a stable increase in the carbon price (Tan and Wang 2017). Coal has also been found to have a strong price effect on the European Union allowance (EUA) (Anke et al. 2020).

Except for the energy consumption effects, the influences of macroeconomic indicators, such as the Goldman Sachs Commodity Index (GSCI) and STOXX Europe 600 index (STOXX), are also important to emission trading market (Zhou and Li 2019). High index levels indicate a booming economy, which means a high carbon allowance demand. Carbon prices are also susceptible to exchange rate fluctuations (Sun and Wang 2020). Except for the influences on carbon price, there are also correlationships between impact factors. For example, the coal and the natural gas are substitutes for each other (Aatola et al. 2013), the oil price has strong significant links with STOXX Europe 600 index (Arouri 2011).

Based on previous related studies, this paper selected energy prices, macroeconomic indexes, and the exchange rate as common determinants of the carbon price. Further, impacts of the COVID-19 pandemic are also considered in this paper. Although the epidemic has resulted in substantial reductions in economic activities (Khurshid and Khan 2021), the decline of carbon allowance demand will not last for a long time as the 2020 oil price dive may result in a higher carbon emission so that rising carbon price (Jefferson 2020; Malliet et al. 2013). Pandemic effects on the carbon price and its potential drivers are also difficult to be quantitatively measured (Wang et al. 2020). This paper extends the research with considering the pandemic factors when analyzing the linkages between carbon trading market and influence factors. The mobility trends data, which represent the social and economic status in the COVID-19 period (Djilali et al. 2020), are considered one of the possible carbon price determinants. In addition, the economic recovery in the post-epidemic period may have positive effects on mobility as the traffic and transport reflect the economic activity (Bernardino et al. 2015).

Although the potential drivers of carbon price are determined based on existing researches, direct analysis on these series may cause spurious regression because of their high nonlinearity and nonstationarity (Marmer 2008). Fortunately, data decomposition methods such as the wavelet transform and the empirical mode decomposition (EMD) have been utilized to solve this problem (Liu and Shen 2019). Of these methods, EMD and its extensions have been popular because of their ability on solving nonstationarity and nonlinearity problems (Huang et al. 1998). As this paper seeks to analyze multi-dimensional time series, the multivariate empirical mode decomposition (MEMD) proposed by Rehman and Mandic (2010) is deemed more appropriate. Furthermore, as the MEMD has a similar mode mixing problem to the EMD, this paper introduces the N-A MEMD to decompose the multi-dimensional series.

After choosing the suitable data decomposition method for multi-dimensional time series analysis, the cross-correlations between variables are needed to be simulated. Many statistical methods have been developed to analyze this problem. For example, the asymmetric effects of oil price changes on environmental pollution have been simulated by using a nonlinear autoregressive distributed lag (ARDL) model (Ullah et al. 2020). These methods have also been used on carbon price; for example, vector autoregression (VAR) and vector error correction (VEC) models have been utilized to explore relationships and fluctuation characteristics of emission trading market and related stock markets (Zhu et al. 2019; Zhou and Li 2019). Considering the non-structural advantages of VAR and VEC models, this paper also selects them to analyze the complicated cross relationships between carbon price and drivers.

Despite there were many methods have been utilized in analyzing carbon price and its determinants, previous researches have tended to analyze these relationships without considering the short-term and long-term differences (Ji et al. 2021); however, the short-term changes are reflected in immediate fluctuations whereas long-term relationships tend to show greater cointegration (Zhu et al. 2018). Furthermore, the statistic model selections were distinctive for short and long terms, which distinguishes this paper from previous research. The evolution relationships in trend modules were determined through comparison. After referencing previous literature, the theoretical framework of this research can be summarized in Fig. 1, including variables selections, cross-relationships analysis, and methodology establishing.

Theoretical framework

Methodology

Original multiple time series of carbon price and associated drivers are difficult to analyze because of their non-stationary and nonlinear characteristics. Further, relationships between the carbon price and its associated factors have been significantly influenced by the COVID-19. The erratic commodity markets and macroeconomic fluctuations have weakened the performance of traditional econometrics models. To alleviate these weaknesses and reveal the causal relationships evolution between the carbon price and impact factors, the multi-scale analysis framework is designed based on the N-A MEMD algorithm and VAR-VEC models as shown in Fig. 2.

Framework for the N-A MEMD VAR-VEC system

First step in the analysis framework is collecting original multi-dimensional series that incorporate the carbon price and former discussed potential drivers. The multivariate time series are initially decomposed into intrinsic mode functions (IMFs) of different frequencies and a residual through the N-A MEMD, which makes series become more stationary and periodic. The Lempel-Ziv (LZ) complexity algorithm proposed by Lempel and Ziv (1976) is utilized to reconstruct the IMFs into high-frequency (HF) and low-frequency (LF) modules, which respectively identify the short- and long-term physical characteristics (Zhang et al. 2008). After testing the unit root existence of HF and LF modules, VAR and VEC models are respectively applied to the stationary and non-stationary series, with the trend module being assessed from the chart analysis. The impulse response function (IRF) is used to explore the reactions in response to endogenous variable shocks in the VAR. As the variance decomposition (VD) captures the response intensity of endogenous variables when there are component shocks, the relative importance of each random fluctuation effect on variables is accordingly determined.

Data decomposition

The MEMD was proposed to extend the EMD to allow for the processing of multichannel signals. Therefore, comparing with the EMD, the MEMD can simultaneously decompose multivariate input signals into corresponding same number IMFs of different frequencies, which allows for direct multichannel modeling. However, the MEMD still has similar disadvantages to the EMD, such as the mode mixing problem. Fortunately, a further extension to the MEMD, the N-A MEMD, has been proposed to resolve this problem.

Multivariate EMD extension

One important step in the MEMD is to calculate the multivariate signal envelopes and local means. To this end, Rehman and Mandic (2010) generated multiple real-valued projections of the signal so that the extrema of these projected signals can be interpolated to yield the desired multi-dimensional envelopes, and the local means were then determined by averaging the envelope curves. In Euclidean coordinate system, the direction vectors in n-dimensional spaces can be represented by points on corresponding unit (n − 1) spheres. Therefore, the determination of suitable direction vectors was treated by finding a uniform sampling scheme on the hypersphere. A sequence of n-dimensional vectors \({\mathbf {v}}(t) = \left ({{v_{1}}(t),{v_{2}}(t), {\ldots } ,{v_{n}}(t)} \right ),t = 1,2,...T\) were assumed to be the MEMD input. The MEMD is detailed in the following.

-

Step 1:

Generate the points set based on the low-discrepancy Hammersley sequence for sampling on an (n − 1) sphere. Assuming \({{\mathbf {\theta }}_{k}} = \left [ {{\theta _{1}^{k}},{\theta _{2}^{k}}, {\ldots } ,\theta _{(n - 1)}^{k}} \right ] \) to be the direction angles on an (n-1) sphere, with \({{\mathbf {D}}^{{\theta _{k}}}} = \left \{ {{d_{1}^{k}},{d_{2}^{k}}, {\ldots } ,{d_{n}^{k}}} \right \}, k=1,2,...,K\) denoting k th set of corresponding direction vectors. K is the number of direction vectors sets. Details of direction vectors determination on a hypersphere can be found in relative mathematical researches (Niederreiter1992).

-

Step 2:

Calculate a projection \({\lambda ^{{\theta _{k}}}}(t)\) along the k th direction vector set \({{\mathbf {D}}^{{\theta _{k}}}}\) for the input signal v(t). For all k, \({{\Lambda }^{{\theta _{k}}}}(t) = \{ {\lambda ^{{\theta _{1}}}}(t),{\lambda ^{{\theta _{2}}}}(t),...,{\lambda ^{{\theta _{K}}}}(t)\} \) is the whole set of projections.

-

Step 3:

Find the time instants set \(\left \{ {t_{l}^{{\theta _{k}}}} \right \}\), which corresponds to the maxima of projected signals set \({{\Lambda }^{{\theta _{k}}}}(t)\).

-

Step 4:

The multivariate envelop curves set \({{\mathbf {\Omega }}^{{\theta _{k}}}}(t)\) is obtained by interpolating \([t_{l}^{{\theta _{k}}},{\mathbf {v}}(t_{l}^{{\theta _{k}}})]\).

-

Step 5:

Average the multivariate envelop curves for K direction vectors sets to get the vector m(t),

$$ {\mathbf{m}}(t) = \frac{1}{K}\sum\limits_{k = 1}^{K} {{{\mathbf{\Omega }}^{{\theta_{k}}}}(t)}. $$(1) -

Step 6:

Similar to the EMD method, sift the m(t) repeatedly from the original input vectors v(t) until the r(t) satisfies the multivariate IMF criteria. Then, apply r(t) to IMF.

$$ {\mathbf{v}}(t) - {\mathbf{m}}(t) = {\mathbf{r}}(t). $$(2) -

Step 7:

When the stopping criteria is satisfied, all IMFs extracted from the original signals are determined. The residual is calculated by subtracting all IMFs from v(t).

Noise-assisted MEMD

By adding Gaussian noise into the MEMD, the N-A MEMD was proposed by Rehman and Mandic (2011). The principle of the N-A MEMD is detailed in this section.

-

Step 1:

Create the uncorrelated Gaussian white noise time series with w channels and the same length with the input vectors v(t).

-

Step 2:

Integrate the white noise (w-dimensions) with the input signals v(t) (n-dimensions) to establish new composite signals ((n + w)-dimensions) before the decomposition. The composite input signal vectors are (v(t),noise(t)) = (v1(t),v2(t),…,vn(t),noise1(t),noise2(t),…, noisew(t)).

-

Step 3:

Decompose the (n + w)-dimensional signals using the MEMD algorithm listed above to determine the multivariate IMFs. The input signals are projected on an (n + w − 1)-sphere and the multivariate envelop mean vector \({\mathbf {m}}^{\prime }(t)\) is then determined. The sifting process for the N-A MEMD is,

$$ ({\mathbf{v}}(t),{\mathbf{noise}}(t)) - {\mathbf{m}}^{\prime}(t) = {\mathbf{r}}^{\prime}(t). $$(3)If \({\mathbf {r}}^{\prime }(t)\) satisfies the IMF conditions, apply the (n + w)-dimensional \({\mathbf {r}}^{\prime }(t)\) to the IMF.

-

Step 4:

Discard the w channels noise related IMFs from the resulting (n + w)-dimensional IMFs. The extracted n-variate IMFs correspond to the original signal.

Module reconstitution based on LZ complexity

Based on Kolmogorov theory, the complexity definition is the minimum binary code length for a string (Kolmogorov1968). The LZ complexity algorithm measures the complexity of the symbol sequences, which means the time series need to be transformed into characters first. Each IMF is binarized into a 0-1 character string, where 1 indicates the value is larger than 0, and 0 indicates the value is less than 0. The algorithm for calculating the LZ complexity is as follows,

-

Step 1:

The input of LZ complexity is the one-dimensional 0-1-character string. Scan the 0-1 string from left to right, with the LZ complexity increasing by 1 whenever a new sub-string appears. In this way, the output c(T), which is the LZ complexity value of each 0-1 string in T periods, is determined. Details of the LZ complexity algorithm can be found in the research of Zozor et al. (2005). To reduce the impact of the sequence length, the normalized complexity lz is shown in the following, where T is the time span for each transformed IMF series.

$$ lz = c(T)/(T/{\log_{2}}T). $$(4) -

Step 2:

Based on the physical significance of the LZ complexity, the higher the complexity, the more complicated the time series, and the lower the complexity, the more periodic the time series. Similar to Zhu et al. (2018), this paper sets γ0 as the critical value. The former Q IMFs are selected as the HF module components, with the remaining IMFs forming the LF module. The minimal value for Q is determined from the following conditions.

$$ \sum\limits_{q = 1}^{Q} {l{z_{q}} \ge } {\gamma_{0}}. $$(5) -

Step 3:

After integrating the former Q IMFs as the HF module and remaining IMFs as the LF module, the residue is identified as the trend module.

VAR-VEC models

Based on the statistical data characteristics, the VAR estimates each endogenous variable in the system as a function of all lagged endogenous variables (Hamilton 1994). This unstructured model analyzes the relationships between the multivariate variables. The VAR model is shown in Eq. (6).

where yt is the f -dimensional vectors for endogenous variables assumed at period t, which are extracted from the n-dimensional original variables based on the economic senses of candidate variables. Dynamics of yt are presumed to be governed by a p th-order Gaussian vector autoregression. xt is the d-dimensional vector for the exogenous variables divided from the n-dimensional original variables, and T is the sample period. The (f × f) vector Φi and the (f × d) vector H are respectively the coefficient matrices for the endogenous and exogenous variables, and εt represents the f -dimensional residuals, which are serially and mutually independent.

Although the VAR model is one of the most classic multivariate methods for economic analysis and forecasting, it demands stationarity, which is rarely possible in the real world. To resolve this problem, the VAR model has been combined with cointegration constraints to be extended as the VEC model (Johansen1995). Johansen and Juselius (1990) assumed there was a long-run equilibrium relationship between the non-stationary variables. The VEC model combines the cointegration concept in the autoregressive model framework with the Gaussian errors. After testing the significance of the cointegration relationships between the variables using the Johansen-Juselius method, there may be e possible stationary linear combinations, that is, there are e cointegration vectors. The VEC model is shown in Eq. (7). The lag and the subscript t − 1 for the corresponding VEC models are respectively p − 1 and t − 1 because of the difference process.

Δ is the first-order difference process, which is also called the I(1) process. Γi are the (f × f) coefficients matrices for the first-order differences of endogenous variables Δyt−i. H, xt and εt are the same as in the VAR model. The (f × f) coefficients matrices π contain information about the long-run relationships between variables, which are decomposed into the product of two (f × e) matrices A and B, with the first being the deviating variables adjustment speed, which adjusts variables back to the long-term equilibrium state, the second being stationary linear cointegration relationships between variables, and ectt− 1 is an error correction vector in the VEC model.

The determination of endogenous and exogenous variables is based on their economic meaning, while the exogenous variables are determined outside the model and are imposed on the model, and the exogenous variables are determined by the model (Chiang 1984; Mankiw 2000). Based on the correlationships analysis of variables in “Literature review”, there are substitution patterns between energy variables, close links between macroeconomic indexes and energy prices, and the economic situation may affect the transportation mobility. Therefore, this paper treats all variables as endogenous in VAR and VEC models.

Data description

The definition and statistical characteristics of variables are shown in Table 1. All variables were transformed using a logarithmic process without changing their function characteristics. This paper chose the DEC21 contract settlement price for the EUA futures to represent the carbon price, with the trading period being from January 21, 2019, to March 26, 2021, in the Intercontinental Exchange (ICE) website (https://www.theice.com), which includes the pre- and post-COVID-19 periods. The split time criterion was based on the availability of Apple mobility trends data. The energy futures series, the economic indexes, and the Apple mobility trends data were extracted from related financial sites, stock exchanges, and company reports, which are detailed in the data availability statement.

Brent crude oil, which is the benchmark for European oil prices, was extracted from the ICE Futures Europe. The Rotterdam coal futures in the Netherlands was selected to represent the coal market, which was also derived from ICE. Because of the global impacts of US natural gas (Arora and CaiArora and Cai), the natural gas futures contract was acquired from the Energy Information Administration (EIA). The GSCI and the STOXX indexes were selected to reflect the regional macroeconomic development levels (Keppler and Mansanet-Bataller 2010; Lutz et al. 2013). The exchange rate EURUSD was also chosen as it has a direct influence on production decisions and investment preferences.

Mobility trends can be measured quantitatively because of the widespread availability of personal mobile devices. Apple company has released a mobility report in the COVID-19 period on driving, walking, and transit mobility data, which indicated the social and economic influences of the pandemic (Apple 2020). Following Ou et al. (2020), the Apple mobility trends data, which were determined based on the baseline day change rate, were selected for the analysis. Because of the transit trend data dearth, only the driving and walking trends data in the report were selected. These mobility trends were set as the EU country median except for Cyprus and Malta, which were not included in the report. The Croatian mobility trends were eliminated according to the interquartile range (IQR) criteria. The median value changes in the mobility trends data were taken to imply the economic and human activity fluctuations in the EU region (Ou et al. 2020).

Variable statistical characteristics in Table 1 were examined in both pre- and post-COVID-19 periods. It can be seen from the mean value that except for oil, the carbon price, energy prices, economic indexes, and exchange rate have decreased slightly. The rapidly falling oil price significantly brought down the minimal and the average oil price. Although there were no great changes in the average, the max-min value span was relatively wide, especially for the carbon price. The standard deviation (Std Dev) values of variables also had higher dispersion degrees in the post-COVID-19 period. These statistical characteristics results indicated that there had been a significant pandemic effect on markets volatility.

Empirical analysis and results

The empirical analysis was conducted using data preprocessing and regression modeling for both pre- and post-pandemic periods, for which Matlab and Eviews were used for the calculations.

Data preprocessing results

The multivariate time series in two periods were both decomposed into eight IMFs and a residual from high frequency to low frequency. As the economic relationships in the initial multi-dimensional IMFs were difficult to explain, this paper reconstructed IMFs into HF and LF modules using LZ complexity, which can represent the short- and long-term volatility respectively (Mensi et al. 2017). The LZ complexity value of each IMF can be found in section 1 in Supplementary Information (SI). The criteria value for γ0 was set at 0.8. The HF module was combined using IMF1-IMF5 and the LF module was combined using IMF6-IMF8, which are depicted in Figs. 3 and 4. The trend modules are discussed later in this paper. The x axis in Figs. 3 and 4 shows the time span, and the y axis shows the decomposed logarithmic series values. For clearer depictions, the variables were split into two line-charts both for HF and LF modules.

Reconstructed series in the pre-COVID-19 period. (a) HF module in the pre-COVID-19 period. (b) LF module in the pre-COVID-19 period

Reconstructed series for the post-COVID-19 period. (a) HF module of common determinants in the post-COVID-19 period. (b) LF module of common determinants in the post-COVID-19 period. (c) HF module of mobility trends in the post-COVID-19 period. (d) LF module of mobility trends in the post-COVID-19 period

Comparisons between HF and LF modules in Figs. 3 and 4 show that the fluctuations in HF modules are higher, and LF modules are more stationary in both periods. Because of the wide range of mobility trends, the HF and LF modules for the LAD and LAW are independently depicted for convenience. Combining the high levels of retail and recreation trends collected in Google’s mobility trend report, which is a similar mobility trend report released by Google company (Google 2020), the rapid rise in Fig. 4c in February 2020 could be the result of festivals and vocations, with the falls in March 2020 and December 2020 in Fig. 4c might be the results of serious pandemic cases and death situations (Johns Hopkins University2021).

The Phillips-Perron (PP) test, which null hypothesis is having a unit root, was used to determine the existence of unit roots, with the Bartlett kernel spectral estimation method and the Newey-West bandwidth being selected in this test. The existence of variable constants or trends was determined based on the Akaike info criterion (AIC), the Schwarz criterion (SC) and the Hannan-Quinn criterion (HQC). Detailed unit root test results for each variable in the two periods are given in section 2 in SI. In both the pre- and post-COVID-19 periods, the HF modules for all variables rejected the null hypothesis at a 1% significance, which indicated that the HF modules were unequivocally stationary. The LF modules analysis showed that the LCP had no unit root in the pre-COVID-19 period; however, while the other variables in this period were not stationary at all, the first-order difference for each variable was stationary, which meant they were I(1). Similarly, the LF modules in the post-COVID-19 were also I(1). The unit root test results supported the different HF and LF model utilization. As this paper mainly focuses on carbon price determinants, the following results report the impact of the other endogenous variables on the carbon price.

Calculation on HF modules

From the unit root test results, the VAR model was selected for HF modules. Five criteria were selected to determine the optimal number of lags in the VAR estimations; the likelihood ratio (LR) test, the final prediction error (FPE), AIC, SC, and HQC. The optimal lags for HF modules in pre-COVID-19 and post-COVID-19 periods were both 1, with the estimation results shown in section 3 in SI. Each equation in the VAR model was estimated separately using ordinary least squares (OLS). The VAR models satisfy the stability conditions and have no characteristic polynomial roots. From the comparison of estimation results in two periods, there were obvious short-term fluctuation relationships differences between the carbon price and factors. More visible coefficient changes are shown in Fig. 5.

Parameters of carbon price endogenous variables

The columns in Fig. 5 show the elastic coefficient values for the lagged variables. Except for the self-correlation, effects of drivers were differently affected by the outbreak of COVID-19, especially the exchange rate LEU, with its effect varying from positive to negative. Other striking variations were the oil coefficients, which were more obvious in the post-COVID-19 period. In general, the coal, natural gas, exchange rate, and STOXX effects on the carbon price were weakened and the GSCI and oil effects were strengthened by the pandemic.

Granger causality test results, which verified the causal relationships between variables, are given in section 4 in SI. The dynamic variable behaviors in the short term became more complex because of COVID-19. The exchange rate and natural gas were found to be the Granger reasons for the carbon price in the pre-COVID-19 period, while the exchange rate, GSCI, oil price, and STOXX were the Granger reasons of carbon price in the post-COVID-19 period. The Apple mobility trends were shown to have direct effects on the exchange rate and indirect effects on the carbon price.

After combining the Granger causality relationships, the IRF of carbon price to endogenous variables was estimated. The aim of IRF was to analyze the effects of imposing a one-time shock on the disturbance term on the current and future values for the response variable. The Cholesky decomposition method was used to solve the orthogonalization IRF process. Figure 6 shows the responses and confidence intervals for the carbon price to endogenous variables, where the y axis shows the response and the x axis shows the lag period. The lag period was set at 50 to show the fluctuation process. There was a positive carbon price response to the exchange rate in the pre-COVID-19 period (Fig. 6a) and a negative response in the post-COVID-19 period (Fig. 6b). Oil was found to have almost no impulse effect on the carbon price in the pre-COVID-19 period according to the non-causal relationship between oil and carbon price. However, the oil effect obviously enhanced in the post-COVID-19 period (Fig. 6b). Also, the carbon price response to the natural gas was eliminated and the GSCI and STOXX effects were strengthened in the post-COVID-19 period.

IRF results. (a) IRF of HF in pre-COVID-19 period. (b) IRF of HF in post-COVID-19 period

The Cholesky decomposition method was also utilized in the VD factorization process. Figure 7 strengthens the Granger causality test and IRF results, where the y axis was the contribution rate and the x axis was the lag period, with the lag period set at 15 to depict the variance decomposition process. The carbon price was mainly self-impacted because of the autocorrelation characteristics based on the high degree of self-explanation. However, the explanation rate decreased from almost 80% in the pre-COVID-19 in Fig. 7a to 70% in the post-COVID-19 period in Fig. 7b. The explanation ability of the exchange rate on the error variance in the carbon price had no obvious differences, which changed from 11 to 9% as shown in Fig. 7a and b. In Fig. 7b, the STOXX explained nearly 8% of the error variance, which was only second to the exchange rate. Both the driving mobility and oil in Fig. 7b explained about 4% of the error variance respectively when focused on the carbon price.

VD results. (a) Pre-COVID-19 VD for the HF module. (b) Post-COVID-19 VD for the HF module

Calculation on the LF modules

The I(1) processes of LF modules were stationary, which supported the utilization of the VEC model. After determining the optimal lags based on the five criteria above, a VEC model for each period was established. The VEC model is an extension of the VAR model considering the long-term cointegration relationships; therefore, it is consistent with the physical characteristics of the LF module. The number of cointegration relationships determined by the Johansen-Juselius (JJ) test, which is a classical method for testing the cointegration relationships between multi-variables, were detailed in section 5 in SI. The principle of the JJ test is to transfer the cointegration tests on the original series yt into determining the number of non-zero eigenvalues for the π in Eq. (7). A trace test was utilized to ascertain the number of non-zero eigenvalues. Because of the zero mean characteristics of the IMF modules, the no intercept or trend condition was selected as the deterministic trend specification for the cointegration equations.

The JJ test indicated that there were respectively five and eight cointegration equations in the error correction term in the pre- and post-COVID-19 periods. As this paper mainly focused on the carbon price fluctuation, the long-term cointegration relationships for the carbon price in the two periods were as follows:

was the long-term relationship in the pre-COVID-19 period, with the cointegration equation in the post-COVID-19 period being:

where the prefixes a − and p − were the indicators for pre- and post-COVID-19 periods. aect2t and pect4t were the linear combinations of variables in each period, which were the residual terms for cointegration equations and the error correction terms in VEC models. The subscripts 2 and 4 for aect2t and pect4t corresponded to the carbon price Cholesky order in the two periods. The cointegration equations results were calculated using Eviews, which has default normalization expressions for all cointegration relations. However, as these expressions did not directly explain the cointegration relationships, restrictions were imposed on the cointegrating vectors to determine the non-normalized cointegration vectors. Equations (8) and (9) are the restricted carbon price cointegration equations in two periods, and the VEC model of carbon price is shown in “Discussion” in SI. The Gaussian-Jordan elimination method verified the feasibility of these restrictions.

From Eqs. (8) and (9), the long-run cointegration relationships in two periods were beyond expectations. In the pre-COVID-19 period, there were negative and positive effects of coal and oil respectively. As for the natural gas, this model had different results with existing researches, which the coefficient of natural gas was negative but existing researches have commonly considered the substitutional role of natural gas with coal may lead to positive effect (Zhu et al. 2019). In post-COVID-19 period, all variables had positive effects on the carbon price according to Eq. (9). Although some unusual calculation results were counter to the logical relationships, the effects of these variables were weak. Because of the logarithmic nature of the model, the estimated coefficients in the cointegration equations could be perceived to be long-run elasticity coefficients. For example, when the natural gas price increased by 1%, the carbon price only decreased 0.01% in the pre-COVID-19 period and only increased 0.0339% in the post-COVID-19 period.

These unusual calculation results for the post-COVID-19 period indicated the eruption of epidemic had changed the relationships between EU ETS and other stock markets. Shocks at the beginning of the post-COVID-19 period and the increasing trends in the latter recovery period caused positive correlationships between carbon price and drivers. In another hand, the decrease of carbon price was limited, unlike previous continuous rapid declines in the financial crisis period in 2008 and European debt crisis in 2011 (Zhu et al. 2015). This may be caused by the EU ETS MSR mechanism; as the aim of MSR is addressing the surplus of allowances and improving the system’s resilience to major shocks (Bruninx et al. 2020). In addition, the LF module cointegration equation calculation results indicated that the external markets had less effects on the ETS over the long term, and the autoregression characteristic of carbon price was more powerful in this term. To verify the strong autoregression of carbon price, the VD results for the VEC models over the long term are shown in Table 2. The VD results indicated the carbon price had almost 90% contribution when there was a shock on the system in the pre-COVID-19 period, and over 80% contribution in the post-COVID-19 period, which strengthened the supposition about MSR. Compared with the HF VD results in Fig. 7, the carbon price explanation increased by about 10% in both periods.

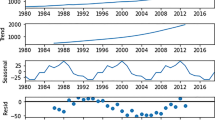

Trend module comparisons

After the decomposition process, the residual modules became more stationary and the time series trends became more legible as shown in Fig. 8, in which the left parts of the vertical dashed line indicate the trends before the pandemic and the right parts indicate the trends after the pandemic.

Trend modules. (a) LAD, LAW, LC, LCP and LO trends. (b) LEU trend. (c) LNG trend. (d) LGSCI and LSTOXX trends

The downward trends of variables in the pre-COVID-19 period were reversed in the post-COVID-19 period. As for the exchange rate, there was no sudden slump when epidemic erupted and had continual growth in the post-COVID-19 period. Some rebounds, such as coal and GSCI, almost reached the previous levels, and some, such as the carbon price, the exchange rate and the natural gas, even surpassed their previous peak values. The trends in Fig. 8 verified the LF module analytical results. The recovery in post-COVID-19 period caused positive relationships between carbon price and impact factors.

Discussion

The objective of this paper is to determine the relationships evolution between the carbon price and impact factors before and after the COVID-19 pandemic. Three aspects including the pandemic impacts, the determinants evolution in multi-scale, and the inner mechanism of ETS are concluded from the calculation results.

Related studies have investigated the effects of the COVID-19 pandemic and quarantine measures on energy consumption and economies. For example, via a qualitative analysis, Mintz-Woo et al. (2021) and Khurshid and Khan(2021) found that the falling energy prices (e.g., oil) resulting from COVID-19 facilitated the carbon price mechanism because of the less harm for producers and more diversified government revenue. In this paper, the oil impact was found to become more evident in the post-pandemic period based on the higher impulse effect and VD magnitude (Figs. 6 and 7) and the higher coefficient (Eq. (9)). With the exception of determining the influence of oil price collapse, this paper also examined the effect trajectories of other potential determinants on the carbon price with considering the mobility restrictions in the COVID-19 period. The short-term calculation results indicated that COVID-19 reinforced the driver effects, as evidenced by the more complicated Granger relationships in the post-COVID-19 period. Over the long term, the common determinant effects abated and the mobility trends became more powerful.

Except for exchange rate, the complete COVID-19 shutdown measures at the beginning of 2020 resulted in steep declines in carbon price and all other influence factors. Because the pandemic has resulted in unprecedented economic crises, this may have resulted in a decrease in emissions permits, and slumps in energy prices, which could have led to greater fossil fuel consumption and increasing emissions allowance demand (Smith et al. 2021). The recovery policies established by governments were designed to prevent their economies slipping into recession, which was evidenced by the steady rebound in carbon prices, energy prices, and the macroeconomic index in this study (Fig. 8).

Previous studies have found that the energy markets and macroeconomic indexes were the main carbon price impact factors (Zhou and Li 2019; Li et al. 2020). However, the carbon price drivers have been verified to be not fixed over time (Batten et al. 2021), which was consistent with the results in this paper. Beyond that, this paper further determined the different factors on multiple timescales, from which it was found that the HF module carbon price was positively affected by the exchange rate and natural gas in the pre-COVID-19 period, and the GSCI, oil price and STOXX impacted the HF module carbon price in the post-COVID-19 period. Comparing with the HF modules, the impacts of drivers over the prolonged period were weaker. Over the long term, around 90% of the carbon price volatility was self-explained when the COVID-19 outbreak was not considered.

The carbon price has experienced continuous decreases in global financial crisis and European debt crisis periods, and the surplus allowance caused by the depressing economy has made carbon price stay low (Zhu et al. 2015). Even the economy recovery after its plunge did not revive the gloomy carbon price (Ellerman et al. 2016). As the purpose of the MSR mechanism is to avoid large structural allowance surplus,Footnote 2 the COVID-19 is a severe test for MSR mechanism on stabilizing the carbon price. Some researchers have considered the MSR mechanism to be an effective instrument for dealing with the exogenous shock brought by COVID-19 in short term (Gerlagh et al. 2020), while others had opinions that the MSR can deal with the exogenous shocks with considering more severe and longer lasting impacts of the pandemic (Azarova and Mier 2021). In this research, the characteristics of the LF and trend module indicated that the MSR adjustments were flexible and the MSR effect was more powerful over the long-term period and in the trend modules, as evidenced by the high autoregressive characteristics of carbon price in LF and trend modules. Although the COVID-19 pandemic shock increased the turmoil in markets and the MSR effect was slightly weakened, the MSR mechanism still was one of the most main reasons for the recovery of the carbon price.

Conclusions

The COVID-19 impact and the associated quarantine measures have slowed economic development and social mobility, and led to a reduction in overall carbon emissions. This paper focuses on the EU ETS and related markets to determine the evolution relationships between the carbon price and the potential drivers in the pre- and post-COVID-19 periods. The N-A MEMD method was employed to simultaneously decompose the multi-dimensional time series into multichannel IMFs and residuals to resolve the nonstationarity and nonlinearity. The LZ complexity algorithm was then used to reconstruct the IMFs into HF, LF and trend modules to analyze the multi-scale relationships between variables. After testing the unit roots of modules, a VAR model was employed on the HF module to determine the short fluctuations and a VEC model was applied to the LF module to describe the long-term cointegration between variables. By combining the trend descriptions, the long-term carbon price autoregression characteristics were determined. This paper also compared the pre- and post-COVID-19 periods, from which the following were found.

-

(1)

The IRF and VD results in both periods indicated that common drivers were the main influences on the short time of the carbon price, and these drivers were heavily affected by market shocks, such as the COVID-19 outbreak. The MSR mechanism was found to be the support of long-term carbon price stabilization, which evidenced by the high autocorrelation characteristics of carbon price.

-

(2)

The comparison of the causal relationships between carbon price and influence factors in pre- and post-COVID-19 periods verified that the pandemic had complicated the cross-correlations of the carbon price and determinants, and the epidemic had amplified the external markets effects on the ETS. These pandemic effects determination results provide a reference for future research to analyze the emergent events impact to the carbon trading market, which is lack of sufficient investigation but very important.

-

(3)

A post-COVID-19 period economic rebound was verified. Because the energy prices were depressed at the beginning of the outbreak, the energy consumption was found to increase in the following year, which resulted in a steady rise in the energy and carbon prices.

These findings can not only provide references on selecting influence factors when forecasting the carbon price, but also examine the effectiveness of current measures on stabilizing the ETS when there are external extreme shocks. According to the continuous raising trends of series in Fig. 8, governments should pay attention on the possible high energy consumption in economic recovery period, which may hinder the emission reduction progress.

Since this paper mainly puts attention on exploring the evolution of relationships between EU ETS and related stock markets in pre- and post-epidemic periods, there are some limitations in current research. First, this research mainly explores the endogenous impact factors, and there may be other possible exogenous drivers for carbon price such as Baidu index. Second, this research only discusses the European markets, while the ETS markets in other regions, such as China, are also deserved to be explored (Cong and Lo 2020). Future research plans to examine the unstructured carbon price impact variables, such as the emission reduction policies (Song et al. 2019) and search indexes (Huang and He 2020). As the carbon emissions trading markets in other countries may have had different reactions to COVID-19, a comparative study with EU ETS could be an interesting research direction, for example, how did the immature emissions trading market in China maintain stability and avoid a carbon price crash during the pandemic?

Availability of data and materials

The data analyzed during the current study are available as follows.

Carbon futures price data sourced from ICE is available on https://www.theice.com/index.

Futures prices of Brent crude oil and Rotterdam coal sourced from ICE are available on https://investing.com/.

GSCI sourced from Chicago Mercantile Exchange and the STOXX are available on https://investing.com/.

Natural gas futures price sourced from EIA is available on https://www.eia.gov/.

Mobility trends data is not publicly available any more due to the expiry date of the Mobility Trend Reports but are available from the corresponding author on reasonable request.

Notes

International Energy Agency. Global Energy Review: CO2 Emissions in 2020 Understanding the impacts of Covid-19 on global CO2 emissions: https://www.iea.org/articles/global-energy-review-co2-emissions-in-2020

Communication from the Commission. Publication of the total number of allowances in circulation for the purposes of the market stability reserve under the EU Emissions Trading System established by Directive 2003/87/EC (2017/C 150/03): http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52017XC0513(01).

References

Aatola P, Ollikainen M, Toppinen A (2013) Price determination in the EU ETS market: Theory and econometric analysis with market fundamentals. Energy Economics 36:380–395. https://doi.org/10.1016/j.eneco.2012.09.009

Anke CP, Hobbie H, Schreiber S, Möst D (2020) Coal phase-outs and carbon prices: Interactions between EU emission trading and national carbon mitigation policies. Energy Policy 144:111647. https://doi.org/10.1016/j.enpol.2020.111647

Apple (2020) Mobility Trend Reports. Apple: Cupertino, CA, USA. https://www.apple.com/covid19/mobility. Accessed 6 April 2021

Arora V, Cai YY (2014) U.S. Natural gas exports and their global impacts. Appl Energy 120:95–103. https://doi.org/10.1016/j.apenergy.2014.01.054

Arouri MEH (2011) Does crude oil move stock markets in Europe? A sector investigation. Econ Model 28:1716–1725. https://doi.org/10.1016/j.econmod.2011.02.039

Azarova V, Mier M (2021) Market Stability Reserve under exogenous shock: The case of COVID-19 pandemic. Appl Energy 283:116351. https://doi.org/10.1016/j.apenergy.2020.116351

Bagchi B, Chatterjee S, Ghosh R, Dandapat D (2020) Impact of COVID-19 on global economy. In: Coronavirus Outbreak and the Great Lockdown. SpringerBriefs in Economics. Springer, Singapore. https://doi.org/10.1007/978-981-15-7782-6_3

Batten JA, Maddox GE, Young MR (2021) Does weather, or energy prices, affect carbon prices?. Energy Economics 96:105016. https://doi.org/10.1016/j.eneco.2020.105016

Bernardino J, Aggelakakis A, Reichenbach M, Vieira J, Boile M, Schippl J, Christidis P, Papanikolaou A, Condeco A, Garcia H, Krail M (2015) Transport demand evolution in Europe-factors of change, scenarios and challenges. European Journal of Futures Research 3(1):1–13. https://doi.org/10.1007/s40309-015-0072-y

Bruninx K, Ovaere H, Delarue E (2020) The long-term impact of the market stability reserve on the EU emission trading system. Energy Economics 89:104746. https://doi.org/10.1016/j.eneco.2020.104746

Chiang AC (1984) Fundamental methods of mathematical economics. McGraw-Hill, Auckland, London

Cong R, Lo AY (2020) Emission trading and carbon market performance in Shenzhen, China. Appl Energy 193:414–425. https://doi.org/10.1016/j.apenergy.2017.02.037

Djilali S, Benahmadi L, Tridane A, Niri K. (2020) Modeling the impact of unreported cases of the COVID-19 in the North African countries. Biology 9:373. https://doi.org/10.3390/biology9110373

Dong F, Gao Y, Li Y, Zhu J, Hu M, Zhang X (2020) Exploring volatility of carbon price in European Union due to COVID-19 pandemic. Environ Sci Pollut Res 29(6):8269–8280. https://doi.org/10.1007/s11356-021-16052-1

Dutheil F, Baker JS, Navel V (2021) Air pollution in post-COVID-19 world: The final countdown of modern civilization?. Environ Sci Pollut Res 28:46079–46081. https://doi.org/10.1007/s11356-021-14433-0

Ellerman AD, Marcantonini C, Zaklan A (2016) The European union emissions ttrading system: Ten years and counting. Rev Environ Econ Policy 10(1):89–107. https://doi.org/10.1093/reep/rev014

Gerlagh R, Heijmans RJ, Rosendahl KE (2020) COVID-19 Tests the market stability reserve. Environ Resour Econ 76(4):855–865. https://doi.org/10.1007/s10640-020-00441-0

Google (2020) COVID-19 Community Mobility Reports. Google: California, USA. https://www.google.com/covid19/mobility/. Accessed 1 March 2022

Hamilton JD (1994) Time Series Analysis. Princeton University Press, Princeton, UK, pp 291–350

Huang NE, Shen Z, Long SR, Wu MLC, Shih HH, Zheng QN, Yen NC, Tung CC, Liu HH (1998) The empirical mode decomposition and the Hilbert spectrum for nonlinear and non-stationary time series analysis. Proceedings of The Royal Society A: Mathematical, Phys Eng Sci 454:903–995. https://doi.org/10.1098/rspa.1998.0193

Huang Y, He Z (2020) Carbon price forecasting with optimization prediction method based on unstructured combination. Sci Total Environ 725:138350. https://doi.org/10.1016/j.scitotenv.2020.138350

Jefferson M (2020) A crude future? COVID-19s challenges for oil demand, supply and prices. Energy Research & Social Science 68:101669. https://doi.org/10.1016/j.erss.2020.101669

Ji CJ, Hu YJ, Tang BJ, Qu S (2021) Price drivers in the carbon emissions trading scheme: Evidence from Chinese emissions trading scheme pilots. J Clean Prod 278:123469. https://doi.org/10.1016/j.jclepro.2020.123469

Johansen S (1995) Likelihood-based inference in cointegrated vector autoregressive models. Oxford University Press, London, pp 45–57

Johansen S, Juselius K (1990) Maximum likelihood estimation and inference on cointegration–with application to the demand for money. Oxford Bulletin of Economics and Statistics 52(2):169–210. https://doi.org/10.1111/j.1468-0084.1990.mp52002003.x

Johns Hopkins University (2021) COVID-19 dashboard by the center for systems science and engineering at Johns Hopkins University. https://coronavirus.jhu.edu/map.html. Accessed 17 June 2021

Keppler JH, Mansanet-Bataller M (2010) Causalities between CO2, electricity, and other energy variables during phase I and phase II of the EU ETS. Energy Policy 38:3329–3341. https://doi.org/10.1016/j.enpol.2010.02.004

Khurshid A, Khan K (2021) How COVID-19 shock will drive the economy and climate? a data-driven approach to model and forecast. Environ Sci Pollut Res 28(3):2948–2958. https://doi.org/10.1007/s11356-020-09734-9

Kolmogorov AN (1968) Logical basis for information theory and probability theory. IEEE Trans Inf Theory 14(5):662–664. https://doi.org/10.1109/TIT.1968.1054210

Lempel A, Ziv J (1976) On the complexity of finite sequenced. IEEE Trans Inf Theory 22 (1):75–81. https://doi.org/10.1109/TIT.1976.1055501

Li ZP, Yang L, Zhou YN, Zhao K, Yuan XL (2020) Scenario simulation of the EU carbon price and its enlightenment to China. Sci Total Environ 723:137982. https://doi.org/10.1016/j.scitotenv.2020.137982

Liu H, Shen L (2019) Forecasting carbon price using empirical wavelet transform and gated recurrent unit neural network. Carbon Management 11(1):25–37. https://doi.org/10.1080/17583004.2019.1686930

Lutz BJ, Pigorsch U, Rotfuss W (2013) Nonlinearity in cap-and-trade systems: the EUA price and its fundamentals. Energy Economics 40:222–232. https://doi.org/10.1016/j.eneco.2013.05.022

Malliet P, Reynes F, Landa G, Hamdi-Cherif M, Saussay A (2013) Assessing short-term and long-term economic and environmental effects of the COVID-19 crisis in France. Environ Resour Econ 76(4):867–883. https://doi.org/10.1007/s10640-020-00488-z

Mankiw NG (2000) Macroeconomics. New York: Worth

Marmer V (2008) Nonlinearity, nonstationarity, and spurious forecasts. J Econ 142(1):1–27. https://doi.org/10.1016/j.jeconom.2007.03.002

Mensi W, Hammoudeh S, Shahzad SJH, Shahbaz M (2017) Modeling systemic risk and dependence structure between oil and stock markets using a variational mode decomposition-based copula method. Journal of Banking & Finance 75:258–279. https://doi.org/10.1016/j.jbankfin.2016.11.017

Mintz-Woo K, Dennig F, Liu HX, Schinko T (2021) Carbon pricing and COVID-19. Clim Pol 21(10):1272–1280. https://doi.org/10.1080/14693062.2020.1831432

Niederreiter H (1992) Random number generation and quasi-Monte Carlo methods. Society for Industrial and Applied Mathematicss, Philadelphia, PA

Ou SQ, He X, Ji WQ, Chen W, Sui L, Gan Y, Lu ZF, Lin ZH, Deng SL, Przesmitzki S, Bouchard J (2020) Machine learning model to project the impact of COVID-19 on US motor gasoline demand. Nature Energy 5:666–673. https://doi.org/10.1038/s41560-020-0662-1

Rasheed R, Rizwan A, Javed H, Sharif F, Zaidi A (2021) Socio-economic and environmental impacts of COVID-19 pandemic in Pakistan-an integrated analysis. Environ Sci Pollut Res 28:19926–19943. https://doi.org/10.1007/s11356-020-12070-7

Rehman N, Mandic DP (2010) Multivariate empirical mode decomposition. Proceedings of The Royal Society 466:1291–1302. https://doi.org/10.1098/rspa.2009.0502

Rehman N, Mandic DP (2011) Filter bank property of multivariate empirical mode decomposition. IEEE Transactions on Signal Processing 59(5):2421–2424. https://doi.org/10.1109/TSP.2011.2106779

Smith LV, Tarui N, Yamagata T (2021) Assessing the impact of COVID-19 on global fossil fuel consumption and CO2 emissions. Energy Economics 97:105170. https://doi.org/10.1016/j.eneco.2021.105170

Song Y, Liu T, Liang D, Li Y, Song X (2019) A fuzzy stochastic model for carbon price prediction under the effect of demand-related policy in China’s carbon market. Ecol Econ 157:253–265. https://doi.org/10.1016/j.ecolecon.2018.10.001

Sun W, Wang YW (2020) Factor analysis and carbon price prediction based on empirical mode decomposition and least squares support vector machine optimized by improved particle swarm optimization. Carbon Management 11(3):315–329. https://doi.org/10.1080/17583004.2020.1755597

Tan XP, Wang XY (2017) Dependence changes between the carbon price and its fundamentals: A quantile regression approach. Appl Energy 190:306–325. https://doi.org/10.1016/j.apenergy.2016.12.116

Tiwari AK, Abakah EJA, Le TL (2021) Leyva-de la Hiz DI Markov-switching dependence between artificial intelligence and carbon price: The role of policy uncertainty in the era of the 4th industrial revolution and the effect of COVID-19 pandemic. Technol Forecast Soc Chang 163:120434. https://doi.org/10.1016/j.techfore.2020.120434

Ullah S, Chishti MZ, Majeed MT (2020) The asymmetric effects of oil price changes on environmental pollution: evidence from the top ten carbon emitters. Environ Sci Pollut Res 27:29623–29635. https://doi.org/10.1007/s11356-020-09264-4

Wang J, Shao W, Kim J (2020) Analysis of the impact of COVID-19 on the correlations between crude oil and agricultural futures. Chaos, Solitons and Fractals: Nonlinear Science, and Nonequilibrium and Complex Phenomena 136:109896. https://doi.org/10.1016/j.chaos.2020.109896

Wang Q, Zhang C (2021) Can COVID-19 and environmental research in developing countries support these countries to meet the environmental challenges induced by the pandemic?. Environ Sci Pollut Res 28:41296–41316. https://doi.org/10.1007/s11356-021-13591-5

Yang S, Chen D, Li S, Wang W. (2020) Carbon price forecasting based on modified ensemble empirical mode decomposition and long short-term memory optimized by improved whale optimization algorithm. Sci Total Environ 716:137117. https://doi.org/10.1016/j.scitotenv.2020.137117

Zhang X, Lai KK, Wang SY (2008) A new approach for crude oil price analysis based on empirical mode decomposition. Energy Economics 30(3):905–918. https://doi.org/10.1016/j.eneco.2007.02.012

Zhao X, Han M, Ding LL, Kang WL (2018) Usefulness of economic and energy data at different frequencies for carbon price forecasting in the EU ETS. Appl Energy 216:132–141. https://doi.org/10.1016/j.apenergy.2018.02.003

Zhou KL, Li YW (2019) Influencing factors and fluctuation characteristics of China’s carbon emission trading price. Physica A 524:459–474. https://doi.org/10.1016/j.physa.2019.04.249

Zhu BZ, Wang P, Chevallier J, Wei YM (2015) Carbon price analysis using empirical mode decomposition. Comput Econ 45:195–206. https://doi.org/10.1007/s10614-013-9417-4

Zhu BZ, Ye SX, Wang P, He KJ, Zhang T, Wei YM (2018) A novel multiscale nonlinear ensemble leaning paradigm for carbon price forecasting. Energy Economics 70:143–157. https://doi.org/10.1016/j.eneco.2017.12.030

Zhu BZ, Ye SX, Han D, Wang P, He KJ, Wei YM, Xie R (2019) A multiscale analysis for carbon price drivers. Energy Economics 78:202–216. https://doi.org/10.1016/j.eneco.2018.11.007

Zozor S, Ravier P, Buttelli O (2005) On Lempel–Ziv complexity for multidimensional data analysis. Physica A 345:285–302. https://doi.org/10.1016/j.physa.2004.07.025

Funding

This work was supported by the National Natural Science Foundation of China (Nos. 71671118 and 71971148); and the China Scholarship Council.

Author information

Authors and Affiliations

Contributions

Zhibin Wu: conceptualization, methodology, validation, formal analysis, writing — review and editing, supervision, funding acquisition. Wen Zhang: conceptualization, methodology, validation, software, formal analysis, investigation, writing — original draft. Xiaojun Zeng: conceptualization, validation, writing — review and editing. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Eyup Dogan

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Nomenclature

Nomenclature

Abbreviation | Meaning | Abbreviation | Meaning |

|---|---|---|---|

MEMD | Multivariate empirical mode decomposition | ARDL | Autoregressive distributed lag |

N-A MEMD | Noise-assisted multivariate empirical mode decomposition | IRF | Impulse response function |

IMFs | Intrinsic mode functions | VD | Variance decomposition |

IMF | Intrinsic mode function | ICE | Intercontinental Exchange |

LZ complexity | Lempel-Ziv complexity | EIA | Energy Information Administration |

HF | High-frequency | IQR | Interquartile range |

LF | Low-frequency | Std Dev | Standard deviation |

VAR | Vector autoregression | SI | Supplementary Information |

VEC | Vector error correction | PP test | Phillips-Perron test |

MSR | Market stability reserve | AIC | Akaike info criterion |

EU ETS | European Union emissions trading system | SC | Schwarz criterion |

ETS | Emissions trading system | HQC | Hannan-Quinn criterion |

EUA | European Union allowance | LR | Likelihood ratio |

GSCI | Goldman Sachs Commodity Index | FPE | Final prediction error |

STOXX | STOXX Europe 600 index | OLS | Ordinary least squares |

EMD | Empirical mode decomposition | JJ test | Johansen-Juselius test |

Rights and permissions

About this article

Cite this article

Wu, Z., Zhang, W. & Zeng, X. Exploring the short-term and long-term linkages between carbon price and influence factors considering COVID-19 impact. Environ Sci Pollut Res 30, 61479–61495 (2023). https://doi.org/10.1007/s11356-022-19858-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-022-19858-9