Abstract

This paper proposes a measure of exchange market pressure for countries operating in hard peg regimes, such as currency unions, currency boards or full dollarization. We use a general model of currency crisis to derive a sustainability index based upon the relationship between the shadow exchange rate and the output gap required to maintain the currency peg. We apply the index to European Union countries in order to assess the sustainability of the euro.

Similar content being viewed by others

Notes

A critical review of the literature on the methods used to calculate EMP can be found in Li et al. (2006). Willett et al. (2012) show how the difficulties encountered in computing EMP are related to the difficulties in classifying exchange-rate regimes. The sustainability of hard peg regimes cannot, of course, be measured using Girton-Roper type indexes since crucial variables such as international reserves, exchange rates, and interest rates are not observable at a country level.

A similar approach can also be found, e.g., in Arghyrou and Tsoukalas (2011) and De Grauwe (2011). However, they do not make use of the shadow exchange rate and also do not derive a sustainability index for currency unions that can act as a signal of vulnerability of member countries to speculative attacks and crises.

A detailed analytical discussion of these two approaches, including the basic models and their extensions centered on the relationship between financial fragility, currency crisis and the contagion across markets and countries, can be found in Piersanti (2012).

We abstract here from the real interest rate effect to focus only on the competitiveness issue which has been central to the policy debate about how to manage and correct macroeconomic imbalances within the euro area (see, e.g., Gross 2012; De Grauwe 2012). The interest effect is explored in Buiter et al. (2001), who use a more general model including an interest channel for the transmission of monetary policy to analyze the collapse of the ERM in Europe.

This is typical of the EMU, where a country willing to join the common currency is required to maintain, for an agreed time span, limited deviation from its target rate against the euro.

See, for example, Bahmani-Oskooee (1991). As the Marshall-Lerner or elasticities condition refers to a long-run analysis, the γ coefficient must be negative and statistically significant.

Analogous results were obtained using estimates of \( \left({y}_t^{i,F}-{\overline{y}}^i\right) \) from the IMF.

Results do not change if the above scale is multiplied by a factor k > 0. In order to rank countries according to their anti-inflation reputation, we used the annual percentage change in CPI over the period 1976–2010.

It is of interest to note, however, that the results (available upon request) show no visible change when θ is left to vary in the range [4.6, 3.7] for all countries.

The conversion rates are: 1.95583 for the Deutsche mark; 6.55957 for the French franc; 200.482 for the Portuguese escudo; 1,936.27 for the Italian lira; 0.787564 for the Irish pound; 340.750 for the Greek drachma; 166.386 for the Spanish peseta.

The figure was built using the transformation of the computed indicators of market pressure for each country in standard indexes with mean 0 and standard deviation 1, and applying the ± 2 standard deviation bounds as critical thresholds to identify crisis episodes in the foreign exchange market. This implies the assumption of normality in the statistical distribution of the market pressure index conforming to the literature (see, e.g., Eichengreen et al. 1995, 1996; Sachs et al. 1996; Kaminsky et al. 1998; Kaminsky and Reinhart 1999).

As shown in Canofari et al. (2014b), the different behavior of standardized EMP indexes in the two sub-periods is consistent with market’s beliefs about euro sustainability as reflected in the dynamics of spreads: in the pre-crisis period (2000–2008) markets looked at the EMU as a fully credible monetary union where the probability to exit is zero and spreads are virtually zero (i.e., investors priced the default risk in non-core countries in the same way as the risk of core countries); after the crisis (2008–2012) investors’ confidence in the irreversibility of the euro loosened, markets started looking at the EMU as a system of fixed exchange rates involving the risk of exchange rate realignments and spreads widened.

This agrees extremely well with the results obtained from the online betting platform INTRADE, which imply that markets priced the probability of a country’s exit from the euro area by the end of 2013 at 65, 40, and 60 % in November 2011, in March 2012 and in August 2012, respectively (see, e.g., Klose and Weigert 2012, Chart 19612; Shambaugh 2012, Fig. 1). It is striking to learn that these probabilities most likely reflect the probability of an exit of Greece.

Including Germany’s rate changes only marginally the results shown in Table 4, as the first component explains in this case 76 % of total variation and the first two account for over 92 % of the total. A more deeply econometric investigation aiming to test the power of our sustainability index in capturing market expectation of a euro break-up in the European sovereign debt crises is in Canofari et al. (2014b). Numerical simulation computing contagion effects across EU peripheral countries, using game theory and a similar macroeconomic set-up, can be found in Canofari et al. (2014a).

References

Arghyrou, M. G., & Tsoukalas, J. D. (2011). The Greek debt crisis: Likely causes, mechanics and outcomes. The World Economy, 34(2), 173–191.

Bahmani-Oskooee, M. (1991). Is there a long-run relation between the trade balance and the real effective exchange rate of LDCs? Economics Letters, 36(4), 403–407.

Berger, W., & Wagner, H. (2005). Interdependent expectations and the spread of currency crises. IMF Staff Papers, 52(1), 41–54.

Buiter, W. H., Corsetti, G., & Pesenti, P. A. (2001). Financial markets and European monetary cooperation: The lessons of the 1992–93 exchange rate mechanism crisis. Cambridge: Cambridge University Press.

Canofari, P., Di Bartolomeo, G., & Piersanti, G. (2014a). “Theory and Practice of Contagion in monetary unions: Domino effects in EMU Mediterranean countries”. International Advances in Economic Research.

Canofari, P., Marini, G., & Piersanti, G. (2014b). “Expectations and Systemic Risk in EMU Government Bond Spreads”. Quantitative Finance.

Cavallari, L., & Corsetti, G. (2000). Shadow rates and multiple equilibria in the theory of currency crises. Journal of International Economics, 51(2), 275–286.

De Grauwe, P. (2011). “The Governance of a Fragile Eurozone.” CEPS Working Document, No. 346, May.

De Grauwe, P. (2012). “In Search of Symmetry in the Eurozone.” CEPS Policy Brief, No. 268, May.

Eichengreen, B. (1994). International monetary arrangements for the 21st century. Washington: Brookings Institution.

Eichengreen, B., Rose, A., & Wyplosz, C. (1995). Exchange market mayhem: The antecedents and aftermaths of speculative attacks. Economic Policy, 21, 249–312.

Eichengreen, B., Rose, A., & Wyplosz, C. (1996). Contagious currency crises: First tests. Scandinavian Journal of Economics, 98, 463–484.

Fischer, S. (2001). Exchange rate Regimes: Is the bipolar view correct? Journal of Economic Perspectives, 15, 3–24.

Fischer, S. (2008). Mundell-Fleming lecture: Exchange rate systems, surveillance and advice. IMF Staff Papers, 55, 367–383.

Ghosh, A. R., Ostry, J. D., & Tsangarides, C. (2010). “Exchange Rate Regimes and the Stability of the International Monetary System”. IMF Occasional Paper, No. 270 (March), International Monetary Fund, Washington, D.C.

Girton, L., & Roper, D. (1977). A monetary model of exchange market pressure applied to the postwar Canadian experience. American Economic Review, 67, 537–547.

Gros, D. (2012). “Macroeconomic imbalances in the Euro area: Symptom or cause of the crisis?”. CEPS Policy Brief, No. 266, April.

Jeanne, O. (1997). Are currency crises self-fulfilling? A test. Journal of International Economics, 43, 263–286.

Kaminsky, G., & Reinhart, C. (1999). The twin crises: The causes of banking and balance-of-payments problems. American Economic Review, 89, 473–500.

Kaminsky, G., Lizondo, S., & Reinhart, C. (1998). Leading indicators of currency crises. IMF Staff Papers, 45, 1–48.

Klose, J., & Weigert, B. (2012). “Determinants of Sovereign Yields Spreads During the Euro – Crises – Fundamental Factors vs Systemic Risk”. German Council of Economic Experts, Working Paper, No 07, November.

Li, J., Rajan,R. S. & Willett, T. D. (2006). “Measuring Currency Crises Using Exchange Market Pressure Indices: The Imprecision of Precision Weights”. Claremont Working Paper, Institute for Economic Policy Studies, Claremont Graduate University.

Masson, P. R. (1999a). Contagion: Macroeconomic models with multiple equilibria. Journal of International Money and Finance, 18, 587–602.

Masson, P. R. (1999b). Contagion: Monsoonal effects, spillovers and jump between multiple equilibria. In P. R. Agénor, M. Miller, D. Vines, & A. Weber (Eds.), The Asian financial crisis: Causes, contagion and consequences. Cambridge: Cambridge University Press.

Obstfeld, M. (1996). Models of currency crises with self-fulfilling features. European Economic Review, 40, 1037–1047.

Piersanti, G. (2012). The macroeconomic theory of exchange rate crises. Oxford: Oxford University Press.

Sachs, J. D., Tornel, A., & Velasco, A. (1996). Financial crises in emerging markets: The lessons from 1995. Brookings Papers on Economic Activity, 27, 147–215.

Shambaugh, J. C. (2012). The Euro’s three crises. Brookings Papers on Economic Activity, 44, 157–231.

Summers, L. H. (2000). International financial crises: Causes, prevention, and cures. American Economic Review: Papers and Proceedings, 90, 1–16.

Velasco, A. (1996). Fixed exchange rates: Credibility, flexibility and multiplicity. European Economic Review, 40, 1023–1035.

Weymark, D. N. (1995). Estimating exchange market pressure and the degree of exchange market intervention for Canada. Journal of International Economics, 39, 273–295.

Willet, T. D., Kim, J., & Bunyasiri, I. N. (2012). Measuring exchange rate flexibility: A two parameter exchange market pressure approach. Global Journal of Economics, 1, 701–728.

Acknowledgments

For helpful comments and discussions, we tank Barbara Annicchiarico, Luisa Corrado, Giovanni Di Bartolomeo, Laurence Harris, Alessandro Piergallini, Pasquale Scaramozzino, Yothin Jinjarak, an anonymous referee and seminar participants at the II Workshop in International Economics, University of Rome Tor Vergata, the XX International Tor Vergata Conference on Money, Banking and Finance, the XXIV Villa Mondragone International Economic Seminar, as well as seminar participants at CeFiMS, SOAS, University of London, the University of Rome Tor Vergata and the University of Teramo.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix A

Table 2 shows augmented Dickey-Fuller (ADF) test statistics for x i,t − m i,t and ε i,t both in levels and first differences. The sample covers quarterly data over the period 1985Q1 – 2010Q2. Lag lengths have been set equal to 5. For both variables, ADF is less than its critical value only when we use first differences. This means that the hypotheses that x i,t − m i,t and ε i,t have a unit root cannot be rejected. On the other hand, we can reject the hypotheses that first differences of x i,t − m i,t and ε i,t have a unit root.

Column 7 of Table 3 shows the vector error correction estimates displaying the long run equilibrium relationship between x i,t − m i,t and ε i,t : Standard errors and T-statistics are shown in brackets. Table 3 shows that we cannot reject the hypothesis that both x i,t − m i,t and ε i,t are cointegrated for each country and that the cointegrating relationships are stable throughout the sample period.

Appendix B

Data Sources

- y t :

-

Real GDP (billions of national currency). Source: IMF: World Economic Outlook. Period: 1999–2012.

- ε i,t :

-

Real effective exchange rate. Source: IMF: International Financial Statistics. Period: 1980Q1 - 2010Q3.

- x t :

-

Goods exports (millions of US Dollars). Source: IMF: International Financial Statistics. Period: 1980Q1 - 2010Q3.

- m t :

-

Goods imports (millions of US Dollars). Source: IMF: International Financial Statistics. Period: 1980Q1 - 2010Q3.

- CPI :

-

Consumer Price Index. Source: OECD: Main Economic Indicators. Period: 1976–2010.

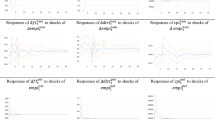

Dynamics of EMP index under alternative values for θ

Rights and permissions

About this article

Cite this article

Canofari, P., Marini, G. & Piersanti, G. Measuring Currency Pressure and Contagion Risks in Countries under Monetary Unions: The Case of Euro. Atl Econ J 42, 455–469 (2014). https://doi.org/10.1007/s11293-014-9434-2

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11293-014-9434-2