Abstract

Innovative start-ups are an important driver of economic growth. This article presents empirical evidence on the effects of research and development (R&D) on new product development, interfirm alliances and employment growth during the early life course of firms. We use a dataset that contains a sample of new firms that is representative of the whole population of start-ups. This dataset covers the first 6 years of the life course of firms. It is revealed that R&D plays several roles during the early life course of high-tech as well as high-growth firms. The effect of initial R&D on high-tech firm growth is through increasing levels of interfirm alliances in the first post-entry years. R&D efforts enable the exploitation of external knowledge. Initial R&D also stimulates new product development later on in the life course of high-tech firms, but this does not seem to affect firm growth. R&D does not affect the growth rate of new low-tech firms, which seem to be driven mainly by the growth ambitions of the founding entrepreneur. The results show that R&D matters for a limited but important set of new high-tech and high-growth firms, which are key in innovation and entrepreneurship policies.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

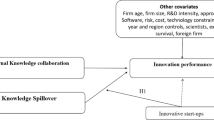

Innovative start-ups are an important driver of economic growth in capitalist economies (Baumol 2002). However, there is still no consensus on what effects innovation activities have on the growth of start-ups. Some studies reveal a positive effect of innovation activities on the growth of new firms (Deeds 2001) and small firms (Storey 1994; Roper 1997), whereas others have found no evidence (Freel 2000; Winters and Stam 2007) or even a negative effect (Freel and Robson 2004). This debate has made some progress by distinguishing different types of growth: recent studies indicate that innovation is a driver for growth only among a minority of fast-growing firms (Coad and Rao 2008; Hölzl 2009). Stimulating the growth of new firms is a key element of entrepreneurship policy that aims to improve the conditions for high-growth start-ups (Smallbone et al. 2002; Fischer and Reuber 2003) in order to spur structural economic change and job creation (Henrekson and Johansson 2009a). Hence, part of the conflicting findings of earlier studies might be due to an apparent heterogeneity among new firms where most firms grow very little or not at all, and a small minority of firms grow very rapidly (Davidsson 2007). Another reason for the lack of consensus on the effect of innovation on firm growth is the diversity of innovation activities in which a firm might be involved in order to grow. One of the most often measured types of innovation activities is R&D. R&D per se might be less important for firm growth compared with the ability of R&D activities to generate new products and alliances with other firms, hence acting as impetus for growing the new firm. In this paper we therefore both examine to what extent R&D activities affects new firm growth directly, or indirectly through new product development and/or alliances with other firms.

Even if innovative start-ups do not succeed to grow, their innovation efforts might improve the performance (Hoetker and Agarwal 2007) or start-up (Wong et al. 2008) of other related firms (knowledge spillovers). So, even if investments in innovation activities do not benefit the firm directly, innovations might provide new knowledge about productive possibilities that other firms will take into account in their innovation or imitation strategies, which will collectively benefit society (see e.g. Arrow 1962; Rosenberg 1990). This is one of the rationales for innovation policy interventions, also advocated in the recent EU Lisbon Strategy. Next to these spillovers from innovation activity, especially small firms are claimed to underinvest in R&D activities, i.e. at a level that is suboptimal from a societal perspective. This is partly because it is more difficult for them to appropriate the returns from resulting innovations due to their limited complementary assets (Teece 1986). Second, these small firms are likely to be resource constrained. Due to information asymmetries and the uncertainty involved in innovation projects, financial markets are less likely to provide the necessary investment for innovative new and small firms (Smallbone et al. 2002; Hall 2002; Canepa and Stoneman 2008). The resulting shortage of investment capital is one reason why innovative small firms in, for example, biotech or information technology are acquired by larger firms that provide the necessary resources for developing and marketing their innovations (Granstrand and Sjölander 1990; Wennberg and Lindqvist 2009). Next to the societal necessities of more investment in R&D to get Europe on a high-growth path, a more comprehensive and coherent growth policy is needed, in which increasing the number of entries and market competition are important elements (Aghion 2006). In this sense, stimulating R&D intensive start-ups might simultaneously serve the two policy goals of increasing R&D levels and the number of competitive entrants. Prior research has shown that, even though small firms in general less often engage in R&D than large firms, when they do so they tend to use their innovative inputs more efficiently than large firms (Acs and Audretsch 1990; Nooteboom 1994).

Most research on the effects of R&D has looked at specific samples of high-tech firms or manufacturing and services firms and tends not to include micro firms (e.g. Kleinknecht and Reijnen 1992; Roper et al. 2008). Since most start-ups have fewer than ten employees, the findings of these earlier studies might not be relevant to the general population of new firms, which is of critical importance for correctly generating and implementing public policies. In this study we use a longitudinal random sample of Dutch firms that we follow over their first 6 years of life. The dataset has several advantages. First, it is representative of the whole population of start-ups, so it does not only include manufacturing and services, but also all other sectors, and in contrast to most other innovation studies it includes micro firms, which make up the majority of the population of start-ups. Second, this dataset includes a rich set of explanatory variables measured at different points in time and we can hence investigate the sequences of innovation activities and the effect of these on firm growth. Third, the data can be used to take into account the skewed nature of firm growth, by analysing the effects of innovation activities on the growth rate of all firms, but also the effects on the growth rate of the fastest-growing firms. The multilevel nature of the data allows us to investigate effects of individual-level characteristics such as the human capital of the founding entrepreneur, firm-level resources such as firm partners and financial capital, and industry-level variables. We use ordinary least-squares (OLS) regression to investigate the drivers of growth in the early life course of firms. In the empirical study we examine firm growth during the early life course and how it is affected by innovation activities such as R&D, interfirm alliances (IFA), and new product development (NPD). We show that, if one looks at the overall population of new firms as a homogenous group, there is no effect of R&D on new firm growth. However, if we distinguish between high-tech and low-tech firms in the population, we find that R&D is strongly related to the growth of new high-tech firms. In addition we found that R&D activities strongly improve the growth rate of the fastest-growing start-ups. R&D seems to play several roles during the early life course of high-tech firms. The effect of initial R&D on growth seems to run via increasing levels of interfirm alliances in the first post-entry years: R&D efforts enable the exploitation of external knowledge. Initial R&D also stimulates new product development later on in the life course of high-tech firms, but this does not seem to affect firm growth.

By providing new insights into the role of innovation activities such as R&D, new product development and interfirm alliances during the early life course of firms, we offer contributions to the innovation literature and the literature on new firm growth. The longitudinal nature of the data also enables us to make stronger statements about the time-dependent effects of innovation activities on firm growth. Our findings provide insights for innovation policy by showing to what degree R&D efforts lead to the development of new products or the creation of interfirm alliances. Our findings also provide insights for entrepreneurship policy by investigating the effects of R&D in combination with either new product development or interfirm alliances on the growth of new firms.

2 Innovation and new firm growth

Innovation is generally defined as the search for, and the discovery, development, improvement, adoption and commercialisation of, new processes, new products and new organisational structures and procedures (Dosi 1988). It involves uncertainty, risk taking, probing and reprobing, experimenting and testing. Similarly, Schumpeter (1934) describes innovation as the combination of resources in a novel way by entrepreneurs. In line with Schumpeter (1934), innovation and new firms are often taken as similar phenomena. New firms are often assumed to embody innovations whilst in reality empirical studies have revealed that the majority of new firms neither innovate nor grow, nor intend to do so (Reynolds and White 1997; Samuelsson and Davidsson 2009; Wiklund et al. 2003). Entrepreneurs that do strive to grow their firms face issues during their life course that are completely different from those of the many start-ups that remain small. New growing firms are unable to sustain growth unless they can expand and renew their resource base with capabilities in activities such as research, product development and alliances (cf. Baldwin and Gellatly 2003; McKelvie and Davidsson 2009). That this is a hazardous undertaking is reflected in the fact that most young firms that do grow also face setbacks during their early life course (Garnsey 1998; Garnsey et al. 2006). Even more established firms that achieve considerable growth are not likely to maintain this growth record (Parker et al. 2005).

To the best of our knowledge, no studies to date have investigated the effect of innovation activities for the growth of general samples of new firms. Some studies reveal a positive effect of innovation activities on the growth of new high-tech firms (Deeds 2001) and small firms (Storey 1994; Roper 1997), whereas others have found no evidence for small firms (Freel 2000; Winters and Stam 2007) or even a negative effect (Freel and Robson 2004). In this still small literature, it is not yet clear whether the effects of innovation activities on growth are causally direct or indirect in nature (Davidsson et al. 2007). While one can imagine that growth-willingness could exhibit direct effects on the growth of a new firm, it seems equally plausible that such entrepreneurial characteristics will have indirect effects on growth by instead spurring R&D, development of new products and initiation of interfirm alliances.

New firms are often characterised by a relatively weak resource base (Garnsey 1998) and to achieve growth they must engage in processes to reconfigure this resource base and learn about new ways to achieve increased efficiency in operations. These processes are enabled by dynamic capabilities (Eisenhardt and Martin 2000). Such capabilities include specific and identifiable processes such as R&D, new product development and alliances. Research and development (R&D) has at least two functions. First, it builds knowledge within the firm to generate inventions (Rosenberg 1990). Second, it improves the firm’s ability to understand and absorb knowledge from outside the firm such as the knowledge spillovers generated by other organisations’ R&D (Cohen and Levinthal 1989). Alliances provide access to complementary resources from external sources, which are often essential in high-tech industries (Powell et al. 1996; Niosi 2003). Finally, product development commonly entails that the varied skills and backgrounds of firm members are combined to create further revenue-producing goods and services. Early engagement in these activities represents possibilities for new firms to develop their innovation activities and building a structure that allows them to leverage their—possibly limited—resources. Thus, we suggest that entrepreneurs can create and adapt the resource base of their new firm by, early on, engaging in R&D activities, and developing new products and alliances with other firms. We therefore expect that engaging in innovation activities early on will have a positive effect on firm growth. In addition, we specify the effect of R&D in two directions: first, initial R&D will improve the exploitation of new product development later on; second, initial R&D will improve the exploitation of interfirm alliances later on. Only few new firms are likely to build capabilities, and these capabilities are not valuable in every context. There may be certain preconditions for the favourable effects of innovation activities. Innovation activities are said to be especially valuable in technologically dynamic environments since this helps alleviate uncertainty (Eisenhardt and Martin 2000). Earlier on, Rosenberg (1990) argued that firms in high-tech industries need to do R&D in order to understand better how and where to innovate. Next to the direct effect of technologically dynamic environments (providing relatively many entrepreneurial opportunities), we thus expect a moderating effect of high tech on the relation between innovation activities and firm growth.

In contrast to the expected positive effects of innovation activities on the growth of firms, multiple studies have failed to confirm the existence of such effects (Freel 2000; Freel and Robson 2004; Winters and Stam 2007). One explanation for this is that innovation does not improve growth for the average firm, but only has a positive effect on the growth rate of fast-growing firms (Freel 2000). Some recent studies find evidence that innovation activities are of crucial importance to stimulate growth of the ‘superstar’ high-growth firms (Coad and Rao 2008; Hölzl 2009). Coad and Rao (2008) have investigated the effects of patenting and R&D on the sales growth of US manufacturing firms. They find that only among a small proportion of fast growers did innovation activities have a strong effect on sales growth; however, the evidence is limited to incumbent firms. Hölzl (2009) studies the effects of innovation activities on employment growth in a stratified random sample of manufacturing firms in 16 EU countries between 1998 and 2000. He finds that innovation in the form of R&D and turnover share of products new to the market is more important for the growth of fast-growing SMEs. Innovation can be seen as a high-risk high-gain strategy: if successful, innovation might provide a growth premium, but it is also very likely that the innovation turns out to be a failure and even a drag on the growth rate of most firms. We will control for this growth effect for superstar firms by focusing on the growth effect of innovation activities on an elite set of fast-growing firms.

3 Research design and measures

In order to explore and explain the effects of R&D on the growth of new firms we use a dataset of firms started in 1994 in The Netherlands, called ‘Start-up panel: cohort 1994’. This makes our studies comparable with earlier studies of firm growth spanning a similar time period (e.g. Dahlqvist et al. 2000; Lotti et al. 2001). The ‘Start-up panel: cohort 1994’ was set up by EIM Business and Policy Research and constitutes a random sample of all firms registered as independent start-ups in 1994; 12,000 firms were approached and almost 2,000 start-ups agreed to participate in the panel in 1994 (Bosma et al. 2004). These firms were surveyed by mail and by computer-assisted telephone interviews. Some participants declined to participate in the panel in later years, ceased economic activities, went bankrupt or moved and could not be traced. This analysis includes the 647 firms that survived and continued to respond to the survey from start-up to the sixth year of existence. The inclusion of surviving firms only indicates a potential danger for biased inferences if, but only if, there are reasons to believe that the theoretically derived predictor variables are also correlated with attrition from the sample. We therefore conducted a nonsurvivor analysis of the sample in the Appendix. All variables were measured during the firms’ first year of existence (1994) and a subset at biannual intervals until 2000.

Growth. Growth of firms can be measured in organisational as well as in financial terms. A focus on the growing organisation means that researchers will call attention to changes in number of establishments or employees. A focus on financial impact of a firm means that measures of outputs (e.g. profits or revenues) or the accumulated value (e.g. assets) will be used. Prior studies reveal that different measures of growth are not necessarily correlated with each other and ensuring consistency in definition between studies is therefore important for comparability (e.g. Delmar 1997). We therefore focus on the measure of growth that is widely used in both the economics and management literature on new firm growth: number of employees (Coad 2009; Delmar 1997). We choose this measure since it is most comparable with that used in other empirical studies. Further, employment growth is a strong indicator of the growth of the assets of the new firm given that human resources are one of the most important assets of new firms. Finally, changes in employees are a conservative measure for investigating the instability of growth, in comparison with more rapidly changing figures such as sales or capital valuation. We used the rate of employment growth over the first 6 years as dependent variable. Exploratory analysis revealed that most firms in the start-up panel (70%) did not grow at all during over their first 6 years (6% shrunk, and 24% grew). These skewed values mirror those of earlier studies (e.g. Fritsch and Weyh 2006; Coad and Rao 2008). We therefore focus also on the growth rate of a specific group of superstar firms, i.e. the 10% fastest-growing firms in our sample (with a growth rate of 250% or more). As a robustness check we also analysed the growth (24%) versus the nongrowth firms (76%).

The R&D activities variable was measured by asking whether the firms performed research and development activities in order to develop new products and/or processes for their firm. Next to this binary variable, an ordinal variable was used that reflects the percentage of labour time that is spent on R&D (ranging from <1%, 1–5%, 5–10%, 10–20%, 20–30%, 30–40%, 40–50%, and >50%).

Alliances was measured by asking whether the firms collaborated with one or more other firms in some way (this could be related to production, purchasing, sales, R&D, and logistics; but is different from ‘pure’ market transactions).

New product development. Firms were asked whether they have been involved in developing new products.

The data reveal that most innovation activities (R&D, alliancing or new product development) are fairly stable over time. About a third of the firms are involved in new product development in some period and about one in four firms are involved in alliances in some period. The number of firms that is involved in R&D activities is much smaller: about one in ten in every period (Fig. 1), confirming prior research that showed that the overwhelming majority of small firms do not perform any R&D (Kleinknecht and Reijnen 1992; Nooteboom 1994).

Innovation activities in three subsequent periods during the early life course

High tech. This variable was measured by asking entrepreneurs whether the products of their firm are based on one of the four following new generic technologies: new materials, biotechnology, medical technology or environmental/energy technology. By measuring the technological basis of the firm’s product we were able to create a more fine-grained variable than the usual industry classification of high tech (cf. Baldwin and Gellatly 1998). About one-third of the firms in our sample classify as high tech. This variable reveals substantial heterogeneity over industries: most firms in manufacturing classify as high tech, while less than 25% of the firms in the retail, transport and communication, and financial and business services are high tech.

Control variables. Previous research has found that small firm growth is strongly dependent on the founders’ willingness to grow (Delmar and Wiklund 2008). We measured growth ambitions of the founders-entrepreneur by asking them “Do you seek to expand the number of personnel on the medium term (2–3 years)?” on a three-point scale. We also controlled for the founder’s gender, general human capital (age, educational level) and specific human capital (prior entrepreneurial experience, leadership experience and industry experience) (cf. Colombo and Grilli 2005; Cooper et al. 1994). Next to these individual level variables, we controlled for firm-level resources. A variety of firm resources can be distinguished, among which financial capital and organisational capital are particularly important. Financial capital was measured by the amount of start-up capital. Two indicators of organisational capital were measured: the number of business partners (entrepreneurial team), and the start-up size of the firm in 1994 in terms of the number of employees. In addition, we controlled for industry characteristics by including industry dummies (manufacturing, construction, retail, wholesale, hospitality, transport and communication, financial and business services, and other services).

A limited set of variables was measured at multiple points in time: R&D, interfirm alliances, new product development and employment size. This enables us to explore the value of particular sequences of innovation activities for the growth of new firms. As most variables are not available at multiple points in time, we could not use panel techniques such as fixed- or random-effects models, and mainly used OLS regression models.

4 Empirical analysis

The means, standard deviations and correlations of all variables are presented in Table 1. The binary and ordinal variables are defined in such a way that the lowest value indicates that the aspect is not present and the highest value indicates that the aspect is present. All indicators of innovation activities are positively and statistically significantly related to the growth of new firms. There are positive and statistically significantly correlations among the innovation activities, which suggests that they are complementary assets. In addition, entrepreneurs’ education level is positively associated with new product development and R&D, indicating that more highly educated entrepreneurs are more likely to build innovative firms. Industry experience has a strong positive relation with interfirm alliances. This suggests that entrepreneurs’ education fosters innovation in general, while industry experience is especially helpful for initiating alliances with other firms. Previous entrepreneurial experience, leadership experience or growth ambitions are not related to initial innovation activities. This is somewhat surprising, and might indicate that some entrepreneurs are pursuing growth strategies that are not based on innovation (as defined here) and alliances. Table 1 also shows that new high-tech firms are more likely to be involved in R&D and in new product development than low-tech firms. However, once firms are involved in R&D, their technology orientation does not affect the intensity of R&D.

The overall average start-up size was 1.6 persons. Start-ups in services and wholesale were the smallest, with only slightly more than one person, while start-ups in manufacturing were the largest with an average size of slightly more than two persons. The largest start-up only employed 40 persons. Given that the minimum efficient size in manufacturing industries is said to range from 31 to more than 1000 employees (Lyons 1980), the size of these start-ups is extremely small [see also Audretsch et al. (1999) in which the average start-up size ranges from 7 to 66 employees in manufacturing industries]. Large start-ups were more likely to be involved in R&D, but not in new product development or interfirm alliances.

Given that dynamic capabilities are complex assets that are built over time, we explored whether there were sequential relations (temporal sequences) between R&D efforts and new product development or interfirm alliances. The only clear pattern found was an increasingly positive effect of R&D on new product development over time (Fig. 2). This seems to confirm the so-called linear model of innovation in which R&D produces inventions that are subsequently developed into new products. The number of firms that combined R&D activities with new product development also increases significantly over time: from 59% (T 0) to 75% (T 2) and 77% (T 3).

Sequential relations of R&D with new product development

We used OLS regression models to examine the relationships between initial R&D and firm growth (Table 2). If all firms are analysed, there was no relation between R&D and firm growth. There is a set of personal characteristics such as industry experience, growth ambitions and the age of the founder that do matter for growth when analysing the whole sample of new firms, which confirms prior studies on the effect of founder characteristics on the post-entry performance of firms (Vivarelli 2004; Bosma et al. 2004; Colombo and Grilli 2005). We also do not find evidence for the more specific effects of R&D combined with either new product development or interfirm alliances, at least not for the overall sample. This turns out to be different for the 10% fastest-growing firms: for this special group of superstars, growth seems to be spurred by R&D.Footnote 1 Next to R&D, starting with a team, and particular characteristics of the founder (having leadership and industry experience, young age), increase the growth rate of these elite growth firms.Footnote 2

R&D is related to the growth of new high-tech firms, but not to the growth of low-tech firms (Table 3). When we look at the more specific effects of R&D for new high-tech firms, we find that the main effect of R&D vanishes, in favour of a positive interaction effect of initial R&D and interfirm alliances in the second year. There is also a positive interaction effect of initial R&D and new product development in the second year, but this effect does not remain statistically significant in the regression model where both interaction effects are introduced simultaneously.

5 Discussion

Even though the population of start-ups is homogenous with respect to age and scale, this study has shown that there is a huge heterogeneity of firms in the population of start-ups (see also Santarelli and Vivarelli 2007). It is not the well-known innovative Schumpeterian entrepreneur that dominates this population. The population of new firms contains the low-tech self-employed in retail, the high-tech R&D-based start-up in manufacturing, the ambitious serial entrepreneur with a team start-up as well as the liquidity-constrained lifestyle entrepreneur. Neglecting this heterogeneity is a dangerous starting point for thinking about the implications for strategy and policy.

Next to this heterogeneity in the nature of new firms, our study shows that there is heterogeneity in the growth function of new firms: the growth of high-tech firms, low-tech firms and superstar-growth firms is driven by different mechanisms. R&D plays an important role in the growth of high-tech new firms as well as of the fastest-growing firms. The growth of low-tech firms, in contrast, seems to be driven mainly by the growth ambitions of the founder.Footnote 3 Growth ambitions seem to act as a substitute of R&D for the growth of low-tech firms. Entrepreneurs of growing high-tech firms can better be characterised as product builders, as the growth of high-tech firms seems to be an unintended side-effect of building a new or better product.

Next to the recognition of R&D in the growth of particular types of firms, this study reveals the complementary and sequential nature of different types of innovation activities. Innovation activities involve the exploration of new possibilities, which might form the input of improved exploitation of goods and services by the firm (cf. March 1991). Two faces of R&D are recognised in the literature: in the linear model of innovation, R&D enables the development of new products; but R&D could also facilitate the absorption of knowledge external to the firm (Cohen and Levinthal 1989). We find evidence of the first sequence in the early life course of firms, i.e. R&D stimulating new product development, but not for the second sequence, i.e. no effect of R&D on subsequent collaboration with external knowledge producers. However, if we look at the exploitation side, the sequence R&D and interfirm alliances turns out to strongly improve the probabilities of growth, while this is less so for R&D followed by new product development. The lack of growth effects of new product development might mean that the fruits of new product development efforts are not easy for the firm to appropriate, or that these efforts are too far from the market and are cannibalising more market-oriented activities, taking away resources that could better be invested in interfirm alliances.

6 Conclusions

The main finding of this study is that R&D plays several roles during the early life course of high-tech as well as high-growth firms. The effect of initial R&D on firm growth seems to be through increasing levels of interfirm alliances in the first post-entry years. R&D efforts enable the exploitation of external knowledge. Initial R&D also stimulates new product development later on in the life course of high-tech firms, but this does not seem to affect firm growth. Indirectly this might affect the growth of other related firms that learn from these development activities (knowledge spillovers).

These findings have several implications for innovation and entrepreneurship theory. First, knowledge exploration stimulates new product development, confirming the linear model of innovation in the context of new high-tech firms. Second, a new insight is that for new high-tech firms R&D does not seem to increase the subsequent exploration of external knowledge (the traditional absorptive capacity argument), but enables the exploitation of external knowledge in interfirm alliances. For entrepreneurship theory, our study shows that R&D and growth ambitions are substitutes for each other in the growth of new firms: the first is important for the growth of high-tech firms, while the latter is important for the growth of low-tech firms.

Our findings might also have implications for innovation and entrepreneurship policy. In order to stimulate product innovations in society, increasing R&D levels seems to be a reasonable policy objective. This study shows that R&D does not in itself seem to improve the performance of all new firms, at least not in the short to medium term. Only high-tech firms seem to grow due to early R&D investments, and this seems to be fruitful especially for firms that also initiate interfirm alliances during their early life course. In another respect, innovative start-ups might be an important focus for innovation policy as they offer new nodes in innovation networks, which adds to the density and diversity of networks in an innovation system (Meeus et al. 2008). This is one way in which knowledge spillovers are realised in the economy.

For the majority of low-tech start-ups these investments in R&D do not seem to matter for growth. Only for superstar-growth firms does increasing R&D seem to improve the growth rate. This brings us to entrepreneurship policies that aim to increase the number of high-growth start-ups. In this context, stimulating R&D is an important way to increase the growth rate of these elite-growth firms, next to triggering young individuals with leadership and industry experience to set out with a team to start a promising business. However, as these high-growth firms can only be recognised in hindsight, it is extremely difficult for policy makers to target their interventions specifically at high-growth firms. Rather, encouraging growth as an attractive goal in itself, especially among highly educated entrepreneurs, appears to be a balanced policy conclusion of this study. This includes considering the role of entrepreneurship education in secondary and post-secondary education (cf. Levie and Autio 2008; Yar et al. 2008), as well as considering how specific regulations might impair the growth willingness of individual entrepreneurs (for example employment protection; see Bosma et al. 2008).

We should be careful not to place too much weight on the role of government interventions. The insights gained in this study provide no legitimation for government intervention. First, questions about market or system failures should be answered: are there appropriability problems regarding the returns of innovation, and does constrained supply of finance lead to underinvestments in innovation? Or does a lack of organisations to ally with constrain the collaborative behaviour of start-ups? For example the funding gap for R&D investments by small and new innovative firms, especially in high-tech sectors, is well recognised in the literature (see Hall 2002; Canepa and Stoneman 2008), and for example R&D tax credits seem to be especially effective for stimulating R&D investments by small firms (Lokshin and Mohnen 2007). There is still a lack of insight into the additionality on the firm level and the costs and benefits of government interventions for society as a whole.

In this study we used fairly simple OLS regression techniques due to data restrictions. Further research should aim at collecting more longitudinal data in order to use panel data regression techniques. In addition, creating and analysing samples that are exposed to different external circumstances related to the business cycle or policy interventions, in different institutional settings, would go beyond the one-country one-period research in this study, and would provide many more insights into innovation and the growth of new firms, and the effects of innovation and entrepreneurship policy.

Notes

This is not driven by the nature of the firms, as in the group of 10-percenters the distribution of high-tech and low-tech firms is the same as in the overall sample. This adds to the evidence that high-growth firms are not overrepresented in high tech sectors (see also Henrekson and Johansson 2009b).

We also performed binary logit regression analysis with growth versus nongrowth as dependent variable (with all firms, as well as high-tech firms only). In these regressions four variables revealed to have strong effects: a positive effect of start-up size, leadership experience and growth ambitions, and a negative effect of the entrepreneur’s age. These analyses are available from the authors upon request.

Nontechnological (i.e., organisational and marketing) innovations might be relatively more important than technological innovation (stimulated by R&D and new product development) for the growth of low-tech firms. Like most other large-scale studies to date, this study has also not taken this type of innovation into account. This is a fruitful area for further research (see for example Rammer et al. 2009).

References

Acs, Z. J., & Audretsch, D. B. (1990). Innovation and small firms. Cambridge, MA: MIT Press.

Aghion, P. (2006). A primer on innovation and growth. Bruegel Policy Brief, October 2006/06, 1–8.

Arrow, K. J. (1962). Economic welfare and the allocation of resources for invention. In R. R. Nelson (Ed.), The rate and direction of inventive activity (pp. 609–626). Princeton: Princeton University Press.

Audretsch, D. B., Santarelli, E., & Vivarelli, M. (1999). Start-up size and industrial dynamics: Some evidence from Italian manufacturing. International Journal of Industrial Organization, 17, 965–999.

Baldwin, J. R., & Gellatly, G. (1998). Are there high-tech industries or only high-tech firms? Evidence from new technology-based firms. Statistics Canada Working Paper No. 120.

Baldwin, J., & Gellatly, G. (2003). Innovation strategies and performance in small firms. Cheltenham: Edward Elgar.

Baumol, W. J. (2002). The free-market innovation machine: Analyzing the growth miracle of capitalism. Princeton, NJ: Princeton University Press.

Bosma, N., Schutjens, V., & Stam, E. (2008). Determinants of growth-oriented entrepreneurship; a multilevel approach. Paper presented at the AAG Conference, Boston.

Bosma, N., Van Praag, C. M., Thurik, A. R., & De Wit, G. (2004). The value of human and social capital investments for the business performance of start-ups. Small Business Economics, 23, 227–236.

Canepa, A., & Stoneman, P. (2008). Financial constraints to innovation in the UK: Evidence from CIS2 and CIS3. Oxford Economic Papers, 60, 711–730.

Coad, A. (2009). The growth of firms: A survey of theories and empirical evidence. Cheltenham: Edward Elgar.

Coad, A., & Rao, R. (2008). Innovation and firm growth in ‘complex technology’ sectors: A quantile regression approach. Research Policy, 37, 633–648.

Cohen, W. M., & Levinthal, D. A. (1989). Innovation and learning: The two faces of R&D. The Economic Journal, 99, 569–596.

Colombo, M. G., & Grilli, L. (2005). Founders’ human capital and the growth of new technology-based firms: A competence-based view. Research Policy, 34(6), 795–816.

Cooper, A. C., Gimeno-Gascon, F. J., & Woo, C. Y. (1994). Initial human and financial capital as predictors of new venture performance. Journal of Business Venturing, 9(5), 371–395.

Dahlqvist, J., Davidsson, P., & Wiklund, J. (2000). Initial conditions as predictors of new venture performance: A replication and extension of the Cooper et al. study. Enterprise & Innovation Management Studies, 1(1), 1–17.

Davidsson, P. (2007). Strategies for dealing with heterogeneity in entrepreneurship research. Paper presented at the Academy of Management Conference, Philadelphia.

Davidsson, P., Delmar, F., & Wiklund, J. (2007). Entrepreneurship and the growth of firms. Cheltenham: Edward Elgar.

Deeds, D. L. (2001). The role of R&D intensity, technical development and absorptive capacity in creating entrepreneurial wealth in high technology start-ups. Journal of Engineering and Technology Management, 18, 29–47.

Delmar, F. (1997). Measuring growth: Methodological considerations and empirical results. In R. Donckels & A. Miettinen (Eds.), Entrepreneurship and SME research: On its way to the next millennium (pp. 199–215). Hants, UK: Ashgate.

Delmar, F., & Wiklund, J. (2008). The effect of small business managers’ growth motivation on firm growth: A longitudinal study. Entrepreneurship Theory and Practice, 32(3), 437–457.

Dosi, G. (1988). Sources, procedures, and microeconomic effects of innovation. Journal of Economic Literature, 26, 1120–1171.

Eisenhardt, K. M., & Martin, J. A. (2000). Dynamic capabilities: What are they? Strategic Management Journal, 21, 1105–1121.

Fischer, E., & Reuber, R. A. (2003). Support for rapid-growth firms: A comparison of the views of founders, government policymakers, and private sector resource providers. Journal of Small Business Management, 41(4), 346–365.

Freel, M. S. (2000). Do small innovating firms outperform non-innovators? Small Business Economics, 14(3), 195–210.

Freel, M., & Robson, P. (2004). Small firm innovation, growth and performance. Evidence from Scotland and Northern England. International Small Business Journal, 22(6), 561–575.

Fritsch, M., & Weyh, A. (2006). How large are the direct employment effects of new businesses? An empirical investigation for West Germany. Small Business Economics, 26(2–3), 245–260.

Garnsey, E. (1998). A theory of the early growth of the firm. Industrial and Corporate Change, 7, 523–556.

Garnsey, E., Stam, E., & Heffernan, P. (2006). New firm growth: Exploring processes and paths. Industry and Innovation, 13(1), 1–20.

Granstrand, O., & Sjölander, S. (1990). The acquisition of technology and small firms by large firms. Journal of Economic Behavior & Organization, 13(3), 367–386.

Hall, B. H. (2002). The financing of research and development. Oxford Review of Economic Policy, 18, 35–51.

Harhoff, D., Stahl, K., & Woywode, M. (1998). Legal form, growth and exit of West-German firms—empirical results for manufacturing, construction, trade and service industries. Journal of Industrial Economics, 46(4), 453–488.

Henrekson, M., & Johansson, D. (2009a). Competencies and institutions fostering high-growth firms. Foundations and Trends in Entrepreneurship, 5(1), 1–80.

Henrekson, M., & Johansson, D. (2009b). Gazelles as job creators—a survey and interpretation of the evidence. Small Business Economics. doi:10.1007/s11187-009-9172-z.

Hoetker, G., & Agarwal, R. (2007). Death hurts, but it isn’t fatal: The post exit diffusion of knowledge created by innovative companies. Academy of Management Journal, 50(2), 446–467.

Hölzl, W. (2009). Is the R&D behaviour of fast-growing SMEs different? Small Business Economics (this issue).

Kleinknecht, A., & Reijnen, J. O. N. (1992). Why do firms cooperate on R&D? An empirical study. Research Policy, 21, 347–360.

Levie, J., & Autio, E. (2008). A theoretical grounding and test of the GEM model. Small Business Economics, 31(3), 235–263.

Lokshin, B., & Mohnen, P. (2007). Measuring the effectiveness of R&D tax credits in the Netherlands. UNU-MERIT Working Paper 2007-025.

Lotti, F., Santarelli, E., & Vivarelli, M. (2001). The relationship between size and growth: The case of Italian newborn firms. Applied Economics Letters, 8, 451–454.

Lyons, B. (1980). A new measure of minimum efficient plant size in UK manufacturing industry. Economica, 47(185), 19–34.

March, J. (1991). Exploration and exploitation in organizational learning. Organization Science, 2(1), 101–123.

McKelvie, A., & Davidsson, P. (2009). From resource base to dynamic capabilities: An investigation of new firms. British Journal of Management, 20(s1), S63–S80.

Meeus, M. T. H., Oerlemans, L. A. G., & Kenis, P. (2008). In B. Nooteboom & E. Stam (Eds.), Micro-foundations for innovation policy (pp. 273–314). Amsterdam: Amsterdam University Press.

Niosi, J. (2003). Alliances are not enough explaining rapid growth in biotechnology firms. Research Policy, 32(5), 737–750.

Nooteboom, B. (1994). Innovation and diffusion in small firms: Theory and evidence. Small Business Economics, 6, 327–347.

Parker, S. C., Storey, D. J., & Van Witteloostuijn, A. (2005). What happens to gazelles? The importance of dynamic management strategy. Paper presented at ERIM Workshop ‘Perspectives on the Longitudinal Analysis of New Firm Growth’, Erasmus University Rotterdam, the Netherlands.

Powell, W. W., Koput, K., & Smith-Doerr, L. (1996). Interorganizational collaboration and the locus of innovation: Networks of learning in biotechnology. Administrative Science Quarterly, 41(1), 116–145.

Rammer, C., Spielkamp, A., & Czarnitzki, D. (2009). Innovation success of non-R&D performers: Substituting technology by management in small firms. Small Business Economics (this issue).

Reynolds, P. D., & White, S. B. (1997). The entrepreneurial process: Economic growth, men, women, and minorities. Westport, CT: Quorum Books.

Roper, S. (1997). Product innovation and small business growth: A comparison of the strategies of German, UK and Irish companies. Small Business Economics, 9, 523–537.

Roper, S., Du, J., & Love, J. H. (2008). Modelling the innovation value chain. Research Policy, 37, 961–977.

Rosenberg, N. (1990). Why do firms do basic research (with their own money)? Research Policy, 19(2), 165–174.

Samuelsson, M., & Davidsson, P. (2009). Does venture opportunity variation matter? Investigating systematic process differences between innovative and imitative new ventures. Small Business Economics. doi:10.1007/s11187-007-9093-7.

Santarelli, E., & Vivarelli, M. (2007). Entrepreneurship and the process of firms’ entry, survival and growth. Industrial and Corporate Change, 16, 455–488.

Schumpeter, J. (1934). The theory of economic development. An inquiry into profits, capital, credit, interest, and the business cycle. Cambridge, MA: Harvard University Press.

Smallbone, D., Baldock, R., & Burgess, S. (2002). Targeted support for high-growth start-ups: Some policy issues. Environment and Planning C, 20(2), 195–209.

Stam, E., Audretsch, D., & Meijaard, J. (2008). Renascent entrepreneurship. Journal of Evolutionary Economics, 18(3), 493–507.

Storey, D. J. (1994). Understanding the small business sector. London: Routledge.

Teece, D. J. (1986). Profiting from technological innovation: Implications for integration, collaboration, licensing and public policy. Research Policy, 15(6), 285–305.

Vivarelli, M. (2004). Are all the potential entrepreneurs so good? Small Business Economics, 23, 41–49.

Wennberg, K., & Lindqvist, G. (2009). The effects of clusters on the survival and performance of new firms. Small Business Economics. doi:10.1007/s11187-008-9123-0.

Wiklund, J., Davidsson, P., & Delmar, F. (2003). What do they think and feel about growth? An expectancy-value approach to small business managers’ attitudes toward growth. Entrepreneurship Theory and Practice, 27(3), 247–270.

Winters, R., & Stam, E. (2007). Beyond the firm: Innovation and networks of high technology SMEs. In J. M. Arauzo & M. Manjón (Eds.), Entrepreneurship, industrial location and economic growth (pp. 235–252). Cheltenham: Edward Elgar.

Wong, P. K., Lee, L., & Foo, M. D. (2008). Occupational choice: The influence of product vs. process innovation. Small Business Economics, 30(3), 267–281.

Yar, D., Wennberg, K., & Berglund, H. (2008). Creativity in entrepreneurship education. Journal of Small Business and Enterprise Development, 15(2), 304–320.

Acknowledgements

The work by Erik Stam was carried out as part of the Innovation and Productivity Grand Challenge, with financial support from the Engineering and Physical Sciences Research Council and the Economic and Social Research Council through the AIM initiative (grant number EP/C534239/1). We would like to thank Elizabeth Garnsey, Alex Coad, Riitta Katilla, Alex McKelvie, Bart Nooteboom and Marco Vivarelli for valuable comments on prior versions of this paper. We would like to thank Petra Gibcus and Jennifer Telussa for research assistance. The final responsibility for the paper remains ours.

Open Access

This article is distributed under the terms of the Creative Commons Attribution Noncommercial License which permits any noncommercial use, distribution, and reproduction in any medium, provided the original author(s) and source are credited.

Author information

Authors and Affiliations

Corresponding author

Appendix: survivor bias

Appendix: survivor bias

A fundamental problem in the analysis of firm growth is survivor bias. If the investigation is only based on surviving firms it is possible that the selection of the sample is correlated to the same variables that affect firm growth. In 1994 the panel consisted of 1,938 start-ups. For our analysis only 647 cases were used.

At the onset we tried creating an inverse Mill’s ratio variable by estimating a probit model of attrition, but we had difficulties finding variables that were significantly related to attrition, possibly since nonresponse is a more random event than firm failure. We therefore traced the differences between firms in our sample and all other firms that started in the same year but that were not included in the final sample. If these two groups would not significantly differ in their initial conditions, our findings regarding firm growth are less in danger of being obscured by survivor bias. Bivariate comparisons revealed that the groups differed only in 2 out of 16 predictor variables (p < 0.05). Older entrepreneurs were more likely to be included in the final sample. This is in contrast to our expectation that older entrepreneurs are more likely to have closed their business (voluntarily) (Harhoff et al. 1998). On the other hand, young entrepreneurs are more likely to be mobile on the labour and housing market, which causes a higher nonresponse rate among them because they are harder to trace year after year (Stam et al. 2008). New firms with low start-up capital were relatively often selected out by early closure in our sample. Given that firm survival is a necessary condition for firm growth, the importance of these variables tends to be understated in the growth analysis of survivors only. This may indicate that we understate the positive effects of the age of the entrepreneur and of start-up capital on new firm growth (given its negative effect on the chance of −100% growth, i.e. firm exit).

Rights and permissions

Open Access This is an open access article distributed under the terms of the Creative Commons Attribution Noncommercial License (https://creativecommons.org/licenses/by-nc/2.0), which permits any noncommercial use, distribution, and reproduction in any medium, provided the original author(s) and source are credited.

About this article

Cite this article

Stam, E., Wennberg, K. The roles of R&D in new firm growth. Small Bus Econ 33, 77–89 (2009). https://doi.org/10.1007/s11187-009-9183-9

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-009-9183-9