Abstract

Using a Pigovian tax to provide incentives for mine rehabilitation may be ineffective if limited liability, (judgement-proof) firms can declare themselves bankrupt to avoid the tax and rehabilitation costs. This paper introduces a model of environmental policy for mining that accounts for bankruptcy risk, profit risk, and a mobilization cost that applies if, following bankruptcy, rehabilitation is funded by the regulator or investor. The results show that making deep-pocketed investors who are never judgement-proof liable for a share of rehabilitation cost is optimal. The share of extended liability depends on the policy setting, control rights over the firm and the firm’s rent. If the firm has control rights over bankruptcy, optimal liability is at least the full cost of rehabilitation. If the investor has control rights then optimal liability is partial. Partial liability also applies when the policy is based on an insurance contract. Mobilization costs for a regulator to engage in rehabilitation mean it is socially optimal for an investor to “prop-up” a firm making moderate losses to complete mine rehabilitation.

Similar content being viewed by others

Notes

The Pigovian tax should be set equal to the marginal social cost of environmental damage. The bond service charge paid to the investor reflects the risk of bankruptcy and the bond amount is related to rehabilitation costs. If the bond amount is reduced as rehabilitation proceeds this means that the service charge acts as an incentive for rehabilitation, but if it is set at a level unrelated to the marginal social cost of environmental damage, it would tend not to be optimal. For large well-diversified firms such as BHP and Rio Tinto, the bond rate may be set at very low levels reflecting the low probability of bankruptcy and thus tends to be sub-optimal for many mining projects. For junior miners engaged in high risk projects the bond service charges are relatively high and may have a strong incentive effect.

Mine rehabilitation can be viewed as reverse mining in that it involves much of the same expertise and equipment as mining. If a mining firm is declared bankrupt and liquidated, the regulator or investor would have to contract for rehabilitation with other firms. It is expected that this would substantially increase the cost of rehabilitation over the cost to the mining firm. In Australian bankruptcy law, environmental liabilities have no special call on the funds remaining when a firm is liquidated (Sommer and Gardiner 2012). Thus these funds are not immediately available to ”prop-up” the firm whilst rehabilitation is completed.

The licence to operate assumption ensures that a solvent firm will always rehabilitate as the value of future projects and the continued support of investors is assumed to exceed the cost of rehabilitation. Regulators may also apply a form of “experience rating” where firms incur higher costs of establishing bonds if their past performance in terms of rehabilitation has been poor.

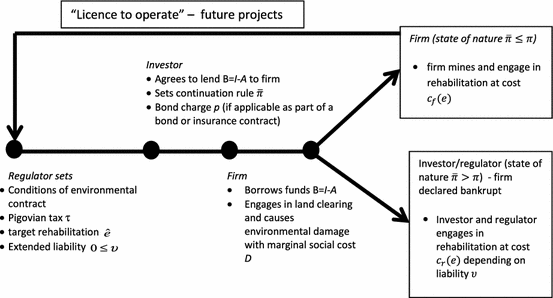

Fig. 1

Timing in the model

The paper does not consider the possibility that the failure of a mining company will have a knock-on effect, so-called snowball effect (Tirole 2010, p. 721), in terms of making investors or guarantors bankrupt.

In the US there are two main forms of bankruptcy. If bankruptcy is managed under Chapter 7 the firm’s assets are liquidated by a trustee. This is roughly equivalent to receivership. Under Chapter 11 bankruptcy rules allow for the firm to re-organise and liquidation can be avoided, this is roughly equivalent to voluntary administration as defined in the Australian law.

This describes mining for bauxite, iron ore and mineral sands where the first stage of mining is land clearing and topsoil removal. After this stage most of the environmental damage has been done.

The focus here is on internal solution, there are three notable corner point solutions, the first is where \(c_f^{\prime } (e_f )>D\,\forall e_f \in [0,1]\) and it is optimal to not undertake any rehabilitation. The second is where \(c_f^{\prime } (e_f )<D\,\forall e_f \in [0,1]\) and it is optimal to rehabilitate completely. Finally there is the case where mining projects are rejected because the environmental costs are so high they are not socially valuable.

When the shadow cost of public funds is zero, the target rehabilitation can be set at the optimal rehabilitation, therefore,\(\tau (\hat{{e}}-e)=0\). If the shadow cost of public funds is positive, the regulator has an incentive to increase the target rehabilitation as a means of generating revenue thus \(\tau (\hat{{e}}-e)>0\).

Following Tirole (2010) the interest rate i is set equal to zero. As the firm’s assets and borrowing drop out of the first order conditions then this assumption does not affect the internal solution. However, it does determine if a project is viable. The modified participation constraint is: \(H(\beta ,\bar{{\pi }},\hbox {e},\tau ,\hat{{e}})\ge (1+i)\hbox {A}\) and borrowing constraint \(F(\beta ,\bar{{\pi }},\hbox {e},\tau ,\upsilon ,\hat{{e}})\ge (1+i)\hbox {B}.\)

The maximum share of profit is adjusted downwards by the investor to account for monitoring cost (Tirole 2010).

The binding participation constraint is included here to define the rent share.

Abandoned mines are defined here as mines where either no rehabilitation has been undertaken or rehabilitation is incomplete and a solvent firm is not directly responsible for rehabilitation.

References

ASIC. (2014). Insolvency statistics—series 1A Companies entering external administration—by industry. Retrieved August 11, 2014 from http://www.asic.gov.au/asic/asic.nsf/byheadline/Insolvency+statistics+-+Series+1A?openDocument

Baron, D. P. (1985). Non-cooperative regulation of a non-localized externality. The RAND Journal of Economics, 16, 553–568.

Blanchard, O., & Tirole, J. (2008). The optimal design of unemployment insurance and unemployment protection. A first pass. Journal of the European Economic Association, 6, 45–77.

Bohm, P., & Russell, C. (1985). Comparative analysis of alternative policy instruments. In A. V. Kneese & J. L. Sweeney (Eds.), Handbook of natural resource and energy economics (Vol. 1, pp. 395–460). New York: Elsevier.

Boyd, J. (2002). Financial responsibility for environmental obligations: Are bonding and assurance rules fulfilling their promises? Research in Law and Economics, 20, 417–486.

Boyer, M., & Laffont, J.-J. (1997). Environmental risks and bank liability. European Economic Review, 41, 1427–1459.

Boyer, M., & Porrini, D. (2008). The efficient liability sharing factor for environmental disasters: Lessons for optimal insurance regulation. The Geneva Papers on Risk and Insurance: Issues and Practice, 33, 337–362.

Burton, M., Zafuda, J., & White, B. (2012). Public Preferences for Timeliness and Quality of Mine Site Rehabilitation. The Case of Bauxite Mining in Western Australia. Resources Policy, 37, 1–9.

Campbell, H. F., & Bond, K. A. (1997). The cost of public funds in Australia. Economic Record, 73, 22–34.

Che, Y. K., & Spier, K. (2008). Strategic judgment proofing. The Rand Journal of Economics, 39, 926–948.

Diamond, D. W. (1984). Financial intermediation and delegated monitoring. Review of Economic Studies, 51, 393–414.

DMP. (2010a). Department of mines petroleum bond policy. Perth, WA: Department of Mines and Petroleum.

DMP. (2010b). Policy options for mining securities in Western Australia. Perth, WA: Department of Mines and Petroleum.

DMP. (2011). Western Australia’s mining security system: Preferred option paper. Perth, WA: Department of Mines and Petroleum.

DMP. (2014). Mineral and petroleum statistics digest 2013. Perth, WA: Department of Mines and Petroleum.

Earnhart, D., & Segerson, K. (2012). The influence of financial status on the effectiveness of environmental enforcement. Journal of Public Economics, 96, 670–84.

Farzin, Y. H. (1996). Optimal pricing of environmental and natural resource use with stock externalities. Journal of Public Economics, 62, 31–57.

Gerard, D. (2000). The law and economics of reclamation bonds. Resources Policy, 26, 189–197.

Hillegeist, S. A., Keating, E. K., Cram, D. P., & Lundstedt, K. G. (2004). Assessing the probability of bankruptcy. Review of Accounting Studies, 9, 5–34.

Hiriart, Y., & Martimort, D. (2006). The benefits of extended liability. The Rand Journal of Economics, 37, 562–582.

Holmstrom, B., & Milgrom, P. (1991). Multitask principal-agent analyses: Incentive contracts, asset ownership, and job design. Journal of Law, Economics and Organization, 7(Special Issue), 25–52.

Laffont, J.-J., & Tirole, J. (1993). A theory of incentives in procurement and regulation. Cambridge, MA: MIT Press.

Mining Act WA. (1978). Retrieved January 8, 2015 from http://www.slp.wa.gov.au/pco/prod/FileStore.nsf/Documents/MRDocument:24560P/FILE/MiningAct1978-08-d0-02.pdf?OpenElement

Ormsby, W. R., Howard, H. M., & Eaton, N. W. (2003). Inventory of abandoned mine sites: Progress 1999–2002. Perth: Geological Service of Western Australia. Record 2003/9.

Perrings, C. (1989). Environmental bonds and environmental research in innovative activities. Ecological Economics, 1, 95–110.

Pigou, A. (1920). The economics of welfare. London: Macmillan.

Pitchford, R. (1995). How liable should a lender be? The case of judgment-proof firms and environmental risk. American Economic Review, 85, 1171–1186.

Shogren, J. F., Herriges, J. A., & Govindasamy, R. (1993). Limits to environmental bonds. Ecological Economics, 8, 109–133.

Solow, R. (1971). The economist’s approach to pollution and its control. Science, 173, 502–511.

Sommer, N., & Gardiner, A. (2012). Environmental securities in the mining industry: A legal framework for Western Australia. Australian Resources and Energy Law Journal, 31, 242–262.

Tirole, J. (2006). The theory of corporate finance. Princeton: Princeton University Press.

Tirole, J. (2010). From Pigou to extended liability: On the optimal taxation of externalities under imperfect financial markets. Review of Economic Studies, 77, 697–729.

Western Australian Legislation. (2012). Mining Rehabilitation Fund Act 2012. Perth, WA: Government of Western Australia State Law Publisher.

White, B., Doole, G., Pannell, D. J., & Florec, V. (2012). Optimal environmental policy design for mine rehabilitation and pollution with a risk of non-compliance due to firm insolvency. Australian Journal of Agricultural Economics, 56, 280–301.

Acknowledgments

The author gratefully acknowledges helpful suggestions from two referees, Graeme Doole, Veronique Florec, Michael Burton and David Pannell. This research was partly funded by an ARC Discovery Project: Presumed Guilty: An Economics Analysis of the Efficiency of Environmental Bonds for the WA Mining Sector (DP0988368). The paper was written while the author was on sabbatical at Stirling University and CSIRO Floreat.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendices

1.1 Appendix 1: Welfare loss due to a lenient cut-off profit

The difference between the regulator’s objective function at the socially optimal cut-off and the firm’s preferred cut-off:

Using the results that:

and that \(c_r (e)=\hbox {cm}+c_f (e),\) gives:

and simplifying:

1.2 Appendix 2: Cut-off profit where the firm determines bankruptcy

The firm’s objective function is:

A binding borrowing constraint (15) implies:

Substitute (26) into (25) for \(\beta \) and cancel to give:

Take the derivative with respect to the cut-off profit \(\bar{{\pi }}\) and set equal to zero gives:

If this is set equal to the condition for the first best cut-off profit \(\bar{{\pi }}^{s}=-c_m \) if an internal solution is feasible this implies an extended liability:

1.3 Appendix 3: Insurance contract

If the premium \(p\) is actuarially fair then \(p=G(\bar{{\pi }})\upsilon ^{In}c_r \), the firm’s objective function is:

or equivalently:

A binding borrowing constraint implies:

Substitute (29) into (28) and simplify to give:

and take the derivative with respect to the cut-off profit \(\bar{{\pi }}\) and set equal to zero gives:

Rights and permissions

About this article

Cite this article

White, B. Do control rights determine the optimal extension of liability to investors? The case of environmental policy for mines. J Regul Econ 48, 26–52 (2015). https://doi.org/10.1007/s11149-015-9276-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11149-015-9276-0