Abstract

This study investigates the dynamic relationship between economic policy uncertainty (EPU), geopolitical risks (GPR), the interaction of EPU and GPR (EPGR), and inflation in the USA, Canada, the UK, Japan, and China. We employ the continuous wavelet transform (CWT) to track the evolution of model variables and the wavelet coherence (WC) to examine the co-movement and lead-lag status of the series across different frequencies and time. To strengthen the WC, we apply the multiple wavelet coherence (MWC) to determine how good the linear combination of independent variables co-moves with inflation across various time-frequency domains. The CWT reveals heterogeneous characteristics in the evolution of each variable across frequencies. Inflation across samples shows strong variance in the short-term and medium-term while the volatility fizzles out in the long-term. For the explanatory variables, a similar pattern holds for EPU except for Japan and China, where coherence is evident in the short-term. The USA’s and Canada’s GPR reveal strong coherence in the short- and medium-term. Also, the UK and China reflect strong coherence in the short-term but weak significance in the medium-term, while Japan’s GPR reflects only strong coherence in the short-term. The EPGR shows strong variation in the short-and-medium-term in the samples except in China. The WC’s phase-difference reflects bidirectional causalities and switches in signs among series across different scales and periods in the samples, while the MWC reveals the combined intensity, strength, and significance of both EPU and GPR in predicting inflation across frequency bands among the countries. Findings also show significant co-movement among series at date-stamped periods, corroborating critical global events such as the Asian financial crisis, Global financial crisis, and COVID-19 pandemic. The paper has policy implications.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In theory, uncertainty plays an important role in the financial and economic decisions of economic agents, investors, and government policy makers and, overall, the macroeconomic fluctuations of the economy (Bernanke 1983; Bloom 2009; Bloom 2014; Pastor and Verones 2012; Baker et al. 2016). Its influence on the real economy is based on the fact that the macroeconomy is a critical factor whose changes are firmly related to policy making, market risk, and uncertainty (Stock and Watson 2012). Macroeconomic fluctuations can be reflected in a decrease in domestic investment, consumption, employment, and output, owing primarily to real options, risk aversion effects, growth options, financial frictions, and the oi-Hartman-Abel effects (Bloom 2014). It is noted that high uncertainty has an adverse impact on the real economy (Istiak 2020). The literature has shown that the 2008 GFC and the consequent recession were mainly a result of inherent financial and uncertainty shocks (Stock and Watson 2012). As such, the relationship between uncertainty and macroeconomic indicators has received special attention after the financial crisis, given that uncertainty was a trigger of the great recession (Bloom 2009; Stock and Watson 2012).

Shocks such as wars, tensions, oil price hikes, and financial panics can cause recessions and uncertainty (Bloom 2014). According to Bloom (2014), this uncertainty can, in turn, be transmitted to the real economy through many channels. One channel is through real option transmission, where firms delay investments and labor employment due to an increase in uncertainty (Bernanke 1983). In Baker et al. (2016), they find that an increase in uncertainty due to economic policy results in a decline in investment and employment in the US. Al-Thaqeb and Algharabali (2019) reported that given uncertainty, there is a delay in investment and spending decisions by individuals and firms. They further revealed that firms adopt conservative behavior during high uncertainty and, as such, reduce investment in output and employment. In examining the economic impact of uncertainty shocks, Bloom (2009) shows that uncertainty derived from economic and political shocks exerts a non-negligible influence on the business cycles from the corporate-level perspective. Through the cost of financing transmission channel, uncertainty raises the risk premium, which further spurs a rise in borrowing costs for firms. The cost of borrowing delays investment in the economy and thus has adverse effects on economic development (Antonakakis et al. 2014). The precautionary savings channel is related to the household whereby uncertainty compels individuals to reduce consumption and expenditure, and increase their savings. This behavioral pattern can exert a negative impact on the real economy (Kimbell 1989). Against these backdrops, research has shed light on the dynamic relationship between uncertainty and macroeconomic activity (Wen et al. 2019; Leduc and Liu 2020). A consensus is that high uncertainty dampens investment and growth and that the behavior of enterprises or investors is influenced by economic policy (Antonakakis et al. 2014).

A single macroeconomic indicator of prime consideration for this study is inflation. While studies have focused on the relationship between uncertainty and the macroeconomy, the empirical assessment of the dynamic relationship between uncertainty measures and inflation is still in its infancy and has not yet reached a consensus conclusion (Jones and Olson 2013; Leduc and Liu 2016). Understanding the dynamics of inflation and uncertainty measures is important for monetary policy analyses. It is relevant in shaping monetary policy responses during highly uncertain periods in ensuring appropriate policy action and bringing inflation to target given the exposure of financial institutions to various amplification channels and the resilience of the financial sector amidst uncertainty shocks. Uncertainty due to demand and supply side shocks may affect inflation volatility. A positive global demand shock is assumed to raise output, inflation, oil price growth, domestic interest rates and appreciate exchange rates, particularly in the G7 and the Euro area (Ha et al. 2019). It is also revealed that a negative non-commodity supply shock raises input costs, dwindles output, and raises inflation, while a positive technology shock increases output but reduces inflation, domestic interest rates, and money demand (Charnavoki and Dolado 2014). A positive supply shock raises output, reduces inflation, and appreciates exchange rates. A positive oil price shock portends positive cost (commodity price) shocks, dampens output and increases commodity prices and inflation, while a negative oil price supply shocks raise oil prices, dwindles output and oil consumption (Charnavoki and Dolado 2014; Ha et al. 2019). According to studies, political instability further leads to lower output and investment, which reduces taxable assets and income required to meet fiscal policy obligations. Improving government revenue can make it optimal for fiscal authorities to raise inflation taxes, while tax evasion and tax collection costs are likely to be heightened in an emerging market and politically unstable environment (Aisen and Veiga 2006). As such, geopolitical instability may trigger an increment in optimal inflation tax and large fiscal deficits, with a resultant volatile inflationary consequence in emerging markets with less developed financial markets. Generally, uncertainty shocks tend to undermine the competence of monetary and fiscal policy makers and diminish their resilience to accommodate and cushion shock effects, causing macroeconomic disequilibrium that is characterized by inflationary trends.

Literature has shown that inflation volatility is characterized by demand and supply shocks, oil price shocks, fiscal policy and exchange rate variations (Charnavoki and Dolado 2014). However, a considerable gap in the literature borders on the existing dynamics between news-based uncertainty measures and inflation. Selecting the appropriate index for measuring uncertainty has become a focal point in recent literature (Wen et al. 2019). In this study, we applied the economic policy uncertainty (EPU) index of Baker et al. (2016) and the geopolitical risk (GPR) index of Caldara and Iacoviello (2022). EPU refers to a non-zero probability of economic (monetary, fiscal, or regulatory) policy changes that influence the decision-making pattern of investors and consumers (Baker et al. 2016). GPR indicates geopolitical occurrences like terrorism, local and regional political instability, political violence, coups d’état, territorial disputes, and war (Caldara and Iacoviello 2022; Caldara et al. 2022) trigger uncertainty. Uncertainty due to inherent policy fluctuations can affect economic agents as their cash flows are adversely affected by negative government actions, and alter their portfolio. Elevated uncertainty has been linked to adverse impacts on economic activity via the “demand” and “supply” sides. From the “demand” side, uncertainty regarding possible outcomes from intended or unintended policy instability of the government and adverse geopolitical happenings may influence macroeconomic activity by delaying enterprises’ investment and hiring, thereby eroding households’ confidence and restraining financial conditions (Caldara et al. 2022). On the “supply” side, heightened uncertainty (i.e., terrorism and wars) dampens physical and human capital accumulation, undermines efficient resource utilization, raises capital flows, reduces the attractiveness of investment, and truncates global supply chains. While the “demand” and “supply” shock dynamics are detrimental to economic activity, their combined impact on inflation is rather unresolved and ambiguous given that the inflationary effects on the supply side may counteract the deflationary effects resulting from the slacking aggregate demand (Caldara et al. 2022).

Against this backdrop, this study investigates the dynamic interactions between EPU, GPR, and inflation under a time and frequency framework. Unlike previous studies, we further used a single variable through an interaction term (EPGR) to measure the simultaneous dynamics of both uncertainty indexes on inflation. While studies have examined the nexus between uncertainty measures and the macroeconomy (Stock and Watson 2012; Bloom 2014; Antonakakis et al. 2014; Wen et al. 2019; Leduc and Liu 2020), trade (Caldara et al. 2019), food, stock and precious metal prices (Pastor and Verones 2012; Batabyl and Kilian 2021; Yilanci and Kilci et al. 2021); corporate risks (Zhang et al. 2021), renewable energy and carbon emissions (Khan and Su 2022; Li et al. 2022), there is little empirical evidence on the dynamics of inflation and uncertainty measures using the wavelet-based approach. This study employs the continuous wavelet transform (CWT) to track the evolution of model variables across frequency bands and periods. The wavelet coherence (WC) is used to capture the co-movement and the lead and lag status between the series and to aid in analyzing the signs of the causality, which offers a comprehensive picture of the relationship, while the multiple wavelet coherence (MWC) is further employed to examine how well the linear combination of independent variables co-moves with inflation across time–frequency domains.

The potency of the wavelet approach is empirically testable in the literature (Goupillaud et al. 1984; Torrence and Compo 1998; Ng and Chan 2012). The wavelet approach allows us to analyze the nexus between the selected variables within the time and frequency, i.e., investment horizons. Given the variations in risk profiles, heterogeneous expectations, and diverse risk-making preferences, the behavioral patterns of market participants may vary in reaction to the dynamics of uncertainty and inflation. Inflation induced by demand and supply shocks, oil price shocks, policy uncertainty, and wars may be perceived differently by market traders. During elevated inflation, holders of fixed assets with long-term cash flows may perceive high inflation as bad news, while holders of commodities with adjustable cash flows may perceive the same news as good. Their selling decisions may also differ on whether they perceive inflation as transitory or permanent. “Bad” news such as war may induce buying or selling perceptions of traders. The economic impacts of wars may be heterogeneous across types of industrial participants. Goods-producing industries could be affected more by wars, while service industries may be more insulated against global supply disruptions (Caldara et al. 2022). Typically, the market is a complex system composed of diverse stakeholders wherein policymakers, whose objective is to maintain equilibrium, tend to be concerned about long term trends while speculators deal in short-term horizons. As a result, time series data derived from the economic activity process are influenced by a variety of components operating at various time and frequency. We therefore hypothesize that the dynamics of uncertainty and inflation will differ across time and frequency. We adopt the wavelet approach based on its advantage in uncovering latent processes with varying cyclical patterns, trends, lead-lag interactions, and asymmetric characteristics of time series (Chakrabarty et al. 2015). The Wavelet approach also suffices when the interactive lead-lag nexus between series is non-linear since the asymmetric effect may be adduced to investors’ heterogeneous expectations across investment horizons.

This paper adds to the literature in several ways. The study investigates the nexus between uncertainty and inflation in a sample of global players (USA, Canada, the UK, Japan, and China) using the most representative proxies of news-based uncertainty measures of EPU and GPR in an asymmetric framework. We used a single variable through an interaction term (EPGR) to measure the simultaneous dynamics of both uncertainty indexes on inflation. We applied the wavelet-based approaches of CWT, WC, and MWC given their potencies in analyzing the dynamics among model return series under a time-frequency framework. We express data in their return form to detect more information about macroeconomic happenings in the real economy. Defining high-frequency series in their returns ensures more details about small fluctuations in asset and commodity prices and common behavioral changes. As a result, because the dataset covers a period of critical global crises, using these data could better capture dynamics among series. These periods thus suggest a horizon when the connection between the series has heterogeneously evolved. The choice of the selected economies is informed by the fact that the US, Canada, the UK, and Japan constitute the G7 bloc, while China is the world’s second-largest economy and a leading emerging market. These economies are regarded as large and open, and, as such, macroeconomic shocks and their monetary policy responses to shocks, e.g., FED and FMOC interest rate hikes in response to inflation, exert much influence on the global economy. The IMF (2012) shows that uncertainty in the US and Europe contributed immensely to the GFC and the sluggish recovery thereafter. The economic systems of these countries indeed show remarkable variations in terms of policy interventions, economic reforms, and financial regulation.

The results of this study show heterogeneous characteristics in the evolution of each variable across frequencies. Inflation across the samples shows strong variance in the short-term and medium-term while the volatility fizzles out in the long-term. For the explanatory variables, a similar pattern holds for EPU except for Japan and China, where coherence is evident in the short-term. The USA’s and Canada’s GPR reveal strong volatility in the short- and medium-term. Also, the UK and China reflect strong coherence in the short-term but weak significance in the medium-term, while Japan’s GPR reflects only strong coherence in the short-term. The EPGR shows strong volatility in the short-and-medium-term in the USA, Canada, the UK, and Japan, except in China. The WC’s phase-difference reflects bidirectional causalities and switches in signs among series across different scales and periods in the samples. The MWC reveals the combined intensity, strength, and significance of both EPU and GPR in predicting inflation across frequency bands among the countries. Findings show significant co-movement among series at date-stamped periods, corroborating critical global events such as the AFC, GFC, and COVID-19 pandemic.

The remaining contents of the paper are structured as follows: Sect. 2 reviews the literature; Sect. 3 explains the methodology; Sect. 4 shows the data employed; Sect. 5 interprets the findings; and Sect. 6 concludes and provides policy implications.

2 Literature review

Theoretically, the literature has shown that uncertainty could be transmitted to the real economy essentially through the real option, cost of financing, and precautionary saving channels (Bernanke 1983; Bloom 2014; Baker et al. 2016; Al-Thaqeb and Algharabah 2019; Leduc and Liu 2020), affecting the “demand” and “supply” sides of the economy. Thereafter, studies have examined the nexus between uncertainty measures and the macroeconomy with a general consensus that heightened uncertainty adversely impacts the economy (Stock and Watson 2012; Pastor and Verones 2012; Bloom 2014; Antonakakis et al. 2014; Baker et al. 2016; Leduc and Liu 2020; Caldara et al. 2022). Other recent studies have examined the linkages between policy uncertainty and other macroeconomic indicators such as food, stock and precious metal prices (Wen et al. 2021; Batabyl and Kilian 2021; Yilanci and Kilci 2021), corporate risks (Zhang et al. 2021), renewable energy, and carbon emissions (Khan and Su 2022; Li et al. 2022). Al-Thaqeb and Algharabah (2019) provided a detailed review of EPU, concluding that policy uncertainty has a non-negligible impact on investment decisions and consumer spending, with significant local and global spillover effects.

However, the assessment of the relationship between uncertainty due to economic and political shocks and inflation is still nascent and has not yet reached a conclusion (Jones and Olson 2013; Leduc and Liu 2016; Meinen and Roeche 2018; Hague and Magnusson 2021; Caldara et al. 2022). The admixture could be attributed to the fact that the inflationary effects on the supply side may offset the deflationary effects of slacking aggregate demand (Caldara et al. 2022). While literature has further shown that inflation volatility can be induced by demand and supply shocks, oil price shocks, fiscal policy and exchange rate variations (Charnavoki and Dolado 2014), the nexus of uncertainties and inflation dynamics has been said to be theoretically mixed (Hague and Magnusson 2021). Increased uncertainty makes firms delay their spending and investment plans. The real-options effects exert a negative impact of uncertainty on prices since, in the long-term, firms cut production due to weak demand, causing downward pressure on inflation (Bloom 2014). While firms may find it optimal to raise prices in reaction to contractionary uncertainty to avoid the risk of being stuck with lower prices,Footnote 1 Through portfolio rebalancing, shocks from EPU and geopolitical-threats may be transmitted to inflation. The preceding reflects the positive causal effect of policy uncertainty and risks on price levels, given the investment driving tendency of commodity price returns. Inflation can also heighten policy uncertainty. High inflation spurs uncertainty in households’ spending and firms’ investment decisions. Uncertainty shocks trigger energy-price increases, disrupt supply chains, push CPI higher, and exacerbate inflationary pressures. High geopolitical instability can also spur higher inflation (Aisen and Veiga 2006), whereas high inflation also generates inefficiencies, dampens society’s welfare, and triggers geopolitical tensions: a reflection of bidirectional causality and feedback dynamics.

From another empirical perspective, Leduc and Liu (2016) show that heightened uncertainty raises unemployment, lowers spending and consumption, and exerts a deflationary impact on general price levels, creating a demand shock in the macroeconomy. Evidence further shows that the predictive tendency of future uncertainty can change over time depending on time horizons and data range (Al-Thaqeb and Algharabali 2019). Istiak and Alam (2019) opine that EPU and oil prices have a non-negligible effect on inflation expectations. Their findings further show asymmetric effects, in which the impacts of uncertainty or increased oil prices on inflation may differ depending on whether the period precedes or follows a financial crisis. Mumtaz and Theodoridis (2018) also observe inflationary impacts for the entire post-war world—II period. Jones and Olson (2013) reveal that the relationship between uncertainty and inflation changed from positive to negative during the mid-to late 1990s, a reflection of asymmetry. Hague and Magnusson's (2021) TVP-VAR further indicates that inflation is negative in the post-WWII period. While Athari et al. (2021) show the heterogeneous reaction of Japan’s inflation to EPU, Meinen and Roeche’s (2018) SVAR approach shows the ambiguous response of inflation to uncertainty. In the UK, Hunt (2007) shows that globalization, pound appreciation, and public goods demands trigger inflation, while Michaelis and Watzka (2017) and Hausman and Wieland (2014) argue the effectiveness of “Abenomics” policy in increasing inflation and long-run inflation expectations. Meanwhile, Arbatli et al. (2017) opine that policy uncertainty portends challenges for Japan’s quest to revamp growth, minimize risks of deflation, lift wages, and improve overall economic performance. Day () further shows that the depreciation of the Renminbi may also have contributed to additional inflationary pressure. Using the SVAR approach, Caldara et al. (2022) show that global geopolitical risk induced u2017ncertainty triggers inflation, with the inflationary impact of higher commodity prices and supply chain disruptions more than offsetting the deflationary influence of lower consumer sentiment and tighter financial conditions. They show that country-specific GPRs are inflationary, with a larger impact in countries with large military spending, public debt, and weak exchange rates.

This current study takes a different look at the dynamics of uncertainty measures and inflation via the wavelet-based approach. We employed EPU and GPR, which are the most representative proxies of news-based uncertainty measures (Baker et al. 2016; Caldara and Iacoviello, 2022); and an interactive term, EPGR, to measure the simultaneous dynamics of both uncertainty indexes on inflation. We specifically employed the CWT, WC, and MWC given their advantages in accommodating heterogeneity, nonlinearity, outliers, and time and frequency variations of time series, which may be linked to investors’ heterogeneous expectations across long, medium, and short horizons.

3 Methodology and data

The wavelet methodology has been widely used in geophysics and more recently in economics and finance (Torrence and Compo 1998; Wu et al. 2020). The wavelet approach is advantageous in time analysis given that: (a) it relaxes the assumption of stationarity; (b) it accommodates time-series with non-normal distribution. (c) It effectively captures time-localized events (d) It analyzes time-series from time and frequency perspectives (d) It effectively shows the strength and direction of association and differentiates between short, medium, and long-term relationships across time (e) It accommodates non-linear relationships typical of time series data (f) It tracks evolution and co-movements among series efficiently (g) It captures bi-directional (lead-lag) among series at different time and frequency combinations (Chakrabarty et al., 2015).

3.1 Continuous wavelet transform and wavelet coherence

Following Wu et al. (2020), we specifically used the wavelet coherence under the Morlet specification defined as follows:

where \(s^{ - 1/2}\) is the normalization factor, which ensures that the variance of \(\left\| {\psi_{u,s} \left( t \right)} \right\|^{2}\) sums up to unity; the precise position of the wavelet is shown by \(u\)(the location parameter); the scale dilation parameter is depicted as \(s\) which shows how the wavelet is stretched or dilated. The Morlet wavelet is defined as follows:

where the central frequency of the wavelet is denoted as \(w_{0}\). Following Rua and Nunes (2009), with convolution applied to a discrete sequence and a scaled and translated wavelet, the CWT is given as:

We derived \(W_{x} \left( {u,s} \right)\) by projecting the specific wavelet \(\psi \left( . \right)\) onto the selected time series. A merit of CWT is that it is able to decompose and reconstruct the function \(x\left( t \right) \in L^{2} \left( {\mathbb{R}} \right)\):

The power spectrum analysis can be derived using Eq. (4), with the specification of the variance being

The red noise background spectrum is used to define the null hypothesis in significance tests for peaks in the wavelet power spectrum. The red-noise background spectrum is calculated using the Monte Carlo simulations (Torrence and Compo 1998). Thus, the wavelet power spectrum distribution for each time \(n\) and scale \(s\) can be expressed as follows:

where the mean spectrum at Fourier frequency \(f\) is denoted by \(P_{f}\). The wavelet scale \(s\) corresponds to the Fourier frequency \(\left( {s \approx 1/f} \right)\). The real wavelet has \(v = 1\), and the complex wavelet \(v = 2\). The variance of the corresponding variable is depicted by \(\mathop \delta \nolimits_{x}^{2}\). Following Rua et al. (2009), we define the cross-wavelet transform of two time series \(\left( X \right)\) and \(\left( Y \right)\) as follows:

where \(\mathop W\nolimits_{n}^{X} \left( s \right)\) and \(\mathop W\nolimits_{n}^{Y} \left( s \right)\) are individual wavelet spectra, \(u\) depicts the position, \(s\) denotes the scale, and \(*\) indicates complex conjugation. The cross-wavelet transform presents the area in time-space with high common power. Hence, \(\mathop W\nolimits_{n}^{Y*} \left( s \right)\) is the complex conjugate of \(\mathop W\nolimits_{n}^{Y} \left( s \right)\). The cross-wavelet power \(\left| {W_{n}^{XY} \left( s \right)} \right|\) measures the mutual local covariance on each scale. Therefore, the WC of the two-time series \(x = \left\{ {x_{n} } \right\}\) and \(y = \left\{ {y_{n} } \right\}\) is explained by searching the frequency bands and time intervals in which they co-vary. This provides a useful tool for detecting co-movement between the uncertainty indexes and inflation. WC is defined as the squared absolute value of normalizing a wavelet cross spectrum to a single wavelet power spectrum (Grinsted et al. 2004). Therefore, we defined the squared wavelet coefficient as follows:

where \(S\) denotes the smoothing parameter, which balances resolution and significance. Also, the bias problem in the wavelet power spectrum and wavelet cross-spectrum is eliminated by the normalizing function of the wavelet coherence. The wavelet coefficient meets the inequality \(0 \le R^{2} \left( {x,y} \right) \le 1\). A value near zero shows a weak correlation while a value close to 1 depicts a strong correlation. According to Torrence and Compo (1998), the phase pattern for wavelet shows any lead and lag relationship between two time series that can be depicted as follows:

\(\phi_{xy}\) describes the phase difference. Where \(\Im\) and \(\Re\) are the imaginary and real parts of the smoothed cross-wavelet transform, respectively. In the WC map, directional arrows are employed to distinguish different phase patterns. When arrows point to the right (left), the series i.e., \(x(t)\) and \(y(t)\) are in-phase (anti-phase). When the series are in-phase, it shows that they follow the same path, and anti-phase illustrates that they move in the opposite direction. As such, in this paper, a right-down or left-up pointed arrow indicates that EPU, GPR and EPGR returns are leading, while a right-up or left-down arrow shows that inflation returns is leading (see Table 7). The horizontal line in the WC graph shows the time dimension, while the vertical line indicates the frequency. The red (blue) color shows a strong (weak) nexus between series.

3.2 Multiple wavelet coherence

The simplest way of understanding the MWC is to compare it with the coefficient of multiple correlation. Similar to the WC, MWC studies the co-movement (coherence) of the combination of two independent variables on a dependent variable; that is, \(x\) and \(y\) on \(z\)(Ng and Chan 2012). Following Wu et al. (2020), the MWC is shown below:

where \(R_{m}^{2}\) depicts the dependence of \(z\) on the linear combination of two other independent variables of interest \(x\) and \(y\) in a time-frequency space. In this paper, \(x\) and \(y\) depict EPU and GPR returns while \(z\) is inflation returns. Again, a Monte Carlo method is employed to calculate the significance levels.

4 Data

This section describes the data and its stochastic properties. The study uses monthly data on economic policy uncertainty (EPU), geopolitical risk (GPR), and an interaction term, EPGR, that measures the simultaneous effects of both EPU and GPR. Monthly data on CPI (inflation) is employed. Though the base year differs, all data ends at 2021:M05. The scope is the USA and Canada (1985: M01-2021: M05), the UK and China (1997: M01-2021: M05), and Japan (1987: M01-2021: M05). We employed two of the most representative measures of uncertainty: the EPU index developed by Baker et al. (2016) and the GPR index developed by Caldara and Iacoviello (2022). We sourced data on EPU from https://www.policyuncertainty.com/. The updated data on the GPR is sourced from https://www.matteoiacoviello.com/gpr.htm. The Federal Reserve Economic Data (FRED) presents data on CPI (https://fred.stlouisfed.org).

Baker et al. (2016) developed a news-based EPU measure. According to the authors, the growth weighted average of 21 country indices of EPU makes up the computation of the EPU index. The index typically consists of newspaper repositories from the “Access World News Bank Service.” The data is sourced through an electronic text searching process that fetches articles containing terms such as economics, deficit, uncertainty, monetary policy, regulation, legislation, White House, Federal Reserve, or Congress.

Similarly, the news-based GPR index was developed by Caldara and Iacoviello (2022). According to the scholars, the updated version of the GPR is calculated by using electronic text searches of key terms related to geopolitical tensions in 10 revered daily newspapers. The authors’ search procedure comprises eight groups of war-related events and geopolitical tension: Group 1 discusses geopolitical tensions; Group 2 defines terms like “peace-threats;” and Groups 3 and 4 discuss military buildups and nuclear threats. Text in Groups 5 and 6 corresponds to terrorist threats and the start of wars.Footnote 2 Groups 7 and 8 identify terrorism and war escalation. Generally, EPU (GPR) is related to the real economy (wars). The EPGR, which denotes high levels of policy uncertainty and geopolitical risks, represents the interaction of the EPU and GPR.

In Fig. 1, we plot the country-specific GPR and EPU indices and inflation for each sample. In the USA, the GPR reflects some notable peak periods (August-1990, January-1991, September-2001, and March-2003), corroborating the early-1990s Gulf War, the 1990s oil price shock, which resulted in inflation, MPR hikes, weak demand, and consumer pessimism, and the early-1990s recession. The highest peaks were observed in the 9/11 attacks and the 2nd Gulf War. The EPU date-stamps September-2001, October-2008, August-2011, and April-2020. These periods corroborate the collapse of the speculative dot-com bubbles; uncertainty occasioned by the 9/11 terror attacks weakened investments; and contributed to the early-2000s recession. We also identify periods within the great recessions of 2007–2009, the COVID-19 pandemic and the Trump election. Given the highly synchronized status of the American and Canadian economies, we observe similar oscillatory peaks of the GPR in August-1990, January-1991, September-2001, and March-2003.

Time patterns of EPU, GPR, and Inflation. The left and right panel for each country depicts the time trend of the EPU-GPR and inflation (INF) respectively

The EPU index recorded continuously flat trends before it peaked in October-2008 and August-2020. October-2008 matches the recession recorded in the Canadian economy based on the uncertainty from the subprime mortgage crisis and the collapse of housing bubbles in the United-States. Hinged on the highly synchronized status of the two economies, shocks within the US economy resulted in a rise in interest rates and a sharp decline in consumer spending and business investment. The global outbreak of the COVID-19 pandemic, the Russia-Saudi Arabia oil price war, the foreign travel bans, and the corporate debt bubble also contributed to a decline in economic activity and an abrupt steep drop in jobs. The COVID-19 pandemic represents the highest peak in the Canadian EPU index.

The GPR for the UK and Japan shows three peak periods: early-1991, September-2001, and the US invasion of Iraq in March-2003, while the UK uncertainty recorded its highest peak during the European debt crisis. The highest EPU peak in Japan was observed in the mid-1990s AFC, when Japan recorded an economic decline, a collapse of real estate and equity markets, further heightened by an overheated economy, uncontrolled money supply, and credit-expansion. The GPR and EPU indexes for China show two peak periods. We date-stamp May-2018 and August-2017 while the policy uncertainty index falls within the inception of COVID-19 in China and the global lockdown, debt, and liquidity crises in 2020.

During these periods, fluctuations in the real economy affected development severely and heightened policy uncertainty. These events influence general price levels, inflation expectations, and the behavioral changes of investors and market participants in the commodity markets. Generally, when there is a sharp rise in EPU and GPR, uncertainty increases commodity prices and inflation (Caldara and Iacoviello 2022). The paper further observes the upward inflationary trends in the selected countries.Footnote 3

We apply log returns through the \(R_{t} = 100 \times In(P_{t} /P_{t - 1} )\) in order to understand macroeconomic happenings and dynamics among series. As such, monthly returns for time t, \(R_{t}\), are calculated using the monthly average price on month t \(\left( {P_{t} } \right)\) and t−1 \(\left( {P_{t - 1} } \right)\).

Table 1 shows the descriptive statistics. While the UK and Canada’s EPU record closely identical average values with similar standard deviation (SD), comparatively, the country-specific EPU of China shows the highest mean value with a corresponding high volatility as reflected in its high standard deviation, while the EPU of Japan reflects the lowest mean and volatility. Although we observed a lower mean of EPU for Japan and the USA, the SD value of the EPU for the USA outweighs Japan. The volatile and oscillatory nature of the EPU is further buttressed by the Jacque Bera normality tests, where the null hypothesis of normal distribution is strongly rejected. Indeed, the skewness and kurtosis of the EPU across countries do not reach the point-specific values of 0 and 3. While the USA and Canada’s EPU are positively skewed, other countries' EPU show leftward skewness. However, EPU across countries is leptokurtic.

The country-specific value of GPR shows that China’s GPR has the highest mean while the USA reveals a negative value and the lowest standard deviation (i.e., volatility). Although the GPR for the UK and Canada show similar means, the Canadians' GPR is the most volatile. In addition, the JB statistic reflects the nonnormality of the GPR across countries coupled with positive skewness and kurtosis exceeding 3. Meanwhile, the EPGR across samples generally shows the strongest volatility among other model series given that it measures the simultaneously dynamics of both EPU and GPR. Its JB statistics, skewness, and kurtosis also confirm the strong oscillatory behavior.

The mean of the inflation in the US, Canada, and China displays similar values. However, the SD of China’s inflation shows that it is the most volatile. The JB statistic, skewness, and kurtosis all reflect that inflation across countries is far from normal. The UK’s inflation is the least volatile, corroborating its low mean. Further, inflation in Canada, Japan, and China exhibits positive skewness while the UK and US inflation are leftward skewed. Meanwhile, inflation across countries is leptokurtic with values above 3. The high kurtosis shows that they are heavily tailed relative to a normal distribution. These findings generally imply the stochastic properties and oscillatory characteristics of series, thus reinforcing the choice of the wavelet approach.

We further examine the unit root of the returns. The study employs the ADF and ZA structural break tests, accommodating both intercept and trend. In Table 2, the ADF results show that virtually all series exhibit mean reversion given that they have been log transformed to capture macroeconomic happenings and variables’ responses. The ZA unit root break test date stamps some notable break dates that are concomitant to global events such as the early 1990s recession, the 1st Gulf War, the 1990s AFC, the Dotcom bubbles in the early 2000s, the 2003 2nd Gulf War, the 2007 sub-prime mortgage crisis, the 2008 GFC, and the 2014 energy crisis.

These stochastic properties make the traditional time-domain causality analysis inaccurate. Therefore, it is clear that financial and economic datasets are likely to record structural breaks, outliers, nonlinearity, and heterogeneous behavior typical of the financial market and the macroeconomy, speculative bubbles, and are unlikely to be time-invariant. The traditional causal outcomes with fixed parameters may not suffice amongst structural breaks. Thus, the stochastic properties of the return’s series support the usage of the wavelet.

5 Results

5.1 Continuous wavelet transform

In this section, we employ the CWT since it suffices in identifying and isolating periodic signals while it also provides a balance between localization of time/frequency and better trade-offs between the detection of volatility/discontinuities. We apply the formulae \((2^{n} ,n = 1,2,3...)\) to decompose the series into different frequency-bands that represent short-, medium- and long-term. The horizontal axis of the CWT graph represents the time dimension and the vertical axis depicts frequency. The frequency bands ranges from 2 to 128 months-scales in the USA, Canada and Japan and 2–64 months scales in the UK and China. The coverage runs from 1985 to 2021 in the USA and Canada, from 1987 to 2021 in Japan, and from 1997 to 2021 in the UK and China. The frequency scales are divided into 2–8 months-scale (short-term), 8–32 months-scale (medium-term) and above 32 months scale (long-term).

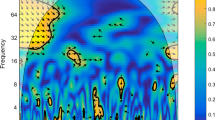

We first display the evolution of inflation for each sample in Fig. 2 (Table 3), followed by the explanatory series of EPU in Fig. 3 (Table 4), GPR in Fig. 4 (Table 5), and EPGR in Fig. 5 (Table 6). The red or hot regions (the blue or cold regions) show strong (weak) variation or intensity of the series. The black contour shows significance at the 5% level based on the Monte Carlo simulations with randomized surrogate time series. Meanwhile, a solid curved line depicts zones within the cone of influence (COI) which are affected by edge effects, while blue or cold islands outside the COI are insignificant (Torrence and Compo 1998).

The plots of CWT for inflation. The cross-hatch indicates regions within the COI and the thick black contour indicates 95% confidence level

The plots of CWT for EPU. The cross-hatch shows regions within the COI and the thick black contour indicates 95% confidence level

The plots of CWT for GPR. The cross-hatch shows regions within the COI and the thick black contour indicates 95% confidence level

The plots of CWT for EPGR. The cross-hatch shows regions within the COI and the thick black contour indicates 95% confidence level

Figure 2 (Table 3) shows that inflation in the sample exhibits high evolution of variances and high-power regions, typically in the 2–8 month and 8–32 month scale. The graph depicts how inflation reacts to macroeconomic events and how it fluctuates dramatically over short and medium time horizons. These results reflect heterogeneity and thus show that the variance in inflation is associated with both time and frequency.

The evolution of inflation in the USA shows heterogeneous tendencies as high coherence and impulse were observed in the short-term and medium-term but decay in the long term. Within this frequency frame, the price level exhibits varying spectral shapes. In the short term (2–8 month frequency band), we notice significant variances within the mid-1980s, 1999, early-2000s, 2007–2011, 2013–2015, and 2021. Essentially, in the 1980s and mid-1980s, US monetary policy underwent changes, as a result of which inflation oscillated significantly and exhibited long-lasting and mild increases. During these horizons and periods, alterations in monetary policy and large economic shocks exerted huge effects on inflation. The CWT shows an episodic drop in the strong coherence within the sub-sample from 1990 to 1997. However, after the AFC, we see high inflation volatility, which is exacerbated by the early 2000s dotcom bubble bust and the 9/11 shocks. In response to the early 2000s recession, the FED’s monetary policy adjustment by reducing the interest rate to rejig the economy resulted in higher inflation expectations. We also detect strong variations during the GFC, the rising gas prices in 2008, 2013–2015 rising energy prices, and the global energy crisis in 2021 given the pandemic. These shocks influence general price levels. In the medium term, significant volatility was observed in 2006–2011. These periods mark when the real estate market froze, the financial crisis began, and the quantitative easing (QE) programs were adopted to counteract the crisis and boost the economy. In particular, the QE embarked upon in 2008 and 2010 to revamp the economy sparked inflation expectations and strong variation/volatility in prices.

The Canadian inflation evolution similarly show some heterogeneity as small islands of coherence were observed in the short-term and medium-term. However, we cannot date-stamp significance above the 32 month-scale. Within the small zones of coherence, the orange color-pallet shows marginally strong variance reflecting the inflation targeting policy of the Bank of Canada. Unlike the USA whose inflation targeting options were implicit before 2012, an explicit inflation target in Canada was formalized in 1991 to ensure price stability and to take preemptive measures in reacting to inflation expectations. The inflation control target was 2% midpoint and this maintained persistence in 2006–2011 given a five-year life span to sustain the 2% inflation midpoint. Given these monetary policy measures, we date-stamp inflation evolution in periods such as the mid-1980s, early-1990s, early-2000s, the 2008-GFC, and the 2021 global lockdown in the short-and-medium frequency bands.

The U.K. inflation show high variances in the 2–8- and 8–32-months frequency scale at different episodes. In the short term, we identify periods of significant-volatility in 2007–2008, 2009, and 2012–2013. The longest island of impulses in the short term is explicit within the 1998–2004. The only zone of coherence in the medium-term falls within the GFC episode from 2008 to 2010. Historically, the sequel to the post war period shows that the U.K. economy experienced strong growth with moderate inflation. The 1970s oil price shock and the phenomenon of wage-inflation spiral constituted the pace of price level within the period. In the 1980s (1989), given the long-term growth episode of the U.K., the phenomenon of the demand-pull inflation becomes more explicit. In the early-1990s (1992), the focal point of the United Kingdom’s monetary framework is an annual inflation target of 2.5 percent and to contain inflation expectation. However, the U.K. operated within the inflation target range of 1–4 percent rather than a point target. Hunt (2007) also opines that the globalization, appreciation of the Pound, and the demand for public goods are factors triggering inflation. The country particularly recorded cost push inflation caused by rising oil prices, devaluation of the pound, and higher taxes within the sub-prime mortgage crisis, the-GFC and post-GFC periods.

In Japan, we highlight islands of significant coherence in the short-and-medium-term. Within the 2–8 month horizon, we observe three episodes of volatility in 1987–1992, 1993–1994, and 1996–2000, coupled with yearly coherence in 1994, 1995, 2000, 2007, and 2016. We further date-stamp strong-oscillation during 2009–2010 and 2016 in the medium-term. However, we cannot establish volatility above the 32 month-scale. Specifically, we date-stamped the mid-1990s AFC when Japan recorded an economic downturn, the collapse of real estate and equity markets, further heightened by overheated economic activity, uncontrolled money supply, and credit expansion. These expansionary policies trigger inflation expectations and a general price level. Although Japan records deflation over the decades, the financial crisis portends adverse shock on the real economy thus impacting inflation. Sequel to the “Abenomics” packages, the monetary policy authorities of Japan set a 2 percent inflation target to be achieved by 2015 and to increase inflation expectations. Michaelis and Watzka (2017) and Hausman and Wieland (2014) argue the effectiveness of “Abenomics” policy in increasing long-run inflation expectations.

Consistent with other samples, we observe heterogeneous characteristics in the evolution of China’s inflation within the short-and-medium scales but not in the long-term. We observe zones of coherence in the short-term, while in the medium-term we date-stamp volatility from 1999 to 2005. Evidence shows that besides money supply, demand shocks, volatility of exchange rate policy, and wage-price spiral contribute to inflationary pressures in China before 2000. Although, since 2002, the People’s Bank of China has embarked on an implicit inflation target. During the AFC, the economy’s ‘pump priming’ policy response to revamp the economy and to contain massive unemployment may have constituted inflation expectations. Also, during the GFC, China’s credit-quota policy tightening in 2007 increased the money supply from 17 percent in 2008 to 30 percent in 2009, triggering inflation in 2009. From 2016, consistent with GDP growth revamping, inflation increased steadily amidst fiscal and financial accommodation by the Chinese authorities. The depreciation of the Renminbi may also have contributed to additional inflationary pressure (Day, 2017).

We further examine the evolution of EPU, GPR, and EPGR (see Tables 4, 5, and 6; Figs. 3, 4, and 5). Regarding the EPU, we observe high volatility in the short-and-medium term in the USA, UK, and Canada with a dominance of coherence in the short-term. We date-stamp two episodes of strong variation in periods, corroborating periods of shocks in the early-1990s and early-2000s recessions in the USA. Given the level of synchronization of the US and Canada’s economies, we also identify two periods of significant volatility in the early-1990s and in the period of the great recession. In the UK, we observe one zone of coherence in the medium-term aligning periods of 2002–2004. The EPU for Japan and China is, however, essentially domiciled within the 2–8 month frequency-bands, suggesting that it is more dominant in the short-horizon. The zones of coherence are more pronounced during the AFC, the GFC (2008), the US debt ceiling in 2011, Brexit in 2016, and Japan’s consumption tax regime.

Baker et al. (2016) opine that the rise in EPU is potentially damaging to the USA. Essentially, strong variance during these periods may suggest a greater prevalence and intensity of concerns related to uncertainty about the government’s economic policies and packages. Indeed, secular growth in government fiscal spending and taxes coupled with government regulation and tax codes may threaten policy related uncertainty. In addition, Arbatli et al. (2017) opine that policy uncertainty portends challenges for Japan’s quest to revamp growth, minimize risks of deflation, lift wages, and improve overall economic performance.

The visual inspection of the GPR shows areas of strong/significant variations within the 2–8 and 8–32 month frequency scales for the USA and Canada. We also observed strong volatility in the short-term but weak significance in the medium-term for the UK and China. We only notice islands of strong coherence in the short-term for Japan and a long but marginally strong zone of coherence in Canada spreading through 2001–2010 in the long-term. These geopolitical risks essentially foreshadow macroeconomic fundamentals in terms of lower investment, stock prices, and employment. Higher geopolitical risk is also associated with a higher probability of economic disasters and risks to the economy (Caldara and Iacoviello 2022). The interaction of EPU and GPR, i.e., EPGR, which represents a high phenomenon of uncertainty and risk, shows strong variance in the short and medium term in the USA, Canada, the UK, and Japan, except in China, where strong coherence falls only within the 2–8 month frequency bands. Generally, we cannot establish significance above the 32-frequency scale across samples.

5.2 Wavelet coherence (WC) and multiple wavelet coherence (MWC)

We further examine the co-movement and lead-lag nexus between the explanatory-variables and inflation using the WC. We estimate Eq. (8) to derive the phase-difference in Table 7. Figure 6 (Table 8) shows a heterogeneous pattern across frequencies with much evident switching behavior in the lead-lag status in the co-movements of EPU and inflation. The US-EPU shows strong-dependency with inflation at the 2–8 month scale while the leading-lagging status of either of the series is uncertain, particularly from 1991 through to 1999. However, we notice a significant switch as inflation leads EPU at the eve of the GFC, the inception of the GFC, and immediately after the global recession. The result shows that inflation heightens policy uncertainty. Essentially, when there is high inflation, there is political pressure to reduce it. As such, future monetary policy can be unpredictable for economic agents, further affecting inflationary policy uncertainty. Typically, high inflation spurs uncertainty in households’ spending and firms’ investment decisions. Heightened inflation can induce higher anticipation of continued price increases in the future (i.e., inflation expectation); as such, monetary policy actors might find it challenging to bring inflation back to target. Central bankers may be faced with either hiking the MPR, leading to excessive tightening of financial markets, or being more accommodative, with attendant effects on the economy. Maintaining a “neutral” i.e., neither accommodative nor restrictive to maintain steady-state full employment may portend a tighter financial condition, thus exacerbating uncertainty. EPU can exert a negative effect on the economy as all economic agents avoid financial risks. Given the dynamic and globally large macroeconomy of the US, the US-EPU is strongly influenced by the rise in energy prices. Therefore, policy responses such as the ratcheting up of interest rates to curb inflation may trigger policy uncertainty in indebted economies and truncate their economic progress.

Wavelet coherence plot for EPU and inflation

We, nonetheless, date-stamp anticyclic pattern in the leading status of inflation within the COVID-19. This negative correlation is also explicit within the 8–32 bands, particularly within 2008–2012 and 2020. This aligns with Leduc and Liu (2016), who show a negative correlation between EPU and inflation. In the long-term, we notice the longer zones of strong coherence spanning through the early-1990s and 2000s recessions, wherein EPU takes a leading position. The results show that the EPU has a leading and positive influence on inflation. Generally, we observe switch in signs and lead-lag status suggesting asymmetric tendencies in the co-movements of inflation EPU. This result corroborates Istiak and Alam’s (2019) that the degree of the nexus of inflation and EPU differs based on periods preceding or following a financial crisis and further reaffirms Jones and Olson’s (2013) findings that EPU inflation correlation changes signs from the mid to late 1990s.

Similar to the US, we notice several islands of coherence between the Canadian-EPU and inflation in the short-term with no clear distinction on lead-lag positions of the series except the In-phase and leading position of inflation which falls within 1994 and 1996. Concomitant to the previous findings, the in-phase and leading positions imply that increasing inflation causes higher EPU. However, this relationship cannot be sustained in corresponding periods in the medium-term. In the medium-term, we observe that EPU has a positive causal effect on inflation spanning from 2000 to 2006 (before the GFC), whereas, during the GFC and post-GFC, inflation has an anticyclic causal influence on EPU. In similar frequency scales and time domains, we see similar results in the United States. However, unlike in the USA, the direction of co-movement between the series cannot be established as neither one leads the other in the long-term.

We further notice significant coherence in the UK EPU-inflation nexus within the 2–8 months-scale. In particular, we notice three episodes of significant co-movement with explicit lead-lag status. Inflation leads EPU in 1999–2002 and 2004–2006, while the pattern of interdependence changes as EPU has a positive causal effect on inflation between 2012 and 2013. The positive causal effects of inflation on EPU corroborates previous findings, while the positive and leading status of EPU results suggest that heightened EPU triggers high inflation in line with theory. We only date-stamp 2020 as the period of strong coherence between EPU and inflation in the medium-term, where the UK-EPU is leading and inflation is following. However, we cannot establish coherence in the long-term.

In Japan, there exists a strong interconnectedness between inflation and EPU in the short-term wherein EPU has a negative causal influence on inflation in the early 2000s. While EPU still maintains its leading-status following Brexit in 2016, the correlation is positive, however. Although we establish strong coherence in the medium-term, the direction of the relationship between the series is uncertain. While we identify the in-phase and the leading-status of inflation during 2007–2010 and 2015–2016 in China, there is an out-of-phase relationship where EPU significantly causes inflation during the COVID-19 (2021) in the short-term. This anti-phase and leading position of EPU still holds between the late-1990s and early-2000s in the medium-term but switches within 2012–2014 when inflation positively causes EPU. Long-term observations revealed long regions of non-negligible coherence with an uncertain direction of co-movement. Generally, while the US-EPU and inflation show strong variance and interdependency across the three horizons, we cannot ascertain the direction of correlation between Japan’s EPU and inflation in the medium-term. Although there is a strong coherence between EPU and inflation in Canada, China, and Japan on a long-term scale, there is no clear-cut lead-lag direction between the series. We cannot record zones of coherence in the long term for the UK.

Figure 7 (Table 9) shows different associations between geopolitical risks and inflation. The US-GPR and inflation show strong-coherency but varying lead-lag status, particularly in the 2–8- and 8–32-month scale. Furthermore, several significant zones of co-movement are established in the short-term. We notice an anticyclic causal effect of inflation on GPR from 1988 to 1989, but the pattern changed following the early 2000s, when GPR shocks spurred higher inflationary pressures. Corroborating Caldara et al. (2022), GPR triggers inflation, higher commodity prices, and supply chain disruptions that are more than offset by the deflationary influence of lower consumer sentiment and tighter financial conditions. They further show that country-specific GPR exerts inflationary pressure, which is more induced in economies with large military spending. The GPR maintained its leading causal effect on inflation after the dotcom bubbles and before and after the GFC. In the medium-term, we notice two-episodes of strong interdependency: from 1988 to 1994, where GPR significantly causes higher inflation; and from 1997 to 2003, within which we observe an anti-phase co-movement from inflation to GPR in 2001–2002.

Wavelet coherence plot for GPR and inflation

We notice heterogeneity in the lead-lag status of GPR and inflation across frequency and time in Canada, the UK, Japan, and China. In the short-term, we briefly observe in-phase status and the leading causal-effect of inflation on GPR briefly in the 1990s in Canada, whereas in the mid-1990s, GPR exerts a positive causal effect on inflation. The GPR further leads inflation in 2006–2007 and 2019, but the co-movement is anticyclic. The anticyclic status switches in 2021 when GPR shocks cause higher inflation. The UK-GPR consistently led inflation in the early 2000s (in-phase) and 2012–2016 (anti-phase). Similarly, the Japan-GPR causes inflation in 2009–2010 but the phase-difference status changes between 2013 and 2015 when we observe an anti-cyclic response of inflation to GPR. In China, we observe GPR causes higher inflation in 2001–2003, whereas inflation leads and GPR follows in 1998–1999 and 2014–2015.

In the medium-term, we observe an out-of-phase causal-flow from inflation to GPR in 1989–1990 and 2014–2016 in Canada. Similarly, in the UK, inflation leads the GPR but we notice an in-phase status within 2018–2020. The wavelet map reveals an anti-cyclic response of Japan-inflation to GPR shocks in the mid-1990s and the COVID-19 periods, whereas we notice in-phase co-movement between inflation and GPR in 2007–2010 when inflation leads GPR. We notice two episodes of causality in China: GPR shocks cause higher inflation in 2012–2014, whereas GPR responds negatively to inflation in 2020.

However, similar to the USA, we identify zones of high coherence in the long-term in Canada, but the direction of causality is unknown. In the UK, there is no evidence of coherence in the long-term. However, in Japan, we date-stamp 2015–2017 when the phase-difference reflects out-of-phase status and a causal-flow from GPR to inflation. We further notice the longest island of coherence in China with an anti-phase status where inflation leads GPR from 2003 to 2013 (Fig. 8).

Wavelet coherence plot for EPGR and inflation

The lead-lag relationship seems to reflect more bi-directional causality between the series at different scales. The results have some implications as GPR causes economic (inflation) upheaval, which can have a feedback-effect on global instability. On the one hand, inflation, being a geopolitical phenomenon, is rooted partly in rising global tensions. GPR shocks trigger a rise in energy costs and disruption in supply chains, thereby pushing prices higher and exacerbating inflationary pressures. On the other hand, inflation may have geopolitical effects. Inflation can provide a fatal spark, trigger geopolitical-tensions and cause revolutionary kindling such as the French-revolution and Arab-spring. This result corroborates Aisen and Veiga's (2006) that high geopolitical-instability spurs higher inflation, while high-inflation also generates inefficiencies, dampens society’s welfare, and triggers geopolitical tensions.

To strengthen the analysis, we further apply the MWC to determine how good the linear combination of independent variables co-move with inflation across various time–frequency domains. As shown in Fig. 9, we observe multiple correlation between EPU, GPR and inflation across countries. We observe significant coherence across all investment horizons in the USA, Canada, Japan, and China while the UK shows much concentration in the short-term than the medium-long term. Generally, we identify a larger zone of significant area through the MWC than through the WC; as such, EPU and GPR can be adduced to be main factors driving inflation across countries. This result reflects that heighten uncertainty increase inflation (Bloom 2014; Caldara et al. 2022).

Multiple wavelet coherence plot for EPU, GPR, and inflation

We conclusively inquire the dynamics between EPU and GPR interactions (i.e., EPGR) and inflation (Fig. 8 and Table 10). The EPGR represents a highly elevated phenomenon of both policy uncertainty and risks. We observe the following significant changes following the interactions: In the short-term, we date-stamp 1995 when the US-inflation leads EPGR while the phase-difference is anti-phase. In Canada, we observe an in-phase co-movement and a leading causal-flow from EPGR to inflation. The UK-EPGR causes higher-inflation in early 2000s while the causal nexus changes during 2012–2013 as inflation leads EPGR. Unlike the mixed-results in the UK, EPGR consistently causes inflation in Japan although the phase-difference changes from in-phase (1993) to out-of-phase (2019). In China, inflation significantly and positively causes EPGR within two periods, 2002–2003 and 2015–2017. The US-inflation consistently leads EPGR in the medium-term although the signs changes from positive in the mid-1990s to negative in the late 1990s to early 2000s. In Canada, we only date-stamp 2009–2010 when we notice an In-phase relationship and the leading status of EPGR. This implies that EPGR positively cause inflation. The UK-inflation leads EPGR in an anti-phase relationship in the early 2000s but follows EPGR in an in-phase relationship between 2014 and 2016. However, we notice islands of significant coherence between EPGR-inflation in Japan but the lead-lag status is unknown while we cannot ascertain coherence for China. In the long-term, we observe longest zones of coherence from 1985 to 2001 within which EPGR causes higher inflation in 1993–1995 in the USA. Meanwhile, in Canada, UK, and China we cannot observe zones of coherence. In Japan, we notice long islands of strong coherence between EPGR-inflation spanning through two episodes from 1987 to 2005 and from 2008 to 2014 but the direction of co-movement is uncertain.

6 Conclusion

This study investigates the causal relationship between EPU, GPR, EPGR, and inflation in the USA, Canada, the UK, Japan, and China. We employed the continuous wavelet transform (CWT) to track the evolution of series across countries and further used the wavelet coherence (WC) to examine the co-movement and the lead-lag status of the variables across different frequencies and time. To strengthen the analysis, we apply the Multiple Wavelet Coherence (MWC) to determine how well the linear combination of independent variables co-moves with inflation across various time-frequency domains.

Using country-specific datasets, the CWT reveals heterogeneous characteristics in the evolution of each variable across frequencies coupled with periods corroborating critical global events. Inflation across samples exhibits significantly strong volatility in the short-and-medium-terms while the inherent variance fizzles out in the long-term. A similar pattern also holds for the EPU, except for Japan and China, where coherence is evident in the short-term. The GPR of the US and Canada reveals strong and significant variation in the short-and medium-term. Also, the UK and China reflect strong coherence in the short-term but weak significance in the medium-term, while Japan’s GPR reflects only strong coherence in the short-term. We, however, notice long but marginally strong zones of variation in Canada, spreading through 2001–2010 in the long-term. Furthermore, the EPGR shows a strong variance in the short-and-medium-term in the USA, Canada, the UK, and Japan, except in China, where strong coherence falls only within the short-horizon. However, we are unable to establish significance for EPGR above the 32-band threshold across samples.

Moreover, the WC’s phase-difference shows mixed results across frequencies and countries. While the US-EPU and inflation show strong variance and interdependency across the three horizons, we cannot ascertain the direction of correlation between Japan’s EPU and inflation in the medium-term. Although there is a strong coherence between EPU and inflation in Canada, China, and Japan on a long-term scale, there is no clear-cut lead-lag direction between the series. However, we cannot record zones of significance in the long-term for the UK. We notice a bidirectional causal nexus between GPR and inflation while the phase-difference reflects switches in signs in the short-term in the USA, Canada, and China. The GPR consistently causes inflation in the UK and Japan, but the relationship changes between in-phase and out-of-phase across time. In the medium-term, GPR causes inflation in an in-phase relationship, while out-of-phase causal flow from inflation to GPR is observed in the USA, China, and Japan. We observe an out-of-phase causal flow from inflation to GPR in Canada, whereas the co-movement is in-phase in the UK. Furthermore, we establish coherence in the long term in the USA and Canada, but the direction of dependency is unknown. While we notice an anti-cyclic causal flow from GPR to inflation in 2015–2017 in Japan, inflation leads to GPR in China. We cannot establish coherence in the UK in the long term. To strengthen the analysis, we apply the MWC. We observe significant coherence across all investment horizons in the USA, Canada, Japan, and China, while the UK shows much more concentration in the short-term than in the medium-long term. The MWC, in general, identifies a larger zone of significant area than the WC; as a result, EPU and GPR can be attributed as the primary factors driving inflation across countries.

We check the dynamics between the EPGR and inflation across samples. We observe a unidirectional causality in the USA across the horizons: inflation leads EPGR (short-term/anti-phase), inflation leads EPGR (medium-term/in-phase and anti-phase), and EPGR leads inflation (long-term/in-phase). In the short-term, the EPGR-inflation in the UK exhibit bidirectional causality with different lead-lag statuses across time whereas the Canada and Japan EPGR lead inflation. We observe inflation leads EPGR in China. While the UK maintains the bidirectional causality in the medium-term, EPGR causes inflation in Canada in an in-phase relationship. However, we notice islands of significant coherence between EPGR-inflation in Japan but the lead-lag status is unknown while we cannot ascertain coherence for China. We cannot observe zones of coherence in Canada, the UK, and China in the long-term, whereas, in Japan, the level of coherence is strong but the lead and lag status is not known.

Given the bidirectional causality, heterogeneity, and asymmetries in signs, policymakers, and other economic agents should consider the varying frequencies in their decisions to assist them in making opt and precise decisions. Indeed, policymakers should exert efforts to understand the lead-lag status to ensure solid policies to mitigate risks. Central banks would also have to recalibrate possible transmission and feedback between EPU, GPR shocks and inflation at different horizons and times to help monitor the dynamics of uncertainty, risks, and inflation. Monetary policy authorities should take apt action to prevent inflation from becoming heightened and keep future inflation expectations in check. While monetary policy rates might have to rise beyond what is currently priced in markets to get inflation back to target in a timely manner, however, precise communication is key to prevent unnecessary volatility in financial markets, through clear guidance about the tightening process. Policymakers, through a selected macroprudential tools, can keep elevated vulnerabilities at bay, such as spike in housing prices while being careful of a broad financial tightening.

Data availability

The data are available on reasonable request.

Code availability

Not applicable.

Notes

Another assumption is that enterprises may not want to raise prices at all (so as not to become less competitive) but reduce costs.

The reader is directed to http://www.policyuncertainty.com/ and https://www.matteoiacoviello.com/gpr.htm for more information on the EPU and GPR index calculations.

Although Japan records deflationary trends in decades, it, however, makes policies such as the “zero interest rate policy” in 1999–2000, “quantitative easing monetary policy” in 2001–2006, and the “Abenomics” policy packages in 2013 to boost economic output, investor confidence, and competitiveness and to battle deflation. Studies further show that “Abenomics” has an enormously significant impact on inflation (Michalis and Watzka 2017).

References

Aisen, A., Veiga, F.J. Political instability and inflationvolatility. IMF working paper no. 06/212 (2006)

Al-Thaqeb, S.A., Algharabali, B.G.: Economic policy uncertainty: a literature review. J. Econ. Asymmetries 20, e00133 (2019)

Antonakakis, N., Chatziantoniou, I., Filis, G.: Dynamic spillovers of oil price shocks and economic policy uncertainty. Energy Econ. 44, 433–447 (2014)

Arbatli, E.C., Davis, S.J., Ito, A., Miake, N., Saito, I. Policy Uncertainty in Japan, no. w23411. National Bureau of Economic Research (2017)

Athari, S.A., Kirikkaleli, D., Yousaf, I., Ali, S.: Time and frequency co-movement between economic policy uncertainty and inflation: evidence from Japan. J. Public Aff. (2021). https://doi.org/10.1002/pa.2779

Baker, S.R., Bloom, N., Davis, S.J.: Measuring economic policy uncertainty. Q. J. Econ. 131(4), 1593–1636 (2016)

Batabyal, S., Killins, R.: Economic policy uncertainty and stock market returns: evidence from Canada. J. Econ. Asymmetries (2021). https://doi.org/10.1016/j.jeca.2021.e00215

Baumeister, C., Peersman, G.: Time-varying effects of oil supply shocks on the US economy. Am. Econ. J. Macroecon. 5(4), 1–28 (2013)

Bernanke, B.S.: Irreversibility, uncertainty, and cyclical investment. Q. J. Econ. 97, 85–106 (1983)

Bloom, N.: The impact of uncertainty shocks. Econometrica 77(3), 623–685 (2009)

Bloom, N.: Fluctuations in uncertainty. J. Econ. Perspect. 28(2), 153–175 (2014)

Caldara, D., Iacoviello, M., Molligo, P., Prestipino, A. Raffo, A.: The Economic Effects of Trade Policy Uncertainty. International Finance Discussion Papers 1256 (2019)

Caldara, D., Conlisk, S., Iacoviello, M., Penn, M.: Do Geopolitical Risks Raise or Lower Inflation?. Federal Reserve Board of Governors (2022)

Caldara, D., Iacoviello, M.: Measuring geopolitical risk. Am. Econ. Rev. 112(4), 1194–1225 (2022)

Chakrabarty, A., De, A., Gunasekaran, A., Dubey, R.: Investment horizon heterogeneity and wavelet: overview and further research directions. Phys. A: Stat. Mech. Appl. 45–61 (2015). https://doi.org/10.1016/j.physa.2014.10.097

Charnavoki, V., Dolado, J.J.: The effects of global shocks on small commodity-exporting economies: lessons from Canada. Am. Econ. J. Macroecon. 6(2), 207–237 (2014)

Day, I.: Underlying Consumer Price Inflation in China, Bulletin – December Quarter 2017, Reverse Bank of Australia (2017). https://www.rba.gov.au/publications/bulletin/2017/dec/4.html

Goupillaud, P., Grossmann, A., Morlet, J.: Cycle-octave and related transforms in seismic signal analysis. Geoexploration 23(1), 85–102 (1984). https://doi.org/10.1016/0016-7142(84)90025-5

Grinsted, A., Moore, J.C., Jevrejeva, S.: Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Process. Geophys. 11(5/6), 561–566 (2004)

Ha, J., Kose, M.A., Ohnsorge, F.: Inflation in Emerging and Developing Economies: Evolution, Drivers, and Policies. World Bank, Washington, DC (2019). License: Creative Commons Attribution CC BY 3.0 IGO. https://doi.org/10.1596/978-1-4648-1375-7.

Haque, Q., Magnusson, L.M.: Uncertainty shocks and inflation dynamics in the US. Econ. Lett. 202, 109825 (2021)

Hausman, J.K., Wieland, J.F.: Abenomics: preliminary analysis and outlook. Brook. Pap. Econ. Act. 2014(1), 1–63 (2014)

Hunt, B.: U.K. UK inflation and relative prices over the last decade: How Important was globalization?. International monetary fund working paper WP/07/208. (2007)

International Monetary Fund (IMF).: World Economic Outlook: Coping with High Debt and Sluggish Growth. IMF Press (2012)

Istiak, K., Alam, M.R.: Oil prices, policy uncertainty and asymmetries in inflation expectations. J. Econ. Stud. 46(2), 324–334 (2019)

Istiak, K.: Economic policy uncertainty and the real economy of singapore. Singap. Econ. Rev. (2020)

Jones, P.M., Olson, E.: The time-varying correlation between uncertainty, output, and inflation: evidence from a DCC-GARCH model. Econ. Lett. 118(1), 33–37 (2013)

Khan, K., Su, C.W.: Does policy uncertainty threaten renewable energy? evidence from G7 countries. Environ. Sci. Pollut. Res. (2022). https://doi.org/10.1007/s11356-021-16713-1

Kimball, M.S.: Precautionary Saving in the Small and in the Large (No. w2848). National Bureau of Economic Research. https://www.nber.org/papers/w2848. (1989)

Leduc, S., Liu, Z.: Uncertainty shocks are aggregate demand shocks. J. Monet. Econ. 82, 20–35 (2016)

Leduc, S., Liu, Z.: The uncertainty channel of the coronavirus. FRBSF Econ. Lett. 7, 1–5 (2020)

Li, X., et al.: Exploring the asymmetric impact of economic policy uncertainty on China’s carbon emissions trading market price: Do different types of uncertainty matter? Technol. Forecast. Soc. Change (2022). https://doi.org/10.1016/j.techfore.2022.121601

Meinen, P., Roehe, O.: To sign or not to sign? On the response of prices to financial and uncertainty shocks. Econ. Lett. 171, 189–192 (2018)

Michaelis, H., Watzka, S.: Are there differences in the effectiveness of quantitative easing at the zero-lower-bound in Japan over time? J. Int. Money Finance 70, 204–233 (2017)

Mumtaz, H., Theodoridis, K.: The changing transmission of uncertainty shocks in the US. J. Bus. Econ. Stat. 36(2), 239–252 (2018)

Ng, E.K., Chan, J.C.: Geophysical applications of partial wavelet coherence and multiple wavelet coherence. J. Atmos. Ocean. Technol. 29(12), 1845–1853 (2012)

Pastor, L., Veronesi, P.: Uncertainty about government policy and stock prices. J. Finance 67(4), 1219–1264 (2012)

Rua, A., Nunes, L.C.: International comovement of stock market returns: a wavelet analysis. J. Empir. Finance 16, 632–639 (2009)

Stock, J.H., Watson, M.: Disentangling the channels of the 2007–09 recession: comments and discussion. Brook. Pap. Econ. Act. 43(1), 81–156 (2012)

Torrence, C., Compo, G.P.: A practical guide to wavelet analysis. Bull. Am. Meteorol. Soc. 79, 61–78 (1998). https://doi.org/10.1175/1520-0477(1998)079%3c0061:APGTWA%3e2.0.CO;2

Wen, F., Xiao, Y., Wu, H.: The effects of foreign uncertainty shocks on China’s macro-economy: empirical evidence from a nonlinear ARDL model. Phys. A (2019). https://doi.org/10.1016/j.physa.2019.121879

Wen, J., Khalid, S., Mahmood, H., Zakaria, M.: Symmetric and asymmetric impact of economic policy uncertainty on food prices in China: a new evidence. Resour. Policy 74, 10224 (2021)

Wu, K., Zhu, J., Xu, M., Yang, L.: Can crude oil drive the co-movement in the international stock market? Evidence from partial wavelet coherence analysis. N. Am. J. Econ. Finance 53, 101194 (2020)

Yilanci, V. Kilci, E.S.: The role of economic policy uncertainty and geopolitical-risks in predicting prices of precious metals: evidence from a time-varying bootstrap causality test. Resour. Policy 72, 102039 (2021)

Zhang, W., et al.: Economic policy uncertainty nexus with corporate risk-taking: the role of state ownership and corruption expenditure. Pac.-Basin Finance J. (2021). https://doi.org/10.1016/j.pacfin.2021.101496

Acknowledgement

The authors appreciate the editorial team and the anonymous reviewers for their comments.

Funding

This research is funded by the University of Economics Ho Chi Minh City, Vietnam.

Author information

Authors and Affiliations

Contributions

All authors contributed equally to this research.

Corresponding author

Ethics declarations

Conflict of interest

None declared by the authors.

Ethical statements

The authors hereby declare that this manuscript is the result of our independent creation under the reviewers’ comments. This research work does not contain any research achievements that have been published or written by other individuals or groups. The authors contributed equally to this manuscript. The legal responsibility of this statement shall be borne by the authors.

Consent for publication

The permission is expressly given.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Adeosun, O.A., Tabash, M.I., Vo, X.V. et al. Uncertainty measures and inflation dynamics in selected global players: a wavelet approach. Qual Quant 57, 3389–3424 (2023). https://doi.org/10.1007/s11135-022-01513-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11135-022-01513-7