Abstract

This paper investigates the incidence of limited attention in a high-stakes business setting: a bar owner may be unable to purge transitory shocks from noisy profit signals when deciding whether to exit. Combining a 24-year monthly panel on the alcohol revenues from every bar in Texas with weather data, we find suggestive evidence that inexperienced, distantly located owners may overreact to the transitory component of revenue relative to the persistent component. This apparent asymmetric response is muted under higher revenue fluctuations. We formulate and estimate a structural model to endogenize attention allocation by owners with different thinking cost. Under the assumptions of the model, we find that 3.9% bars make incorrect exit decisions due to limited attention. As exits are irreversible, permanent decisions, small mistakes at the margin interpreting profit signals can lead to large welfare losses for entrepreneurs.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Deliberation about an economic decision is a costly activity. As human cognition is a scarce resource, decision makers cannot consider all possible influences. How do people choose which factors to consider? While this question first appeared in the economics literature over sixty years ago (Simon, 1955) and a more recent literature has generated models as well as lab and field experiments (Gabaix et al., 2006; Hanna et al., 2014), field evidence remains thin. The best evidence comes from consumer decisions: not noticing add-ons to a larger purchase such as shipping charges (Brown et al., 2010; Hossain & Morgan, 2006), left-digit bias in used car mileage or grocery prices (Lacetera et al., 2012; Busse et al., 2013; Strulov-Shlain, 2023; Kraft & Rao, 2023), overspending minutes of cellphone usage plan (Grubb & Osborne, 2015), and the automatic renewal of subscription services (Einav et al., 2023).Footnote 1

We examine inattention and its implications in high-stakes decisions by firms. Firms often need to make forecasts based on repeated, noisy observations and then make an irreversible decision. For example, employers try to predict worker productivity before making firing decisions, and venture capitalists try to predict new start-ups’ prospects before making investments. In this study, we examine bar owners who try to infer the underlying profitability of their bars before making exit decisions. Owners should form rational expectations of the future profitability of their bars based on the profit record of the bar through time. The profit record, however, is affected by a large of numbers of factors that warrant attention: local demand, the bar’s quality and specialty, fixed and variable costs, and, often, transitory shocks such as weather variation, local sports team victories, or a flu outbreak.

We focus on the bar owners’ limited ability to purge transitory shocks, particularly weather shocks, from their observed profit signals. Transitory shocks temporarily shift profits, but a rational decision maker should know to net out of these transitory shocks from future profitability. If an owner already knows her true profitability, a temporary shock should not change her decision to exit. Therefore, the degree to which the owner accounts for past weather shocks in her exit decision reveals the existence and magnitude of her inattention to these transitory shocks. While there are many factors that bar managers should consider (and perhaps do not), we choose weather shocks because they are exogenous, measurable, and unpredictable, thus capturing the nature of transitory shocks (e.g. Conlin et al., 2007; Simonsohn, 2010). Furthermore, while the economic impact of weather is relatively small for individual bar owners,Footnote 2 its aggregate impact on the macroeconomy can be large.Footnote 3 Generally, weather shocks enter a (potentially inattentive) decision maker’s belief formation process, giving rise to the possibility of misinterpretation and incorrect perception.

To assess the empirical relevance of inattention, we use monthly alcohol revenue for every bar that operated in Texas between January 1995 and November 2018. We supplement this data with Texas weather station data and local market attributes. We first demonstrate that daily weather shocks in heat index, precipitation, and unfavourable characteristics (such as fog, rain drizzle, snow ice pellets, hail, and thunder) are correlated with alcohol revenue, and such effects vary from season to season. Overall, the weather effects are economically small but statistically significant, exactly what we look for in our research design –- we need to find transitory shocks that decisions makers may not pay attention to. If these shocks had substantial effects, then decision makers would recognize the impact immediately.

Decomposing revenue into a persistent component and a transitory component, we then show that owners of different attributes appear to react to these two components differently when making exit decisions. As the revenue records data separately identify owners and bars, we are able to construct measures of owner heterogeneity. In particular, we observe whether an owner has experience operating another restaurant or bar prior to the opening of the focal bar, and the distance between owner’s mailing address and bar location. We find that inexperienced, distantly located bar owners behave as if overreacting to the transitory component relative to the persistent component; moreover, they seem to react more to transitory revenue than experienced, closely located owners do. We consider this evidence consistent with limited attention by decision makers with heterogeneity cost of casting attention.

These asymmetric responses are unlikely due to alternative explanations such as ability to smooth revenue shocks, credit constraints, and projection bias. First, we show the magnitude of weather effects on revenue is similar across inexperienced and experienced owners. Therefore, experienced owners are unlikely to manage their business better to smooth out the impact of the transitory shocks they face. Second, we show owners that are likely to be credit-constrained (because of factors other than experience) respond more to both the persistent and the transitory components of revenue, instead of overreacting to the transitory component relative to the persistent component. Our results on owner experience and distance to owner are therefore unlikely to be driven by credit constraints. Third, we show that owners shift weight from the transitory component to the persistent component when revenue variation is higher, suggesting that owners rationally allocate attention when it is more warranted. This is against the prediction of projection bias because such bias is about the undue influence of the shock at the moment of decision-making. A more volatile environment should not affect an owner’s reliance on current states to infer future states.

Motivated by our descriptive results, we formulate a structural model that builds on theory and lab evidence about limited attention. As emphasized in DellaVigna (2018), a structural model allows us to calibrate magnitudes and examine the welfare impact of inattention. We estimate a single-agent model of belief formation and dynamic exit decisions, in which the owner of a bar updates beliefs about the bar’s underlying profitability after observing (alcohol) revenues, and if the present discounted value of future profits falls short of the outside option, the owner exits. In the Bayesian learning process, we build a “pre-step”, in which the owner solves an attention allocation problem to recover the true profit signals. The decision maker needs to weigh the benefit of observing the true state of the world and the cost of casting attention to recognize transitory shocks. The pre-step attention allocation problem incorporates Gabaix’s, (2014) “sparsity” model of rational inattention. In this model, the decision maker allocates attention to build an optimally simplified representation of the world that is “sparse,” that is, uses few parameters that are non-zero, and then choose her best action given this sparse representation.Footnote 4 We add to Gabaix’s model by modeling thinking cost as a stochastic process and linking it to the personal attributes of decision makers, which enables separate identification of the underlying profitability and the cost of thinking. Estimating this “limited attention” parameter and its relationship with decision makers’ attributes allows us to evaluate heterogeneous welfare trade-offs across firms and owners.

Under the assumptions of the structural model, we demonstrate the prevalence of inattention among bar owners. Of the 8,995 owners in our data, an average owner’s probability of paying no attention to the transitory nature of transitory shocks (and, in turn, overreacting to them) ranges from 76 to 87%, depending on the specification. Even if an owner is paying attention, her attention only amounts to roughly one third of the full attention spectrum. The amount of attention, however, displays significant heterogeneity across owners in data. This heterogeneity is driven by the within variation of a bar’s revenue, the cross-sectional variation in owner experience and the distances from owner’s mailing address to the bar location.

The prevalence of inattention has economic consequences. Consistent with Taubinsky and Rees-Jones, (2018) who emphasize the importance of incorporating heterogeneity into behavioral welfare analysis, our counterfactual exercises show that 351 bars (3.9% of the total) would have made different exit decisions had they paid full attention. For these 351 bars, the payoff to better decisions is overwhelmed by a much higher cost of casting attention. These magnitudes indicate that our study identifies minor frictions in business owners’ decision-making processes instead of major mistakes. Such inattention may be inconsequential if it merely changes the timing of a decision by a few months; but it can matter greatly if a few negative transitory shocks propel the owner to think the bar is unprofitable and thus the owner decides to exit prematurely. The model implies that negative shocks affect welfare more than positive shocks because negative shocks can cause a potentially successful bar to close, eliminating many potential years of profits. In contrast, positive shocks allow a bad bar to stay open, usually delaying the inevitable by a short period of time, so the misinterpretation of the revenue signal affects outcomes to a limited extent. This is particularly relevant in the case of a new entrepreneur with a short operating history to rely on and some unfortunate early negative shocks. Even if the premature failure can be “rescued” by chain corporations and business-savvy investors who spot these as opportunities, there will be distributional consequences with the young, inexperienced entrepreneurs on the side of loss.Footnote 5

Our work is distinct from the prior literature because of the focus on firms and managers.Footnote 6 The traditional economic framework assumes firms make fully rational decisions, in which managers seek to maximize the present value of current and future earnings, solve a dynamic optimization problem, and play a Bayesian Nash Equilibrium. These assumptions are well-grounded: the stakes are often higher for firms, and their decisions can involve long and careful deliberations in a collective setting. Perhaps more importantly, the market mechanism should attenuate biases in firms’ decision-making processes. Nevertheless, there is an increasing sense that managers may not make optimal decisions. After all, firms are run by humans who may be subject to behavioral biases, mistakes, and limited ability to compute and retain information. Standard dynamic models require extraordinary information retention and processing capabilities (Pakes, 2016). Field evidence on behavioral decision-making by firms is, at best, sparse in industrial organization (DellaVigna, 2018), though some work has started to explore the situations in which firms do not appear to behave according the standard economic models (e.g. Aguirregabiria & Jeon, 2020; Backus et al., 2022; DellaVigna & Gentzkow, 2019; Doraszelski et al., 2018; Goldfarb & Xiao, 2011; Goldfarb & Yang, 2009; Hortacsu et al., 2019).

One main challenge, perhaps limiting the flow of new work in this area, is to find settings of persistent behavioral biases that can be identified by data. The novelty of our work lies in the observation that weather shocks can be interpreted as transitory shocks in a bar’s revenue records that a decision maker needs to cast attention to. Our model has a unique mechanism of heterogeneous decision-making: some decision makers, particularly inexperienced ones, have difficulty separating “observable” noise from true signals. Furthermore, we leverage on a setting with heterogenous owners and infrequent firm decisions, in which bounded rationality is likely to be more important (Camerer & Malmendier, 2007). Lastly, we depart from previous empirical literature on inattention because of the approach we take to model inattention. We model inattention in a cost–benefit analysis rational inattention framework.Rational inattention occurs when people only pay attention to those factors that are sufficiently important that it is worth the cost of thinking (Veldkamp, 2011). A rational inattention framework allows us to consider the welfare impact of marginal reductions in the cost of paying attention. This contrasts with models that focus on inertia (e.g. Miravete and Palacios-Huerta, 2014; Handel, 2013) or heuristics (e.g. Gabaix et al., 2006; Lacetera et al., 2012) in which the welfare analysis does not include explicit attention costs. We use observed variation — in monthly revenue and owner attributes — to measure the benefit and cost of paying attention. Gabaix, (2014) emphasizes that this approach is based on robust psychological facts and can be applied to give many classical economic theories a behavioral update. By illustrating the role of heterogeneous decision-making ability in high-stakes business settings, our results can inform broader, macro-level analysis that incorporates such distortions in firm-level decision-making.

2 Data

Our raw data were collected in December 2018 and contain the universe of Texas restaurants and bars with licenses to sell alcoholic beverages from January 1995 to November 2018, roughly a 24-year span. We have a monthly panel of establishment identification code, name, street address, and revenue from alcoholic beverages.Footnote 7 Moreover, we have the taxpayer identification code for each establishment as well as taxpayer name, address, and telephone number. This feature of the data allows us to separate the owner (the taxpayer) from the establishments she owns. The data are collected for the purpose of tax collection and are available from the Texas Comptroller of Public Accounts.

Using this information, we generate a bar-month level dataset between January 1998 and October 2018 for all bars that opened in January 1998 or later (251 months in total). As we detail below, we use the first three years of data (1995 to 1997) to create measures of owner experience in the restaurant and bar industry. We use November 2018 data to identify exit for establishments that operate until October 2018.

The January 1995 to October 2018 raw data contain 40,299 establishments and 2,576,506 establishment-month observations. In order to have a consistent measure of establishment experience, we drop all establishments that experienced an ownership change in their operating history. These establishments account for 6.75% of the total number of establishments. We do this because our model relies on the owner being aware of the history of the establishment, in terms of revenue and (if attentive) weather. New owners of a pre-existing establishment may not satisfy this criterion. Furthermore, ownership change could be seen as an exit due to failure, or as a signal of success. Dropping such establishments enables a cleaner interpretation of our empirical results. We then drop all establishments that opened prior to January 1, 1998 because we do not have measures of owner experience (which we measure over the three years prior to the month the establishment opens) for these establishments. These account for 19% of the total number of establishments. Finally, we drop observations from establishment owners with at least 25 different establishments at some point in the data period. This is another 4.99% of the total number of establishments. This leaves 27,885 establishments.

Distinguishing bars from restaurants

To ensure that alcohol revenue accounts for the majority of revenue, we manually cleaned our data to distinguish bars from restaurants. To do so, we searched for each of these 27,885 establishments online between January and March 2019. Importantly, online sources such as Yelp, Facebook, the Wayback Machine, and local news outlets provide information on many bars and restaurants that have long closed. Where available, we emphasized the Yelp classification. We classified sports bars and dance clubs as bars, and hotel, golf clubs, adult entertainment, cinemas, and legion halls as unsure. There were 434 establishments that we could not find online and we classified them as unsure. From this effort, we identified 8,995 from their online profiles that were primarily bars and 13,999 that were primarily restaurants, leaving 4,891 were not clearly one or the other.

The 8,995 bars provide the main data in the analysis, totaling 422,651 bar-months. Constructing the variables for analysis involves creating measures of owner experience, owner attributes, bar exit, bar revenue, bar attributes, and controls for the local business environment. We discuss each of these below. Table 1 presents bar-level information on key variables that we study, including whether a bar ever exited from business during our data span, owner experience, and owner attributes. Table 2 presents information on time-varying bar attributes and local market attributes at the bar-month level.

Bar exit

As noted by Parsa et al, (2005), there are several different ways to define exit in this industry: closing, ownership change, or bankruptcy. We focus on closings, defined as situations where an establishment ceases to operate at an address with the same name.Footnote 8 That is, an establishment exits even if a new establishment at the same address appears with the same owner. Overall, 65% of the bars in our data exit by the end of the period (the rest are right-censored), compared to 57% of restaurants and 70% of those we could not classify. On a bar-month basis, 1.4% of bar-months in the data involve an exit. This base rate of exit is roughly in line with estimates by Parsa et al., (2005, 2014).

Owner experience

Before we identify whether a bar owner has experience in the industry, we need to identify whether two establishments are owned by the same person. To do so, we first use the taxpayer identification code. If this matches, then there is a common owner. This definition misses matches in which one owner holds multiple establishments in partnerships or holding companies. To fix this problem, we use the other taxpayer information provided in the data. If the taxpayer information for two establishments has the same phone number, the same address, and a similar name, we also assume the establishments have the same owner. While identifying similar names is inherently a judgment call, we looked at inclusion or exclusion of initials (Mary Smith, Mary A. Smith, Mary Andrea Smith), partnerships (Mary Smith, John Smith and Mary Smith), iterations of the same holding company (MAS Inc., MAS II Inc.), and what appear to be misspellings. Because we restrict on matching phone numbers and matching addresses, common names are unlikely to be a problem. At the same time, we likely underestimate owner matches in the sense that it is likely that some holding companies with distinct names are owned by the same person.Footnote 9 Our manual cleaning increased the percentage of owners with prior experience in the Texas bar/restaurant industry from 15 to 19%.

Our experience measure focuses on whether the owner owned a bar or restaurant in Texas prior to opening the focal business. We include both bars and restaurants under the experience measure because experience at restaurants is highly relevant to managing bars and vice versa. We emphasize the level of experience at opening for two reasons. First, prior research in entrepreneurship emphasizes differences between first time and “serial” entrepreneurs (e.g., Lafontaine & Shaw, 2016; McGuire, 2021; Xu & Ni, 2022). Serial entrepreneurs are more likely to succeed, perhaps because they have a broader set of experience, enabling them to be more of a jack-of-all-trades (Lafontaine & Shaw, 2016; Lazear, 2005) or perhaps because of better inherent ability. The second reason is for identification: the experience accumulated since the opening of the focal establishment is collinear with a variety of other factors that may affect revenue including learning about quality, building reputation, and selection bias related to accumulated time since opening. Together these reasons suggest that focusing on owners’ pre-existing experience at time of opening the focal business provides a cleaner measure of the variation in experience across owners.

We develop two experience measures, one binary and the other continuous. The binary measure is an indicator for whether the owner owned at least one establishment in the three years prior to opening the focal establishment. This dummy variable provides a stark distinction between experienced and inexperienced. As shown at Table 2, 19% of bar owners had owned a bar or restaurant in the three years prior to opening the focal bar. The continuous measure counts the number of establishment-months over all establishments the owner owned in the previous three years prior to opening the focal establishment. For example, if at the time when an owner opens her third establishment, her first one had been open for 24 months and her second one had been open for 6 months, then we measure the owner’s pre-existing experience for her third establishment as 30 establishment-months. In our data the average of this experience measure is about 8 establishment-months, and the maximum is 562. This variable is highly skewed to the right and therefore we add 1 to this number and take natural log of it in our empirical analysis.

Restaurant revenue

Our data contain rich information about a key source of establishment profitability: Alcohol revenue (Brown, 2007). Unfortunately, our data do not contain information on total revenues or profits. Therefore, in the analysis that follows, we assume that alcohol revenues are strong signals of bar profitability, at least up to the power of bar-level random effects. This is the main reason we distinguish bars from restaurants, rather than using the entire dataset of bars and restaurants. Specifically, we assume that a bar’s variation in profitability is proportional to the variation in (log) alcohol revenue. Online Appendix E.1 provides further evidence of the usefulness of alcohol revenue as a proxy for bar or restaurant success, though we cannot directly test the assumption on proportionality of log alcohol revenue to profitability. We deflate all revenues using the Consumer Price Index for all U.S. urban consumers and report in 2018 dollars. The average bar in the data earns slightly more than $52,500 per month in alcohol revenue. This number is highly skewed to the right, with a within-establishment standard deviation of about $30,000 and a between-establishment standard deviation of $56,000.

Weather and weather shocks

Using an establishment’s address, we identify the closest weather station and use daily weather reports from that station on temperature (measured in degrees Fahrenheit), relative humidity (measured in percentage), precipitation (measured in inches), and the number of days with unfavorable weather (unfavorable weather includes fog, rain drizzle, snow ice pellets, hail, and thunder). The weather reports we use are Global Summary of the Day, which is computed and reported from global hourly station data by the National Oceanic and Atmospheric Administration.Footnote 10

The top panel of Table 3 report summary statistics of monthly average of daily weather faced by Texas bars. Texas has warm weather with an average of 70 degrees Fahrenheit. In parts of Texas, the warm weather is often accompanied by high levels of humidity during summer months. As humidity affects human comfort and henceforth decisions to dine out, we construct a heat index based on daily mean temperature and relative humidity.Footnote 11

Hurricanes are common near the coast. Using data from the Federal Emergency Management Association (https://www.fema.gov/disasters), we coded whether a hurricane-related disaster was declared for each Texas county in each month. If the incident period of a hurricane included any part of a month in a county, it was coded as having a hurricane that month. Because hurricanes are a salient event that are likely to completely shut down the bars, in the analysis below we do not consider these as transitory shocks that the owners might not notice. Instead, we include them as controls recognizing that the label of “persistent” is not an accurate description for this variable.

In our main empirical analysis, we use three dimensions of weather shocks. We construct these shocks at the daily level and then aggregate them to the monthly level. For heat index and precipitation, we perform the following steps to define monthly weather shocks.

-

1.

For every weather station, we calculate the (long-run) “normal” value of a certain month as the average of the corresponding weather element across all days reported for the month from 1995 to 2018.

-

2.

We calculate the deviation of the actual daily weather element from its normal value in the month.

-

3.

We take the monthly average of the daily weather deviation across all reported days during a year-month combination to construct the “shock” variable.

The definition of the shock for the number of days with unfavorable weather is slightly different. We first sum up all the days with unfavorable weather within a month and then deduct the (long-run) normal of this measure from it.

In total we have three dimensions of weather shocks: heat, precipitation and the number of days with unfavorable weather. We present the summary statistics of these weather shocks in the bottom panel of Table 3. All three dimensions have a mean of roughly zero, but the standard deviations are large with occasional extreme weather events.

Controls

We include controls for bar and location characteristics to capture persistent demand and cost shifters. Our choice of controls is informed by prior work on restaurant and bar failures (Parsa et al., 2005, 2014) that emphasizes local characteristics including demographics, local competition, and chain affiliation. For demographics and local characteristics, we merge in U.S. Census and Zip Code Business Patterns in the corresponding years and use zip code level information on the number of restaurants, population, fraction black, fraction Hispanic, fraction under 18, fraction over 65, average household income, fraction with a bachelor’s degree, fraction rural, and fraction foreign born. We also add a control for the number of months since the bar opened, the squared term of it, and a dummy for likely lease renewal periods (a multiple of 12 months since opening, as in Abbring & Campbell, 2005). For the random effect specifications, we add time-invariant owner attributes, including the distance (in miles) from the location of the bar owner’s address for tax purposes to the bar location, whether the owner has only a single establishment, and whether the listed taxpayer is an individual’s name rather than a business name.Footnote 12

3 Empirical support for limited attention

Next, we provide stylized facts that support a model of inattention. Our empirical analysis begins with a decomposition of revenue into two components: one that displays persistence and the other that is transitory in nature. Taking the results of the decomposition as data, we show owners of different attributes have asymmetric responses to the two components of revenue in their exit decisions. Specifically, inexperienced, distantly located owners overreact to the transitory component relative to the persistent component. In contrast, experienced, distantly located owners seem to recognize the nature of transitory shocks and, in turn, have a relatively muted response to them. We then provide evidence supporting our emphasis on the role of inattention against alternative explanations, including revenue smoothing, credit constraints, and projection bias.

3.1 Decomposition of revenue into persistent and transitory components

We write the logarithm of each establishment’s revenue as a linear function of weather shocks, the full set of controls \(X_{jt}\), month-of-the-year fixed effects \(Month_{t}\), year fixed effects \(Year_{t}\), and establishment fixed effects \(\mu_{j}\). We use a log-linear revenue model because the distribution of alcohol revenue of bars is highly skewed to the rightFootnote 13; taking the natural logarithm of revenue will minimize the influence of outliners. For bar j in month t:

In Eq. (1), weather shocks include shocks on three dimensions: heat index, precipitation, and the number of days with unfavorable weather. We assume \(\varepsilon_{jt}^{r}\) is independently distributed over time but correlated across all establishments in a county. We therefore cluster the standard errors at the county level.Footnote 14 Note that the effect of weather shocks on revenue, \(\alpha_{quarter}^{1}\), is quarter-specific, which allows us to capture potential seasonal differences in the correlation between weather and revenue. For example, a warm winter may lure consumers to dine out but a hot summer may have the opposite effect.

Table 4 columns 1 to 4 report estimation results quarter by quarter: January-March, April-June, July–September, and October-December. The most relevant weather shock variables (based on the magnitude and statistical significance level) vary by quarter. In quarter 1 warmer weather increases revenue but unfavorable weather decreases it; in quarter 2 both warmer weather and more precipitation increase revenue; in quarter 3 more precipitation reduces revenue; and in quarter 4 the only thing matters is the number of days with unfavorable weather. Column 5 shows the results of this regression pooling all quarters together: warmer temperatures are associated with higher alcohol revenue, but precipitation and days with unfavorable weather have a negative and insignificant relationship to alcohol revenue. Based on the comparison between the first four columns and column 5, we can see that pooling the four quarters together masks substantial variation across seasons. This comparison affects our modeling choice in Section 4, in which we allow the effects of weather shocks to be quarter specific.

In estimating Eq. (1), our focus is not on the interpretation of the magnitudes. It is useful to confirm that weather affects revenue as expected — weather shocks have small effects, so it is justifiable that decision makers with high thinking costs ignore weather shocks. The sign of the coefficients in these regressions are not easy to interpret in each case, suggesting a limitation of any interpretation that emphasizes what a positive and negative weather shock should be. For our analysis, however, the core relationship we establish here is that the estimated weather effects represent transitory shocks that should average to zero in the long run. By design of this study, we look for transitory shocks that decision makers may not pay attention to — if these shocks had large effects, then decision makers would recognize its impact immediately (for example, restaurant decision makers would likely recognize the impact of a hurricane on revenue) or allocate attention to understand its effects.Footnote 15

Given the marked differences of weather effects across seasons, our main results use the quarter-by-quarter estimates in columns 1 through 4 of Table 4 for the decomposition. For every establishment in the data for a given month, we decompose log alcohol revenue into two components: the transitory component and the persistent component:

We repeat the above decomposition exercise separately for each subgroup of establishments that we call during our empirical analysis: inexperienced versus experienced owners, nearby versus distant owners, individual versus business owners, and single versus multiple establishment owners. The purpose of doing this is to allow weather shocks have a flexible effect on every subgroup of establishments and hence the decomposition is accurate for each subgroup.Footnote 16

Table 5 reports the summary statistics of the decomposed revenue components for all bar-months and then for subgroups for owners. The transitory shocks average to zero, which is as expected, with a large standard deviation. More importantly, there is almost no difference across owners with different experience levels and different distances to establishment location. Next, we investigate how bar owners respond to persistent shocks versus transitory ones. If bar owners are fully attentive, the effects of transitory shocks should have no effect on their perception of bar profitability.

3.2 Owner response to different components of revenue

Table 6 examines the responsiveness of an owner’s exit decisions to the different components of revenue. It is a linear regression of exit on the transitory component, the persistent component, time-invariant owner attributes (\(X_{j}\)),Footnote 17 time-varying establishment and market attributes \(X_{jt}\), month-of-the-year fixed effects \(Month_{t}\), year fixed effects \(Year_{t}\), and lastly, establishment-level random effects \(\xi_{j}\). Establishment-level fixed effects are not identified here because each bar exits only once. Specifically, the regression equation is:

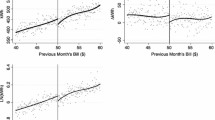

In Eq. (4), we assume \(\varepsilon_{jt}^{x}\) is independently distributed over time but correlated across all establishments in a county. We therefore cluster the standard errors at the county level. Column 1 of Table 6 reports estimation results for Eq. (4) for all 8,995 bars. The effects of revenue fluctuations are substantial. Take the effects of transitory shocks as an example: a 1% increase in transitory revenue will reduce monthly exit probability by 0.038 percentage point, or equivalently a 10% increase in transitory revenue will reduce monthly exit probability by 0.38 percentage point –- 10% is more like a windfall due to a usually good month of weather. Given the baseline monthly exit rate is only 1.4% on average, a decrease of monthly exit probability by 0.38 percentage point is a large effect, which accumulates to roughly 5 percentage point decrease at the annual level. Strikingly, variation in the persistent and transitory components of revenue affect exit likelihood equally.Footnote 18 That is, a typical owner recognizes little difference between the persistent and transitory components. This is in contrast to the predictions of full attention: transitory shocks should have no impact on the exit decisions of fully attentive owners. This is our first evidence of inattention.

Column 1, again, masks large differences in the responses of different owners. Columns 2 (inexperienced owners only) and 3 (experienced owners only) of Table 6 show heterogeneity across types in the responses to different revenue components. There are two types of asymmetries. First, between the two types of owners, inexperienced owners respond more to the transitory component of revenue than experienced owners do. Second, between the two components of revenue, inexperienced owners respond more to the transitory component than to the persistent component. Columns 4 (including owners whose mailing address is more than the median distance—5 miles—away from establishment location) and 5 (including owners whose mailing address is less than 5 miles from establishment location) of this table report owners’ response to the two revenue components with respect to distance. Presumably, local owners are more likely to observe weather variation as well as other on-site demand shocks. These two columns show roughly the same two types of asymmetry in columns 2 and 3, and the asymmetry seems to be even more pronounced. That is, local owners behave more in line with attentive decision-making as they dampen their reaction to transitory revenue, but distant owners fail to respond to transitory shocks correctly.Footnote 19 The magnitude of the asymmetry across types are sizable: across columns (2) and (3), the inexperienced type’s monthly exit probability is 0.03 percentage point higher than that of the experienced type following a 10% increase in transitory revenue, while the local type’s is 0.11 percentage point higher than that of the distant type. Again, given the base monthly exit rate is only 1.4%, these are large differences. The statistical significance of the differences in response to the two types of revenues are supported by the Wald test statistics at the bottom of the table. These results are suggestive of the interpretation we emphasize. The small magnitude and marginal statistical significance mean that our analysis could be interpreted as a proof of concept rather than a definitive set of results about differences between experienced and inexperienced firm owners.

In Eq. (4), a bar’s revenue is decomposed into the persistent and transitory parts. In this decomposition, it is possible to that some persistent revenue variations are assigned to transitory. That is, the error in Eq. (2) could include time-varying unobservables that shift a bar’s revenue permanently, for example, the turnover of the kitchen crew or an interior design upgrade. The nature of this problem is a measurement error issue –- we measure transitory shocks with errors that could go either way. With this issue, the coefficient of transitory revenue is subject to attenuation bias –- some of our results and interpretation are weakened by the existence of such bias.Footnote 20

3.3 Alternative explanations

While these asymmetric responses are consistent with limited attention to transitory shocks, it is possible other explanations could also rationalize these results. We consider three alternative explanations:

Shock smoothing

Experienced owners may be better skilled at handling other aspects of restaurant operation; in particular, they could do a better job smoothing out the effect of negative weather shocks on revenue. For example, an experienced owner may adjust the menu to boost revenue in bad weather (e.g., iced cocktails in unusually hot weather), and therefore the owner responds less to negative weather shocks. As noted earlier, columns 6 and 7 of Table 4 show that there is no significant difference between experienced and inexperienced owners in terms of relationship between weather and revenue. These columns use revenue as the dependent variable but add an interaction between weather and two different experience measures. The interactions between weather and experience are all insignificant, suggesting that experienced owners are not better at managing weather shocks. Moreover, Table 5 shows that the transitory component of revenue averages zero with almost identical standard deviations across the different levels of experience and distance. Thus, any significant differences we find in the exit decisions of experienced and inexperienced owners are unlikely to be driven by differences in how the weather shocks affect alcohol revenue.

Credit constraints

The level of owner experience could be correlated with the credit constraints she faces, and this could explain why experienced and inexperienced owners react to revenue variations differently.Footnote 21 In particular, inexperienced owners may react to revenue variations more as they may more likely lack cash reserves or investor/banking connections.

This argument, however, does not explain all results shown in Table 6. First, if inexperienced owners face more credit constraints than experienced owners do, they should react more to persistent revenue variations as well. Cash inflows, after all, bear no mark whether it is generated by the persistent or transitory component. In columns (2) and (3) of Table 6, however, we show inexperienced owners respond less to the persistent component of revenue than experienced owners do. Second, credit constraints cannot explain the distance results in columns (4) and (5). Owners whose mailing address are more than five miles away from bar location, if anything, are more likely to be corporations and chain establishments, which are more likely to have deeper pockets. As shown in these columns, distant owners react more to transitory revenues than nearby owners do, which points to onsite observation and monitoring rather than credit constraints.

We provide Table 7, which investigates the effects of credit constraints, as a contrast to Table 6, which investigate the effects of limited attention. In Table 7, we examine other dimensions of owner attributes that are very likely correlated with credit constraints. In columns 2 and 3, we compare owners without and with an official business name on their tax filings. Compared to owners with a business name on their tax forms (rather than a personal name), these are less established businesses and, therefore, more likely to be subject to credit constraints. We find that owners without a formal business name are indeed more responsive to both transitory and persistent revenue than owners with a formal business name are. Similarly, columns 4 and 5 compare owners of a single establishment to owners of multiple establishments. Owners of multiple establishments may be able to alleviate credit constraints by cross-subsidizing establishments suffering negative shocks. We find that owners of a single establishment are indeed more responsive to both components of revenue than owners with multiple establishments are. There is no asymmetry in the response to transitory and persistent revenue, which is clearly shown in Table 7. The contrast between Tables 6 and 7 suggests that our results on transitory shocks for inexperienced and distant owners are unlikely to be driven by credit constraints.

Projection bias

It is possible that inexperienced owners suffer more projection bias, and therefore overreact to the transitory component of revenue. Projection bias refers to the situation when a decision maker’s prediction of future utility is systematically off in the direction of current utility. For example, Conlin et al., (2007) show that people are overly influenced by current weather when placing catalog orders for cold-weather items. A bar owner may think this month’s bad weather will persist and then exit the business. If more experienced owners have less projection bias, they will respond less to transitory shocks. In short, projection bias is about false expectations on future states given current states, not about inattention to current states.

The project bias explanation, again, does not explain the distance result in Table 6. It also does not explain the results in Table 8, in which we include interaction terms between revenue volatility and the persistent and transitory components of revenue into Eq. (4). We measure revenue volatility by the within-establishment standard deviation of a bar’s log revenue. Results show that owners shift weight from the transitory component to the persistent component under higher revenue volatility. The significantly positive coefficient before the interaction between the transitory component and revenue volatility means that the owners mute reaction to transitory revenue under higher revenue fluctuations. The significantly negative coefficient before the interaction between the persistent component and revenue volatility means that the owner relies more on persistent revenue under higher revenue fluctuations. Such effects hold up for different subgroups, as shown from column 2 to column 5. These results are highly consistent with a rational inattention explanation in Gabaix’s, (2014) framework: owners are able to recognize transitory shocks when attention is warranted because of a more chaotic environment. These results cannot be explained by project bias. Revenue volatility should not affect the owner’s reliance on current states to infer future states as projection bias is based on the instantaneous shocks at the moment of decision making instead of on the distribution of past shocks.Footnote 22

Discussion

Overall, we interpret our descriptive results as consistent with a theory of rational inattention. While we cannot rule out all possible other explanations, the results presented above are not consistent with some of most obvious: skill at smoothing out transitory shocks, credit constraints, and projection bias. Motivated by our evidence consistent with limited attention, we construct a structural model to evaluate the welfare trade offs of rational inattention.

Before detailing our inattention model, it is important to note that we do not model the process of learning to pay attention. We identify a difference between experienced and inexperienced owners, but we cannot say whether that difference is driven by the experienced owners learning the importance of weather or by experienced owners being more (inherently) skilled at recognizing the importance overall. In a traditional learning model, all the information is presented to the decision maker, including weather shocks. Then the decision maker learns the relationship between all this information and profitability. Our inattention model puts some structure on the initial state: Given the large amount of information on numerous dimensions, we provide information on what is obviously relevant on day one and which factors predict which people will pay attention to which information. In this way, our model is a useful step forward toward a model in which owners learn to separate signal from noise.

4 Model

Based on the above stylized facts, we formulate a structural model of attention allocation, belief formation, and exit decisions, in which the owner of an establishment learns about its persistent profitability over time. In this model, an establishment’s underlying profitability is initially unknown to the owner. The owner observes a noisy signal of profitability every period, which is subject to the influence of transitory shocks such as local demand, cost fluctuations, incidental factors, and most importantly, weather variation. The owner’s limited ability to fully attend to the noise in the profit signals prevents her from learning about the true profitability of the establishment. The owner then compares her (potentially biased) expected present discounted value of her establishment with her time-specific outside option when deciding whether the establishment should exit from business. Exiting is the only choice the owner makes. Once exiting, the establishment cannot return.

This outline is similar to standard models in the literature on exit such as Jovanovic, (1982) in the sense that a decision maker updates beliefs using signals of different accuracy.Footnote 23 What is distinct in our model is that we provide a behavioral foundation of attention allocation based on the sparsity-based model of bounded rationality as in Gabaix, (2014). In our model of attention allocation, the owner’s pre-existing experience, her distance from establishment location, and the variances of the establishment revenue affect her exit decisions only through her attention allocation process. The degree to which the owner accounts for past transitory shocks in her exit decision reveals the existence and magnitude of her limited attention. To keep the presentation concise, we will focus on detailing the attention allocation model embedded within an owner's belief formation and exit decision. The full characterization of the model, along with discussions on model identification and estimation details, is deferred to online Appendix C for brevity.

4.1 Transitory shocks in the revenue generating process

At the end of every period t, the owner of an establishment \(j\) receives a revenue record \(R_{jt}\) in each time period, which can be written as:

In Eq. (5), \(\eta_{j}\) is the establishment fixed effect, \(X_{jt}\) is a vector of establishment and market attributes, \(Q_{t}\) is a vector of quarterly dummies, and \(W_{jt}\) is vector of weather shocks as described in Section 2. All \(\alpha ^{\prime}s\) are model parameters to be estimated. The effect of weather shocks on revenue, \(\alpha_{quarter}^{W}\), depends on the quarter.

At the end of Eq. (5), the error term \(\upsilon_{jt}\) is i.i.d. distributed across establishments and across time. We assume \(\upsilon_{jt} \sim N\left( {0,\sigma_{r}^{2} } \right)\). As a time-variant component of an establishment’s revenue record, \(\upsilon_{jt}\) captures all other transitory shocks, for example, local sports team victories, flu season, etc. That is, \(\upsilon_{jt}\) takes the same role as weather shocks, which are transitory shocks that require attention cast by the owner. Therefore, we define \(\omega_{jt}\) as the summation of weather shocks and \(\upsilon_{jt}\)

In Eq. (6), \(\omega_{jt}\) represents the true state of the world, which is the full amount of transitory shocks that the owner can recognize. The amount of attention on \(\omega_{jt}\) depends on the importance of recognizing the true state of the world and the cost of thinking of the decision maker.

4.2 Perception of transitory shocks: a sparsity-based model of bounded rationality

At entry, the owner allocates her attention on \(\omega_{jt}\), which are transitory shocks in the revenue generating process. In this subsection we build a behavioral foundation for potential underestimation or even ignorance of \(\omega_{jt}\), adapting the sparsity-based model of bounded rationality as in Gabaix, (2014). In Gabaix’s model, the decision maker solves an optimization problem featuring a quadratic proxy for the benefits of thinking and a formulation of the costs of thinking. The solution to this problem is an optimally simplified representation of the world that is “sparse”, that is it contains few parameters that are non-zero. The decision maker then chooses the optimal action given this sparse representation of the world.

We set up the following optimization problem as in Gabaix, (2014):

In Eq. (7), the first term is the utility loss from an imperfect representation of the world, and the second term is the penalty for lack of sparsity, representing the cost of thinking about the true state of the world. The owner chooses \(\tau_{j} \in \left[ {0,1} \right]\) to minimize the sum of utility loss and thinking cost. When \(\tau_{j}\) is closer to 1, the utility loss is small but the thinking cost is large; when \(\tau_{j}\) is closer to 0, the thinking cost is small but the utility loss is large. In the utility loss part, we use \(VarR_{j}\), the within establishment variance of revenue \(R_{jt}\), to measure the importance of knowing the true state of the world. When this variance is 0, monthly revenue is a fixed number so there is no need to think about transitory shocks. The higher this variance is, the larger is the loss from not paying attention to \(\omega_{jt}\). In terms of thinking cost, \(\mathop \kappa \limits^{\sim }_{j}\) is the time-invariant thinking cost of the owner. We assume that \(\mathop \kappa \limits^{\sim }_{j}\) follows a Lognormal distribution with mean \(Z_{j} \kappa\) and variance normalized to 1.Footnote 24 That is,

Equation (8) specifies the cost of thinking as a random process. Given the same \(Z_{j}\), different decision makers may have different thinking costs and choose different \(\tau_{j}\) to recognize the impact of transitory shocks. We use owner experience and the distance from the owner’s mailing address to the establishment location as two covariates that shift the mean of the thinking cost distribution. It is important to note that the owner experience and owner distance measures may correlate with owner ability, but we need to cautious about any causal interpretation. In particular, owner experience may measure inherent differences in owner skills rather than the causal impact of experience on behavior. Modeling thinking cost as a stochastic process and linking it to the personal attributes of decision makers is an enhancement of Gabaix, (2014), who models the cost of thinking as a parameter value instead of a function. We think it is useful to model the cost of thinking as potentially heterogeneous across individuals. It enables separate identification of a bar’s underlying profitability and the owner’s cost of thinking.

To complete the attention allocation model, we now take a stand on how much the owner knows about her own thinking cost. It is unrealistic that in a model of inattention a decision maker knows exactly what her thinking cost is or exactly what \(VarR_{j}\) is. We assume that the owner knows the payoffs of the problem as proxied by \(VarR_{j}\),Footnote 25the distribution of her thinking cost, and whether the thinking cost is above or below \(VarR_{j}\). The owner’s solution to the optimization problem characterized by (7) is:

The solution states that the owner mutes her attention to zero when her thinking cost is above \(VarR_{j}\), and that she pays a fixed amount of attention every period when her thinking cost is below \(VarR_{j}\). Equation (9) includes the expectation, \(E\left[ {\mathop \kappa \limits^{\sim }_{j} \left| {\mathop \kappa \limits^{\sim }_{j} \le VarR_{j} } \right.} \right]\) because that the owner does not observe her exact thinking cost (\(\mathop \kappa \limits^{\sim }_{j}\)) and, therefore, forms an expectation of \(\mathop \kappa \limits^{\sim }_{j}\) conditional on \(\mathop \kappa \limits^{\sim }_{j} \le VarR_{j}\). We derive \(E\left[ {\mathop \kappa \limits^{\sim }_{j} \left| {\mathop \kappa \limits^{\sim }_{j} \le VarR_{j} } \right.} \right]\) and hence \(E\left[ {\tau_{j} |\mathop \kappa \limits^{\sim }_{j} \le VarR_{j} } \right]\) in Online Appendix C.7. Note that \(\tau_{j} \in \left[ {0,1} \right]\). If \(\tau_{j} = 1\), the owner pays full attention to \(\omega_{jt}\); if \(\tau_{j} < 1\), she pays muted attention; if \(\tau_{j} = 0\), she pays zero attention. Zero attention means that the owner has no ability to separate transitory shocks out of the revenue record.

Appendix C describes how the owner takes the bounded rationality parameter \(\tau_{j}\) to interpret the noisy revenue signal \(R_{jt}\) she receives every period. With the (potentially biased) interpretation, she updates her belief about the underlying profitability of the establishment, compares the present discounted value of her future profits with her outside option, and decides to exit. To summarize, we have a structural model based on standard Bayesian learning from repeated signals of revenues. We inject a modicum of bounded rationality into this model by allowing imperfect recognition of the impact of transitory shocks on these signals. This particular dimension of limited attention is the focus of this project. Quantifying the magnitude of limited attention in our data gives us a measure of bounded rationality in a high-stakes business setting.

5 Structural results

5.1 Model estimates

We present our key structural estimates in Table 9 (with the full set of parameters in Online Appendix Table 5). In column (1), we use owner experience, measured by a dummy variable indicating whether the owner has owned a bar/restaurant in the 3 years before opening the focal establishment in the cost of thinking function. In column (3), we use owner experience, measured in the log number of establishment-months the owner has operated in 3 years before opening the focal establishment in the cost of thinking function. In columns (2) and (4), we add a dummy variable indicating whether the distance from owner mailing address to establishment location is greater than 5 miles into the column (1) and (3) specifications respectively. All four models fit the data well. In particular, the average and variance of the simulated exit probability are almost the same as those of observed exit probability.

In the thinking cost function, we see both owner experience and distance to owner play a statistically significant role. Qualitatively, owner experience lowers thinking cost, while distance to owner increases it. Such effects are statistically significant for owner experience in all specifications, but lose some statistical power for distance to owner in column 4.

The magnitude is not straightforward to interpret by looking at these coefficients, as the extent of limited attention is a non-linear function of model parameters and data variation. These estimates suggest a high prevalence of inattention. Of the 8,995 owners in our data, an average owner’s probability of paying zero attention ranges from 76 to 87%. Even if an owner is paying attention, her attention is limited, on average. Conditional on paying some attention, the mean amount of attention (denoted by \(E\left( {\tau_{j} |\tau_{j} \ge 0} \right)\)) ranges from 0.32 to 0.39 across specifications. The unconditional mean amount of attention (denoted by \(E\left( {\tau_{j} } \right)\)) is even lower, ranging from 0.07 to 0.17 across specifications. Taubinsky and Rees-Jones, (2018) find that consumers underreact to non-salient sale taxes as if the taxes were only 25% of their size. Chetty et al., (2009) find this number to be 6% for alcoholic beverages and 35% for grocery store purchases. Our estimate \(E\left( {\tau_{j} } \right)\) has a similar interpretation and falls into the same range.

Also like this prior research, we find substantial heterogeneity in attention allocation, reflected by the estimated variance of inattention. Heterogeneity in attention is driven by a large, significantly negative estimate of the effect of owner experience on thinking costs. Experienced owners have lower cost of thinking relative to the variance of transitory shocks, allowing them to recognize the existence of transitory shocks in their revenue signals. The largest barrier seems to be whether an owner pays attention at all. Once an owner crosses the barrier, the heterogeneity is smaller.

5.2 Welfare trade offs of paying attention

Next, we assess the cost and benefit of paying attention. In our model, paying attention is valuable if it leads to better decision-making. It can be very costly because the owner must pay attention in all periods up to the point when decisions with and without attention differ. To capture this trade off, we first simulate exit events under our estimated model (“estimated attention simulation”), and then simulate exit events under the assumption that every owner has \(\tau_{j} = 1\) (labeled the “full attention simulation”). In all simulations presented in Table 10 (and Appendix Tables D.1 and D.2), we use the estimated structural parameters corresponding to column 4, Table 9.

We find that roughly 3.9% of the 8,995 bars — 351 bars — would have made a better decision in the operating history of the full attention simulation. We regard this magnitude to be consistent with our priors. It is not so large to suggest that paying attention to these transitory shocks is of first order importance, nor so small that it has a negligible aggregate impact. For these 351 bars, we can express the cost and benefit of paying full attention in dollars. The cost is estimated from the cost of thinking function. The cost for a bar owner in any month is how much revenue the owner would have to pay (or receive) so that the owner forms the correct belief about her bar’s monthly profitability as if she pays full attention. The benefit is estimated from the penalty of incorrect decisions. It is how much a bar’s owner is willing to pay (or receive) in order to avoid incorrect staying or exit decisions in the month where decisions differ.Footnote 26 To evaluate both cost and benefit on a monthly basis, we divide total cost and total benefit by the number of months leading up to the month where decisions differ between the full attention simulation and the estimated attention simulation.

Panel A of Table 8 reports the cost and benefit analysis of paying full attention for these 351 bars. The first two rows report summary statistics about the total cost or benefit for a bar. The next two rows report the same summary statistics per establishment-month. These numbers clearly indicate that the cost of paying full attention dominates the benefit of doing it. Although the benefit is equivalent to roughly $2,000 for a median bar, the cost is roughly $15,000.Footnote 27 Both benefit and cost are highly skewed to the right, reflected by much higher means than medians. There is significant heterogeneity across bars. For some bars, the incorrect timing of exit has catastrophic consequences, but paying full attention to avoid these incorrect decisions is nevertheless too costly ex ante.

5.3 The value of having an experienced owner

Given the substantial cost of paying attention, a natural question is what alleviates the burden so that the owners make better decisions. In our estimated model, it points to the owner’s pre-existing experience before opening a bar. Most owners (81%) have no such experience; among the owners with such experience, it can range from 1 month to more than 10 years. Experienced owners have a lower cost of thinking, so the owner pays more attention to transitory shocks and, in turn, makes better decisions. Using our estimated model and simulations, we can translate this value into dollar amounts: It is how much a bar’s owner is willing to pay (or receive) to make better decisions as if she had a certain number of years in experience.

Looking owners whose decisions would be improved if they made decisions like owners with more years of experience, Panel B of Table 8 reports that, on average, the value of having an experienced owner is large. Specifically, gaining one year of experience is equivalent to about $900 monthly for a median bar, gaining three years $1,100, and gaining ten years $1,400. One way to think about these numbers is that they are salary premiums the bar might be willing to pay for managers with additional experience in the profession. Under this interpretation, the salary premium associated with one year of industry experience is about $11,000 a year ($900 × 12 months), while the salary premium associated with ten years of industry experience about $17,000 a year ($1,400 × 12 months). These averages mask significant heterogeneity. This heterogeneity in the value of experience is correlated with traits of the individual decision makers (for example, the value of additional experience is small if the owner is already an industry veteran) and attributes of the business environment (for example, the value of experience is small if business is very stable, with little month-to-month variation).Footnote 28 Overall, our results point to an understudied area of firm-level heterogeneity: heterogeneity in the ability to attend to information in decision-making.

6 Conclusion

In this paper, we document the incidence of inattention in firm decisions and propose a likely mechanism through which deficient attention may have economic consequences. Transitory shocks, such as weather shocks, should be netted out of the expectation of future profitability, but inattentive decision makers may not be able to perform the decomposition and hence overreact to these temporary shocks. We leverage the exogeneity and unpredictability of weather to separate the attentive and inattentive decisions. By estimating a model of exit decisions with an attention allocation pre-stage, we are able to assess the extent to which the owner accounts for past weather shocks. Our results suggest the presence of inattention. We are able to gauge the economic magnitude of this firm-level limited attention problem and evaluate the value of experience. In doing so, we contribute to the recent effort to introduce behavioral deviations into the field of empirical industrial organization. The evidence is this paper is consistent with prior work on consumer and investor inattention and is therefore a step toward understanding limited attention at a larger scale.

Somewhat more speculatively, our results provide insight into the fundamental determinants of market structure, competitiveness, and performance. In the United States, 13.9 million new firms entered between 1991 and 2009, while 12.3 million firms exited over the same period (Elfenbein & Knott, 2015). A better understanding of various factors behind a firm’s exit serves to inform regulatory, antitrust, and trade policies on competition. As documented by previous empirical work (Dunne et al., 1988), there is considerable heterogeneity in firm survival by type of entrant within an industry and significant correlations in entry and exit rates across industries. Our work provides a plausible explanation for these stylized facts. If decision makers are subject to different degrees of bounded rationality, their exit decisions will capture this heterogeneity and affect the extent of market competitiveness. If inexperienced managers of good firms often exit too early because of bad luck, then this will reduce competitiveness and enable weaker firms to persist. Perhaps more importantly, bounded rationality may well mark other business decisions. For example, poorly made entry decisions will lead to ex-post regret and consequently hasty exits, implying positively correlated entry and exit rates. While we model only the exit decision here, we believe our results help inform our understanding of the potential role for bounded rationality in the rich, diverse, and often puzzling patterns others have observed in firm turnover and industry structure.

As final concluding remarks, we acknowledge some important limitations of this project. First, we cannot separately identify whether the measured difference in experience is driven by selection effects (better bar owners open a second bar) or the causal effects of experience. The best claim we can put on our results is that experience correlates with the owner’s ability to cast attention. Although there is prior laboratory and field work that documents how experience generally leads to better decision making (summarized by Al-Ubaydli & List, 2016), we do not have an identification strategy to distinguish the selection and causal channels of owner experience. Second, our structural analysis relies on strong parametric assumptions in the decision maker’s attention allocation problem (as well as how she updates her beliefs using a Bayesian learning model) to evaluate the monetary loss due to the incidence of inattention. Consequently, the exact magnitudes of the loss should be taken with a grain of salt. Third, our estimates are small and somewhat noisy. Therefore, we interpret our results as suggestive. A cautious interpretation could see this paper as a proof of concept about how differences between experienced and inexperienced firm owners can be used to understand bounded rationality in a real business setting. Lastly, in our bounded rationality framework, we still allow for a substantial degree of rationality. Our model presumes that the bar owners are capable of sophisticated calculation, which may not hold in reality. We only examine one dimension of sparsity and one dimension of bounded rationality. We choose these particular dimensions in order to more precisely understand one type of friction in a firm’s decision-making process. With this caveat, the credibility of the magnitudes of our welfare results are subject to our peculiar assumptions on what types of limited rationality are at play in firm decisions and how exactly these behavioral biases manifest themselves. Despite these limitations, we aspire to stimulate future research into limited attention, bounded rationality, and more fundamentally, the black box of imperfect decision-making at the firm level.

Data availability

We will make our code available, and the publicly available data. The alcohol revenue data is not publicly available, but we will provide interested researchers with the steps needed to request, access, and use the data.

Notes

More work in a similar vein studies a wide range of settings: “buy-it-now” options on eBay (Malmendier and Lee, 2011), packaged grocery (Clerides and Courty, 2017), state taxes (Chetty et al., 2009, Taubinsky and Rees-Jones, 2018), financial services (Stango and Zinman, 2014), insurance (Handel, 2013, Ho et al. (2015), and electricity bills (Hortacsu, Madanizadeh and Puller, 2017).

For example, it does not seem to be part of standard advice to starting restauranteurs: In the 908-page Restaurant Manager’s Handbook (Brown, 2007), the weather is not mentioned as a profit driver.

Boldin and Wright (2015) find that deviations in weather from seasonal norms can shift the monthly payroll numbers by more than 100,000 in either direction, and the Central Bankers using current major macroeconomic indicators completely ignore such effects.

Our counterfactual simulations show that experience is especially useful in reducing welfare loss due to incorrect inference when the bar is hit with negative shocks. As transitory shocks can be interpreted as luck, our model implies that an owner’s experience helps her to recognize the role of lucky or unlucky events. When the firm is unlucky, the owner needs experience as a substitute to correctly assess the situation and avoid a potentially costly error. This contrasts with the existing literature viewing skill and luck in entrepreneurship as complementary (e.g. Plehn-Dujowich, 2010; Gompers et al., 2006).

A small but growing literature documents the incidence of limited attention and assesses the welfare trade-offs of a decision maker’s inattention. These papers recover primitive parameters in consumer preferences so they are able to perform counterfactual analysis to evaluate welfare trade-offs (e.g. Grubb and Osborne, 2015; Lacetera, Pope and Sydnor 2012). This literature shows that public policies aiming to improve consumer attention can have large welfare-enhancing effects.

When we refer to bars and restaurants together, we call them “establishments”.

As noted above, we believe that ownership changes are not a useful measure of exit because such a change could be a good or bad outcome to the owner, depending on the circumstances.

Bankruptcy is relatively rare, and it is difficult to track down comprehensive data and match it to the individual taxpayers. Therefore, we do not use it as a measure in our setting.

Investigating whether the chain may provide value in reducing boundedly rational decisions of managers would require data on whether each individual establishment has the same decision maker. Some large chains do appear to use the same taxpayer identification and address while others do not. While this might be indicative of the existence of franchise arrangements, we do not have data to confirm this. For this reason, we only keep owners that never own 25 or more establishments in their operating history.

The data is available at https://www.ncdc.noaa.gov/cdo-web/datasets.

The heat index is a function of daily mean temperature and relative humidity, as defined by the National Weather Service (see https://www.wpc.ncep.noaa.gov/html/heatindex_equation.shtml). All our empirical results are robust to using daily mean temperature instead of heat index.

We define a business name as separate from an individual owner as the listed taxpayer containing information that suggested a company or business (“LLC”, “Inc.”, “bar”, “ranch”, “of”, “Dallas”, etc.). By inspection, we identified 458 such strings. The remaining bar owners were listed as individuals or pairs of individuals.

The mean of revenue is about $53,000 in 2015 dollars, far above the median of $32,000. The skewness of the revenue distribution is almost 8, while the skewness of the natural logarithm of the revenue is close to 0.

Note that notation in Section 3 does not carry on to the structural model.

Columns 6 and 7 show that experienced owners are not significantly different from inexperienced owners in terms of the relationship between the weather and their revenue. We will return to this result below in discussing alternative explanations.

We report results by quarter and experience in Online Appendix Table 6, and by quarter and distance in Online Appendix Table 7. In addition, Online Appendix Table 8 shows that our main results are robust to alternative functional forms in creating the decomposition, for example, a spline for the heat index, allowing serial correlation of error term over time, using establishment random effects, etc. We interpret this robustness to suggest the linear functional form we use in our main specification captures the key relationships in the data. We also examine robustness to alternative samples: using owners with only a single establishment, dropping extreme weather, and finally, using restaurants instead of bars.

Time-invariant owner attributes include owner experience, distance from owner to establishment location, whether the owner has just a single establishment, and whether the owner’s name is not an official business name.

We perform a Wald test of linear hypotheses that the coefficients of transitory revenue and persistent revenue are equal and report the test statistics at the bottom of Table 4. In column 1 the significant level of the test is 77.4% and thus we cannot reject the null hypothesis that these two coefficients are equal.

Online Appendix Table 9 to 11 show the robustness of this asymmetric response result. In general, the results hold up strongly with the exception of using restaurants instead of bars. For restaurants, the first asymmetry result holds up: inexperienced restaurant owners do respond more to the transitory component than experienced ones do. The second asymmetry result breaks down: experienced restaurant owners respond more to the transitory component than to the persistent component. As alcohol revenue is a much smaller part of restaurant revenue, we believe the results on bars are more informative.

We do not know how this bias will affect results across different types of owners; if the attenuation bias affects experienced owners more, we may lose our results on the asymmetric responses to transitory revenue across types.

Holtz-Eakin, Joulfaian, and Rosen (1994) and Andersen and Nielsen (2012) show that new firm survival is related to the liquidity constraints, using owners’ inheritances for identification.

This argument is inspired by Busse et al, (2015), which propose a method to distinguish projection bias from salience (paying attention). They argue that projection bias predicts overreaction to shocks in an absolute sense, but salience takes effect when the decision maker observes shocks relative to some benchmark.

We normalize the variance to be 1 because multiplying the same constant with \(\mathop \kappa \limits^{\sim }_{j}\) and \(VarR_{j}\) gives us the same answer in Eq. (9). Similarly, Eq. (9) shows that adding the same constant to \(\mathop \kappa \limits^{\sim }_{j}\) and \(VarR_{j}\) only affect the solution marginally (and through functional form). In the attention allocation problem, what matters is the relative importance of the owner attributes compared to the expected benefit of attention. Therefore, we do not have a constant term in the mean of \(\mathop \kappa \limits^{\sim }_{j}\).

The owner could have done research about the chosen location of their establishment and understood the variance of profit from month-to-month operations.

In our simulations, we assume that exit decisions are permanent: once a bar exits, it cannot return to business. This assumption makes incorrect exit decisions and incorrect staying decisions asymmetric when we calculate welfare trade-offs. Avoiding an incorrect staying decision typically yields a benefit over just one period. Avoiding an incorrect exit decision yields a benefit over multiple (consecutive) periods.

A thinking cost this high is likely driven by our distributional assumption in Eq. (8) –- the lognormal distribution is highly skewed to the right.

Appendix D further discusses the relationship between experience and luck. Table D.1 shows that owner experience reduces welfare loss due to inattention, especially when a bar is hit with a sequence of bad luck. This suggests experience and luck act like substitutes instead of complements.

References

Abbring, J. H., & Campbell, R. J. (2005). A firm’s first year discussion paper 2005-046/3. Tinbergen Institute.

Abbring, J. H., & Campbell, R. J. (2003). A structural empirical model of firm growth, learning, and survival. NBER Working paper 9712.

Abel, A. B., Eberly, J. C., & Panageas, S. (2013). Optimal inattention to the stock market with information costs and transactions costs. Econometrica, 81(4), 1455–1481.

Aguirregabiria, V., & Jeon, J. (2020). Firms’ beliefs and learning: models, identification, and empirical evidence. Review of Industrial Organization, 56, 203–235.

Al-Ubaydli, O., & List, J. (2016). Field experiments in markets. NBER Working paper #2213. https://doi.org/10.3386/w22113

Andreas, K., & Rao, R. S. (2023). Behavioral Skimming Theory and Evidence from Resale Markets. Working paper.

Backus, M., Blake, T., Masterov, D., & Tadelis, S. (2022). Expectation, disappointment, and exit: evidence on reference point formation from an online marketplace. Journal of the European Economic Association, 20(1), 116–149.

Bertrand, M., & Schoar, A. (2003). Managing with style: the effect of managers on firm policies. The Quarterly Journal of Economics, 118, 1169–1208.

Boldin, M., & Wright, J. H. (2015). Weather-Adjusting Economic Data. Brookings Papers on Economic Activity (pp. 227–260). https://www.brookings.edu/wpcontent/uploads/2016/07/PDFBoldinTextFallBPEA.pdf

Brown, D. R. (2007). The Restaurant Manager’s Handbook: How to Set Up, Operate, and Manage a Financially Successful Food Service Operation. Revised Fourth edition. Atlanta Publishing Group Inc.