Abstract

The risk of market exit that business firms face is significant and differs widely across countries. This paper explores the links between countries’ business conditions and the exit risk at the country level. We set up a general equilibrium model which allows us to derive sharp predictions concerning how key factors which shape a country’s business and trade environment impact on the exit risk of firms which operate in these environments. The model is able to explain the negative correlation between countries’ average labor productivity and the perceived risks of exit borne out in the facts and its predictions accord with evidence on country differences in business conditions.

Similar content being viewed by others

Notes

Using a panel of manufacturing plants in the U.S., Dunne et al. (1988), Baily et al. (1992), Doms et al. (1995) and Bernard et al. (2006) show that productivity has a sizable negative effect on the probability of firm exit. Similar findings have been obtained for the UK (Disney et al. 2003), France (Bellone et al. 2006), Sweden (Greenaway et al. 2008), Spain (Esteve-Pérez and Mañez-Castillejo 2008) and Portugal (Carreira and Teixeira 2011).

We abstract from the business cycle and from short-run adjustment. We also refrain from considering a richer microeconomic environment (e.g. competition, investments, bankruptcy laws) that an IO analysis would push for. See Atkeson and Burstein (2010).

Our assumptions on the traditional sector and the quasi-linear utility fix the real wage (and the terms of trade) and remove income effects from the modern sector, respectively. This gives the framework a partial equilibrium flavor, but does not remove the interaction between product and labor markets such that we still have a full-fledged trade model (see e.g. Tabuchi and Thisse 2006). Note also that quasi-linear preferences have been shown to “behave reasonably well in general equilibrium settings” (Dinopoulos et al. 2011).

Our model uses continuous time so that the initial time span is infinitesimally small. However, exploring our model economically makes it necessary to translate the concept of “points in time” to reality and interpret it as a small and limited amount of time, e.g. one or 2 years.

If G a (ϕ) stochastically dominates G b (ϕ) in terms of the hazard rate order, then firms drawing from G a (ϕ) have a greater chance of getting a higher productivity than firms drawing from G b (ϕ). See appendix D for details.

The equilibrium under autarky is easily derived by assuming t i → ∞ so that f xi j i (t i ) → 0.

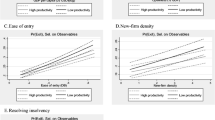

Great efforts have been made to develop statistics on firm dynamics in many countries in recent years (see Dunne et al. 2009). These efforts have largely been independent, however, and so the data reflect strong country idiosyncrasies. For example, in contrast to Germany, countries like Spain, Italy and Greece do not embrace small enterprises in their statistics. Hence their insolvency rates are biased downwards. Moreover, in Mediterranean countries firms often choose less formal and juridical ways to deal with bankruptcy which are also not included in the data (e.g. a settlement or a moratorium, see CreditReform 2007, 2009). An important recent initiative involving researchers from more than 20 countries has started to standardize data definitions and to construct comparable statistics. However, despite intensive efforts measurement differences still exist (see Bartelsman et al. 2009).

In 2009, Creditreform conducted a survey among German export firms about their experience in their export markets. PIR reflects perceptions of more than 360 firms, with more than 50 % of them having export experience for more than 25 years. We are aware that the number of respondents is relatively limited, but we hope that it spurs research and greater advances in the field of international comparability of firm exit rates.

References

Atkeson A, Burstein AT (2010) Innovation, firm dynamics, and international trade. J Polit Econ 118(3):433–484

Baily MN, Hulten CR, Campbell D (1992) Productivity dynamics in manufacturing plants. Brookings Papers on Economic Activity, Microeconomics 1992. 187–249

Bartelsman E, Haltiwanger, Scarpetta S (2009) Measuring and analyzing cross-country differences in firm dynamics. In: Dunne T, Jensen JB, Roberts MJ (eds) Producer dynamics. New evidence from micro data. University of Chicago Press, Chicago and London

Bellone F, Musso P, Nesta L, Quéré M (2006) Productivity and market selection of French manufacturing firms in the nineties. Revue de l’OFCE 97bis. 319–349

Bernard AB, Jensen JB, Schott PK (2006) Survival of the best Fit: exposure to low wage countries and the (Uneven) growth of US manufacturing plants. J Int Econ 68(1):219–237

Bernard AB, Jensen JB, Schott PK (2009) Importers, exporters, and multinationals: a portrait of firms in the U.S. that trade goods. In: Dunne T, Jensen JB, Roberts MJ (eds) Producer dynamics. New evidence from micro data. University of Chicago Press, Chicago and London

Bohnstedt A, Schwartz C, Südekum J (2012) Globalization and strategic research investments. Res Policy 41(1):13–23

Carreira C, Teixeira P (2011) The shadow of death: analysing the pre-exit productivity of Portuguese manufacturing firms. Small Bus Econ 36(3):337–351

Colantone I, Sleuwaegen L (2010) International trade, exit and entry: a cross-country and industry analysis. J Int Bus Stud 41(7):1240–1257

Colantone I, Coucke K, Sleuwaegen L (2010) Low-cost import competition. Do small firms respond differently? Open Access publications from Katholieke Universiteit Leuven Nr. 123456789/264494

CreditReform (2007) Insolvenzen in Europa, Jahr 2006/07, Verband der Vereine Creditreform e.V., available online on www.creditreform.at

CreditReform (2009) Insolvenzen in Europa, Jahr 2008/09, Verband der Vereine Creditreform e.V., available online on www.creditreform.at

Demidova S (2008) Productivity improvements and falling trade costs: Boon or Bane. Int Econ Rev 49(4):1437–1462

Demidova S, Rodríguez-Clare A (2009) Trade policy under firm-level heterogeneity in a small economy. J Int Econ 78(1):100–112

Dinopoulos E, Fujiwara K, Shimomura K (2011) International trade and volume patterns under Quasilinear preferences. Rev Dev Econ 15(1):154–167

Disney R, Haskel J, Heden Y (2003) Restructuring and productivity growth in UK manufacturing. Econ J 113(489):666–694

Djankov S, La Porta R, Lopez-de-Silanes F, Shleifer A (2002) The regulation of entry. Q J Econ 117(1):1–37

Doms M, Dunne T, Roberts MJ (1995) The role of technology use in the survival and growth of manufacturing plants. Int J Ind Organ 13(4):523–542

Dunne T, Roberts MJ, Samuelson L (1988) Patterns of firm entry and exit in U.S. manufacturing industries. RAND J Econ 19(4):495–515

Dunne T, Jensen JB, Roberts MJ (2009) Producer dynamics. New evidence from micro data. University of Chicago Press, Chicago and London

Esteve-Pérez S, Mañez-Castillejo JA (2008) The resource-based theory of the firm and firm survival. Small Bus Econ 30(3):231–249

Greenaway D, Gullstrand J, Kneller R (2008) Surviving globalisation. J Int Econ 74(2):264–277

Hopenhayn (1992) Entry, exit, and firm dynamics in long-run equilibrium. Econometrica 60:1127–1150

Melitz M (2003) The impact of trade on intra-industry reallocations and aggregate industry productivity. Econometrica 71(6):1695–1725

Melitz M, Ottaviano G (2008) Market size, trade, and productivity. Rev Econ Stud 75:295–316

Pflüger M, Suedekum J (2013) Subsidizing firm entry in open economies. J Public Econ 97(1):258–271

Redding S (2011) Theories of heterogeneous firms and trade. Annu Rev Econ 3:77–105

Tabuchi T, Thisse J-F (2006) Regional specialization, urban hierarchy, and commuting costs. Int Econ Rev 47(4):1295–1317

World Bank (2010) Doing Business 2010. The World Bank

Acknowledgements

We thank Daniel Bernhofen, Rainald Borck, Carsten Eckel, Andreas Haufler, Christian Holzner, Richard Kneller, Johann Lambsdorff, Dominika Langenmayr, Jörg Lingens, Philipp Schröder, Jens Südekum, Zhihong Yu, the participants of workshops and conferences in Aarhus (School of Business), Glasgow (EEA), Lausanne (ETSG), Münster, Munich and Nottingham (GEP) and two anonymous referees for their stimulating comments on previous versions of this paper. Financial support from Deutsche Forschungsgemeinschaft (DFG) through PF 360/5–1 is gratefully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendices

1.1 Appendix A-The Comparative Statics of the Exit Rates

Mature firm concept. Take the derivative of \( E{{\left[ {\delta {{{\left( \phi \right)}}^{-1 }}\left| {\phi > {\phi^{*}}} \right.} \right]}^{-1 }}=\left[ {1-G\left( {{\phi^{*}}} \right)} \right]{{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi } \right]}^{-1 }} \) with respect to ϕ *. This yields \( \frac{{dE{{{\left[ {\delta {{{\left( \phi \right)}}^{-1 }}\left| {\phi > {\phi^{*}}} \right.} \right]}}^{-1 }}}}{{d{\phi^{*}}}}=g\left( {{\phi^{*}}} \right){{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\frac{{g\left( \phi \right)}}{{\delta \left( \phi \right)}}} d\phi } \right]}^{-1 }}\left[ {\frac{{1-G\left( {{\phi^{*}}} \right)}}{{\delta \left( {{\phi^{*}}} \right)}}{{{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\frac{{g\left( \phi \right)}}{{\delta \left( \phi \right)}}} d\phi } \right]}}^{-1 }}-1} \right]<0 \).

We find that \( {{{dE{{{\left[ {\delta {{{\left( \phi \right)}}^{-1 }}\left| {\phi > {\phi^{*}}} \right.} \right]}}^{-1 }}}} \left/ {{d{\phi^{*}}}} \right.} > 0 \) iff \( {{{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\delta \left( {{\phi^{*}}} \right)\delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi } \right]}} \left/ {{\int\nolimits_{{{\phi^{*}}}}^{\infty } {g\left( \phi \right)} d\phi }} \right.} > 1 \), which holds true for any density g(ϕ) as δ(ϕ *) > δ(ϕ)

The failing start-up concept. Substituting \( E{{\left[ {\delta {{{\left( \phi \right)}}^{-1 }}\left| {\phi > {\phi^{*}}} \right.} \right]}^{-1 }}=\left[ {1-G\left( {{\phi^{*}}} \right)} \right]{{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi } \right]}^{-1 }} \) into the risk of start up failure yields \( G\left( {{{\phi }^{*}}} \right){{M}_{e}}/M = G\left( {{{\phi }^{*}}} \right)/\int_{{{{\phi }^{*}}}}^{\infty } {\delta {{{\left( \phi \right)}}^{{ - 1}}}g\left( \phi \right)} d\phi \) which is increasing in ϕ * (as G(ϕ *) rises whereas \( \int\nolimits_{{{\phi^{*}}}}^{\infty } {\delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi \) decreases in ϕ * as \( \delta {{\left( \phi \right)}^{-1 }}g\left( \phi \right)>0 \)).

The overall exit rate. We use \( E{{\left[ {\delta {{{\left( \phi \right)}}^{-1 }}\left| {\phi > {\phi^{*}}} \right.} \right]}^{-1 }}=\left[ {1-G\left( {{\phi^{*}}} \right)} \right]{{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi } \right]}^{-1 }} \) in the overall exit rate to get \( {{{{M_e}}} \left/ {M} \right.}={{\left[ {\int\nolimits_{{{\phi^{*}}}}^{\infty } {\delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi } \right]}^{-1 }} \) which increases in ϕ *as \( \delta {{\left( \phi \right)}^{-1 }}g\left( \phi \right)>0 \).

1.2 Appendix B-The Link Between the Productivity Cutoffs in the Open Economy

-

(i)

We depart from the ratios of the ZCPCs \( {r_i}\left( {\phi_i^{*}} \right)=\sigma {w_i}{f_i} \) and \( {r_{xi }}\left( {\phi_{xi}^{*}} \right)=\sigma\,{w_i}\,{f_{xi }} \), where \( {r_i}(\phi_i^{*}) \) and \( {r_{xi }}\left( {\phi_{xi}^{*}} \right) \) are home (export) market profits of firms from country i and follow the procedure in Demidova (2008) and get \( \phi_{xi}^{*}={{\left( {{{{{w_i}}} \left/ {{{w_j}}} \right.}} \right)}^{{\sigma /\left( {\sigma -1} \right)}}}{t_i}\phi_j^{*} \) where \( {t_i}\equiv {\tau_{ij }}{{\left( {{f_{xi }}/{f_j}} \right)}^{{1/\left( {\sigma -1} \right)}}} \).

-

(ii)

We assume that only firms that serve the domestic market can export, i.e. \( \phi_{xi}^{*} > \phi_i^{*} \). This holds true if \( {\tau_{ij }}{{\left( {{f_{xi }}/{f_i}} \right)}^{{1/\left( {\sigma -1} \right)}}}\left( {{P_i}/{P_j}} \right){{\left( {{L_i}/{L_j}} \right)}^{{1/\left( {\sigma -1} \right)}}} > 1 \). With \( {P_i}={{\left( {\beta {L_i}/\sigma {f_i}} \right)}^{{1/\left( {1-\sigma } \right)}}}w_i^{{\sigma /\left( {\sigma -1} \right)}}{{\left( {\rho \phi_i^{*}} \right)}^{-1 }} \) this becomes \( {f_{xi }}/{f_j} > \tau_{ij}^{{1-\sigma }}{{\left( {{w_j}/{w_i}} \right)}^{\sigma }}{{\left( {\phi_i^{*}/\phi_j^{*}} \right)}^{{\sigma -1}}} \) (The price index follows from \( {P_i}=M_{ti}^{{1/\left( {1-\sigma } \right)}}p\left( {{{{\widetilde{\phi}}}_{ti }}} \right) \) where \( {M_{ti }}\equiv {M_i}+{M_{xj }} \) is the mass of all (domestic and foreign) firms selling their products in i and \( {{\widetilde{\phi}}_{ti }}\equiv {{\left[ {\left( {{1 \left/ {{{M_{ti }}}} \right.}} \right)\left\{ {\int\nolimits_{{\phi_i^{*}}}^{\infty } {{\phi^{{\sigma -1}}}{M_i}\left( \phi \right)d\phi } +{{{\left( {{{{{w_j}}} \left/ {{{w_i}}} \right.}} \right)}}^{{1-\sigma }}}{{{\left( {{\tau_{ji }}} \right)}}^{{1-\sigma }}}\int\nolimits_{{\phi_{xj}^{*}}}^{\infty } {{\phi^{{\sigma -1}}}{M_{xj }}\left( \phi \right)d\phi } } \right\}} \right]}^{{{1 \left/ {{\left( {\sigma -1} \right)}} \right.}}}} \) a measure of their average productivity. Consumer in i spend \( {M_{ti }}\,{r_i}\left( {{{{\widetilde{\phi}}}_{ti }}} \right)=\beta {L_i} \) on heterogeneous goods. With \( {r_i}\left( {{{{\widetilde{\phi}}}_{ti }}} \right)={{\left( {{{{\widetilde{\phi}}}_{ti }}/\phi_i^{*}} \right)}^{{\sigma -1}}}{r_i}\left( {\phi_i^{*}} \right) \) and \( {r_i}\left( {\phi_i^{*}} \right)=\sigma\,{w_i}\,{f_i} \) we get \( {M_{ti }}=\beta {L_i}{{\left( {{{{\widetilde{\phi}}}_{ti }}/\phi_i^{*}} \right)}^{{1-\sigma }}}/\sigma\,{w_i}{f_i} \)).

1.3 Appendix C: The Equilibrium Condition in the Open Economy

The free entry condition (FEC) states that the value of entry is zero in equilibrium, \( {v^E}\equiv E\left[ {\sum\nolimits_{t=0}^{\infty } {{{{\left( {1-\delta \left( \phi \right)} \right)}}^t}\pi \left( \phi \right)} } \right]-w\,{f_e}=E\left[ {\pi \left( \phi \right)/\delta \left( \phi \right)} \right]-w\,{f_e}=0 \). Under international trade, the FEC for country i is as stated in section 4. As \( {\pi_i}\left( \phi \right)={r_i}\left( \phi \right)/\sigma - > {w_i}{f_i} \), the expected profits become \( E\left[ {\left. {{{{{\pi_i}\left( \phi \right)}} \left/ {{\delta \left( \phi \right)}} \right.}} \right|\phi >\phi_i^{*}} \right]={{{E\left[ {\left. {{{{{r_i}\left( \phi \right)}} \left/ {{\delta \left( \phi \right)}} \right.}} \right|\phi >\phi_i^{*}} \right]}} \left/ {\sigma } \right.}-{w_i}{f_i}E\left[ {\left. {\delta {{{\left( \phi \right)}}^{-1 }}} \right|\phi >\phi_i^{*}} \right] \). We use \( r\left( \phi \right)={{\left( {\phi /{\phi}^{\prime}} \right)}^{{\sigma -1}}}r\left( {\phi^{\prime}} \right) \) where \( \phi_i^{{\prime \sigma -1}}\equiv E\left[ {\left. {{{{{\phi^{{\sigma -1}}}}} \left/ {{\delta \left( \phi \right)}} \right.}} \right|\phi >\phi_i^{*}} \right] \) to write the expected profits as \( {\pi_i}\left( {\phi_i^{\prime }} \right)-{w_i}{f_i}\left( {E\left[ {\left. {\delta {{{\left( \phi \right)}}^{-1 }}} \right|\phi >\phi_i^{*}} \right]-1} \right) \). \( E\left[ {\left. {{{{{\pi_{xi }}\left( \phi \right)}} \left/ {{\delta \left( \phi \right)}} \right.}} \right|\phi >\phi_{xi}^{*}} \right]={\pi_{xi }}\left( {{{{\phi^{\prime}}}_{xi }}} \right)-{w_i}{f_{xi }}\left( {E\left[ {\left. {\delta {{{\left( \phi \right)}}^{-1 }}} \right|\phi >\phi_{xi}^{*}} \right]-1} \right) \) follows by analogy. The zero cutoff profit conditions (ZCPCs) are defined by \( {r_i}\left( {\phi_i^{*}} \right)=\sigma\,{w_i}{f_i} \) and \( {r_{xi }}\left( {\phi_{xi}^{*}} \right)=\sigma\,{w_i}{f_{xi }} \). Using \( r\left( {\phi \prime } \right)={{\left( {\phi \prime /{\phi^{*}}} \right)}^{{\sigma -1}}}r\left( {{\phi^{*}}} \right) \), we get \( {\pi_i}\left( {\phi_i^{\prime }} \right)=\left[ {{{{\left( {{{{\phi_i^{\prime }}} \left/ {{\phi_i^{*}}} \right.}} \right)}}^{{\sigma -1}}}-1} \right]{w_i}{f_i} \) (domestic ZCPC) and \( {\pi_{xi }}\left( {\phi_{xi}^{\prime }} \right)=\left[ {{{{\left( {{{{\phi_{xi}^{\prime }}} \left/ {{\phi_{xi}^{*}}} \right.}} \right)}}^{{\sigma -1}}}-1} \right]{w_i}{f_{xi }} \) (export ZCPC). Plug the ZCPCs into the FEC, substitute \( \phi _{i}^{{\prime \sigma - 1}} \equiv E\left[ {\left. {{{\phi }^{{\sigma - 1}}}/\delta \left( \phi \right)} \right|\phi > \phi _{i}^{*}} \right] = \int_{{\phi _{i}^{*}}}^{\infty } {{{\phi }^{{\sigma - 1}}}\cdot \delta {{{\left( \phi \right)}}^{{ - 1}}}g\left( \phi \right)} d\phi /\left[ {1 - G\left( {\phi _{i}^{*}} \right)} \right] \) and use \( \phi_{xi}^{*}={{\left( {{{{{w_i}}} \left/ {{{w_j}}} \right.}} \right)}^{{\sigma /\left( {\sigma -1} \right)}}}{t_i}\phi_j^{*} \) to derive Eq. (2). The limits of j(ϕ *) are \( \mathop{\lim}\limits_{{\phi^{*}\to \infty }}j\left( {\phi^{*}} \right)=0 \) and \( \mathop{\lim}\limits_{{{\phi^{*}}\to 1}}j\left( {{\phi^{*}}} \right)=E\left[ {\left( {{\phi^{{\sigma -1}}}-1} \right)\cdot \delta {{{\left( \phi \right)}}^{-1 }}} \right]>0 \), the slope is \( {{{dj\left( {{\phi^{*}}} \right)}} \left/ {{d{\phi^{*}}}} \right.}=-\left( {\sigma -1} \right){{{\phi {\prime^{{\sigma -1}}}\left[ {1-G\left( {{\phi^{*}}} \right)} \right]}} \left/ {{{\phi^{{*\sigma }}}}} \right.} < 0 \).

1.4 Appendix D: Comparative Statics of the Equilibrium

We apply Cramer’s rule to Eq. (2). By Leibniz’ rule we get \( {{{\partial H}} \left/ {{\partial \phi_H^{*}}} \right.} < 0 \), \( {{{\partial H}} \left/ {{\partial \phi_F^{*}}} \right.} < 0 \), \( {{{\partial F}} \left/ {{\partial \phi_H^{*}}} \right.} < 0 \), and \( {{{\partial F}} \left/ {{\partial \phi_F^{*}}} \right.} < 0 \). The determinant of the matrix of derivatives of Eq. (2) is positive, as \( \phi {\prime^{{\sigma -1}}}\left[ {1-G\left( {{\phi^{*}}} \right)} \right]=\int\nolimits_{{{\phi^{*}}}}^{\infty } {{\phi^{{\sigma -1}}}\cdot \delta {{{\left( \phi \right)}}^{-1 }}g\left( \phi \right)} d\phi \) decreases in ϕ * and \( \phi_{xi}^{*} > \phi_i^{*} \).

Unilateral trade integration. We get \( - {{{\partial H}} \left/ {{\partial {f_{xH }}}} \right.} > 0 \), \( - {{{\partial F}} \left/ {{\partial {f_{xF }}}} \right.} > 0 \), \( - {{{\partial F}} \left/ {{\partial {t_F}}} \right.} > 0 \), \( - {{{\partial H}} \left/ {{\partial {t_H}}} \right.} > 0 \), and \( {{{\partial H}} \left/ {{\partial {t_F}}} \right.}={{{\partial H}} \left/ {{\partial {f_{xF }}}} \right.}={{{\partial F}} \left/ {{\partial {t_H}}} \right.}={{{\partial F}} \left/ {{\partial {f_{xH }}}} \right.}=0 \). It follows that \( - {{{\partial \phi_i^{*}}} \left/ {{\partial {t_i}}} \right.} > 0 \), \( - {{{\partial \phi_i^{*}}} \left/ {{\partial {t_j}}} \right.} < 0 \), \( {{{\partial \phi_i^{*}}} \left/ {{\partial {f_{xi }}}} \right.} < 0 \) and \( {{{\partial \phi_i^{*}}} \left/ {{\partial {f_{xj }}}} \right.} > 0 \).

Symmetric trade integration. By total differentiation of \( \phi_H^{*}=\phi_H^{*}\left( {{t_H},{t_F}} \right) \) and setting \( d{t_H}=d{t_F}=dt \) we have \( {{{d\phi_H^{*}}} \left/ {dt } \right.}={{{\partial \phi_H^{*}}} \left/ {{\partial {t_H}}} \right.}+{{{\partial \phi_H^{*}}} \left/ {{\partial {t_F}}} \right.} \). It is easy to show that the productivity in H increases by symmetric trade integration, \( {{{d\phi_H^{*}}} \left/ {dt } \right.} > 0 \), whenever \( \frac{{{{f}_{F}}{{W}^{\sigma }}}}{{{{f}_{{xF}}}}}\frac{{\phi _{H}^{{*\sigma - 1}}}}{{\phi _{F}^{{*\sigma - 1}}}}{{\phi }^{\prime }}_{F}^{{\sigma - 1}}\left[ {1 - {{G}_{F}}\left( {\phi _{F}^{*}} \right)} \right] - \frac{{{{t}_{H}}}}{{t_{F}^{\sigma }}}\phi _{{xF}}^{{\prime \sigma - 1}}\left[ {1 - {{G}_{F}}\left( {\phi _{{xF}}^{*}} \right)} \right] > 0 \). This is the case whenever the countries have similar business conditions, which is reflected by similar cutoff productivities (i.e. \( \phi_H^{*}\approx \phi_F^{*} \)), or whenever H has a strong comparative advantage, i.e. \( \phi_H^{*} > >\phi_F^{*} \) (from app. C it then follows that \( \phi_{xF}^{*} > >\phi_F^{*} \); recall that \( {{{d\phi {\prime^{{\sigma -1}}}\left[ {1-G\left( {{\phi^{*}}} \right)} \right]}} \left/ {d} \right.}{\phi^{*}} < 0 \)). If H has a strong comparative disadvantage so that \( \phi_H^{*} < <\phi_F^{*} \), symmetric trade integration decreases H’s cutoff productivity, whereas the cutoff of F increases due to symmetry.

Changes in business conditions. We find \( \partial \phi_i^{*}/\partial {f_{ei }} < 0 \), \( {{{\partial \phi_i^{*}}} \left/ {{\partial {f_{ej }}}} \right.} > 0 \), \( {{{\partial \phi_H^{*}}} \left/ {{\partial W}} \right.} > 0 \) and \( {{{\partial \phi_F^{*}}} \left/ {{\partial W}} \right.} < 0 \) where \( W\equiv {{{{w_F}}} \left/ {{{w_H}}} \right.} \). Concerning fixed labor investments, we have \( {{{\partial \phi_H^{*}}} \left/ {{\partial {f_H}}} \right.} > 0 \) if \( {j_H}\left( {\phi_H^{*}} \right)\phi_F^{{\prime \sigma -1}}\left[ {1-{G_F}\left( {\phi_F^{*}} \right)} \right] > {{{{{{\left( {\phi_{xH}^{\prime}\phi_{xF}^{\prime }} \right)}}^{{\sigma -1}}}\left[ {1-{G_H}\left( {\phi_{xH}^{*}} \right)} \right]\left[ {1-{G_F}\left( {\phi_{xF}^{*}} \right)} \right]}} \left/ {{\left[ {\tau_{HF}^{{\sigma -1}}\tau_{FH}^{{\sigma -1}}\phi_H^{{*\sigma -1}}} \right]}} \right.} \). This is the case whenever trade costs are high (consider \( {\tau_{HF }}={\tau_{FH }}=\tau \to \infty \)). If trade costs are sufficiently small, then \( {{{\partial \phi_H^{*}}} \left/ {{\partial {f_H}}} \right.} < 0 \). Increases in f F increase the domestic cutoff unambiguously, \( {{{\partial \phi_H^{*}}} \left/ {{\partial {f_F}}} \right.} > 0 \).

Technological potential. We model differences in technological potential by hazard rate stochastic dominance (HRSD) as in Demidova (2008). A productivity distribution G a (ϕ) stochastically dominates a distribution G b (ϕ) in terms of the hazard rate order, \( {G_a}\left( \bullet \right){\succ_{hr }}{G_b}\left( \bullet \right) \), if \( {g_a}\left( \phi \right)/\left[ {1-{G_a}\left( \phi \right)} \right] < {g_b}\left( \phi \right)/\left[ {1-{G_b}\left( \phi \right)} \right] \) holds true for any given productivity level ϕ. The merits of HRSD is that it allows us to compare the expectations of an increasing function above a given cutoff level, i.e. if y(x) is an increasing function, then \( {E_H}\left[ {y(x)\left| {x>\phi } \right.} \right] > {E_F}\left[ {y(x)\left| {x>\phi } \right.} \right] \). To analyze the impact of a greater technological potential, rewrite \( {j_a}\left( {{\phi^{*}}} \right) \) as follows \( {j_a}\left( {{\phi^{*}}} \right)\equiv \int\nolimits_{{{\phi^{*}}}}^{\infty } {\left( {{\phi^{{\sigma -1}}}-1} \right)\cdot \delta \left( \phi \right){\;^{-1 }}\cdot {g_a}(\phi )} d\phi =\left[ {1-{G_a}\left( {{\phi^{*}}} \right)} \right]\cdot {E_a}\left[ {\left. {\left( {{\phi^{{\sigma -1}}}-1} \right)\cdot \delta \left( \phi \right){\;^{-1 }}} \right|\phi > {\phi^{*}}} \right] \). We get \( {j_a}\left( {{\phi^{*}}} \right)-{j_b}\left( {{\phi^{*}}} \right)=\left[ {1-{G_a}\left( {{\phi^{*}}} \right)} \right]\cdot {E_a}\left[ {\left. {\left( {{\phi^{{\sigma -1}}}-1} \right)\delta {{{\left( \phi \right)}}^{-1 }}} \right|\phi > {\phi^{*}}} \right]-\left[ {1-{G_b}\left( {{\phi^{*}}} \right)} \right]\cdot {E_b}\left[ {\left. {\left( {{\phi^{{\sigma -1}}}-1} \right)\delta {{{\left( \phi \right)}}^{-1 }}} \right|\phi > {\phi^{*}}} \right] \). If \( {G_a}\left( \bullet \right){\succ_{hr }}{G_b}\left( \bullet \right) \), then \( \left[ {1-{G_a}\left( {{\phi^{*}}} \right)} \right]>\left[ {1-{G_b}\left( {{\phi^{*}}} \right)} \right] \) for any given productivity level ϕ *. As \( e\equiv \left( {{\phi^{{\sigma -1}}}-1} \right)\cdot \delta \left( \phi \right){\;^{-1 }} > 0 \) and de/dϕ, we have \( {E_a}\left[ {\left. \bullet \right|\phi > {\phi^{*}}} \right] > {E_b}\left[ {\left. \bullet \right|\phi > {\phi^{*}}} \right] \) and \( {j_a}\left( {{\phi^{*}}} \right) > {j_b}\left( {{\phi^{*}}} \right) \).

Consequently, if the technological potential of country H increases in the sense of HRSD, the value of the equilibrium condition \( H\left( {\phi_H^{*},\phi_F^{*}} \right) \) increases in the short-run whereas the equilibrium condition \( F\left( {\phi_H^{*},\phi_F^{*}} \right) \) remains unchanged. Consequently, \( \phi_H^{*} \) increases and \( \phi_F^{*} \) decreases.

Existence and uniqueness of the equilibrium. In equilibrium, both conditions in Eq. (2) have to be fulfilled. Furthermore, it must hold true that \( \phi_i^{*} > 1 \). As the domestic cutoff decreases with domestic disadvantages and foreign advantages, we assume that the countries must not be too different in aggregate (as a disadvantage with respect to factor can be compensated by an advantage with respect to another) to generate positive and meaningful cutoff productivities.

Rights and permissions

About this article

Cite this article

Pflüger, M., Russek, S. Business Conditions and Exit Risks Across Countries. Open Econ Rev 24, 963–976 (2013). https://doi.org/10.1007/s11079-013-9277-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11079-013-9277-5