Abstract

The popularity and potential of FinTech for generating business value has been highlighted in an evolving number of studies. Nevertheless, there is still ambiguity on the success of such disruptive technologies. To address this gap, this paper draws on a case study of an IT vendor in Japan. We interview key stakeholders involved in the case project to (i) explore the success factors of FinTech applications adopted by non-financial organisations, (ii) illustrate the applicability of the multi-dimensional project success framework in FinTech projects, and (iii) highlight the importance of the FinTech Project Management field that warrants further investigation. We contribute to the IT Project Management field, where we extend the theoretical background with aspects of FinTech adoption and success. We also inform practice in terms of lessons for managers to improve the existing processes and assist their organisations in business transformational initiatives using FinTech.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Over the last years, Financial Technology (FinTech) has received considerable attention from both academics and practitioners due to their potential in digitally transforming networks of supply chains in almost every business sector (Chen et al. 2019; Fosso Wamba et al. 2018). Global funding of FinTech projects has been rising rapidly from $38.1 billion for all of 2017 to $57 billion in 2018 (KPMG 2018). FinTech builds upon Information Technology (IT) to offer financial products and services within the banking industry, with more advanced risk management, trade processing, cash management and data-analysis tools deployed by the financial institutions (Gomber et al. 2018; Zavolokina et al. 2017). Hence, the FinTech sector has applied disruptive technologies (e.g. Blockchain, Data Analytics, etc.) transforming existing business models and developing new products (e.g. cashless payments, robo-advisors etc.) in the financial services industry. More importantly, FinTech offers trust, confidence, and transparency for the systems and transactions in a field where these aspects are most required (Gozman et al. 2018; Leong 2018; Papazafeiropoulou and Spanaki 2016).

The literature on FinTech has mainly focused on its business value, with scholars scoping at the potential and benefits accruing from its adoption (Belanche et al. 2019; Mori 2016; Ryu 2018). For instance, Pollari (2016) has investigated the benefits of Fintech from a strategic perspective, underlining its importance for creating trust and suggesting that it can assist in lowering entry barriers for new entrants, creating new business models and new products, and streamlining processes. Hung and Luo (2016) studied the strategic planning of a Bank for investing in a Fintech company in Taiwan. In contrast, Arner et al. (2017) have looked into the Fintech benefits for the financial sector, including increased trust in the financial services industry, reduced time-to-market for innovative products, employment for financial professionals, and creation of financial start-ups. Leong (2018) have investigated the development and emergence of a Fintech firm from an information management perspective, looking at digital capabilities such as e-commerce and big data analysis. What is evident from the literature (Arner et al. 2017; Fosso Wamba et al. 2018; Pollari 2016) is that the key benefit of Fintech is on providing business value especially in digitally transforming businesses and eliminating transaction costs.

The popularity and potential of FinTech for generating business value has been highlighted (Belanche et al. 2019; Fosso Wamba et al. 2018; Leong 2018); however, there is still ambiguity on how to understand the success of technology adoption within the last century (Marikyan et al. 2020), and specifically FinTech adoption (Fosso Wamba et al. 2018). Investigating such a topic is essential as it will help organisations unlock the value that Fintech can add to their efficiency and performance and improve their current approaches of data-driven sustainable development and capabilities (Mikalef et al. 2018, 2020). Furthermore, as incorporating Fintech and digital technologies in organisations requires examining their adoption from a broader perspective, understanding and assessing the value of these technologies can be rather critical in various terms. The importance is highlighted when (i) designing and refining FinTech, ensuring that resources are in place for its development/adoption and that it is linked to strategic objectives and KPIs (Mikalef et al. 2019) and (ii) creating a Fintech ecosystem (Pappas et al. 2018; Tsujimoto et al. 2018). The FinTech ecosystem is comprised and supported by the organisational actors, their generation of data, and their interactions and communications that will lead to the creation of value, as well as to business and societal change (I. Lee and Shin 2018). Diemers et al. (2015) argue that FinTech creates an ecosystem that includes five elements, that is, the FinTech start-ups (providing the services), technology developers, government (legislation), financial customers, and the traditional financial institution. Consequently, due to the complexity of the stakeholders involved in this ecosystem, there is always a question if an assessment of FinTech value and success goes beyond the assessment of IT value, as new technologies can result in further risks (Jones et al. 2019).

Therefore, this research focuses on what constitutes the value of FinTech projects. It does so by assessing the success of FinTech projects based on IT project success principles (Matta and Ashkenas 2003; Shenhar et al. 2001). The research question of this study, is hence, how can organisations assess their Fintech initiatives and realise gains and business value from their efforts? Explicitly, we draw on a case study of a project by an IT vendor in Japan and interviews with Project Management professionals from a wide range of FinTech segments. We contribute to the field of FinTech and IT project management by (i) exploring multi-dimensional the success factors (Shenhar et al. 2001) of FinTech applications adopted by non-financial organisations, (ii) illustrating the applicability of the multi-dimensional project success framework (Shenhar et al. 2001) in FinTech projects and (iii) highlight the FinTech Project Management field as an area for future research studies. Our findings can provide important lessons for managers to improve the existing processes and assist the organisations in business transformational initiatives.

The paper is structured as follows. After a review of the literature on FinTech retrospectives and the success and failure factors within the IT Project Management space, the methodology of the study is followed by the presentation and discussion of the findings. In conclusion, the paper presents the lessons learnt from the retrospectives and proposes the topic area for research and improvement for the future.

2 Background

In this section, we briefly discuss the evolution of FinTech and then we transition to IT project management and in particular assessment of IT projects using the multi-dimensional project success framework (Shenhar et al. 2001) to explore further the retrospectives of success and failure. The background and previous research in FinTech and IT project success assessment assist in building the exploratory case study theoretically and extending the theoretical approaches within the scope of IT project management.

2.1 The Evolution of Financial Technology (FinTech)

“FinTech” is a compound term for Financial Technology, which denotes the organisations or the representatives of the organisations that combine financial services with innovative technologies (Fosso Wamba et al. 2018). There are multiple definitions for “FinTech” mostly as a technologically enabled financial innovation, which leads to new business models, applications, processes and products that could have a material effect on financial markets, institutions and the provision of financial services (Fosso Wamba et al. 2018; McNevin 2016; Schwabe 2016). Fintech in the study of Ryu (2018) appears as an emerging financial service or sector combined with financial and IT services or industries. Lee and Shin (2018) present FinTech as an innovative ecosystem comprised of various players, as it is also presented in the study of Diemers et al. (2015). The key stakeholders of the FinTech ecosystem could be fintech start-ups technology developers, government, financial customers and traditional financial institutions (I. Lee and Shin 2018). According to the same study (I. Lee and Shin 2018), the FinTech industry introduces various business models relevant to each product or service provided: payments, wealth management, crowdfunding, lending, capital market and insurance services. These organisations aim to attract clients through products and services that are more automated, user-friendly, efficient and transparent than those currently available through the traditional banking institutions (I. Lee and Shin 2018; Zavolokina et al. 2017). In addition to offering products and services within the banking industry, FinTech branches out towards distribution of insurance and other financial instruments as well as third-party services (Kavuri and Milne 2019).

The link between financial and IT services is not always self-evident (Ryu 2018), as the opportunities, risks and legal implications of Fintech are different from existing templates for finance or conventional IT approaches. Arner et al. (2017) mention the first differentiating factor that comes from the policy-making agenda and the industrial context and is not from the technology itself but from the actors applying the technology (so the policy-making context for FinTech is actor-driven in contrary to IT that is technology-driven). Secondly, IT has a significant role in FinTech as the facilitator of the FinTech product/services, enabling and providing them with distinguishing features (Ryu 2018). However, IT is not only a facilitator or an enabler for effectively delivering financial services but a true innovator or a disrupter for redesigning the existing value chain while bypassing the conventional financial operation patterns(Arner et al. 2017; Gomber et al. 2018; Ryu 2018). That is also the reason why this study will explore the FinTech project success through an IT project management lens to understand FinTech success where IT is the critical factor in non-financial companies. The IT project success framework (Shenhar et al. 2001) could provide a multi-dimensional understanding required for this study in terms of the actors, IT and overall project objectives for FinTech project success in non-financial companies.

Since FinTech involves the introduction of IT to meet the financial needs and demands of users, the question of whether FinTech related issues are different from issues related to IT comes to the foreground (Belanche et al., 2019; Leong, 2018). For instance, issues related to FinTech adoption have been studied in the IS literature including payment (Foster and Heeks 2013), crowdfunding (e.g., Burtch et al. 2013), and lending (e.g., Burtch et al. 2014). Recent work has looked into the dynamics between banks and telecoms when it comes to providing mobile payments (De Reuver et al. 2015), and the importance of FinTech from a strategic perspective arguing about its assistance in lowering barriers for new entrants, creating new business models and products, as well as streamlining and improving processes and operations (Hung and Luo 2016; Pollari 2016). Arner et al. (2017) argued that FinTech could bring numerous benefits for the financial sector, including trust in the financial services, reduced time-to-market for new products and services and the creation of start-ups. In contrast, Leong (2018) looked at benefits from an information management perspective (digital capabilities such as e-commerce and big data analysis) during the development of a FinTech company in China that offers microloans to college students (Leong 2018).

Still, there is limited, if any, literature that discusses the assessment of FinTech value (Chen et al. 2019; Fosso Wamba et al. 2018). Such research is important as it assists organisations that would like (i) to unlock the value of FinTech, improving their current approaches of data-driven sustainable development; (ii) to design, refine, and adopt these technologies (Mikalef et al. 2018) ensuring that appropriate resources are in place for their strategic development and that FinTech is linked to their strategic objectives and KPIs (Mikalef et al. 2019); and (iii) to create a FinTech ecosystem (Pappas et al. 2018; Tsujimoto et al. 2018) that is comprised and supported by the organisational stakeholders, their data, and their interactions and communications. Such an ecosystem is essential as it will enable organisations to create business and societal value.

2.2 Project Success Framework

Literature has long acknowledged project value (success) as a multi-dimensional construct (e.g. Engelbrecht et al. 2017; Gingnell et al. 2014). In the IT literature, measuring systems success is a dominant area of interest in multiple studies (Dwivedi et al. 2014; Zhou et al. 2018), and the focus is mostly on the “IT” technical aspects and not always on the IT project management and its success (e.g. DeLone and McLean 1992; 2003; Petter et al., 2012; Seddon, 1997; Tan & Pan, 2002). For instance, following the Project Management Institute guidelines, project success is conceptualised in terms of whether the project adhered to budget, schedule, and specifications (Gingnell et al. 2014; Standish Group 2015) or whether the realisation of benefits takes place. Other literature perceives project success as comprised of two parts, namely “project management success” referring to the short-term view of project success (the accomplishment of cost, time, and quality objectives), and “project success” (budget, schedule, specifications, objectives, satisfaction stakeholder/user needs) (Gingnell et al. 2014; Standish Group 2015).

Literature has discussed the application of the IT/IS Success Models on IT projects to assist the emerging IT/IS requirements (Petter et al. 2012). These models have mostly synthesised the latest various IT Success perspectives and measures, measuring success based on the needs of the organisations and stakeholders. These models were developed mostly around the context of Enterprise Systems (Baskerville et al. 2000; Davenport 1998, 2000; Davenport et al. 2004; S. M. Lee and Lee 2012; Scott and Vessey 2000; Tan and Pan 2002) and serve as success frameworks in the broader area of Technology Management. Still, assessment of IT project success can be challenging as costs, risks and benefits can be underestimated (Bhattacharya et al. 2012; Bhattacharya and Seddon 2011; Dalcher 2012, 2015; Engelbrecht et al. 2017; Marchewka 2009). More attention needs to be devoted to how organisations assess IT project success and revise their business strategy around the new technology (Choudrie and Dwivedi 2005; Dwivedi et al. 2013).

In our study, we assess FinTech project success following the Multi-dimensional Project Success Framework (Shenhar et al. 2001) that focuses on assessing IT project success. The rationale behind the use of this framework is twofold: (a) FinTech projects are part of an organisation’s strategic initiative as they are executed with short- and long- term objectives in times of technological uncertainty, and (b) FinTech Project Success is measured taking into consideration the various interests and perspectives of the key stakeholders involved. Therefore, the Multi-dimensional Project Success Framework focuses on both the time-dependency of technological projects and the multiple interests of the stakeholders. It discusses project success in terms of the following dimensions (Shenhar et al. 2001):

-

Success Dimension 1 – Project Efficiency (Meeting Constraints): Project efficiency is a short-term dimension that expresses the efficiency in which the resource constraints were met and how the project was managed. While the dimension could be assessed immediately, it is difficult to judge long-term project success and the organisational benefits. However, due to the shorter product cycles and the increased competition, time-to-market has become a vital component in gaining competitive advantage. The dimension, thus, assists organisational business performances through the enhancement of project efficiency, and act as an enabler for early product introduction leading towards product competitiveness.

-

Success Dimension 2 – Impact on the customer: This dimension links the customer and addresses the criticality of meeting the customer requirements. Meeting functional and technical specifications as well as the performance measures comprises within this dimension. Meeting performance affects the customers, who assess the product’s feasibility towards their business needs. Therefore, the framework considers meeting performance objectives to be one of the central elements. From the development team’s perspective, the dimension also includes the level of customer satisfaction and the willingness of the customer to work in collaboration for future generations of the project or separate projects.

-

Success Dimension 3 – Business and Direct Success: This dimension addresses the impact, both immediate and direct, the project may have on the customer organisation. It includes the measures of the new process performing time, cycle time, yield, and quality, all of which measures the impact on the performance of the organisation.

-

Success Dimension 4 – Preparing for the Future: This dimension directs the challenge of preparing the organisational and technological infrastructure for future use. It is a long-term dimension that addresses the questions regarding the organisational preparation needed to exploit future opportunities such as other markets, ideas, innovations and products.

All these dimensions are essential during different intervals with respect to the completion of the project. The first dimension is relevant during the project execution phase, where the attributes such as meeting resource constraints and measuring deviations from plans could be measured. However, upon the completion of the project, the relevance of this dimension tends to diminish over time. Following that, the second dimension, that is, the impact on them and customer satisfaction are essential. The impact of the third dimension, the business and direct success, can only be experienced much later. The relative importance of the fourth dimension can only be measured a few years following the completion of the project when the long-term benefits could be realised.

2.3 The Japanese FinTech Context

Our case study lies within the Japanese context. Japan is experiencing rapid growth within its FinTech industry (Nakaso 2016). The investment towards the FinTech industry in Japan rose to 65 million USD in 2015, which amounts to nearly 20% growth from 2014 (Accenture 2016). Although the industry is proliferating, the number of FinTech organisations within Japan is limited (Suzuki and Ochiai 2017), out of which a large percentage is currently delivering new financial products and services through the incorporation of up-and-coming technologies such as AI, Blockchain and Cloud-Computing (Suzuki and Ochiai 2017). At the same time, the rapid proliferation of smartphones in the country since 2010 has led to the emergence of FinTech firms offering application-based services for Personal Financial Management such as Moneytree, Money Forward and Zaim (Khare et al. 2019).

In the recent years, FinTech application providers have begun to integrate their services with traditional financial institutions with the most prominent example being the collaboration between Money Forward and the SBI Sumishin Net Bank alongside Tokai Tokyo Securities (Khare et al. 2019). Behind the momentum, the government has recognised the importance of FinTech towards the country’s economic growth and has stated the need to set new research and development themes to facilitate the creation of new business areas (Nakaso 2016). Furthermore, with the relaxation of the regulatory framework and the availability of new fund-raising methodologies for the start-ups, the domestic market is expected to experience growth in the years ahead (Khare et al. 2019). Given the rapid growth, popularity, and challenges related to FinTech projects in Japan, there is a need to understand better the success of such projects (Winkler et al. 2008) and how adoption success could be achieved as an overall objective, especially in the non-financial organisation, providing the impetus for researching within the Japanese context.

3 Methodology

The research follows the exploratory case study approach (Yin 2009), as the focus is on realising the dynamics present within single settings (Eisenhardt 1989). The case of FinTech Project Management cannot be separated from the organisational context (Orlikowski and Baroudi 1991), thereby allowing concepts to emerge from the data (Miles and Huberman 1994)while answering questions as to how and why are posed (Yin 2009). The interest of this research study is to provide insights into the FinTech Project Management areas of interest from ABC’s case study evidence (ABC is a pseudonym). The specific case was selected based on shorter-term forethought and intention parameters (Pettigrew 1990). The network and familiarity of the researchers with the involved organisations and the Japanese context in the chosen project made the selection of the specific case an informed choice (with a higher likelihood of being granted access) based on resource and opportunity considerations (Pan and Tan 2011, p. 165). The chosen project was a representative example of FinTech initiative in Japan, but not a unique one (Siggelkow 2007), providing ground so as the findings can be generalisable (Pan and Tan 2011).

3.1 Research Design

A qualitative approach was followed where Project/Programme Managers were interviewed. The research design followed four stages: the first stage involved getting an in-depth understanding of the products and services offered in the FinTech industry, the outlook of the Japanese FinTech market, commercially deployed IT Project Management frameworks and the success factors of successful IT project execution (review of previous studies of FinTech and IS Project Success). In the second stage, the case study at ABC Company was discussed through interviews with various stakeholders of a failed project initiative, that is, DM (first round of interviews –exploratory interviews). Through these interviews, the study aimed to identify critical success factors for the execution of FinTech projects and establish the areas of concern for senior management. The third stage involved benchmarking of the processes, tools, techniques, frameworks and technologies utilised to execute IT projects in the Japanese FinTech industry (second round of interviews –confirmatory interviews). Information gathered through the initial three stages was coded through using thematic analysis.

3.2 Case Background: The ABC Company

The data collection follows a failed project initiative DM of “ABC” (a pseudonym) chosen to serve as the unit of analysis, the base for the overall objective of the case study. ABC is a software firm, located in Japan, which specialises in providing a range of software development, system integration services and IS/IT supporting services. ABC, founded in the early 90ies, has been a very successful IT service provider over the last decades and continues to do so by providing high-quality advance IS/IT solutions to the customers.

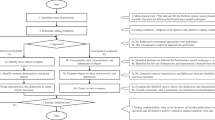

Recently, ABC, as an IT supplier undertook a project entitled “DM” (Fig. 1) to develop a portion of a cashless payment solution in collaboration with the IT services provider NTT DATA. The collaboration between the ABC and the NTT DATA seemed promising as in Japanese context; such collaborative pattern is often in order to deliver the faster and more reliable project (but also to maintain “good relationships” and “trust” within the sector). However, the project failed to deliver the objectives set by the customer (the customer was a non-financial organisation acquiring to adopt cashless payments), thus, tarnishing the relationship between the two organisations. The aftermath of the situation prompted the senior management of the ABC to adopt a new business model where the organisation would transition from being an IT vendor/supplier (B2B) to an off-the-shelf solutions provider (B2C) thus initiating an internal business transformation within the firm. A critical part of this transformational process was to evaluate the current Project Management methodologies, tools and techniques utilised by the team leading the project and to make necessary improvisations to ensure that the failure of the project DM would not be repeated.

The DM Project

3.3 Data Collection and Analysis

Our sampling strategy was based on informed decisions of the researchers and the type of the study (Suri 2011). Identifying information-rich cases can be achieved through purposeful sampling, as it provides access to key stakeholders of the phenomenon under research (Suri and Clarke 2009). An intensity sampling approach for data collection is employed to avoid sample bias from the case study (Benbasat et al. 1987; Siggelkow 2007). The study herein followed Patton’s principles (2002) about sample bias through a selection of cases that are excellent or rich examples of the phenomenon of interest, but not highly unusual cases. Cases that manifest sufficient intensity to illuminate the nature of success or failure, but not at the extreme (Patton 2002).

A hybrid combination sampling technique was applied, consisting of expert views and maximum variation of these views. Expert sampling is a form of purposeful sampling, which is used to glean knowledge from individuals who have a particular set of expertise (Patton 2002; Suri 2011). This approach is mainly dependent on the judgment of the researcher during the selection of the units that are to be studied (Suri 2011). Unlike the techniques used under the probability sampling, the objective of purposeful sampling is to develop a sample with the intention of generalising from the respective sample to the population of interest (A. S. Lee and Liebenau 2013). In return, the expertise being investigated could form the basis of the research while highlighting new areas of interest during the exploratory phase of the qualitative research (Patton 2002; Suri 2011).

Following the tenets of purposeful sampling, eight participants were interviewed in two rounds (exploratory and confirmatory), all of whom have IT Project Management expertise. The common denominator of the participants is the experience each of these individuals possessed in the execution of IT projects within the FinTech space in Japan and worldwide. The study included the individuals who have participated in the DM project and had managed such projects for over three decades as well as ones who have recently embarked on the journey of IT Project Management. The purpose here was to identify perspectives the individuals have on each of the dimensions of the Multidimensional Project Success Framework and their criticality towards project success within the Japanese FinTech market (Table 1).

The interviews were divided into two sections for each of the rounds (exploratory/confirmatory) (Table 5 in the Appendix). The first part intended to establish the experiences each of the participants had within IT Project Management environments (Exploratory, round 1). Additionally, the section provided an insight to the amount, and the types of projects each of these individuals were managing; the project management methodologies they have commonly employed; how they perceived IT project success as an individual as well as an organisation; and level of involvement they have had on the IT projects managed. The second half of the questions (confirmatory, round 2) intended to analyse the responses of the interviewees and relate that to each of the four dimensions presented in the Multidimensional Project Success Framework. All the interviewees were asked to provide feedback on the criticality of each dimension to identify the effectiveness of the framework. We note here that the questions included in Table 5 (Appendix) structured the protocol for each of the foci (Project Experience/Multi-dimensional framework). This means that for each one of the questions, follow-up questions were asked, including asking the interviewees for examples to justify their answers.

The case followed the thematic analysis approach (Boyatzis 1998; Braun and Clarke 2006) for identifying codes and themes in the dataset. The coding stage of the study included the steps of Braun and Clarke (2006)namely: a) Familiarisation with the data, b) Generating initial codes, c) Searching for themes, d) Reviewing themes, e) Defining and naming themes, f) Producing the report. We used the dimensions of Project Success Framework (Shenhar et al. 2001) as themes (Table 2). These themes were continuously refined as the researchers went back and forth to the data, building thus the subthemes and the analysis (see Table 6 in Appendix).

4 Analysis and Discussion of the Findings

The study focused on the research question on a) how organisations can assess their Fintech initiatives and b) how they can realise gains and business value from their efforts. Therefore, there are two stages for the interviews; the first is focusing on the assessment of the FinTech initiatives (exploratory stage of the assessment ways) and the second on the business value of them (explaining further the value gained from such initiatives and the assessment efforts through the confirmatory stage).

The following section presents the findings of the interviews through analysis and the associated quotes. The discussions presented herein stem from the discussions of the first and second round of the interviews with the participants/stakeholders. The first stage was exploratory, and the second a follow-up confirmatory stage, where the participants had the chance to revise and enhance the discussion with more insight. The interview rounds (first and second) were not distinguished for presentation purposes but also because it is the profile of the participant that provides credibility to the quotes and ideas expressed (purposeful sampling technique).

4.1 Exploratory Analysis (Round 1)

4.1.1 Project Efficiency

As per the responses gathered, the data could be divided into two categories. First, the interviewees who were working on the customer-side (Participant 5, Participant 6 and Participant 7) all agreed that the “operational constraints”, although they act as a baseline for project completion, are not the most important factor when it comes to measuring the overall project success.

"In general, the overall success of the project is determined whether there is a roll-out in the end. As quality is the most important factor in financial systems, exceeding the schedule/budget constraints can be acceptable. If the schedule is un-movable, exceeding the budget is the only way because quality cannot be compromised". (Participant 7)

This was further verified through the response of Participant 6, who discussed additional factors:

"Budget and schedule is always a limitation, and naturally, the project has to be delivered with the allocated budget and time. However, in HSBC exceeding the budget would not be considered as a failure (not drastic budget deviations). If project/programme management foresees such case as "a showstopper" we always have the flexibility to avoid project failures by adopting other methods like adjusting the scope of the project / adopt phase approach for the product delivery".

On the contrary, Participant 8 added that

"This varies as per the contractual obligations the organisation has with the clients. More often than not, it is encouraged to complete the project within the set operational constraints based on the time, cost and quality. In exceptional situations, the client would agree to relax some of the set constraints or compromise on one or more of the said aspects but, internally, it is not encouraged to do so".

Participant’s 8 view was further echoed by the ABC correspondents, all of whom emphasised the importance of meeting the operational constraints set aside at the start of the project. It could be understood through the data collected that the Project Managers who managed FinTech Projects for Supplier organisations perceived project success as the ability to produce project deliverables within the constraints set by the customers to manage the profit margins for their respective projects. Whereas their counterparts correlated the impact, each project had on the business strategy to the overall project success.

4.1.2 Impact on the Customer

There was a mutual agreement between the interviewees on the importance of customer satisfaction to a Project Manager.

Participant 6 stated that the business streams fund most of the technology implementation projects; hence, “customer satisfaction would often come from the internal business departments (e.g. Retail Banking, Corporate Business etc.). Customer satisfaction is one indicator in the project success”.

He further mentions that, in order to facilitate this, design documentation such as functional and technical specifications as well as business requirement documents are shared with the business stakeholders and processed only upon the sign-off from the business. He believes that this ensures “the business has an early understanding of the product, which leads to the confidence of the system as well as the satisfaction of the functionalities”. This could further be verified by the response of Participant 7, who added that “the customer is the Project Sponsor, who usually is from the business department. Customer Satisfaction is paramount as the Project Sponsor is the one who provides the funding for the projects”.

It was discovered that the supplier-based Project Managers felt more strongly about fulfilling the criteria set within this dimension and strongly emphasised the importance of customer satisfaction for future business opportunities. Participant 1 felt that a “Project Manager located onsite at a customer organisation effectively acts as an Account Manager between the two organisations and, thus, played a crucial role in the overall revenue generation”.

Participant 8 added further into this statement saying that “the organisation I work for are currently on the PSL (Preferred Suppliers List) of our customer organisations. Usually, at the end of each year, there is a review of this list, and poor performers are let off. Therefore, the satisfaction of our clients indirectly equates to the financial health of our organisation and any benefits we might receive as employees”. Participant’s 7 view on that was quite indifferent on this subject as he mentioned that “in financial institutions, the customers are the business departments. Therefore, the success/failure of the individual project does not affect future business opportunities”. He made a division on the perspectives between the Project Managers from the customer organisations to those of Supplier organisations.

4.1.3 Business and Direct Success

The study identified that, depending on the nature of the IT projects, the measures to assess the business and direct success would be different. These measures can be summarised as follows:

-

Efficiency Enhancement Projects: Tasks and are completed faster, and the measures would be based on the time saved.

-

Cost Saving Projects: Projects that are initiated to reduce the cost of running the business. For example, the electronic archive of documents will eliminate paper and printer costs, and the measure would be the dollar amount saved.

-

Labour Saving Projects: The projects that are initiated to automate the day-to-day processes in the business. For example, Robotic Process Automation (RPA) can eliminate manual work, and the measure would be the labour cost saved.

-

Profit-Driven Projects: New products and services are developed through the project to create a new, enhanced and existing stream of revenue generation for the firm. For example, for a new financial product roll-out, and the measure would be the profits generated.

-

Feature Enhancement Projects: Usually, these projects increment feature enrichment, and the benefits would be intangible. The success measure would be based on the number of fixes and enhancement made.

Participant 7 further added that “the benefits would be felt immediately after the roll-out, but the full benefits will usually take some time to be completely realised”, whereas, he admitted that in some cases, it would be difficult to estimate when the benefits would be fully realised.

In addition to the above categorisation, two sub-categories were identified shedding more light into the process of the measurement of the business and the direct impact:

-

Run-the-Business Projects: Projects under this category mainly involved in enhancing the existing IT systems and the technology within the organisation. This includes upgrading software versions and software functionality and evergreening of technology. For such changes, the common areas that would measure the business impact would be the manual process elimination; the overall cost savings; improvement of performances and the capacity of the systems (in order to handle larger volumes of data). Impact of such projects can be seen immediately or within a shorter period.

-

Change-the-Business Projects: These Projects make changes to the way the business operates and serve the customers. This often includes new technological implementation and new system implementation for internal as well as external customers. The impact would be measured on the time the organisation takes to penetrate the target market segments; offer new services to customers, and reduce the cost for this procedure. In such projects, the impact could be felt mid-to-long term, which could vary from 6 months to 2 years.

On the contrary, Participant 1 stated that the “primary attributes utilised internally to measure the success of the project were the ability to deliver the chunks of works at a time agreed prior to the initiation of the project and also the ability to meet the functional and non-functional requirements as agreed”. Participant 1 further reinstated that any additional costs that occurred during the project life will need to be borne by the supplier (ABC) and, hence, the importance is placed upon the operational constraints. Participant 2 and Participant 3 did not comment on this matter as they felt that they had little insight into the internal measures taken by the customer organisations.

4.1.4 Preparing for the Future

From the responses gathered, this dimension emerged as the one where the least amount of attention was paid. Participant 2, Participant 3, and Participant 4, all agreed that due to the nature of their responsibilities, they are doubtful to be involved nor to have an insight to the long-term business strategy of their respective customers. Participant 6 felt that most of the projects he manages are in place to improvise the current business processes and the overall efficiency of the business. He further stated that “some implementations are a mixture, hence, could not clearly be defined as strategic (e.g. exploiting new markets) or enabling for future (e.g. innovation)”. Participant 5, who is exercising the responsibilities of Chief Information Officer, stated that aligning the IT strategy alongside the organisational strategy and harnessing new technical innovations through the Research and Development Centre lies within his current responsibilities. He furthered this statement saying, “ it is a continuous process in which the department seeks to improvise on how it could benefit the business through the cutting-edge technology”.

4.2 Confirmatory Analysis (Round 2)

The case study findings are discussed through the dimensions of Project Success Framework (Shenhar et al. 2001) as themes to understand the factors behind DM’s failure. Moreover, the findings are analysed to provide lessons on how causalities such as the DM Project could be avoided.

Table 6 (Appendix) summarises each of the subject areas categorised as themes which were discussed during the interviews and the emerging sub-themes that arose upon the completion of the thematic analysis. These sub-themes are further elaborated in the next section to draw conclusions from the data collected. The coding scheme is divided into two Perspectives, as these were highlighted as important in the initial phase of the interviews and discussions: (a) the customer’s perspective and (b) the supplier’s perspective. The categorisation of the sub-themes is divided in theory-driven themes (from the Multi-dimensional Success Framework), assisting the analysis.

4.2.1 Project Efficiency

Before making any conclusion on the success/failure of a project, the multiple stakeholders should agree upon the assessment criteria. In our study, the participants believed that, while operational constraints form an essential criterion in measuring the project success, it is not sufficient to form the baseline from which the success could be measured. A common attribute found within this group of participants was that all of them had spent most of their career managing projects that are internal to their respective organisations. Project success can mean the same thing for all the parties involved is a common misconception within the Project Management world (Savolainen et al. 2012). The objective of the customer is to minimise the cost of the project delivery, whereas the aim of the suppler is to maximise the profit (Savolainen et al. 2015). Our findings coincide with the literature of IT Project Management stating the combination of criteria including meeting time, functionality, cost and quality as most common for the measurement of project success (Anda et al. 2009). However, in 2010, de Bakker et al. (2010) questioned these criteria arguing that using the aforementioned operational constraints could easily lead towards the misconception that an IT project has failed or vice-versa (de Bakker et al. 2010). The rationale provided here is that the defined initially requirements are bound to change as the project proceeds and, hence, almost an impossible task to provide an adequate estimation at the inception of the project (de Bakker et al. 2010). The operational estimates are often made prior to understanding the problem domain, and they are often flawed as they are made at the wrong time by the wrong people, leading to the conclusion that there is little to be concerned if a project does not meet the cost or schedule targets (Yang et al. 2011).

4.2.2 Impact on the Customer

All interviewees highlighted the importance of the impact on the customer and the overall customer satisfaction to be critical in determining project success. However, the rationale behind the importance of this success factor differed quite significantly between the Project Managers from the customer’s end to that of the supplier’s. Table 3 displays the benefits each party stands to gain by fulfilling the demands presented within this dimension.

However, the differences in customer perspectives are not studied in most of the literature on IT project success. In their study, Ahonen and Savolainen (2010) analysed a group of terminated IT project cases. In one of the cases, the supplier finished the project on time. However, once the system was implemented, the customer was not satisfied with the system yet paid the invoice in full nevertheless (Ahonen and Savolainen 2010; Savolainen et al. 2015). This project from the customer’s perspective was a failure, whereas, from the supplier’s perspective, the situation was not as transparent. The supplier did manage to deliver the project on time, within the budget, and as per the scope agreed with the customer and received the payment in full, yet the project failed to fulfil the business needs within the customer organisation (Savolainen et al. 2015).

British Standard for Project Management BS6079 (British Standard 2000) defined Project Management as the continuous planning; monitoring and control of a project; and the motivation of all those who are involved in it to achieve the objectives on time and to the specified cost, quality and performance. As per the Project Success Framework (Shenhar et al. 2001), three of the four success criteria are based on the post-implementation of the project and relies heavily on customer satisfaction.

Customer satisfaction in Project Management can be referred to as the degree to which the project meets or exceeds the expectations of the customer (Pinto and Mantel 1990). This includes the quality of the project deliverables, overall stakeholder experience, and the communication between internal and external stakeholders throughout the project lifecycle (Pinto 2013; Pinto and Slevin 1987). While these success criteria are critical for the overall success of the project, it is found to be compromised the most. As per Gartner’s 2018 IT Key Metrics Data report, 26% of the internal project participants felt that they have not adequately met the customer expectations, rating their perception of customer satisfaction as “expectations not met” or “somewhat disappointing” (Hall et al. 2017).

From the rationale mentioned above, one constant that is perhaps more transparent than the rest is the effort taken by these individuals to ensure the business relationships they have with their respective stakeholders are protected, and the trust that is bestowed upon them has adhered. Trust is the most important element of any business transaction in Japan. It is crucial to have a trustworthy and harmonic relationship between business partners (Pinto et al. 2009; Smyth et al. 2010).

One of the Key Performance Indicators within the FinTech Project Management industry in Japan is the number of post-implementation issues and problems addressed by the Production Support team. The measures mentioned above are in place to minimise such instances, but the handover documentation allows the maintenance teams to support the customers if an issue arises. However, The Impact on the customer is a dimension in which there is no uniformity in the time required to measure its success. Though usually it would be felt short-term, it varies based on the purpose and the type of the project, which channels towards the third dimension (“Business and Direct Success”).

4.2.3 Business and Direct Success

The time taken to experience business and direct success caused by a project depends on the nature of the project undertaken. From the responses received, five categories were identified and are summarised in Table 4. The data presented in Table 4 diminish the ability to assess the success or the failure of a project following the implementation or the closedown process as there would not be sufficient time for the customer organisation to realise if the project did deliver the benefits as expected (Shenhar et al. 2001). Therefore, it is important to understand the difference between “project management success” and “project product success’.

Table 4 is developed based on theoretical and empirical research conducted by multiple researchers. Table 4 distilled a broad range of IT success measures into an integrated view of IS/IT success, as displayed above (DeLone and McLean 2003). While these two aspects are outside the scope of this project, it is safe to assume that Table 4 presents a strong argument that the efficiency of the Project Management processes would not guarantee that the resulting product or services developed would have the intended impact on the customer organisation. Therefore, it could be considered as a critical success factor to have a well laid out Benefit Review plan following the conclusion of the project to measure the overall success of the project and to involve the supplier parties in such assessments.

4.2.4 Preparing for the Future - Customer-Supplier Dynamics

This dimension addresses the problems surrounding the organisational and technological infrastructure for the future (Shenhar et al. 2001), and it was the most challenging to gather sufficient information for. The fact that supplier parties were not being involved in defining the business future of their customers is one of the key challenges faced while assessing the dimension. This was further highlighted during the analysis of the case study where it was revealed that the supplier’s side Project Manager had very little insight to the long-term benefits NTT DATA stood to gain from the DM project. This begs the questions that if and to what extent the supplier should be involved in refining the business strategy of a customer given the challenge that the benefits of this dimension could only be realised in the longer-term.

5 Implications

We contribute to the field of FinTech and IT project management by (i) exploring multi-dimensional the success factors (Shenhar et al. 2001) of FinTech applications adopted by non-financial organisations, (ii) illustrating the applicability of the multi-dimensional project success framework (Shenhar et al. 2001) in FinTech projects, and (iii) highlight the FinTech Project Management field as a rich area for future investigation. Our study discusses the different stakeholder perceptions of project success and failure and illustrates two contrasting perspectives Customer: failure vs supplier: not transparent) of success, instead of focusing only on the customer satisfaction side (Pinto and Mantel, 1990). We highlight the importance of the impact on the customer and the overall customer satisfaction in determining project success and underline the differences in customer perspectives with regard to impact and satisfaction. Furthermore, we offer a classification of projects and measures to assess their business and direct success, distinguishing between “project management success” and “project product success” and subsequently relating these to short/medium/long term impact. Therefore, we contribute to IT project management by looking at how organisations assimilate the project/system, support, execute or even revise their business strategy around the new technology in place (Choudrie and Dwivedi 2005; Dwivedi et al. 2013).

We illustrate the applicability of the Project Success Framework to assess the value (success) of FinTech projects based on IT project management (Matta and Ashkenas 2003; Shenhar et al. 2001). We argue that organisations can use this framework to assess their FinTech initiatives to check whether they have realised or will realise gains and business value from their adoption efforts (Mikalef et al. 2018). Nevertheless, this needs to look beyond the sole use of operational indicators as it could lead to incomplete and misleading assessments (Fosso Wamba et al. 2018; McNevin 2016; Schwabe 2016; Zavolokina et al. 2017). Therefore, the multiple stakeholders of such projects need to cooperate, collaborate, and create a synergy of necessary capabilities linked to strategic objectives and KPIs (Mikalef et al. 2019). This synergy will lead to project success, and the creation of a FinTech ecosystem (Diemers et al. 2015; Pappas et al. 2018; Tsujimoto et al. 2018) comprised and supported by the organisational actors, their generation of data, and their interactions and communications. This ecosystem would go beyond the mere use of IT, and therefore create value, as well as business and societal change.

From a practitioner perspective, as many companies have started already their FinTech journey, there is still lack of knowledge and skills with regard to, for instance, how rapidly can financial systems change for FinTech and how efficient this change can be, how participants in projects could better cooperate so as to minimise risks and maximise benefits and impact for the customer, how the project requirements can be monitored and regulatory requirements can be enforced and how success can be measured (Fosso Wamba et al. 2018). This study offers then, by applying the Project Success Framework (Shenhar et al. 2001)lessons and/or guidelines per each of these dimensions to project and business managers who would like to engage in FinTech projects or assess the trajectory and current state of their FinTech projects.

6 Conclusion and Way Forward

This research was based on the paucity of the literature to assess the meaning and success of FinTech technologies. The multi-dimensional project success framework (Shenhar et al. 2001) provided a lens to assess the success of FinTech projects based on IT project management in the Japanese context. We illustrated the applicability of this framework in FinTech projects and discussed whether the assessment of such projects’ success is different from IT projects.

One of the limitations of the paper is the relatively small size that was used for the case study and interviews. Furthermore, our study is based on a single case in a particular context and therefore, the results cannot be generalised. However, the aim of the study is not statistical generalizability (Guba and Lincoln 1994; Lincoln and Guba 1990).On the contrary, we generalise from empirical statements to theoretical statements (A. S. Lee and Baskerville 2003), that is, what Yin (2009) suggests as generalising from case study findings to theory. We, therefore, inform theory as we provide an alternative view of a phenomenon and our results need to be judged depending on the plausibility of the reasoning used when analysing the findings and drawing conclusions from our data.

Further research could elaborate on the findings in multiple case studies, in a variety of FinTech Projects within Japan and other countries worldwide to verify and expand the findings of this study. Future research could focus on the impact of cultural aspects within the Project Management profession in the Japanese FinTech industry, or the use of Japanese inspired methods for agile development, such as Kanban (Cao et al. 2009; Polk 2011) or alternative approaches of systems development (Conboy 2009; Dennehy and Conboy 2017, 2018; Nunamaker et al. 1990). The various perceptions of Success of FinTech projects should be further investigated in different levels (Project/Programme Managers) due to the presence of the customer-supplier dynamics and views on success, creating a conflict of interest

References

Accenture. (2016). Fintech and the evolving landscape: Landing points for the industry. Accenture.

Ahonen, J. J., & Savolainen, P. (2010). Software engineering projects may fail before they are started: Post-mortem analysis of five cancelled projects. Journal of Systems and Software., 83, 2175–2187. https://doi.org/10.1016/j.jss.2010.06.023.

Anda, B., Hansen, K., & Sand, G. (2009). An investigation of use case quality in a large safety-critical software development project. Information and Software Technology., 51, 1699–1711. https://doi.org/10.1016/j.infsof.2009.04.005.

Arner, D. W., Barberis, J., & Buckley, R. P. (2017). FinTech, regTech, and the reconceptualisation of financial regulation. Northwestern Journal of International Law and Business.

Baskerville, R., Pawlowski, S., & McLean, E. (2000). Enterprise resource planning and organisational knowledge: Patterns of convergence and divergence. In Proceedings of the twenty first international conference on Information systems (pp. 396–406). Association for Information Systems.

Belanche, D., Casaló, L. V., & Flavián, C. (2019). Artificial intelligence in FinTech: Understanding robo-advisors adoption among customers. Industrial Management and Data Systems., 119, 1411–1430. https://doi.org/10.1108/IMDS-08-2018-0368.

Benbasat, I., Goldstein, D. K., & Mead, M. (1987). The case research strategy in studies of information systems. MIS Quarterly, 11(3), 369–386.

Bhattacharya, P. J., & Seddon, P. B. (2011). Going beyond operations with Enterprise systems. ACIS 2011 Proceedings.

Bhattacharya, P. J., Seddon, P. B., & Scheepers, R. (2012). Enterprise systems for innovation in products and processes: Beyond operational efficiency. In ACIS 2012: Location, location, location: Proceedings of the 23rd Australasian Conference on Information Systems 2012 (pp. 1–11). ACIS.

Boyatzis, R. E. (1998). Transforming qualitative information: Thematic analysis and code development. Thousand Oaks: Sage Publications, Inc..

Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2), 77–101.

British Standard. (2000). Project management Ð Part 3 : Guide to the management of business related project risk Association of Project Managers. Bsi.

Burtch, G., Ghose, A., & Wattal, S. (2013). An empirical examination of the antecedents and consequences of contribution patterns in crowd-funded markets. Information Systems Research, 24(3), 499–519.

Burtch, G., Ghose, A., & Wattal, S. (2014). Cultural differences and geography as determinants of online prosocial lending. Mis Quarterly, 38(3), 773–794.

Cao, L., Mohan, K., Xu, P., & Ramesh, B. (2009). A framework for adapting agile development methodologies. European Journal of Information Systems., 18, 332–343. https://doi.org/10.1057/ejis.2009.26.

Chen, M. A., Wu, Q., & Yang, B. (2019). How valuable is FinTech innovation? Review of Financial Studies., 32, 2062–2106. https://doi.org/10.1093/rfs/hhy130.

Choudrie, J., & Dwivedi, Y. K. (2005). Investigating the research approaches for examining technology adoption issues. Journal of Research Practice, 1(1), 1.

Conboy, K. (2009). Agility from first principles: Reconstructing the concept of agility in information systems development. Information Systems Research., 20, 329–354. https://doi.org/10.1287/isre.1090.0236.

Dalcher, D. (2012). The nature of project management: A reflection on the anatomy of major projects by Morris and Hough. International Journal of Managing Projects in Business., 5, 643–660. https://doi.org/10.1108/17538371211268960.

Dalcher, D. (2015). Going beyond the Waterfall: Managing Scope Effectively Across the Project Life Cycle. Project Management Journal. https://doi.org/10.1002/pmj.21475.

Davenport, T. H. (1998). Putting the enterprise into the enterprise system. Harvard Bus.Rev., 76(4), 121–131 http://dl.acm.org/citation.cfm?id=280994.280995.

Davenport, T. H. (2000). Mission critical : Realising the promise of enterprise systems. Boston: Harvard Business School Press.

Davenport, T. H., Harris, J. G., & Cantrell, S. (2004). Enterprise systems and ongoing process change. Business Process Management Journal, 10(1), 16–26. https://doi.org/10.1108/14637150410518301.

de Bakker, K., Boonstra, A., & Wortmann, H. (2010). Does risk management contribute to IT project success? A meta-analysis of empirical evidence. International Journal of Project Management, 28, 493–503. https://doi.org/10.1016/j.ijproman.2009.07.002.

DeLone, W. H., & McLean, E. R. (2003). The DeLone and McLean model of information systems success: A ten-year update. In Journal of Management Information Systems (Vol. 19, pp. 9–30). https://doi.org/10.1080/07421222.2003.11045748.

DeLone, W. H., & McLean, E. R. (1992). Information systems success: The quest for the dependent variable. Information Systems Research, 3(1), 60–95.

Dennehy, D., & Conboy, K. (2017). Going with the flow: An activity theory analysis of flow techniques in software development. Journal of Systems and Software., 133, 160–173. https://doi.org/10.1016/j.jss.2016.10.003.

Dennehy, D., & Conboy, K. (2018). Identifying challenges and a research agenda for flow in software Project Management. Project Management Journal., 49, 103–118. https://doi.org/10.1177/8756972818800559.

De Reuver, M., Verschuur, E., Nikayin, F., Cerpa, N., & Bouwman, H. (2015). Collective action for mobile payment platforms: A case study on collaboration issues between banks and telecom operators. Electronic Commerce Research and Applications, 14(5), 331–344.

Diemers, D., Lamaa, A., Salamat, J., & Steffens, T. (2015). Developing a FinTech ecosystem in the GCC: let's get ready for take off. Strategy&. https://www.strategyand.pwc.com/m1/en/reports/2015/developing-fintech-ecosystem-gcc.html. Accessed 28 June 2020.

Dwivedi, Y. K., Ramdani, B., Williams, M. D., Mitra, A., Sukumar, R., & Williams, J. (2013). Factors contributing to successful ERP implementation in locally–owned and multinational firms in India. International Journal of Indian Culture and Business Management, 6(4), 458–476.

Dwivedi, Y. K., Wastell, D., Laumer, S., Henriksen, H. Z., Myers, M. D., Bunker, D., Elbanna, A., Ravishankar, M. N., & Srivastava, S. C. (2014). Research on information systems failures and successes: Status update and future directions. Information Systems Frontiers., 17, 143–157. https://doi.org/10.1007/s10796-014-9500-y.

Eisenhardt, K. M. (1989). Building theories from case study research. The Academy of Management Review., 14, 532. https://doi.org/10.2307/258557.

Engelbrecht, A., Gerlach, J. P., Benlian, A., & Buxmann, P. (2017). Analysing employees' willingness to disclose information in enterprise social networks: The role of organisational culture. In Proceedings of the 25th European Conference on Information Systems, ECIS 2017.

Fosso Wamba, S., Kala Kamdjoug, J. R., Bawack, R., & G. Keogh, J. (2018). Bitcoin, Blockchain, and FinTech: A systematic review and case studies in the supply chain. Production Planning and Control.

Foster, C., & Heeks, R. (2013). Innovation and scaling of ICT for the bottom-of-the-pyramid. Journal of Information Technology, 28(4), 296–315.

Gingnell, L., Franke, U., Lagerström, R., Ericsson, E., & Lilliesköld, J. (2014). Quantifying success factors for IT projects-an expert-based Bayesian model. Information Systems Management., 31, 21–36. https://doi.org/10.1080/10580530.2014.854033.

Gomber, P., Kauffman, R. J., Parker, C., & Weber, B. W. (2018). On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. Journal of Management Information Systems. https://doi.org/10.1080/07421222.2018.1440766.

Gozman, D., Liebenau, J., & Mangan, J. (2018). The innovation mechanisms of Fintech Start-Ups: Insights from SWIFT's Innotribe Competition. Journal of Management Information Systems. https://doi.org/10.1080/07421222.2018.1440768.

Guba, E. G., & Lincoln, Y. S. (1994). Competing paradigms in qualitative research. In Handbook of qualitative research.

Hall, L., Stegman, E., Futela, S., & Gupta, D. (2017). IT key metrics data 2018: Key industry measures: Banking and financial services analysis: Current year. Gartner Research Report.

Hung, J. L., & Luo, B. (2016). FinTech in Taiwan: A case study of a Bank's strategic planning for an investment in a FinTech company. Financial Innovation., 2. https://doi.org/10.1186/s40854-016-0037-6.

Jones, S., Irani, Z., Sivarajah, U., & Love, P. E. D. (2019). Risks and rewards of cloud computing in the UK public sector: A reflection on three Organisational case studies. Information Systems Frontiers., 21, 359–382. https://doi.org/10.1007/s10796-017-9756-0.

Khare, A., Ishikura, H., & Baber, W. W. (Eds.). (2019). Transforming japanese business: rising to the digital challenge. Springer Nature.

Kavuri, A. S., & Milne, A. K. L. (2019). Fintech and the future of financial services: What are the research gaps? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3333515.

KPMG. (2018). The pulse of Fintech 2018. Kpmg.

Lee, A. S., & Baskerville, R. L. (2003). Generalising generalizability in information systems research. Information Systems Research., 14, 221–243. https://doi.org/10.1287/isre.14.3.221.16560.

Lee, A. S., & Liebenau, J. (2013). Information systems and qualitative research. In Information Systems and Qualitative Research. https://doi.org/10.1007/978-0-387-35309-8_1.

Lee, I., & Shin, Y. J. (2018). Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons., 61, 35–46. https://doi.org/10.1016/j.bushor.2017.09.003.

Lee, S. M., & Lee, S.-H. (2012). Success factors of open-source enterprise information systems development. Industrial Management and Data Systems, 112(7), 1065–1084. https://doi.org/10.1108/02635571211255023.

Leong, K. (2018). FinTech (financial technology): What is it and how to use technologies to create business value in Fintech way? International Journal of Innovation, Management and Technology. https://doi.org/10.18178/ijimt.2018.9.2.791.

Lincoln, Y. S., & Guba, E. G. (1990). Judging the quality of case study reports. Internation Journal of Qualitative Studies in Education, 3(1), 53–59.

Marchewka, J. (2009). Information technology project management. In Information technology project management.

Marikyan, D., Papagiannidis, S., & Alamanos, E. (2020). Cognitive dissonance in technology Adoption: A Study of Smart Home Users. Information Systems Frontiers. https://doi.org/10.1007/s10796-020-10042-3.

Matta, N. F., & Ashkenas, R. N. (2003). Why good projects fail anyway. Harvard Business Review.

McNevin, A. (2016). What is "Fintech." Computer Business Review.

Mikalef, P., Boura, M., Lekakos, G., & Krogstie, J. (2019). Configurations of big data analytics for firm performance: An fsQCA approach. In 25th Americas Conference on Information Systems, AMCIS 2019.

Mikalef, P., Pappas, I. O., Krogstie, J., & Giannakos, M. (2018). Big data analytics capabilities: A systematic literature review and research agenda. Information Systems and e-Business Management., 16, 547–578. https://doi.org/10.1007/s10257-017-0362-y.

Mikalef, P., Pappas, I. O., Krogstie, J., & Pavlou, P. A. (2020). Big data and business analytics: A research agenda for realising business value. Information and Management., 57, 103237. https://doi.org/10.1016/j.im.2019.103237.

Miles, M. B., & Huberman, A. M. (1994). Qualitative data analysis: an expanded sourcebook (2nd ed.). Thousand Oaks ; London: Sage.

Mori, T. (2016). Financial technology: Blockchain and securities settlement. Journal of Securities Operations & Custody Taketoshi Mori Journal of Securities Operations & Custody., 71, 308–314. https://doi.org/10.1016/j.pec.2007.11.025.

Nakaso, H. (2016). FinTech – Its impacts on finance , Economies and Central Banking. Bank of Japan.

Nunamaker, J. F., Chen, M., & Purdin, T. D. M. (1990). Systems development in information systems research. Journal of Management Information Systems., 7, 89–106. https://doi.org/10.1080/07421222.1990.11517898.

Orlikowski, W. J., & Baroudi, J. J. (1991). Studying information technology in organisations: Research approaches and assumptions. Information Systems Research, 2, 1–28.

Pan, S. L., & Tan, B. (2011). Demystifying case research: A structured-pragmatic-situational (SPS) approach to conducting case studies. Information and Organization., 21, 161–176. https://doi.org/10.1016/j.infoandorg.2011.07.001.

Papazafeiropoulou, A., & Spanaki, K. (2016). Understanding governance, risk and compliance information systems (GRC IS): The experts view. Information Systems Frontiers, 18(6), 1251–1263. https://doi.org/10.1007/s10796-015-9572-3.

Pappas, I. O., Mikalef, P., Giannakos, M. N., Krogstie, J., & Lekakos, G. (2018). Big data and business analytics ecosystems: Paving the way towards digital transformation and sustainable societies. Information Systems and e-Business Management., 16, 479–491. https://doi.org/10.1007/s10257-018-0377-z.

Patton, M. Q. (2002). Designing qualitative studies. Qualitative research and evaluation methods, 3, 230–246.

Petter, S., DeLone, W., & McLean, E. R. (2012). The past, present, and future of “IS success”. Journal of the Association for Information Systems, 13(5), 341–362.

Pettigrew, A. M. (1990). Longitudinal field research on Change: Theory and Practice. Organization Science. https://doi.org/10.1287/orsc.1.3.267.

Pinto, J. K. (2013). Lies, damned lies, and project plans: Recurring human errors that can ruin the project planning process. Business Horizons., 56, 643–653. https://doi.org/10.1016/j.bushor.2013.05.006.

Pinto, J. K., & Mantel, S. J. (1990). The causes of project failure. IEEE Transactions on Engineering Management., 37, 269–276. https://doi.org/10.1109/17.62322.

Pinto, J. K., & Slevin, D. P. (1987). Critical factors in successful project implementation. IEEE Transactions on Engineering Management., EM-34, 22–27. https://doi.org/10.1109/TEM.1987.6498856.

Pinto, J. K., Slevin, D. P., & English, B. (2009). Trust in projects: An empirical assessment of owner/contractor relationships. International Journal of Project Management., 27, 638–648. https://doi.org/10.1016/j.ijproman.2008.09.010.

Polk, R. (2011). Agile & Kanban in coordination. In Proceedings - 2011 Agile Conference, Agile 2011. https://doi.org/10.1109/AGILE.2011.10.

Pollari, I. (2016). The rise of Fintech opportunities and challenges. JASSA.

Ryu, H.-S. (2018). Understanding benefit and risk framework of Fintech adoption: Comparison of early adopters and late adopters. In Proceedings of the 51st Hawaii International Conference on System Sciences. https://doi.org/10.24251/hicss.2018.486.

Savolainen, P., Ahonen, J. J., & Richardson, I. (2012). Software development project success and failure from the supplier's perspective: A systematic literature review. International Journal of Project Management., 30, 458–469. https://doi.org/10.1016/j.ijproman.2011.07.002.

Savolainen, P., Ahonen, J. J., & Richardson, I. (2015). When did your project start? - the software supplier's perspective. Journal of Systems and Software., 104, 32–40. https://doi.org/10.1016/j.jss.2015.02.041.

Schwabe, G. (2016). FinTech – What' s in a name ? International Conference on Information Systems.

Scott, J. E., & Vessey, I. (2000). Implementing Enterprise resource planning Systems: The Role of Learning from Failure. Information Systems Frontiers, 2, 213–232. https://doi.org/10.1023/A:1026504325010.

Seddon, P. B. (1997). A respecification and extension of the DeLone and McLean model of IS success. Information Systems Research, 8(3), 240–253. https://doi.org/10.1287/isre.8.3.240.

Shenhar, A. J., Dvir, D., Levy, O., & Maltz, A. C. (2001). Project success: A multi-dimensional strategic concept. Long Range Planning., 34, 699–725. https://doi.org/10.1016/S0024-6301(01)00097-8.

Siggelkow, N. (2007). Persuasion with case studies. Academy of Management Journal, 50(1), 20–24.

Smyth, H., Gustafsson, M., & Ganskau, E. (2010). The value of trust in project business. International Journal of Project Management., 28, 117–129. https://doi.org/10.1016/j.ijproman.2009.11.007.

Standish Group. (2015). CHAOS report 2015. The Standish Group International, Inc.

Suri, H. (2011). Purposeful sampling in qualitative research synthesis. Qualitative Research Journal, 11(2), 63–75.

Suri, H., & Clarke, D. (2009). Advancements in research synthesis methods: From a methodologically inclusive perspective. Review of Educational Research, 79(1), 395–430.

Suzuki, Y., & Ochiai, T. (2017). Japan's fintech strategy a work in progress. International Financial Law Review.

Tan, C.-W., & Pan, S. (2002). ERP success: The search for a comprehensive framework.

Tsujimoto, M., Kajikawa, Y., Tomita, J., & Matsumoto, Y. (2018). A review of the ecosystem concept — Towards coherent ecosystem design. Technological Forecasting and Social Change, 136, 49–58. https://doi.org/10.1016/j.techfore.2017.06.032.

Winkler, J. K., Dibbern, J., & Heinzl, A. (2008). The impact of cultural differences in offshore outsourcing-case study results from German-Indian application development projects. Information Systems Frontiers., 10, 243–258. https://doi.org/10.1007/s10796-008-9068-5.

Yang, L. R., Huang, C. F., & Wu, K. S. (2011). The association among project manager's leadership style, teamwork and project success. International Journal of Project Management., 29, 258–267. https://doi.org/10.1016/j.ijproman.2010.03.006.

Yin, R. K. (2009). Case study research: Design and methods (4th ed., Vol. 5). London: Sage.

Zavolokina, L., Dolata, M., & Schwabe, G. (2017). FinTech transformation: How IT-enabled innovations shape the financial sector. In Lecture Notes in Business Information Processing. https://doi.org/10.1007/978-3-319-52764-2_6.

Zhou, M. J., Lu, B., Fan, W. P., & Wang, G. A. (2018). Project description and crowdfunding success: An exploratory study. Information Systems Frontiers., 20, 259–274. https://doi.org/10.1007/s10796-016-9723-1.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix 1

Appendix 1

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Jinasena, D.N., Spanaki, K., Papadopoulos, T. et al. Success and Failure Retrospectives of FinTech Projects: A Case Study Approach. Inf Syst Front 25, 259–274 (2023). https://doi.org/10.1007/s10796-020-10079-4

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10796-020-10079-4