Abstract

In this paper we analyse the evolution of the current account as a percentage of GDP for a group of Central and Eastern European Countries. Instead of analysing only the variable for unit roots, we go a step further and test for different speeds of mean reversion dependent on break dates endogenously determined. We apply the Bai and Perron method to find that most countries have managed to balance their current account, but some of them should keep an eye on the low speed of mean reversion and the deviation of the time trend from balance.

Similar content being viewed by others

Notes

See Cuestas and Gil-Alana (2016) for other detrending methods.

In the “Appendix” we also show the results of estimating threshold equations. However, the results are not directly comparable with the time-break equation estimations.

References

Bai J, Perron P (1998) Estimating and testing linear models with multiple structural changes. Econometrica 66(1):47

Bai J, Perron P (2003a) Computation and analysis of multiple structural change models. J Appl Econom 18(1):1–22

Bai J, Perron P (2003b) Critical values for multiple structural change tests. Econom J 6(1):72–78

Balassa B (1964) The purchasing-power parity doctrine: a reappraisal. J Polit Econ 72(6):584–596

Bhargava A (1986) On the theory of testing for unit roots in observed time series. Rev Econ Stud 53(3):369–384

Bohn H (2007) Are stationarity and cointegration restrictions really necessary for the intertemporal budget constraint? J Monet Econ 54(7):1837–1847

Christopoulos D, León-Ledesma MA (2010) Current account sustainability in the US: what did we really know about it? J Int Money Finance 29(3):442–459

Cuestas JC (2013) The current account sustainability of european transition economies. J Common Mark Stud 51(2):232–245

Cuestas JC, Gil-Alana LA (2011) Unemployment hysteresis, structural changes, non-linearities and fractional integration in European Transition Economies, University of Sheffield. Sheffield Economics Research Papers 2011005

Cuestas JC, Gil-Alana LA (2016) Testing for long memory in the presence of non-linear deterministic trends with Chebyshev polynomials. Stud Nonlinear Dyn Econom 20(1):57–74

Cuestas JC, Ordóñez J (2018) Fiscal consolidation in Europe: has it worked? Appl Econ Lett 25(16):1179–1182

Cuestas JC, Staehr K (2013) Fiscal shocks and budget balance persistence in the EU countries from Central and Eastern Europe. Appl Econ 45(22):3211–3219

Cuestas JC, Gil-Alana LA, Staehr K (2014) Government debt dynamics and the global financial crisis: has anything changed in the EA12? Econ Lett 124(1):64–66

Cuestas JC, Ordóñez J, Staehr K (2019) Unit labour costs and the dynamics of output and unemployment in the Southern European crisis countries. Empirica 46(3):597–616

Cunado J, Gil-Alana LA, de Gracia FP (2010) European current account sustainability: new evidence based on unit roots and fractional integration. East Econ J 36(2):177–187

De Grauwe P (2012) The governance of a fragile Eurozone. Aust Econ Rev 45(3):255–268

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74(366a):427–431

Elliott G, Rothenberg TJ, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64(4):813–836

Gros D (2012) On the stability of public debt in a monetary union. J Common Mark Stud 50(s2):36–48

Harkmann K, Staehr K (2018) Current account dynamics and exchange rate regimes in Central and Eastern Europe. Eesti Pank, Working Paper Series. https://www.eestipank.ee/sites/eestipank.ee/files/publication/en/WorkingPapers/2018/wp08_2018.pdf. 31 July 2019

Holmes MJ (2004) Current account deficits in the transition economies. Prague Econ Pap 13(4):347–358

Holmes MJ, Panagiotidis T (2009) Cointegration and asymmetric adjustment: some new evidence concerning the behavior of the U.S. current account. B E J Macroecon. https://doi.org/10.2202/1935-1690.1665

Ng S, Perron P (2001) LAG length selection and the construction of unit root tests with good size and power. Econometrica 69(6):1519–1554

Perron P (1989) The great crash, the oil price shock, and the unit root hypothesis. Econometrica 57(6):1361–1401

Perron P, Vogelsang TJ (1992a) Nonstationarity and level shifts with an application to purchasing power parity. J Bus Econ Stat 10(3):301–320

Perron P, Vogelsang TJ (1992b) Testing for a unit root in a time series with a changing mean: corrections and extensions. J Bus Econ Stat 10(4):467–470

Phillips PCB (1987) Time series regression with a unit root. Econometrica 55(2):277–301

Phillips Peter C B, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75(2):335–346

Roubini N, Wachtel P (1998) Current account sustainability in transition economies. National Bureau of Economic Research. Working Paper. http://www.nber.org/papers/w6468. 31 July 2019

Samuelson PA (1964) Theoretical notes on trade problems. Rev Econ Stat 46(2):145–154

Taylor AM (2002) A century of current account dynamics. J Int Money Finance 21(6):725–748

Trehan B, Walsh CE (1991) Testing intertemporal budget constraints: theory and applications to U. S. federal budget and current account deficits. J Money Credit Bank 23(2):206–223

Acknowledgements

The authors gratefully acknowledge comments from an anonymous referee and the editor on an earlier draft. The usual disclaimer applies. Juan Carlos Cuestas acknowledges the financial support from the MINEIC-AEI-FEDER ECO2017-85503-R and ECO2017-83255-C3-3-P projects, both of them from ‘Ministerio de Economía, Industria y Competitividad’ (MINEIC), ‘Agencia Estatal de Investigación’ (AEI) Spain and ‘Fondo Europeo de Desarrollo Regional’ (FEDER). Mercedes Monfort is grateful for support from the University Jaume I research project UJI-B2017-33. The views expressed are those of the authors and do not necessarily represent the official views of Eesti Pank or the Eurosystem.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

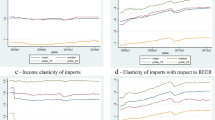

As requested by an anonymous referee we provide estimates of the threshold equations, using as potential threshold variables gross domestic product (y), its first difference, and one lag, and the real effective exchange rate (rer) based on consumer price indexes against the 27 main trade partners, with its first differences and one lag. The estimated equation is similar to Eq. (2), but in this case, t is replaced by the threshold variable Th. The model choses the best threshold variable by using information criteria. The data for these two variables are also obtained from Eurostat. The results, displayed in Table 5, show that depending on the case, the threshold may depend on either of those variables. However, these results are not directly comparable with those of Table 4.

In general, though with a few exceptions, we find that the larger the y/rer or the change in them, the faster the mean reversion of the current account is to equilibrium.

Rights and permissions

About this article

Cite this article

Cuestas, J.C., Monfort, M. Current account sustainability in Central and Eastern Europe: structural change and crisis. Empirica 48, 141–153 (2021). https://doi.org/10.1007/s10663-020-09473-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10663-020-09473-7