Abstract

In the early 2000s, several countries in the euro area (EA), mostly in the South, experienced an increase in current account deficits, while Northern countries saw an increase in current account surpluses. During the euro crisis, the South transitioned from a current account deficit to a surplus, while the North's surplus widened, thereby increasing the EA's overall current account surplus. To analyze the causes of the current account adjustment in the EA during the 2010s and to identify economic policies that reduce external imbalances, we employ a New Keynesian DSGE model with three regions (the North of the EA, the South of the EA, and the rest of the world). Our analysis reveals that the EA's expansionary monetary policy, fiscal consolidation, and lackluster productivity performance explain a significant portion of the current account adjustment. Furthermore, we find that the fiscal revaluation and expansion of the North would have limited effects on external imbalances.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

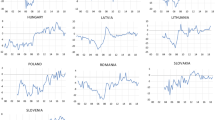

At the beginning of the 2000s, several countries in the euro area (EA)—primarily in the South, such as Greece, Ireland, Italy, Portugal, and Spain—experienced an increase in current account deficits, while Northern economies—Austria, Belgium, France, Finland, Germany, and the Netherlands—saw an increase in current account surpluses (as shown in Fig. 1).Footnote 1 Capital flowed from the North to the South, leading to overheating of the Southern economies. However, this trajectory was not sustainable as it caused a loss of price competitiveness. Ultimately, the global financial crisis (GFC) of 2008–2009 caused the bubble to burst.

Source: World Bank (2019)

Current account balance (% of GDP) of the North, the South and the euro area (selected countries).

During the euro crisis it was acknowledged that the “European Monetary Union is currently experiencing a serious internal balance of payments crisis” (Sinn 2012, 3). It was widely argued that “[t[he real problem with Europe is the huge divergence in costs between the core [the North] and the periphery [the South]“ (Pettis 2012). Pettis (2012) emphasizes that “[i]f the surplus nations ever hope to get repaid—i.e. to reverse those capital flows—then it must be obvious that the trade imbalances must also reverse “ and that “[f]or debt not to build up to unsustainable levels in the deficit countries, both deficits and surpluses must ultimately be reversed.“ Fig. 2 demonstrates that following the GFC, real exchange rates in the South have depreciated, indicating an improvement in price competitiveness, albeit at different rates and to varying degrees across countries. However, as shown in Fig. 1, current account imbalances have not reversed as expected. From 2011 to 2017, the South shifted from a current account deficit to a surplus, with a 6.2% GDP improvement, while the North's current account surplus expanded further by 1.4% relative to GDP.

Source: Eurostat (2019)

Real effective exchange rate (consumer price indices, 17 trading partners) in selected euro area countries.

The EA's current account balance shifted significantly from a roughly balanced position pre-2011 to a sizable surplus of almost 4% by 2017. This is indicative of the South's repayment of previously accumulated external debt through current account surpluses vis-à-vis the rest of the world (RoW). The interactions between the EA's North and South, as well as between the EA and the RoW, have been critical in shaping the current account developments of the region over the past two decades. In this paper, we focus on the period from 2011 to 2017 and employ a New Keynesian DSGE model with three regions (the South of the EA, the North of the EA, and the RoW) to shed light on these interactions. Our main contribution is to analyze the causes of the improvement of the North's and the South's current account balances after the start of the euro crisis. We also discuss policies that have been suggested to reduce the external imbalances within the EA but have not been implemented.

Our analysis indicates that a combination of monetary expansion, fiscal consolidation, and disappointing total factor productivity (TFP) growth contributed significantly to the current account adjustment in the EA during the 2010s. Initially, the European Central Bank (ECB) was hesitant to pursue an aggressive expansionary monetary policy following the GFC, unlike other major central banks. However, it later implemented a strongly expansionary policy in the latter part of the decade. In 2017, the ECB's monetary policy deviated by approximately 4 percentage points from the Taylor rule, relative to that of the US, indicating a relative loosening of the policy in the EA. To understand the impact of the ECB's monetary policy on the current account of the South and the North, we analyze the consequences of a 4 percentage point decrease in the annual EA interest rate. While the benefits of a monetary expansion on the current account are well established, our contribution lies in evaluating the specific effects of the ECB's policy on the two regions. Our research indicates that the ECB's expansionary monetary policy had a positive impact on the current account surplus of both the North and South of the EA. Specifically, it depreciated the euro and improved the current account surplus of the North and South by 0.7% and 1.2% of GDP, respectively. This finding is consistent with Lee and Chinn's (2006) empirical research, which indicates that expansionary monetary policy leads to short-term improvements in the current account through immediate depreciation of the real exchange rate, with effects gradually fading over time.

After the GFC, public debt burdens increased and the EA implemented fiscal consolidation. According to the IMF (2018), the structural fiscal balances in the South and the North improved by 4.1% and 2.7% of GDP, respectively, between 2011 and 2017. Using these estimates, we calibrated the sizes of fiscal shocks to analyze the current account effects of the EA's fiscal consolidation. Our findings suggest that it substantially improved the current account of the South by 1% relative to GDP, while the effect on the North's current account was small at 0.3% of GDP. This outcome can be explained by the South's stronger consolidation. In a study by Abbas et al. (2011), a 1% of GDP fiscal consolidation was found to improve the current account by an average of 0.3% of GDP, but the effect is weaker during large fiscal consolidations. Our results are consistent with this empirical estimate. However, our simulations also indicate that the fiscal consolidation of the 2010s had a negative effect on output in both regions. As such, our analysis underscores the importance of carefully considering the trade-offs between current account adjustments and the potential adverse impact on output when implementing fiscal consolidation policies.

In the 2010s, the growth of TFP in the EA has been slow compared to the rest of the world. The Conference Board (2019) data shows that between 2011 and 2017, TFP rose only 0.4% in the South, 2.4% in the North, and 4.2% in the RoW. Our analysis aims to quantify the current account effects of this observed TFP performance. We find that the negative TFP relative to the RoW in the EA contracted relative GDP, but also improved the current account of the EA. TFP shocks improved the South’s current account by 0.3% of GDP, while the effect on the North’s current account was negligible. Kollmann et al. (2016) studied the effects of TFP shocks in a three-region model and found that a positive TFP shock improves the trade balance of the region that experiences the shock. In contrast, our findings show that a positive TFP shock relative to other regions in the RoW deteriorates its current account and improves the current account of the region with the worst TFP performance. The key difference is that our TFP shock accumulates gradually, which is consistent with empirical evidence. Bussière et al. (2010) empirically found that a 1% increase in productivity deteriorates the current account balance by 0.11% of GDP. Our model suggests that the GDP-weighted fall in productivity relative to the world in the South is 3.6%. Therefore, the South’s fall in TFP should improve the current account by roughly 0.4% of GDP. Our finding of 0.3% of GDP is slightly smaller than the empirical estimate. The EA's new productivity challenge is to improve TFP in the South. However, our simulations suggest that this would increase output but worsen the current account.

According to our simulations, the combination of monetary, fiscal, and TFP shocks contributed to a current account improvement of 2.5% and 1% of GDP for the South and the North, respectively, between 2011 and 2017. These results align well with the observed improvements of 6.2% and 1.4% of GDP, respectively. While it is evident that other shocks affected the EA's economy during this time period, our analysis indicates that the shocks we examined can account for 40% and 69% of the observed current account adjustments in the South and the North, respectively. If the Armington elasticity, which measures the responsiveness of the demand for a particular good to changes in its price relative to the prices of other goods, is higher than our baseline value of 2, then the current account responses to shocks would be stronger. This would improve the model's ability to explain the observed current account adjustments.

The European project is a critical policy topic, and we are analyzing potential economic policies that could address external imbalances within the EA. There are different views on the cause of the imbalances, with one perspective attributing them to the South's lost competitiveness and the policies enacted to improve it. Alternatively, some argue that excessive price competitiveness in some Northern countries, through measures like wage moderation, contributed to the imbalances. The IMF (2014), for instance, suggests that Germany's real exchange rate was undervalued by 5–15%. While most analyses have focused exclusively on the South's need to restore its competitiveness, they have overlooked the significance of the North's need to appreciate its real exchange rate and reduce its current account surplus. Our focus is on two policies that the North could implement to address these imbalances: fiscal revaluation and expansion.

The absence of a nominal exchange rate as an adjustment instrument poses a challenge to correcting external imbalances in a monetary union. One potential solution is a fiscal devaluation, where employers' social contributions (SCR) are reduced and the Value Added Tax (VAT) is increased to boost domestic producers' competitiveness and exports. However, the effectiveness of fiscal devaluations is debated. While Farhi et al. (2014) find that a fiscal devaluation can mimic the effects of a nominal exchange rate devaluation, Engler et al. (2017) show that a fiscal devaluation in the South of 1% of GDP has only a small effect on the trade balance and real exchange rate.

In addition to fiscal devaluations, a fiscal revaluation in the North can also correct the divergence in price competitiveness between the North and the South. This involves increasing the SCR and reducing the VAT rate, which improves the South's international price competitiveness relative to the North. Our new analysis shows that a North's fiscal revaluation of 1% of GDP improves the South's current account balance by slightly less than 0.2% of GDP but deteriorates the North's current account by 0.2% of GDP. Our finding is consistent with previous studies that show a fiscal devaluation in the South has a small effect on the trade balance and the current account (Hohberger and Kraus 2016; Engler et al. 2017, 2018; Gomes et al. 2016). In fact, De Mooij and Keen (2013) found that reducing the VAT rate by 0.9 percentage points and increasing the SCR rate by 2 percentage points worsens net exports by 0.2% of GDP, which is consistent with our result of -0.2% of GDP. Overall, our results suggest that fiscal revaluations and devaluations may not be effective policy tools to reduce external imbalances, contrary to the claim of Farhi et al. (2014). Thus, the design of the EU fiscal policy should take into account the limitations of these policy tools.

In the early 2010s, a case could be made for fiscal expansion in the EA due to a negative output gap and low inflation. However, concerns about fiscal solvency prevented the South from implementing it, so a fiscal expansion had to come from the North, according to Blanchard et al. (2017). However, their analysis of the North's fiscal expansion using a DSGE model is inadequate for addressing external imbalances within the EA because the current account balance is always assumed to be zero. Romer (2012) argues that the North's fiscal expansion would shrink its current account surplus and have a positive effect on the South's economy. We find that it would increase output in both regions, but would worsen the North's current account balance due to the import component of public demand. Our contribution is to show that a fiscal expansion of 1% of GDP in the North would only improve the South's current balance by approximately 0.1% of GDP, while the North's current balance would deteriorate by roughly 0.2% of GDP. Although our results suggest that the North's fiscal expansion would reduce external imbalances in the EA, the benefits are relatively small. In a study by Abbas et al. (2011), a fiscal consolidation of 1% of GDP improved the current account by an average of 0.3% of GDP, but the effect was smaller in advanced economies. Our finding is consistent with this empirical evidence.

The paper is organized as follows: Section 2 introduces the model used in this study. Section 3 provides details of the model's parameterization. Section 4 examines the adjustment of the EA’s current account in the 2010s. Section 5 analyzes various economic policies that have been proposed to address external imbalances within the EA, but have not been implemented. Section 6 conducts sensitivity analysis to test the robustness of the results. Lastly, Section 7 draws policy conclusions based on the findings of the study.

2 Model

We use a DSGE model as in Engler et al. (2018) which is a 3-country extension of Engler et al. (2017). We extend the model by adding public consumption, TFP and monetary policy shocks. The size of the world economy is normalized to 1. Households are indexed by \(i\;\epsilon \left[\mathrm{0,1}\right]\). Two countries have formed a monetary union (MU) and a third country has a floating currency vis-à-vis the monetary union. We refer to the countries as the North (N), the South (S), and the rest of the world (RoW). Households \(i\;\epsilon \left[0,n\right]\) reside in the South, households with index \(i\;\epsilon \left[n,m-n\right]\) in the North and those indexed by \(i\;\epsilon \left[m,1\right]\) in the RoW.

2.1 Households

Engler et al. (2017) examined the influence of rule-of-thumb households on the trade balance effects of fiscal policy and determined that they have a negligible impact. While it is true that the introduction of rule-of-thumb households could have a more significant impact on the output effects of fiscal policy (see e.g. Tervala and Watson 2022), it would not significantly affect the main outcomes of this paper, which focus on external imbalances. Consequently, all economies in our model are characterized by a representative household with identical preferences. The utility function of the South’s representative household is

where \({\mathbb{E}}_{t}\) is the expectations operator, \(\beta\) is the discount factor, \({C}_{t}\) is a private consumption index, \({N}_{t}\) is the labor supply, and \(1/\phi\) is the Frisch elasticity of labor supply.

The South’s consumption index is

\({C}_{S,t}\), \({C}_{N,t}\) and \({C}_{RoW,t}\) denote the consumption by the South’s households of the South’s, the North’s and the RoW’s goods, \(\omega\) is the share of the South’s goods in the South’s consumption, \(\varpi -\omega\) is the share of the North’s goods, \(1-\varpi\) is the share of the RoW’s goods and \(\sigma\) is the elasticity of substitution between goods produced in different regions (the Armington elasticity). The consumption indexes of the North and the RoW are

The South’s consumption of domestically-produced goods is defined as a continuum of differentiated goods, indexed by \(i\;\epsilon \left[0,n\right]\) that are sold at the price \({P}_{S,t}(i)\)

where \(\epsilon >0\) is the elasticity of substitution between goods produced in the same countryThe North’s consumption of goods produced in the North and the RoW’s consumption of domestically-produced goods is defined as

The private demand function for the South’s, the North’s and the RoW’s goods by the South’s households are.

\({P}_{S,t}\left(i\right)\) is the price of the South’s good i while \({P}_{S,t}\) is the price index corresponding to the South’s consumption basket which can be interpreted as a producer-price index. The nominal exchange rate is denoted by \({E}_{t}\). It is expressed as the amount of the foreign currency needed to buy one euro. An increase in \({E}_{t}\) is an appreciation of the euro. The producer-price indexes are defined as

The overall consumer-price indexes are

The budget constraint of the South’s household is

where \({\tau }_{t}^{VAT}\) is the value added tax (VAT) rate, \({B}_{t}^{N}\) and \({B}_{t}^{RoW}\) denote holdings by the South household of the North’s and the RoW’s bonds at the beginning of the period t, \({R}_{t-1}^{MU}\) and \({R}_{t-1}^{RoW}\) are the gross return on bonds between t-1 and t in the monetary union and the RoW, \({W}_{t}\) is the nominal wage, \({\Pi }_{t}\) are the profits of the South’s firms and \({T}_{t}\) are lump-sum transfers. The return on the RoW’s bonds, denominated in the RoW’s currency, depends also on the nominal exchange rate \({E}_{t}\).

Our model exhibits stationarity, implying that over the long term, external debts revert to their initial level, even in the absence of a risk premium or adjustment costs on the net foreign asset position, despite the existence of incomplete markets at the international level. Notably, the Blanchard-Kahn conditions hold in our model, ensuring stationary behavior. The optimal consumption decision is given by the Euler equation:

2.2 Monetary and Fiscal Policy

The central bank of the EA, called the ECB, adjusts the interest rate in response to the deviations of euro-area pre-tax inflation from the zero inflation target. Similarly, the RoW’s central bank reacts to the inflation rate in the RoW. \({R}_{t}^{MU}\) and \({R}_{t}^{RoW}\) are set according to a Taylor-type rule with interest rate smoothing:

The average inflation rate in the monetary union is the GDP-weighted average of the inflation rates in the South and the North. The coefficient \({\alpha }_{\pi }\) is chosen by the central banks and \(\gamma\) measures interest rate smoothing. The deviations from the policy rule, \({\Delta }_{MU,t}\) and \({\Delta }_{RoW,t}\), follow an AR(1) process with zero mean:

with \({\rho }_{r}\in \lceil\left.\mathrm{0,1}\right)\) for \(r=MU, RoW\). In the later part of the study, it is demonstrated that the ECB's monetary policy deviated significantly from the Taylor rule. The AR(1) process is useful in capturing a persistent deviation from the central bank's reaction function.

We extend the model of Engler et al. (2018) by adding public consumption. The public consumption bundle consumed by the government is identical to the private consumption bundle. The government budget is financed through VAT and SCRs with the VAT rate \({\tau }_{t}^{VAT}\) charged on consumption expenditures and the SRC rate \({\tau }_{t}^{SCR}\) charged on wages paid by firms. The government’s budget constraint is

Government spending, \({G}_{t}\), and the VAT and SCR tax rates follow exogenous processes. They are subject to deviations from their respective steady state values, denoted by \({\overline{\tau }}^{VAT}\), \({\overline{\tau }}^{SCR}\) and \(\overline{G }\), as they are hit by unanticipated shocks, \({\varepsilon }_{G,t}\), \({\varepsilon }_{VAT,t}\), \({\varepsilon }_{SCR,t}.\) These shocks represent the government’s discretionary changes. The evolution of the fiscal variables is defined by the AR(1) process:

with \({\rho }_{x}\epsilon \left[\mathrm{0,1}\right]\) for \(x=G, VAT, SCR\).

2.3 Trade Balance and the Terms of Trade

Total demand for the South’s good i is the sum of the demand in the South, in the North, and the RoW:

\({Y}_{S,t}\) is the overall demand for the South’s good.

The trade balance (\({TB}_{t}\)) is the difference between output and private and public consumption, expressed in terms of consumption goods:

The terms of trade are defined as the ratio of producer-price indexes expressed in common currency

The terms of trade of the South express the relative price of the South’s goods in terms of foreign country’s goods.

2.4 Wage Setting

All households supply an imperfectly substitutable and differentiated labor service of type z, \({N}_{t}\left(z\right),\) to firms. Firm i employs \({N}_{t}(i,z)\) hours of differentiated labor services z and aggregates labor inputs to the labor index \({N}_{t}(i)\) used in the production of good i

Then firm i's demand for labor-type z is

where \({W}_{t}\left(z\right),\) and \({W}_{t}\) are the type specific and aggregate wage levels with

The aggregate demand for labor type \(z\), \({N}_{t}(z)\), is calculated by aggregating the firm-specific demand functions over all firms

Wage setting is delegated to labor-type specific labor unions. A fraction \(1-{\theta }_{w}\) of labor unions can reset their wages each period. Unions that readjust their wage \({W}_{t}(z)\) in t, aims to maximize the lifetime utility of households taking account of the probability of not being able to reset their wage in \(t+s\), their budget constraint and the aggregate demand for labor type \(z\). The first-order condition is

Labor unions set the wage \({W}_{t}^{*}\) so the future stream of marginal revenues from working is a constant mark-up \({\epsilon }_{w}/({\epsilon }_{w}-1)\) over the expected sum of the labor supply’s marginal cost.

In period \(t\), the aggregate wage index is a mixture of the prevailing wage in period \(t-1\) from the fraction \({\theta }_{w}\) of labor unions that can’t readjust in period t and the optimal wage set in period \(t\) by a fraction \(\left(1-{\theta }_{w}\right)\) of labor unions:

The production function of firm i determines the amount of labor index \(N(i)\) needed in the production of one unit of output, \(Y(i)\):

where \({A}_{t}\) is an index of TFP and subject to unexpected TFP shocks, \({\varepsilon }_{A,t}\). We assume that innovations induce a gradual and lasting change in TFP:

On the path to a new steady-state, only a fraction \(\left(1-\delta \right)\) of the innovation in TFP will be passed on to the next period. The hat notation denotes percentage changes from the initial steady state.

The aggregate level of employment, \({N}_{t}\), is an aggregation of firm-specific demand functions over all firms and labor types:

Wage and dispersion, \({s}_{t}^{p}\) and \({s}_{t}^{w}\), cause an efficiency cost in production.

2.5 Firms and Price Setting

Firms minimize costs for a given level of production and take into account the payroll tax \({\tau }_{t}^{SCR}\). The real marginal cost, \({{MC}_{t}}^{r}\), in terms of the domestically produced goods is

where \({sw}_{t}\) is inefficient wage dispersion. The real profits of firm i’s are

The choice between producer currency pricing (PCP) and local currency pricing (LCP) by firms engaged in international trade can be a critical determinant of the transmission of economic shocks across countries in open-economy DSGE models. The empirical evidence on this topic has been inconclusive thus far. We assume that all firms set prices in the currency of the producer for all markets, which implies full exchange rate pass-through. Incomplete exchange rate pass-through may characterize the euro-area economy, especially in terms of import prices (Ortega and Osbat 2020). The PCP assumption could affect trade balance and relative price dynamics in the short term. Nevertheless, our subsequent explanation clarifies that the combination of assuming PCP and setting a low Armington elasticity results in a realistic response of the trade balance to changes in the international price ratio in our model. Prices are set in a staggered fashion. Firms can reset their prices in a given period with probability \(1-{\theta }_{p}\). A firm that is able to set its optimal price \({P}_{S,t}^{*}\) in period \(t\) maximizes the expected value of its real profits. It takes into account the probability \({\theta }_{p}\) of not being able to reset prices in period \(t+s\), its real marginal cost, the demand for its good, and the stochastic discount factor \({\mathrm{Q}}_{t,t+s}= {\beta }^{s}{\mathbb{E}}_{t}\left[\frac{\left(1+{\tau }_{t}^{VAT}\right)}{\left(1+{\tau }_{t+s}^{VAT}\right)}\frac{{P}_{t}}{{P}_{t+s}}\frac{{C}_{t}}{{C}_{t+s}}\right]\). The firm’s maximization problem is

The first-order condition is

The aggregate producer-price index of the South is the weighted average of the optimal price \({P}_{S,t}^{*}\) and the average price in the previous period, \({P}_{S,t-1}\):

3 Parameter values

We carefully selected parameters to ensure that our model accurately reflects economic features of the South, the North, and the rest of the world (RoW). The EA we studied consists of countries that have been members since 2003. We excluded Luxembourg from our analysis because of its small size. Our choice of parameters closely follows previous work by Engler et al. (2017) and Engler et al. (2018). As in Engler et al. (2018), we used data from the OECD (2018) and World Bank (2019) to establish the relative sizes of the regions and their corresponding import-to-GDP ratios. However, slight adjustments were made to the import-to-GDP ratios to achieve a balanced steady state, where per capita consumption and output levels are equal across regions, and trade between them is balanced. Specifically, we set the relative size of the RoW at 82%, which represents the 10-year average of relative GDPs from 2004 to 2013, as reported in Engler et al. (2018). In 2011, the South accounted for 34% of the EA GDP, equivalent to approximately 6% of the world economy, while the North's share was roughly 12%. We assume that the share of imported goods in the South's consumption basket corresponds to the GDP-weighted import-to-GDP ratios. According to Engler et al. (2017), the GDP-weighted import-to-GDP ratio in the South was 33% in 2011, which means that the share of domestic consumption in the South is assumed to be 67%. As mentioned, we assume that the levels of per-capita output and consumption are equal across regions, and that trade between them is balanced. This implies that the initial share of imported goods in the North's consumption basket is 17%, with the remaining 83% representing domestic consumption. Engler et al. (2018) find that the import-to-GDP of the South (North) from the North (South) at 6% (5%) and from the RoW at 27% (12%). The share of the South's and North's goods in the RoW's consumption basket hast to set at 1% and 3%, respectively, implying that the share of home-goods in the RoW is roughly 96%. Consequently, there is a pronounced home bias in consumption across all regions (Table 1).

The model parameters are set as follows: the discount factor is 0.99, the inverse Frisch elasticity is 1, and the Armington elasticity is 2, which is a key parameter. Feenstra et al. (2018) find that the macroelasticity, which measures substitution between home and foreign goods, is roughly 2. The elasticity of substitution between goods produced in the same region and the elasticity of substitution between different types of labor are both set at 9. Engler et al. (2017) set the probability of not adjusting prices and wages at 0.66 and 0.75, respectively, based on the evidence of Druant et al. (2009) on wage and price adjustment in the EA. This implies that the average duration between price and wage adjustments is three and four quarters, respectively. The coefficient for inflation in the monetary policy rule is set at 2, and the degree of interest rate smoothing at 0.7, which are in line with estimates for the ECB (Pinkwart 2013). There is no clear consensus on the persistence of monetary shocks, with Galí (2015) setting it at 0.5 and Jermann and Quadrini (2012) obtaining an estimate of 0.203. Our choice is 0.4, which is roughly their average. Based on Kemmerling’s (2009) findings, Engler et al. (2017) calculated that the GDP-weighted average for the SCR (VAT) rate in the EA is 24% and 16%, respectively. The persistence of tax shocks is set at 1, which implies that they are permanent. We extend Engler et al. (2018) by incorporating public consumption and TFP performance. We set the initial share of public consumption at 21% based on the World Bank’s (2019) data for the EA. The persistence of public consumption shocks in the case of fiscal consolidation is set at 0.9, while it is set at 0.8 in the case of the North’s fiscal expansion. Finally, we set δ at 0.15 to ensure gradual growth in TFP for all three regions.

4 Productivity, Monetary and Fiscal Policy in the 2010s

In Fig. 1, it can be observed that since 2011, the current account surplus of the North has increased, the South has transitioned from a deficit to a surplus, and the EA's current account surplus has significantly grown. The economic policies of the EA have been characterized by loose monetary policy since the mid-2010s, severe austerity measures in the early 2010s, and poor TFP performance. In this section, we aim to examine the implications of these policies on the EA's current account during the period of 2011–2017.

4.1 Monetary Policy

During and after the GFC, many central banks lowered their policy rates to the zero lower bound and initiated unconventional monetary policy to lower market interest rates. The US interest rates can be used as a proxy for world interest rates. According to the Global Financial Cycle, US monetary policy and financial conditions have a significant influence on financial markets worldwide. Moreover, central banks in several countries follow US monetary policy to reduce currency fluctuations against the US dollar. Figure 3 illustrates the Wu-Xia shadow rate (Wu and Xia 2016) of monetary policy for the EA and the US at the annual level, as well as the interest rates implied by the original Taylor rule (Taylor 1993), where r* is set at 1. The figure shows that the ECB's monetary policy became loose relative to that of the US in the latter part of the 2010s, with a relative deviation from the Taylor rule of approximately 4 percentage points in 2017. In other words, the deviation from the Taylor rule was 4 percentage points higher in the EA than in the US. Therefore, we set the size of the ECB's monetary policy shock at 4 percentage points.

The findings presented in Fig. 4 demonstrate the impact of an annual 4 percentage point decrease in the EA interest rate, with inflation rates expressed as annualized percentage points, interest rates in annualized basis point deviations, and deviations of trade and current account balances expressed as a percentage of initial output. For all other variables we report percentage deviations from their steady state values. The depreciation of the nominal and real exchange rates following the interest rate fall results in an expenditure switching effect, where the goods produced in the EA become relatively cheaper, thus boosting the demand for them and reducing the demand for goods produced in the RoW. As illustrated in Fig. 4, the EA's monetary policy has led to an increase in the North's and the South's current account surpluses by 0.7% and 1.2%, respectively, relative to GDP, driven by the varying degrees of openness of these regions. It is worth noting that the EA's current account surplus started to grow in 2015, following a decline in the ECB's shadow policy rate below the US rate, as indicated in Fig. 1.

Expansionary monetary policy in the EA

We analyze the consequences of a 4 percentage point decrease in the EA interest rate. However, Fig. 3 reveals that the difference between the ECB's shadow rate and the US interest rate has exceeded 4 percentage points since 2016, with an average difference of 8 percentage points in 2017. Thus, our simulation may underestimate the current account effect of the ECB's monetary expansion. It is possible that monetary policy has been the primary driver of the improvement in the current account in the latter part of the 2010s. According to Gibson et al. (2021), the announcement by the ECB in January 2015 that it would initiate asset purchases had a significant impact on sovereign ratings and spreads. A common factor between our findings and those of Gibson et al. (2021) is that both studies emphasize the significant impact of the ECB’s unconventional monetary policy on the EA’s economy and financial markets.

Lee and Chinn (2006) conducted an empirical analysis on the relationship between monetary policy, the real exchange rate, and the current account. They found that an expansionary monetary policy causes an immediate depreciation of the real exchange rate, which gradually returns to its initial level. This real depreciation improves the current account in the short term, but the effect fades away over time. Our simulation results are fully consistent with these empirical observations. Moreover, our findings align with those of the most open economy models.

Backus et al. (1994) found that the median correlation between net exports (as a percentage of GDP) and the terms of trade (defined as the logarithm of the ratio of the import deflator to the export deflator) was -0.46. Our model estimates that the South's net exports experienced a peak effect of 1.2% of GDP, while the GDP-weighted peak change in the South's terms of trade relative to the rest of the world was -3.09%. The correlation between net exports and the terms of trade in our model is -0.4, which is consistent with the empirical evidence. The precise trade balance response in our model to fluctuations in the international price ratio validates our choice of using PCP and a low Armington elasticity.

4.2 Fiscal Consolidation

In the 2010s, the EA implemented fiscal consolidation to reduce public deficits and public debt-to-GDP ratios. According to the IMF (2018), the GDP-weighted improvement in the structural fiscal balances in 2011–2017 was 4.1% of GDP in the South and 2.7% of GDP in the North. We use these estimates to analyze the effect of a negative fiscal spending shock that is 4.1% of GDP in the South and 2.7% of GDP in the North. Therefore, we opted for an expenditure-based fiscal consolidation approach, rather than a tax-based one, given the dominant emphasis on expenditure cuts as a means of achieving fiscal consolidation in the EA since 2011, as documented by Rannenberg et al. (2015).

Figure 5 illustrates the significant negative impact of fiscal consolidation on the GDP of the South and a relatively smaller effect on the North. However, the positive current account effect is 1.04% of GDP for the South and 0.31% of GDP for the North. The fiscal consolidation measures have contributed to the improvement of the current account balance in both regions, with the stronger measures in the South leading to a more significant current account improvement. The figure also demonstrates a real exchange rate depreciation in both regions of the EA due to fiscal consolidation. Benetrix and Lane (2013) present empirical evidence suggesting that a positive fiscal shock results in the appreciation of the real exchange rate in the short and medium term for a panel of EA countries. Our findings align with these empirical results.

Fiscal consolidation in EA

Kollmann et al. (2016) investigated the consequences of the EA's fiscal expansion in a model featuring regions that represent the EA, the US, and the rest of the world. They discovered that it leads to a real exchange rate appreciation, a decline in the trade balance, and an increase in output in the EA. Our research is consistent with their results. However, our contribution is to analyze the impacts of fiscal consolidation on the external balances of the North and the South.

In an empirical study conducted by Abbas et al. (2011), a fiscal consolidation of 1% of GDP was found to improve the current account by 0.3% of GDP. Although the current account effect in our paper is weaker, it is important to note that Abbas et al. also found that the effect is much weaker during episodes of large fiscal consolidations. In addition, Bussière et al. (2010) estimate the effect to be 0.14% of GDP. Therefore, our results are broadly in line with these empirical estimates.

Our simulation shows that the fiscal consolidation implemented during the 2010s had a negative effect on output in both regions of the EA. Therefore, the fiscal expansion proposed by the Next Generation EU can be beneficial for the EU/EA as it can support the recovery from the COVID-19 recession. This approach helps to avoid repeating the mistake of the 2010s, which was implementing fiscal consolidation during the early stages of the recovery.

4.3 Productivity

TFP growth has been sluggish worldwide since the GFC. We calculated the growth of TFP for the model's regions between 2011 and 2017, using the TFP data from the Conference Board (2019). Our analysis revealed that TFP in the South grew by only 0.4%, while in the North, it rose by 2.4%. Meanwhile, TFP growth in the RoW was 4.2%. These results suggest that the EA experienced a significant negative TFP shock relative to the RoW. We investigate the impact of TFP performance on the current account by introducing TFP shocks at the magnitudes corresponding to the growth rates observed in our model's regions between 2011 and 2017.

Figure 6 displays the effects of TFP shocks on the regions. They appreciate the real exchange rates in both the South (by 0.95%) and the North (by 0.73%) and improve the South's current account by 0.3% of GDP. However, the North's current account is hardly affected, with only a -0.05% of GDP impact. The RoW experiences the best TFP performance and thus sees the largest fall in producer price inflation. The increase in the relative supply of goods causes them to be sold at lower relative prices, leading to a real exchange rate depreciation. In the short term, the South is relatively rich and, for consumption smoothing purposes, runs a current account surplus despite a real exchange rate devaluation. Our results differ from those of Kollmann et al. (2016) who found that both temporary and permanent positive TFP shocks in the EA induce a trade balance improvement. Lee and Chinn (2006) find empirical evidence that the comovement between the real exchange rate and the current account is indeed positive following a productivity shock. Empirical research conducted by Basu et al. (2006) suggests that a positive TFP shock results in a significant depreciation of the real exchange rate. Our finding is consistent with this empirical evidence.

Productivity shocks

In an empirical study, Bussière et al. (2010) find that a 1% increase in country-specific productivity worsens the current account balance by 0.11% of GDP. In our model, we simulate a 2% (3.8%) fall in TFP for the South relative to the North (the RoW), which results in a GDP-weighted fall in TFP relative to the world of roughly 3.6%. Applying the result of Bussière et al. (2010) to our model suggests that a TFP fall of 3.6% should improve the current account by roughly 0.4% of GDP. However, our finding shows a smaller effect of 0.3% of GDP. While improving the TFP of the South would have substantial benefits, our simulations suggest that it could have a negative effect on the current account of the South.

5 North’s Economic Policy and External Imbalances

5.1 Fiscal Revaluation

In a monetary union, nominal exchange rate devaluations are not possible. As an alternative, a fiscal devaluation has been proposed for the EA's South to potentially depreciate the real exchange rate. While Farhi et al. (2014) found that this policy can replicate the effects of a nominal exchange rate devaluation, Engler et al. (2017) have shown that a 1% of GDP fiscal devaluation in the South only depreciates the real exchange rate by 0.3% and improves the trade balance by 0.3% of GDP. These findings question the effectiveness of fiscal devaluations. The real exchange rate reflects a country's price competitiveness relative to its competitors. The IMF (2014) estimated that Germany's real exchange rate was undervalued by 5–15%. The IMF further recommended that additional policies are necessary to facilitate more rapid rebalancing in the EA, and that Germany could significantly contribute to promoting regional rebalancing. The North's fiscal revaluation could enhance the South's price competitiveness by improving its relative exchange rate. Some argue that the North's wage moderation has excessively improved its price competitiveness, and a fiscal revaluation in the North could be a way to share the burden of adjustment. While previous DGSE literature has only focused on fiscal devaluations in individual countries or groups of countries that resemble the South, our study explores the potential effects of a fiscal revaluation in the North.

In Fig. 7, we present the effects of a 1% of GDP fiscal revaluation in the North. This policy leads to an appreciation of the North's real exchange rate and a decrease in output, both in the North and the South. While it reduces the external imbalance within the EA, the effects on the current account balances are small: it improves the South's current account balance only by 0.16% of GDP, while worsening the North's by 0.21%. Despite being new findings, these results are consistent with the existing literature that focused on fiscal devaluations in the South. However, it is worth noting that the positive effect on the South's output in the medium term is weak and short-lived. Moreover, the current account effects of the fiscal revaluation are small compared to the size of the tax reform. These results highlight the challenges of using fiscal revaluations as a policy tool to address external imbalances in a monetary union. They also suggest that other policies, such as productivity-enhancing reforms, may be more effective in achieving the desired macroeconomic outcomes.

Fiscal revaluation in the north

In Fig. 7, we examine the impact of a fiscal revaluation of 1% of GDP in the North. Our findings show that such a policy would lead to an appreciation of the real exchange rate and a decrease in output in both the North and the South in the short term, while reducing the external imbalance within the EA. However, the effects on current account balances are relatively small, with only a 0.16% improvement for the South and a 0.21% worsening for the North. These effects are negligible compared to the size of the tax reform. Moreover, our results suggest that any positive effect on the South's output in the medium term is weak and short-lived. While previous studies have not examined the effects of fiscal revaluations on external imbalances, our findings provide new insights. Nevertheless, the impact on current accounts of a fiscal revaluation in the North can be compared with the impact of the South's fiscal devaluation.

Engler et al. (2018) found that a 1% of GDP fiscal devaluation improves the South's current account by 0.3% of GDP, while Cizkowicz et al. (2020) found that the average effect on net exports in DSGE models to be 0.7% of GDP. However, Engler et al. (2017) also highlight that the effect of a fiscal devaluation depends on country size and openness to trade. While a fiscal devaluation improves price competitiveness, this comes at the expense of other countries, and its impact on the current account diminishes as more countries implement the policy. In our model, the North's fiscal revaluation of 1% of GDP appreciates its real exchange rate, reduces output in both the North and South in the short term, and improves the external imbalance within the EA. However, the improvement in the South's current account is only 0.16% of GDP, while the North's deteriorates by 0.21% of GDP. While these effects are small compared to the size of the tax reform, they demonstrate that the impact of fiscal revaluations on current accounts varies depending on the country size and degree of openness. Our results differ from the existing literature, which focuses on fiscal devaluations in individual countries or groups of countries similar to the South, whereas the North has a larger economy and is less open to the rest of the world.

As depicted in Fig. 7, a fiscal revaluation initially leads to an appreciation of the real exchange rate, but this effect gradually weakens over time. Arach and Assisi (2021) empirical study finds that a fiscal devaluation results in a depreciation of the real exchange rate in the short term, but this effect also gradually fades away and eventually disappears in the long term. Our results are consistent with this empirical evidence.

The empirical paper by De Mooij and Keen (2013) finds that a 1 percentage point increase in the VAT rate improves net exports by 0.23% of GDP, but there is no statistically significant effect of an increase in SCR. These findings imply that a reduction of the VAT rate by 0.9 percentage points and an increase of the SCR rate by 2 percentage points would worsen net exports by 0.21% of GDP, which corresponds to a fiscal devaluation of 1% of GDP in our model. Our result of -0.21% is in line with the empirical evidence of De Mooij and Keen (2013).

Holzner et al. (2018) conducted an empirical study on the trade balance effects of fiscal devaluations in European Union countries, including the South, which is the same group of countries studied in our research. Their findings show that a fiscal devaluation of 1% of GDP in the South improves the trade balance by 0.75% of GDP. This suggests that the net export effects of a fiscal revaluation or devaluation may be greater than what our simulations suggest, indicating that our model could underestimate the impact of the North's fiscal revaluation on the South's net exports. However, Holzner et al. (2018) highlight that their conclusions are similar to Engler et al. (2017) in that fiscal devaluations are not an effective substitute for nominal exchange rate devaluations. Our study adds to these findings, showing that the North's fiscal revaluation has limited effects on external imbalances between the North and South. This highlights the need for the EU to recognize that fiscal revaluations and devaluations are not effective tools to reduce cost divergence and external imbalances, contrary to the claims made by Farhi et al. (2014). The absence of the nominal exchange rate as an adjustment instrument remains a significant challenge for economic integration in the EA.

5.2 Fiscal Expansion

One potential policy to reduce external imbalances within the EA is through a fiscal expansion in the North. Romer (2012) suggests that a fiscal expansion in trade surplus countries could boost domestic demand and growth, ultimately benefiting their struggling neighbors. Blanchard et al. (2017) similarly argue that a fiscal expansion is necessary for the EA, but note that the South may face concerns about fiscal solvency that could limit its ability to implement such policies. As a result, a fiscal expansion from the North may be necessary to address the imbalances.

Figure 8 illustrates the impact of a fiscal expansion of 1% of GDP in the North, which leads to output gains in both the North and the South. However, the effect on external imbalances is limited: the South's current account only improves by 0.1% of GDP, while the North's current account deteriorates by approximately 0.2% of GDP. Therefore, while a fiscal expansion in the North would be beneficial for the EA, it is not a comprehensive solution to address external imbalances. Abbas et al. (2011) report that a fiscal consolidation of 1% of GDP improves the current account by an average of 0.3% of GDP, while Bussière et al. (2010) find a smaller effect of 0.14% of GDP. Our result falls between these two empirical estimates. Benetrix and Lane (2013) found that a positive fiscal shock leads to a short- and medium-term appreciation of the real exchange rate in EA countries. Our results are consistent with theirs.

Fiscal expansion in the north

Blanchard et al. (2017) used a DSGE model to analyze the effect of the North's fiscal expansion on the South's output and found that it is negative due to the monetary policy response outweighing the demand stimulus from the North's expansion and the depreciation of the South's real exchange rate. However, our model shows that the positive effects dominate and the North's fiscal expansion has a positive externality on the South's output. Our results align with the findings of Auerbach et al. (2020) that the spillover effect of a fiscal expansion under a fixed exchange rate is positive.

Blanchard et al. (2017) used a framework that assumes the current account balance is always zero, which is not well-suited to address the external imbalances within the EA. On the other hand, our paper is consistent with the view of Romer (2012) that a fiscal expansion can stimulate output in the North, reduce its current account surplus, and positively affect the South through trade linkages. However, our model suggests that the trade effect may not be as large as Romer suggests, even with a plausible degree of trade linkages. In addition, our finding that the North's fiscal expansion has limited benefits for external imbalances is consistent with the empirical findings.

6 Sensitivity Analysis

Feenstra et al. (2018) stress that the Armington elasticity, which measures the substitutability between goods produced in different countries or regions, is a crucial parameter in international economics as it determines the strength of the relative demand response to changes in relative international prices. Based on their average macroelasticity estimate, Feenstra et al. (2018) find that the Armington elasticity is around 2. However, Dong's (2012) estimate is slightly lower at 1.5, while Imbs and Mejean (2015) report a higher estimate at approximately 3, based on their aggregate elasticity.

Figure 9 illustrates the sensitivity of the current account response to changes in the Armington elasticity. When the Armington elasticity is reduced from 2 to 1.5, the current account response of the South (and North) to a monetary expansion decreases from 1.17% (0.7%) of GDP to 0.4% (0.25%) of GDP. A smaller (higher) Armington elasticity implies that domestic and foreign goods are poorer (better) substitutes, and therefore, the expenditure-switching effect of a real exchange rate change is weaker (stronger). As a result, the smaller (higher) the Armington elasticity, the weaker (stronger) the current account effect of shocks. Figure 9 highlights that the current account response is sensitive to changes in the Armington elasticity. We want to emphasize that the effects of shocks on the current account are not sensitive to other parameters.

Sensitivity analysis: The current account response

7 Conclusion

The instability of capital flows can lead to overheating, financial bubbles, and ultimately result in financial crises. In the period between the creation of the Euro and the GFC, capital flow instability led to an increase in the current account deficit of the South, while the North's surplus grew. The EA experienced an internal balance of payments crisis in the early 2010s, and it was commonly believed that both the North and the South's external balances needed to be reversed (Pettis 2012). However, following the onset of the Euro crisis, the South moved from a current account deficit to a surplus, while the North's surplus continued to increase. As a result, the EA's aggregate current account balance shifted from a roughly balanced position to a substantial surplus. Our main contribution is to study the causes of the current account adjustment in the EA after the onset of the Euro crisis. Our simulations illustrate that the monetary expansion, fiscal consolidation, and weak TFP performance of the EA may explain a significant portion of the current account adjustment in the 2010s. These macroeconomic policies and factors may have resolved the EA's internal balance of payments crisis.

In the latter part of the 2010s, the ECB implemented a loose monetary policy, which improved the South's and the North's current account surplus by 1.2% and 0.7% of GDP, respectively. Our model suggests that the ECB's monetary policy is likely the main cause of the improvement in the current account in the latter part of the 2010s. The relationship between monetary policy, the real exchange rate, and the current account, as well as between net exports and the terms of trade in our model, is consistent with the empirical evidence of Lee and Chinn (2006) and Backus et al. (1994).

Our study highlights the considerable effect of fiscal consolidation during the euro crisis on the South's current account balance (1% of GDP), while the effect on the North is more modest (0.3% of GDP). These findings are consistent with empirical evidence from Abbas et al. (2011) and Bussière et al. (2010) on the impact of fiscal consolidation on the current account. However, our results also reveal that the fiscal consolidation in the 2010s had a significant negative effect on output. To avoid making the same mistake during the current COVID-19 recession, the Next Generation EU initiative could prove beneficial for the EU/EA by supporting the recovery and preventing damaging fiscal consolidation measures in the early stages.

During the 2010s, the EA experienced a negative TFP shock, particularly in the South, relative to the rest of the world. Our analysis shows that this TFP performance has improved the South's current account by 0.3% of GDP, while having virtually no effect on the North's current account. This result contrasts with Kollmann et al. (2016), who find that the EA's poor TFP causes a fall in net exports. However, our model is able to match the empirically observed positive comovement between the real exchange rate and the current account following a TFP shock (Lee and Chinn 2006) and the positive response of the current account to a negative TFP shock (Bussière et al. 2010), which is not captured by Kollmann et al. (2016). In the 2020s, improving the South's TFP is a crucial productivity challenge for the EU, and this would have significant benefits. However, our simulations suggest that it may have an adverse effect on the current account of the EA's South.

Effective economic policies are crucial for the success of the European project. In this study, we examine two potential policies aimed at reducing external imbalances within the EA. One option is a fiscal revaluation of the North, which our novel results show would have limited benefits in reducing external imbalances. It is important to acknowledge that neither fiscal revaluations nor devaluations are effective policy tools to affect external imbalances, contrary to the claim of Farhi et al. (2014). An alternative option is a fiscal expansion in the North, which our simulations show would have a small positive impact on the South's current account and a limited negative impact on the North's current account, contradicting the argument of Romer (2012). Therefore, we conclude that neither fiscal revaluation nor fiscal expansion in the North is an effective tool to reduce the current account imbalances within the EA.

It is important to acknowledge that the main findings of the study may depend on certain modeling choices. The model employing PCP has the capacity to replicate the observed median correlation between net exports and the terms of trade. Nevertheless, the option of using LCP alongside an alternative, plausible calibration of the model might also align with the observed patterns. We consider investigating alternative export/import pricing strategies to be a topic worthy of future research. We acknowledge that the absence of capital in our model represents a limitation, and we recognize that including capital in the model is an area of focus for future research. The trade balance and output effects resulting from our assumed expenditure-based fiscal consolidation could potentially exhibit variation compared to those stemming from tax-based fiscal consolidation. Consequently, investigating how significantly the primary findings are influenced by the composition of fiscal consolidation presents a promising avenue for future research.

Data Availability

The data used in Fig. 1 are openly available in World Bank Open Data at http://data.worldbank.org/ “Current account balance (BoP, current US)(BN. CAB. XOKA. CD)” and “GDP(currentUS)(NY.GDP.MKTP.CD)”. The data used in Fig. 2 are openly available in Eurostat database at https://ec.europa.eu/eurostat/data/database “Industrial countries' effective exchange rates including new Member States - annual data [ert_eff_ic_a], Real Effective Exchange Rate (deflator: consumer price indices - 17 trading partners - Euro Area)”. The data used in Fig. 3 are openly available in World Economic Outlook Database at https://www.imf.org/en/Publications/WEO/weo-database/2020/October “Output gap in percent of potential GDP” and “Inflation, average consumer prices”; in Fred Database at https://fred.stlouisfed.org “Federal Funds Effective Rate (DFF)”; and; “European Central Bank shadow rate” and “United States shadow fed funds rate” at https://sites.google.com/view/jingcynthiawu/shadow-rates.

Notes

We focus on countries that have been members of the euro area at least since 2003. However, we ignore Luxembourg due to its small size.

References

Abbas SMA, Bouhga-Hagbe J, Fatás A, Mauro P, Velloso RC (2011) Fiscal policy and the current account. IMF Econ Rev 59:603–629

Arach G, Assisi D (2021) Fiscal devaluation and relative prices: Evidence from the Euro area. Int Tax Public Financ 28:685–716

Auerbach A, Gorodnichenko Y, Murphy D (2020) Local fiscal multipliers and fiscal spillovers in the USA. IMF Econ Rev 68:195–229

Backus D, Kehoe PJ, Kydland FE (1994) Dynamics of the trade balance and the terms of trade: The J-Curve? Am Econ Rev 84:84–103

Basu S, Kimball MS, Fernald JG (2006) Are technology improvements contractionary? Am Econ Revi 96:1418–1448

Benetrix AS, Lane PR (2013) Fiscal shocks and the real exchange rate. Int J Cent Bank 9:6–37

Blanchard O, Erceg CJ, Lindé J (2017) Jump-starting the euro area recovery: Would a rise in core fiscal spending help the periphery? NBER Macroecon Annu 31:103–182

Bussière M, Fratzscher M, Müller GJ (2010) Productivity shocks, budget deficits and the current account. J Int Money Financ 29:1562–1579

Cizkowicz P, Radzikowski B, Rzonca A, Wojciechowski W (2020) Fiscal devaluation and economic activity in the EU. Econ Model 88:59–81

Conference Board (2019) Total economy database available at https://www.conference-board.org/data/economydatabase/index.cfm?id=27762 (accessed on 23 Dec 2019)

De Mooij R, Keen M (2013) ‘Fiscal devaluation’ and fiscal consolidation: The VAT in troubled times, in: Fiscal Policy after the Financial Crisis, ed. by A. Alesina, F. Giavazzi (Chicago: University of Chicago Press), 443–485

Dong W (2012) The role of expenditure switching in the global imbalance adjustment. J Int Econ 86:237–251

Druant M, Fabiani S, Kezdi G, Lamo A, Martins F, Sabbatini R (2009) How are firms’ wages and prices linked: Survey evidence in Europe. Eur Cent Bank Work Pap Ser 1084

Engler P, Ganelli G, Tervala J, Voigts S (2017) Fiscal devaluation in a monetary union. IMF Econ Rev 65:241–273

Engler P, Pasch S, Tervala J (2018) Third country effects of fiscal devaluations. Econ Lett 163:13–16

Eurostat (2019) Industrial countries' effective exchange rates including new Member States - annual data [ert_eff_ic_a], Real Effective Exchange Rate (deflator: consumer price indices - 17 trading partners - Euro Area), availabe at https://ec.europa.eu/eurostat/databrowser/view/ERT_EFF_IC_A/default/table?lang=en

Farhi E, Gopinath G, Itskhoki O (2014) Fiscal devaluations. Rev Econ Stud 81(2):725–760

Feenstra RC, Luck P, Obstfeld M, Russ KN (2018) In search of the Armington elasticity. Rev Econ Stat 100:135–150

Galí J (2015) Monetary policy, inflation, and the business cycle: An introduction to the new Keynesian framework and its applications. Princeton University Press, Princeton

Gibson HD, Hall SG, GeFang D, Petroulas P, Tavlas GS (2021) Cross-country spillovers of national financial markets and the effectiveness of ECB policies during the euro-area crisis. Oxf Econ Pap 73:1454–1470

Gomes S, Jacquinot P, Pisani M (2016) Fiscal devaluation in the Euro area: A model-based analysis. Econ Model 52:58–70

Hohberger S, Kraus L (2016) Is fiscal devaluation welfare enhancing? Econ Model 58:512–522

Holzner M, Tkalec M, Vizek M, Vukšić G (2018) Fiscal devaluations: Evidence using bilateral trade balance data. Rev World Econ 154:247–275

Imbs J, Mejean I (2015) Elasticity optimism. Am Econ J Macroecon 7:43–83

IMF (2014) Germany: 2014 article IV consultation—staff report; press release; and statement by the executive director for Germany. IMF Country Report No. 14/216

IMF (2018) World economic outlook database October 2018 (accessed on 24 Apr 2019)

IMF (2020) World economic outlook database October 2020 (accessed on 16 Nov 2020)

Jermann U, Quadrini V (2012) Macroeconomic effects of financial shocks. Am Econ Rev 102:238–271

Kemmerling A (2009) Taxing the Working Poor: The Political Origins and Economic Consequences of Taxing Low Wage. Edward Elgar Publishing, Cheltenham

Kollmann R, Pataracchia B, Raciborski R, Ratto M, Roeger W, Vogel L (2016) The post-crisis slump in the Euro area and the US: Evidence from an estimated three-region DSGE model. Eur Econ Rev 88:21–41

Lee J, Chinn MD (2006) Current account and real exchange rate dynamics in the G7 countries. J Int Money Financ 25:257–274

OECD (2018) Data available online at https://www.oecd.org/eco/outlook/economic-outlook-november-2018/ (accessed 29 Apr 2019)

Ortega E, Osbat C (2020) Exchange rate pass-through in the Euro area and EU countries. Countries ECB Occasional Paper Series No. 241

Pettis M (2012) Europe has a much bigger problem than debt, and nobody has any clue how to fix it. Bus Insider available at https://www.businessinsider.com/europe-has-a-much-bigger-problem-than-debt-and-nobody-has-any-clue-how-to-fix-it-2012-1?r=USIR=T. Accessed 16 May 2019

Pinkwart N (2013) Quantifying the European Central Bank’s interest rate smoothing behavior. Manchester Sch 81:470–492

Rannenberg A, Schoder C, Strasky J (2015) The macroeconomic effects of the euro area's fiscal consolidation 2011–2013: A simulation-based approach. Res Tech Pap 03/RT/2015, Central Bank of Ireland

Romer C (2012) Fiscal policy in the crisis: Lessons and policy implications. Presentation at the IMF Fiscal Forum, Washington, DC

Sinn H-R (2012) The European balance of payments crisis: An introduction. Cesifo 13:3–10

St. Louis Fed (2019) Effective fed funds rate. Data available online at https://fred.stlouisfed.org/ (accessed 18 Apr 2019)

Taylor JB (1993) Discretion versus policy rules in practice. Carn-Roch Conf Ser Public Policy 39:195–214

Tervala J, Watson T (2022) Hysteresis and fiscal stimulus in a recession. J Int Money Finance 124:102614

World Bank (2019) Data available online at http://data.worldbank.org/ (accessed 23 Apr 2019)

Wu JC (2019) European Central Bank shadow rate and United States shadow fed funds rate. Available at https://sites.google.com/view/jingcynthiawu/shadow-rates (accessed 30 Apr 2019)

Wu JC, Xia FD (2016) Measuring the macroeconomic impact of monetary policy at the zero lower bound. J Money Credit Bank 48:253–291

Acknowledgements

The authors express their gratitude for the feedback provided by the editor (George Tavlas), the two anonymous reviewers, and participants of seminars at the 23rd INFER Annual Conference, the 10th UECE Conference on Economic and Financial Adjustments, and the "Back to normal?" Or "Is there a 'new normal' in EU Economic Policies and Governance?" workshop.

Funding

Open Access funding provided by University of Helsinki including Helsinki University Central Hospital.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of Interest

The authors have no relevant financial or non-financial interests to disclose and have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Pasch, S., Tervala, J. Current Account Adjustment of the Euro Area in the 2010s: Causes and Policies. Open Econ Rev (2023). https://doi.org/10.1007/s11079-023-09732-7

Accepted:

Published:

DOI: https://doi.org/10.1007/s11079-023-09732-7