Abstract

Cost of capital is an important driver of investment decisions, including the large investments needed to execute the low-carbon energy transition. Most models, however, abstract from country or technology differences in cost of capital and use uniform assumptions. These might lead to biased results regarding the transition of certain countries towards renewables in the power mix and potentially to a sub-optimal use of public resources. In this paper, we differentiate the cost of capital per country and technology for European Union (EU) countries to more accurately reflect real-world market conditions. Using empirical data from the EU, we find significant differences in the cost of capital across countries and energy technologies. Implementing these differentiated costs of capital in an energy model, we show large implications for the technology mix, deployment, carbon emissions and electricity system costs. Cost-reducing effects stemming from financing experience are observed in all EU countries and their impact is larger in the presence of high carbon prices. In sum, we contribute to the development of energy system models with a method to differentiate the cost of capital for incumbent fossil fuel technologies as well as novel renewable technologies. The increasingly accurate projections of such models can help policymakers engineer a more effective and efficient energy transition.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In making the transition to a carbon neutral economy by 2050, the European Union (EU) is facing a very large challenge. What we know with certainty is that the transition requires large amounts of private and public investment. Estimates range between 1 and 2% of EU GDP (e.g. McCollum et al. 2013, 2018; OECD/IEA and IRENA 2017; European Commission 2018). This is well below total annual savings and investment, so the challenge is not raising the money but rather “Shifting the Trillions” from fossil fuels to renewables (Hansen et al. 2017). Indeed, policymakers are starting to do so. The European Commission, for example, in its recent Green Deal programme (European Commission 2020a) has announced it will shift over 1 trillion euros into the transition, as evidenced by the recently approved 7-year budget.

In allocating these funds, policymakers in Europe and elsewhere rely heavily on models and model projections (Luderer et al. 2012; Capros et al. 2016). Recent model simulations have shown that a transition towards a 100% renewable energy-based power system by 2050 is feasible (Jacobson et al. 2018; Bogdanov et al. 2019b), although large uncertainties remain around the most efficient technological pathways and the overall costs for the transition (Paroussos et al. 2019a). But as illuminating as well-built and carefully calibrated model simulations are, they inevitably rely on a large number of simplifying assumptions. In addition, the complexity of the models does not always reveal how sensitive the outcomes to such assumptions.

In this paper, we zoom in on assumptions concerning the weighted average cost of capital (WACC).Footnote 1 The WACC is a fundamental driver in investment decisions in the private sector. The typical assumption in models routinely used to simulate transition pathways is that all technologies face similar or the same WACCs in all countries and over time (e.g. Capros et al. 2016; Bogdanov et al. 2019b; IEA 2020). Prior research shows, however, that cost of capital differs significantly between technologies and countries (Ondraczek et al. 2015; Steffen 2020) (Egli 2020) and also changes over time as technologies mature (a phenomenon referred to as “financing experience”) (Egli et al. 2018). It has also been demonstrated that outcomes are very sensitive to changes in the WACC in stylized power generation investment models (Iyer et al. 2015; Hirth and Steckel 2016). In this paper, we show that taking such differences into account yields very different modelling outcomes, potentially leading to misguided policy conclusions. One would, for example, at uniform WACCs over- and underestimate the adoption of renewables in risky and safer countries, respectively. In a time when energy transition is high on the policy agenda and the trillions are actually being shifted, such errors can be costly, and building methodologies and models that more accurately describe the transition is an urgent challenge for academics.

To address this challenge, we formulate two related research questions. First, we investigate (RQ A): What is the effect of the introduction of differentiated WACCs for reference scenarios (based on current legislation) for the electricity system? Second, and even more important (RQ B): How do differences in cost of capital affect the optimal transition pathway for more ambitious climate policies in Europe?

To answer our research questions, we make two empirical and one conceptual contribution to an emerging literature that calls for differentiated data on WACCs for modelling the energy transition in a more realistic way (Gupta et al. 2014; Egli et al. 2019; Bachner et al. 2019). First, we develop a comprehensive dataset on real-world WACCs for all electricity production technologies and all EU countries using new data from a variety of sources and a novel empirical approach. Second, using this dataset, we compare model projections for a reference and an ambitious climate policy scenario for European countries up to 2050 to show how differentiated WACCs change the transition pathways, emissions and costs. Our simulations are carried out on the GEM-E3-Power model (which is the electricity module of the macro-economic GEM-E3 model). By considering differences in WACCs for renewable and fossil fuel-based technologies, we address the shortcoming that there is a strong focus on the WACC of renewables because these technologies seem to carry more technical and market risks, while WACC assumptions for fossil fuels facing rising transition and policy risks are set to low historic or “standard” values from the literature. Third, our approach conceptually opens up the possibility to model WACCs dynamically over time. As a case in point, we incorporate financing experience curves (Egli et al. 2018) in the GEM-E3-Power model to project declining WACCs for renewables as their deployment increases.

Our results show that differentiating WACCs by country for the Europe-28 have significant impact on our model outcomes. Renewables become more competitive in low-risk countries, while they are less so in high-risk countries. As country risk and the potential for renewables are not aligned, this implies that without policy the transition is unlikely to evolve in a cost-effective manner.

The remainder of this paper is structured as follows: Section 2 provides a brief summary of the literature on the cost of capital in the energy sector, covering both empirical and model-based literature on the cost of capital. Our methodology for deriving country- and technology-specific WACCs is explained in Section 3, where we also present our estimated WACCs. Section 4 presents the results when these WACCs are implemented in the GEM-E3-Power model to explore the effects on technology mix, electricity costs, CO2 emissions and diffusion of low-carbon technologies. Section 5 concludes.

2 Conceptual background: financing conditions for energy technologies

The scientific literature on financing investment to mitigate climate change was limited and fragmented for a long period (Gupta et al. 2014) but has rapidly expanded in recent years (Steckel et al. 2017; Polzin et al. 2017; Mazzucato and Semieniuk 2018). The deployment of renewable power generation technologies to mitigate carbon emissions typically requires high upfront investment (Schmidt 2014; Tietjen et al. 2016; Bachner et al. 2019). In the absence of fuel costs, costs of capital account for a much higher share of total costs compared to incumbent fossil fuel technologies like gas and coal (Schmidt 2014; Fragkos et al. 2017; Krey et al. 2019), requiring substantial upfront financing. This puts the cost of capital centre stage in computing and projecting future levelized costs of electricity (LCOE) and electricity prices that in turn drive the diffusion of said technologies in energy markets. The empirical evidence shows that these LCOE can differ widely across technologies and countries (Steffen 2020; Duffy et al. 2020) and change significantly over time, also because of changing costs of capital (Egli et al. 2018; Egli 2020).

Ondraczek et al. (2015), for example, stress the importance of the cost of capital as a determinant in the cost of solar power and argue this has been overlooked in global assessments of the cost of solar photovoltaic (PV). The authors then used differentiated WACCs to determine the discount rate in the LCOE for every country in their sample. These WACCs were shown to differ by as much as a factor 8 between countries, with the lowest values in developed countries such as Japan, the UK and the Netherlands and the highest values in emerging and developing countries such as Brazil and Madagascar. The authors found that the variation in costs of capital is more important for investment decisions in solar PV than the variation in the quality of solar resources and that differences are driven by interest rates, debt shares and systemic risk.

A similar argument can be made against assuming stable WACCs over time. In addition to time-varying interest rate levels, risk (or risk perception) is an important driver in the cost of capital. As low-carbon technologies require more upfront investment than high-carbon technologies, de-risking will benefit the former more and can be a strong driver for accelerating the deployment of clean energy technologies (Schmidt 2014; Schinko and Komendantova 2016; Komendantova et al. 2019). Differentiated WACCs per technology, country and over time can also emerge because of heterogeneity on the finance supply side. Best (2017) examined whether a country’s stock of financial capital (credit to the private sector by banks and outstanding private debt securities) affects its ability to support the energy transition. The author then argues that on the one hand, competition between capital providers helps to lower the cost of capital when there is a large supply. On the other hand, if there is a shortage of financial capital, then certain energy projects may not be economically viable due to high cost of capital. The author finds that across countries, the availability of financial capital contributes to investments in more capital-intensive energy technologies (i.e. technologies with a higher share of capital costs in total lifecycle costs). For lower-income (developing) countries, financial capital contributes to the transition from (traditional) biomass towards fossil fuels. For high-income countries, financial capital supports transitions towards more capital-intensive energy technologies such as wind energy.

Taken together, we conclude from the scientific evidence that WACCs for energy investments in renewables or fossil fuel–based technologies are important drivers of investment decisions. Moreover, it is a fact that WACCs differ across countries, between technologies and over time. This fact, however, has not yet changed the way most energy-economy system models treat financial markets. Very few models take a consistent perspective and use differentiated costs of capital at the level of technologies, countries and/or regions (Hirth and Steckel 2016; Paroussos et al. 2019b; Bachner et al. 2019). In line with traditional economic modelling, financial markets are typically assumed to be highly integrated, such that capital is assumed to be globally available at a uniform market rate of return. Consequently, there is no comprehensive and transparent treatment of investment and technology risks in the available economy-energy models (e.g. Bogdanov et al. 2019b; Krey et al. 2019).

In a recent paper, Egli et al. (2019) stressed the need to include differentiated WACC assumptions by country and technology to improve the understanding of energy transition pathways (see also Bachner et al. 2019). Egli et al. (2019) argue that using a uniform cost of capital across countries in energy transition modelling can lead to distorted policy recommendations. They show that the cost of capital is substantially lower in industrialized countries and thus the LCOE of solar PV is substantially lower in those countries compared to low-income countries (despite the higher solar radiation, technology efficiency and hence potential in these countries). The authors conclude that energy system models that compare countries—and particularly countries across different income and investment risk classes—should use country-specific (and technology-specific) costs of capital. In their reply, Bogdanov et al. (2019a) agree that the representation of costs of capital in energy system models should be improved.

There is a small and emerging body of literature presenting model-based evidence on the role of WACCs in the transition towards a future electricity mix. Hirth and Steckel (2016), for example, use the power market model EMMA to examine the role of both carbon taxes and cost of capital in the development of the electricity mix. Their paper focuses on emerging economies, which are characterized by high cost of capital, and they project that only a combination of carbon pricing and low cost of capital leads to a significant share of renewables in energy supply. Bachner et al. (2019) investigated determinants of the WACCs in Europe’s electricity sector, building on a computable general equilibrium (CGE) model coupled with electricity modelling (WEGDYN). They concluded that empirically more realistic differentiated cost of capital for different renewable electricity technologies show positive effects on the macroeconomic level and that uniform WACC assumptions in energy models introduce significant biases in the results. Paroussos et al. (2019a) used the CGE model GEM-E3 with differentiated assumptions on interest rates and concluded that the Italian economy can benefit from the low-carbon transition in cases where Italian firms and households have access to low-cost financial resources. These papers show the relevance of WACCs, but fall short of introducing WACCs that differ over time, space and technology in a systematic and comprehensive way.

3 Methods and data

In this section, we describe the methodology we used to assemble the country-specific WACCs for European countries for a range of fossil fuel (oil, gas, nuclear) and renewable power technologies (hydro, solar PV, wind onshore and offshore, biomass).Footnote 2

3.1 Estimating WACC for energy technologies

To derive reasonable assumptions for the cost of capital of different power generation technologies, an important differentiation must be made between the financing structures used for different technologies. In industrialized countries, most fossil fuel-based power plants (which are dispatchable) are being operated on a merchant basis, selling their electricity to the wholesale market, and as such have been realized on the balance sheet of utilities (IEA 2016; Diaz-Rainey and Premachandra 2017; Helms et al. 2020; Steffen 2020). Hence, the cost of capital for thermal and hydro power plants is determined by the WACC of utilities (Cambini and Rondi 2010; Helms et al. 2020). Historically, the same is true for hydro power plants. The majority of non-hydro renewable energy plants (which are not dispatchable) are operated on the basis of a contractually or legally fixed price per unit of electricity produced (e.g. in the form of a feed-in tariff, feed-in premium or a long-term power purchase agreement allocated in renewable energy auctions) and are realized on the balance sheet of non-recourse special purpose vehicles, financed through project finance (Henderson 2016; OECD 2016; Steffen 2018). Hence, the cost of capital for renewable energy plants is determined on the level of individual projects (Steffen 2020). While in reality not all thermal and hydro plants exclusively rely on corporate finance and not all renewable energy plants exclusively rely on project finance, we believe that the differentiation is a reasonable approach to estimate WACCs for different technologies based on available data. A more nuanced approach with respect to financing structures by technology and country is an area for further research.

3.1.1 WACCs for utility power plants

To calculate a country-specific and technology-specific average utility WACC, we carried out the following steps: First, we collected financial data for a representative sample of European utility companies from Thomson Reuters Eikon (STOXX Europe 600 Utilities index), which includes these firms’ financial data on balance sheets, income statements and cash flow statements. Second, we followed Kling et al. (2021) in calculating the overall WACC per utility i for the years t = {2009, …, 2018}:

where Lit denotes the leverage ratio (total debt over total capital) for utility i in year t. We measure the cost of debt, rD, by using interest expense of utility i in year t divided by total debt reported for that period:

To obtain firm-level proxies for the cost of equity, rEit, we rely on dividend payments relative to the value of equity for utility i in year t:

Third, we calculated the country-utility WACC by weighing each overall utility WACC by their respective country exposure using the country share of utilities’ revenue:

where \( {s}_{it}^c \) is the share of sales in country c for utility i in year t. If the utility’s WACC was missing for a given year, it was replaced with the WACC from the previous year. This resulted in 110 country-year observations based on 29 utilities active in 13 European countries. These WACCs include the risk-free rate, rf, a premium for country and policy risk, pc, and for market and technology risk, pT, as well as a residual of company-specific risks that we may assume is random.

where we consider the technology risk premium, pT, a weighted average of technology-specific risk premia multiplied by the share of that technology in a country’s (utility) generation mix. To estimate the overall utility WACC as well as technology-specific utility WACCs for the remaining EU countries, we used the following procedure: From the country-specific utility WACCs, we first subtracted the long-term government bond rate to eliminate the risk-free rate and country risk component, rft + pc. We then ran a simple ordinary least square (OLS) regression (without a constant because the shares add up to 1) with WACC cleaned of country risk as the dependent variable and the share of generation per source per country as our independent variables (Eurostat 2020a):

where share of coal, gas, nuclear, hydro and other renewables represent the share of these technologies in country c’s power generation mix (expressed in GWh) at time t (taken from the Eurostat database). The estimated coefficients (included in the online appendix) now represent the average % point additional financing cost for utilities per 1% point increase of the share of that source in the country’s electricity mix. An estimated coefficient of 0.05 for example would imply that the WACC of a utility increases by 0.05% or 5 basis points for every 1% point increase in the share of that technology in its portfolio (in country c). The obtained values for coal (0,051***), nuclear (0,049***) and hydro (0,035***) are in the range of other earlier empirical calculations (Ecofys 2014) and model assumptions (Bachner et al. 2019). Gas plants (0,010 but insignificantly different from 0) are a lot cheaper than in other studiesFootnote 3. Our predicted utility WACCs per technology and country (see Table 1) then represent the WACC for a hypothetical case in which a utility invests in a technology in a country that produces all power with that technology.

3.1.2 Project-level WACCs for non-hydro renewable energy technologies

For project-financed assets, it is not possible to derive the cost of capital directly from financial market data. Financing is typically provided via bank loans and equity investment, for which the conditions are typically not disclosed (Krupa and Harvey 2017; Steffen 2020). Steffen (2020) surveys a number of methods that have been proposed to estimate cost of capital values for the purpose of model calibration, drawing on deal data, expert surveys, the replication of auction results and financial market data as a proxy for untraded assets. Particularly for wind onshore, the coverage is very good (data for 26 out of 28 countries), whereas less data is available for offshore wind (only 5 out of 23 countries that border the sea) and for solar PV (data for Germany and Greece). Hence, we start with data available from Steffen (2020) and impute missing values following an approach proposed in that paper, using the average technology markup between solar PV, wind onshore and wind offshore from OECD countries. This seems reasonable, as technology differences in cost of capital appear quite stable across countries (Steffen 2020). Finally, we had to derive values for those countries for which not a single technology value was available, Malta and Luxembourg, which have very small renewable energy markets in the EU context but whose values are required for completeness of the WACC database. Using geographic and economic proximity as a heuristic, we assume that the cost of capital for Luxembourg is the average of the values from Belgium, Germany and France and that the cost of capital for Malta is the average of values from Italy and Cyprus. All resulting values are given in Table 1. The obtained values are slightly higher than earlier empirical calculations (Ecofys 2014) and model assumptions (Bachner et al. 2019) potentially better reflecting market and policy risks in the different countries.

3.2 Financing experience

Research has shown that financing conditions for renewable energy technologies are dynamic (Egli et al. 2018, 2019; Egli 2020; Steffen 2020). Specifically, Egli et al. (2018) have identified an experience effect among renewable energy debt providers: They measured improving financing conditions as debt providers (e.g. banks) learned and became acquainted with novel technologies. Additionally, changing policies and the penetration of renewable technologies may also change the (perceived) risk inherent in traditional power production technologies over time (e.g. stranded assets and clean-up costs).

Here, we operationalize the concept of “financing experience” by calculating a hypothetical experience rate on the full cost of capital and introduce dynamics in the WACCs for onshore wind, offshore wind and solar PV by implementing this experience rate into the GEM-E3-Power model. We assume that experience only happens on the debt margin, as shown in Egli et al. (2018). This is a conservative approach for two reasons. First, on the equity side, margins may decrease with increasing technology data, better assessment models and increasing investor competition. Given the lack of data, however, we exclude such effects in our approach. Second, as financing markets for these technologies become more mature, projects are typically able to attract higher debt shares, resulting in higher leverage. As the cost of debt is commonly lower than the cost of equity (because the risk to equity holders is greater than the risk to debt lenders), assuming a constant leverage over time is again a conservative choice.Footnote 4 We decompose the after-tax WACC according to the standard formula:

where DT, avg indicates the average cost of debt for technology, T; mTt is the debt margin; τavg is the tax rate; LT, avg is the leverage ratio; and ET, avg is the cost of equity. As the starting year of the data is 2015, we use 3-year averages (2014–2016) for the time-invariant components (D, τ, L, E) and estimated debt margins for each year from 2000 to 2015, as in Egli et al. (2018). The resulting WACC by technology T and year t is a number to identify the effect of debt margin decline on the overall WACC. We use a classic experience curve, where the cost of capital decreases by a constant percentage, bT, for each doubling of cumulative technology deployment (Rubin et al. 2015):

Solving our equation for bT, we get

We populate Eq. (9) with historic solar PV and onshore wind deployment and the costs of capital from 2000 to 2015 to calculate the experience parameter bT. Finally, the financing experience rate (ER) on the overall cost of capital is given by Eq. (10):

We then use the parameters bT to model future cost of capital developments for each country dependent on domestic deployment YTt. Contrary to the estimated experience rate in Egli et al. (2018), this approach operationalizes financing experience with respect to cumulative technology deployment (i.e. MW) instead of investment (i.e. USD). For onshore wind and solar PV, increases in cumulative installed capacity are moderate, whereas increases may be larger for offshore wind in some countries. In line with this, technology cost reductions (costs per MW) may be more pronounced for offshore wind and our operationalization may slightly overestimate cost of capital decreases for offshore wind. Furthermore, this approach operationalizes experience on a country level (with respect to domestic deployment) instead of globally as in Egli et al. (2018).Footnote 5 For onshore wind, the estimated learning rates range from 3.7% (global) to 5.7% (domestic), and for solar PV, they range from 4.6% (global) to 4.4% (domestic). For implementation in our model and to illustrate the principle, we chose 5% as the “financing experience rate” for onshore wind, offshore wind and solar PV technologies, which is close to the median across different deployment specifications. Choosing a uniform “financing experience rate” is a fair approximation in the context of Europe as the European RE financing market is highly internationalized and cross-border financing in very common (see e.g. data description in Egli et al. 2018).

3.3 Electricity system modelling

3.3.1 Model description

To illustrate the impact of using more realistic differentiated WACCs per country and technology over time, we use the GEM-E3-Power model (Capros et al. 2013). This model is a bottom-up, technologically rich electricity module describing the development of the power generation mix under alternative policy assumptions in the 2015–2050 period. The electricity module is hard-linked with the core GEM-E3 model, a multi-sectoral Computable General Equilibrium (CGE) that describes the complex interactions between the economy, the labour market, the energy system and the environment and has been extensively used in European Commission energy and climate policy impact assessments, including the Energy Roadmap 2050 (European Environment Agency 2011), Climate Package for 2030 (European Commission 2019) and the recent Clean Planet for All strategy (European Commission 2018). The hard link between the power model and GEM-E3 improves the representation of the electricity sector in conventional CGE models through constant elasticity of substitution (CES) functions, by integrating explicit bottom-up modelling of power generation technologies. Here, we use the GEM-E3-Power as a stand-alone modelling tool without linking it to the CGE model, covering the 28 EU member states separately (as well as all G20 economies).

The GEM-E3-Power model simulates a competitive wholesale electricity market subject to various constraints (i.e. on technology limitations, fuel potentials, storage, grids and systems) and calculates investment in new power plants, which are influenced by sectoral electricity demand, load duration curves, decommissioning of old and inefficient power plants (normal and accelerated) and the already decided investment and policy measures. Electricity demand is set exogenously and is derived from the official Reference scenario used by the European Commission (Capros et al. 2016). The model decides on the optimal investment and operation of the electricity system in order to minimize intertemporal total costs to produce electricity, including capital expenditures (CAPEX), operation and maintenance (O&M) expenditures, carbon costs and costs to purchase fuels (used as inputs to power plants), while meeting system constraints in each time segment (e.g. electricity demand, technology potentials, system reliability and flexibility, power trade, resource availability, storage and policy constraints). Thirteen power generation options are included in the model (coal, oil, gas- and biomass-fired, nuclear, hydro, PV, wind onshore, wind offshore, geothermal, carbon capture and storage (CCS) coal, CCS gas and CCS biomass) and compete based on LCOE to meet the electricity requirements in each year and time segment. The WACC assumptions influence the decision to invest in different power supply technologies, as, for example, high WACC values negatively impact the competitiveness of capital-intensive technologies like PV and wind. The model can represent various policy instruments that influence the development of the power system in each country, such as emission trading scheme (ETS) carbon prices, phase-out policies (for coal and nuclear), renewable subsidies or feed-in-tariffs and technology standards.

The modelling includes non-linear cost-supply curves for fossil fuels, nuclear plants and renewable technologies. These are numerical functions with increasing slopes serving to capture exhaustion of renewable energy potential (e.g. for solar PV, wind and hydro plants), take-or-pay contracts for fuels, the possible promotion of domestically produced fuels, fuel supply response (increasing prices) to increased fuel demand by the power sector, difficulties in developing CO2 storage areas, acceptability and policies regarding nuclear site development. The non-linear cost-supply curves are fully included in the optimization of capacity expansion and operation of the electricity system in the GEM-E3-Power model.

In line with empirical findings and state-of-the-art in energy-economy modelling, GEM-E3-Power incorporates endogenous technological progress (especially for low-carbon technologies like wind and PV), through learning-by-doing curves that define the reduction in technology costs gained through cumulative capacity installations reflecting learning from experience and economies of scale in production (Krey et al. 2019; IEA 2020). The learning rates derive from extensive literature review and are presented in Paroussos et al. (2019b). The integration of endogenous technological progress, grounded in empirical analysis, enables the improved representation of cost reductions for low-carbon technologies by 2050.

All the above elements included in GEM-E3-Power (e.g. cost-supply curves, reliability, technology and flexibility constraints, endogenous technological progress, electricity storage) provide an improved representation of the capacity expansion and operation of the electricity system, capturing its specificities, constraints and technology dynamics. The model is also enhanced with the innovative feature of a “financing experience” curve in order to endogenously capture the complex interlinkages between technology deployment, system investment and financial learning (as presented in Section 3.2). In future extensions, similar dynamics in utility WACCs might be explored for fossil fuel-based technologies facing increasing risks in the transition. To avoid confounding these different effects, we abstract from such dynamics here.

3.3.2 Scenario descriptions

A series of specifications are considered to assess the impact of alternative WACC assumptions on electricity system development, technology uptake and electricity costs in EU countries. These different WACC specifications are analysed for two stylized scenarios that reflect different levels of climate policy ambition. In the “Reference” scenario, ETS and other climate policies (i.e. Energy Efficiency Directive, measures to support renewable energy sources [RES] expansion, nuclear-related limitations) continue to 2050 in line with current legislation (Capros et al. 2016) (Ref). In the “Ambitious Decarbonization” scenario, climate policies’ stringency increases to meet the EU long-term mitigation goals with emissions reductions of 85–95% by 2050 from 1990 levels (European Commission 2018) (Amb). In both scenarios, ETS prices are the primary policy lever towards electricity sector decarbonization, as they incentivize the uptake of low and zero-carbon technologies. With ambitious climate policies, ETS prices increase gradually to 333€/tnCO2 in 2050 (in line with European Commission, 2018), while in the Reference scenario they rise to about 89€/tnCO2 in 2050 (see Figure 1). The Ambitious Decarbonization scenario requires a rapid increase in ETS price in the period by 2035 to incentivize the massive upscaling of low-carbon technologies; in the longer term, technology learning leads to increased competitiveness of RES technologies without the need for stronger ETS price signals.

Evolution of ETS carbon price in Reference and Ambitious Decarbonization scenarios (€/tnCO2)

Concerning alternative WACC assumptions, three specifications are considered. The first is based on the current/default model setting without differentiation in WACCs, using a uniform WACC value of 8.5% for all countries and technologies, as in leading energy-economy models (IEA 2020) (UNI). In the second specification, the differentiated WACC values as calculated in Section 3.1 are used in the GEM-E3-Power model for specific countries and technologiesFootnote 6 and are allowed to influence investment decisions (DIFF). The last specification aims to explore the role of financing experience in technology uptake and costs by explicitly integrating financing experience curves for PV, wind onshore and offshore in GEM-E3-Power (DIFF+FE). In this specification, country WACCs for these technologies are assumed to decline over time induced by higher cumulative deployment as described in Section 3.2.

4 Results

4.1 Impacts on technology uptake and investment decisions

Our scenario results show that differentiated WACC assumptions have large impacts on investment decisions and technology uptake both in the medium and in the long term. The implications differ by country and depend highly on the WACC values for power generation technologies and mostly for solar PV and wind, which account for most of the EU’s electricity investment. As expected, the impacts are more pronounced in countries that have very divergent WACC values relative to the uniform benchmark. Below, we discuss the impacts of using differentiated WACCs in the Reference scenario for the EU overall and for two specific countries, Germany and Greece, where country risk premia deviate the most and WACC estimates are based on a broad empirical basis (see Section 3.3.2).

At the EU28 level, we observe that the switch from uniform to differentiated WACCs leads to lower future shares of fossil fuel-based plants and higher shares of renewables in both the Reference and the Ambitious Decarbonization scenarios. In the Reference scenario, the uptake of RES is higher in the differentiated WACC case, with the RES share increasing to 45% in 2030 and 66% in 2050 (relative to 40% and 61%, respectively, in the uniform WACC case). This effect is mainly driven by a substitution of gas capacity by more solar PV and wind power plants. WACC values for PV and wind onshore are lower on average (and in most European countries) than the default WACC value of 8.5%. While gas-fired power plants have even lower WACCs in most EU countries, the impact of a lower WACC is larger for the more capital-intensive clean energy technologies. An exception is 2050 in the Ambitious Decarbonization scenario, which has almost zero fossil fuel capacity (without CCS) across all specifications. There the differentiated WACCs lead to a substitution of offshore wind with solar PV. Introducing financing experience affects all RES WACCs similarly and therefore only has a modest effect on the technology mix.

Concerning Germany, its electricity mix is set for a rapid transformation away from coal and nuclear combined with a massive uptake of wind and PV (coupled with gas in the Reference simulations). As the country has very low WACCs for most power generation technologies, reflecting its credible policy and financial environment with limited risks (Egli et al. 2018), the deployment of capital-intensive options accelerates when WACCs are differentiated (Figure 2). This means a faster uptake of solar PV and wind onshore, combined with a reduced contribution of gas, which is characterized by lower CAPEX and high operation and fuel costs. The effect is more pronounced in the Reference scenario compared to the Ambitious Decarbonization scenario.

Electricity generation shares by technology for all EU-28 countries, Germany and Greece

Concerning Greece, the electricity sector is in the middle of a transition towards renewable energy but is hindered by the high (perceived) risks and WACCs facing new investment. The recent Greek policy plans to phase out lignite-based electricity production is reflected in the Reference case, which shows a rapid reduction of carbon-intensive generation (lignite and oil) and increased contribution of natural gas, solar PV and wind. The very high WACC values (see Angelopoulos et al. (2017) for a detailed analysis of the causes) negatively impact the competitiveness of capital-intensive low-carbon options (like wind and PV) and thus in the Reference scenario the share of renewable energy in 2050 is lower with differentiated WACCs (72% compared to 85%). On the other hand, gas deployment is higher to meet electricity requirements, implying a large role for gas as the “bridging” fuel.

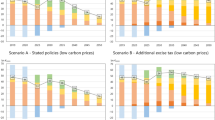

Generally, the impacts of using differentiated WACCs are more pronounced in the Reference case, as the high ETS carbon prices imposed in the decarbonization context have a huge impact on relative technology competitiveness and constrain the portfolio of competitive technologies. As observed in Figure 3, this is a robust finding for all EU countries. In countries with low WACC values (i.e. Germany, Luxembourg, Belgium, Austria, Denmark, the UK and Italy), the shares of renewable energy are higher in both the Reference scenario and the Ambitious Decarbonization scenario. In contrast, RES competitiveness and uptake are lower in countries with high WACC values, including Greece, Ireland, Bulgaria, Croatia and Romania. GEM-E3-Power shows that other capital-intensive technologies may also benefit in the differentiated WACC context in cases in which they have lower WACCs than RES (i.e. nuclear in Finland and Hungary or gas-fired CCS in the Netherlands). The inter-substitution among RES is mostly driven by the relatively lower WACCs of PV relative to wind onshore and offshore in most EU countries.

Difference in renewable energy share between DIFF+FE and UNI by country in 2030 shown for the Reference scenario and the Ambitious Decarbonization scenario. Reading example: +15% means that the RE share is 15% higher in a given country in 2030 when using differentiated costs of capital including financing learning compared to uniform costs of capital

4.2 Impacts on emissions and electricity costs

As shown, WACC assumptions change the technology portfolios. Consequently, they will also have an impact on both CO2 emissions and electricity costs. Countries with low WACC values for low-carbon technologies show more rapid reduction of emissions and more moderate electricity system costs as the uptake of RES accelerates.

First, with respect to emissions, Figure 4 shows that the impact of using differentiated WACCs (including financing experience) is more pronounced in the Reference case, with 15% lower EU electricity-related CO2 emissions in 2030 (24% in 2050) relative to the uniform WACC scenario (i.e. around 65–110 Mt lower). Most of this reduction comes from large-emitting economies with low WACC values for PV and wind (i.e. Germany, the UK, Italy, the Netherlands, Portugal, Belgium and Austria); in contrast, emissions are higher in countries where WACCs for low-carbon technologies are high (i.e. Ireland, Greece and Portugal). While the overall emission impact of differentiated WACCs is very low in the Ambitious Decarbonization scenario, there are nonetheless important spatial/country effects with lower emissions in lower-risk countries such as France, Germany or the UK and substantially higher emissions in higher-risk countries such as Greece and Spain.

Electricity-related CO2 emissions and costs (excluding T&D) for EU-28. Panels on the left show the evolution over time. Maps on the right display percentage differences by country in 2050 from DIFF+FE to UNI for the Reference scenario (middle) and the Ambitious Decarbonization scenario (right). Reading example for the maps: −20% means that the CO2 emissions (or costs) are 20% lower for a given country in 2050 when using differentiated costs of capital including financing learning compared to uniform costs of capital

Second, with respect to electricity system costs (which include the costs for storage), Figure 4 shows the same inverse-U pattern across time for all specifications and scenarios. The introduction of high ETS prices would drive a restructuring of the electricity sector, induced by increased uptake of low and zero-carbon technologies (mostly solar PV and wind). In the Ambitious Decarbonization scenario, investment requirements and system CAPEX would increase (despite RES technology progress), but O&M and fuel costs are lower compared to Reference levels due to the rapid phase-out of fossil fuel–fired power plants. Overall, the cost impacts of decarbonization are relatively modest in most EU countries, with only limited exceptions in countries that have low potential for key mitigation options like wind and PV.

The cost impacts of using differentiated WACCs (including financing experience) are similar across both scenarios (both relative and absolute). As in most countries, average WACCs are lower relative to the uniform value of 8.5%, and electricity system costs tend to be lower both in the Reference and in the Ambitious Decarbonization context. Electricity system costs are on average 0.011 €/KWh and 0.012 €/KWh lower, respectively. In 2018, the EU net electricity generation totalled 2806 TWh (Eurostat 2020b). Assuming the more realistic differentiated costs of capital would thus mean a cost reduction at the EU level of €30.87 billion and €33.67 billion per annum until 2050, respectively. Moreover, spatial patterns are also similar across both scenarios: With the exception of Greece, all countries either encounter substantially lower or roughly similar costs when accounting for WACC differences. The reduction is particularly large in lower-risk countries (e.g. Germany, Belgium, the Netherlands).

The integration of financing experience curves in the model leads to a further reduction in electricity system costs, especially in countries that show a large reduction in WACCs due to high-capacity growth over the 2020–2050 period. At the EU level (Figure 4), financing experience leads to an additional reduction of average power generation costs by 3.5% in 2050 in the Ambitious Decarbonization scenario with differentiated WACCs. This cancels out about 15% of the cost increases induced by ambitious decarbonization policies, bringing the average electricity generation costs closer to the Reference scenario levels.

5 Discussion and conclusions

To date, energy and electricity system models as well as more extensive general equilibrium and integrated assessment models are used intensively to guide Europe’s Green Deal and energy transitions in Europe and beyond. These models show that a near-zero emission energy system is feasible in Europe, and although massive investment by public and private sectors is required to achieve the ambitious policy targets, the transition also seems economically feasible (Fragkos and Kouvaritakis 2018; Zappa et al. 2019; European Commission 2020b). These projections, however, rest on simplifying assumptions on financial markets (Egli et al. 2019). Many models assume that the costs of capital are uniform across countries and technologies and over time (Bogdanov et al. 2019b; IEA 2020). In this paper, we have shown that this assumption finds little support in the data, and more importantly, relaxing it changes model-based projections significantly.

When we allow for country-level differences in the cost of capital, the cross-country variation, even in such an integrated market as the European Union, can drive the allocation of capital away from a cost-effective energy transition pathway. Capital-intensive renewables in particular tend to cluster in low-risk countries (Bachner et al. 2019). For wind power, this may coincide well with the physical availability of wind resources, but for solar PV, this clearly is not the case, as some southern EU countries with favourable PV potentials tend to face high country risks and consequently high WACCs (e.g. Greece) (Steffen 2020).

Our paper has important policy implications. First and foremost, it should serve as a caveat to policymakers taking model simulations as accurate and precise projections of the impact of their policies; the projections in a model simulation are only as relevant and accurate as the assumptions underlying the model. When model outcomes prove very sensitive to alternative (and more realistic) assumptions, as we have shown in this paper they do, then caution is warranted. Assuming a uniform WACC for all countries or technologies will lead to under- and/or overestimation of both the speed and costs of transition (as shown in Figure 4) as well as to sub-optimal investment decisions for energy technologies and policies. Thus, the integration of WACCs differentiated by country and technology in energy-economy system models will improve their representation of investment decisions and ensure consistency with real-world data and observations.

The simulations in this paper also bring into focus new policy levers. Our simulations show that differentiated WACCs are likely to lower the overall costs of the low-carbon transition in the EU. Hence, countries with lower WACCs can opt for a more rapid and ambitious transition than expected without incurring higher costs, reducing the overall emissions faster. Moreover, financial experience contributes to lowering transition costs in all countries. However, the costs of capital for different technologies in different countries of the EU remain very sensitive to fiscal and financial regulations set directly and indirectly by policymakers at the national and EU level.

Implementing policies that cause WACCs for renewable energy production to converge to the lowest levels in the EU, especially for projects in member states with ample underdeveloped renewable energy resources, can give the energy transition a boost at relatively low costs. As long as country risk determines (to a large extent) where renewable energy is penetrating fastest, a policy that would make such premia converge is an effective tool to promote a more efficient transition. As part of its Green Deal, Europe might therefore consider setting up a system to equalize WACCs for RES across the European Union by pooling the risks (Agora Energiewende 2018). Similarly, the financing experience effects can be considered positive externalities (as e.g. technology learning) that the entire market benefits from but that private investors have no incentive to finance. This could justify policies that foster data exchange among investors or provide an important co-benefit to policies that increase deployment (e.g. public (co-)investments; see Deleidi et al. 2020) as investment experience reduces WACCs through lower risk premia.

Given the capital intensity of renewable energy production, we claim that such policies can be efficient and complement energy and climate policies relying on carbon pricing, carbon taxes and outright subsidies for renewable production per MWh that aim to make renewable energy competitive on LCOE terms. The cost structure of most renewables implies that their competitiveness is strongly affected by the cost of capital. Policymakers can directly affect this key driver through institutions like the European Investment Bank, and thereby affect private investment decisions in the energy sector.

The analysis in this paper also opens up avenues for future research. First, one could implement WACCs in more complex and sophisticated models, capturing the interlinkages between the energy transition and the macro-economy (including the links between the financial sector and the real economy). In particular, the differentiation of WACCs in leading energy-economy and integrated assessment models will significantly improve their real-world relevance and the accuracy of their projections on cost-optimal allocation of low-carbon investment to different technologies, sectors and regions (such as energy efficiency investment in the built environment and decarbonization of transport). Second, the WACC estimations introduced here could be further improved and extended, for example by applying the method to non-EU countries, which will potentially show larger influence (e.g. in low-income countries that have very high WACCs). There is, of course, no substitute for collecting more and better data on WACCs, and we also believe our estimation methods merit further scrutiny and should not be taken at face value. Third, this paper focuses on power sector technologies only. In future work, scholars should also estimate costs of capital and endogenize financial experience curves for other low-carbon technologies that are important for the transition (i.e. electric vehicles, batteries, heat pumps, biofuels and green hydrogen).

Notes

We use WACC and cost of capital interchangeably throughout this paper.

Data and code can be made available upon reasonable request.

We see that gas in particular has low average risk premia, which can be explained by the fact that costs for gas plants are largely OPEX driven, and gas is considered a “bridge” option towards low-carbon transition and does not involve high risks for stranded assets (like coal or nuclear).

However, one has to note that we use the leverage from German projects (2014–2016), which is rather high. Hence, the cost of debt is comparatively more important in determining the cost of capital than the cost of equity, and changes in the debt margin are therefore more important.

Note that Egli et al. (2018) show that the estimated experience rates on debt margins are robust to using European instead of global investment figures.

In this scenario, WACC values are kept frozen until 2050 at their 2015 levels. The only exception is Greece, where some adjustments are implemented, to reflect the recent reduction in risk premia and WACCs in the last 4 years following the recovery of the Greek economy.

References

Agora Energiewende (2018) Reducing the cost of financing renewables in Europe. Agora Energiewende, Berlin, Germany

Angelopoulos D, Doukas H, Psarras J, Stamtsis G (2017) Risk-based analysis and policy implications for renewable energy investments in Greece. Energy Policy 105:512–523. https://doi.org/10.1016/j.enpol.2017.02.048

Bachner G, Mayer J, Steininger KW (2019) Costs or benefits? Assessing the economy-wide effects of the electricity sector’s low carbon transition – the role of capital costs, divergent risk perceptions and premiums. Energy Strateg Rev 26:100373. https://doi.org/10.1016/j.esr.2019.100373

Best R (2017) Switching towards coal or renewable energy? The effects of financial capital on energy transitions. Energy Econ 63:75–83. https://doi.org/10.1016/j.eneco.2017.01.019

Bogdanov D, Child M, Breyer C (2019a) Reply to ‘Bias in energy system models with uniform cost of capital assumption’. Nat Commun 10:1–2. https://doi.org/10.1038/s41467-019-12469-y

Bogdanov D, Farfan J, Sadovskaia K et al (2019b) Radical transformation pathway towards sustainable electricity via evolutionary steps. Nat Commun 10:1–16. https://doi.org/10.1038/s41467-019-08855-1

Cambini C, Rondi L (2010) Incentive regulation and investment: evidence from European energy utilities. J Regul Econ 38:1–26. https://doi.org/10.1007/s11149-009-9111-6

Capros P, De Vita A, Tasios N, et al (2016) EU Reference Scenario 2016 - energy, transport and GHG emissions Trends to 2050. https://ec.europa.eu/energy/sites/ener/files/documents/REF2016_report_FINAL-web.pdf . Accessed 23 Jun 2020

Capros P, Van Regemorter D, Paroussos L et al (2013) GEM-E3 model documentation. JRC Scientific and Policy Reports 26034

Deleidi M, Mazzucato M, Semieniuk G (2020) Neither crowding in nor out: public direct investment mobilising private investment into renewable electricity projects. Energy Policy 111195. https://doi.org/10.1016/j.enpol.2019.111195

Diaz-Rainey DJTI, Premachandra IM (2017) The impact of liberalization and environmental policy on the financial returns of European Energy Utilities. EJ 38. https://doi.org/10.5547/01956574.38.2.dtul

Duffy A, Hand M, Wiser R et al (2020) Land-based wind energy cost trends in Germany, Denmark, Ireland, Norway, Sweden and the United States. Appl Energy 277:114777. https://doi.org/10.1016/j.apenergy.2020.114777

Ecofys (2014) Subsidies and costs of EU energy Final report. European Commission, Brussels

Egli F (2020) Renewable energy investment risk: an investigation of changes over time and the underlying drivers. Energy Policy 140:111428. https://doi.org/10.1016/j.enpol.2020.111428

Egli F, Steffen B, Schmidt TS (2018) A dynamic analysis of financing conditions for renewable energy technologies. Nat Energy 3:1084–1092. https://doi.org/10.1038/s41560-018-0277-y

Egli F, Steffen B, Schmidt TS (2019) Bias in energy system models with uniform cost of capital assumption. Nat Commun 10:1–3. https://doi.org/10.1038/s41467-019-12468-z

European Commission (2018) In-depth analysis in support on the COM(2018) 773: a Clean Planet for all - European strategic long-term vision a prosperous, modern, competitive and climate neutral economy. In: Knowledge for policy - European Commission. https://ec.europa.eu/knowledge4policy/publication/depth-analysis-support-com2018-773-clean-planet-all-european-strategic-long-term-vision_en. Accessed 23 Jun 2020

European Commission (2020a) Financing the green transition: the European green deal investment plan and just transition mechanism. https://ec.europa.eu/commission/presscorner/detail/en/ip_20_17

European Commission (2019) EUCO scenarios. Energy - European Commission. https://ec.europa.eu/energy/data-analysis/energymodelling/euco-scenarios_en.

European Commission (2020b) Proposal for a regulation of the European parliament and of the council establishing the framework for achieving climate neutrality and amending Regulation (EU) 2018/1999 (European Climate Law), Brussels

European Environment Agency (2011) A roadmap for moving to a competitive low carbon economy in 2050. European Environment Agency, Brussels

Eurostat (2020a) Energy data. https://ec.europa.eu/eurostat/web/energy/data/database. Accessed 4 Aug 2020

Eurostat (2020b) Electricity production, consumption and market overview - statistics explained. https://ec.europa.eu/eurostat/statisticsexplained/index.php/Electricity_production,_consumption_and_market_overview. Accessed 4 Aug 2020

Fragkos P, Kouvaritakis N (2018) Model-based analysis of intended nationally determined contributions and 2 °C pathways for major economies. Energy 160:965–978. https://doi.org/10.1016/j.energy.2018.07.030

Fragkos P, Tasios N, Paroussos L et al (2017) Energy system impacts and policy implications of the European Intended Nationally Determined Contribution and low-carbon pathway to 2050. Energy Policy 100:216–226. https://doi.org/10.1016/j.enpol.2016.10.023

Gupta S, Harnisch J, Barua DC et al (2014) Chapter 16 - Cross-cutting investment and finance issues. In: Climate change 2014: Mitigation of climate change. IPCC Working Group III Contribution to AR5. Cambridge University Press

Hansen G, Eckstein D, Weischer L, Bals C (2017) Shifting the trillions. Germanwatch, Bonn

Helms T, Salm S, Wüstenhagen R (2020) Investor-specific cost of capital and renewable energy investment decisions. In: Donovan CW (ed) Renewable Energy Finance: Funding The Future Of Energy. World Scientific, Second Edition, pp 85–111

Henderson M (2016) Financing renewable energy. In: Morrison R (ed) The Principles of Project Finance. Routledge, New York, pp 163–182

Hirth L, Steckel JC (2016) The role of capital costs in decarbonizing the electricity sector. Environ Res Lett 11:114010. https://doi.org/10.1088/1748-9326/11/11/114010

IEA (2020) World energy model documentation. International Energy Agency, Paris

IEA (2016) World Energy Investment:2016

Iyer GC, Clarke LE, Edmonds JA et al (2015) Improved representation of investment decisions in assessments of CO 2 mitigation. Nat Clim Chang 5:436–440. https://doi.org/10.1038/nclimate2553

Jacobson MZ, Delucchi MA, Cameron MA, Mathiesen BV (2018) Matching demand with supply at low cost in 139 countries among 20 world regions with 100% intermittent wind, water, and sunlight (WWS) for all purposes. Renew Energy. https://doi.org/10.1016/j.renene.2018.02.009

Kling G, Volz U, Murinde V, Ayas S (2021) The impact of climate vulnerability on firms’ cost of capital and access to finance. World Dev 137:105131. https://doi.org/10.1016/j.worlddev.2020.105131

Komendantova N, Schinko T, Patt A (2019) De-risking policies as a substantial determinant of climate change mitigation costs in developing countries: case study of the Middle East and North African region. Energy Policy 127:404–411. https://doi.org/10.1016/j.enpol.2018.12.023

Krey V, Guo F, Kolp P et al (2019) Looking under the hood: a comparison of techno-economic assumptions across national and global integrated assessment models. Energy 172:1254–1267. https://doi.org/10.1016/j.energy.2018.12.131

Krupa J, Harvey LDD (2017) Renewable electricity finance in the United States: a state-of-the-art review. Energy 135:913–929. https://doi.org/10.1016/j.energy.2017.05.190

Luderer G, Bosetti V, Jakob M et al (2012) The economics of decarbonizing the energy system—results and insights from the RECIPE model intercomparison. Clim Chang 114:9–37. https://doi.org/10.1007/s10584-011-0105-x

Mazzucato M, Semieniuk G (2018) Financing renewable energy: who is financing what and why it matters. Technol Forecast Soc Chang 127:8–22. https://doi.org/10.1016/j.techfore.2017.05.021

McCollum DL, Nagai Y, Riahi K et al (2013) Energy investments under climate policy: a comparison of global models. Clim Change Econ 04:1340010–1340010. https://doi.org/10.1142/S2010007813400101

McCollum DL, Zhou W, Bertram C et al (2018) Energy investment needs for fulfilling the Paris Agreement and achieving the sustainable development goals. Nat Energy 3:589–599. https://doi.org/10.1038/s41560-018-0179-z

OECD (2016) OECD business and finance outlook 2016, Chapter 5: fragmentation in clean energy investment and financing. OECD, Paris

OECD/IEA and IRENA (2017) Perspectives for the Energy investment needs for a low-carbon energy system about the Iea

Ondraczek J, Komendantova N, Patt A (2015) WACC the dog: the effect of financing costs on the levelized cost of solar PV power. Renew Energy 75:888–898. https://doi.org/10.1016/j.renene.2014.10.053

Paroussos L, Fragkiadakis K, Fragkos P (2019a) Macro-economic analysis of green growth policies: the role of finance and technical progress in Italian green growth. Clim Chang. https://doi.org/10.1007/s10584-019-02543-1

Paroussos L, Mandel A, Fragkiadakis K et al (2019b) Climate clubs and the macro-economic benefits of international cooperation on climate policy. Nat Clim Chang 9:542–546. https://doi.org/10.1038/s41558-019-0501-1

Polzin F, Sanders M, Täube F (2017) A diverse and resilient financial system for investments in the energy transition. Curr Opin Environ Sustain 28:24–32. https://doi.org/10.1016/j.cosust.2017.07.004

Rubin ES, Azevedo IML, Jaramillo P, Yeh S (2015) A review of learning rates for electricity supply technologies. Energy Policy 86:198–218. https://doi.org/10.1016/j.enpol.2015.06.011

Schinko T, Komendantova N (2016) De-risking investment into concentrated solar power in North Africa: impacts on the costs of electricity generation. Renew Energy 92:262–272. https://doi.org/10.1016/j.renene.2016.02.009

Schmidt TS (2014) Low-carbon investment risks and de-risking. Nat Clim Chang 4:237–239. https://doi.org/10.1038/nclimate2112

Steckel JC, Jakob M, Flachsland C et al (2017) From climate finance toward sustainable development finance. Wiley Interdiscip Rev Clim Chang 8:e437. https://doi.org/10.1002/wcc.437

Steffen B (2020) Estimating the cost of capital for renewable energy projects. Energy Econ 88:104783. https://doi.org/10.1016/j.eneco.2020.104783

Steffen B (2018) The importance of project finance for renewable energy projects. Energy Econ 69:280–294. https://doi.org/10.1016/j.eneco.2017.11.006

Tietjen O, Pahle M, Fuss S (2016) Investment risks in power generation: a comparison of fossil fuel and renewable energy dominated markets. Energy Econ 58:174–185. https://doi.org/10.1016/j.eneco.2016.07.005

Zappa W, Junginger M, van den Broek M (2019) Is a 100% renewable European power system feasible by 2050? Appl Energy 233–234:1027–1050. https://doi.org/10.1016/j.apenergy.2018.08.109

Acknowledgements

This research was conducted as part of the EU’s Horizon 2020 research and innovation programme, project INNOPATHS (grant agreement No. 730403), and project GREENFIN (European Research Council, grant agreement No 948220). As part of the INNOPATHS project, it was partly supported by the Swiss State Secretariat for Education, Research and Innovation (SERI) under contract number 16.0222. The opinions expressed and arguments employed here in do not necessarily reflect the official views of the Swiss Government. Mette Huijgens and Nielja Knecht provided excellent research assistance.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

ESM 1

(XLSX 402 kb)

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Polzin, F., Sanders, M., Steffen, B. et al. The effect of differentiating costs of capital by country and technology on the European energy transition. Climatic Change 167, 26 (2021). https://doi.org/10.1007/s10584-021-03163-4

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10584-021-03163-4