Abstract

This study utilizes social exchange theory to argue that a more complete picture of the effects of China’s FDI in Africa needs to include non-economic factors, especially institutional forces that incorporate macro political considerations. We propose that economic dependencies created by China’s FDI in Africa are reciprocated by votes in international organizations, and thus, we hypothesize and test that increasing China’s FDI in African nations leads to increased political alignment in international affairs with those African nations. The proposed relationship, however, will be weakened for African countries with stronger governance mechanisms. Using data for China’s FDI in African countries from 2001–2019, we find support for our hypotheses. We find that China’s economic engagement in Africa has resulted in increased political alignment on international issues evidenced by votes in United Nations organizations raising the possibility Africa’s most attractive resource may not be economic, but rather political. This, however, poses the question of whether votes are a ‘resource’ that can be traded for economic purposes.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

THINK AGAIN: China doesn’t need Africa’s minerals. It needs African votes (the Africa Report, November 10, 2022)

Political candidates exchanging money for votes are considered corrupt ‘vote buying’ and illegal in many countries. What happens, however, when countries ‘exchange’ money for votes in international organizations? Is it corrupt vote buying or implicit quid pro quo in international affairs? Political scientists have found evidence of trading money for votes in international organizations. Countries elected to the United Nations Security Council (UNSC), for example, experienced a 59% increase in US foreign aid (Kuziemko and Werker 2006), with similar effects on Japanese and German foreign aid (Vreeland & Dreher, 2014). This is particularly worrisome since most of the aid provided directly to governments is commonly used to boost the political ambitions of recipient leaders (Adhikari, 2019). While the issue of trading votes for money is quite important in the social and political arena of foreign aid, it becomes even more salient in the economic realm of foreign direct investments (FDI) and loans. It raises the question of whether (ethically and otherwise) votes can be considered as resources to be traded between country partners for economic returns. This issue is particularly germane when it comes to China’s economic engagement with Africa. Indeed, what China is getting, or hopes to get, from its FDI and loans to Africa is generating considerable controversy.

China is currently Africa’s largest economic partner with Sino-Africa trade topping $284 billion in 2022 (Bociaga, 2023). There are over 10,000 Chinese firms operating in Africa having invested more than $2 trillion dollars over the past two decades (Jayaram et al., 2017). And this trend is increasing. This is reflected with China’s Foreign Direct Investment (FDI) to Africa that increased 4191% between 2001 and 2019 raising questions regarding what China hopes to gain from its FDI to Africa. Assertions regarding how China will leverage its economic engagement in Africa have generated controversy with headlines such as ‘China in Africa: Investment or exploitation’ (Al Jazeera, 2014) or ‘Clinton warns against “new colonialism” in Africa’ (Quinn 2011). Similarly, then U.S. Secretary of State John Bolton characterized Chinese investment in Africa as predatory, i.e., ‘the strategic use of debt to hold states in Africa captive to Beijing’s wishes and demands.’ The implications for the Chinese investments and lending in Africa go beyond popular press headlines and political jabs. The implications suggest real and serious consequences for development in Africa with concerns as to whether ‘China is making their lunch or eating it’ (The Economist, 2011). More worrisome are fears that China may use its increasing economic power to extract concessions that may be economically and politically detrimental to the continent. As Steve Kull, director of the program on International Policy attitudes noted ‘China may feel that it is only natural it should seek advantages in its trading relations…’ (BBC, 2011).

This study examines how China’s economic engagement in Africa is potentially leveraged into political influence. We specifically investigate whether China’s FDI and loans to Africa lead to quid quo pro of votes in international affairs, or in other words, whether China trades economic engagement for votes by African countries. Indeed, Africa’s most attractive ‘resource’ may not be economic, but rather political. With 54 nations across 5 regions, the African Union (AU) represents the largest voting bloc in international organizations. As the headline of the Africa Report article quoted above alludes, the quest for these votes might be driving China’s FDI in Africa. We utilize social exchange theory (SET) to argue that China’s economic engagement generates costly obligations with which African countries reciprocate in the international political arena, thus, creating a mutual dependency. This dependency is, however, asymmetrical. Hirschman (1945:17) identified disparities in economic dependence as an ‘effective weapon in the struggle for power,’ likely to be parlayed into political influence, and as such, we expect China’s FDI in Africa to lead to political alignment of African recipient countries with China in international affairs.

Political alignment represents the similarity of national preferences in international affairs based on national ideologies and orientations, which are thought to be key in facilitating countries toward congruent behavior (Gartzke, 1998). This congruent behavior is reflected in votes in UN organizations. Evidence is, however, mounting that these voting preferences, especially for less developed countries, may not be driven as much by national ideologies and preferences but more so as quid pro quo for financial aid. This literature has mainly focused on major donor countries—United States, France, United Kingdom, Germany, and Japan who also largely control disbursements by IMF and World bank (Adhikari, 2019). Less known is whether other countries use alternative economic inducements to trade for votes. While China may not be a major donor nation, it is still an economic powerhouse with vested political interests in the outcome of votes in international organizations. Understanding how China wields its economic power to achieve these interests is critical to understanding Chinese economic activity around the world, especially Africa.

This study uses the lens of social exchange theory to argue that a more complete picture of the effects of China’s FDI and loans in Africa needs to include non-economic factors, incorporating institutional forces that potentially integrate macro political considerations into Chinese multinational enterprise (MNE) strategies abroad (Cui and Jiang 2012). We propose that China’s FDI and loans in Africa generate an asymmetric economic relationship. This creates an economic power imbalance resulting in African nations dependence on China. The high mutual dependence of the relationship provides African countries with the option to countervail increasing FDI from China by exchanging with another resource sorely needed by China; support in international organizations stemming from political alignment.

As such, our research contributes to the literature in several ways. First it highlights the ethical considerations that arise when political quid pro quos enter the economic realm. Social exchange theory (SET) identifies six different types of resources (love, status, information, money, goods, and services) that are exchanged in different types of relationships (Cropanzano & Mitchell, 2005). We identify a seventh, votes, but bring to debate the ethical considerations that arise when votes in international organizations are ‘traded.’ Votes in international organizations are supposed to reflect national ideologies and preferences. Economic inducements such as FDI and loans can hardly be construed as reflecting national ideologies. This is particularly salient since research has shown that such financial inducements channeled through recipient governments are often used to solidify the political fortunes of the ruling class (Adhikari, 2019). Our findings show that less transparent governments are more susceptible to trade votes for economic engagement highlighting the question of whether this is normal quid pro quo in international relations or another avenue for corruption.

Furthermore, there has often been difficulty empirically separating investment from loans because of the lack of transparency surrounding Chinese investment deals. This ambiguity means that some investment packages, especially by state-owned enterprises that are not transparent about their finances or operations (Cannizzaro & Weiner, 2018) can simultaneously be interpreted as loans or investments. We utilize a composite measure of FDI that includes both direct investment and loans, thereby providing a more realistic purview of actual FDI activity. In addition, eschewing any assumptions of homogeneity within Africa, we specifically examine both the within country and between country effects of Chinese economic engagement. Finally, our findings show that not all determinants of emergent market MNE strategies are in the economic sphere. With 54 votes in United Nations bodies, Africa has the largest international voting bloc. This is apparently a very valuable resource that draws attention to the continent – albeit not an economic resource.

Background and Theory

FDI in Africa

According to neo classical theory and the endogenous model, capital inflow in the form of FDI and loans primarily affect the host economy through economic growth (Yimer, 2023). Theoretically, this economic growth occurs because of knowledge transfers, managerial capability spillovers, increased labor productivity, and increased competitiveness (Carkovic & Levine, 2002). Similarly, development theorists argue that FDI and loans provide capital inflows that release recipient economies from the binding constraint of domestic savings to stimulate domestic investments that boost domestic growth and real income (Ajayi, 2006). Despite the consistency of theoretical mechanisms through which capital inflows affect economic growth, the empirical evidence in Africa as with most developing economies is mixed (Yimer, 2023). While Lumbila (2005) and Brambila-Macias and Massa (2010) for example, found FDI positively affected economic growth in Sub-Saharan African countries, Akinlo (2004), Adams (2009), Udo and Obiora (2006) and Ayanwale (2007) did not find any effect of FDI on economic growth in different African countries.

One possible explanation for these mixed findings is that capital inflows such as FDI and loans have no direct effect on growth. Their effect is rather contingent on prevailing socio-economic and political factors that allow for the exploitation of the positive spillover effects (Carkovic & Levine, 2002). Trevino and Upadhyaya (2003) for example find that the positive effect of FDI on economic growth is more likely to occur in more open economies. In some economies, capital inflows are diverted to non-economically optimal uses, thus, not contributing to economic growth (Adams, 2009). The investments of capital inflows are directed more by politics than by economic rationale. This is more likely when provider of the capital, in this case China, is not motivated by economic considerations. Dreher et al. (2019) for example found that African political leaders’ birthplaces received substantially, and disproportionately more Chinese government financed projects than other areas.

The government of China plays a major role in determining whether and how Chinese firms engage in FDI, especially since FDI is an integral part of the government’s strategy (Duanmu, 2014; Li et al., 2013). The Chinese government supports FDI as a means for internationalizing Chinese firms and an essential mechanism for the continued development of China’s foreign policy objectives (Buckley, et al., 2018). Seventy-seven (77%) percent of the top Chinese FDI firms in 2015 for example were state-owned enterprises (MOFCOM, 2016). These firms are essentially extensions of the Chinese government, and as government institutions, are expected to serve a political mandate in their FDI decisions (Cui & Jiang, 2012).

Even for the minority of privately owned firms, engaging in FDI still requires close government collaboration and regulation (Jin, 2015). Much of the funding for FDI projects are provided by state-owned banks. Furthermore, because the Renminbi (RMB) is not freely exchanged, all conversions into foreign currency to use in FDI require prior state approval. China’s foreign reserve policy is structured to empower the government. The Chinese government’s active involvement in identifying host countries reveals a new level of business-government interaction that links foreign policy to FDI decisions (Kynge, 2017). Finally, the government of China is extremely active in negotiating the structure of investment projects, especially financing on behalf of Chinese MNCs. Take for example the Nairobi expressway completed in May 2022 that was supposed to be a public private partnership between the Kenyan government and China Road and Bridge Corporation (CRBC). The over $650 mm project was negotiated by the Chinese government as part of the Belt and Road Initiative in Africa. It was ‘financed’ by a direct loan to the Kenyan government from the state-owned China Communications Construction Company (parent of CRBC) on the condition that the project be carried out by CRBC. Moja Expressway, a subsidiary of CRBC will operate the expressway as a toll road for 27 years to repay the loan. Officially, this is listed as a loan to the Kenyan government, but practically, this is FDI by CRBC in Kenya. Essentially, Chinese FDI, rather than being mostly market driven, is subservient to the regulatory institutions and, thus, could also be a tool in the arsenal of the government as a mechanism of its pursuit of a broader economic, political, and foreign policy agenda (Buckley et al., 2018).

International Political Alignment

Gone are the days when China was characterized as ‘bereft of friends,’ ‘a beacon to no one – and, indeed, an ally to no one’ (Segal, 1999: 33). The rise of China as an economic power and its subsequent ‘emergence as an active player in the international arena’ (Medeiros & Fravel, 2003: 22) has led to increased international activism reflected in many global issues such as climate talks, reforming global economic and financial systems, and water diplomacy (Hongzhou & Mingjiang, 2020). China’s ability to align and cooperate with other nations to develop alternative international alliances that protect its global interests (Struver, 2012) is a central part of its foreign policy. This is exemplified in alliances and joint diplomatic efforts such as BRICS (Brazil, Russia, India, China, and South Africa), BASIC (Brazil, South Africa, India, and China) and Shanghai Cooperation Organization (SCO).

China’s unique and rapid transformation has challenged the West-dominated liberal world order (Mearsheimer, 2014). This has led to resistance especially among liberal western nations who see a threat in China’s rise as a potential ‘clash of civilizations.’ This clash is most reflected in voting on United Nations (UN) resolutions and necessitates China seeking allies especially in Africa given African countries’ political weight in international organizations. Seeking allies in the UN “allows China to find like-minded allies and mitigates any sense that it has to operate in all circumstances under the constraints of a western-style international order” (Foot 2014: 1092). Political alignment with foreign policy issues can be attained through diplomatic, military, or economic linkages (Struver, 2016). Economic interaction is a key mechanism through which such allies are created. Economic interaction between countries generally affects the value that each country places on the relationship.

Social Exchange: FDI for Votes

The quest to find ‘like-minded allies’ in international affairs often entails the trading of favors between countries. We draw on social exchange theory (SET) to explain why countries need to reciprocate these benefits for them to continue. Social exchange theory refers to the ‘voluntary actions of individuals that are motivated by the returns they are expected to bring and typically do in fact bring from others’ Blau (1964:91). There are three key features of SET: (1) an actor initiates a treatment targeted toward another (2) the target responds to the treatment, and (3) a relationship is formed that perpetuates the interaction (Cropanzano et al., 2017). In this case, China provides FDI and loans to African countries. These countries respond by voting in alignment with China in international organizations. This creates a pattern of economic engagement and interaction. More economic engagement promotes further continuation of other relationships, encouraging both sides to converge on shared interests, for example, with foreign policy (Flores-Macias and Kreps, 2013). Increased economic interaction, and thus, dependence between states would result in foreign policy convergence (Hirschman, 1945). This results from stronger economic interactions which leads to higher costs if the economic relationship is interrupted.

Power imbalance and interdependence builds on Emerson’s (1962) theory of power dependence. The power capability of an actor relative to another, according to Emerson’s framework, is determined by the actor’s dependence on the other party. To assess the actual dynamics of exchange between parties, their relative power capabilities to each other must be evaluated simultaneously. This dyadic approach provides two different dimensions of power capability: power interdependence and imbalance. Power interdependence measures the actors’ mutual dependence on each other while imbalance captures the relative difference in power between two actors. Power interdependence and power imbalance are independent dimensions of structural power capability. This allows for differing levels of power imbalance and interdependence within a dyad (Casaciaro & Piskorski, 2005).

Emerson (1972) argued that there is a direct connection between power and social exchange. This is particularly the case with social debts arising from inequality in the exchange that are settled by acts of subjugation by the less powerful party. When economic interaction takes place between asymmetric partners, the smaller state faces much higher costs from disruptions in the economic relationship. As a result, Hirschman (1945) argued, economic interactions can, therefore, become an arena for the transmission of influence by a stronger state. The United Nations General Assembly (UNGA) and affiliated organizations provide the arena in which foreign policy and political alignment potentially occurs. On a fundamental level, asymmetric economic interactions increase the susceptibility of weaker countries to stronger countries’ demands, especially those that are not directly communicated. Direct and indirectly communicated demands may be granted because of the fear that investments and other economic benefits may be at risk; consequently, the weaker state’s positions become subsumed in the foreign policy positions of the more powerful state (Dreher et al., 2008). Political alignment with a stronger state allows weaker partners to become part of a larger and stronger collective when dealing with global policy issues, yielding additional benefits for the weaker state. However, the tradeoffs or downside for the weaker states are less defined and may evolve over time.

Thus, although China’s FDI in Africa creates an economic power imbalance in favor of China, it is simultaneously met by high mutual dependence because African countries constitute the largest voting bloc in international organizations. Therefore, consistent with SET, African countries reciprocate Chinese FDI by aligning their votes in international organizations to Chinese positions.

H1: China’s FDI in Africa will be positively related with African countries’ international political alignment with China.

The Moderating Effect of Host Country Governance

Host African countries also play a role in China’s ability to utilize economic engagement for political ends. We examine the specific ‘opportunity’ afforded to China when African countries have weak governance mechanisms. Host country governance is defined as ‘the traditions and institutions by which authority in a country is exercised. This includes (a) the process by which governments are selected, monitored, and replaced; (b) the capacity of the government to effectively formulate and implement sound policies; and (c) the respect of citizens and the state for the institutions that govern economic and social interactions among them.’ (Kaufmann et al., 2010:4). We specifically argue that the effect of Chinese FDI on international political alignment will be weakened in better governed African countries for two reasons.

One of the central principles of Chinese investment is the noninterference principle or ‘no conditions attached.’ This is in stark contrast to investments from Western countries predicated on democracy or human rights conditions. Such conditions will be more attractive to leaders of countries with weak governance who are more likely to be authoritarian and less receptive to western ideals. The lack of democracy and transparency makes it possible for these leaders and the elite to direct FDI from China to projects favoring their core groups of supporters thereby increasing their chances of staying in power (Raess et al., 2022). This makes leaders of countries with weak governance more amenable to the unwritten quid pro quo that comes with the FDI from China.

Second, democracies in Africa in general have better governance than autocracies (Guseh & Oritsejafor, 2018). When it comes to UN voting, democracies are more aligned with the West and less susceptible to Chinese positions (Carter & Stone, 2015). Better governed countries in Africa, likely democracies, have the added burden of having to explain and face public scrutiny over their UN votes, especially when such votes deviate from historical precedence of aligning with the West. This makes it less likely that any quid pro quo from FDI would remain ‘hidden’ and raises the threshold of investment likely to convince the leaders of better governed countries to align with China. This argument leads to our next Hypothesis:

H2: The strength of host country governance will moderate the effect of FDI and political alignment such that better governed countries will be less susceptible to political alignment effects of FDI.

Method

Our sample consists of all 54 African countries from 2001 to 2019. Western Sahara, although a member of the African Union, is not recognized by China and is not a member of the UN and, therefore, is not included in our sample. We collect data from multiple sources – United Nations (General Assembly votes), World Bank (Africa Development Indicators, World Integrated Trade Solution, Worldwide Governance Indicators), United Nations Trade and Development (UNCTAD)’s Bilateral FDI Statistics and China-Africa Research Initiative from the School of Advanced International Studies at Johns Hopkins University.

Measures

Dependent Variable: Change in political alignment with China. Our dependent variable is the change in political alignment across consecutive years between China and each African country. We utilize yearly ideal points of all countries to calculate political alignment. Ideal points, constructed from the United Nations General Assembly voting data, are an indicator of a nation’s foreign policy preferences relative to the liberal Western order. Specifically, the ideal points are generated using the item response theory (IRT) statistical model to estimate one-dimensional national preference vis-à-vis a US-led liberal order (Dreher et al. 2017). The ideal points have a mean of 0 and a standard deviation of 1, with lower values indicating deviance from the US-led liberal order and higher values indicating congruency with the US-led liberal order. The ideal points improve upon conventional dyadic nation preference similarity indicators such as Affinity or S-scores (Gartzke, 1998; Signorino & Ritter, 1999) by allowing for more valid inter-temporal comparisons (Liao & McDowell, 2016). It is a more consistent measure of two countries’ alignment on political preference than voting agreement percentage, which can move dramatically due to changes in agenda even when the underlying preferences do not change. For each African country, we calculate political alignment with China each year using the following formula:

where PA(it) is country i’s political alignment with China at year t; Idealpoint(it) is country i’s ideal point at year t; idealpoint(china, t) is China’s ideal point at year t. We use the absolute value of the difference because we are only interested in the level of (mis) /alignment but not the direction of the difference (more liberal/conservative). The absolute difference reflects the misalignment, so to be consistent with the phrasing of our hypotheses, we multiply it by -1 to reflect the alignment. We then create a change in political alignment with China by subtracting the previous year’s value from the current year’s value (PA(it)—PA(i, t-1)). Therefore, our final variable reflects the yearly change in political alignment. The ideal points measure has been commonly used in related studies. For example, Yang et al. (2022) examined China’s FDI in developed countries and foreign policy convergence, and they constructed a similar measure using ideal points. Kaya and Woo (2022) examine China’s influence in the Asian Infrastructure Investment Bank and use a similar ideal points distance measure. Raess et al. (2022) used the same ideal points distance measure in their study of the effects of Chinese foreign aid and political alignment.

Independent Variables: Our main independent variable is the FDI inflow from China. As a result of the intertwined relationship between the Chinese government and China’s MNCs, calculating FDI from China is not as straightforward as with Western countries. MNCs can directly invest in foreign markets as customarily done by Western MNCs. This is usually funded with loans from state-run banks. Alternatively, the state-run banks (through the government) could finance the foreign project by lending the money directly to the foreign government on condition the specified Chinese MNC obtains the contract for the project. This is common with large infrastructure projects, and such financing will be accounted as loans rather than FDI. To obtain a full picture, we add both reported FDI inflow from China and loans from China as our measure of FDI inflow. We obtained bilateral FDI data from United Nations Trade and Development (UNCTAD)’s Bilateral FDI Statistics, which provides FDI data for 206 countries from 2001 to 2012. The FDI data after 2012 is obtained from the China-Africa Research Initiative in the School of Advanced International Studies at Johns Hopkins University. The loan data is also obtained from the China-Africa Research Initiative in the School of Advanced International Studies at Johns Hopkins University. An annual total amount (in billion U.S. dollars) of FDI inflow and loan from China into an African country is used as our main independent variable. As a robustness check, we also use FDI stock from China as an alternative measure.

Host Country Governance. We obtain governance indicators from the World Bank’s Worldwide Governance Indicators (Kaufmann et al., 2010), which is widely used in global business literature (e.g., Ding et al., 2016; Mensah, 2014; Saeed et al. 2022). The WGI index reports on six broad dimensions of governance for over 200 countries and territories over the period 1996–2020 – Voice and Accountability, Political Stability, Government Effectiveness, Regulatory Quality, Rule of Law, and Control of Corruption. We perform a factor analysis on the six dimensions and generate a composite score using the factor loadings of the six dimensions. Specifically, the principal-component factors method shows a one-factor solution with the following factor loadings: Voice and Accountability (0.838), Political Stability (0.788), Government Effectiveness (0.937), Regulatory Quality (0.913), Rule of Law (0.968), and Control of Corruption (0.917).

Control variables. When predicting political alignment with China, we include several control variables that may affect the investigated relationships, including total net FDI inflow, remittance, military expense, GDP per capita, GDP growth, GDP, oil production, Chinese immigrant population, export to China, and import from China. Net FDI inflows (measured in billion U.S. dollars) are the yearly total value of inward direct investment made by all foreign entities. Remittance is the yearly value (measured in billion U.S. dollars) of current transfers by migrant workers and wages and salaries earned by nonresident workers. Personal transfers include all current transfers between resident and nonresident individuals. Compensation of employees refers to the income of border, seasonal, and other short-term workers who are employed in an economy where they are not residents and of residents employed by nonresident entities. Migrant remittances have emerged as a significant source of external finance for developing countries and has important implications on national policy choices (Singer, 2010). Military expense (measured in billion U.S. dollars) is the yearly total amount of all current and capital expenditures on the armed forces. Countries with military expenses may experience slower economic growth and deter FDI (Dunne & Tian, 2013). GDP per capita (measured in U.S. dollars) is the yearly gross domestic product divided by midyear population. GDP growth is measured as the annual percentage growth rate of GDP at market prices based on constant local currency. GDP is measured as the log of a country’s GDP (in billion U.S. dollars). Oil production is measured as the log of annual quantity of petroleum and other liquids (in million barrels). Chinese immigrant stock is measured as the log of annual total count of Chinese immigrants that reside in each African country. Export to China (measured in billion U.S. dollars) is the yearly total value of goods that the African country exports to China, while import from China (measured in billion U.S. dollars) is the yearly total value of goods that an African country imports from China.

Results

Since not all countries have data for all years, the final dataset is an unbalanced panel data. We, therefore, use fixed-effects panel linear regressions in all analyses. The fixed-effects model accounts for unobserved country-level characteristics (e.g., culture, political environment, and historical relationship with China, etc.), and thus, it may reduce potential endogeneity due to such country-level characteristics. We test the moderation effect of African countries’ governance indicators by creating interaction terms of the composite score of governance with investments from China. All the predictors and control variables are lagged by one year. Descriptive statistics and correlation matrix of all variables are presented in Table 1 and Table 2. We tested multicollinearity by calculating variance inflation factors (VIFs) scores. The VIF values for all variables range from 1.01 to 4.20, which are well below the threshold of 10, suggesting that there is no excessive multicollinearity present in the data.

Table 3 presents the regression results of predicting Change in political alignment with China using FDI and loan from China. Model 1 includes control variables only, Model 2 tests the main effect of FDI inflow and loan from China, Model 3 includes Governance, and Model 4 includes the interaction term. All models are tested with year and country fixed effects, and standard errors are clustered at the country level.

Hypothesis 1 proposed that investment from China will be positively related to the change in political alignment with China. Model 2 shows that FDI inflow and loans from China is positive and significant (b = 0.015, p = 0.001), indicating that investment from China is positively related to change in political alignment. Thus, hypothesis 1 is supported. Specifically, at the mean, a $1 billion increase in FDI and loan inflow from China is associated with a 5% increase in political alignment with China. In other words, on average, if China invests $20 billion in an African country, it will achieve full political alignment (the difference in the ideal point is zero). It is noteworthy that the magnitude of the effect varies greatly among different African countries. For example, Senegal’s average alignment with China is −0.15, so a $10 billion investment from China would achieve full alignment. Yet, Sudan’s average alignment with China is −0.71, so $47 billion investment is needed from China to achieve full alignment.

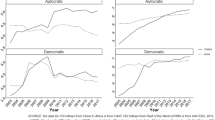

Hypothesis 2 proposes that African countries’ governance moderates the effect of Chinese investment in Africa on political alignment such that for countries with stronger governance mechanisms, Chinese economic engagement will have a weaker effect on political alignment. Model 4 of Table 3 shows that the interaction term is negative and significant (b = −0.049, p = 0.025). Thus, Governance weakens the positive effect of FDI inflow and loans from China, which shows support for H2. We plot the interaction effects in Fig. 1a and marginal effects in Fig. 1b.

a Interaction Plots of FDI Inflow and Loan from China and Governance. b dMarginal Effects of FDI Inflow and Loan from China

As shown in Fig. 1a, the positive effect of FDI inflow and loans from China weakens as Governance increases, and the positive effect flips into a negative effect at high levels of Governance. To further probe into the moderation effect, we conducted a marginal effects analysis and plotted the results in Fig. 1b. The marginal effects analysis allows us to see how the average effect of FDI inflow and loans from China changes across the whole range of Governance. As is shown in Fig. 1b, the average effects of FDI inflow and loans from China gradually weakens as the value of Governance increases from -2 to 2 (about -2 SD to + 2 SD). When Governance is at -2, every one-billion increase in FDI inflow and loans from China results in 0.085 increase in Change in political alignment with China, which is about 28.6% of the average political alignment with China of the sample. The average effect of FDI inflow and loans from China becomes insignificant when Governance is at -0.4, and it flips into negative. The negative average effect becomes significant (at p < 0.1 level) when Governance is at 0.8. When Governance is at 2, every one-billion increase in FDI inflow and loans from China results in 0.108 decrease in Change in political alignment with China, which is about 35.5% of the average political alignment with China of the sample.

An interesting insight can be gained by taking a closer look into the interaction effects between Chinese investment and host country governance. Generally, host countries with stronger governance mechanisms are more likely to be aligned politically with China even without any Chinese investment, and more Chinese investment would actually drive these countries away from China. Yet, host countries with weak governance are susceptible to Chinese investments, and they increase their political alignment with China as the investment increases. To summarize, the governance strength of host countries significantly weakens the effects of investments from China on the change in political alignment with China.

Supplementary Analysis

Dynamic Panel-Data Model

While Chinese FDI and loans influence an African country’s political alignment with China, the increased political alignment can further increase Chinese investment. The recursive relationship may lead to the problem of simultaneity, which is a common source of endogeneity. To alleviate the concern of simultaneity, we test the hypotheses using a dynamic panel model approach. We use the Arellano-Bond estimator (Arellano & Bond, 1991), which is a generalized method of moments estimator that uses lagged values of variables as instrumental variables, which is an effective way to alleviate concerns about simultaneity (Hill et al., 2021). Results reported on Table 4 show that FDI inflow and loans from China has a positive effect on Change in political alignment with China (b = 0.016, p = 0.058). Further, the interaction term is negative and significant (b = −0.056, p = 0.076).

FDI Stock from China

To show the robustness of our results, we run the same models with the total FDI stock from China as the independent variable. These results are reported on Table 5. Results show that FDI stock from China has a significant positive effect in all years (b = 0.011, p = 0.002). Thus, it is generally consistent with the primary results using FDI inflow and loans from China. However, the moderation effect of Governance is not significant.

Different Effects of FDI and Loans

To test the possible different effects between FDI and Loan, we run the same models by separating FDI inflows from China and Loans from China. Results reported on Table 6 show that FDI inflow from China has an effect on the level of Political alignment with China (b = 0.146, p = 0.095). As for Loans from China, it has effects on the Change in political alignment with China (b = 0.015, p = 0.000), and Governance weakens such effect (b = −0.036, p = 0.095). Together, the results suggest that FDI and Loans from China have distinct effects on a host country’s political alignment with China. FDI influences the overall degree of political alignment whereas Loans affect the increases in political alignment.

The Effects of Chinese Investment in Different Time Periods

It is possible that the effect of Chinese investment changes over time. Thus, we conduct additional analysis using piecewise regression to test how the effect changes over different time periods using four-year intervals. The results are presented in the following table (Table 7). As shown, the effect of FDI inflow and loans from China varies across the five different time periods. Specifically, it has no effect in 2001–2004, a positive effect in 2005–2008 (b = 0.126, p = 0.017), a positive effect in 2009–2012 (b = 0.063, p = 0.100), no effect in 2013–2016, and a positive effect in 2017–2020 (b = 0.017, p = 0.000). (Table 7)

FDI From U.S. and Political Alignment with U.S.

Our results also present the possibility that increasing globalization as reflected in increasing OFDI leads to increased international political alignment. That would mean that our results are instead capturing increasing international consensus due to globalization. If this is correct, increasing China’s OFDI to Africa would also lead to increasing political alignment with U.S., the anchor point of the Western liberal order. If as we hypothesized, China’s OFDI leads African countries to change their political interests to align with China’s, then increasing Chinese OFDI would rather lead to decreasing African countries’ alignment with the U.S. as they shift toward alignment with China. We, therefore, ran the analyses, but this time with political alignment with the U.S. as the dependent variable. Results reported on Table 8 show that FDI stock from China is negatively related to Change in political alignment with U.S. (b = −0.011, p = 0.032) and is negatively related to Political alignment with U.S. (b = −0.021, p = 0.014). This offers some evidence that our results are not capturing trends in international consensus building as increasing FDI and loans from China to African countries leads to increasing political alignment with China while simultaneously leading to decreasing political alignment with the U.S.

Further, we tested the effects of FDI from U.S. on the political alignment between African countries and U.S. as well as China. Results reported on Table 9 show that FDI from U.S. have no effects on the change or level of political alignment with U.S. However, FDI from U.S. is negatively related to both Change in political alignment (b = −0.176, p = 0.020) with China and Political alignment with China (b = −0.453, p = 0.056).

Sub-Saharan African Countries

In another robustness test, we remove northern African countries (Morocco, Algeria, Tunisia, Libya, Egypt, Sudan) from the full sample because these countries have distinct cultural and political characteristics that differ from the rest of the African countries (Sub-Saharan Africa). We test the hypotheses using the Sub-Saharan African countries sample and the results are consistent. These results are reported on Table 10. Specifically, regarding FDI inflow and loan from China, it has a positive effect on Change in political alignment with China (b = 0.014, p = 0.001). Regarding the moderation effects of Governance, it weakens the positive effect of FDI inflow and loans from China (b = −0.036, p = 0.049). Thus, the overall results on the Sub-Saharan sample are consistent with the full Africa sample.

Additional Robustness Tests

We Conducted Various Other Robustness Tests

Some of the control variables are highly correlated, which raises the concern regarding multicollinearity. We checked the VIF value. Import from China has the highest VIF value (4.06), followed by GDP (3.32), and military expense (2.88). As a general rule of thumb, VIF values greater than 10 indicate the presence of multicollinearity. Therefore, the multicollinearity issue in our data is not very concerning. Nevertheless, we tried removing the three above-mentioned variables that have the highest VIF values and the regression results remain consistent. Specifically, FDI and loan from China has a positive effect on Change in Political Alignment with China (b = 0.017, p = 0.000). Further, Governance weakens the main effect of FDI and loan from China (b = −0.042, p = 0.052). Therefore, the results are consistent after removing the three highly correlated variables.

Discussion and Conclusion

The pace of China’s economic engagement in Africa has grown significantly in the past two decades. According to data from China-Africa Research Initiative in the School of Advanced International Studies at Johns Hopkins University, China’s OFDI and loans to Africa grew from $0.298bn in 2001, peaking at $30.5bn in 2016 to $9.5bn in 2019, an increase of over 3113%. Other financial engagements by China in Africa are increasing concomitantly. The financing of Chinese contracted projects in Africa for example, have also been increasing and peaked at $55bn in 2015 (Krukowska, 2018). Similarly, by 2016, China was by far the largest exporter to Africa accounting representing 17.5% of African imports. By mid-2017 there were more than 10,000 Chinese-owned companies operating in Africa (Jayaram et al., 2017). Clearly, China’s economic engagement in Africa is substantial and increasing.

Although globalization is ubiquitous, China’s economic engagement in Africa seems to raise more eyebrows than expected. Then U.S. Secretary of State John Bolton described China’s economic engagement in Africa as predatory, that is, ‘the strategic use of debt to hold states in Africa captive to Beijing’s wishes and demands’ (Landler & Wong, 2018). Others argue that Chinese investments rather foster greater independence of African countries, as they are long-term and without any ‘paternalistic’ or ‘imperialist’ preconditions usually found in investments from the west (Lee, 2017). These concerns have increased considerably with the Belt and Road Initiative that also includes several African countries. Academic research has been limited in its ability to shed light on this phenomenon. Research on the motivations underlying China’s economic engagement in Africa has been largely yielded inconclusive results (Ross, 2015), in part due to reliance on mainstream theories of internationalization such as Dunning’s (1980) eclectic theory. The dominance of state-owned enterprises, availability of FDI capital provided by state-owned banks and centralized economic planning creates idiosyncratic permutations peculiar to China (Ross, 2015) that limits the applicability of traditional economic theories (Buckley et al., 2007a, 2007b).

This study extends the lens used to explore China’s economic engagement in Africa. We propose that non-economic factors, particularly institutional forces that shape both macro and micro strategies must be considered to gain a better understanding of the effects of China’s FDI in Africa. China’s regulatory institutional environment shapes MNE FDI strategies such that in Africa, China’s FDI gives it significant leverage as it increases costly obligations and resource dependence on the part of many African countries. African countries respond to this dependency by countering with a readily available political resource, votes within international organizations. In this context, African countries respond by creating a mutual dependency in reciprocating with vote alignment. Finally, we also incorporate the role of the strength of the host country’s governance mechanism. Better governed African countries would be less susceptible to the unwritten obligations from FDI. Overall, the analyses provide strong support for our hypotheses.

This study simultaneously considers whether China’s proposed stance of ‘trading’ economic resources for votes that achieve political alignment is ethical. We discuss and investigate the power asymmetry between China and its African FDI partners to consider whether ‘votes’ might be considered as just another resource along with love, status, information, money, goods, and services. We question whether power asymmetry between the two states makes it difficult for ‘mutual’ dependency to occur. Power influences the partnership dynamics available to China’s FDI recipients and greatly limits their response to exchange requirements that China dictates. Power, as defined by Castells (2016), is the ‘relational capacity that enables certain actors to asymmetrically influence the decisions of others in ways that favor the empowered actors’ will, interests, and values.’ To maintain the exchange relationship, China’s FDI recipients (African countries) reciprocate with perhaps another resource they have available, votes in international organizations. This brings the discussion full circle to yield that perhaps ‘votes’ are resources for those who maintain limited options to reciprocate exchange relationships.

This study, therefore, joins a nascent but growing list of studies that have started to examine the role of politics or political institutions in FDI (e.g., Cui and Jiang 2012; Munjal et al., 2022; Wang et al., 2021). It confirms the argument that non-economic factors should be taken into consideration when examining economic phenomena such as FDI. In this case, China pursues diplomacy in both the economic and political arenas. Economic factors such as the search for natural resources or markets for products may have attracted China to Africa, but in the past decade, the African resource apparently most attractive to China is not an economic one, but rather political alignment which results in voting congruency by African countries in international organizations.

Our study also has a couple of limitations. First our measure of political alignment is fairly restrictive. We capture only the changes in preferences that result from voting in UN organizations. Most international relations issues though are not resolved through UN voting but rather through bilateral and multilateral negotiations. These unfortunately are often not public. We, however, believe our measure provides a conservative test of our arguments as UN voting represents a very public irreversible show of alignment. Future research could use qualitative analyses of public statements by country leaders as a richer but more nuanced measure. In addition, we do not examine how bilateral relationship between China and individual African countries affects political alignment. Several millennia of trading (Kenya & Tanzania) for example, or co-membership in BRICS (South Africa) means in some cases special bilateral ties might be equally as relevant. Although we empirically control for unobserved country-level characteristics by using fixed-effects modeling, a future study could enhance the literature by specifically hypothesizing on how specific bilateral ties influences China-Africa relationship, especially economic engagement.

Finally, by broadening our lens beyond merely an economic perspective, we derive the effects of China’s FDI in Africa by examining how actual FDI varies across different counties and time relative to specific outcomes, in this case international political alignment. While understanding the proximal effect of China’s economic engagement in Africa is instructive, equally instructive is knowing the long-term impact of this engagement, especially when there may be competing sources of investments. Future research could examine the long-term impact of China’s FDI relative to Europe and U.S. FDI on key metrics such as economic development, unemployment or even spurring new business development.

Data availability

Not applicable. This study uses copyrighted data, but from publicly available sources.

References

Adams, S. (2009). Foreign direct investment, domestic investment, and economic growth in sub-Saharan Africa. Journal of Policy Modeling, 31, 939–949.

Adhikari, B. (2019). Power politics and foreign aid delivery tactics. Social Science Quarterly, 100(5), 1523–1539.

Ajayi, S.I. (2006) FDI and economic development in Africa. In ADB/AERC international conference on accelerating Africa’s development five years into the 21st century, Tunis, November (pp. 22–24).

Akinlo, A. E. (2004). Foreign direct investment and growth in Nigeria. Journal of Policy Modeling, 26, 627–639.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: monte carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297.

Ayanwale, A. (2007). FDI and economic growth: Evidence from Nigeria [African Economic Research Consortium Paper No. 165]. African Economic Research Consortium.

BBC (2011). Rising concern about China’s Increasing Power: Global Poll.

Bociaga, R. (2023). China-Africa trade soars on spike in commodity prices. NikkeiAsia January 27, 2023

Brambila-Macias, J., & Massa, I. (2010). The global financial crisis and sub-Saharan Africa: The effects of slowing private capital inflows on growth. African Development Review, 22, 366–377.

Buckley, P. J., Clegg, L. J., Cross, A. R., Liu, X., Voss, H., & Zheng, P. (2007a). The determinants of outward Chinese foreign direct investment. Journal of International Business Studies, 38(4), 499–518.

Buckley, P. J., Clegg, L. J., Cross, A. R., Liu, X., Voss, H., & Zheng, P. (2018). A retrospective and agenda for future research on Chinese outward foreign direct investment. Journal of International Business Studies, 49(1), 4–23.

Buckley, P. J., Devinney, T. M., & Louviere, J. J. (2007b). Do managers behave the way theory suggests? A choice-theoretic examination of foreign direct investment location decision-making. Journal of International Business Studies, 38, 1069–1094.

Cannizzaro, A. P., & Weiner, R. J. (2018). State ownership and transparency in foreign direct investment. Journal of International Business Studies, 49(2), 172–195.

Carkovic, M., & Levine, R. (2002). Does Foreign Direct Investment Accelerate Economic Growth? in H. T. Moran, E. Graham, M. Blomstrom (eds.), Does FDI Promote Development? Washington, DC: Institute for International Economics.

Carter, D. B., & Stone, R. W. (2015). Democracy and multilateralism: The case of vote buying in the UN General Assembly. International Organization, 69(1), 1–33.

Castells, M. (2016). The sociology of power: My intellectual journey. Annual Review of Sociology, 42, 1–19.

Cui, L., & Jiang, F. (2012). State ownership effect on firms’ FDI ownership decisions under institutional pressure: a study of Chinese outward-investing firms. Journal of International Business Studies, 43, 264–284.

Ding, S., Qu, B., & Wu, Z. (2016). Family control, socioemotional wealth, and governance environment: the case of bribes. Journal of Business Ethics, 136(3), 639–654.

Dreher, A., Fuchs, A., Parks, B., Strange, A. M., & Tierney, M.J. (2017). Aid, China, and Growth: Evidence from a New Global Development Finance Dataset. AidData Working Paper #46. Williamsburg, VA: AidData.

Dreher, A., Fuchs, A., Hodler, R., Parks, B., Raschky, P., & Tierney, M. (2019). African leaders & the geography of China’s foreign assistance. Journal of Development Economics., 140, 44–71.

Dreher, A., Nunnenkamp, P., & Thiele, R. (2008). Does US aid buy UN general assembly votes? a disaggregated analysis. Public Choice, 136, 139–164.

Dreher, A., Sturm, J.-E., & Vreeland, J. R. (2009). Global horse trading: IMF loans for votes in the united nations security council? European Economic Review, 53(7), 742–757.

Duanmu, J.-L. (2014). State-owned MNCs and host country expropriation risk: The role of home state soft power and economic gunboat diplomacy. Journal of International Business Studies, 45(8), 1044–1060.

Dunne, J. P., & Tian, N. (2013). Military expenditure and economic growth: A survey. The Economics of Peace and Security Journal, 8(1), Article 1.

Emerson, R. M. (1962). Power-dependence relations. American Sociological Review, 31–41.

Emerson, R. M. (1972). Exchange theory, part II: Exchange relations and networks. Sociological theories in progress, 2, 58–87.

Flores-Macias, G. A., & Kreps, S. E. (2013). The Foreign Policy Consequences of Trade: China’s Commercial Relations with Africa and Latin America. The Journal of Politics, 75(2), 357–371.

Fong, W., & Sakib, N. (2021). A “Good” country without democracy: can China’s outward FDI buy a positive state image overseas? Politics & Policy, 49(5), 1146–1191.

Gartzke, E. (1998). Kant we all just get along? opportunity, willingness, and the origins of the democratic peace. American Journal of Political Science, 42(1), 1–27.

Guseh, J. S., & Oritsejafor, E. O. (2018). Governance and democracy in Africa: Regional and continental perspectives. Rowman & Littlefield.

Hill, A. D., Johnson, S. G., Greco, L. M., O’Boyle, E. H., & Walter, S. L. (2021). Endogeneity: a review and agenda for the methodology-practice divide affecting micro and macro research. Journal of Management, 47(1), 105–143.

Hirschman, A. (1945). National Power and the Structure of Foreign Trade. University of California Press.

Hongzhou, Z., & Mingjiang, L. (2020). China’s water diplomacy in the Mekong: a paradigm shift and the role of Yunnan provincial government. Water International, 45(4), 347–364.

Jayaram, K., Kassiri, O. & Yuan Sun, I. (2017). The Closest look yet at Chinese economic engagement in Africa. Mckinsey 2017 Report on Africa.

Jin, X. (2015). Deregulation in Chinese outbound direct investment: 2014 and beyond. King and Wood Mallesons, 24.

Kaufmann, D., Kraay, A., & Mastruzzi, M. (2010). Response to ‘What do the worldwide governance indicators measure?’ The European Journal of Development Research, 22, 55–58.

Kaya, A., & Woo, B. (2022). China and the Asian Infrastructure Investment Bank (AIIB): Chinese Influence Over Membership Shares? The Review of International Organizations, 17, 781–813.

Krukowska, M. (2018). China’s economic expansion in Africa–selected aspects. International Business and Global Economy, 37(1), 84–97.

Kuziemko, I., & Werker, E. (2006). How much is a seat on the Security Council worth? Foreign aid and bribery at the United Nations. Journal of Political Economy, 114(5), 905–930.

Kynge, J. (2017). Beijing’s chicanery leaves western business guessing. Financial Times, 08 August 2017.

Landler, M., & Wong, E. (2018). Bolton Outlines a Strategy for Africa That’s Really About Countering China. The New York Times

Lee, C. (2017). The specter of global china: politics, labor, and foreign investment in Africa. University of Chicago Press. https://doi.org/10.7208/9780226340975

Li, J., Newenham-Kahindi, A., Shapiro, D. M., & Chen, V. Z. (2013). The two-tier bargaining model revisited: theory and evidence from China’s Natural Resource Investments in Africa. Global Strategy Journal, 3(4), 300–321.

Liao, S. L., & McDowell, D. (2016). No reservations: international order and demand for the renminbi as a reserve currency. International Studies Quarterly, 60(2), 272–293.

Lumbila, K.N. (2005). Risk, FDI and economic growth: A dynamic panel data analysis of the determinants of FDI and its growth impact in Africa. American University.

Mearsheimer, J. J. (2014). Why the Ukraine crisis is the West’s fault: the liberal delusions that provoked Putin. Foreign Affairs, 93, 77.

Medeiros, E. S., & Fravel, M. T. (2003). China’s new diplomacy. Foreign Affairs, 82, 22.

Mensah, Y. M. (2014). An analysis of the effect of culture and religion on perceived corruption in a global context. Journal of Business Ethics, 121(2), 255–282.

Munjal, S., Varma, S., & Bhatnagar, A. (2022). A comparative analysis of Indian and Chinese FDI into Africa: the role of governance and alliances. Journal of Business Research, 149, 1018–1033.

Raess, D., Ren, W., & Wagner, P. (2022). Hidden Strings Attached? Chinese (Commercially Oriented) Foreign Aid and International Political Alignment. Foreign Policy Analysis, 18(3).

Ross, A. G. (2015). An empirical analysis of Chinese outward foreign direct investment in Africa. Journal of Chinese Economic and Foreign Trade Studies.

Saeed, A., Baloch, M., & Riaz, H. (2022). Global insights on TMT gender diversity in controversial industries: a legitimacy perspective. Journal of Business Ethics, 179(3), 711–731.

Segal, G. (1999). Does China Matter?. Foreign Affairs, 24–36.

Signorino, C. S., & Ritter, J. M. (1999). Tau-b or Not Tau-b: measuring the similarity of foreign policy positions. International Studies Quarterly, 43(1), 115–144.

Singer, D. A. (2010). Migrant remittances and exchange rate regimes in the developing world. American Political Science Review, 104(2), 307–323.

Trevino, L. J., & Upadhyaya, K. P. (2003). Research note foreign aid, FDI and economic growth: evidence from Asian countries. Board of Advisers Chairperson, 12(2), 119.

Udo, E.A., Obiora, I.K. (2006). Determinants of foreign direct investment and economic growth in the West African monetary zone: A system equations approach.

Vreeland, J. R., & Dreher, A. (2014). The political economy of the United Nations Security Council: Money and influence. Cambridge University Press.

Wang, D., Zhu, Z., Chen, S., & Luo, X. R. (2021). Running out of steam? A political incentive perspective of FDI inflows in China. Journal of International Business Studies, 52, 692–717.

Yang, G., Tang, T., Wang, B., & Qi, Z. (2022). Money talks?: An analysis of the international political effect of the Chinese overseas investment boom. Review of International Political Economy, 29(1), 202–226.

Yimer, A. (2023). When does FDI make a difference for growth? A comparative analysis of resource-rich and resource-scarce African economies. International Finance, 26(1), 82–110.

Quinn (2011) Clinton warns against “new colonialism” in Africa Reuters, June 11, 2011. https://www.reuters.com/article/world/us-politics/clinton-warns-against-new-colonialism-in-africaidUSTRE75A0RI/#:~:text=%22We%20don't%20want%20to,a%20five%2Dday%20Africa%20tour.

Funding

Open access funding provided by University of Pretoria.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Ndofor, H.A., Jones, C.D. & Li, M. What Happens When Your Hand is in My Pocket: The Foreign Policy Effects of China’s Foreign Direct Investment in Africa. J Bus Ethics (2024). https://doi.org/10.1007/s10551-024-05794-w

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10551-024-05794-w