Abstract

Platforms can create value within their ecosystems through their investments. In this paper, we model a monopolistic platform choosing the level of a demand-enhancing investment and the membership fees that sellers and buyers pay to access the platform. We find that platform size and quality are large when the degree of product differentiation among sellers and investment productivity are high. Platform profit and users’ surplus are aligned. If the platform sells a product under its brand, incentives to invest are higher, compared to a pure marketplace, and sellers’ surplus can be larger if the degree of product differentiation is low.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Digital platforms are ubiquitous. The economy has been revolutionised, by the “business model that uses technology to connect people, organizations, and resources in an interactive ecosystem in which an amazing amount of value can be created and exchanged” (Parker et al. 2016, p. 3): most of the innovative services that appeared in the last decades, such as retail and marketplace services, mobile commerce, customer service, e-procurement, and purchase-to-pay, are commonly traded online by economic platforms operating on the Internet or in social networks. Besides e-commerce businesses (Amazon, eBay), several creative industries such as Google (search engine), Facebook (social network), and Sony (gaming) as well as the modern cultural and tourism industries (Netflix, Spotify, YouTube, Booking.com, Expedia, TripAdvisor etc.) produce and distribute their contents by open or closed platforms. Not only platforms themselves are among the most innovative and successful start-up initiatives in recent years; but, more and more, both established businesses and new entrepreneurial ventures rely on them for their growth and performance (Jullien and Sand-Zantman 2021).

Value creation by platform-based technology ecosystems is related in a key way to the ecosystem’s capacity to foster complementary innovation from autonomous firms (Cennamo and Santaló 2019; Kretschmer et al. 2022) and to the action of platforms acting as “private regulators” who govern access to and interactions around the platform (Boudreau and Hagiu 2009). However, platforms can create substantial value within their ecosystems also through their strategic investments. Through investments in areas such as infrastructure, technology, data analytics, and content creator support, platforms can contribute to their long-term success in the digital landscape.

Against this background, in this paper we build a model to investigate the decision problem of a monopolistic platform simultaneously choosing (i) the level of its investment and (ii) the membership fees that sellers and buyers pay to access the platform, in a context where sellers compete in the product market. The investment we consider is demand-enhancing, and it affects symmetrically the demand function of the sellers that are in the market. There are several examples of such kind of investment:

-

In the video game industry, console producers make large investments in order to improve the technological features of their console, which may advantage consumers in the use of any video game offered by developers (Schilling 2003);

-

E-commerce platforms invest in high-quality logistics, enhancing customer experience irrespective of the seller they buy from (Cui et al. 2020);

-

Online video platforms invest to provide content producers with high-quality infrastructure and video creation support tools, benefiting all users;

-

Food delivery platforms invest in real-time tracking and route optimization to improve the delivery speed, which consumers value irrespective of the restaurant they choose;

-

Online travel agencies invest in customer service, which creates value for guests, irrespective of the hotel they choose.

Our analysis starts with the case of a pure marketplace, i.e. a platform that only enables third-party sellers to sell to buyers. The results can be summarized as follows. First, platform size (measured by the total number of users joining the platform) and platform quality (measured by the level of investment) co-move, in that they are both large when the degree of product differentiation among sellers and investment productivity are high. When products are highly differentiated, the platform can admit more sellers, with a limited effect on their profitability. Due to positive cross-group effects, the platform finds it convenient to admit more buyers as well. In a larger platform, the incentives to invest in quality increase; since a higher level of investment strengthens the positive cross-group effects, this reinforces the incentive to have a larger number of buyers and sellers joining the platform. When investment productivity is high, investment in quality is large, making the platform more attractive. As more buyers and sellers join the platform, this further reinforces the incentive to invest in quality.

Second, optimal membership fees respond differently to variations in product differentiation and investment productivity. If platform quality is high because investment is highly productive, fees are high on both sides of the market. If platform quality is high because product differentiation is high, membership fees should be low for sellers (attracting them in high numbers with a limited impact on their profits) and high for buyers (whose willingness to pay to join the platform would be high due to the high number of sellers and high quality). Finally, platform profit and users’ surplus are aligned, since they react in the same way to variations in product differentiation and investment productivity.

We then move to the analysis of a hybrid platform, i.e. a platform that also sells a product under its brand. Amazon, Apple, Nintendo, and Sony are all examples of hybrid platforms. In this case, we show that the platform incentives to invest are higher compared to a pure marketplace because the platform can appropriate a higher fraction of seller surplus for its product. As a result, the platform size is larger as well. It turns out that sellers’ surplus can be larger if the degree of product differentiation is low enough. In this case, the positive impact of investment on sellers’ profit more than compensates for the negative impact of more intense competition. Also in this case, then, platform profit and users’ surplus are aligned.

The rest of the paper is organized as follows. In Sect. 2 we review the streams of literature our paper builds on and contribute to. In Sect. 3 the basic set-up of the model is described, while the results are presented and discussed in Sect. 4. In Sect. 5 we analyze the case of a hybrid platform. Finally, Sect. 6 concludes, by providing a set of managerial and policy implications and possible avenues for future research.

2 Literature review

Our paper contributes to three strands of literature concerning multi-sided platforms, which we will review in this section. First, we consider platform investment strategies, as a special case of non-price strategies. Second, we review the recent literature on hybrid platforms, as our paper also deals with hybrid platforms’ impact on the market equilibrium in the presence of platform investment. This type of strategy is an instance of non-price strategy, but we will cover the literature studying it in a dedicated subsection, given its particular relevance in the latest years. Finally, we analyse how platform strategies interact with seller competition, the other distinctive feature of our model.Footnote 1

2.1 Platform investment

Among platform non-price strategies, the topic of platform investment strategies has received some attention in the economics literature.Footnote 2 Anderson et al. (2014) investigated, as a key decision in platform design, the level of platform performance to invest in new product development, such as the choice between investing in platform performance or holding back investment to facilitate third-party content development in markets that exhibit two-sided network externalities. Casadesus-Masanell and Llanes (2015) examine how incentives to invest in platform quality are influenced by the degree of platform openness. In a proprietary platform, investments to improve quality are made by the platform owner; in an open platform, investments are made by application developers and advanced users. While the nature of cross-payments between users and developers plays a role in determining investments in open platforms, they found that it has no impact on proprietary platforms. A proprietary platform would invest efficiently if adoption by users and developers were efficient, but entry is not efficient, so investment is not either. Tan et al. (2020) develop a model to explore the key trade-offs behind platforms’ investment in integration tools and how such investment interacts with pricing decisions in a two-sided market. Generally, higher levels of integration investment by platforms become desirable when the platform has access to a large pool of content providers and consumers, can develop highly effective integration tools that reduce third-party development costs, and operates in a market where content providers earn a sufficient high-profit margin by creating highly valued content for the consumer market. Finally, Etro (2021a) considers a setting where an ad-funded platform competes with a device-funded platform, investigating how the difference in the business model can modify the incentive of each platform in investing in its quality and in introducing first-party apps.Footnote 3

While this literature mainly considers the choice between investing in platform performance or in third-party content (Anderson et al. 2014), focusing on the incentives of each platform in investing in its quality (Etro 2021a), we first model the choice of a platform’s demand-enhancing investment, examining the effect of investment productivity and the degree of product differentiation among sellers on the relationship between platform size and quality. This insight can deepen our understanding of how platform investment strategies respond to market conditions, contributing to the literature on platform non-price strategies.

2.2 Hybrid platforms

The literature concerning hybrid platforms is sprouting, with a particular interest in understanding whether having a hybrid platform is to be preferred to a pure marketplace case. Hagiu and Spulber (2013) introduced investment in first-party content as a strategic variable for two-sided platforms and showed the interplay with the platforms’ pricing strategies to solve the market coordination problem, when two-sided platforms provide first-party content which makes participation more attractive to buyers, independently of the presence of the sellers, but do not consider explicitly the competition among sellers. Anderson and Bedre-Defolie (2021) propose a model featuring a platform that implements an ad valorem fee structure based on revenue and has the option to operate as a hybrid platform, allowing free entry of sellers in a monopolistic competition setting with horizontal differentiation. Anderson and Bedre-Defolie (2022) extend the Anderson and Bedre-Defolie (2021) model by studying the introduction of either transaction or ad valorem fees for sellers, while buyers are not charged any fees.

Other works modelling hybrid platforms include Hagiu et al. (2022), Etro (2021b) and Etro (2023). In Hagiu et al. (2022), products are identical and sold by “fringe” producers (few in number), but there is also a high-quality seller offering a distinguished product who can invest further to improve it. Etro (2021b) develops a marketplace model (along the lines of Amazon’s one) that hosts third-party sellers offering a variety of independent products. The platform has the choice to provide some of these products as a first-party retailer, purchasing from manufacturers and reselling directly on the platform, or as a producer and retailer of private label products. Finally, Etro (2023) creates a model featuring a hybrid platform that sells its own products and charges commissions to third-party sellers under monopolistic competition with free entry. This model can represent cases where the platform does not favor its products through worse conditions or higher commissions for third-party sellers.Footnote 4

Within this literature, our paper contributes to the ongoing discussion on the welfare implications of platform strategies and regulatory considerations, such as a ban on dual mode. Most of the literature has focused on consumers’ welfare in evaluating social welfare impact of hybrid platforms, often highlighting the negative impact on sellers’ profit. Since Hagiu et al. (2022) and Etro (2023) suggest that a ban on dual mode could harm consumers, while Anderson and Bedre-Defolie (2022) find the opposite result, we identify a new mechanism based on platform investment through which a ban on dual mode could harm not only consumers but also sellers.

2.3 Competition among sellers

Studies investigated how fees can be used by gatekeepers or platforms to regulate the interaction between hosted sellers. The closest paper to ours is Belleflamme and Peitz (2019a), which is discussed for comparison in Sect. 3.

Among early works, Baye and Morgan (2001) studied the case of a monopoly gatekeeper that uses access fees to control seller competition on its platform, in the case of homogeneous products, while Belleflamme and Toulemonde (2009) considered both fees and subsidies and studied how a new platform can use these to compete with an already existing one, in presence of intra- and inter-group externalities. Hagiu (2009) considers how buyers’ love for variety in a two-sided market setting can shape platform pricing choice, also concerning the choice between membership and transaction fees, in the presence of competition among producers. Belleflamme and Toulemonde (2016) introduced intra-group externalities in the two-sided single homing model by Armstrong (2006), alongside the inter-group already considered by the previous model. Later, Belleflamme and Peitz (2019b) showed that competing sellers may be more willing to accept exclusivity agreements to relax competition among them, in particular cases. Recently, Karle et al. (2020) studied sellers’ strategies in the presence of platform competition: when it is intense, they try to avoid it by moving to other platforms, and this market segmentation leads to an increase in the fees; when instead competition is weak, sellers tend to refer to the same platform, and this increase competition among platforms to attract sellers. This results in a negative correlation between fees and platform competition. Teh (2022) analyses the case where the platform operates solely as a marketplace, investigating which type of fees are to be preferred: the platform’s incentives in its governance design choices are strongly linked to the pricing instrument used and market characteristics such as seller’s marginal cost and aggregate demand elasticity. In particular, for volume-aligned fee instruments (such as per-transaction fees, proportional fees when seller marginal costs are high, and buyer participation fees), the governance model that maximizes profit also maximizes transaction volume, intensifies competition among sellers, and generates lower transaction value. For seller-aligned fee instruments (proportional fees when seller marginal costs are low, seller participation fees, two-part tariffs), the governance design that maximizes profit is biased towards increasing seller surplus, thus leading to insufficient competition among sellers.

Within this literature, we are the first to consider an investment decision by the platform. This decision impacts not only the intensity of the positive cross-group effects but also the negative within-group effect due to competition, with the latter depending on the degree of product differentiation. Consequently, the pricing strategy of the platform is affected as well, as fees must be utilized not only to manage competition but also to appropriate the value created by the investment.

3 The model

In this section, we set up our model (3.1), we report the equilibrium solution (3.2), and we perform a welfare analysis (3.3). Our model builds on Belleflamme and Peitz (2019a). In fact, in the pure marketplace, we model seller competition as they do, but we allow the platform to choose the level of a demand-enhancing investment in addition to membership fees.

3.1 Set up of the model

The model considers a population of \(n_{b}\) buyers and \(n_{s}\) sellers interacting on a monopolistic platform. Buyers’ utility function is given byFootnote 5:

\(q_{0}\) is an Hicksian composite commodity with price \(p_{0}=1.\) Parameter \(\lambda\) (with \(0\le \lambda \le 1\)), measures the degree of substitutability between products. A is a parameter affecting symmetrically the marginal utility of products offered by sellers. We shall assume \(A={\bar{A}}+a\). \(a\ge 0\) is the level of demand-enhancement investment by the platform, associated with a quality improvement for all the products offered on the platform. Without loss of generality, we shall assume \({\bar{A}}-c=1\), where \(c<{\bar{A}}\) is the average cost of sellers.

The buyer maximizes her utility \(U(q_{0};q_{1},q_{2},\ldots ,q_{n_{s}})\) subject to the budget constraint \(y=q_{0}+\sum _{k=1}^{n_s}p_{k}q_{k}\), where y is the income and \(p_{k}\) is the price of \(q_{k}\). This yields the linear demand function, where \(q_{-k}=\) \(\underset{g\ne k}{\overset{}{\sum } }q_{g}\):

On the supply side, given the demand functions, sellers compete by offering horizontally differentiated products. Competition is à la Cournot. As for the two extreme cases of \(\lambda\), when \(\lambda =1\) the products are homogeneous, while, for \(\lambda =0\), sellers are monopolists in their market. Production is characterized by constant returns to scale so that the total cost function for the seller k producing a quantity \(q_{k}\) is given by \(C(q_{k})=cq_{k}\). The profit function for seller k is:

The net surplus of visiting the platform for sellers and buyers is given by \(v_{s}=r_{s}+\pi (n_{b},n_{s},a)-m_{s}\) and \(v_{b}=r_{b}+u(n_{b},n_{s},a)-m_{b}\). \(r_{g}\) is the stand-alone utility on side \(g\in \left\{ b,s\right\}\), \(\pi (n_{b},n_{s},a)\) and \(u(n_{b},n_{s},a)\) are the net gains from trade, for sellers and buyers respectively, while \(m_{g}\) is the membership fee imposed by the platform on side g.

Following Belleflamme and Peitz (2019a), we shall assume the existence of a mass Z of buyers and sellers, with Z large, which have an opportunity cost of entry which is uniformly distributed over \(\left[ 0;Z\right]\). If follows that \(n_{s}\) and \(n_{b}\) are given by:

from which:

The platform profit will derive then from the membership fees, after having considered the cost for the demand-enhancing investment \(C_{A}(a)=\frac{\gamma a^{2}}{2}\), with \(\gamma >0.\) The higher \(\gamma\), the less appealing will be the investment. The platform profit is then given by:

The timing of the game is such that, at stage \(t=0\), the platform fixes \(m_{b}\), \(m_{s}\) and a, while at stage \(t=1,\) sellers compete fixing quantities simultaneously in the Cournot game.

3.2 Equilibrium

The model is solved proceeding backward, considering first the Cournot equilibrium at stage \(t=1,\) (3.2.1), to move then to the choice problem for the platform at stage \(t=0,\) (3.2.2).

3.2.1 Stage \(t=1\): sellers’ choice

The derivation of equilibrium for the Cournot case yields the following values (the proof is in Appendix A):

By plugging (6) and (7) into \(U(\cdot )-\underset{k=1}{\overset{n_{s}}{\displaystyle \sum }}p_{k}^{*}q_{k}^{*}\), we obtain the net surplus for the consumer w as:

We can define \({\widetilde{\pi }}(n_{s},a)\equiv \frac{\left( 1+a\right) ^{2}}{ \left[ 2+\lambda (n_{s}-1)\right] ^{2}}\) and \({\widetilde{u}}(n_{s},a)\equiv \frac{\left( 1+a\right) ^{2}\left[ 1+\lambda (n_{s}-1)\right] }{2\left[ 2+\lambda (n_{s}-1)\right] ^{2}}\), so that we have:

3.2.2 Stage \(t=0\): platform choice

By plugging (3) and (4) into the platform profit function (5), we obtain:

Solving the maximization problem for the platform, we get the following necessary first order conditionsFootnote 6:

The necessary and sufficient second order conditions for a maximum requireFootnote 7:

with \(\gamma\) that must be "large enough" for (16–18) to be satisfied.Footnote 8

By inspection of (13)–(15) we can identify the forces that are at work in our model. In (13), the term \(n_{s}\left[ {\widetilde{u}}(n_{s},a)+{\widetilde{\pi }}(n_{s},a)\right] >0\) captures the positive cross-group effect for buyers; in (14), the term \(n_{b} \left[ {\widetilde{u}}(n_{s},a)+{\widetilde{\pi }}(n_{s},a)\right] >0\) is associated to the positive cross-group effect for sellers, while the term \(n_{s}n_{b} \left[ \frac{\partial {\widetilde{u}}(n_{s},a)}{\partial n_{s}}+\frac{\partial {\widetilde{\pi }}(n_{s},a)}{\partial n_{s}}\right] <0\) arises due to competition, and so it corresponds to a negative within-group effect. Such effects are already present in Belleflamme and Peitz (2019a), but in our setting their intensity depends upon the level of investment a. Finally \(n_{s}n_{b}\left[ \frac{\partial {\widetilde{u}}(n_{s},a)}{\partial a}+ \frac{\partial \widetilde{\pi }(n_{s},a)}{\partial a}\right] >0\) measures an investment effect, corresponding to the creation of value put forth by the platform through a. Such effect is absent in Belleflamme and Peitz (2019a).

3.3 Welfare analysis

We define social welfare (W) as the sum of three elements: i) platform profit, ii) sellers’ surplus, net of entry cost, and iii) buyers’ surplus, net of entry cost. In this section we first derive each of these elements, which we will be compared across different scenarios in Sects. 4 and 5; then, we consider constrained welfare maximization, i.e. we determine the social welfare maximization values of \(n_s\), \(n_b\), and a, assuming entry into the platform by both sellers and buyers as long as net surplus is positive.

The total net seller surplus is given byFootnote 9:

where the threshold \({{\underline{z}}}_s\), such that seller i joins the platform if \({z_i\le {\underline{z}}}_s\), is given by \({{\underline{z}}}_s=v_s=n_s\). It follows that total net surplus can be written as \(\frac{{n_s}^2}{2}\).

The total net buyer surplus is given by:

where the threshold \({{\underline{z}}}_b\), such that buyer i joins the platform if \({z_i\le {\underline{z}}}_b\), is given by \({{\underline{z}}}_b=v_b=n_b\). Similarly as before, it follows that total net surplus can be written as \(\frac{{n_b}^2}{2}\).

As a consequence, W is defined as:

Plugging equations for \(m_s\) and \(m_b\) into W, and simplifying we get

From the first order conditions for the maximization of W (see Appendix B), it follows that the number of sellers and buyers admitted by the monopolist platform is lower than the social optimum. Due to sellers’ and buyers’ heterogeneity, the platform faces the standard price-quantity trade-off: as a consequence, membership fees are too high from the social point of view.

4 Results

In Sect. 4.1, we analyse the role of seller competition intensity (inversely related to degree of product differentiation \(\lambda\)) and of investment productivity (inversely related to \(\gamma\)) in determining the optimal platform strategy, defined as the number of sellers and buyers admitted and the level of investment. We will refer to \(n_{b}+n_{s}\) as platform size and to a as platform quality. In Sect. 4.2, we examine the platform fees that support the optimal strategies. In Sect. 4.3, we investigate the impact of intensity competition and investment productivity on the welfare of all involved agents. In Sect. 4.4, we extend the model to include other forms of platform investment, and we also consider different models of competition, as well as the issue of transaction fees.

4.1 Platform strategy: the role of competition intensity and investment productivity

Although we specify functional forms for all our relations, using the standard approach based on the implicit function theorem on the first-order conditions system (13) - (15) did not provide clear-cut comparative statics results. For this reason, we made use of supermodularity analysis (Topkis 1978; Milgrom and Shannon 1994) to analyze how \(n_{b}\), \(n_{s}\), and a respond to variations in \(\lambda\) and \(\gamma\).Footnote 10 In fact, supermodular techniques, which for smooth functions rely only on second-order derivatives’ signs, identify in our case a set of important complementarity relations between the set of endogenous and (an appropriate transformation of) the exogenous parameter. \(n_{b}\), \(n_{s}\), and a are complementary to a given parameter if an increase in the latter increases the marginal return of the former, and, at the same time, all the cross-derivatives involving \(n_{b}\), \(n_{s}\), and a are positive, so that the three endogenous variables co-move upwards for higher values of the parameter. We define \(\lambda ^{^{\prime }}=-\lambda\), so that \(\lambda ^{^{\prime }}\) is directly related to the intensity of competition. Proposition 1 follows.

Proposition 1

\(n_{b}\), \(n_{s}\), and a are complementary to \(\lambda ^{\prime }=-\lambda\).

Proof

The proof is reported in Appendix A. \(\square\)

The intuition behind the proposition is straightforward. A lower intensity of competition reduces the negative within-group effect due to competition. As a consequence, the platform can admit more sellers, with a limited effect on their profitability, while extracting part of their surplus through relatively high membership fees. Due to positive cross-group effects, the platform finds it then convenient to admit more buyers as well. In a larger platform, the incentives to invest in quality increases (see (15)); which, in turn, increases the incentive to have a larger number of buyers and sellers who join the platform, since the a higher level of investment strengthens the positive cross-group effects.

Similarly, we define \(\gamma ^{^{\prime }}=\frac{1}{\gamma }\), so that \(\gamma ^{^{\prime }}\) is directly related to the degree of platform investment productivity, i.e., how easy is for the platform to increase its quality. Proposition 2 follows.

Proposition 2

\(n_{b}\), \(n_{s}\), and a are complementary to \(\gamma ^{\prime }=\frac{1}{\gamma }\).

Proof

The proof is reported in Appendix A. \(\square\)

The direct effect of a reduction in \(\gamma\) is obvious: a lower associated cost increases the investment in quality. Since both buyers’ and sellers’ payoffs are positively affected by quality investment, an increase in a makes the platform more attractive, with more buyers and sellers joining the platform; this, in turn, reinforces the incentive to invest in quality.

The results obtained imply that, in general, we should expect platform size and platform quality to move in the same direction. This result would be analogous to what could be obtained in a standard monopoly setting. In fact, low values of \(\lambda\) imply a low marginal “cost” for expanding size (as the negative impact of expanding \(n_{s}\) is limited); and the larger the size, the larger are the incentives to invest in activity that increase the price consumers are willing to pay. Similarly, low values of \(\gamma\) reduce the cost of expanding quality, leading to higher consumers’ willingness to pay. As a consequence, incentives to expand size are larger.

There results are in line with the anecdotal evidence we can observe in platform markets. Firms such as Amazon or Apple are well-known as having a market dominant position and a superior performance due to their investment in demand-enhancing features.

In the case of Amazon, the COVID-19 pandemic has represented a positive shock to demand, leading to an 38% increase in annual net sales revenue, against the 20% in the previous year (Statista 2024). In 2022, consistent with the prediction of our model, Amazon launched a 1 billion venture investment program called the Amazon Industrial Innovation Fund (AIIF), to spur and support innovation in customer fulfillment, logistics, and the supply chain.Footnote 11 As scholars found that an increase in delivery speed increases third-party sellers’ sales (Deshpande and Pendem 2023), we can expect Amazon sales to increase further. In addition, vertical integration of the delivery system, as the one carried on by Amazon, can be seen as a reduction of costs of the investment in logistics, since this increases the control over the transportation process, also allowing for stronger economies of scale. This choice is also expected to have a positive impact on size.

In the case of Apple, our result can be used to speculate about the impact of the EU Digital Market Act (DMA) on this company. The DMA requires to permit third-party app stores to sell and distribute apps on iOS systems (Crémer et al. 2024). This legal requirement could actually increase the number of developers offering innovative apps, whose diversification could be seen as a decrease of intensity of competition, possibly attracting even more developers and users. In that case, this could trigger investment in apps quality control (Caminade and Borck 2023), with a positive effect on platform attractiveness for buyers (and hence for sellers). At the same time, reduced costs of such investment would entail an additional positive effect on the number of buyers and sellers joining the platform, via the increase in the investment level.

Plots of \(n_s^*\), \(n_b^*\), and \(a^*\)

For further illustration, we present numerical simulations to observe the behaviour of the equilibrium levels of our endogenous variables \(n_{s}\), \(n_{b}\), and a. In particular, after having fixed values of \(r_{b}\), \(r_{s}\), and \(\gamma\), such that the SOCs (16–18) are always satisfied, we computed the value of the endogenous variables and of the other variables of interest for values of \(\lambda \in [0,1]\), with a step of 0.025 (41 runs for each simulation). The results of the numerical simulation with \(r_{b}=r_{s}=2\) for different levels of \(\gamma\), namely 6.55525, 10, 20, and \(\gamma \rightarrow \infty\) are reported in the Supplementary Material.Footnote 12Fig. 1 reports the four plots of \(n_{s}^{*}\), \(n_{b}^{*}\), and \(a^{*}\) as \(\lambda\) increases. As determined by Proposition 1 all the three variables are decreasing in \(\lambda\), besides \(a^{*}\) when \(\gamma \rightarrow \infty\).Footnote 13 Moreover, as \(\gamma\) increases, the endogenous variables decrease in \(\lambda\) at a lower pace. When \(\gamma\) is low, the investment level is more responsive to the factors affecting the return to investment, including the intensity of competition, and due to complementarity this affects also the number of buyers and sellers joining the platform in equilibrium.

4.2 Platform pricing

In this analysis, we were not able to get analytical results, so we resort to numerical simulations, using the same parameterization of the previous subsection.

Plots of \(m_s^*\) and \(m_b^*\)

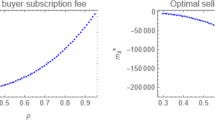

In Fig. 2 we report the behaviour of the equilibrium fees \(m_{s}^{*}\) and \(m_{b}^{*}\) as \(\lambda\) increases, for various levels of \(\gamma\). As we can see, the seller fees are always increasing in \(\lambda\), besides for the situation in which \(\gamma\) is at (around) the minimum value that allows for having the SOCs respected, in which the fees are first decreasing (up to a value of \(\lambda\) between 0.075 and 1) and then increasing again in \(\lambda\). For what concerns the buyer’s fee we note that \(m_{b}^{*}\) is always decreasing in \(\lambda\) for \(\gamma =6.55525\) and for \(\gamma\) equal to 10. For higher values of \(\gamma\), there is maximum in the support [0, 1]. This maximum is in correspondence with a higher value of \(\lambda\) as \(\gamma\) increases.

There are a number of implications we can derive from Fig. 2. First, membership fees for sellers are always higher than those for buyers. This occurs because the platform prefers to expand the size by admitting relatively more buyers than sellers since the latter are associated with a negative within-group effect due to competition which is absent for the former. Second, additional insights are obtained if we consider these results together with those obtained in Sect. 4.1. If we fix the value of \(\gamma\), we know that platform quality is relatively large if \(\lambda\) is low, and small if \(\lambda\) is high. This implies that, if we compare platforms of different quality due to different competitive environments, higher quality is associated with lower fees for sellers, but higher for buyers. In other words, the platform captures value disproportionally from buyers. However, if quality differs because of different investment productivities, higher quality is associated with higher fees both for sellers and buyers.

4.3 Welfare: platform profit and participants’ net surplus

As for the sellers’ and buyers’ net surplus are concerned, in Sect. 3.3 we showed how both sellers’ and buyers’ net surplus are increasing in the number of sellers and buyers respectively. As in Sect. 4.1 we showed that \(n_{b}\) and \(n_{s}\) are decreasing in \(\lambda\) and in \(\gamma\), it follows that both sellers’ and buyers’ net surplus are decreasing in \(\lambda\) and in \(\gamma\) as well.

Concerning the platform, we obtained analytical results for its profitability, summarized in Proposition 3.

Proposition 3

Platform profit is decreasing in \(\lambda\) and \(\gamma\).

Proof

The proof is contained in Appendix A. \(\square\)

The interpretation of Proposition 3 relies heavily upon what we showed above. A lower intensity of competition and a higher investment productivity makes the platform more profitable because they both trigger mutually reinforcing effects involving larger size (more sellers and buyers joining the platform) and higher quality. In other words, platforms hosting sellers with highly differentiated products are expected to be of larger size, higher quality and higher profitability. For illustration, Fig. 3 reports numerical simulations for the equilibrium values of sellers’ and buyers’ net surplus and platform profit, based on the same parameter values as before. As one can see, the steepness of the lines changes too as \(\gamma\) increases, with a lower degree of convexity for all three lines.

Plots of the net surplus of the seller (red, left axis), the net surplus of the buyer (black, left axis), and the platform’s profit (blue, right axis)

Economically speaking, a higher competition intensity between the sellers reduces their surplus, as one could expect, but it also reduces the buyer surplus and the platform’s profit. The former result, also present in Belleflamme and Peitz (2019a), is the net impact of a positive effect due to price reduction, and a negative effect due to lack of product variety. As for the latter result, we observe that the platform, in order to reduce the magnitude of the negative within-group effect, fixes higher fees to sellers, reducing their number in the platform. However, this reduces for the platform the incentive to invest, and for both reasons a lower number of buyers are willing to enter the market, shrinking the demand. Consequently, the platform tries to attract more buyers by reducing their fees, to avoid their utility to decrease too much. However, this strategy does not compensate for the loss of profit due to the reduction of the number of sellers inside the market.Footnote 14

A similar issue occurs when the cost of investment increases. In fact, a higher cost will reduce investment, and hence the demand and sellers’ profits. Notwithstanding the reduction in the membership fee for sellers, their number will be lower, and buyers’ surplus will shrink due to a reduction both in quality and number of sellers. A smaller size would entail a lower profit for the platform.

4.4 Extensions: other forms of platform investment, competition, and fees

The results obtained so far are robust to different assumptions concerning the nature of platform investment and competition. Consider cost-reducing investment first.Footnote 15 Assume that \(A={\bar{A}}\) and \(c={\overline{c}}-\theta\), where \(\theta\) is the investment in process innovation by the platform, and \({\bar{A}}\) \(-{\overline{c}}=1\). All the analysis so far goes unchanged. Alternatively, suppose the platform investment can reduce \(\lambda\), thus increasing the degree of product differentiation (as in Lin and Saggi 2002).Footnote 16 If the investment gets more productive, the platform will invest more, \(\lambda\) will be lower, and \(n_{s}\) and \(n_{b}\) will be higher so that the complementarity result is confirmed.

Another relevant form of platform investment is advertising. Following Zhou et al. (2022), there are three advertising schemes for a two-sided platform with a buyer side and a seller side: no advertising on both sides; advertising on a single side; and advertising on both sides. For example, advertising represents one of the leading instruments for brand investment of several food delivery platforms and online travel agencies. In the Supplementary Material, we represent advertising as an investment that increases stand-alone utility for buyers, thus corresponding to a form of persuasive advertising (Belleflamme and Peitz 2015).Footnote 17 The main results are unaffected, in particular those concerning complementarity. However, the result now hinges only upon the direct effect that investment has on the net surplus of one side of the market, without influencing the intensity of cross-group effects.

Results are also robust also to different modelling assumptions as for competition is concerned. In particular, results are unaffected if considering monopolistic competition with consumers having CES preferences over differentiated products. Similarly, assuming Bertrand’s competition instead of Cournot is inconsequential if the degree of product differentiation is sufficiently small.Footnote 18

Finally, in our setting, a general analysis of transaction fees turns out to be intractable. This is of course a limitation of our work, given the relevance of transaction fees in practice. However, we were able to analyze the special setting of one-sided pricing (in which transaction fees are levied on sellers only) with \(\lambda\) small. In this context, our results continue to hold.Footnote 19

5 Hybrid platform

In this section, we consider the case of a hybrid platform, in which the platform offers its product in competition with independent sellers. Following the literature, we will also refer to this as a dual mode. We will compare the outcomes with those derived in Sect. 4 for a pure marketplace, along the lines of Anderson and Bedre-Defolie (2021) and Hagiu et al. (2022). For the sake of simplicity, we assume that the product offered by the platform is symmetric with respect to those offered by independent sellers. We continue to denote with \(n_{s}\) the number of independent sellers operating in the market so that \(n_{s}+1\) is the total number of sellers (products) that are offered on the platform. The number of independent sellers and buyers joining the platform become:

where the H superscript will be used from now on to denote all the endogenous variables when the platform offers its product. It follows that:

Platform profit will derive then from the membership fees and the net surplus from joining the platform obtained by the seller “owned” by the platform (which does not pay the membership fees). After having considered the cost for the demand-enhancing investment a, this yields:

By plugging (19) and (20) into the platform profit function (21), we obtain:

The first result we find is that the platform obtains a higher profit when offering its product. To see this, we can compare \(\Pi _{P}^{{}}\) and \(\Pi _{P}^{H}\) for \(n_{b}^{H}=n_{b},a_{{}}^{H}=a\) and \(n_{s}^{H}=n_{s}-1\), where \(n_{s},n_{b}\) and a stand for generic values in a pure marketplace case, and \(n_{s}^{H},n_{b}^{H}\) and \(a^{H}\) in the case of a hybrid platform. \(\Pi _{P}^{H}>\Pi _{P}^{{}}\) reduces to \(2n_{s}-1>0\), which is always satisfied. The intuition is straightforward, in that the platform offering its product obtains the gross surplus of joining the platform for the seller, which is always higher than the membership fee can obtain from an independent seller.

Solving the maximization problem for the platform, we get the following necessary first order conditions:

If we evaluate the first order conditions (23)–( 25) at the values \(n_{s}^{H}=n_{s}^{*}-1,n_{b}^{H}=n_{b}^{*}\) and \(a^{H}=a^{*}\) (where \(n_{s}^{*},n_{b}^{*}\) and \(a^{*}\) are the solution of the system (13)–(15)) we obtain:

Such conditions imply that a hybrid platform has the incentive to increase the total number of sellers operating in the market, compared to a pure marketplace case. In the former case, the platform can fully appropriate the surplus generated by one seller, while appropriation is partial in the latter.

It is straightforward to prove that all the second derivatives for \(\Pi _{P}^{H}\) (as those computed in Lemmas 1 and 2) are equivalent to those for \(\Pi _{P}^{{}}\), evaluated in \(n_{s}+1\), with \(n_{s}>0.\) The signs are thus the same. Since \(\frac{\partial ^{2}\Pi _{P}^{H}}{\partial n_{b}\partial n_{s}}>0\), \(\frac{\partial ^{2}\Pi _{P}^{H}}{ \partial n_{b}\partial a}>0\), and \(\frac{\partial ^{2}\Pi _{P}^{H}}{\partial n_{s}\partial a}>0\), an increase in \(n_{s}\) leads to an increase in \(n_{b}\) and a. Therefore, hybrid platforms make buyers better off. The impact on sellers’ net surplus, instead, is ambiguous. For sellers, the negative effect of an increase in competition may be compensated by the positive effect of a larger number of buyers and a higher level of investment. Figure 4 reports the difference between the seller net surplus in the hybrid case compared to the pure marketplace case. It turns out that such a difference is positive whenever \(\lambda\) is low enough. In addition, the threshold is higher the lower the value of \(\gamma\). The economic intuition is straightforward: if products are sufficiently differentiated, the negative “competition effect” for independent sellers resulting from a hybrid platform is limited. Similarly, Fig. 5 compares welfare, which turns out to be always higher in the hybrid platform case.Footnote 20

Plots of the difference of the seller surplus in case of the hybrid platform and in the marketplace case, for \(\gamma =6.55525\) (black), 10 (red), 20 (blue), and \(\infty\) (green). The horizontal dashed line is on the value 0

Plots of the difference of welfare in case of hybrid platform and in the marketplace case, for \(\gamma =6.55525\) (black), 10 (red), 20 (blue), and \(\infty\) (green)

6 Discussion and conclusions

In this section, we discuss the main implications for platform managers and the policy implications of our model. In the final conclusions, we highlight our contribution on the platform literature and suggest further extensions to be studied.

6.1 Discussion: managerial implications

Our results suggest several managerial implications. The first concerns the role of demand-enhancing investments as an instrument for value creation. We show that the return of such investments depends crucially on the sellers’ competitive environment. Therefore firms should conceive their investment policy upon a clear understanding of the nature of competition on the platform. In addition, if platforms can have an impact on the actual (or perceived) degree of product differentiation in the market, they should accompany investments with interventions aimed at increasing it. In addition, investment turns out to be complementary to the decision to offer first-party content in a hybrid platform setting. In our case, the dual mode has simultaneously the effect of enhancing platform quality and allowing the platform to appropriate fully the value generated by one product (Zhu 2019).

The second implication concerns value capture, or monetization. Our results on the optimal membership fees suggest that the best way for platforms to appropriate the return of investment depends on which factors prevail in determining the level of investment. If platform quality is “high” because of idiosyncratic R &D capabilities, corresponding to low values of \(\gamma\) in our model, the platform can take advantage of its competitive advantage by raising fees on both sides of the market. If, instead, large investments are driven by low intensity of competition in the final market, the platform should capture value on the buyers’ side, while keeping the membership fees for sellers low to incentivize their decision to join the platform. Finally, our results could help management in making decisions for successful platform launches. On one hand, we showed that demand-enhancing investments reinforce the cross-group effects; therefore, they should be considered complementary to those strategies that the management literature has identified to overcome the well-known “chicken-or-egg” problem (e.g., Parker et al. 2016).Footnote 21 On the other hand, our model suggests that also the profitability of a platform business idea depends on the nature of the resulting competitive environment on the platform. As a consequence, this factor should be taken into consideration when developing (or financing) a platform business idea or another.

6.2 Discussion: policy implications

Our model provides a few lessons also in the realm of policy. At a general level, our results suggest the importance of considering how policy interventions could impact the return to demand-enhancing (including technological) investment, much in line with the traditional discussion of static vs dynamic efficiency in competition and regulation policy. The specific case we investigate concerns hybrid platforms. Much of the recent literature on the theme had been motivated by a policy research question, i.e. if platforms should be allowed or not to sell on their marketplaces (Hagiu et al. 2022), also motivated by an actual debate in the US and abroad. Focusing on consumers’ welfare, some works suggest that a ban on the dual mode could harm consumers (Hagiu et al. 2022; Etro 2023), while others find the opposite result (Anderson and Bedre-Defolie 2022). In that respect, our paper identifies a new mechanism (investment), through which a ban of the dual mode could in fact harm not only consumers but sellers as well, and unambiguously would reduce social welfare. Similar considerations could emerge for other platform business practices that, in principle, could be the object of regulation. For instance, the literature has suggested that in the presence of competition among sellers, a platform may recommend products so that consumer search is discouraged, and competition is relaxed (Chen and He 2011; Eliaz and Spiegler 2011). However, lower intensity of competition may increase the incentives towards investment, favouring consumers. Along the same lines, platform sharing of customer personal data with sellers may increase sellers’ profit, as this lead to the offer of customized products. Consumers may be worse off if customization comes with a lower fraction of surplus accruing to them (Belleflamme and Peitz 2021). However, this result is less likely if the return to investment increases with customization, as it is likely the case.

6.3 Conclusions and the way ahead

The model developed in this paper is a contribution to the burgeoning literature on the interaction between price and non-price strategies in platform design. There are several extensions that we could explore in the future. The first one is to move from a monopolistic platform to platform competition (Rietveld and Schilling 2021). In this context, we could compare the results of setting with simultaneous choices of investment and fees, with those of a two-stage game, in which investment in quality in the first stage can affect platform competition in the second stage through a strategic effect. In a competitive setting, following Halaburda and Yehezkel (2019) and Halaburda et al. (2020), we could consider investment in quality as non-price strategies of focal and non-focal platforms, and the effect of focality on the equilibrium. Additional themes for analysis under competition could include the role of platform vertical differentiation (Gabszewicz and Wauthy 2014; Angelini et al. 2021), platform investment in single-homing and multi-homing context (Jeitschko and Tremblay 2020; Geng et al. 2023) and behaviour-based price discrimination (Carroni 2018). A second extension could be to consider the existence of alternative sales channels for sellers and to investigate to what extent contractual conditions such as price parity clauses affect investment incentives (Mantovani et al. 2021).

Notes

Another branch of the platform literature has considered focality as a key parameter. The concept of platform focality is defined by Caillaud and Jullien (2003) and extended by Halaburda and Yehezkel (2019) to model platform competition when one of the platforms benefits from a focal position. The advantage of the focal platform consists of dominating the market since each agent has fulfilled the expectations of the other agents’ beliefs. In forming their beliefs, each agent expects that any other agent will join the focal platform whenever prices are set by the focal platform. If an equilibrium exists, the low-price strategies of a non-focal platform do not affect the equilibrium. As the notion of focality is strictly related to competition among platforms, we return to this point in the conclusion when discussing future avenues for research. We thank an anonymous reviewer for this suggestion.

A recent work by Lefouili and Madio (2022) investigates how changes in platform liability can impact its investment choices, both in harm prevention and innovation. The latter can happen either through a direct effect, when liability increases the platform’s incentive to invest, or an indirect effect, in case a more stringent liability regime can rise the entry barrier and then reduce platform competition, affecting the platform’s incentive to innovate.

This quasi-linear quadratic utility function is the same used in Belleflamme and Peitz (2019a). It is widely adopted in industrial organization for tractability, since linear demand functions are derived from the representative consumer’s maximization problem, and it requires the negative terms to obtain concavity. We also observe that the concerns raised by Amir et al. (2017) do not apply to our case, since we restrict our attention to the substitute products case. See also Choné and Linnemer (2019) for a historical overview.

Under monopoly, a setting in which the platform would choose the investment level before the membership fees would be inconsequential, leading to (13)–(15) as first order conditions. The choice of a would affect platform second-stage choices, but in equilibrium the impact on profit is nil due to the envelope theorem (see Belleflamme and Peitz (2015) for formal treatment of a similar argument concerning R &D investment in oligopoly). Things would change in presence of competition between platforms, where investment in the first stage would induce also a strategic effect. We will return on this point in the conclusions.

We observe that in the left side of inequality (18), the second term is positive, while the third and the fourth terms are negative, based on the results shown in Appendix A. Since condition (17) must be satisfied as well, \(\frac{\partial ^{2}\Pi _{P} }{\partial a^{2}}\) must be "sufficiently negative" for (18) to be satisfied. This requires \(\gamma\) to be "large". If not, the complementarity among \(n_{b}\), \(n_{s}\), and a (see Sect. 4.1) would lead the platform to increase the investment indefinitely.

Inframarginal sellers make a positive net surplus, notwithstanding free entry, to due seller heterogeneity. The same occurs to buyers.

See Amir (2005) for a survey on supermodularity and complementarity.

Quoting from the Amazon Website (2024): "As customers increasingly shop online [emphasis added] and look for even faster delivery, Amazon continues to invent new ways to raise the bar on customer and employee experience (...)".

6.55525 is an approximation of the minimum value of \(\gamma\) that satisfies the SOCs when \(r_{s}=r_{b}=2\), for any value of \(\lambda\). We approximate \(\gamma \rightarrow \infty\) by fixing \(\gamma =10^{12}\).

Obviously, in the last case, the platform never invests, independently of the intensity of competition.

This result hinges upon the specific functional form adopted for the linear demand functions, which implies that total market size increases as the number of sellers (and thus products) increases. If that is not the case, only the price effect is present and so an increase in product differentiation has a negative effect on buyers. See the Supplementary Material for further details.

For instance, platforms can invest in technologies that improve the back-office activities of sellers.

For instance, tools offered by online video platforms may allow creators to differentiate their content.

Chiaromonte (2019) highlights how the informative function of advertising has lost importance in the digital age, since consumers can get information about almost all goods from the web, making advertising made by digital platforms mostly persuasive.

See the Supplementary Material for details.

See the Supplementary Material for details.

For comparability with the previous plots, in these Figures we consider the same parameterization used in the pure marketplace case. However, for the hybrid case, second order conditions require \(\lambda\) to be above a threshold for low values of \(\gamma\) (\(\gamma =6.55525\) and \(\gamma =10\)). This explains the curves’ behavior in the plots.

We observe that some of these strategies may be accommodated in our model as well. It is the case of the “big-bang adoption strategy” ( Parker et al. 2016, p. 97), basically corresponding to one of the extensions mentioned in Sect. 4.4, where investment increases the stand-alone utility of joining the platform.

References

Amazon Website (2024) Introducing the $1 billion Amazon industrial innovation fund. Accessed 11 Mar 2024. https://www.aboutamazon.com/news/innovation-at-amazon/introducing-the-1-billion-amazon-industrial-innovation-fund

Amir R (2005) Supermodularity and complementarity in economics: an elementary survey. South Econ J 71(3):636–660

Amir R, Erickson P, Jin J (2017) On the microeconomic foundations of linear demand for differentiated products. J Econ Theory 169:641–665

Anderson SP, Bedre-Defolie O (2021) Hybrid platform model. CEPR discussion paper no. DP16243

Anderson SP, Bedre-Defolie O (2022) Online trade platforms: hosting, selling, or both? Int J Ind Organ 84:102861

Anderson EG Jr, Parker GG, Tan B (2014) Platform performance investment in the presence of network externalities. Inf Syst Res 25(1):152–172

Angelini F, Benassi C, Castellani M (2021) Platform competition and willingness to pay in a vertical differentiated two-sided market. Econ Bull 41(2):772–780

Armstrong M (2006) Competition in two-sided markets. Rand J Econ 37(3):668–691

Baye MR, Morgan J (2001) Information gatekeepers on the Internet and the competitiveness of homogeneous product markets. Am Econ Rev 91(3):454–474

Belleflamme P, Peitz M (2010) Platform competition and seller investment incentives. Eur Econ Rev 54(8):1059–1076

Belleflamme P, Peitz M (2015) Industrial organization: markets and strategies, 2nd edn. Cambridge University Press, Cambridge

Belleflamme P, Peitz M (2019a) Managing competition on a two-sided platform. J Econ Manag Strategy 28(1):5–22

Belleflamme P, Peitz M (2019b) Platform competition: who benefits from multihoming? Int J Ind Organ 64:1–26

Belleflamme P, Peitz M (2021) The economics of platforms. Cambridge University Press

Belleflamme P, Toulemonde E (2009) Negative intra-group externalities in two-sided markets. Int Econ Rev 50(1):245–272

Belleflamme P, Toulemonde E (2016) Who benefits from increased competition among sellers on B2C platforms? Res Econ 70(4):741–751

Boudreau KJ, Hagiu A (2009) Platform rules: multi-sided platforms as regulators. In: Gawer A (ed) Platforms, markets and innovation. Edward Elgar, pp 163–191

Caillaud B, Jullien B (2003) Chicken & egg: competition among intermediation service providers. Rand J Econ 34(2):309–328

Caminade J, Borck J (2023) The continued growth and resilience of Apple’s App store ecosystem. Analysis group report. https://www.apple.com/newsroom/pdfs/the-continued-growth-and-resilience-of-apples-app-store-ecosystem.pdf. Accessed 6 Mar 2024

Carroni E (2018) Behaviour-based price discrimination with cross-group externalities. J Econ 125:137–157

Casadesus-Masanell R, Llanes G (2015) Investment incentives in open-source and proprietary two-sided platforms. J Econ Manag Strategy 24(2):306–324

Cennamo C, Santaló J (2019) Generativity tension and value creation in platform ecosystems. Organ Sci 30(3):617–641

Chen Y, He C (2011) Paid placement: advertising an search on the Internet. Econ J 121(556):309–328

Chiaromonte N (2019) Essay on advertising in digital platforms and their taxation. Unpublished doctoral dissertation. Università degli Studi di Milano

Choné P, Linnemer L (2019) The quasilinear quadratic utility model: an overview. CESifo working paper no. 7640. https://www.cesifo.org/DocDL/cesifo1_wp7640.pdf. Accessed 10 Mar 2024

Crémer J, Heidhues P, Schnitzer M, Scott Morton F (2024) Apple’s exclusionary app store scheme: an existential moment for the Digital Markets Act. Retrieved 7 Mar 2024 from Voxeu at https://cepr.org/voxeu/columns/apples-exclusionary-app-store-scheme-existential-moment-digital-markets-act

Cui R, Li M, Li Q (2020) Value of high-quality logistics: evidence from a clash between SF Express and Alibaba. Manag Sci 66(9):3879–3902

Deshpande V, Pendem PK (2023) Logistics performance, ratings, and its impact on customer purchasing behavior and sales in e-commerce platforms. Manuf Serv Oper Manag 25(3):827–845

Eliaz K, Spiegler R (2011) A simple model of search engine pricing. Econ J 121(556):F329–F339

Etro F (2021a) Device-funded vs ad-funded platforms. Int J Ind Organ 75:102711

Etro F (2021b) Product selection in online marketplaces. J Econ Manag Strategy 30:614–637

Etro F (2023) Hybrid marketplaces with free entry of sellers. Rev Ind Organ 62:119–148

Gabszewicz JJ, Wauthy XY (2014) Vertical product differentiation and two-sided markets. Econ Lett 123(1):58–61

Geng Y, Zhang Y, Li J (2023) Two-sided competition, platform services and online shopping market structure. J Econ 138:95–127

Hagiu A (2009) Two-sided platforms: Product variety and pricing structures. J Econ Manag Strategy 18(4):1011–1043

Hagiu A, Spulber D (2013) First-party content and coordination in two-sided markets. Manag Sci 59(4):933–949

Hagiu A, Teh T-H, Wright J (2022) Should platforms be allowed to sell on their own marketplaces? Rand J Econ 53:2297–327

Halaburda H, Yehezkel Y (2019) Focality advantage in platform competition. J Econ Manag Strategy 28(1):49–59

Halaburda H, Jullien B, Yehezkel Y (2020) Dynamic competition with network externalities: how history matters. Rand J Econ 51(1):3–31

Jeitschko TD, Tremblay MJ (2020) Platform competition with endogenous homing. Int Econ Rev 61(3):1281–1305

Jullien B, Sand-Zantman W (2021) The economics of platforms: a theory guide for competition policy. Inf Econ Policy 54:100880

Karle H, Peitz M, Reisinger M (2020) Segmentation versus agglomeration: competition between platforms with competitive sellers. J Polit Econ 128(6):2329–2374

Kretschmer T, Leiponen A, Schilling MA, Vasudeva G (2022) Platform ecosystems as meta-organizations: implications for platform strategies. Strateg Manag J 43(3):405–424

Lefouili Y, Madio L (2022) The economics of platform liability. Eur J Law Econ 53:319–351

Lin P, Saggi K (2002) Product differentiation, process R &D, and the nature of market competition. Eur Econ Rev 46(1):201–211

Liu Q, Nedelescu D, Gu J (2021) The impact of strategic agents in two-sided markets. J Econ 134:195–218

Mantovani A, Piga CA, Reggiani C (2021) Online platform price parity clauses: evidence from the EU Booking.com case. Eur Econ Rev 131:103625

Milgrom P, Shannon C (1994) Monotone comparative statics. Econometrica 62(1):157–180

Parker G, Van Alstyne M, Choudary S (2016) Platform revolution. WW Norton & Company

Rietveld J, Schilling MA (2021) Platform competition: a systematic and interdisciplinary review of the literature. J Manag 47(6):1528–1563

Schilling MA (2003) Technological leapfrogging: lessons from the US video game console industry. Calif Manag Rev 45(3):6–32

Statista (2024) Amazon—statistics & facts. https://www.statista.com/topics/846/amazon/. Accessed 11 Mar 2024

Tan B, Anderson EG Jr, Parker GG (2020) Platform pricing and investment to drive third-party value creation in two-sided networks. Inf Syst Res 31(1):217–239

Teh T-H (2022) Platform governance. Am Econ J Microecon 14(3):213–254

Topkis DM (1978) Minimizing a submodular function on a lattice. Oper Res 26(2):305–321

Zhou Y, Zhang Y, Wahab M (2022) Optimal pricing and choice of platform advertising schemes considering across-side network effect. Manag Decis Econ 43(4):1059–1079

Zhu F (2019) Friends or foes? Examining platform owners’ entry into complementors’ spaces. J Econ Manag Strategy 28(1):23–28

Acknowledgements

Previous versions of this paper have been presented at SIE 2019, JEI 2019, ASSET 2019, SIE 2021, XII NERI Workshop 2022, and EARIE 2022.

Funding

Open access funding provided by Università degli Studi di Milano within the CRUI-CARE Agreement. No funding was received to assist with the preparation of this manuscript.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Appendices

Appendix A: Proofs

This appendix contains a series of results used in the proofs of the Propositions and the proofs themselves.

1.1 Sellers maximization problem

The seller k in our game maximize the function, with respect to \(q_k\), as reported in Sect. 3.1:

Here, as in the main text, \(q_{-k}=\sum _{g\ne k} q_g\).

The FOC for seller k is equal to:

Denoting with \(q_k^*\) the equilibrium quantity, for symmetry we have \(q_{-k}^*=(n_s-1)q_k^*\). This leads to:

Substituting the equilibrium quantity in the inverse demand function, we get:

Notice that, since we assumed \({\bar{A}}-c=1\), this boils down to:

1.2 Lemmas

Lemma 1

Starting from (13–15) we obtain the second order derivatives for the endogenous variables as follows:

Proof

The proof is straightforward. \(\square\)

Lemma 2

The second order derivatives considering exogenous parameters \(\lambda\) and \(\gamma\) are:

Proof

The proof is straightforward. \(\square\)

Lemma 3

By (10) and (11) we have, for sellers and buyers:

By (15) and for \(n_{s}\ge 1\) and \(0\le \lambda \le 1\) we have for the platform:

Proof

The proof is straightforward. \(\square\)

1.3 Proofs of Propositions

Proof of Proposition 1

Since \(\lambda ^{\prime }=-\lambda\), \(\frac{\partial ^{2}\Pi _{P}}{\partial n_{b}\partial \lambda }=-\frac{\partial ^{2}\Pi _{P}}{ \partial n_{b}\partial \lambda ^{\prime }}\), \(\frac{\partial ^{2}\Pi _{P}}{ \partial n_{s}\partial \lambda }=-\frac{\partial ^{2}\Pi _{P}}{\partial n_{s}\partial \lambda ^{\prime }}\), and \(\frac{\partial ^{2}\Pi _{P}}{\partial a\partial \lambda }=-\frac{\partial ^{2}\Pi _{P}}{\partial a\partial \lambda ^{\prime }}.\) Therefore, based on the preliminary results reported above, we obtain:

for \(n_{s}\ge 1\) and \(0\le \lambda \le 1\).

Supermodularity follows.

Proof of Proposition 2

In addition to what we show above, it follows from:

This ends the proof.

Proof of Proposition 3

By means of the envelope theorem, we obtain:

This completes the proof.

Appendix B: Welfare analysis

The first order conditions for the maximization of W are as follows:

If we plug the values \(n_s^*\), \(n_b^*\), and \(a^*\) that satisfy the first order conditions for platform profit maximization from equations (13), (14), and (15) into (B.1), (B.2), and (B.3), we obtain:

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Angelini, F., Castellani, M. & Zirulia, L. Platform investment and seller competition in two-sided markets. J Econ (2024). https://doi.org/10.1007/s00712-024-00874-x

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s00712-024-00874-x