Abstract

We apply a dynamic stochastic control (DSC) approach based on an open-loop linear feedback policy to a classical asset-liability management problem as the one faced by a defined-benefit pension fund (PF) manager. We assume a PF manager seeking an optimal investment policy under random market returns and liability costs as well as stochastic PF members’ survival rates. The objective function is formulated as a risk-reward trade-off function resulting in a quadratic programming problem. The proposed methodology combines a stochastic control approach, due to Primbs and Sung (IEEE Trans Autom Control 54(2):221–230, 2009), with a chance constraint on the PF funding ratio (FR) and it is applied for the first time to this class of long-term financial planning problems characterized by stochastic asset and liabilities. Thanks to the DSC formulation, we preserve the underlying risk factors continuous distributions and avoid any state space discretization as is typically the case in multistage stochastic programs (MSP). By distinguishing between a long-term PF liability projection horizon and a shorter investment horizon for the FR control, we avoid the curse-of-dimensionality, in-sample instability and approximation errors that typically characterize MSP formulations. Through an extended computational study, we present in- and out-of-sample results which allows us to validate the proposed methodology. The collected evidences confirm the potential of this approach when applied to a stylized but sufficiently realistic long-term PF problem.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

We consider an asset-liability management (ALM) model for a defined benefit (DB) open pension fund (PF) in which we assume a PF manager seeking an optimal dynamic investment strategy under a set of asset and liability constraints. This class of Institutional ALM problems is well known and it has been studied under several modeling approaches. We are here primarily interested on the assumptions governing the problem underlying probability space and the associated optimization approaches: in particular in presence of a discrete probability space, a long-term ALM problem finds a natural formulation as a multistage stochastic program (MSP), see Abdelaziz et al. (2007), Consigli and Dempster (1998), Geyer and Ziemba (2008), Mulvey and Ziemba (1998), Pflug and Świetanowski (1999), and Ziemba (2007). Alternatively, without a precise specification of underlying stochastic factors, robust optimization (RO) approaches allow for the introduction of uncertainty sets in which the problems’ random parameters are assumed to vary, see (Ben-Tal et al. 2000) and more recently (Gülpinar and Pachamanova 2013). Distributionally robust optimization (DRO) methods have been proposed in recent years, where the uncertainty model doesn’t require the specification of a probability measure, as further clarified below in this introduction. Finally, preserving an assumption of a continuous probability space, different formulations of a dynamic stochastic control (DSC) problem are possible.

In this article we assume a continuous probability distribution and consider an open-loop predictive control approach to solve the problem through a semi-definite programming formulation which is extended to accommodate a chance constraint on the PF funding ratio. The chance-constrained DSC method we consider finds its rationale in the context of an ALM problem formulation, as we try to make clear in what follows.

As for existing approaches, in the presence of realistic PF ALM problem instances, MSP formulations are able to accommodate a rich set of assumptions and market details, see Consigli et al. (2017), Duarte et al. (2017) and Moriggia et al. (2019), and they have also been formulated with probabilistic constraints, starting with (Haneveld et al. 2010) where integrated chance constraints (ICC) were introduced and then by Toukourou and Dufresne (2018). This problem formulation, due to the discrete scenario tree representation, is known to face a possible curse of dimensionality, the problem’s in-sample instability (Kaut and Wallace 2007) and approximation errors (Maggioni and Pflug 2016, 2019). The first two represent a non trivial trade-off with significant numerical implications. Furthermore in presence of specific modeling and statistical assumptions for scenario tree generation, MSP approaches carry a significant model risk that may lead to inefficient decision processes. Within a discrete multistage model, ICC have proven effective in terms of accuracy and flexibility (Duarte et al. 2017).

An alternative is represented by RO methods, in which uncertain problem coefficients are constrained to be inside deterministic uncertainty sets. This approach was recently applied to a dynamic ALM problem by Gülpinar and Pachamanova (2013) and specifically to a PF problem by Pachamanova et al. (2016) and Iyengar and Ma (2016). In Pachamanova et al. (2016) a comparison with an MSP formulation and solution method was also presented. Following (Pachamanova et al. 2016), the PF problem can be reformulated in a convex way and efficiently solved with interior-point methods. In Iyengar and Ma (2016) the authors, noticeably in this context, extend the approach to propose a chance constrained robust model. Chance constraints are here approximated by a Bonferroni inequality leading, as common in RO problems, to a second-order conic programming (SOCP) formulation. A possible drawback of RO models has emerged however due to the difficulty to accommodate long-term market dynamics in a consistent uncertainty set specification, often leading to very conservative portfolio policies with poor out-of-sample performance (Consigli et al. 2016a). In this article, we approximate a chance constraint on the FR through a \({\check{C}}eby{\check{s}}\ddot{e}v\) inequality.

The drawbacks of the previous two approaches may in principle be overcome through distributionally robust optimization (DRO) methods pioneered in Zácková (1966). The DRO approach can be regarded as a generalization of MSP and RO, accounting for both the decision maker’s attitude to risk and ambiguity. A growing literature in this direction both from theoretical and applied point of view can be found in Chang et al. (2017), Consigli et al. (2016b) and Liu et al. (2018), also specifically for financial management problems but mostly limited to the solution of static, one-period, problems (Pflug and Wozabal 2007; Delage and Ye 2010; Paç and Pınar 2014; Zhu and Fukushima 2009). To date dynamic DRO approaches have typically considered adaptive decisions in the form of so-called decision rules (Georghiou et al. 2015; Kuhn et al. 2011). Unfortunately the decision rules approximation is not suitable for a PF ALM problem formulation characterized by uncertain return coefficients multiplying adaptive decisions.

Going back to the risk factors’ continuous probability space assumption, stochastic control approaches provide a viable methodology for purely asset allocation problems but have not been previously applied to ALM PF problems, primarily because of the unrealistic limits they impose on the decision space. Yet, following (Herzog et al. 2006) where a model predictive control was applied to a dynamic asset allocation problem with Value-at-Risk (VaR) constraints, this approach, even if very occasionally, has been applied to financial decision problems. An optimal control formulation based on a specific affine parametrization of the recourse policy, for instance, has been considered in Calafiore (2008) for a multi-period financial asset allocation problem but yet with no liabilities involved, a short term planning horizon and no chance constraints.

In this article, along this line of research, we apply a linear plus open-loop recursive control approach to a constrained linear system with a chance constraint on the PF’s FR, rather than on the VaR, and show that this methodology is suitable to solve a sufficiently realistic and operational PF problem. We follow pretty closely the approach proposed in Primbs and Sung (2009) which, however, is extended to consider a probabilistic constraint on the PF solvency condition. As mentioned, the chance constraint is here approximated by a \({\check{C}}eby{\check{s}}\ddot{e}v\) inequality: this is a choice primarily motivated by the possibility to accommodate alternative distributional assumptions on assets’ return processes fixing only their mean and variance-covariance matrix, and also by the evidence that such approximation may turn out to be conservative (Peng et al. 2021), a positive feature in presence of a risk control problem. We present a set of evidences in a case-study on this very point. Alternative formulations of probabilistic constraints may employ either other types of inequality (Iyengar and Ma 2016; Peng et al. 2021) or implement directly some form of cardinality constraints (Curtis et al. 2018).

The chance constraint on the FR is further motivated by the evidence that none of previous modelling efforts tackled in a sufficiently effective and realistic way the regulatory constraints that in practice affect any operational PF problem: the sector’s social implications indeed over the years (EIOPA 2018; OECD 2011) have led in most advanced pension systems to the introduction of minimal PF funding levels.

To the best of our knowledge, the approach developed in this article, has never been applied to a PF ALM problem, despite the centrality of the PF solvency constraints and the need to combine the very long maturity of open PF liabilities with a tight short-term control of the PF solvency. The main motivations of the proposed approach, specifically related to this class of Institutional ALM problems can be summarized:

-

Its long-term nature: the PF liabilities span several decades and uncertainty over future cash-flows increases greatly as the planning horizon increases.

-

The employed roll-over online optimization approach helps combining long-term liability evaluation with an effective control of short-term funding conditions, under an assumption of continuous uncertainty.

-

Indeed, to limit the associated model risk, the presented methodology relies on the specification of a white noise process including several possible parametric representations.

-

The resulting optimal strategies aim at stabilizing and preserving the PF long-term solvency. In the short and medium term we approximate the ambiguous chance constraints (Erdoğan and Iyengar 2006) on the fund’s solvency condition by \({\check{C}}eby{\check{s}}\ddot{e}v\) inequalities. Notice that the formulation of the funding constraint in probabilistic form has strong operational and practical motivations and it is fully justified by the market authorities’ monitoring process (OECD 2008).

Our contributions to the state-of-the-art in this application domain may be summarized. From a methodological viewpoint: (1) we extend (Calafiore 2008; Primbs and Sung 2009) to account for chance constraints on the funding level and (2) we tackle through an on-line approach a realistic dynamic PF ALM problem with continuous uncertainty. From an application viewpoint, the adoption of a generic random white noise process as generator of the underlying uncertainty helps analysing the ex-post implications of alternative market conditions on the optimal policy, and at the PF funding level. The presented approach, thus (3), allows the estimation of the optimal policy sensitivity to a relaxation of the FR constraint under different PF manager risk attitude assumptions. In the section devoted to the computational results, we analyze a set of in-sample evidences to validate the approach and then benchmark out-of-sample, the resulting optimal policies against a set of commonly adopted portfolio strategies in the pension market.

The paper is organized as follows: Sect. 2 describes the defined benefit pension fund problem, Sect. 3 proposes the optimal control model with chance-constraints for the asset-liability management problem. Numerical results are presented in Sect. 4. Conclusions follow. Several subsections are introduced to frame the analysis more accurately and ease the model and methodology descriptions.

1.1 Notation

In what follows, \({\mathbb {R}}^{n}\) denotes the space of real n-dimensional vectors, \({\mathbb {R}}^{n\times n}\) the space of \(n\times n\) real matrices and \({\mathbb {R}}^{n\times n}_s\) the space of real \(n\times n\) symmetric matrices. \({\mathbb {R}}_{+}\) is the set of nonnegative real numbers. For \(A\in {\mathbb {R}}^{n\times n}_s\), \(A\succ 0\) (\(A \succcurlyeq 0\)) means that A is positive definite (positive semi-definite) and \(Tr(\cdot )\) denotes the trace operator. The identity matrix of order n is denoted with \( \underset{(n\times n)}{{\mathbb {I}} }\) and \( \underset{(n\times n)}{{\mathbb {1}}}\) denotes the matrix with all elements equal to 1. Let \({\mathbb {I}}^{j,j}\) be a matrix of all 0’s, but the (j, j)-th element which is equal to 1, and \(Diag\left( a_{1},\dots , a_{n}\right) \) a diagonal matrix with elements \(a_{1},\dots , a_{n}\). Asterisks in a matrix denote symmetric elements.

Uncertainty is modeled by the probability space \(({\mathbb {R}}^{d}, {\mathcal {F}}, {\mathbb {P}})\), which consists of the sample space \({\mathbb {R}}^{d}\), the \(\sigma -\)algebra \({\mathcal {F}}\) and the probability measure \({\mathbb {P}}\). The elements of the sample space are denoted by \({{\varvec{\xi }}}\) and are assumed to possess a temporal structure in that they are representable as \({{\varvec{\xi }}}:= \left( {{\varvec{\xi }}}_{1},\dots ,{{\varvec{\xi }}}_{\tau } \right) \). The random vectors \({{\varvec{\xi }}}_{t}\in {\mathbb {R}}^{d_t}\), \(t\in {\mathcal {T}}:=\left\{ 1,2,\dots ,\tau \right\} \) have marginal supports \(\Omega _t\in {\mathbb {R}}^{d_t}\) where \(\sum _{t=1}^{\tau }d_t=d\) with constant \(d_t:=d/\tau \). We define the history of the random vector up to time t as \({{\varvec{\xi }}}^{t}:=\left( {{\varvec{\xi }}}_{1},\dots ,{{\varvec{\xi }}}_{t} \right) \). Furthermore for each t, we introduce the information set \({\mathcal {F}}^t\) which corresponds to the \(\sigma \)-algebra generated by \({{\varvec{\xi }}}^{t}\) (with \({\mathcal {F}}^t\subseteq {\mathcal {F}}^{t+1}\)). We denote random variables by bold letters and the expectation operator by \({\mathbb {E}}\left[ \cdot \right] \). Expectation conditional on the filtration \({{{\mathcal {F}}}}^{t}\) is denoted \({\mathbb {E}} \left[ \cdot |{{{\mathcal {F}}}}^{t} \right] \). With \({{{\mathcal {P}}}}\) we denote a family of probability measures such that \({\mathbb {P}} \in {{{\mathcal {P}}}}\) which share some common properties. We distinguish between an investment horizon \({{{\mathcal {T}}}}\) and a (more-extended) liability valuation horizon beyond \(\tau \), i.e. \(\tau _{\Lambda }\gg \tau \), \({{{\mathcal {T}}}}_{\Lambda }:=\left\{ 1,2,\dots , \tau _{\Lambda } \right\} \). This distinction helps separating the liability evaluation from the core optimal control problem investment horizon. The asset universe of the fund is assumed to include a cash account and a set \({{{\mathcal {I}}}}:=\left\{ 1,\dots ,I\right\} \) of liquid assets (government and corporate bonds and stocks).

2 The defined benefit pension fund problem

Defined benefit (DB) pension plans are still characterizing the majority of the pension systems in advanced economies despite an ongoing prevalent transition to defined contribution (DC) schemes. In a DB plan the retirement income depends on the accumulation phase and on the length of the contribution history; however it does not depend on the market performance of the pension fund. Accordingly the PF manager of a DB scheme carries the risk of the portfolio under-performing the market, since the pensions to be delivered depend on a precise mathematical and actuarial salary fraction. Of primary importance to the portfolio manager will then be the dynamic evolution of the fund’s asset to liability ratio, or funding ratio (FR): the (market) value of the investment portfolio, sometimes referred to as the plan portfolio, must be sufficient to cover the value of the fund liabilities. The PF manager seeks an investment policy able, together with the active members contributions, to generate the liquidity needed to cover current and perspective retirement obligations. This is the primary constraint imposed on institutional portfolios by international regulatory bodies (Parliament 2009).

The PF model develops around the definition of the FR. Let \({{\varvec{\phi }}}_t:=\frac{{{\varvec{X}}}_{t}}{{\varvec{\Lambda }}_{t}}\), where \({{\varvec{X}}}_{t}\) denotes the portfolio market value and \({{\varvec{\Lambda }}_{t}}\) the Pension Fund liability, or Defined Benefit Obligation (DBO) at time \(t\in {\mathcal {T}}\). If \({{\varvec{\phi }}}_t\) is greater (lower) than 1, the pension fund’s current asset will be sufficient (insufficient) to cover the present value of the future pension obligations. The PF will accordingly be overfunded (underfunded). A FR close to 1 will characterize a fully funded PF. Notice that a FR below 1 would not necessarily imply a liquidity deficit exactly as an overfunding condition would not imply a liquidity surplus: the PF manager will have to monitor both the cash condition of the fund as its funding status. For occupational pension funds we consider in the model formulation, Solvency II-type of constraints that in case of excessive underfunding force the PF to recapitalize with a given time tolerance. Under these assumptions, rather than almost-sure constraints as in MSP formulations (Consigli et al. 2017), it is natural to consider a chance constraint on the funding condition. Consistently with DB conventions, we assume pension liabilities generated exogenously and come back to their estimation later in Sect. 4.2 after discussing the core investment planning problem.

The pension fund liquidity in stage t is determined by the difference between benefits (outflows) and contributions (inflows). We represent this uncertain stream of payments with the stochastic process \({{\varvec{l}}}:=\left\{ {{\varvec{l}}}_{t} \right\} , {t \in {\mathcal {T}}}\) where \({{\varvec{l}}}_t\) is the net payment over the period between t and \(t+1\), that we assume liquidated at time \(t+1\). The process \({{\varvec{l}}}\) is typically estimated by PF actuarial divisions and its evolution is influenced by several random factors, such as mortality rates, inflation, interest rates, salary growth. Following (Lauria 2017) and as further clarified below, we define \({{\varvec{l}}}\) as a random process driven by demographic and economic variables.

Following a simple regulatory approach, we assume a given, exogenous, FR threshold \(\phi \) and define \({\varvec{\Lambda }}^{\phi }_{t}:= \phi {\varvec{\Lambda }}_{t}\). An almost sure (a.s.) constraint, often adopted in PF models (Consigli et al. 2017), on the FR would read \({{\varvec{X}}}_{t}\ge {\varvec{\Lambda }}^{\phi }_{t}\) a.s., for \(t \in {{{\mathcal {T}}}}\). Given the time tolerance and the flexibility governing real-world recapitalization measures, however, as (Iyengar and Ma 2016; Duarte et al. 2017) we propose in this article a more realistic approach based on a chance constraint on the funding condition of the PF:

Through constraint (1) we introduce in the model a delicate trade-off between the funding level \(\phi \) and the tolerance \(\alpha \in \left[ 0,1\right] \). Independently from the regulatory constraints on the FR, PF managers will in general select a target funding level and depending on the market phase relax through \(\alpha \) the policy constraint. On the other hand, given \(\alpha \) and \(\phi \), at \(t=1\) the portfolio manager will typically make sure that such constraint will not be binding. See on this point the computational evidences produced in Sect. 4. While the PF liability \({\varvec{\Lambda }}_{t}\) is determined exogenously, the investment portfolio \({{\varvec{X}}}_t\) is endogenous to the optimal policy and includes all assets and the cash position.

2.1 Model of uncertainty

We focus briefly on the uncertainty model statistical assumptions over \({{{\mathcal {T}}}}\). The following random vector process \({{\varvec{\xi }}}:={\left\{ {{\varvec{\xi }}}_{t}\right\} _{t \in {{{\mathcal {T}}}}}}\), with

will determine the uncertainty over the investment horizon, where the random process \({\varvec{r}}_{l,t}:=\frac{{{\varvec{l}}}_{t+1}}{{{\varvec{l}}}_{t}}-1\) defines the relative change in net pension payments. We assume that \({{\varvec{\xi }}}\) follows a process with given constant mean \(\mu := \left[ \mu _{0},\mu _{1},\dots ,\mu _{I},\mu _{l} \right] \) and given variance-covariance matrix \(\Sigma \), and to know only this information on the probability distribution. We introduce \(I+2\) uncorrelated white noise processes \(\left\{ {{\varvec{w}}_{j,t}}\right\} _{t \in {{{\mathcal {T}}}}}\), for \( j=1,\dots , I+2\), with unit variance, i.e. \({\mathbb {E}}\left[ {{\varvec{w}}}_{j,t}\right] =0\), \({\mathbb {E}}\left[ {{\varvec{w}}}_{j,t}^{2}\right] =1\), \({\mathbb {E}}\left[ {{\varvec{w}}}_{j,t},{{\varvec{w}}}_{i,t}\right] =0\) for \(j \ne i\), \(\forall t \in {{{\mathcal {T}}}}\) and define \(\mathbf \xi \) relying on \(\Sigma \) Cholesky decomposition. Let \(\Gamma :=[\gamma _{i,j}]\) be the lower-triangular matrix of the Cholesky decomposition \(\Sigma =\Gamma ^{\top }\Gamma \), then we write asset returns and relative liability changes, for \(t \in {{{\mathcal {T}}}}\), as:

We make the following remarks:

-

(i)

From (3) the net benefits relative increments evolve with a constant mean \(\mu _l\): this coefficient will be implied out from the benefits’ dynamic generated by an exogenous liability model. In an open fund the evolution of those cashflows is proportional to the evolution of the old-age dependency ratio DR for given average contribution and benefit rates. Net benefits are assumed uncorrelated with asset returns and driven by the PF liabilities. Their evolution over \({\mathcal {T}}\) will determine the PF cash requirements over the medium term \(\tau \), while their dynamic over \({\mathcal {T}}_{\lambda }\) will determine the PF current DBO.

-

(ii)

Notice that the only distributional assumption made is that the random variables \({{\varvec{w}}_{j,t}}\) are independent and identically distributed (i.i.d.). Thus we only require that the process \({{\varvec{\xi }}}\) belongs to the class of processes with given first and second central moments \(\mu \) and \(\Sigma \). Both statistical models (2) and (3) assume a relatively standard set of random diffusion processes, whose market consistency may be questioned in specific market phases (Kolm et al. 2014).

-

(iii)

The coefficients of the asset return process (2) are estimated directly through sample statistics from market data with weekly frequency. The correlation matrix is also estimated directly from data. We present in Appendix A the asset returns mean and standard deviation estimates when employing maximum likelihood (ML) estimation. We also compare the correlation matrix with two matrices based on copula functions. The presented evidences support the adopted statistical characterization of the return process. In Sect. 2.2 here next, we clarify how the random processes for asset returns and liability costs do determine the asset and liability portfolio dynamics.

2.2 Asset and liability dynamics

The investment strategy is determined by the amounts \({{\varvec{x}}}_{i,t}\) invested in each asset \(i\in {{{\mathcal {I}}}}\) after rebalancing at \(t\in {\mathcal {T}}\), plus cash \({{\varvec{x}}}_{0,t}\). We suppose that the pension fund starts with an initial amount \(x_{i,1}\) invested in the i-th asset and an initial cash surplus. The portfolio evolution is denoted with \(\left\{ {{\varvec{x}}}_{t}\right\} _{t \in {{{\mathcal {T}}}}}\) where:

We assume a control process \(\left\{ {{\varvec{u}}}_{t}\right\} _{t \in {{{\mathcal {T}}}}}\) adapted to the filtration \(\left\{ {{{\mathcal {F}}}}^{t}\right\} _{t \in {{{\mathcal {T}}}}}\) defined by a sequence of trading (rebalancing) decisions, with buyings \({{\varvec{x}}}_{i,t}^{+}\) and sellings \({{\varvec{x}}}_{i,t}^{-}\) at times t:

When selecting the portfolio allocation, the portfolio manager knows the value of the PF obligation and we assume that she/he will look for an optimal portfolio policy able to preserve or recover a stable funding condition over the next few years. As time progresses, she/he will reformulate the problem relying on realized market values and PF members dynamics but always facing a residual uncertainty.

To quantify the random dynamics of the plan portfolio, consider the process \({\varvec{r}}_{0} := \left\{ {\varvec{r}}_{0,t}\right\} _{t \in {{{\mathcal {T}}}}}\) for the short interest rate on the cash account and \({\varvec{r}}_i:=\left\{ {\varvec{r}}_{it}\right\} _{t \in {{{\mathcal {T}}}}}\) for the total return process of the i-th asset over t to \(t+1\). The portfolio evolution over time is determined by market returns and rebalancing decisions:

At \(t=1\) the PF manager will sell from the initial portfolio or buy new assets to determine the initial optimal portfolio allocation.

The cash balance evolution depends on rebalancing decisions and net pension payments: at \(t=1\) a cash surplus is assumed (net of pensions and contributions). We also assume constant transaction costs \(\eta ^{+}_{i}\) and \(\eta ^{-}_{i}\) on buying and selling decisions. Given an initial cash surplus \({{\varvec{x}}}_{0,1}=\bar{{\varvec{x}}}_{0,1}\), the cash balance evolution is:

The plan portfolio \({{\varvec{X}}}_{t}:=\sum _{i=0}^{I}{{\varvec{x}}}_{i,t}\) is evaluated at time t after rebalancing and it will drive the funding ratio FR, while (5) will determine the PF liquidity gap: in presence of excessive net benefit payments \({{\varvec{l}}}_{t}\), the PF manager will start selling assets, in this way affecting the FR. Based on (2)-(3), we can write the inventory balance equations (4) and (5) as:

and

Finally, we add a new equation describing the evolution of \(\left\{ {\varvec{l}}_{t}\right\} _{t \in {{{\mathcal {T}}}}}\):

We can now introduce the state variable vector \(\mathbf{x}_{t}:=\left[ {{\varvec{x}}}_{0,t},\dots ,{{\varvec{x}}}_{I,t},{{\varvec{l}}}_{t}\right] ^{\top }\in {\mathbb {R}}^{I+2},\quad t\in {\mathcal {T}}\) and define the assets evolution of the pension fund through the linear system:

where the matrices \(A,B,C_{j}\) and \(D_{j}\) are defined as follows:

where

We consider next a possible formulation of the PF investment problem as a constrained stochastic control problem with state and control multiplicative noise and, following the approach in Primbs and Sung (2009), solve it as a semidefinite programming problem. We then consider the problem refinement induced by a chance constraint on the funding ratio.

3 Optimal pension fund asset-liability management

The following sequence of non-anticipative portfolio recourse decisions, shortly investment policy, and liability, or DBO values, is considered in the decision process:

The portfolio strategy is expected to preserve the PF liquidity and at the same time to comply with the constraint on the FR. We assume a risk-averse PF manager with mean-variance preferences and formulate the decision problem with an objective function based on a trade-off between a maximum growth problem and the minimization of the squared difference between a portfolio value trajectory and a target portfolio path \(G_{t}\). The objective function reads:

where, in the given set-up, different specifications of \(\gamma \in [0,1]\) will span alternative trade-offs and risk profiles; the definition of the target function \(G_t\) can be calibrated by the PF manager to reflect a DBO evolution and ease the satisfaction of the chance constraint. Alternatively, as mostly the case in many applications, the target function will reflect a desirable portfolio return path. The relevance of such trade-off will be tested in the case study.

We consider a general quadratic objective function, which in matrix form reads as follows:

with

\(q_t := \left( -\gamma + 2\gamma G_{t} {-} 2G_{t}\right) \left[ {\begin{array}{ccc} \underset{(1\times (I+1))}{{\mathbb {1}}}&0 \end{array} } \right] {\in {\mathbb {R}}^{I+2}},\) and \(q^{0}_t := G_{t}^2\in {{\mathbb {R}}}.\)

Eq. (15) is minimized, given the linear system (9) and, for \(t \in {{{\mathcal {T}}}}\), a set of no-short selling \({{\varvec{x}}}_{i,t}\ge 0, i=0,\dots ,I\) and technical constraints on the control variables: namely \({{\varvec{u}}}_{t} \ge 0\), and \({{\varvec{x}}}^{-}_{i,t}\le {{\varvec{x}}}_{i,t}\), \(i\in {\mathcal {I}}\) which can be rewritten as:

where:

3.1 Open-loop control formulation with linear feedback

Consider now the objective function (15), the liability and return dynamics, respectively in (8) and (9), and the policy constraints (16). Here next we formalize the system dynamics once a feedback rule is considered as control function.

To this aim let \({ \mathbf{x}}_{t}^{*}:=\left[ { x}_{0,t}^{*},\dots ,{ x}_{I,t}^{*},{ l}_{t}^{*}\right] ^{\top } \) be the initial conditions at time t and \(\bar{\mathrm {x}}_{k}\):=\({\mathbb {E}}\left[ \mathbf{x}_{k}|{{{\mathcal {F}}}}^{t}\right] \) be the conditional expectation of the state vector with respect to the filtration \({{{\mathcal {F}}}}^{t}\) (see Primbs and Sung 2009). For \(k=t+1,\dots ,t+\tau -1\), we denote with \({{\varvec{u}}}_{k}\) the control vector.

We can now define the following finite horizon control problem, in which the vector \({{\varvec{u}}}_{k}\) is specified as the sum of the open-loop controls \({\bar{u}}_{k}\) and a linear feedback function \(K_{k}\left( \mathbf{x}_{k}-\bar{\mathrm {x}}_{k}\right) \). We denote this problem formulation by \({{\mathbf {P}}}\left( \mathbf{x}_{t}^{*}, \tau \right) \):

where the minimization is taken over \({\bar{u}}_k\), for \(k=t,...,t+\tau \) and \(K_k\), for \(k=t+1,...,t+\tau \).

Let’s summarize the key elements of problem (17–22):

-

The optimal policy in \({{\mathbf {P}}}\left( \mathbf{x}_{t}^{*}, \tau \right) \) is based on the specification, for \(k=t,\dots ,t+\tau \), of the controls \({{\varvec{u}}}_{k}\) as the sum of the open-loop controls \({\bar{u}}_{k}\) and a linear term \(K_{k}\left( \mathbf{x}_{k}-\bar{\mathrm {x}}_{k}\right) \).

-

Equation (21) focuses on the feedback rule: given an initial control \(u_1\) at subsequent stages the optimal control policy will react to deviations from a mean portfolio allocation depending on the multiplicative factor \(K_k\): this acts as a mean-reverting coefficient that will drive the speed of the adjustments so to minimize the quadratic cost function.

-

We see that for \(k=t,\dots ,t+\tau -1\), the mean portfolio evolution can be determined as \(\bar{\mathrm {x}}_{k+1}=A\bar{\mathrm {x}}_{k}+B{\bar{u}}_{k}\).

-

The portfolio evolution is stochastic and determined in each stage, for given controls and linear operators \(A,B,C_j,D_j\), by a continuous source of uncertainty \({{\varvec{w}}}_{j,k}\) for all j, k.

-

The constraint (22) forces the investment strategy not to go short but only in expectation: this relaxation of the no short-selling condition helps taking full advantage of the convergence speed of semidefinite programs’ algorithms. Notice however, that short positions are allowed only after the initial allocation: indeed throughout the case study, consistently with PF practice, no short positions are allowed at \(t=1\).

-

The solution of the problem depends on \(\tau \) and the initial states \(\mathbf{x}_t^{*}\). For every instance of \(\mathbf{P}(\mathbf{x}_t^{*},\tau )\), before t all statistical coefficients are assumed constant and to trace the market evolution, they are updated as t increases when a new problem is formulated.

3.2 Semidefinite program formulation

The solution of problem (17–22) leads to the definition of the optimal control \({\bar{u}}_{t}\) to be implemented by the pension fund manager. Once new information on returns and payments becomes available at time \(t+1\), a new vector of initial conditions \(\mathbf{x}_{t+1}=\left[ x_{0,t+1},\dots , x_{I,t+1}, l_{t+1}\right] ^{\top } \) will be computed, and the next control \( {\bar{u}}_{t+1}\) obtained by solving the optimization problem \(\mathbf{P}\left( \mathbf{x}_{t+1}^{*},\tau \right) \).

We first show that key quantities, such as the mean and covariance processes, can be characterized in a convex manner. We then use these results to formulate the finite horizon optimization \(\mathbf{P}\left( \mathbf{x}_{t}^{*},\tau \right) \) in the receding horizon approach as a semi-definite program. The significance of a semi-definite programming formulation is that the on-line optimizations are relatively tractable, indicating that real time implementation is possible.

Let \(\Psi _{k}\):=\({\mathbb {E}}\left[ \left( \mathbf{x}_{k} -\bar{\mathrm {x}}_{t}\right) \left( \mathbf{x}_{k}-\bar{\mathrm {x}}_{k}\right) ^{\top }\right] \) be the conditional variance-covariance matrix. From the first period t, we have:

For \(k>t\) the evolution of the variance-covariance matrix is:

Under the assumption that \(\Psi _{k}\succ 0\), \(k=t,\dots ,t+ \tau -1\), and defining \(U_{k} := K_{k}\Psi _{k}\), an upper bound on \(\Psi _{k}\) can be expressed, by using Schur complements, as the following linear matrix inequalities:

Notice that both the mean and covariance have been characterized in a convex manner as in (24), (25) and (26). Analogous bounds on the variance-covariance matrix of vector \([{\mathbf {x}}_{k}, {{\varvec{u}}}_{k}]\) can be obtained by introducing matrix variables \(P_{k}\), for \(k=t,\dots ,t+\tau \), such that:

We partition each matrix \(P_{k}\), for \(k=t,\dots ,t+\tau \) in three blocks \(P^{\mathrm{x}}_{k} \in {\mathbb {R}}^{n \times n}\), \(P^{\mathrm {x}u}_{k} \in {\mathbb {R}}^{m \times n}\), \(P^{u}_{k} \in {\mathbb {R}}^{m \times m}\) such that:

Equation (27) can be rewritten as a linear matrix inequality using Schur complements. When \(k=1\) we can write:

For \(k=t,\dots ,t+\tau -1\), we obtain:

Finally, when \(k=t+\tau \) we do not have controls and equation (30) can be replaced by:

The auxiliary matrices \(P^{\mathrm{x}}_{k}\) enable us to rewrite the objective function (17) as:

Problem (17–22) can now be replaced by the following semi-definite program \(\mathbf{P}\left( {\mathbf {x}}_{t}^{*},\tau \right) \), for \(k=t,\dots ,t+\tau \):

This problem can be efficiently solved for practical choices of the finite horizon \(\tau \) and number of assets I in the investment universe thanks to the reformulation as a semi-definite program. The investment horizon of the PF manager is \(\tau \), based on financial and economic motivations as well as operational practice. Here the focus is on a relatively frequent rebalancing assumption and a medium term investment horizon, which allows a tight control of the PF FR. For regulatory purposes \(\tau \) does not need to be consistent with the pension fund population expected lifetime. In the problem formulation, consistently with the adopted DB scheme, liabilities are exogenous to the optimal control, which, instead, depends on the random asset returns \({{\varvec{r}}}\). These are characterized by a mean vector and variance-covariance matrix, estimated from past data: for each t the elements \(\left[ \mu _{0},\mu _{1},\dots ,\mu _{I}\right] \) and \(\left[ \Sigma \right] _{i,j} i=1,\dots ,I+1,j\le i\) are derived from historical returns.

3.3 Liability evaluation and chance constraints on the funding ratio

Let’s now focus on the liabilities. Net benefits \({{\varvec{l}}}\) depend on economic factors and on PF members’ incoming and outgoing intensity. In presence of an open fund the active to passive members ratio will evolve over time according to generation dynamics. In this model the dependency ratio depends on mortality scenarios and the net benefits will be determined for given DR evolution, average benefit and contribution rates, by the inflation process.

The computation of the PF DBO \({\varvec{\Lambda }}_t\) over \({{{\mathcal {T}}}}\) relies on a Monte Carlo (MC) approach, where over a given long horizon \(\tau _{\Lambda }\) and relying on a members’ updating rule and evolution of the term structure of interest rates, we determine future net benefits and the forward estimates of the liability value through a consistent discounting process (EIOPA 2021). A simplified pension model is presented in Supplementary Materials in which a single representative benefit class is assumed. A PF manager feasible investment policy must satisfy the chance constraint in eq. (1).

For every \(t \in {{{\mathcal {T}}}}_{\Lambda }\), \(k>t\) we generate \(s=1,2,\ldots ,S\) sample paths \({\hat{l}}_{s,k}\) and \({\hat{\iota }}_{s,k}\) respectively for the net benefits \({{\varvec{l}}}\) and a technical discount rate \({{\varvec{\iota }}}\) between t and \(t+\tau _{\Lambda }\). The net benefits \({\hat{l}}_{s,k}\) are computed for constant contribution and benefit rates from given active and passive members’ scenarios. Then, the mean \(\mu _{l}\) and the variance \(\left[ \Sigma \right] _{I+2,I+2}\) will be estimated directly from \( {\hat{l}}_{s,k}\) for \(k=t,\dots ,t+ \tau +1\) and \(s=1,\dots ,S\). The net benefits are assumed uncorrelated with the asset returns. For every \(k=\{t, t+1, \dots ,t+\tau \}\) we have:

For every t we derive the set of estimates \(\left[ \Lambda ^{\phi }_{t}, \dots , \Lambda ^{\phi }_{t+\tau }\right] \) needed, for every problem instance \(\mathbf{P}\left( \mathbf{x}_{t}^{*},\tau \right) \), to instantiate constraint (1).

Following Eq. (34) increasing interest rates in the economy will affect positively the PF liability, while longevity phenomena will carry a negative effect that may be compensated only by a decreasing DR. In recent years negligible or even negative interest rates in OECD economies together with longevity phenomena had a widespread negative impact on global PFs. This evidence provides an additional motivation to introduce a chance constraint on the FR.

The probabilistic constraint (1), which can be equivalently written as

can indeed be effectively approximated through a \({\check{C}}eby{\check{s}}\ddot{e}v\) inequality to complete the problem specification (32–(33). Consider the following conservative approximation of the set of chance constraints (1), based on the one-side \({\check{C}}eby{\check{s}}\ddot{e}v\) inequality (Pintér 1989). For each \(k=t+1,\cdots , t+\tau \), let \(\sigma ^{2}_{X,k}\) and \(\mu _{X,k}\) be the variance and the mean of the portfolio value \({\mathbf {X}}_k\) respectively. We have:

which, for \(k=t\), is automatically satisfied. Now, since \(\mu _{X,k}^2={\mathbb {E}}\left[ {{\varvec{X}}}_{k}^{2}\right] -\sigma ^{2}_{X,k}\), we have:

Due to (27) we have that \(P^{\mathrm{x}}_{k}-{\mathbb {E}}\left[ {\mathbf{x}}_{k}{\mathbf{x}}_{k}^{\top }\right] \succcurlyeq 0\), for \(k=t,\dots ,t+\tau \), which implies \({\mathbb {1}}^{\top }P^{\mathrm{x}}_{k} {\mathbb {1}}^{\top }-{\mathbb {1}}^{\top }{\mathbb {E}}[ {\mathbf{x}}_{k}{\mathbf{x}}_{k}^{\top }]{\mathbb {1}}\ge 0\). It is straightforward to show that \({\mathbb {1}}^{\top }{\mathbb {E}}[ {\mathbf{x}}_{k}{\mathbf{x}}_{k}^{\top }]{\mathbb {1}}={\mathbb {E}}[ {\mathbf{X}}_{k}^{2}]\), so that the following condition holds:

and in turn we have:

By defining the variance of the i-th state variable at k with \(\sigma ^{2}_{i,k}\) and the covariance between the i-th and the j-th state variables with \(\sigma _{i,j,k}\), we can write the portfolio variance at k as \(\sigma ^{2}_{X,k}=\sum _{i=0}^{I}\sigma ^{2}_{i,k}+2\sum _{i=0}^{I}\sum _{j<i} \sigma _{i,j,k}\), which can be bounded as follows:

In conclusion, a conservative approximation of the set of chance constraints (1) is determined:

We evaluate in the numerical study the sensitivity of the optimal policy to the above chance constraint. Notice that the distributional assumptions on the mean and variance-covariance matrix of the random process are updated in time. Alternative approaches to approximate the chance constraint on the FR can be considered as in Iyengar and Ma (2016) preserving the assumption of a continuous probability space: the adoption of \({\check{C}}eby{\check{s}}\ddot{e}v\) however is appropriate when considering a regulatory compliance problem.

4 Computational evidence

We present an extended set of computational results to validate the proposed methodology and discuss its main implications. The collected evidences span several aspects of the problem, since, to the best of our knowledge, this is the first time in which this optimal control methodology is extended to include a chance constraint approximation and applied to a pension fund ALM problem.

Here next let \({{\mathbf {P}}}\left( {{\mathbf {x}}}_{t}^{*},\tau , \gamma , \alpha \right) \) denote a problem instance specified at time t with initial portfolio \(\mathrm {x}_{t}\), investment horizon \(\tau \), risk-reward trade-off \(\gamma \) and chance constraint tolerance \(\alpha \). We assess the effectiveness of the proposed approach to control the PF long-term funding conditions through the solution of a sequence of chance-constrained Strategic Asset Allocation (SAA) problems and evaluate the impact of alternative objective function specifications. Portfolio revisions occur in \(t=1\) and with quarterly frequency: accordingly \(\tau \) is defined in quarterly terms.

In this section we first summarize the main features of the adopted data set, its statistical properties and the initial funding conditions of the pension fund based on liabilities’ expected dynamics over a 30 year horizon i.e. \(\tau _{\Lambda }=120\) quarters. We test two initial funding conditions of the PF: (i) a stressed case in which \(X_1=\Lambda ^{\phi }_1\) and (ii) a standard, more operational, case in which at \(t=1\) the portfolio value is set slightly above the minimal funding level \(\phi \). Then after we present evidences on the solution of a SAA problem, which is extended through a rolling window approach for out-of-sample backtesting, to span 10 years of market history.

Following the problem formulation (32) subject to the constraints from (33) to (40), when analysing a single problem solution, after the first stage \(t=1\), the investment policy and the terminal portfolio distribution will depend on an optimal linear feed-back rule, the specified target function \(G_t\) and market conditions. Accordingly, we are interested to evaluate how alternative specifications of the white noise in (2) and (3) will affect the main solution outputs for given optimal linear feed-back. Consistently with finance theory (Sornette et al. 2000; Kolm et al. 2014) and stylized market evidences (Barro et al. 2019; Xiong and Idzorek 2011), three random noises with increasing kurtosis are considered. We select in particular, a standard normal, a t-Student with 4 degrees of freedom and a Generalized Hyperbolic (GH) distribution with negative skewness; the three density functions are drawn in Fig. 1. The different probability distributions are considered to verify by simulation the consistency of the optimal solutions and chance constraints tolerance with respect to alternative asset returns dynamics.

Probability density functions for \({\varvec{w}}\) defined on \( ({\mathbb {R}}^{d}, {{{\mathcal {F}}}},{\mathbb {P}}), {\mathbb {P}} \in {{{\mathcal {P}}}}\) under a standard normal, t-Student with 4 degrees of freedom and Generalised Hyperbolic distribution with parameters \(\left[ \lambda ,\alpha ,\beta ,\delta ,\mu \right] =[-2.9,0.58,-0.59,2.9,0]\)

4.1 Data specification and experimental set-up

In this case study, the asset universe \({\mathcal {I}}=\left\{ 1,\dots ,I\right\} \) is composed by four Euro Area Government bond indices, Barcap Euro Gov Bond 1-3, 3-5, 7-10 and 30 year maturity, and by three equity indices MSCI-Europe, MSCI-USA, MSCI-World. Results are presented relying on three asset classes for Money market, Bond and Equity, including respectively: Cash and Bond 1–3; Bond 3–5, 7–10 and 30 years; and the 3 MSCI equity indices. We refer to “Appendix 5” for assets’ return statistics. Taking also into account the models’ statistical assumptions, the adopted investment universe may be representative of market spans by institutional investors focusing primarily on bond and equity markets. It is thus not intended to describe investment domains of pension funds currently operating in global markets, that would typically include real estate assets as well as inflation-linked bonds. We see however that the adopted investment domain is sufficient to convey the main features of the approach presented so far. A standard 3 year investment horizon will be considered consistently with medium term operational practice and strategic planning.

Correlation coefficients over the 10 years between equity markets are very high and indeed the US and World equity benchmarks are very highly correlated, leaving little space to diversification benefits. On the other hand those three equity indices may diverge in specific subperiods and be jointly included in optimal PF portfolios. We check such possibility in the out-of-sample section.

The problem has been implemented in MATLAB and solved relying on Mosek v.9, a software with a specialized interior-point solver for semi-definite programs, on a 3.4 GHz Intel Core i7 machine, with a RAM of 16 GH running Windows 10 as operating system (ApS 2019). We present in Table 1 evidence on the problems dimension and solution times for different investment horizons, 2, 3 and 4 years \((\tau \in \left\{ 8,12,16\right\} )\) respectively.

At current time \(t=1\), given an estimate of the liability value \(\Lambda _{1}=21.252\) Mln Euros (determined with a valuation horizon \(\tau _{\Lambda }=120\) quarters, or 30 years) and a funding level \(\phi = 0.9\), we assume an initial portfolio worth \(X_1=19.125\) Mln Euros, to reflect a stressed market condition. In Sect. 4.4 to assess the effectiveness of \({\check{C}}eby{\check{s}}\ddot{e}v\) inequality to approximate the chance constraint on the funding ratio, we assume also a less challenging, but operationally surely more realistic initial portfolio of \(X_1=20.189\) Mln Euros, slightly above the funding level \(\phi \). Transaction costs are set to \(\eta ^{-}_{i} = \eta ^{+}_{i} = 0.001\), for \(i = 1,\dots ,I\).

Following the average returns in Table 5, the target function \(G_{t+j}, j=1,\dots ,\tau \) in (14) is based on a \(1\%\) quarterly net return target: \(G_{t+j} = (1+0.01)^{j}X_{t}\), net of current benefit costs. For \(t=1\) the \(1\%\) compounded return would determine over 3 years a target wealth of \(G_{12}=21.552\) Mln Euros.

Several results are presented first, for in-sample model validation, with respect to a single problem instance \({{\mathbf {P}}}\left( {{\mathbf {x}}}_{t}^{*},\tau , \gamma , \alpha \right) \) for different specifications of \(\tau \in \left\{ 8,12,16\right\} \), \(\gamma \in \left\{ 0.1,0.5,0.9\right\} \) and \(\alpha \in \left\{ 0.01,0.02,0.05\right\} \), and then extended through rolling windows to span a 10 year period with resulting additional, in this case out-of-sample, results. Throughout, by forcing slightly its meaning, we denote as in-sample all those evidences associated with optimal, model-based, problem solutions without any market-based validation and as out-of-sample the results collected, ex-post, when evaluating a given strategy once market information becomes available. In-sample analysis aims primarily at checking the results consistency with the main problem assumptions thus for model validation, while out-of-sample backtesting intends to evaluate the what-if in case an optimal strategy is actually implemented over time, given observed market data.

By setting \(\gamma \in \left\{ 0.1, 0.5, 0.9\right\} \) in (14) we derive different characterizations of the optimization problem: as \(\gamma \) increases an increasing weight is on the expected wealth maximization objective and a decreasing weight on the squared difference with respect to the target. We analyse:

-

The net benefits evolution, the associated dependency ratio and PF liability over a 30 year horizon;

-

The optimal first stage decision \({{\mathbf {x}}}_1^{*}\) under alternative specifications of \(\tau \), \(\gamma \) and \(\alpha \);

-

The evidence on chance constraints violation and target achievement likelihood from the portfolio distribution based on different white noise specifications and benchmarking different investment rules;

-

The associated optimal investment policy over \(t=1,...,12\), from the initial investment decision \(\mathbf{x}_1^{*}\), taken under full uncertainty, to the optimal controls over the investment horizon with respect to \({\varvec{w}}\) in (2) and (3);

-

The out-of-sample performance of the optimal policy over the 2008-2018 period against a representative set of investment policies.

Throughout the case study no policy bounds nor turnover constraints on the investment strategy, as would be canonical in PF management problems (Consigli et al. 2017; Bertocchi et al. 2010; Blome S. 2007), will be imposed to facilitate the results interpretation. The only policy constraint we consider is the no short selling constraint to be satisfied in expectation, thus generating the semidefinite program formulation.

4.2 Liability evolution

We consider an open pension fund with an evolving number of active, 18 to 65-year old, and passive, beyond 65-year old members. The liability model (see Supplementary Materials and Lauria (2017)) accounts for stochastic mortality rates, inflation and discount rates. Every year new pensioners are replaced by new active members according to an exponential distribution: incoming PF participants are younger than middle-age members. As mentioned in Sect. 3.3, the net benefits \({{\varvec{l}}}_{t}\) and the stream of liability values in (34) are then obtained by Monte Carlo simulation as \({\hat{l}}_{s,t}, s=1,\dots ,S\). We plot the mean, the mean +/- the standard deviation and the extreme scenarios of net pension payments in Fig. 2a, and of the dependency ratio, defined as the ratio of passive to active members multiplied by a hundred, in Fig. 2b. The resulting average mean value \(\mu _{l}\) is equal to 0.0171 per quarter (see formula (3)).

Monte Carlo simulations of net pension payments (panel a), associated dependency ratio (panel b) over 30 years

The evidence in Fig. 2 describes an increasing pension fund liability driven by a decreasing active to passive ratio. The PF DBO at \(t=1\) is computed as the expected value of net benefits over the following 30 years.

The estimated evolution of the DBO \(\mathbf{\Lambda }_t\) over the \(2013-2017\) period is displayed in Fig. 3. Such evolution will determine the PF funding condition at \(t=1\): the PF is assumed to be underfunded with FR \({\varvec{\phi }}_1=0.9\).

Estimated 3 year DBO evolution, January 1, 2013 estimate

We show in the sequel that indeed the partition of the PF manager decision horizon in two parts: until \(\tau \) as investment horizon and until \(\tau _{\Lambda }\) for liability evaluation is consistent with a FR long-term improvement. The PF manager is assumed to seek an optimal risk-reward tradeoff according to the objective (14) and at the same time, through the chance constraints (40), preserve a sufficient funding condition.

4.3 Optimal initial portfolio

We present in Table 2 a comprehensive set of results on first stage optimal allocations for \(t=1\): January 1, 2013 and different investment horizons \(\tau \in \{8,12,16\}\), risk-reward trade-offs (\(\gamma \in \{0.1,0.5,0.9\}\)), when no chance constraints are imposed on the funding ratio (\(\alpha =1\)) or when such constraint is active and a tolerance \(\alpha \in \{0.01,0.02,0.05\}\) is considered. The individual assets are aggregated into a Money market or Bond or Equity asset classes (see “Appendix 6” for detailed results with every investment opportunity).

We analyse the initial optimal allocation of a dynamic strategy as the three parameters \(\tau , \gamma , \alpha \) change. In principle we may expect an increasing risky allocation as \(\gamma \) and \(\alpha \) increase: we see indeed here below that for increasing \(\gamma \) and, given \(\gamma \), increasing \(\alpha \) the portion invested in bonds decreases in favour of equity investments and this tendency is even stronger as the investment horizon increases.

As relevant and sound financial evidence we see from Table 2, that:

-

As \(\gamma \) increases from 0.1 to 0.9: for \(\tau =8\) the fraction invested in equities increases respectively from \(44\%\) under \(\gamma =0.1\) to \(63\%\) under \(\gamma =0.9\) when \(\alpha =1\); from \(14\%\) to \(36\%\) when \(\alpha =0.01\) and from \(39\%\) to \(49\%\) when \(\alpha =0.05\). The associated short term money market and bond investments decrease in proportion. As the investment horizon increases to \(\tau =16\) we see that when \(\alpha =1\) the equity investment increases from \(55\%\) under \(\gamma =0.1\) to \(83\%\) under \(\gamma =0.9\); for \(\alpha =0.01\) from \(41\%\) to \(49\%\) and for \(\alpha =0.05\) from \(73\%\) to \(86\%\), money market and bond investments decrease in proportion. A similar pattern is observed when \(\tau =12\).

-

The difference between the optimal portfolios with or without active chance constraints is remarkable as the risk-reward trade-off changes due to an increasing \(\gamma \), thus reflecting a reduced focus on the target return function. When the investment horizon increases to 4 years we see that the risky allocation becomes less sensitive to the chance constraints. As \(\alpha \) increases from 0.01 to 0.05, fixed income allocations decrease in percentage and the equity allocation increases. Take \(\gamma =0.5\) and \(\tau =12\): at \(\alpha =0.01\) the fixed income investment is around \(60\%\) and goes down to \(50\%\) when \(\alpha =0.05\). It can be observed that even a small change from 0.01 to 0.02 has an impact on the first stage optimal portfolio composition. Similar patterns for the other investment horizons and risk-reward trade-offs. The sensitivity of the first stage optimal portfolio to variations of the chance-constraint tolerance reflects the effectiveness of the introduced approximation bounds.

-

The maximum investment in bonds and money market is roughly equal to \(85\%\) of the portfolio value for \(\gamma =0.1, \alpha =0.01, \tau =8\), while the maximum investment in equity, roughly \(86\%\) of the total portfolio value, occurs for \(\gamma =0.9, \alpha =0.05, \tau =16\).

-

For \(\tau =12\), under \(\gamma =0.1\) or 0.5 and \(\alpha =0.01\), we observe, interestingly, that both optimal portfolios are close to the canonical \(60-40\), bond–equity, fix-mix strategic asset allocation often adopted by investment managers in practice. Looking closely at the solution output, we see that if no chance constraints are active then a relevant portion of the fixed income portfolio, though, is invested in the money market. This is interesting since we are considering a PF problem and for \(\gamma =0.1\) the optimal strategy will be primarily determined by the squared difference with respect to the target. In this case, in absence of the chance constraint, the optimal portfolio will be more liquid. We see however in the next Sect. 4.4 that such investment policy will not be regulatory compliant.

Already in the first stage of a dynamic policy, the impact of the chance constraints on the optimal portfolio is relevant and indeed we see that a relaxation of the chance constraint tolerance from 0.01 to 0.05 affects the optimal first stage decision increasingly as \(\gamma \) and \(\tau \) increase.

We concentrate in what follows on the canonical 3 year horizon (\(\tau =12\)) and analyze more in detail the implications of the investment strategies on the funding condition.

We test the effectiveness of chance constraints approximations in the linear policy by simulating 5000 trajectories \(\left\{ {{\varvec{w}}}^{(s)}_{t} \right\} _{t=1}^{12}\), \(s=1,\dots ,5000\).

4.4 Chance constraints tolerance and target wealth

The implications on the problem solution and resulting funding condition of a conservative approximation of chance constraints as in (40), are assessed by estimating ex-post the exceedance probabilities \({\mathbb {P}}(\Lambda ^{\phi }_t-X_t)\), as we vary the tolerance \(\alpha \) and the objective function trade-off \(\gamma \), under different white noise parametric assumptions.

We consider two cases:

-

1.

An initial portfolio of \({{X}^1_1}=20.189\) Mln Euros.

-

2.

An initial portfolio, as above, of \({{X}^2_1}=19.125\) Mln Euros (see “Appendix 7”);

The rationale of the two alternatives can be found in the associated initial violation probabilities: in the first case \({\mathbb {P}}\left[ (\Lambda ^{\phi }_1-X^2_1) \ge 0\right] =0\) while in the second \({\mathbb {P}}\left[ (\Lambda ^{\phi }_1-X^1_1)\ge 0\right] =1\).

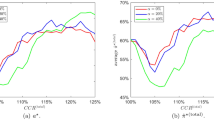

We display in Fig. 4 the exceedance probabilities for a 3 year investment problem where the initial portfolio value is \(95\%\) of the liability value (case 1). In such a situation the portfolio manager wishes to preserve the funding condition slightly above regulatory constraints as is typically the case in an operational context. We show that for \(\gamma =0.5\) the introduction of the chance constraints is critical to achieve a good funding condition relative to the \(\gamma =0.1\) case. The evidence for \(\gamma =0.9\) is not reported, being fully consistent with the \(\gamma =0.5\) case. Those results are all model-dependent: first the problem is solved under a specific combination of \(\gamma \) and \(\alpha \) or without chance constraints and either relying on the associated optimal investment policy or on a predetermined policy rule, then we estimate stage by stage, ex-post, depending on the white noise distribution, the proportion of scenarios (out of 5000) exceeding the tolerance.

The probability of violating the constraints are compared to three classical (non-optimized) investment rules: a buy-and-hold equally weighted portfolio and two fix-mix portfolios: 40% bonds and %60 stocks and 60% bonds and %40 stocks. Within each problem specification those policy rules are implemented directly leading to the results in Fig. 4.

The results presented in Fig. 4 provide immediate evidence of the effectiveness of the resulting optimal policies to comply with the regulatory constraint for different tolerance levels. The issue is now not how fast violation probabilities decrease but how effectively they are controlled by an optimal chance-constrained policy relative to the other cases.

Probability of chance constraint violations with \(\phi =0.9\) and with an initial portfolio \({X_1^1}= 0.95\Lambda _{1}^{0.9}\), under different assumptions on the noise distribution for \(\tau =12\). Fixed mix are always bond–equity classes with money market or cash as part of the bond class

From the plots in Fig. 4 we can surely confirm that under the different probabilistic assumptions:

-

In case of Gaussian white noise assumption, unlike in any other case, the violation probabilities remain at 0 over the entire 3-year investment horizon, under either \(\gamma =0.1\) or 0.5.

-

When assuming a \(t-LS\) assumption, the violation probabilities are consistent with the postulated tolerances throughout the investment horizon. As before unlike in the alternative cases.

-

In the bottom two plots, under a skewed GH assumption, again unlike the alternative cases, violation probabilities are controlled over the investment horizon but exceed the tolerances by a certain degree.

Figure 4 provides evidence of the effectiveness and operational viability of the introduced chance-constrained approximation. We refer to “Appendix 7” for a stressed PF funding condition (case 2).

4.4.1 Summary evidences

We focus here on the end of the investment horizon and the portfolio value distribution associated with different specifications of the white noise distribution \({\varvec{w}}\). Under the chance constraint least tolerance \(\alpha =0.01\) and \(X_1=\Lambda _1^{\phi }\) we present in Fig. 5 the terminal wealth distributions generated by the solutions \({{\mathbf {P}}}\left( {\mathbf {x}}_{t}^{*},12, \gamma , 0.01 \right) \), with \(\gamma \in \{0.1,0.5,0.9\}\) together with the liability constraint \(\Lambda ^{\phi }_{12}\) (vertical dashed red line), and the target portfolio value (vertical dashed blue line). In order to provide a more comprehensive set of evidences, we present in Table 3 an extended set of statistics. The results are collected for the case \(\gamma =0.1\) from the simulated optimal portfolio values at the horizon under alternative chance constraint tolerances \(\alpha \). We compare the optimal chance-constrained portfolio in-sample results with two alternative fix-mix policies over the 12 quarters from 2013 to 2015.

Simulated optimal portfolios CDFs for \(\tau = 12\), \(\gamma \in \{0.1,0.5,0.9\}\) and \(\alpha =0.01\)

The difference among the three portfolio distributions (Normal, t-student and Generalized Hyperbolic) are tolerable and indeed under any \(\gamma \) the generated distributions exceed the target with different probability and satisfy the chance constraint tolerance. The GH distribution, as expected due to its fat tails and negative skewness, is the one which exceeds the most the \(1\%\) constraint violation tolerance (\(\alpha =0.01\)). Relative to the other chance-unconstrained cases, the model without chance constraints has the least constraint violations when the objective parameter \(\gamma \) is set equal to 0.1.

The evidences in Fig. 4 and 5, in Table 3 and “Appendix 7” allow several relevant remarks:

-

Under any probabilistic assumption, in-sample when considering optimal chance-constrained portfolios the funding condition either improves or it is strictly under control and within the portfolio tolerance level over the planning horizon.

-

As \(\alpha \) decreases, when an initial stressed funding condition is assumed, a least tolerance over the chance constraint violation, leads consistently to improved funding conditions and a smooth convergence to full funding under Gaussian or t-student white noise assumptions.

-

For given \(\gamma \), we see that the collected evidences are robust across different probabilistic assumptions even if they worsen slightly as we move from the normal standard or the t-Student to the generalized hyperbolic cases.

-

Under any model instance, the risk-adjusted returns, measured by the Sharpe ratio, are consistently higher when chance constraints are active than under any other portfolio policy: we show in Sect. 4.5 that this evidence is confirmed out-of-sample.

-

Across all implemented models, the \({{\mathbf {P}}}\left( {\mathbf {x}}_{t}^{*},12, 0.1, \alpha \right) \) instances for \(\alpha =0.01\) or 0.02 generate consistently the best risk-reward and constraints violation trade-offs. See also Table 7 in “Appendix 6” for the good diversification properties of the associated optimal portfolios.

The computational evidences presented so far are encouraging in terms of both the effectiveness of the adopted approach to control the FR through a probabilistic constraint and the relevant difference with respect to either the no chance-constrained case or the benchmark investment rules. In “Appendix 8” we discard the \({\alpha =1}\) case and provide more in-sample evidences on the investment policy evolution over time and under different noise assumptions. In the following sections we consider only the case of \(X_1=\Lambda ^{0.9}_1\).

4.5 Out-of-sample analysis

We present in this section the out-of-sample evidences over a 10 year horizon, the evolution of the optimal first stage portfolio and the associated portfolio value based on observed market data. The reference problem instance is again a 3-year optimal control problem with quarterly rebalancing, \(\gamma =0.5\), \(\alpha =0.01\) and \(X_1=\Lambda _1^{0.9}\). Every problem instance is associated with a moving data history of two years. We apply a rolling window procedure starting with the solution of the January 1, 2008 problem and ending with the solution of the October 1, 2017 problem. Every problem instance is solved having as input the optimal portfolio obtained in the previous instance, updated with the realized (historical) returns. As before we consider quarterly steps of the rolling window and accordingly the optimal portfolio is assumed to undergo quarterly rebalancing decisions. In practice, Pension funds tend to revise their strategic asset allocation depending on the market phase from twice to four times per year.

No policy bounds nor turnover constraints have been imposed and Fig. 6 shows indeed that the portfolio undertakes significant revisions over the 10 years but, overall presents good diversification properties. In specific periods we see that an only equity portfolio is optimal, as during 2011–2012, or an only fixed income portfolio as in 2009 or 2016 or a balanced well diversified portfolio as in 2015 and in the last quarter of the test period.

At the end of the 10 years an average out-of-sample return of \(4.331\%\) per annum is recorded, based on a final portfolio value at December 31, 2017 of \(\mathbf{X}_t= 2.0968e+07\) and an initial value on January 2008 of \(\mathbf{X}_t=1.3721e+07\) €.

Portfolio policy evolution over 2008–2018—first stage decision, out-of-sample performance

As final evidence of this case study we analyse the out-of-sample performance of the optimal portfolio against a selected set of benchmark policies and in relationship with the evolution of the PF liability. We consider the following strategies:

-

1.

The optimal chance constrained policy generated by the sequence of \({{\mathbf {P}}}({\mathbf {x}}_t^{*},12,0.5,0.01)\) problems for t spanning from the \(1^{st}\) quarter of 2008 to the \(4^{th}\) quarter of 2017.

-

2.

A fix-mix strategy based on a \(50\%\) investment in Money market and Bonds and the remaining \(50\%\) in equity (strategy 1).

-

3.

A fix-mix strategy based on a \(60\%\) investment in Money market and Bonds and the remaining \(40\%\) in equity (strategy 2).

-

4.

A fix-mix strategy based on long-term bonds: namely \(50\%\) in Bonds 7-10 and \(50\%\) in Bond 30 (strategy 3).

-

5.

A fix-mix strategy based on a \(60\%\) investment in Equity and the remaining \(40\%\) in Money market and Bonds (strategy 4).

-

6.

A fully diversified 1/I policy in which at every rebalancing decision the optimal portfolio is evenly distributed across all asset classes.

-

7.

A constant investment policy only in long-term 30 year bonds.

-

8.

A constant policy fully concentrated in USA equity. These two last policies will thus replicate the associated total return benchmarks.

Out-of-sample portfolio performance relative to benchmark policies for \(\tau =12\), \(\gamma =0.5\) and \(\alpha =0.01\)

From Fig. 7 we see that in specific periods, after 2015 and between 2010 and 2014 the optimal investment policy significantly outperforms the other policies and generates a positive outcome while all other strategies lead to negative performances. Even more relevant the evidence that \(X_t\) starts in 2008 with a \(\phi =90\%\) underfunding condition relative to the PF DBO \({\varvec{\Lambda }}_t\) (dashed red line) and over time reaches a stable and robust overfunding condition: over the 10 years we see that, as also indicated in the previous sections, the PF liability increases and it reaches at the end of 2017 a value of roughly 18802 Mln Euros with a PF portfolio worth 20.968 Mln Euros and a FR \({\varvec{\phi }}_t=1.115\).

5 Conclusions

In this article we have extended the optimization approach developed in Primbs and Sung (2009) to account for chance constraints on a PF solvency condition and for the first time apply the methodology to an open occupational DB pension fund ALM problem. From a methodological perspective we try to overcome the limits associated with classical multistage stochastic programs (Consigli et al. 2017) namely due to scenario tree approximation errors, curse of dimensionality, and the difficulty to integrate in an effective way regulatory constraints formulated as chance constraints. The proposed methodology has been shown to achieve the long term control of a PF solvency condition relying on the solution of a sequence of medium-term strategic allocation problems.

The adopted model of uncertainty for asset returns and liability costs relies on a vector random process driven by a white noise which for sensitivity analysis and simulation purposes has been given three alternative probability distributions. An extensive set of computational evidences allowed us to verify and share several aspects of the adopted approach and its implications.

The following can be regarded as main contributions of this research:

-

The formulation of the ALM problem as a stochastic control problem with probabilistic constraints whose solution is based on a medium-term investment horizon \(\tau \), justified by the funding ratio tight control and a long-term liability evaluation horizon \(\tau _{\Lambda }\).

-

A thorough study of the effectiveness of chance constraints on the optimal solution and the implications on the ALM policy of funding ratio regulatory compliance.

-

The characterization of the optimal investment policy in presence of different risk-reward, chance constraints tolerance and medium term planning horizons with collected evidences consistent with evolving market conditions.

-

The evaluation of alternative white noise probabilistic assumptions, corresponding to different market phases, on the portfolio wealth distributions and PF funding condition. Mainly through simulation we have seen how different market volatility conditions will impact the overall PF solvency. A topic that can be extended further be subject to a more rigorous analysis.

-

Finally, both in- and out-of-sample optimal chance constrained portfolios lead to robust return generation over the selected test-period and show a good portfolio diversification.

We believe that this approach can represent under relatively mild assumptions an effective alternative to currently employed ALM methods.

Change history

21 July 2022

Missing Open Access funding information has been added in the Funding Note

References

Abdelaziz FB, Aouni B, Fayedh RE (2007) Multi-objective stochastic programming for portfolio selection. Eur J Oper Res 177(3):1811–1823

ApS M (2019) The MOSEK optimization toolbox for MATLAB manual. Version 9.0. http://docs.mosek.com/9.0/toolbox/index.html

Barro D, Canestrelli E, Consigli G (2019) Volatility versus downside risk: performance protection in dynamic portfolio strategies. CMS 16(3):433–479

Ben-Tal A, Margalit T, Nemirovski A (2000) Robust modeling of multi-stage portfolio problems. Springer, Boston, pp 303–328

Bertocchi M, Schwartz S, Ziemba W (2010) Optimizing the aging, retirement and, pension dilemma. Wiley Finance, New York

Blome S, Fachinger K, Franzen D, Scheuenstuhl G, Yermo J (2007) Pension fund regulation and risk management: results from an ALM optimisation exercise. In: OECD working papers on insurance and private pensions, vol 8. OECD Publishing, pp 1–60. https://doi.org/10.1787/171755452623

Calafiore GC (2008) Multi-period portfolio optimization with linear control policies. Automatica 44(10):2463–2473

Chang Z, Song S, Zhang Y, Ding J-Y, Zhang R, Chiong R (2017) Distributionally robust single machine scheduling with risk aversion. Eur J Oper Res 256(1):261–274

Consigli G, Dempster M (1998) Dynamic stochastic programming for asset-liability management. Ann Oper Res 81:131–161

Consigli G, Kuhn D, Brandimarte P (eds) (2016) Optimal financial decision making under uncertainty. In: International series in operations research and management science, Vol. 245. Springer

Consigli G, Kuhn D, Brandimarte P (2016) Optimal financial decision making under uncertainty. In: Consigli G, Kuhn D, Brandimarte P (eds) International series in operations research and management science. Springer, Berlin, pp 255–290

Consigli G, Moriggia V, Benincasa E, Landoni G, Petronio F, Vitali S, di Tria M, Skoric M, Uristani A (2017) Optimal multistage defined-benefit pension fund management. In: Consigli G, Zambruno SS (eds) Handbook on recent advances in commodity and financial modeling, vol 257. International series in operations research and management science. Springer, New York, pp 267–296

Curtis FE, Wachter A, Zavala VM (2018) A sequential algorithm for solving nonlinear optimization problems with chance constraints. SIAM J Optim 28(1):930–958

Delage E, Ye Y (2010) Distributionally robust optimization under moment uncertainty with application to data-driven problems. Oper Res 58(3):595–612

Duarte TB, Valladão DM, Veiga Á (2017) Asset liability management for open pension schemes using multistage stochastic programming under solvency-ii-based regulatory constraints. Insurance Math Econom 77:177–188

EIOPA (2018) Insurance and pensions: securing the future. EIOPA Publications, New York

EIOPA (2021) Technical documentation: Eiopa’s risk-free interest rate term structure. EIOPA Publications, Frankfurt a. M.

Erdoğan E, Iyengar G (2006) Ambiguous chance constrained problems and robust optimization. Math Program 107(1–2, Ser. B):37–61

Georghiou A, Wiesemann W, Kuhn D (2015) Generalised decision rule approximations for stochastic programming via liftings. Math Program 152(1–2):301–338

Geyer A, Ziemba WT (2008) The Innovest Austrian pension fund financial planning model InnoALM. Oper Res 56(4):797–810

Gülpinar N, Pachamanova D (2013) A robust optimization approach to asset-liability management under time-varying investment opportunities. J Bank Finance 37(6):2031–2041

Haneveld WKK, Streutker MH, Van Der Vlerk MH (2010) An ALM model for pension funds using integrated chance constraints. Ann Oper Res 177(1):47–62

Herzog F, Keel S, Dondi G, Schumann LM, Geering HP (2006) Model predictive control for portfolio selection. In: 2006 American Control Conference. IEEE, pp 8–pp

Iyengar G, Ma AKC, (2016) A robust optimization approach to pension fund management. In: Asset management. Springer, pp 339–363

Kaut M, Wallace SW (2007) Evaluation of scenario-generation methods for stochastic programming. Pac J Optim 3(2):257–271

Kolm PN, Tütüncü R, Fabozzi FJ (2014) 60 years of portfolio optimization: practical challenges and current trends. Eur J Oper Res 234(2):356–371

Kuhn D, Wiesemann W, Georghiou A (2011) Primal and dual linear decision rules in stochastic and robust optimization. Math Program 130(1):177–209

Lauria D (2017) Pricing and hedging pension fund liability via portfolio replication. Ph.D. thesis

Liu Y, Xu H, Yang S-JS, Zhang J (2018) Distributionally robust equilibrium for continuous games: Nash and stackelberg models. Eur J Oper Res 265(2):631–643

Maggioni F, Pflug GC (2016) Bounds and approximations for multistage stochastic programs. SIAM J Optim 26(1):831–855

Maggioni F, Pflug GC (2019) Guaranteed bounds for general nondiscrete multistage risk-averse stochastic optimization programs. SIAM J Optim 29(1):454–483

Moriggia V, Kopa M, Vitali S (2019) Pension fund management with hedging derivatives, stochastic dominance and nodal contamination. Omega 87:127–141

Mulvey J, Ziemba WT (1998) Asset and liability management systems for long-term investors: discussion of the issues. In: Ziemba W, Mulvey J (eds) Worldwide asset and liability modeling. Cambridge University Press, Cambridge, pp 3–38

OECD (2008) OECD private pensions outlook. OECD publications, Paris

OECD (2011) OECD factbook 2011, public finance-pension expenditure

Paç AB, Pınar MÇ (2014) Robust portfolio choice with CVaR and VaR under distribution and mean return ambiguity. TOP 22(3):875–891

Pachamanova D, Gulpinar NEC (2016) Robust data-driven approaches to pension fund asset-liability management under uncertainty. In: Consigli G, Kuhn D, Brandimarte P (eds) Int Ser Oper Res Manag Sci. Springer, pp 89–119

Parliament (2009) Directive 2009/138/EC of the European Parliament and of the Council of 25 November 2009 on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II), https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:32009L0138

Peng S, Maggioni F, Lisser A (2021) Bounds for probabilistic programming with application to a blend planning problem. Eur J Oper Res 297:964–976

Pflug GC, Świetanowski A (1999) Dynamic asset allocation under uncertainty for pension fund management. Control Cybern 28:755–777

Pflug GC, Wozabal D (2007) Ambiguity in portfolio selection. Quant Finance 7(4):435–442

Pintér J (1989) Deterministic approximations of probability inequalities. Z Oper-Res 33(4):219–239

Primbs J, Sung C (2009) Stochastic receding horizon control of constrained linear systems with state and control multiplicative noise. IEEE Trans Autom Control 54(2):221–230

Sornette D, Andersen JV, Simonetti P (2000) Portfolio theory for “fat tails’’. Int J Theor Appl Finance 3(03):523–535

Toukourou YA, Dufresne F (2018) On integrated chance constraints in ALM for pension funds. ASTIN Bull J IAA 48(2):571–609

Xiong JX, Idzorek TM (2011) The impact of skewness and fat tails on the asset allocation decision. Financ Anal J 67(2):23–35

Zácková aka, Dupačová J (1966) On minimax solutions of stochastic linear programming problems. Casopis pro Pestovani Mathematiky 91:423–430

Zhu S, Fukushima M (2009) Worst-case conditional value-at-risk with application to robust portfolio management. Oper Res 57(5):1155–1168

Ziemba WT (2007) The Russell-Yasuda, InnoALM and related models for pensions, insurance companies and high net worth individuals. In: Zenios SA, Ziemba WT (eds) Handbook of asset and liability management: applications and case studies. Elsevier, North-Holland Finance handbook series, pp 861–962