Abstract

This paper investigates the responses of house prices and household credit to monetary policy shocks in Norway, using Bayesian structural VAR models. The analysis indicates that the effect of a monetary policy shock on house prices is large, while the effect on household credit is muted. This is consistent with a relatively small refinancing rate (refinancing rate refers to the share of outstanding mortgages that are refinanced each period due to changes in, for example, house prices or interest rate) of the mortgage stock each quarter. Using monetary policy to guard against financial instability by mitigating property-price movements may prove effective, but trying to mitigate household credit may prove costly in terms of GDP and inflation variation.

Similar content being viewed by others

Notes

For example, Svensson (2010).

For example, Borio and Zhu (2008).

Monetary Policy Report 1/14.

See Kohn (2006) for an elaboration of this argument.

The next section describes the data transformations. The data sources are reported in “Appendix 1”.

See “Appendix 2” for a detailed description of the prior.

Christiano et al. (1999) provide an overview of identification of monetary policy shocks in structural VARs.

These restrictions are consistent with the DSGE model in Iacoviello (2005).

See Faust and Leeper (1997) for a further discussion of long-run restrictions.

Ordering: 1 GDP, 2 Inflation, 3 Credit, 4 Exchange rate, 5 House Prices, 6 Interest rate.

Suggesting that the level of real credit is integrated of order 2.

I remove growth cycles longer than 8 years as suggested in Christiano and Fitzgerald (2003).

This ratio does not change if real house price growth is also filtered using a band-pass filter, as almost all of the variation in real house price growth is business cycle variation.

Figure 4 also shows a cross-check where an HP filter with \(\hbox {lambda} = 1600\) is used instead of the band-pass filter. The choice of filtering technique does not seem to have a impact on the impulse responses.

Estimating a monetary policy shock where both the exchange rate and house prices are ordered after interest rates in the Choleski ordering does not change the impulse responses or reduce the price puzzle in this model.

See, for example, Iacoviello (2005).

Share of mortgages with fixed interest rate(approximately): Norway 10%, USA 85%, Sweden 40% [Source: Statistics Norway and Calza et al. (2013)].

I do not allow for more variables due to the curse of dimensionality problem. The number of parameters in a VAR increases exponentially with the number of variables.

OLS estimates of the parameters are used in this exercise.

In a Diebold–Mariano test, 250 of the 400 reduced form models have a significantly higher MRSE than the “best” model(at a 5% level). The main reduced form model presented in this paper has the 23rd lowest MRSE, not significantly higher than the best model.

GDP growth, residential investment growth and consumption growth.

Core inflation and domestic inflation.

References

Alpanda S, Zubairy S (2014) Addressing household indebtedness: monetary, fiscal or macroprudential policy? Working paper, Bank of Canada

Aoki K, Proudman J, Vlieghe G (2004) House prices, consumption, and monetary policy: a financial accelerator approach. J Financ Intermed 13(4):414–435

Assenmacher-Wesche K, Gerlach S (2008) Ensuring financial stability: financial structure and the impact of monetary policy on asset prices. IEW—working papers, Institute for Empirical Research in Economics—University of Zurich

Bagliano FC, Morana C (2012) The great recession: US dynamics and spillovers to the world economy. J Bank Finance 36(1):1–13

Basel Committee on Banking Supervision (2010) Guidance for national authorities operating the countercyclical capital buffer. Technical report, Bank For International Settlements

Bernanke B, Gertler M (1999) Monetary policy and asset price volatility. Econ Rev Q 4:17–51

Bernanke BS, Gertler M (2001) Should central banks respond to movements in asset prices? Am Econ Rev 91(2):253–257

Bernanke BS, Gertler M, Gilchrist S (1999) The financial accelerator in a quantitative business cycle framework. In: Taylor JB, Woodford M (eds) Handbook of macroeconomics, chapter 21. Elsevier, Amsterdam, pp 1341–1393

Bjørnland HC, Henning JD (2010) The role of house prices in the monetary policy transmission mechanism in small open economies. J Financ Stab 6(4):218–229

Borio CEV, Lowe P (2004) Securing sustainable price stability: should credit come back from the wilderness? BIS working papers. Bank for International Settlements

Borio C, Zhu H (2008) Capital regulation, risk-taking and monetary policy: a missing link in the transmission mechanism? BIS working papers. Bank for International Settlements

Calza A, Monacelli T, Stracca L (2013) Housing finance and monetary policy. J Eur Econ Assoc 11:101–122

Carlstrom CT, Fuerst TS, Paustian M (2009) Monetary policy shocks, Choleski identification, and DNK models. J Monet Econ 56(7):1014–1021

Carstensen K, Hülsewig O, Wollmershäuser T (2009) Monetary policy transmission and house prices: European cross-country evidence. Cesifo working paper series, CESifo Group Munich

Castelnuovo E (2012) Testing the structural interpretation of the price puzzle with a cost-channel model. Oxf Bull Econ Stat 74(3):425–452

Cecchetti SG, Genberg H, Lipsky J, Wadhwani S (2000) Asset prices and central bank policy. The Geneva report on the world economy, international centre for monetary and banking studies, pp 160

Chomsisengphet S, Pennington-Cross A (2006) Subprime refinancing: equity extraction and mortgage termination. Working paper series, Federal Reserve Bank of St. Louis

Chowdhury I, Hoffmann M, Schabert A (2006) Inflation dynamics and the cost channel of monetary transmission. Eur Econ Rev 50(4):995–1016

Christiano LJ, Eichenbaum M, Evans CL (1999) Monetary policy shocks: what have we learned and to what end? In: Taylor JB, Woodford M (eds) Handbook of macroeconomics, vol 1, chapter 2. Elsevier, Amsterdam, pp 65–148

Christiano LJ, Fitzgerald TJ (2003) The band pass filter. Int Econ Rev 44(2):435–465

Christiano LJ, Eichenbaum M, Vigfusson R (2007) Assessing structural VARs. In: NBER macroeconomics annual 2006, NBER chapters. National Bureau of Economic Research, Inc, pp 1–106

Farrant K, Peersman G (2006) Is the exchange rate a shock absorber or a source of shocks? New empirical evidence. J Money Credit Bank 38(4):939–961

Faust J, Leeper EM (1997) When do long-run identifying restrictions give reliable results? J Bus Econ Stat 15(3):345–353

Fry R, Pagan A (2011) Sign restrictions in structural vector autoregressions: a critical review. J Econ Lit 49(4):938–960

Gelain P, Lansing KJ, Natvik GJ (2015) Leaning against the credit cycle. Norges Bank working paper 4

Goodhart C, Hofmann B (2008) House prices, money, credit, and the macroeconomy. Oxf Rev Econ Pol 24(1):180–205

Hagelund K, Sturød M (2012) Norges Bank’s output gap estimates. Norges Bank Staff Memo, pp 8–12

Iacoviello M (2005) House prices, borrowing constraints, and monetary policy in the business cycle. Am Econ Rev 95(3):739–764

Jarocinski M, Smets FR (2008) House prices and the stance of monetary policy. Federal Reserve Bank of St. Louis Review, pp 339–366

Kohn DL (2006) Monetary policy: a journey from theory to practice. Speech at the European Central Bank Colloquium held in honour of Otmar Issing, Frankfurt, March

Koop G, Korobilis D (2009) Bayesian multivariate time series methods for empirical macroeconomics. MPRA Paper, University Library of Munich, Germany

Lall S, Cardarelli R, Elekdag S (2009) Financial stress, downturns, and recoveries. IMF working papers, International Monetary Fund

Lasèen S, Strid I (2013) Debt dynamics and monetary policy: a note. Working paper series, Sveriges Riksbank

Monetary Policy Report 1/14. Norges Bank

Musso A, Neri S, Stracca L (2011) Housing, consumption and monetary policy: how different are the US and the euro area? J Bank Finance 35(11):3019–3041

Norges Bank (2013) Criteria for an appropriate countercyclical capital buffer. Norges Bank Papers, pp 1–13

Rabanal P (2007) Does inflation increase after a monetary policy tightening? Answers based on an estimated DSGE model. J Econ Dyn Control 31(3):906–937

Ravenna F, Walsh CE (2006) Optimal monetary policy with the cost channel. J Monet Econ 53(2):199–216

Reinhart CM, Rogoff KS (2014) This time is different: a panoramic view of eight centuries of financial crises. Ann Econ Finance 15(2):1065–1188

Rubio M (2011) Fixed- and variable-rate mortgages, business cycles, and monetary policy. J Money Credit Bank 43(4):657–688

Sims CA (1980) Macroeconomics and reality. Econometrica 48(1):1–48

Sims CA, Zha T (1999) Error bands for impulse responses. Econometrica 67(5):1113–1156

Steigum E (2010) Norwegian economy after 1980: from crisis to success. Working paper, CME/BI

Svensson LEO (2010) Inflation targeting. In: Friedman BM, Woodford M (eds) Handbook of monetary economics, vol 3, chapter 22. Elsevier, Amsterdam, pp 1237–1302

Svensson LEO (2013) Leaning against the wind leads to a higher (not lower) household debt-to-GDP ratio. Working paper, The Institute for Financial Research and Swedish House of Finance and Stockholm School of Economics and IIES, Stockholm University

Taylor J (2007) Housing and monetary policy. Discussion papers, Stanford Institute for Economic Policy Research

Uhlig H (2005) What are the effects of monetary policy on output? Results from an agnostic identification procedure. J Monet Econ 52(2):381–419

Vargas-Silva C (2008) Monetary policy and the US housing market: a VAR analysis imposing sign restrictions. J Marcroecon 30:977–990

Woodford M (2012) Inflation targeting and financial stability. Nber working papers, National Bureau of Economic Research, Inc

Acknowledgements

I thank Knut Are Aastveit, Q. Farooq Akram, Andrew Binning, Leif Brubakk, Claudia Foroni, Francesco Furlanetto, Gisle James Natvik, Kjetil Olsen, Francesco Ravazzolo and Lars Svensson for helpful comments

Author information

Authors and Affiliations

Corresponding author

Additional information

This publication should not be reported as representing the views of Norges Bank. The views expressed are those of the authors and do not necessarily reflect those of Norges Bank.

Appendices

Appendix 1: Data

-

Nominal interest rate Norway: Three-month money market rate (NIBOR). Source: Norges Bank

-

Prices Norway: Seasonally adjusted consumer price index adjusted for tax changes and excluding energy products (CPI-ATE). Sources: Statistics Norway and Norges Bank

-

Domestic Prices Norway: Seasonally adjusted consumer price index domestic sources adjusted for tax changes and excluding energy products. Sources: Statistics Norway and Norges Bank

-

Prices Abroad: Trade-weighted consumer price index for 25 trading partners. Sources: Ecowin and Norges Bank

-

Real house prices: Seasonally adjusted nominal house prices deflated by the CPI-ATE. Sources: Statistics Norway, Eiendomsmeglerforetakenes forening (EFF), Finn.no, Eiendomsverdi and Norges Bank

-

Real household credit: C2 for households chained and break-adjusted deflated by the CPI-ATE and adjusted for population growth. Sources: Statistics Norway and Norges Bank

-

GDP mainland Norway: Seasonally adjusted GDP mainland Norway (volumes) from national accounts adjusted for population growth. Source: Statistics Norway

-

Household consumption: Seasonally adjusted household final consumption (volumes) from national accounts adjusted for population growth. Source: Statistics Norway

-

Residential investment: Seasonally adjusted gross investment in housing (volumes) from national accounts adjusted for population growth. Source: Statistics Norway

-

Real exchange rate: Trade-weighted nominal exchange rate index (I-44) for 44 trading partners adjusted for relative prices in Norway and abroad. Sources: Thomson Reuters, Statistics Norway, Ecowin and Norges Bank

-

Hours worked: Total hours worked in mainland Norway from national accounts adjusted for population growth. Source: Statistics Norway

-

Population: Population from 16 to 74. Source: Statistics Norway

-

Output gap: The percentage deviation between GDP for mainland Norway and projected potential GDP for mainland Norway estimated by Norges Bank. See Hagelund and Sturød (2012) for a more detailed description of the output gap estimation. Source: Norges Bank

-

Interest rates abroad: Trade-weighted 3-month nominal money market interest rate for four trading partners (SWE, USA, EUR and GBR) Sources: Thomson Reuters and Norges Bank

-

Population USA: Working-age population. Source: Bureau of Labor Statistics

-

Prices USA: Consumer price index (CPI). Sources: OECD, Main Economic Indicators (database)

-

Real house prices USA: Residential property prices, existing houses adjusted for CPI. Source: Federal Housing Finance Agency (FHFA)

-

Real household credit USA: Credit to households and NPISHs provided by all sectors adjusted for CPI and population growth. Source: BIS

-

Oil price: Brent dated. Source: Thomson Reuters

Appendix 2: Bayesian estimation and priors

I use an uninformative version of the natural conjugate priors described in Gary and Dimitris (2009). For simplicity, assume Eq. 1 is rewritten in the following form:

where X now includes all regressors in Eq. 1, i.e. lagged endogenous, the constant and the time trend and E has a variance–covariance matrix \(\varSigma \). Since \(A = (C_0 \quad C_1 \quad A_1 \quad A_2)^{\prime }\), Eq. 3 can be written in the following form:

where n is the number of endogenous variables in the VAR and \(\alpha = \mathbf {(}A)\). The natural conjugate prior has the following form:

and

where \(\underline{\alpha }\), \(\underline{V}\), \(\underline{\nu }\) and \(\underline{S}\) are hyperparameters. Noninformativeness is then achieved by setting \(\underline{\nu }=\underline{S}=\underline{V}^{-1}=cI\) and letting \(c\rightarrow {0}\). With this prior the posterior becomes:

and

where

and

where T is the number of observations and \({\hat{A}} = (X^{\prime }X)^{-1}X^{\prime }Y\) is the OLS estimate of A.

Appendix 3: Robustness

In order to arrive at the best alternative reduced form specifications, I estimate a large number of candidate VARs and compare their out-of-sample forecasting performance. The number of variables in each VAR is 6 or 7Footnote 20 with a lag order of two or three. A general requirement is that every individual VAR includes the main variables of interest, namely the nominal interest rate, real house price growth and real household credit growth. The candidate reduced form VARs are then generated by adding all possible three or four-variable subsets from a larger set of potentially relevant variables. The list of “relevant” variables includes GDP growth (mainland Norway), output gap, change in output gap, change in hours worked, consumption growth, core inflation, domestic inflation, residential investment growth, change in the real exchange rate, foreign interest rates and real foreign interest rates. This amounts to approximately 400 reduced form models.

All the reduced form models are estimated from 1994 Q1 to 2003 Q4 and than recursively estimated from 2004 Q1 to 2013 Q4.Footnote 21 In the recursive estimation period, the out-of-sample point forecast error is stored. The average mean root squared forecast error (MRSE) for interest rate, house prices and household credit 1–8 quarters ahead is then calculated. The MRSE is adjusted for the standard deviation of the variables when the MRSEs for the three variables of interest are weighted together. The ten models with the lowest MRSE are reported in Table 3.Footnote 22 Given the potential importance of the oil price for the Norwegian economy, I also estimate the benchmark model with oil price (measured in USD) as an exogenous variable.

Monetary policy shocks are identified for all the models in Table 4 and the oil price model using sign restrictions. I impose the restriction that all economic activityFootnote 23 and inflationFootnote 24 measures do not on impact increase after a contractionary policy shock and that the real exchange rate appreciates. I place no restrictions on the response of foreign interest rates or the oil price. Figure 13 shows the median response of real house prices and real household credit to a monetary policy shock for all the models in Table 3 and the model with oil price. This robustness exercise supports the claim that the effect of a monetary policy shock is relatively large for house prices and small for household credit.

Appendix 4: Figures

See Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12 and 13.

Core inflation Norway (in this figure, 4-period log difference of prices is used since this is how Norges Bank presents inflation in MPRs. In the models in this paper, log first differences are used)

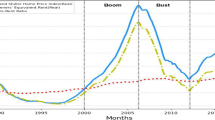

Credit and house prices

Band-pass filtered credit gap. The band-pass filter applied removes growth cycles longer than 8 years. The first difference of this series is used in the models

Robustness: filtering of the data. Monetary policy shock(sign restrictions) with alternative data transformations. Impulse responses from a monetary policy shock. Identification is achieved through sign restrictions on impact. Solid black lines are median estimates from the baseline model, while dotted lines are the 16th and 84th percentile probability bands, also from the baseline model. The blue dotted lines are the median response when credit is differenced twice. The red dotted lines show the median response when a band-pass filter is applied to all growth series, while the green circled lines are the median response when a HP filter with \(\hbox {lambda} = 1600\) is used to filter the credit growth series. (Color figure online)

Monetary policy shock: sign restrictions. Impulse responses from a monetary policy shock. Identification is achieved through sign restrictions on impact. Solid lines are median estimates, while dotted lines are the 16th and 84th percentile probability bands

Monetary policy shock: Choleski. Monetary policy ordered last. Impulse responses from a monetary policy shock. Identification is achieved through a Choleski factorisation of the variance–covariance matrix with interest rate ordered last. Solid lines are median estimates, while dotted lines are the 16th and 84th percentile probability bands

Monetary policy shock: Choleski. House prices ordered last. Impulse responses from a monetary policy shock. Identification is achieved through a Choleski factorisation of the variance–covariance matrix with house prices ordered last and interest rate ordered penultimate. Solid lines are median estimates, while dotted lines are the 16th and 84th percentile probability bands

Monetary policy shock: long- and short-run restrictions. Impulse responses from a monetary policy shock. Identification is achieved through a combination of zero and long- run restrictions. Solid lines are median estimates, while dotted lines are the 16th and 84th percentile probability bands

Monetary policy shock: real credit over GDP. Impulse responses from a monetary policy shock on real household debt/GDP using the four identification schemes described above. Solid lines are median estimates, while dotted lines are the 16th and 84th percentile probability bands

Real house prices and real household credit per capita

Variance decomposition. Contributions from monetary policy shock. Share of total forecast error variance. The reported shares are median over the posterior distribution for the different identification assumptions

Monetary policy shock(sign restrictions) in different subsamples. Impulse responses from a monetary policy shock for three different subsamples and the full sample. Identification is achieved through sign restrictions on impact. Solid black lines are median estimates from the full sample, while dotted black lines are the 16th and 84th percentile probability bands, also from the full sample. The coloured dotted lines are median estimates from the different subsamples. (Color figure online)

Robustness: reduced form model. Monetary policy shock(sign restrictions). Impulse responses from a monetary policy shock for all the models in Table 3. Identification is achieved through sign restrictions on impact. The lines are median estimates from the different models

Rights and permissions

About this article

Cite this article

Robstad, Ø. House prices, credit and the effect of monetary policy in Norway: evidence from structural VAR models. Empir Econ 54, 461–483 (2018). https://doi.org/10.1007/s00181-016-1222-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-016-1222-1