Abstract

Hedonic pricing, estimating the value of housing characteristics through the use of transactions data, is one of the most common tasks performed by real estate researchers. However, transaction frequency varies over time, locations, and other factors. In contrast, two-thirds of homeowners have mortgages that they pay each month. This manuscript explores the use of mortgage payment data as an alternative or supplemental means to derive the value of housing characteristics. Insofar as price affects default and housing characteristic values determine price, housing characteristic values affect default. The implicit housing characteristic values come from parameter values that fit observed patterns of payments and defaults. We find a strong correlation (0.74−0.92) between the transaction-based and the implicit approaches. In addition, the Monte Carlo simulation indicates that the mortgage based pricing model has potential to help reveal housing market information especially during low sales activity and/or high default rate situations.

Similar content being viewed by others

Notes

See Malpezzi (2003) for a general review of hedonic pricing as well as Goodman (1998) for a review of the early history of hedonic pricing involving Court (1939) and others. See Harrison and Rubinfeld (1978) for a hedonic pricing study involving pollution, Bateman et al. (2001) for a discussion of traffic and house prices as well as Brasington and Haurin (2006) for the relation between educational variables and house prices.

This is subject to all the conditions associated with the option approach to mortgage payment and default. To the degree that individuals systematically default for various other or subjective reasons, this reduces the power of this model to describe behavior. However, the importance of house prices in the default decision has widespread empirical support.

Pace and Zhu (2015) showed evidence that mortgage behavior reflects housing price information in a repeated sales setting.

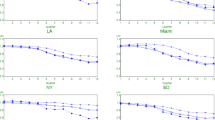

The impacts with different merge criteria are investigated, and the results are not sensitive to some specific merge criteria.

The BBx data has very few new purchase loans in recent years. In order to have enough sales, we need to combine all previous sales data together. In doing so, there could be a mismatch of sample periods for the implicit and the sales based samples.

References

Bateman, I., Day, B., Lake, I., & Lovett, A. (2001). The effect of road traffic on residential property values: a literature review and hedonic pricing study. Economic and Social Research Council.

Brasington, D., & Haurin, D.R. (2006). Educational outcomes and house values: a test of the value added approach. Journal of Regional Science, 46, 245–268.

Court, A.T. (1939). Hedonic price indexes with automobile examples, dynamics of automobile demand, (pp. 98–119). New York: General Motors.

Deng, Y., Quigley, J.M., & Order, R. (2000). Mortgage terminations, heterogeneity and the exercise of mortgage options. Econometrica, 68, 275–307.

Epperson, J.F., Kau, J.B., Keenan, D.C., & Muller, W.J. (1985). Pricing default risk in mortgages. Real Estate Economics, 13, 261–272.

Goodman, A.C. (1998). Andrew court and invention of hedonic pricing analysis. Journal of Urban Economics, 44, 291–298.

Harrison, D. Jr., & Rubinfeld, D.L. (1978). Hedonic housing prices and the demand for clean air. Journal of Environmental Economics and Management, 5(1), 81–102.

Kau, J.B., Keenan, D.C., & Kim, T. (1994). Default probabilities for mortgages. Journal of Urban Economics, 35, 278–296.

Keenan, M. (2015). Property sales are running at 50pc ‘normal’ rate, Irish Independent. July 14.

Koo, R., & Sasaki, M. (2008). Obstacles to affluence: thoughts on Japanese housing, NRI Papers, No. 137.

Malpezzi, S. (2003). Hedonic pricing models: a selective and applied review. In O’Sullivan, T., & Gibb, K. (Eds.) Section in housing economics and public policy: essays in honor of Duncan Maclennan. Oxford, UK: Blackwell Science Ltd.

Pace, R.K., & Zhu, S. (2015). Inferring price information from mortgage payment behavior: a latent index approach. Journal of Real Estate Finance and Economics, 1–22.

Zhu, S., & Pace, R.K. (2014). Modeling spatially interdependent mortgage decisions. Journal of Real Estate Finance and Economics, 49(4), 598–620.

Acknowledgments

The authors would like to thank Kiplan Womack, Jeffrey Cohen, Erik Johnson and Scott Wentland for their very insightful comments on the paper. We appreciate the very helpful comments from the other participants at the UConn Real Estate Symposium, the FMA 2015 conference, the ARES 2016 conference and the AREUEA 2016 conference. Shuang Zhu would like to thank the generous summer research support from K-State College of Business Administration. This research was partially supported by a grant from the National Science Foundation (award number: 1212112). All errors are our own.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Pace, R.K., Zhu, S. Implicit Hedonic Pricing Using Mortgage Payment Information. J Real Estate Finan Econ 54, 387–402 (2017). https://doi.org/10.1007/s11146-016-9578-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-016-9578-8