Abstract

This study investigates the different channels through which internationally active banks can provide loans abroad. Using data on German banks from 2002 to 2010, we contrast determinants for cross-border lending by the parent bank with lending by affiliates located abroad. We show that lending by parent banks is based almost entirely on supply-side determinants, in particular on bank-specific factors. The more the loans are intermediated by banks’ affiliates located abroad, the more relevant become foreign countries’ demand and risk characteristics. This applies in particular when banks operate via locally focused affiliates - rather than regionally active hub affiliates - as well as when the affiliates have the status of branches as opposed to legally independent subsidiaries. In general, banks with a greater risk aversion withdraw more from foreign lending during the financial crisis, especially following the collapse of Lehman Brothers. However, at a Tier I capital ratio of around 11 %, a further increase in the ratio did not affect lending anymore.

Similar content being viewed by others

Notes

For this, we use confidential micro data on German banking groups from the Deutsche Bundesbank, provided by the Research Data and Service Centre of the Deutsche Bundesbank.

Using aggregate data, Cetorelli and Goldberg (2011) find that the larger the pre-crisis dollar vulnerability of a country’s aggregate banking system, the lower was its post-crisis lending growth to emerging economies by parent banks and – to a lesser extent – by affiliates.

In a study on lending by affiliates of multinational banks from the EU, Navaretti et al. (2010) find that the internal capital market at least complements external sources of funding.

Dietrich and Vollmer (2010) model a trade-off: They also see the affiliates abroad profit from soft local information, but a potential local bank manager’s opportunistic behavior may render the bank’s internal capital markets inefficient.

This may apply, for instance, to syndicated loans or loans to multinational companies.

Capital markets also attributed some risk to large banks even before the financial crisis, which was reflected in bank-specific subordinated debt spreads (see Sironi 2003 who looks at large European banks).

An important reason to exclude short-term lending is that it includes trade financing, for which the determinants are different and cannot be accurately explained with our approach. This theory is underpinned by the estimation output for short-term lending provided in the robustness checks in Section 5. Besides see Fig. 1 for developments in overall private-sector loans by German banks and Fig. 2 for developments in long-term versus total foreign loans to the foreign private sector by the German banks examined in this study.

All institutions including their head institutions, acting as central banks for coop banks and saving banks, enter the sample separately.

In general, in our sample we deal with M&A through backward integration. In a very few cases, where strategical units with activities vis-à-vis several countries moved abroad – either because of sale or because of a regrouping from one bank to another within an international holding structure – we lose comprehensive information on this business field from then on. We therefore decided to drop the relevant observations.

The type of business with countries hosting large financial centers is largely driven by financial deals with special purpose entities as well as by banks’ proprietary trading in portfolio instruments – both businesses with motivations different to those of lending to the real economy. For the classification of offshore financial centers we use the definition of the Financial Stability Forum (2000), the predecessor of today’s Financial Stability Board, published in 2000. In addition, we exclude the UK and the US from our sample since they represent large financial hubs for German banks. However, we conduct a robustness check in Section 5 of the paper including the UK and the US. For the complete list of countries defined as financial centers, see Table 1.

As for Serbia and Montenegro, which split in 2006, most explanatory variables are available only for the former union, we treat these countries as one for the purpose of this analysis.

Next to the external positions of banks data, we use the Monthly balance sheet statistics (period: 2003Q1-2010Q4). For a detailed description of the External positions report, see Fiorentino et al. (2010). The activities of subsidiaries located abroad are reported by the German parent bank if it is the majority shareholder. There are no exemption limits for the reports.

The transaction data are calculated by the Bundesbank. The majority of cleaning is due to exchange rate movements. Here, the variations in the stocks denominated in foreign currency due to movements of the end-of-month exchange rates are eliminated. Besides, there is a correction for statistical effects, e.g. errors in compilation and adjustments by reporting banks. Finally, write-downs and write-ups that are reported by the banks are taken out – however, only for the parent bank entity and not for the affiliates for which no such data are filed.

The correlation between the amount of foreign lending and having an affiliate in the same country amounts to 26 %.

It also equals 0 if bank i does not supply any loans at all to country k (either via the parent bank or via affiliates located abroad). The quality of the results remains unchanged in a robustness check which, for the assessment of affiliate relevance, excludes banks that do not supply any loans at all to country k.

According to the F-tests, all groups of variables are, in their respective specifications, jointly significant.

20 As mentioned in footnote 18, in a robustness check, we exclude banks that do not supply any loans at all to a country. The quality of the results remains unchanged.

We specifically rely on risk-weighted assets as, in our opinion, they best mirror the risk incorporated in a parent bank’s balance sheet total. In a study on the implications of monetary policy for German bank lending, Ehrmann et al. (2001) also points this out. Of course, the Tier 1 to RWA ratio may also be shifted due to adjustments of the internally applied risk weight formulas. However, as these model shifts are infrequent (rare events) and as we refer to the change in the Tier 1 ratio rather than the level, they are not likely to have a substantial effect on our regression results.

Though, there is a mechanical link between lending and the capital ratio via the risk weighted assets which depend on lending and which enter the capital ratio in the denominator, we can treat it for different reasons as exogenous. First, this link is quantitatively very small. Nevertheless, the Tier 1 to RWA ratio enters our regressions with a lag. Besides, the amount of Tier 1 capital proves to be the driver behind changes in the capital ratio. We are more explicit on the endogeneity of this central variable in our robustness checks in Section 5.

Regulation and their implications for Tier 1 capital, especially within the scope of Basel III, came to the fore in the course of 2010. Therefore, it is possible to interpret changes in the capital ratio up to the end of our sample (2010) as a measure of risk aversion. Just after our period under review, from 2011 on, adjustments in this ratio more likely reflect preparations to meet the new requirements – which many banks intended to fulfill much before the official start of Basel III.

CAMEL stands for Capitalization, Asset Quality, Management, Earnings and Liquidity.

We believe our measure of capitalization (core capital / risk-weighted assets) to be the right one with regard to our interpretation of the capital ratio as an indicator of risk aversion. Nevertheless, other measures that do not include risk-weighted assets (Tier I capital to total assets, equity to total assets, etc.) are also used in the literature to assess capitalization (see the discussion by Kick et al. 2010). For example, Buch et al. (2009) find that banks with a higher ratio of Tier I capital to total assets are less likely to establish affiliates in foreign countries. Once abroad however, their activities seem to be more stable.

We use the average ratio of interest income to equity over the past four quarters in order to assess the performance of a bank over a longer period of time, and thus avoid issues of reverse causality.

With this profitability measure we refer to the classical measure return on equity. However, we restrict the income component to interest income as we view profitability in the lending business as most relevant for the maintenance of loan issuance during the crisis. Although the variable interest income to equity actually captures both profitability in lending and the relevance of the classical banking business, with our variable capital market activity we seek to isolate the latter effect more.

We take the average capital market activity over the past four quarters to better assess the bank’s strategy.

Giannetti and Laeven (2012) investigate international syndicated lending during the financial crisis and find an increasing home bias of lenders’ loan origination.

This prevents the results from being distorted by a pure scale effect, since it might be the case that large banks generally tend to carry out large loan transactions.

Using empirical checks, we can rule out that affiliates are per se more relevant in large foreign countries. The correlation between foreign country real GDP and affiliate relevance amounts to no more than about 7 %.

The BLS questions German banks about the credit standards that they set for long-term loans.

Fixed capital formation is a more direct way to capture loan demand, especially from non-bank firms, than GDP growth. A four-quarter average of fixed capital formation over GDP is used in order to better assess market potential. We do not, moreover, rely on lending by domestic banks (line 22d of the IFS statistics) as a proxy for loan demand. First, this variable does not capture any lending activities by other foreign banks. Second, likely competition in lending between local and foreign banks could distort the accuracy of the variable as a proxy for demand.

Many studies include Foreign Direct Investment (FDI) flows as explanatory variables for foreign lending (e.g. Buch 2000). We find that FDI is highly correlated with bilateral trade. We therefore agree with Jeanneau and Micu (2002) and do not include both factors in the regressions. As a large part of bilateral trade is closely related to FDI because it stems from intra-firm trade by multinational firms, we decided to concentrate on bilateral trade figures as an explanatory variable.

This interpretation of the variable Bilateral trade openness is supported by the fact that short-term loans and thus trade credit are excluded from the analysis.

As the financial cycle may differ significantly from an economy’s real cycle, stock market volatility is assumed to be a better measure for financial stability than e.g. the output gap.

The variable is averaged over four quarters in order to match the dimension in which we proxy for demand.

In unreported regressions we tested whether lending by local banks in the different countries is, on aggregate, related to proxies for local demand and risk. We were able to confirm that local banks’ lending to the private sector across the countries reacts to similar demand and risk factors like to those to which domestic bank lending reacts in Germany. Hence, German parent bank lending to these countries does indeed differ from the behavior of local banks, while affiliates behave more like the latter.

Furthermore, banks do not move to lending to the public sector in Germany: although, in a rather continuous fall from 2002 to February 2009 the stocks of loans to the German public sector went down from €437 billion to €302 billion, the figures subsequently remained rather stable from then onwards until the end of 2010.

A high value is defined as the average value of Other countries’ real GDP growth relative to localbeyond the 75th pctl. of the distribution. A low value is defined as the average value of Other countries’ real GDP growth relative to localbelow the 25th pctl. of the distribution.

An average of 65 % of subsidiaries’ total assets are accounted for by lending business, while for branches the comparable figure is 78 %. Hence subsidiaries’ business relies more on other activities, which is reflected in higher holdings of securities and other financial assets. Within the loan portfolio, which is also comprised of loans to banks and governments, subsidiaries issue roughly 1/4 to foreign firms, while branches allocate more than 1/3 of their lending to this type of borrower.

References

Aiyar (2012) From financial crisis to great recession: the role of globalized banks. Amer Econ Rev Papers Proc 102:225–230

Altunbas Y, Gambacorta L, Marques-Ibanez D (2009). Bank risk and monetary policy. ECB Working Paper Series, No. 1075

Buch C (2000) Why do banks go abroad? Evidence from German data. Fin Markets, Instit Instr 9(1):33–67

Buch C, Koch C, Kötter M (2009) Margins of international banking: is there a productivity pecking order in banking, too? Discussion Paper, Series 2, Banking and Financial Studies, No. 12/2009. Economic Research Centre, Deutsche Bundesbank

Buch C, Koch C, Kötter M (2011) Crises, rescues, and policy transmission through international banks. Discussion Paper, Series 1, Economic Studies, No. 15/2011. Economic Research Centre, Deutsche Bundesbank

Deutsche Bundesbank (2009) Developments in lending to the German private sector during the global financial crisis, Deutsche Bundesbank. Monthly Report, September 2009, 15–32

Calvo G, Leiderman L, Reinhart C (1993) Capital inflows and real exchange rate appreciation in Latin America – the role of external factors. IMF Staff Papers 40:108–151

Campello M (2002) Internal capital markets in financial conglomerates: evidence from small bank responses to monetary policy. J Fin 57:2773–2805

Cetorelli N, Goldberg L (2012) Banking Globalization and monetary transmission. J Fin 67:1811–1843

Cetorelli N, Goldberg L (2011) Global banks and international shock transmission: evidence from the crisis. IMF Econ Rev 59(1)

Chuhan P, Claessens S, Mamingi N (1998) Equity and bond flows to Latin America and Asia: the role of global and country factors. J Develop Econ 55:439–463

Cohen B H (2013) How have banks adjusted to higher capital requirements? BIS Q Rev, September 2013, 25–66

Dietrich Diemo, Vollmer Uwe (2010) International banking and liquidity allocation cross-border financial services versus multinational banking. J Fin Serv Res 37:45–69

de Haas R, van Horen N (2013) Running for the exit: international bank lending during a financial crisis. Rev Fin Stud 26(1):244–285

de Haas R, van Horen N (2012) International shock transmission after the Lehman brothers collapse: evidence from syndicated lending. Amer Econ Rev Papers Proc 102:231–237

de Haas R, van Lelyfeld I (2006) Foreign banks and credit stability in Central and Eastern Europe. A panel data analysis. J Bank Fin 30:1927–1952

de Haas R, van Lelyfeld I (2010) Internal capital markets and lending by multinational bank subsidiaries. J Fin Intermed 19:1–25

Ehrmann M, Gambacorta L, Martinez-Pargez J, Sevestre P, Worms A (2001) Financial systems and the role of banks in monetary policy transmission in the euro area. Bundesbank Discussion Paper, No. 18/2001. Economic Research Centre, Deutsche Bundesbank

Financial Stability Forum (2000) Press Release, May 26

Fiorentino E, Koch C, Rudek W (2010) Technical documentation microdatabase: external position reports of German banks. Deutsche Bundesbank, Technical Documentation

Frey R, Kerl C (2015) Multinational banks in the crisis: foreign affiliate lending as a mirror of funding pressure and competition on the internal capital market. J Bank Fin 50:52–68

Giannetti M, Laeven L (2012) The flight home effect: evidence from the syndicated loan market during financial crises. J Fin Econ 104:23–43

Hempell H, Sorensen C (2010) The impact of supply constraints on bank lending in the euro area: crisis induced crunching? ECB Working Paper Series. No. 1262

Houston J, James C (1998) Do bank internal capital markets promote lending? J Bank Fin 22:899–918

Jeanneau S, Micu M (2002) Determinants of international bank lending to emerging market countries. BIS Working Paper No. 112. Bank for International Settlements, Basel

Kick T, Koetter M (2007) Slippery slopes of stress: ordered failure events in German banking. Discussion Paper,Series 2, Banking and Financial Studies, No. 03/2007. Economic Research Centre, Deutsche Bundesbank

Kick T, Koetter M, Poghosyan T (2010) Recovery determinants of distressed banks: regulators, market discipline, or the environment? Discussion Paper,Series 2, Banking and Financial Studies, No. 02/2010. Economic Research Centre, Deutsche Bundesbank

Kishan R, Opiela T (2000) Bank size, bank capital, and the bank lending channel. J Money Credit Bank 32(1):121–141

McCauley R, McGuire P, von Peter G (2010) The architecture of global banking: from international to multinational? BIS Q Rev, March 2010, 25–37

McGuire P, Tarashev N (2008) Bank health and lending to EMs. BIS Q Rev, December 2008, 67–80

Navaretti G, Calzolari G, Pozzolo A, Levi M (2010) Multinational banking in Europe - financial stability and regulatory implications: lessons from the financial crisis. Econ Pol, October 2010, 703–753

Olivero M, Li Y, Jeon B (2011) Competition in banking and the lending channel: evidence from bank-level data in Asia and Latin America. J Bank Fin 35:560–571

Peek J, Rosengren E (2000) Implications of the globalization of the banking sector: the Latin American experience. New England Econ Rev, September/October 2000, 45–63

Rose A, Wieladek T (2011) Financial protectionism: the first tests. External MPC Unit Discussion Paper, No. 32, Bank of England

Sironi A (2003) Testing for market discipline in the European banking industry: evidence from subordinated debt issues. J Money Credit Bank 35(3):443–472

Acknowledgments

This paper represents the personal opinions of the authors and does not necessarily reflect the views of the Deutsche Bundesbank.

This paper has benefited from valuable comments by Carmela D’Avino, Jörg Breitung, Claudia Buch, Ulrich Grosch, Heinz Herrmann, Thomas Kick, Cordula Munzert, Winfried Rudek, Peter Tillmann and the participants of the Bundesbank Workshop on The Costs and Benefits of International Banking in Eltville. All remaining errors and inaccuracies are our own. The paper was written while receiving financial support from the University of Giessen (C. Kerl), which we gratefully acknowledge.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix: A Figures

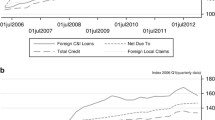

Overall non-bank private-sector loans of German banks. This graph depicts overall private-sector lending to Germany and to all foreign countries by the German banking system. The series are based on monthly observations reported to the Deutsche Bundesbank by German banks and their affiliates (branches and subsidiaries) located abroad. Source: Deutsche Bundesbank, Monthly balance sheet statistics and External positions of banks, 2002Q2-2010Q4 / own calculations

Foreign non-bank private-sector loans issued by selected German banks: transaction-induced development versus stocks. This graph is based on the sample of 69 banks that are used for the analysis in this paper. Banks qualify for our sample if they are among the top 100 largest banks and are domestically owned. Besides, promotional banks (directly or indirectly government-owned and with special tasks serving the German economy) are excluded. Owing to a number of bank mergers in the period under review, which we handle by backward integration, we include figures for 140 banks overall. The sample covers 84 % of total foreign private-sector lending by the German banking system. The underlying monthly series have been transformed into quarterly series. Dashed series represent our own calculations: Transaction-induced changes in foreign lending are added to the stock of foreign loans of German banks vis-á-vis the foreign private sector observed in 2002Q2. Source: Deutsche Bundesbank, Monthly balance sheet statistics and External positions of banks, 2002Q2-2010Q4 / own calculations

Model. This figure illustrates the empirical approach that we follow. >>Realized loan variation << describes the depended variable in the empiricial estimation, while the four sets of factors are explanatory variables

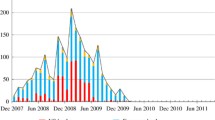

Components of the change in core capital ratio. In this graph we split the change in core capital ratios of banks in our sample (69 banks that are used for the analysis in this paper) into three components: the change in Tier 1 capital, the change in risk-weighted assets relative to the balance sheet total (which represents the average riskiness of the assets), and the adjustment of the balance sheet total. This decomposition is done three times, from 2003Q3 to 2007Q2 (pre-crisis), from 2007Q3 to 2008Q2 (crisis: pre-Lehman) and from 2008Q3 to 2010Q4 (crisis: post-Lehman). Figures are averages over time periods, and within each period weighted averages of all banks in the sample (balance sheet totals serve as weights). We thereby follow the methodology put forward by Cohen (2013). Source: Deutsche Bundesbank, Monthly balance sheet statistics and External positions of banks, 2003Q3-2010Q4 / own calculations

Appendix: B Tables

Rights and permissions

About this article

Cite this article

Frey, R., Kerl, C. & Lipponer, A. Withdrawal from Foreign Lending in the Financial Crisis by Parent Banks and Their Branches and Subsidiaries: Supply Versus Demand Effects. J Financ Serv Res 54, 1–48 (2018). https://doi.org/10.1007/s10693-016-0260-3

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10693-016-0260-3