Abstract

Inference on impulse response functions from vector autoregressive models is commonly done using bootstrap methods. These methods can be inaccurate in small samples and for persistent processes. This article investigates the construction of skewness-adjusted confidence intervals and joint confidence bands for impulse responses with improved small sample performance. We suggest to adjust the skewness of the bootstrap distribution of the autoregressive coefficients before the impulse response functions are computed. Using extensive Monte Carlo simulations, the approach is shown to improve the coverage accuracy in small- and medium-sized samples and for unit-root processes.

Similar content being viewed by others

Notes

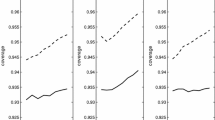

Berkowitz and Kilian (2000, p. 30) conjecture that the poor performance of the bootstrap confidence intervals in the presence of unit roots and roots close to unity is due to small sample bias. The evidence presented in this article suggests that the skewness plays an important role.

Simulations of DGPs with higher lag orders than considered here or by Kilian (1998b) indicate that the AICc might provide to low estimated lag orders and the AIC might be preferable. Research into the optimal information criterion for bootstrap confidence intervals and bands at different sample sizes may be helpful.

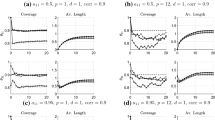

Note that the 100% coverage in the initial period in the third quadrant is due to this IRF being restricted to zero by the Cholesky decomposition, which is in accordance with the assumed DGP.

This supposes that we equally dislike positive and negative deviations from the nominal coverage level. Arguably, too low coverages might be considered as a more severe violation of the idea underlying the construction of confidence intervals.

References

Akaike, H.: A new look at the statistical model identification. IEEE Trans. Autom. Control 19(6), 716–723 (1974)

Basawa, I.V., Mallik, A.K., Cormick, W.P., Reeves, J.H., Taylor, R.L.: Bootstrapping unstable first-order autoregressive processes. Ann. Stat. 19, 1098–1101 (1991)

Benkwitz, A., Neumann, M.H., Lütekpohl, H.: Problems related to confidence intervals for impulse responses of autoregressive processes. Econom. Rev. 19(1), 69–103 (2000)

Berkowitz, J., Kilian, L.: Recent developments in bootstrapping time series. Econom. Rev. 19(1), 1–48 (2000)

Bose, A.: Edgeworth correction by bootstrap in autoregressions. Ann. Stat., 1709–1722 (1988)

Efron, B.: Nonparametric standard errors and confidence intervals. Can. J. Stat. 9, 139–172 (1981)

Efron, B., Tibshirani, R.: Bootstrap methods for standard errors, confidence intervals, and other measures of statistical accuracy. Stat. Sci. 1(1), 54–75 (1986)

Grabowski, D., Staszewska-Bystrova, A., Winker, P.: Generating prediction bands for path forecasts from SETAR models. Stud. Nonlinear Dyn. Econom. 21(5) (2017)

Hall, P.: The Bootstrap and Edgeworth Expansion. Springer, New York (1992)

Hurvich, C.M., Tsai, C.L.: Regression and time series model selection in small samples. Biometrika 76, 297–307 (1989)

Hurvich, C.M., Tsai, C.L.: A corrected Akaike information criterion for vector autoregressive model selection. J. Time Ser. Anal. 14, 272–279 (1993)

Inoue, A., Kilian, L.: Bootstrapping autoregressive processes with possible unit roots. Econometrica 70(1), 377–391 (2002)

Inoue, A., Kilian, L.: The continuity of the limit distribution in the parameter of interest is not essential for the validity of the bootstrap. Econom. Theory 19(6), 944–961 (2003)

Inoue, A., Kilian, L.: Inference on impulse response functions in structural VAR models. J. Econom. 177(1), 1–13 (2013)

Inoue, A., Kilian, L.: Joint confidence sets for structural impulse responses. J. Econom. 192(2), 421–432 (2016)

Kilian, L.: Small-sample confidence intervals for impulse response functions. Rev. Econ. Stat. 80(2), 218–230 (1998a)

Kilian, L.: Accounting for lag order uncertainty in autoregressions: the endogenous lag order bootstrap algorithm. J. Time Ser. Anal. 19(5), 531–548 (1998b)

Kilian, L.: Finite-sample properties of percentile and percentile-t bootstrap confidence intervals for impulse responses. Rev. Econ. Stat. 81(4), 652–660 (1999)

Kilian, L.: Impulse response analysis in vector autoregressions with unknown lag order. J. Forecast. 20, 161–179 (2001)

Kilian, L., Lütkepohl, H.: Structural Vector Autoregressive Analysis. Cambridge University Press, Cambridge (2017)

Kim, J.H.: Bias-corrected bootstrap prediction regions for vector autoregression. J. Forecast. 23(2), 141–154 (2004)

Lütkepohl, H.: Comparison of criteria for estimating the order of a vector autoregressive process. J. Time Ser. Anal. 6, 35–52 (1985)

Lütkepohl, H.: Asymptotic distributions of impulse response functions and forecast error variance decompositions of vector autoregressive models. Rev. Econ. Stat. 72(1), 116–125 (1990)

Lütkepohl, H.: New Introduction to Multiple Time Series Analysis. Springer, Berlin (2005)

Lütkepohl, H., Staszewska-Bystrova, A., Winker, P.: Comparison of methods for constructing joint confidence bands for impulse response functions. Int. J. Forecast. 31(3), 782–798 (2015)

Lütkepohl, H., Staszewska-Bystrova, A., Winker, P.: Confidence bands for impulse responses: Bonferroni vs. Wald. Oxf. Bull. Econ. Stat. 77, 800–821 (2015)

Pope, A.L.: Biases of estimators in multivariate non-Gaussian autoregressions. J. Time Ser. Anal. 11(3), 249–258 (1990)

Sims, C.A., Zha, T.: Error bands for impulse responses. Econometrica 67(5), 1113–1155 (1999)

Staszewska, A.: Representing uncertainty about response paths: the use of heuristic optimisation methods. Comput. Stat. Data Anal. 52(1), 121–132 (2007)

Staszewska-Bystrova, A., Winker, P.: Constructing narrowest pathwise bootstrap prediction bands using Threshold Accepting. Int. J. Forecast. 29(2), 221–233 (2013)

Staszewska-Bystrova, A., Winker, P.: Measuring forecast uncertainty of corporate bond spreads by Bonferroni-type prediction bands. Cent. Eur. J. Econ. Model. Econom. 2, 89–104 (2014)

Stine, R.A.: Estimating properties of autoregressive forecasts. J. Am. Stat. Assoc. 82(400), 1072–1078 (1987)

Sugiura, N.: Further analysis of the data by Akaike’s information criterion and the finite corrections. Commun. Stat. A7, 13–26 (1978)

Wolf, M., Wunderli, D.: Bootstrap joint prediction regions. J. Time Ser. Anal. 36(3), 352–376 (2015)

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We are indebted to Lutz Kilian and Helmut Lütkepohl for helpful comments on an earlier draft of this paper. We also wish to thank participants of the 2018 European Summer Meeting of the Econometric Society and of the Jahrestagung des Vereins für Socialpolitik 2018 for helpful discussions. The authors are responsible for all remaining shortcomings. Support from the National Science Center, Poland (NCN) through MAESTRO 4: DEC-2013/08/A/HS4/00612 is gratefully acknowledged.

Appendix

Appendix

See Tables 7, 8, 9, 10, 11, 12, 13, 14, and 15

Rights and permissions

About this article

Cite this article

Grabowski, D., Staszewska-Bystrova, A. & Winker, P. Skewness-adjusted bootstrap confidence intervals and confidence bands for impulse response functions. AStA Adv Stat Anal 104, 5–32 (2020). https://doi.org/10.1007/s10182-018-00347-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10182-018-00347-9