Abstract

Background

During the last decade, pharmaceutical spending for patients with attention-deficit-hyperactivity disorder (ADHD) has been escalating internationally.

Objectives

First, to estimate future trends of ADHD-related drug expenditures from the perspectives of the statutory health insurance (SHI; Gesetzliche Krankenversicherung, GKV) in Germany and the National Health Service (NHS) in England, respectively, for children and adolescents age 6 to 18 years. Second, to evaluate the budgetary impact on individual prescribers (child and adolescent psychiatrists and pediatricians treating patients with ADHD) in Germany.

Methods

A model was developed to predict plausible scenarios of future pharmaceutical expenditures for treatment of ADHD. Model inputs were derived from demographic and epidemiological data, a literature review of past spending trends, and an analysis of new pharmaceutical products in development for ADHD. Only products in clinical development phase III or later were considered. Uncertainty was addressed by way of scenario analysis. For each jurisdiction, five scenarios used different assumptions of future diagnosis prevalence, treatment prevalence, rates of adoption and unit costs of novel drugs, and treatment intensity.

Results

Annual ADHD pharmacotherapy expenditures for children and adolescents will further increase and may exceed €310 m (D; E: ₤78 m) in 2012 (2002: ~€21.8 m; ~₤7.0 m). During this period, overall drug spending by individual physicians may increase 2.3- to 9.5-fold, resulting from the multiplicative effects of four variables: increased number of diagnosed cases, growing acceptance and intensity of pharmacotherapy, and higher unit costs of novel medications.

Discussion

Even for an extreme low case scenario, a more than six-fold increase of pharmaceutical spending for children and adolescents is predicted over the decade from 2002 to 2012, from the perspectives of both the NHS in England and the GKV in Germany. This budgetary impact projection represents a partial analysis only because other expenditures are likely to rise as well, for instance those associated with physician services, including diagnosis and psychosocial treatment. Further to this, by definition budgetary impact analyses have little to nothing to say about clinical appropriateness and about value of money.

Conclusion

Providers of care for children and adolescents with ADHD should anticipate serious challenges related to the cost-effectiveness of interventions.

Similar content being viewed by others

Background

In the United States, identification of attention-deficit/hyperactivity disorder (ADHD) among children and adolescents showed the greatest increase of all categories of psychosocial problems [1], and the percentage of children with a diagnosis of ADHD receiving medications increased from 32% in 1979 to 78% in 1996 [1–3]. For the mid-1990s, overall psychostimulant treatment prevalence rates in children and adolescents were found at about 2.5% [4], ranging from 1.9% in a California health plan [5] to 3.0% in national database analyses [6, 7]. In the late 1990s, growth rates of stimulant prescriptions accelerated in the United States [8, 9]. For 1997, treatment prevalence was reported at 4.1% (or 78% of children with ADHD) [10]. In a survey of school nurses conducted in Baltimore, Maryland, in 1998, 2.92% of all public school students (N = 816,465) were administered a medication for ADHD in school; 84% of those (2.46%) received methylphenidate [4]. In 1999, in a nationally representative, commercially insured sample population 5 to 14 years old, the one-year prevalence of stimulant treatment was 4.2 percent in the United States [11]. According to another survey conducted between 1997 and 1999 among parents of elementary school children in public elementary schools in North Carolina, medication prevalence was even 7% in the population studied, with stimulants accounting for 93% of the prescriptions [12]. More recent data have been somewhat contradictory, with one analysis finding a treatment prevalence of 4.8% in children (age 6–12 years) and 3.2% in adolescents (age 13–19 years), suggesting that the steep increase of the late 1990s may have attenuated in these age groups [13], whereas another study published by Medco Health Solutions [14], a large U.S. pharmacy benefit management organization, still found the number of individuals age 19 years or younger using ADHD medications increasing by 49% (males) and 82% (females) between 2000 and 2004.

Meanwhile, the growth of pediatric psychotropic prescriptions has become an international phenomenon [15]. For stimulant treatment, similar trends as in the US – albeit at lower absolute levels – have been observed in Canada [16] and Europe. For instance, in Spain the consumption of methylphenidate increased by 8% annually from 1992 to 2001 [17]. A study in six general practices in the Netherlands showed a threefold rise of methylphenidate users between 1998 and 2003 [18]. In England, the number of methylphenidate prescriptions dispensed in the community increased from 126,000 in 1998 to 389,200 in 2005 (or +207%; cf. Figure 1a), compared to a total growth of prescriptions of +40% during the same period [19]. In Germany, the number of defined daily doses (DDDs) of methylphenidate prescribed for outpatients insured by statutory sick funds ("Gesetzliche Krankenversicherung", GKV, covering approximately 90% of the German population) grew 47-fold between 1992 and 2005 [20], while total prescriptions written in Germany decreased by 41% in the same period (cf. Figure 2).

ADHD-related prescriptions and expenditures in England, 1998 – 2005. a: Prescription items dispensed in the community; b: Expenditures by category p.a.; DEX: dexamphetamine (DexedrineR and others); MPH: methylphenidate; IR: immediate-release formulations (RitalinR and generics); MR: modified-release formulations (ConcertaR XL, EquasymR XL; RitalinR SR imports); MOD: modafinil (ProvigilR, licensed for daytime sleepiness); ATX: atomoxetine (StratteraR); PEM: pemoline (VolitalR, before 2002 only, not shown due to small volume); data source: NHS Prescription Cost Analysis 1999–2006 [19]. Note that these data include prescriptions for adults with ADHD and also for other indications (narcolepsy).

Methylphenidate prescriptions trend in Germany, 1992 – 2005. Methylphenidate prescriptions grew 47-fold from 1992 to 2005. During the same period, total prescriptions in Germany declined by 41 percent. Data source: Wissenschaftliches Institut der AOK, Schwabe and Paffrath, 1993 – 2006 [20]; note change of database for year 2001/2002. All data refer to prescriptions reimbursed by statutory health insurance (SHI, "GKV", covering approximately 90 percent of German population); excluding parallel imports. Note that these data include prescriptions for adults with ADHD and also for other indications (narcolepsy).

Much of the debate triggered by this trend has focused on medical aspects, such as concerns about potential overuse of psychostimulants [21, 22] and adverse treatment effects [23]. It has, however, been argued that underuse may be more of a problem, at least in Europe [24], and low rates of recognition of ADHD or hyperkinetic disorder in the United Kingdom were associated with insensitive diagnostic assessments [25]. Recent German methylphenidate prescription analyses based on a regional sample of 11,235 children and adolescents with a diagnosis of ADHD in Germany (year 2003) did not reveal overuse [26]. Even for the United States, no evidence was found to substantiate claims of abuse and inappropriate use of methylphenidate [27], although there have been occasional reports on diversion to peers of stimulant medications, especially short-acting formulations [28, 29].

Beyond clinical implications, in an era of limited available resources, the economic dimension associated with increased health care utilization can no longer be ignored. In economic terms, the opportunity cost of medical interventions will be approximated by their budgetary impact – in particular, if a payers' perspective is adopted. Indeed, budgetary impact analyses are requested by a growing number of health care policy makers as an input into the decision-making process about health care resource allocation [30]. In practice, results of such analyses are frequently interpreted with a notion of "affordability" in mind. Unfortunately budget impact may exceed the pure effects of increased treatment rates if, for instance, rates of diagnosis (administrative prevalence), unit costs (for instance owing to introduction of novel, usually more expensive treatment options, which may be used in addition to or substituting cheaper alternatives), or treatment intensity (in terms of dose or duration) change simultaneously. No doubt, all these factors come into play in ADHD among children and adolescents. More than this, they may interact with each other, reinforcing their combined effects: for instance, availability of more expensive novel medications will result in enhanced communication and promotional efforts by their manufacturers, which in turn will – in addition to their direct influence on physician treatment choices (i.e., increase market share) – influence awareness and identification of the disorder (i.e., increase market size and aggregate number of prescriptions [25, 31, 32]). Furthermore, recent results of long-term clinical trials such as the landmark NIMH Multimodal Treatment Study (MTA) have demonstrated the effectiveness, in particular in terms of ADHD core symptom relief, of an intense medication management strategy [33–38]), thus contributing to the increasing acceptance and intensity of pharmacotherapy.

With the introduction of new products commanding higher units costs (cf. Table 1), growth of pharmaceutical spending has outpaced the rising number of prescriptions. In the United States, prescription drug expenditures for ADHD in children increased by 183% between 2000 and 2003. By 2003, spending on behavioral medications to treat children had overtaken both the antibiotic and asthma segments, which are traditionally high-use categories in pediatric medicine [39]. According to IMS data, total U.S. sales of ADHD drugs reportedly rose from US-$759 million in 2000 to US-$3.1 billion in 2004 [40]. Analysts from Merrill Lynch expect the U.S. ADHD market (including adult patients) to exceed US-$4 billion by 2010 on the back of new products (cf. below, Table 2[41]).

In Germany, total GKV outpatient spending for psychostimulants rose from €1.25 m in 1995 to €23.7 m in 2002 (before the first modified-release product had been launched) and €51.6 million in 2004 [20], 56% of which were accounted for by MPH-MR12. Spending for ADHD medications reached €82 million in 2005, exceeding our earlier forecasts, which had predicted annual expenditures of approximately €108 million (range from €62 to €155 million) by 2009 [42, 43]. Apart from the launch of atomoxetine in March 2005, this substantial increase was primarily driven by spending for two modified-release preparations of methylphenidate (cf. Table 1), both of which ranked among the top-100 products in terms of sales [44].

In England spending for ADHD-related pharmacotherapy, including modafinil and atomoxetine, increased from 1998 (₤3.1 million) to 2005 (₤24.4 million) by +695% (Figure 1b), again exceeding the growth of prescriptions (for ADHD treatments between 1998 and 2005, +132%)[19]. One new product (MPH-MR12, cf. Table 1) alone accounted for 42% of prescriptions, and 45% of pharmaceutical expenditures, for ADHD in 2005 [19]. Average costs per prescription rose steadily from ₤13.68 in 1998 to ₤46.94 in 2005, driven by price increases for dexamphetamine and a shift to more expensive new products: Combined, all new products with once-daily administration (in principle, MPH-MR08, MPH-MR12, Ritalin SR, and ATX) accounted for 54% of total ADHD-related prescriptions and 65% of sales in 2005 [19]. These Prescription Cost Analysis data for England do not include items dispensed in hospitals.

The high rate of adoption of new products with once-a-day administration schedules reflects the well-known problems associated with administration of a mid-day dose (during school) in children and adolescents with ADHD [45, 46]. Obviously, here a disorder-specific clinical need contributes to the fact that current trends of ADHD prescribing behavior mirror a more general pattern encountered in European pharmaceutical markets, namely, that the diffusion of new products consistently represents the single most important growth driver [47]. These observations raise the urgent question whether, and to what extent, pharmaceutical spending for children and adolescents with ADHD may continue to escalate in the foreseeable future. It is the purpose of this paper to shed some light on this issue, using the examples of England and Germany.

Methods

A forecasting model was developed to project the likely pharmaceutical expenditures for children and adolescents (age 6–18 years) with a diagnosis of ADHD in England and Germany through 2012, specifying assumptions and assumed relationships between variables in a transparent manner. Model outcomes were used to estimate the impact on drug spending by individual German physicians involved in care for ADHD patients, after validation of the model by replicating historic data (from 1998 to 2005). Key uncertainties were addressed using scenario analysis, combining objective information with specific assumptions about future events [48].

The model was restricted to pharmaceutical spending. It combined, in a hierarchical structure, (1) epidemiological information (demographic and prevalence data) with assumptions on (2) recognition rates (diagnosis prevalence), (3) rate of patients receiving drug therapy (treatment prevalence), (4) availability and adoption of new products, incorporating information on therapeutic profiles, (5) diffusion and market shares for alternative preparations, by category and by product, including generic substitution, (6) treatment intensity (expressed as average number of days times defined daily doses), (7) acquisition cost per defined daily dose for each product, from the perspectives of the NHS (England) or the GKV (Germany), respectively. For validation of the model, available data on the variables above were used to compare model outcomes with the historic evolution of drug spending in England and Germany. Extensions of the model were used to estimate the impact of the projections on drug budgets of individual pediatricians and specialists in child and adolescent psychiatry participating in care for patients with ADHD in Germany. Details on data sources and assumptions are provided in Table 2.

Results

1. New products in development (and further assumptions)

The market for ADHD treatment has attracted pharmaceutical companies to invest heavily in new product development. Results of literature searches and the database analysis [49] are summarized in Table 3.

A number of further pharmaceutical preparations and variants of methylphenidate are in phase III of clinical development in Europe, some of which have already received marketing authorization in the United States. These include a transdermal system (TDS, approved as DaytranaR in the United States, April 2006) of methylphenidate with duration of action of 12 hours (wear time, 9 hours). At present, in the absence of head-to-head trials against established oral formulations, the main advantage of this product seems to be convenience-related [49–51]. For modeling, it has therefore been assumed that it would capture no more than 10% of methylphenidate prescriptions. This implies the expectation that there will be no significant problems associated with skin sensitization.

Dexmethylphenidate, the chirally pure active isomer of methylphenidate, has been licensed as FocalinR (Novartis) in the US in May 2005, also as an extended-release formulation [49, 52]. As there is currently no evidence of superiority in terms of efficacy or tolerability [49, 53], it has been assumed that FocalinR will become available in Europe without a price premium over branded immediate-release (RitalinR, also Novartis) or modified-release methylphenidate (ConcertaR, Janssen-Cilag), respectively. Given its investment in FocalinR, it has been considered unlikely that Novartis would launch RitalinR LA (a long-acting preparation of methylphenidate available in the United States and some other markets) in England and Germany.

At the time of writing, few scientific data were in the public domain about lisdexamphetamine mesylate (NRP104), a new chemical entity that is an inactive prodrug of amphetamine believed to have a reduced potential for abuse and overdose compared to other ADHD drugs. The reason is that the amphetamine is conjugated to a specific amino acid and is activated only when metabolized in the gastrointestinal tract. Shire filed the product with the Food and Drug Administration (FDA) in December 2005 for the treatment of ADHD in children aged 6 to 12. Phase III study results presented at the Annual Meeting of the American Psychiatric Association in Toronto, May 2006, indicated similar efficacy and tolerability compared to mixed amphetamine salts (AdderallR) and duration of action of 12 hours [49]. A preliminary review of NRP104 by the U.S. Drug Enforcement Administration indicated that the compound would not be subject to controlled-substance scheduling [54], although this initial judgment has been revised since. The compound was launched by Shire in the United States end of July 2007 under the trade name "VyvanseR". For modeling it was assumed that the product will be introduced to the English and German markets in 2008 and (except for the "Extremely Low Case" scenario) overtake modified-release methylphenidate products in terms of prescriptions by 2012. Obviously, this rests on the assumption that clinical advantages of NRP104 (regarding abuse potential, possibly tolerability profile, as well as label and summary of product characteristics) will be confirmed.

Modafinil has been licensed as "ProvigilR" as a wake-promoting agent for patients with narcolepsy and shift work sleep disorder in the United States and England. Its manufacturer, Cephalon, has reformulated modafinil for children as once-daily 85 mg film-coated tablets, which it claims to be smaller and easier to swallow. Of note, this change of formulation should protect the new indication from generic competition [49]. While its mechanism of action is not fully understood, modafinil is classified as nonstimulant [55–57]. Similar to atomoxetine [58], a selective norepinephrine reuptake inhibitor, improvement of core symptoms had an effect size on core symptoms (school version of ADHD-RS) of 0.69 [59] to 0.76 [60]. This compares to effect sizes around 1.0 typically achieved with stimulants [58]. In August 2006, Cephalon announced discontinuation of modafinil development for ADHD due to safety concerns raised by the FDA, and the company intends to replace modafinil by its successor compound in development, armodafinil [61]. It has been assumed for modeling that armodafinil (like atomoxetine [62, 63]) would become a second line treatment option after stimulants.

Finally, mixed amphetamine salts are marketed successfully in the U.S. (AdderallR, AdderallR XR, by Shire) but have been licensed neither in England nor in Germany. It is believed that these products will not become available in Europe. Further compounds in phase II clinical development for ADHD include selective GABA-B receptor antagonists (SGS742, by Saegis, a privately held company with Novartis among its investors) and ampakine molecules (by Cortex). These projects have been excluded from the present study in light of their inherent uncertainty; statistically, attrition rates of compounds in clinical phase II are as high as 62% [64].

2. Projected budgetary impact from the perspectives of the German Statutory Health Insurance (SHI, GKV) and the National Health Service (NHS) in England

First, the model was calibrated using data on ADHD-related prescriptions and expenditures from 1998 to 2005 (cf. above). Besides a base case for projection through 2012 (Figure 3), four additional scenarios were defined to address the uncertainty surrounding critical assumptions (for details, see above and Table 4). Two scenarios (upper and lower bounds of base case) represented plausible variants, assuming different rates of treatment prevalence and intensity. Two further scenarios reflected extremes, the lower one assuming no price premiums for the new products and low treatment intensity, while the high extreme combined the effects of intense treatment with higher price premiums for new products.

Projected prescription drug expenditures for ADHD in children and adolescents, 2001 – 2012 (base case). a, b: Defined daily doses (DDDs) p.a.; c, d: expenditures by category p.a.; e, f: total (cumulated) expenditures p.a.; left: England; right: Germany. MPH: methylphenidate; IR: immediate-release formulations (RitalinR, branded generics [EquasymR, MedikinetR], generics; FocalinR); MR: modified-release formulations (ConcertaR XL, EquasymR XL, MedikinetR retard, FocalinR XR; MPH-Patch: transdermal system (DaytranaR); LisDEX: lisdexamphetamine (NRP104); Nonstimulants: atomoxetine (StratteraR), armodafinil (NuvigilR); DEX: dexamphetamine (England only).

While all scenarios will be described briefly below, Tables 4 and 5 have been limited to a more detailed account of the base case and the extreme scenarios. Interested readers may retrieve the full details from our Institute's website [97].

The base case scenario, which is believed to reflect the most probable course of future events, implies an increase of drug spending for children and adolescents with ADHD for year 2012 by a factor of 12 (GKV in Germany) or 10 (NHS in England) over 2002. Assuming an annual growth rate of 5% for drug expenditures between 2005 and 2012 (except for ADHD in children and adolescents), then the projected ADHD treatment costs (from the NHS perspective, £78 million) would make up 3.8% of NHS spending for CNS drugs in 2012, compared to just 0.77% in 2002. For the German GKV (projected spending, €311 million), the corresponding figures would be 12.9% of total spending for psychotropic drugs in 2012, compared to 1.8% in 2002. This increase is driven by the multiplicative effects of increasing awareness and recognition of ADHD, growing rates of pharmacotherapy, somewhat increased intensity (dose and duration) of treatment, and the shift to novel, more expensive products (cf. Figure 3). The upper and lower bounds of the base case can be interpreted as sensitivity analyses with regard to treatment intensity; these indicate a plausible range of spending estimates from €259 to €380 million in Germany and from £63 to £101 million in England in 2012. The differences between both jurisdictions reflect the effects of differences in population size, unit costs, available products, and a lower baseline and less dynamic increase in England compared to Germany.

The extremely high scenario indicates the sensitivity of projections to higher prices of new products (cf. Tables 4 and 5). Additional scenarios were computed and fell within the range indicated. Of note, a scenario with much less successful lisdexamphetamine (assuming no advantage over modified-release methylphenidate) produced a spending projection of €249 million or £67 million in 2012, roughly corresponding to the lower bound of the base case (Figure 4). An extremely low case was calculated resting on very conservative assumptions (cf. Tables 4 and 5) regarding diagnosis and treatment prevalence rates, absence of any further increase in treatment intensity, a disappointing clinical profile and subsequent low adoption rate of lisdexamphetamine, and denial of market access for modafinil and armodafinil. This led to an estimated spending of €170 m or £49 million in 2012, still an increase over 2002 by a factor >6 for both Germany and England (Figure 4).

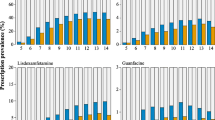

Range of plausible projections: expenditures under extreme case scenarios, 2001–2012. a, b: "High Extreme" Case; c, d: Base Case modified "LisDEX without clinical advantage over MPH-MR"; e, f: "Low Extreme" Case; left: England; right: Germany. MPH: methylphenidate; IR: immediate-release formulations (RitalinR, branded generics [EquasymR, MedikinetR], generics; FocalinR); MR: modified-release formulations (ConcertaR XL, EquasymR XL, MedikinetR retard, FocalinR XR; MPH-Patch: transdermal system (DaytranaR); LisDEX: lisdexamphetamine (NRP104); Nonstimulants: ATX, atomoxetine (StratteraR), ARM, armodafinil (SparlonR); DEX: dexamphetamine (England only).

3. Impact on individual physicians

These projections have been related to individual German physicians involved in care for children and adolescents with ADHD. Since ADHD care is a highly concentrated phenomenon (cf. Table 2), average spending (again, from the perspective of the GKV) for ADHD pharmacotherapy was calculated for the top-50% of child and adolescent psychiatrists, and the top-20% of pediatricians (see Figure 5).

Projected impact of ADHD treatment for children and adolescents on individual physicians' prescription drug expenditures, 2001–2012 (base case). a: Child and adolescent psychiatrists; b: pediatricians in private practice in Germany. Expenditures expressed as €/physician and year; perspective of statutory health insurance (i.e., excluding privately health insured patients). Data represent average values for one of the upper 50% of child and adolescent psychiatrists and one of the upper 20% of pediatricians in terms of relative involvement in care for ADHD patients, respectively. Concentration of care modeled according to Nordbaden data [74]. Abbreviation: Non-ADHD-Rx: expenditures for treatment of conditions other than ADHD.

Under base case assumptions, total annual drug spending of these child and adolescent psychiatrists would grow from an average total of less than €30,000 per physician in 2002 to €282,000 in 2012, of which €264,000 would be caused by prescriptions for ADHD treatment in children and adolescents (Figure 5). (Of course, as adult patients with ADHD have not been included in this analysis, the total budgetary impact of ADHD may be greater for those specialists who also treat adults, for example parents of patients.) This almost tenfold increase is the result of (a) the projected ADHD spending in combination with (b) the high concentration of patients among a small total number of specialists and (c) the very small number of prescriptions traditionally written by this specialist group. Even for the extremely low case looked at, this overall increase of drug spending by individual physicians would result in >5-fold drug spending caused by these specialists in 2012, compared to 2002. In this most conservative scenario, €144,500 or 89% of projected expenditures of €162,600 per physician in 2012 would still be accounted for by young ADHD patients.

Pediatricians as a group cause higher drug expenditures, and each of them treats a smaller number of ADHD patients compared to specialists, even those who are among the top-20% service providers for children with ADHD among their group. Hence, the incremental impact of ADHD-related spending is smaller compared to child and adolescent psychiatrists (Figure 4). Still, under base case conditions, ADHD-related pharmaceutical expenditures would account for 39% (or €75,000 out of €193,000 per physician in 2012, assuming a 5% growth rate of non-ADHD pharmaceutical spending) of total drug costs induced by this group. These figures compare with average drug costs of €83,000 per pediatrician in 2002. Thus, ADHD-related prescriptions alone would account for two thirds of the growth in drug expenditures caused by these physicians between 2002 and 2012.

Discussion and limitations

Without exception, all plausible scenarios for England and Germany point to a further increase of expenditures for ADHD medication. The striking extent of the projected increase may appear counterintuitive, but it is easily explained by the simultaneous and multiplicative effects exerted by four variables, i.e., increases in diagnosis prevalence, treatment prevalence, treatment intensity, and the shift to more expensive new products. Over a wide range of assumptions, all projections concur indicating a strong impact of this increase on the individual drug budgets of physicians treating patients with ADHD.

Some important limitations of the present analysis warrant discussion. First, the present analysis does not purport to convey value judgments. It has little to nothing to say about the clinical appropriateness of the prescriptions analyzed; its mere focus is on their budgetary impact.

Second, there is substantial uncertainty around future events. Compounds in development may be discontinued, marketed drugs may be withdrawn because of serious adverse events, safety concerns may slow down diffusion of new products, and so on. The dynamic health policy environment is yet another factor. However, it would hardly be a prudent response to uncertainty to abandon planning and taking a proactive role in the pursuit of efficient service provision.

In strategic management, scenario analysis is a well-established tool to deal with environmental uncertainty [65]. The practice of scenario planning implicitly acknowledges that "best guesses" of future events may be wrong. Therefore, any scenario should not be confused with a forecast of the future. Multiple scenarios are pen-pictures of a range of plausible futures (Figures 3 and 4). Though each individual scenario has an infinitesimal probability of actual occurrence, combined a range of scenarios can shed light on possible future outcomes. This in turn should enable to plan for the range of futures that could, plausibly, unfold.

A third important limitation of this study concerns its restricted scope. Although pharmaceutical spending is likely to rise faster than other ADHD-related expenditures, it is certainly not the only cost component to be considered in a complete budgetary impact analysis [30, 66]. Even more importantly, cost analyses illuminate just one half of the health economic equation; they do not provide information on "value for money", frequently analyzed in terms of cost-effectiveness [67]. Cost-effectiveness analyses of ADHD treatment strategies, however, have been rare [68], are only now beginning to appear [69–71], and have generally been limited to a one-year time horizon [72].

Implications

In combination, the scenarios developed here strongly suggest that the trend of rising drug expenditures for ADHD may not abate in the near future (Figure 3).

They further indicate that physicians involved in providing care for children and adolescents with ADHD should anticipate escalating expenditures and challenging questions from payers (Figure 5). In particular for German child and adolescent psychiatrists, as well as for pediatricians in private practice, there will be a growing need to demonstrate appropriate prescribing practices and the achievement of clinical benefits commensurate with levels of spending.

Likewise, pharmaceutical manufacturers developing and selling products for the treatment of patients with ADHD will need to produce timely evidence supporting the economic value of their products.

Finally, it should be noted that the present study was limited to ADHD in children and adolescents age 6 to 18 years. There is reason to assume that adult ADHD may be associated with substantial spending dynamics, which has only just begun to show [73]. This fact, however, lends further support to the key conclusion of the present study, namely, that there will be a rapidly growing need for health economic evidence on the value of clinical interventions for ADHD.

Abbreviations

- ARM:

-

armodafinil

- ATX:

-

atomoxetine

- DEX:

-

dexamphetamine

- dMPH:

-

dexmethylphenidate

- FDA:

-

Food and Drug Administration, the United States regulatory agency deciding on marketing authorizations for pharmaceutical products

- GKV:

-

Gesetzliche Krankenversicherung, statutory health insurance in Germany, covering approximately 90% of the population

- IR:

-

immediate release (formulation)

- LisDEX:

-

lisdexamphetamine, a prodrug of amphetamine in phase III clinical development

- MAS:

-

mixed amphetamine salts

- MOD:

-

modafinil

- MPH:

-

methylphenidate

- MR:

-

modified release (formulation)

- MR08:

-

modified release formulation with duration of action of approximately 8 hours

- MR12:

-

modified release formulation with duration of action of approximately 12 hours

- NHS:

-

National Health Service (England)

- SHI:

-

statutory health insurance in Germany (see GKV)

- TDS:

-

transdermal system

References

Kelleher KJ, McInerny TK, Gardner WP, Childs GE, Wasserman RC: Increasing identification of psychosocial problems: 1979–1996. Pediatrics. 2000, 105 (6): 1313-1321. 10.1542/peds.105.6.1313.

Robison LM, Sclar DA, Skaer TL, Galin RS: National trends in the prevalence of attention-deficit/hyperactivity disorder and the prescribing of methylphenidate among school-age children: 1990–1995. Clinical Pediatrics. 1999, 38 (4): 209-217. 10.1177/000992289903800402.

Zito JM, Safer DJ, dosReis S, Magder LS, Gardner JF, Zarin DA: Psychotherapeutic medication patterns for youths with attention-deficit hyperactivity disorder. Archives of Pediatrics & Adolescent Medicine. 1999, 153: 1257-1263.

Safer DJ, Malever M: Stimulant treatment in Maryland public schools. Pediatrics. 2000, 106: 533-539. 10.1542/peds.106.3.533.

Habel LA, Schaefer CA, Levine P, Bhat AK, Elliott G: Treatment with stimulants among youths in a large California health plan. Journal of Child and Adolescent Psychopharmacology. 2005, 15 (1): 62-67. 10.1089/cap.2005.15.62.

Safer DJ, Zito JM, Fine EM: Increased methylphenidate usage for attention-deficit disorder in the 1990s. Pediatrics. 1996, 98 (6): 1084-1088.

Shatin D, Drinkard CR: Ambulatory use of psychotropics by employer-insured children and adolescents in a national managed care organization. Ambulatory Pediatrics. 2002, 2 (2): 111-119. 10.1367/1539-4409(2002)002<0111:AUOPBE>2.0.CO;2.

Lin SJ, Crawford SY, Lurvey PL: Trend and area variation in amphetamine prescription usage among children and adolescents in Michigan. Social Science & Medicine. 2005, 60 (3): 617-626. 10.1016/j.socscimed.2004.06.002.

Thomas CP, Conrad P, Casler R, Goodman E: Trends in the use of psychotropic medications among adolescents, 1994–2001. Psychiatric Services. 2006, 57 (1): 63-69. 10.1176/appi.ps.57.1.63.

Guevara J, Lozano P, Wickizer T, Mell L, Gephart H: Psychotropic medication use in a population of children who have attention-deficit hyperactivity disorder. Pediatrics. 2002, 109 (5): 733-739. 10.1542/peds.109.5.733.

Cox ER, Motheral BR, Henderson RR, Mager D: Geographic variation in the prevalence of stimulant medication use among children 5 to 14 years old: results from a commercially insured US sample. Pediatrics. 2003, 111: 237-243. 10.1542/peds.111.2.237.

Rowland AS, Umbach DM, Stallone L, Naftel AJ, Bohlig EM, Sandler DP: Prevalence of medication treatment for attention deficit-hyperactivity disorder among elementary school children in Johnston County, North Carolina. American Journal of Public Health. 2002, 92 (2): 231-234.

Zuvekas SH, Vitiello B, Norquist G: Recent trends in stmulant medication among U.S. children. American Journal of Psychiatry. 2006, 163 (4): 579-585. 10.1176/appi.ajp.163.4.579.

Medco Health Solutions: Research reveals adult diagnosis of ADHD growing faster than children diagnosis. Press Release. September 15, 2005. http://www.epilepsy.com/ last accessed June 30, 2006.

Wong ICK, Murray ML, Camilleri-Novak D, Stephens P: Increased prescribing trends of paediatric psychotropic medications. Archives of Disease in Childhood. 2004, 89: 1131-1132. 10.1136/adc.2004.050468.

Miller AR, Lalonde CE, McGrail KM, Armstrong RW: Prescription of methylphenidate to children and youth, 1990–1996. Canadian Medical Association Journal (CMAJ). 2001, 165 (11): 1489-1494.

Criado Álvarez JJ, Romo Barrientos C: Variabilidad y tendencias en el consumo de metilfenidato en España. Estimación de la prevalencia del trastorno por déficit de atención con hiperactividad. Revista de Neurología. 2003, 37 (9): 806-810.

Donker GA, Groenhof F, van der Veen VJ: Toenemend aantal voorschriften voor methylfenidaat in huisartspraktijen in Noordoost-Nederland, 1998–2003. Nederlands Tijdschrift voor Geneeskunde. 2005, 30 (31): 1742-1747.

Department of Health: Prescription Cost Analysis England. 2005, London: National Health Service (NHS), Health and Social Care Information Centre, Health Care Statistics. Also previous issues, years 2006;p 1999–2005

Schwabe U, Paffrath D: Arzneiverordnungs-Report 2006. 2007, Berlin, Heidelberg, New York: Springer, also previous issues, years 1993–2006

DeGrandpre R: Ritalin Nation: Rapid-Fire-Culture and the Transformation of Human Consciousness. 2000, New York, NY: Norton

Perring C: Medicating children: the case of Ritalin. Bioethics. 1997, 11 (3–4): 228-240. 10.1111/1467-8519.00061.

Kociancic T, Reed MD, Findling RL: Evaluation of risks associated with short- and long-term psychostimulant therapy for treatment of ADHD in children. Expert Opinion on Drug Safety. 2004, 3 (2): 93-100. 10.1517/14740338.3.2.93.

Ekman JT, Gustafsson PA: Stimulants in AD/HD, a controversial treatment only in Sweden?. European Child & Adolescent. 2000, 9: 312-313. 10.1007/s007870070036.

Foreman DM, Foreman D, Prendergast M, Minty : Is clinic prevalence of ICD-10 hyperkinesis underestimated? Impact of increasing awareness by a questionnaire screen in a UK clinic. European Child & Adolescent Psychiatry. 2001, 10 (2): 130-134. 10.1007/s007870170036.

Schlander M, Schwarz O, Viapiano M, Bonauer N: Methylphenidate prescriptions for children and adolescents with attention-deficit/hyperactivity disorder (ADHD): new data from Nordbaden/Germany. Value in Health. 2006, 9 (6): A191-192.

Llana ME, Crismon ML: Methylphenidate: increased abuse or appropriate use?. Journal of the American Pharmaceutical Association. 1999, 39 (4): 526-530.

Wilens T: Subtypes of ADHD at risk for substance abuse. Presentation at the 157th Annual Meeting of the American Psychiatric Association; New York, NY: May 1–6, 2004

Graff Low K, Gendaszek AE: Illicit use of psychostimulants among college students: a preliminary study. Psychology, Health & Medicine. 2002, 7: 283-287. 10.1080/13548500220139386.

Trueman P, Drummond M, Hutton J: Developing guidance for budget impact analysis. Pharmacoeconomics. 2001, 19 (6): 609-621. 10.2165/00019053-200119060-00001.

Donohue JM, Berndt ER: Direct-to-consumer advertising and medication choice. Journal of Public Policy & Marketing. 2004, 23 (2): Fall 2004

Mizik N, Jacobson R: Are physicians "easy marks"? Quantifying the effects of detailing and sampling on new prescriptions. Management Science. 2004, 50 (12): 1704-1715. 10.1287/mnsc.1040.0281.

Abikoff HG, Hechtman L, Klein RG, Weiss G, Fleiss K, Etcovitch J, Cousins L, Greenfield B, Martin D, Pollack S: Symptomatic improvement in children with ADHD treated with long-term methylphenidate and multimodal psychosocial treatment. Journal of the American Academy of Child and Adolescent Psychiatry. 2004, 43 (7): 802-811. 10.1097/01.chi.0000128791.10014.ac.

Klein RG, Abikoff HG, Hechtman L, Weiss G: Design and rationale of controlled study of long-term methylphenidate and multimodal psychosocial treatment in children with ADHD. Journal of the American. 2004, 43 (7): 792-801.

MTA Cooperative Group: A 14-month randomized clinical trial of treatment strategies for attention-deficit/hyperactivity disorder. Archives of General Psychiatry. 1999, 56: 1073-1086. 10.1001/archpsyc.56.12.1073.

MTA Cooperative Group: Moderators and mediators of treatment response for children with attention-deficit/hyperactivity disorder: the multimodal treatment study of children with attention-deficit/hyperactivity disorder. Archives of General Psychiatry. 1999, 56: 1088-1096. 10.1001/archpsyc.56.12.1088.

MTA Cooperative Group: National Institute of Mental Health Multimodal Treatment Study of ADHD follow-up: 24-month outcomes of treatment strategies for attention-deficit/hyperactivity disorder. Pediatrics. 2004, 113 (4): 754-761. 10.1542/peds.113.4.754.

Swanson JM, Kraemer HC, Hinshaw SP, Arnold LE, Conners CK, Abikoff HB, Clevenger W, Davies M, Elliott GR, Greenhill LL, Hechtman L, Hoza B, Jensen PS, March JS, Newcorn JH, Owens EB, Pelham WE, Schiller E, Severe JB, Simpson S, Vitiello B, Wells K, Wigal T, Wu M: Clinical relevance of the primary findings of the MTA: success rates based on severity of ADHD and ODD symptoms at the end of treatment. Journal of the American Academy of Child & Adolescent. 2001, 40 (2): 168-179. 10.1097/00004583-200102000-00011.

Medco Health Solutions: Medco study reveals pediatric spending spike on drugs to treat behavioral problems. Solutions Today. May 18, 2004. http://www.drugtrend.com; last accessed June 15, 2005

Scrip: Senator calls for a "comprehensive review" of ADHD drug risks. Scrip World Pharmaceutical News. 2006, 3131 (February 8, 2006): 14.

Scrip: Cephalon's modafinil formulation for ADHD "approvable" in the US. Scrip World Pharmaceutical News. 2005, 3101 (October 25, 2005): 27.

Schlander M: Budgetary Impact of Treatments for Attention-Deficit/Hyperactivity Disorder (ADHD) in Germany: Increasing Relevance of Health Economic Evidence. 2004, 16th World Congress of the International Association for Child and Adolescent Psychiatry and Allied Professions (IACAPAP), Berlin, August 22–26, 2004. Book of Abstracts, Steinkopff-Verlag, Darmstadt, S-111–516, 187

Schlander M: Vor der Ökonomisierung der ADHS-Therapie? Gesundheitsökonomische Aspekte. Doch unzerstörbar ist mein Wesen... Diagnose AD(H)S – Schicksal oder Chance?. Edited by: Fitzner T, Stark W. 2004, Weinheim: Beltz, 417-466.

Glaeske G, Janhsen K: GEK-Arzneimittel-Report 2006. 2006, Bremen, Schwaebisch-Gmuend, Schriftenreihe zur Gesundheitsanalyse, 44.

Hack S, Chow B: Pediatric psychotropic medication compliance: a literature review and research-based suggestions for improving treatment compliance. Journal of Child and Adolescent Psychopharmacology. 2001, 11 (19): 59-67. 10.1089/104454601750143465.

Swanson J: Compliance with stimulants for attention-deficit/hyperactivity disorder. Issues and approaches for improvement. CNS Drugs. 2003, 17 (2): 117-131. 10.2165/00023210-200317020-00004.

Schlander M: Arzneimittelversorgung und Kostendaempfungspolitik: Perspektiven ein Jahr nach dem GMG. Medizinische Klinik. 2005, 100 (6): 314-324. 10.1007/s00063-005-1040-2.

Makridakis S, Wheelwright SC, Hyndman RJ: Forecasting – Methods and Applications. 1998, New York, NY: Wiley, 3

InnoVal-HC: New products in development for treatment of ADHD: Literature review, Scrip and Pharmalive database analysis and interpretation. 2006, Aschaffenburg, Germany: Institute for Innovation & Valuation in Health Care, data on file

Anderson VR, Scott LJ: Methylphenidate transdermal system in attention-deficit hyperactivity disorder in children. Drugs. 2006, 66 (8): 1117-1126. 10.2165/00003495-200666080-00007.

McGough JJ, Wigal SB, Abikoff H, Turnbow JM, Posner K, Moon E: A randomized, double-blind, placebo-controlled, laboratory classroom assessment of methylphenidate transdermal system in children with ADHD. Journal of Attention Disorders. 2006, 9 (3): 476-485. 10.1177/1087054705284089.

McGough JJ, Pataki CS, Suddath R: Dexmethylphenidate extended-release capsules for attention-deficit/hyperactivity disorder. Expert Review of Neurotherapeutics. 2005, 5 (4): 437-441. 10.1586/14737175.5.4.437.

Wigal S, Swanson JM, Feifel D, Sangal RB, Elia J, Casat CD, Zeldis JB, Conners CK: A double-blind, placebo-controlled trial of dexmethylphenidate hydrochloride and d,l-threo-methylphenidate hydrochloride in children with attention-deficit/hyperactivity disorder. Journal of the American Academy of Child & Adolescent Psychiatry. 2004, 43 (11): 1406-1414. 10.1097/01.chi.0000138351.98604.92.

Rosack J: Regulatory and Legal Briefs. Psychiatry News. 2006, 41 (2): 30.

Ballon JS, Feifel D: A systematic review of modafinil: potential clinical uses and mechanisms of action. Journal of Clinical Psychiatry. 2006, 67 (4): 554-566.

Turner D: A review of the use of modafinil for attention-deficit hyperactivity disorder. Expert Review of Neurotherapeutics. 2006, 6 (4): 455-468. 10.1586/14737175.6.4.455.

Waxmonsky JG: Nonstimulant therapies for attention-deficit hyperactivity disorder (ADHD) in children and adults. Essential Psychopharmacology. 2005, 6 (5): 262-276.

Steinhoff K: Attention-deficit/hyperactivity disorder: medication treatment-dosing and duration of action. American Journal of Managed. 2004, 10 (4): S99-S106.

Biederman J, Swanson JM, Wigal SB, Kratochvil CJ, Boellner SW, Earl CQ, Jiang J, Greenhill L: Efficacy and safety of modafinil film-coated tablets in children and adolescents with attention-deficit/hyperactivity disorder: results of a randomized, double-blind, placebo-controlled, flexible-dose study. Pediatrics. 2005, 116 (6): e777-e784. 10.1542/peds.2005-0617.

Swanson JM, Greenhill LL, Lopez FA, Sedillo A, Earl CQ, Jiang JG, Biederman J: Modafinil film-coated tablets in children and adolescents with attention-deficit/hyperactivity disorder: results of a randomized, double-blind, placebo-controlled, fixed-dose study followed by abrupt discontinuation. Journal of Clinical Psychiatry. 2006, 67 (1): 137-147.

Scrip: Cephalon drops Sparlon for attention deficit hyperactivity disorder after FDA rejection. Scrip World Pharmaceutical News. 2006, 3183 (August 10, 2006): 21.

Remschmidt H, by the Global ADHD Working Group: Global consensus on ADHD/HKD. European Child & Adolescent Psychiatry. 2005, 14 (3): 127-137. 10.1007/s00787-005-0439-x.

Schlander M: Long-Acting Medications for the Hyperkinetic Disorders: A Note on Cost-Effectiveness. European Child & Adolescent Psychiatry. 2007, March 30, 2007.

Kola I, Landis J: Can the pharmaceutical industry reduce attrition rates?. Nature Reviews Drug Discovery. 2004, 3 (8): 711-715. 10.1038/nrd1470.

Goodwin P, Wright G: Decision Analysis for Management Judgment. 2004, Chichester, England: John Wiley & Sons, 3

Matza LS, Paramore C, Prasad M: A review of the economic burden of ADHD. Cost effectiveness and Resource Allocation. 2005, 3: 5-10.1186/1478-7547-3-5.

Drummond MF, Sculpher MJ, Torrance GW, O'Brien BJ, Stoddart GL: Methods for the economic evaluation of health care programmes. 2005, Oxford: Oxford University Press, 3

Romeo R, Byford S, Knapp M: Annotation: economic evaluations of child and adolescent mental health interventions: a systematic review. Journal of Child Psychology and Psychiatry. 2005, 46 (9): 919-930. 10.1111/j.1469-7610.2005.00407.x.

Jensen PS, Garcia JA, Glied S, Crowe M, Foster M, Schlander M, Hinshaw S, Vitiello B, Arnold LE, Elliott G, Hechtman L, Newcorn JH, Pelham WE, Swanson J, Wells K: Cost-effectiveness of ADHD treatments: findings from the multimodal treatment study of children with ADHD. American. 2005, 162 (9): 1628-1636.

Schlander M: Cost-effectiveness of treatment options for attention-deficit/hyperactivity disorder (ADHD) in children and adolescents: what have we learnt?. 17th World Congress of the International Association for Child and Adolescent Psychiatry and Allied Professions (IACAPAP), Melbourne, September 10–14, 2006. Book of Abstracts, 43 (Abstract No. 2040), [http://www.michaelschlander.com]

Schlander M, Schwarz O, Hakkaart-van Roijen L, Jensen PS, Persson U, Santosh P, Trott GE, the MTA Cooperative Group: Cost-Effectiveness of Clinically Proven Treatment Strategies for Attention-Deficit/Hyperactivity Disorder (ADHD) in the United States, Germany, The Netherlands, Sweden, and United Kingdom. Value in Health. 2006, 9 (6): A312.

Schlander M: Cost-effectiveness of ADHD treatment strategies: what we do know ... and what we do not know ... 13th International Congress of the European Society for Child and Adolescent Psychiatry (ESCAP), Florence, August 26, 2007, [http://www.michaelschlander.com]

Schlander M, Schwarz O, Viapiano M, Bonauer N: Off-label utilization of methylphenidate for adults with attention-deficit/hyperactivity disorder: insights from the Nordbaden project. Value in Health. 2006, 9 (6): A311.

Schlander M, Schwarz O, Trott GE, Viapiano M, Bonauer N: Who cares for patients with attention-deficit/hyperactivity disorder (ADHD)? Insights from Nordbaden (Germany). European Child and Adolescent Psychiatry. 2007, April 28, 2007.

Joint Formulary Committee: British National Formulary (BNF). 2006, London: British Medical Association/Royal Pharmaceutical Society of Great Britain, March 2006, 51

Gelbe Liste Pharmindex. Last accessed July 1, 2006, [http://www.gelbe-liste.de]

Office for National Statistics (ONS), London, England. [http://www.statistics.gov.uk]

Statistisches Bundesamt, Wiesbaden, Germany. [http://www.destatis.de]

American Psychiatric Association: Diagnostic and statistical manual of mental disorders (DSM-IV). 1994, American Psychiatric Association, Washington, DC, 4

World Health Organization: International statistical classification of diseases and related health problems (ICD-10). 1992, Geneva, Switzerland: The World Health Organization, 10

Taylor E, Doepfner M, Sergeant J, Asherson P, Banaschewski T, Buitelaar J, Coghill D, Danckaerts M, Rothenberger A, Sonuga-Barke E, Steinhausen H-C, Zuddas A: European guidelines for hyperkinetic disorder – first upgrade. European Child & Adolescent Psychiatry. 2004, 13 (Suppl 1): 7-30.

Faraone SV, Sergeant J, Gillberg C, Biederman J: The worldwide prevalence of ADHD: is it an American condition?. World Psychiatry. 2003, 2 (2): 104-113.

Green M, Wong M, Atkins D: Diagnosis and treatment of attention-deficit/hyperactivity disorder in children and adolescents. 1999, Technical Review No 3. Rockville, MD: Agency for Health Care Policy and Research, AHCPR Publication No 99-0050

Bruehl B, Doepfner M, Lehmkuhl G: Der Fremdbeurteilungsbogen fuer hyperkinetische Stoerungen (FBB-HKS) – Praevalenz hyperkinetischer Stoerungen im Elternurteil und psychometrische Kriterien. Kindheit und Entwicklung. 2000, 9: 115-125.

Ford T, Goodman R, Melltzer H: The British Child and Adolescent Mental Health Survey 1999: the prevalence of DSM-IV disorders. Journal of the American Academy of Child and Adolescent. 2003, 42 (10): 1203-1211. 10.1097/00004583-200310000-00011.

Koester I, Schubert I, Doepfner M, Adam C, Ihle P, Lehmkuhl G: Hyperkinetische Stoerungen bei Kindern und Jugendlichen: Zur Haeufigkeit des Behandlungsanlasses in der ambulanten Versorgung nach den Daten der Versichertenstichprobe AOK Hessen/KV Hessen. Zeitschrift fuer Kinder- und Jugendpsychiatrie und Psychotherapie. 2004, 32: 157-166. 10.1024/1422-4917.32.3.157.

Ferber Lv, Lehmkuhl G, Koester I, Doepfner M, Schubert I, Froelich J, Ihle P: Methylphenidatgebrauch in Deutschland: Versichertenbezogene epidemiologische Studie ueber die Entwicklung von 1998 bis 2000. Deutsches Aerzteblatt. 2003, 100: A41-A46.

Schubert I, Koester I, Adam C, Ihle P, Ferber Lv, Lehmkuhl G: Hyperkinetische Stoerung als Krankenscheindiagnose bei Kindern und Jugendlichen – eine versorgungsepidemiologische Studie auf der Basis der Versichertenstichprobe KV Hessen/AOK Hessen. Abschlussbericht an das Bundesministerium fuer Gesundheit und soziale Sicherung. 2002, University of Cologne, Cologne, Germany

Schlander M, Schwarz O, Viapiano M, Bonauer N: Methylphenidate prescriptions for children and adolescents with attention-deficit/hyperactivity disorder (ADHD): new data from Nordbaden, Germany. Value in Health. 2006, 9 (6): A191-A192.

Schubert I, Selke GW, Osswald-Huang P-H, Schroeder H, Nink K: Methylphenidat-Verordnungsanalyse auf der Basis von GKV-Daten. 2002, Wissenschaftliches Institut der AOK (WidO), Bonn, Germany

Michelson D, Faries D, Wernicke J, Kelsey D, Kendrick K, Sally RS, Spencer T, the Atomoxetine ADHD Study Group: Atomoxetine in the treatment of children and adolescents with attention-deficit/hyperactivity disorder: a randomized, placebo-controlled, dose-response study. Pediatrics. 2001, 108 (5): 1-9. 10.1542/peds.108.5.e83.

Spencer T, Heiligenstein JH, Biederman J, Faries D, Kratochvil CJ, Conners CK, Potter WZ: Results from 2 proof-of-concept, placebo-controlled studies of atomoxetine in children with attention-deficit/hyperactivity disorder. Journal of Clinical Psychiatry. 2002, 63 (12): 1140-1147.

Marcus SC, Wan GJ, Kemner JE, Olfson M: Continuity of methylphenidate treatment for attention-deficit/hyperactivity disorder. Archives of Pediatrics & Adolescent Medicine. 2005, 159: 572-578. 10.1001/archpedi.159.6.572.

Sanchez RJ, Crismon ML, Barner JC, Bettinger T, Wilson J: Assessment of adherence measures with different stimulants among children and adolescents. Pharmacotherapy. 2000, 25 (7): 909-917. 10.1592/phco.2005.25.7.909.

Kanavos P: Policy approaches to pharmaceutical pricing and reimbursement in European countries. 2006, London: London School of Economics, unpublished manuscript

Kassenaerztliche Vereinigung Baden-Wuerttemberg: Verordnungsdaten 2004. 2006, Personal communication

InnoVal-HC Website. [http://www.innoval-hc.com/]

Author information

Authors and Affiliations

Corresponding author

Authors’ original submitted files for images

Below are the links to the authors’ original submitted files for images.

Rights and permissions

This article is published under license to BioMed Central Ltd. This is an Open Access article distributed under the terms of the Creative Commons Attribution License (http://creativecommons.org/licenses/by/2.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

About this article

Cite this article

Schlander, M. Impact of Attention-Deficit/Hyperactivity Disorder (ADHD) on prescription dug spending for children and adolescents: increasing relevance of health economic evidence. Child Adolesc Psychiatry Ment Health 1, 13 (2007). https://doi.org/10.1186/1753-2000-1-13

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/1753-2000-1-13