Abstract

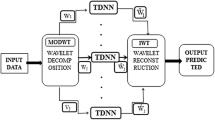

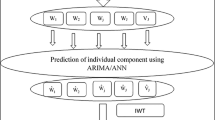

It has been observed that most of the agricultural time series data in general and price data in particular are non-linear, non-stationary, non-normal and heteroscedastic in nature. Therefore, application of usual linear and nonlinear parametric models like Autoregressive integrated moving average (ARIMA), Generalized autoregressive conditional heteroscedastic (GARCH) and their component models fail to capture the variability present in the series. It is also very difficult to extract actual signal from noisy time series observations. In this regard, nonparametric wavelet technique has the advantage of pre-processing the series to extract the actual signal. Optimizing level of decomposition and choosing appropriate wavelet filter can represent the series with high chaotic nature and sophisticated nonlinear structure more effectively. The decomposition can describe the useful pattern of the series from both global as well as local perspective. The wavelet decomposed components can be modeled using Machine Learning techniques like Artificial Neural Network (ANN) to result in wavelet-based hybrid models and eventually, inverse wavelet transform can be carried out to obtain the prediction of original series. The above algorithm has been applied for modeling monthly modal wholesale price of tomato for Burdwan market, West Bengal, India. Haar and D4 wavelet filters have been applied using two levels of decomposition i.e. 3 and 6. The prediction accuracy of the hybrid model is compared empirically with that of ARIMA, GARCH and ANN model and it is observed that hybrid algorithm outperformed the other models.

Similar content being viewed by others

References

Ahmed NK, Atiya AF, El Gayar N, El Shishiny H (2010) An empirical comparison of machine learning models for time series forecasting. Econ Rev 29(5–6):594

Anderson JA (1995) An introduction to neural networks. MIT Press, Cambridge

Anjoy P, Paul RK (2017) Comparative performance of wavelet-based neural network approaches. Neurl Comput Appl 31:3443–3453

Antoniadis A (1997) Wavelets in statistics: a review. J Ital Stat Soc 6:97–144

Bollerslev T (1986) Generalized autoregressive conditional heteroscedasticity. J Econom 31:307–327

Daubechies I (1992) Ten lectures on wavelets. SIAM, Philadelphia

Engle RF (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of U.K. inflation. Econometrica 50:987–1008

Freeman J, Skapura D (1991) Neural networks: algorithms, applications, and programmingtechniques. Addison-Wesley, Reading

Gao R, Du L, Duru O, Yuen KF (2021) Time series forecasting based on echo state network and empirical wavelet transformation. App Soft Comput 102:107–111

Hagan MT, Demuth HB, Beale M (1996) Neural network design. WS/KENT Publishing Co, Boston

Hylleberg S, Engle RF, Granger CWJ, Yoo BS (1990) Seasonal integration and cointegration. J Econ 44:215–238

Karsoliya S (2012) Approximating number of hidden layer neurons in multiple hidden layer BPNN architecture. Int J of Eng Tren and Tech 31(6):714–717

Lee HW, Beh WL, Lem KH (2020) Wavelet as a viable alternative for time series forecasting. Aust J Stat 49:38–47

Li X, Tang P (2020) Stock index prediction based on wavelet transform and FCD-MLGRU. J Fore 39(8):1229–1237

Liu H, Shi J (2013) Applying ARMA-GARCH approaches to forecasting short-term electricity prices. Energy Econ 37:152–166

Liu H, Shi J, Qu X (2013) Empirical investigation on using wind speed volatility to estimate the operation probability and power output of wind turbines. Energy Convers Manag 67:8–17

Merdun H, Çinar Ö (2010) Artificial neural network and regression techniques in modelling surface water quality. Environ Prot Eng 36(2):95–109

Paul RK (2015) ARIMAX-GARCH-WAVELET model for forecasting volatile data. Model Assist Stat Appl 10(3):243–252

Paul RK, Garai S (2021) Performance comparison of wavelet-based machine learning technique for forecasting agricultural commodity prices. Soft Comput 25:12857–12873

Paul RK, Prajneshu GH (2009) GARCH nonlinear time series analysis for modeling and forecasting of India’s volatile spices export data. J Indian Soc Agric Stat 63(2):123–131

Paul RK, Prajneshu GH (2013) Wavelet frequency domain approach for modelling and forecasting of Indian monsoon rainfall time-series data. J Indian Soc Agric Stat 67(3):319–327

Paul RK, Rana S, Saxena R (2016) Effectiveness of price forecasting techniques for capturing asymmetric volatility for onion in selected markets of Delhi. Indian J Agric Sci 86(3):303–309

Paul RK, Paul AK, Bhar LM (2020) Wavelet-based combination approach for modeling sub-divisional rainfall in India. Theor Appl Climatol 139(3–4):949–963

Percival DB, Walden AT (2000) Wavelet methods for time series analysis. Cambridge University Press, Cambridge

Verikas A, Bacauskiene M (2003) Using artificial neural networks for process and systemmodeling. Chemo Intel Lab 67:187–191

Vidakovic B (1999) Statistical modeling by wavelets. John Wiley, New York

Wang W, Van Gelder PHAJM, Vrijing JK, Ma J (2005) Testing and modeling autoregressive conditional heteroskedasticity of streamflow processes. Nonlinear Process Geophys 12:55–66

Werbos PJ (1988) Generalization of backpropagation with application to a recurrent gas market model. Neural Netw 1(4):339–356

Acknowledgements

The authors are grateful to the anonymous reviewer for the extensive comments that helped in improving the quality of this manuscript.

Funding

This research received no external funding.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that there are no conflicts of interest in publishing this manuscript.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Paul, R.K., Garai, S. Wavelets Based Artificial Neural Network Technique for Forecasting Agricultural Prices. J Indian Soc Probab Stat 23, 47–61 (2022). https://doi.org/10.1007/s41096-022-00128-3

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41096-022-00128-3