Abstract

Multiple price lists have emerged as a simple and popular method for eliciting risk preferences. Despite their popularity, a key downside of multiple price lists has not been widely recognized — namely that the approach is unlikely to generate sufficient information to accurately identify different dimensions of risk preferences. The most popular theories of decision making under risk posit that preferences for risk are driven by a combination of two factors: the curvature of the utility function and the extent to which probabilities are weighted non-linearly. In this paper, we show that the widely used multiple price list introduced by Holt and Laury (The American Economic Review 92(5) 1644–1655 2002) is likely more accurate at eliciting the shape of the probability weighting function, and we construct a different multiple price list that is likely more accurate at eliciting the shape of the utility function. We show that by combining information from different multiple price lists, greater predictive performance can be achieved.

Similar content being viewed by others

Notes

The word “multiple” in multiple price list is redundant since the word “list” already implies repetitive choices. Nevertheless, we adopt the phrasing MPL in this paper as it is more commonly used in the literature than other variants such as “choice list.”

If interest rests solely in creating a single index of risk preference without committing to a single theory, there are some relatively simple methods available such as the one shown in exercise 3.6.3 in Wakker (2010).

One can of course utilize several MPLs and scale up the payoffs as H&L did to allow for a wider range of monetary amounts (thus providing more information on the shape of the utility function). However, those researchers interested in adding a quick and simple risk preference elicitation device to their studies are unlikely to want to add numerous MPLs simply to get an informed shape of the utility function.

Rabin (2000) argues that, assuming Expected Utility Theory (EUT), anything but risk-neutrality over modest stakes implies absurd levels of risk aversion over larger stakes. Cox and Sadiraj (2006) show that the same implications do not follow for the EUT model of income but only for the terminal wealth model. Of course, there have been several quibbles about this issue (Palacios-Huerta and Serrano 2006; Rubinstein 2006; Watt 2002; Wakker 2010, pp. 242-245).

There are a few other papers that have constructed tasks that vary the payoff amounts and hold probabilities constant albeit their aim was different than this paper. For example Bruner (2009) asks whether equivalent changes in the expected value of a lottery, achieved by either changing the probability of a reward or by changing the reward itself, will be preferred by risk averse agents as predicted by EUT (he finds that they do). More recently, Bosch-Domènech and Silvestre (2013) compare a standard H&L task with a task they adopt from Abdellaoui et al. (2011) (which in turn is similar to the certainty equivalents method of Cohen et al. (1987)) for embedding bias. They find that the H&L task is susceptible to embedding bias while the Abdellaoui et al. (2011) task is not.

For example, if an individual (with EUT preferences) switched from choosing option A to option B on the sixth row of the original H&L task, it would imply a CRRA between 0.14 and 0.41. Likewise, in the payoff-varying MPL with constant probabilities, a switch from choosing option A to option B on the sixth row would also imply (assuming EUT preferences) a CRRA between 0.14 and 0.41.

There is one additional feature of the payoff-varying MPL shown in Table 2 that bears mention. Although it does not totally do away with the aforementioned confound between w(p) and U(x) when we assume rank-dependent preferences, the confound completely disappears if people weight probabilities as in original prospect theory. In this case, in the payoff-varying MPL people will choose option A when w(0.5)U(A H) + w(0.5)U(1.6) > w(0.5)U(B H) + w(0.5)U(1). One can divide both sides of this inequality by w(0.5) to see that option A will be chosen when U(A H) + U(1.6) > U(B H) + U(1), or rewriting: \(1<\frac {U(1.6)-U(1)}{U(B^{H} )-U(A^{H} )}\). This last inequality does not contain the term w(0.5), thus, the choice of option A over B cannot be explained by probability weighting. Stated differently, even if an individual weights probabilities non-linearly in the fashion given by original prospect theory, only the shape of U(x) will dictate their choices in the payoff-varying MPL shown in Table 2. This condition could only be obtained because of our choice of the probability value 0.5. For any other probability value the weighting function does not drop out and the confound remains. Thus, in the original H&L task (which uses probabilities from 0 to 1), the confound between w(p) and U(x) remains even if preferences are given by original prospect theory. Note that since most empirical estimates suggest that w(0.3)≈0.3, it is possible to also use this empirical relation to create a MPL that avoids probability weighting.

Subjects were told that “In addition to a fixed fee of €10, you will have a chance of receiving additional money up to €25. This will depend on the decisions you make during the experiment.”

16 out of 100 subjects failed to pass this test concerning comprehension of lotteries and were omitted from our sample.

In our experiment, we did not impose monotonicity on choices or provide warnings when monotonicity was violated. Although such a procedure could be implemented, it is unclear if it is superior to simply observing how people behave when unconstrained.

The log likelihood function is maximized using standard numerical methods. The statistical specification also takes into account the multiple responses given by the same subject and allows for correlation between responses by clustering standard errors, which were computed using the delta method. Therefore, standard errors allow for intrasubject correlation to account for the fact that subjects made repeated choices and observations are not independent at the subject level. The robust estimator of variance that relaxes the assumption of independent observations involves a slight modification of the robust (or sandwich) estimator of variance (StataCorp 2011, pp. 295).

In the original H&L task, we can also estimate a non-parametric utility function and instead estimate the two utility differences shown in Eq. 1: [U(1.6)−U(0.1)] and [U(3.85) − U(2)]. In this latter case, however, the standard deviation, σ, is no longer separately identified and must be normalized to one. In the H&L MPL, this formulation is actually observationally equivalent to the CRRA specification with σ freely estimated; both utility specifications give identical maximum likelihood function values and probability weighting estimates. These results are shown in the Electronic Supplementary Material Table B.2.

We also considered alternative estimations that take into account individual heterogeneity: i) we added a mean-zero random effect to the utility difference between option A and B and then estimated the variance of this random effect ii) we modeled the coefficient of risk aversion as a random coefficient and estimated the mean and variance (\({\sigma _{r}^{2}}\)) iii) we modeled the probability weighting parameter as a random coefficient and estimated the mean and variance. Models with random coefficients like ii) and iii) are often hard to converge but for models for which convergence was achieved, we found that estimates were very close to the estimates we report in the paper. We therefore conclude that heterogeneity is unlikely to affect any of our conclusions.

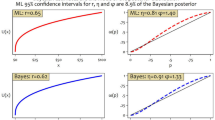

Our composite model takes the estimate of the curvature of the probability weighting from the H&L task and the estimate of the curvature of the utility function from the payoff-varying MPL. An alternative approach is to pool the two data sets and estimate a combined model. When we do this for the low payoff task, we find an estimate of r = 0.3249 and γ = 0.6904, and σ = 0.5883, all of which are significantly different from zero. However, this model exhibits significantly poorer out of sample predictions with the OSLLF =−0.5222 and percentage of correct predictions=76.42% than the composite model discussed in the main text. A similar result holds for the high payoff task.

References

Abdellaoui, M., Driouchi, A., & L’Haridon, O. (2011). Risk aversion elicitation: Reconciling tractability and bias minimization. Theory and Decision, 71(1), 63–80.

Andersen, S., Harrison, G.W., Lau, M.I., & Rutström, E.E. (2006). Elicitation using multiple price list formats. Experimental Economics, 9(4), 383–405.

Andersen, S., Harrison, G.W., Lau, M.I., & Rutström, E.E. (2008). Eliciting risk and time preferences. Econometrica, 76(3), 583–618.

Andersen, S., Harrison, G.W., Lau, M.I., & Rutström, E.E. (2014). Discounting behavior: a reconsideration. European Economic Review, 71, 15–33.

Becker, G.M., DeGroot, M.H., & Marschak, J. (1964). Measuring utility by a single-response sequential method. Behavioral Science, 9(3), 226–232.

Bellemare, C., & Shearer, B. (2010). Sorting, incentives and risk preferences: Evidence from a field experiment. Economics Letters, 108(3), 345–348.

Binswanger, H.P. (1980). Attitudes toward risk: Experimental measurement in rural India. American Journal of Agricultural Economics, 62(3), 395–407.

Binswanger, H.P. (1981). Attitudes toward risk: Theoretical implications of an experiment in rural India. Economic Journal, 91(364), 867–890.

Bleichrodt, H. (2002). A new explanation for the difference between time trade-off utilities and standard gamble utilities. Health Economics, 11(5), 447–456.

Bosch-Domènech, A., & Silvestre, J. (2013). Measuring risk aversion with lists: A new bias. Theory and Decision, 75(4), 465–496.

Bruner, D., McKee, M., & Santore, R. (2008). Hand in the cookie jar: an experimental investigation of equity-based compensation and managerial fraud. Southern Economic Journal, 75(1), 261– 278.

Bruner, D.M. (2009). Changing the probability versus changing the reward. Experimental Economics, 12(4), 367–385.

Camerer, C.F., & Ho, T.-H. (1994). Violations of the betweenness axiom and nonlinearity in probability. Journal of Risk and Uncertainty, 8(2), 167–196.

Cohen, M., Jaffray, J.-Y., & Said, T. (1987). Experimental comparison of individual behavior under risk and under uncertainty for gains and for losses. Organizational Behavior and Human Decision Processes, 39(1), 1–22.

Cox, J.C., & Sadiraj, V. (2006). Small- and large-stakes risk aversion: Implications of concavity calibration for decision theory. Games and Economic Behavior, 56(1), 45–60.

Csermely, T., & Rabas, A. (2016). How to reveal people’s preferences: Comparing time consistency and predictive power of multiple price list risk elicitation methods. Journal of Risk and Uncertainty. doi:10.1007/s11166-016-9247-6.

Drichoutis, A.C., & Lusk, J.L. (2014). Judging statistical models of individual decision making under risk using in- and out-of-sample criteria. PLoS ONE, 9(7), e102269.

Eckel, C.C., & Wilson, R.K. (2004). Is trust a risky decision? Journal of Economic Behavior & Organization, 55(4), 447–465.

Erdem, T. (1996). A dynamic analysis of market structure based on panel data. Marketing Science, 15(4), 359–378.

Fischbacher, U. (2007). z-tree: Zurich toolbox for ready-made economic experiments. Experimental Economics, 10(2), 171–178.

Glockner, A., & Hochman, G. (2011). The interplay of experience-based affective and probabilistic cues in decision making. Experimental Psychology, 58(2), 132–141.

Greiner, B. (2004). An online recruitment system for economic experiments. In Kremer, K., & Macho, V. (Eds.) Forschung Und Wissenschaftliches Rechnen. Gwdg Bericht 63. Ges. für wiss (pp. 79–93). Göttingen: Datenverarbeitung.

Harrison, G.W., Johnson, E., McInnes, M.M., & Rutström, E.E. (2005). Risk aversion and incentive effects: Comment. The American Economic Review, 95(3), 897–901.

Harrison, G.W., Lau, M.I., & Rutström, E.E. (2009). Risk attitudes, randomization to treatment, and self-selection into experiments. Journal of Economic Behavior & Organization, 70(3), 498–507.

Harrison, G.W., & Rutström, E.E. (2008). Risk aversion in the laboratory. In Cox, J.C., & Harrison, G.W. (Eds.) Research in Experimental Economics Vol 12: Risk Aversion in Experiments (Vol. 12 pp. 41–196). Bingley: Emerald Group Publishing Limited.

Hey, J.D., & Orme, C. (1994). Investigating generalizations of expected utility theory using experimental data. Econometrica, 62(6), 1291–1326.

Holt, C.A., & Laury, S.K. (2002). Risk aversion and incentive effects. The American Economic Review, 92(5), 1644–1655.

Holt, C.A., & Laury, S.K. (2005). Risk aversion and incentive effects: New data without order effects. The American Economic Review, 95(3), 902–904.

Lusk, J.L., & Coble, K.H. (2005). Risk perceptions, risk preference, and acceptance of risky food. American Journal of Agricultural Economics, 87(2), 393–405.

Miller, L., Meyer, D.E., & Lanzetta, J.T. (1969). Choice among equal expected value alternatives: Sequential effects of winning probability level on risk preferences. Journal of Experimental Psychology, 79(3), 419–423.

Norwood, B.F., Lusk, J.L., & Brorsen, B.W. (2004a). Model selection for discrete dependent variables: Better statistics for better steaks. Journal of Agricultural and Resource Economics, 29(3), 404–419.

Norwood, B.F., Roberts, M.C., & Lusk, J.L. (2004b). Ranking crop yield models using out-of-sample likelihood functions. American Journal of Agricultural Economics, 86(4), 1032–1043.

Palacios-Huerta, I., & Serrano, R. (2006). Rejecting small gambles under expected utility. Economics Letters, 91(2), 250–259.

Prelec, D. (1998). The probability weighting function. Econometrica, 66(3), 497–528.

Quiggin, J. (1982). A theory of anticipated utility. Journal of Economic Behavior & Organization, 3(4), 323–343.

Rabin, M. (2000). Risk aversion and expected-utility theory: a calibration theorem. Econometrica, 68(5), 1281–1292.

Roy, R., Chintagunta, P.K., & Haldar, S. (1996). A framework for investigating habits, “the hand of the past,” and heterogeneity in dynamic brand choice. Marketing Science, 15(3), 280–299.

Rubinstein, A. (2006). Dilemmas of an economic theorist. Econometrica, 74 (4), 865–883.

Saha, A. (1993). Expo-power utility: A flexible form for absolute and relative risk aversion. American Journal of Agricultural Economics, 75(4), 905–913.

Selten, R., Sadrieh, A., & Abbink, K. (1999). Money does not induce risk neutral behavior, but binary lotteries do even worse. Theory and Decision, 46(3), 213–252.

StataCorp. (2011). Stata 12 base reference manual.. College Station, TX: Stata Press.

Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5(4), 297–323.

Wakker, P., & Deneffe, D. (1996). Eliciting von Neumann-Morgenstern utilities when probabilities are distorted or unknown. Management Science, 42(8), 1131–1150.

Wakker, P.P. (2010). Prospect theory for risk and ambiguity. Cambridge: Cambridge University Press.

Watt, R. (2002). Defending expected utility theory. The Journal of Economic Perspectives, 16(2), 227–229.

Wu, G., & Gonzalez, R. (1996). Curvature of the probability weighting function. Management Science, 42(12), 1676–1690.

Acknowledgments

The authors would like to thank Peter Wakker and Glenn Harrison for helpful comments on the manuscript and John Hey for helping shorting out estimation related questions. We also gratefully acknowledge the critical reviews by multiple referees on previous versions of our paper.

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Drichoutis, A.C., Lusk, J.L. What can multiple price lists really tell us about risk preferences?. J Risk Uncertain 53, 89–106 (2016). https://doi.org/10.1007/s11166-016-9248-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11166-016-9248-5

Keywords

- Expected utility theory

- Multiple price list

- Probability weighting

- Rank dependent utility

- Elicitation methods