Abstract

In this study, we investigate the relationship between CEO tenure and cost of debt. Using a sample of the FTSE All-Share Index firms listed on the London Stock Exchange for the period 2009 to 2018 and the ordinary least squares regression (OLS) estimation method, we find that cost of debt is higher for firms with CEOs in their early tenure in office than those in their later tenure in office. Further analysis shows that board independence attributes including (1) the proportion of independent directors on the board, (2) full (100%) independent audit committee members, and (3) a lead independent director representation on the board interact with CEO early tenure in office to reduce cost of debt due to the board’s effective monitoring ability when the CEO is new and risk-seeking. Our study extends CEO tenure and corporate outcomes in general and in particular CEO risk-taking incentives and cost of debt literature, and has important implications for firms seeking to raise finance from the debt market when their CEO is new as well as identifying the control mechanisms that they need to put in place to lower the cost of debt.

Similar content being viewed by others

Notes

More broadly, DeFusco et al. (1990) report a negative reaction of bond price following the announcement of the adoption of managerial stock option plan. Ortiz-Molina (2006) also documents a positive association between managerial ownership and borrowing costs, and that stock options held by the firm’s top five managers have a larger effect on cost of debt than stock ownership has. Similarly, while Billett et al. (2010) document a positive (negative) market reaction to delta (vega) following the first-time award of stock options to CEOs, Knopf et al. (2002) report a positive impact of the number of shares held by the CEO on derivatives but their subsequent findings suggest a negative (positive) impact of CEO vega (delta) on derivatives.

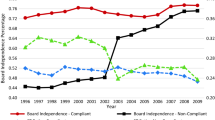

The board independence attributes we consider in this study include the proportion of independent directors on the board, full (i.e. 100%) independent audit committee members, and a lead independent director representation on the board.

It is important to highlight that a lead independent director representation on the board—has surprisingly not been tested on managerial risk-taking or cost of debt. However, previous literature suggests that a lead independent director representation on the board improves board monitoring (Chen and Ma 2017) and investment efficiency (Rajkovic 2020). Therefore, we include a lead independent director representation on the board in our board independence attributes analysis.

In this study, we select board independence attributes as effective monitoring mechanisms because the existing literature has found them to improve corporate governance quality (Chen and Ma 2017) and, therefore, they are more likely to restrict risk-taking behaviour during the CEO’s career cycle and reduce cost of debt.

Shaw (2012) also finds competing results when the sensitivities of CEO stock and option compensation portfolios to stock price (delta) and stock return (vega) volatility are used to proxy CEO risk-taking incentives.

Even though our study period is restricted from 2009 to 2018 due to CEO tenure and cost of debt data availability from the Bloomberg terminal, the 10-year period is a suitably long and sustained period to investigate this important and interesting topic.

In calculating the cost of debt, Bloomberg use the debt adjustment factor that captures the average yield spread between corporate bonds for a given credit class and the government bonds.

We employ the first 3 years of a firm’s CEO in office to proxy CEO early tenure because it is well documented in the existing literature (e.g., Ali and Zhang 2015; Mitra et al. 2020) that CEOs are likely to engage in very risky operations during this period of their career cycle than in their later years in office and debtholders are likely to factor this period in when determining their risk premium. Hence, we define CEO’s early tenure to capture the first three years in office.

The components of the CEO compensation include salary, bonus, pension, and other awards (but excluding share options).

Although our sample size reduced to 2033 firm-year observations for CAPEX and 1988 firm-year observations for R&D when missing values are not coded as zero, our results (untabulated) from these reduced samples are qualitatively similar to the main results reported in Table 3.

The results (untabulated) from further test for differences between firms with CEOs in their early tenure in office and those in their final year in office are qualitatively similar to the reported results under Panel B of Table 1.

Chen et al. (2016) argue in their study that the industry average of the CEO tenure from the previous year may affect a firm’s CEO tenure but it is not likely to be related to the outcome variable. We follow a similar assumption and use CEOTenure_INDAVG as our instrumental variable.

In our second approach of addressing endogeneity, we could not find any valid instrument for the interaction terms (i.e. CEO tenure and the board independent attributes) and, therefore, we use other governance controls to further check the robustness of our results in Sect. 6.1.

References

Adams RB, Funk P (2012) Beyond the glass ceiling: does gender matter? Manag Sci 58(2):219–235

Akbar S, Kharabsheh B, Poletti-Hughes J, Shah SZ (2017) Board structure and corporate risk taking in the UK financial sector. Int Rev Financ Anal 50:101–110

Ali A, Zhang W (2015) CEO tenure and earnings management. J Account Econ 59(1):60–79

Anderson RC, Mansi SA, Reeb DM (2004) Board characteristics, accounting report integrity, and the cost of debt. J Account Econ 37(3):315–342

Ashbaugh H, LaFond R, Mayhew BW (2003) Do nonaudit services compromise auditor independence? Further evidence. Account Rev 78(3):611–639

Ashbaugh-Skaife H, Collins DW, LaFond R (2006) The effects of corporate governance on firms’ credit ratings. J Account Econ 42(1–2):203–243

Aslan H, Kumar P (2012) Strategic ownership structure and the cost of debt. Rev Financ Stud 25(7):2257–2299

Axelson U, Bond P (2009) Investment bank career. Working Paper. Stockholm School of Economics and University of Pennsylvania

Ball R, Bushman RM, Vasvari FP (2008) The debt-contracting value of accounting information and loan syndicate structure. J Account Res 46(2):247–287

Bargeron LL, Lehn KM, Zutter CJ (2010) Sarbanes-Oxley and corporate risk-taking. J Account Econ 49(1–2):34–52

Bhojraj S, Sengupta P (2003) Effect of corporate governance on bond ratings and yields: the role of institutional investors and outside directors. J Bus 76(3):455–475

Billett MT, Mauer DC, Zhang Y (2010) Stockholder and bondholder wealth effects of CEO incentive grants. Financ Manag 39(2):463–487

Bradley M, Chen D (2015) Does board independence reduce the cost of debt? Financ Manag 44(1):15–47

Charness G, Gneezy U (2012) Strong evidence for gender differences in risk taking. J Econ Behav Organ 83(1):50–58

Chen MA, Ma H (2017) Lead directors, monitoring, and forced CEO turnover. Working Paper. https://editorialexpress.com/cgi-bin/conference/download.cgi?db_name=CICF2017&paper_id=974. Accessed 20 Jan 2021

Chen S, Ni X, Tong JY (2016) Gender diversity in the boardroom and risk management: a case of R&D investment. J Bus Ethics 136(3):599–621

Chen WT, Zhou GS, Zhu XK (2019) CEO tenure and corporate social responsibility performance. J Bus Res 95:292–302

Cheng S (2004) R&D expenditures and CEO compensation. Account Rev 79(2):305–328

DeAngelo LE (1988) Managerial competition, information costs, and corporate governance: the use of accounting performance measures in proxy contests. J Account Econ 10(1):3–36

Dechow PM, Sloan RG (1991) Executive incentives and the horizon problem: an empirical investigation. J Account Econ 14(1):51–89

DeFusco RA, Johnson RR, Zorn TS (1990) The effect of executive stock option plans on stockholders and bondholders. J Finance 45(2):617–627

Desai H, Hogan CE, Wilkins MS (2006) The reputational penalty for aggressive accounting: earnings restatements and management turnover. Account Rev 81(1):83–112

Dhaliwal D, Hogan C, Trezevant R, Wilkins M (2011) Internal control disclosures, monitoring, and the cost of debt. Account Rev 86(4):1131–1156

Elamer AA, Ntim CG, Abdou HA, Owusu A, Elmagrhi M, Ibrahim AEA (2021) Are bank risk disclosures informative? Evidence from debt markets. Int J Finance Econ 26(1):1270–1298

Elliott JA, Shaw WH (1988) Write-offs as accounting procedures to manage perceptions. J Account Res 26(Suppl.):S91–S119

Elyasiani E, Jia JJ, Mao CX (2010) Institutional ownership stability and the cost of debt. J Financ Mark 13(4):475–500

Ertugrul M, Hegde S (2008) Board compensation practices and agency costs of debt. J Corp Finance 14(5):512–531

Ezeani E, Salem R, Kwabi F, Boutaine K, Komal B (2021) Board monitoring and capital structure dynamics: evidence from bank-based economies. Rev Quant Finance Account 58:473–498

Fama EF (1980) Agency problems and the theory of the firm. J Polit Econ 88(2):288–307

Francis J, LaFond R, Olsson P, Schipper K (2005) The market pricing of accruals quality. J Account Econ 39(2):295–327

Gibbons R, Murphy KJ (1992) Optimal incentive contracts in the presence of career concerns: theory and evidence. J Polit Econ 100(3):468–505

Hambrick DC, Fukutomi GD (1991) The seasons of a CEO’s tenure. Acad Manag Rev 16(4):719–742

Harjoto M, Laksmana I (2018) The impact of corporate social responsibility on risk taking and firm value. J Bus Ethics 151(2):353–373

Henderson AD, Miller D, Hambrick DC (2006) How quickly do CEOs become obsolete? Industry dynamism, CEO tenure, and company performance. Strateg Manag J 27(5):447–460

Hermalin BE, Weisbach MS (1998) Endogenously chosen boards of directors and their monitoring of the CEO. Am Econ Rev 88:96–118

Holmström B (1982) Moral hazard in teams. Bell J Econ 13(2):324–340

Holmström B (1999) Managerial incentive problems: a dynamic perspective. Rev Econ Stud 66(1):169–182

Jensen MC, Meckling WH (1976) Theory of the firm: managerial behavior, agency costs and ownership structure. J Financ Econ 3(4):305–360

Jianakoplos NA, Bernasek A (1998) Are women more risk averse? Econ Inq 36(4):620–630

Joni J, Ahmed K, Hamilton J (2020) Politically connected boards, family and business group affiliations, and cost of capital: evidence from Indonesia. Br Account Rev 52(3):100878

Kabir R, Li H, Veld-Merkoulova YV (2013) Executive compensation and the cost of debt. J Bank Finance 37(8):2893–2907

Kalyta P (2009) Accounting discretion, horizon problem, and CEO retirement benefits. Account Rev 84(5):1553–1573

Kennedy P (2008) A guide to econometrics. Blackwell Publishing, Malden

Knopf JD, Nam J, Thornton JH Jr (2002) The volatility and price sensitivities of managerial stock option portfolios and corporate hedging. J Finance 57(2):801–813

Lardaro L (1993) Applied econometrics. Harper Collins College Publishers, New York

Levinthal DA, March JG (1993) The myopia of learning. Strateg Manag J 14(S2):95–112

Lorca C, Sánchez-Ballesta JP, García-Meca E (2011) Board effectiveness and cost of debt. J Bus Ethics 100(4):613–631

Luo X, Kanuri VK, Andrews M (2014) How does CEO tenure matter? The mediating role of firm–employee and firm–customer relationships. Strateg Manag J 35(4):492–511

Mahoney L, Roberts RW (2007) Corporate social performance, financial performance and institutional ownership in Canadian firms. Account Forum 31(3):233–253

Miller D, Shamsie J (2001) Learning across the life cycle: experimentation and performance among the Hollywood studio heads. Strateg Manag J 22(8):725–745

Mitra S, Song H, Lee SM, Kwon SH (2020) CEO tenure and audit pricing. Rev Quant Finance Account 55(2):427–459

Ni Y, Purda LD (2012) Does monitoring by independent directors reduce firm risk? Available at SSRN 1986289

Ortiz-Molina H (2006) Top management incentives and the pricing of corporate public debt. J Financ Quant Anal 41(2):317–340

Owusu A, Weir C (2016) The governance–performance relationship: evidence from Ghana. J Appl Account Res 17(3):285–310

Owusu A, Weir C (2018) Agency costs, ownership structure and corporate governance mechanisms in Ghana. Int J Account Audit Perform Eval 14(1):63–84

Owusu A, Zalata AM, Omoteso K, Elamer AA (2022) Is there a trade-off between accrual-based and real earnings management activities in the presence of (fe)male auditors? J Bus Ethics 175(2):815–836

Oyer P (2008) The making of an investment banker: stock market shocks, career choice, and lifetime income. J Finance 63(6):2601–2628

Pandey R, Biswas PK, Ali MJ, Mansi M (2020) Female directors on the board and cost of debt: evidence from Australia. Account Finance 60(4):4031–4060

Pittman JA, Fortin S (2004) Auditor choice and the cost of debt capital for newly public firms. J Account Econ 37(1):113–136

Pourciau S (1993) Earnings management and nonroutine executive changes. J Account Econ 16(1–3):317–336

Rajkovic T (2020) Lead independent directors and investment efficiency. J Corp Finance 64:101690

Sengupta P (1998) Corporate disclosure quality and the cost of debt. Account Rev 73(4):459–474

Sharma DS, Tanyi PN, Litt BA (2017) Costs of mandatory periodic audit partner rotation: evidence from audit fees and audit timeliness. Audit J Pract Th 36(1):129–149

Shaw KW (2012) CEO incentives and the cost of debt. Rev Quant Finance Account 38(3):323–346

Shi C (2003) On the trade-off between the future benefits and riskiness of R&D: a bondholders’ perspective. J Account Econ 35(2):227–254

Strong JS, Meyer JR (1987) Asset writedowns: managerial incentives and security returns. J Finance 42(3):643–661

Tran DH (2014) Multiple corporate governance attributes and the cost of capital—evidence from Germany. Br Account Rev 46(2):179–197

Usman M, Farooq MU, Zhang J, Makki MAM, Khan MK (2019) Female directors and the cost of debt: does gender diversity in the boardroom matter to lenders? Manag Audit J 34(4):374–392

Wu S, Levitas E, Priem RL (2005) CEO tenure and company invention under differing levels of technological dynamism. Acad Manag J 48(5):859–873

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Owusu, A., Kwabi, F., Ezeani, E. et al. CEO tenure and cost of debt. Rev Quant Finan Acc 59, 507–544 (2022). https://doi.org/10.1007/s11156-022-01050-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-022-01050-2