Abstract

The role of the construction industry in economic growth has been widely discussed in the extant literature, but existing studies have not investigated the disaggregated impact of construction investments on the production and social sectors. This study examines the disaggregated effect of construction investments on the Saudi economy. The study uses a social accounting matrix of Saudi Arabia and constructs a dynamic computable general equilibrium model. The findings reveal that construction investments significantly boosted GDP and aggregate investments in the first two periods; however, the growth declined in the following three periods. This finding underlines the importance of long-term investments in the construction sector and calls for continuous monitoring and updating of the investment policy for sustainable development. This study also presents the disaggregated impact of investments on the value-added by each sector of the economy. The ranking of sectors exhibits that mining and quarry activities underwent a high increase in value-added, second to construction activities. Other economic activities also experienced growth in value-added and some of them changed their ranks within the five years.

Similar content being viewed by others

Introduction

The construction and real estate market is strongly interconnected with other sectors of the economy, either as a stimulator for more production for some sectors (backward linkage) or as a supplier meeting the demand of other sectors (forward linkage) (Ahmed et al. 2021a, b; Ali et al. 2019; Ciaschini and Socci 2007). The construction industry contributes not only to economic development but also to the promotion of socioeconomic and sustainable development in other industries by producing construction products (Hu and Liu 2017).

A wide strand of literature has addressed the interdependencies between the construction, real estate, and finance sectors (Li et al. 2022), taking into account the diversity of territorial contexts from a socioeconomic (Ahmed and Medabesh 2020; David and Halbert 2014; Okunev et al. 2000; Popescu and Cişmaşu 2013; Sim and Chang 2006) and institutional perspectives (Aveline-Dubach 2008; Theurillat et al. 2010; Theurillat and Crevoisier 2014). In their seminal work, Chen and Tongurai (2021) investigated the relationship between the construction/real estate market and the industrial metals market in China and demonstrated through a vector autoregression model, causality study, and cointegration analysis that the industrial metals market has both short- and long-run associations with the real estate market and that changes in copper futures prices are highly attributed to the size of newly started constructions. Moreover, Diana and Negescu (2013) outlined the unfavorable effects of the real estate market downfall on construction companies and manufacturers of construction materials after the financial crisis of 2008. With more than 20 million jobs in more than 3.29 million companies, mainly micro and small companies, and as one of the main consumers of intermediate products and services, contributing almost 10% to the GDP, the construction sector plays a significant role in the European economy, and its performance can heavily influence the overall growth of the economy (Diana and Negescu 2013).

Hence, the construction sector is a pillar stone in the world economy. It is mostly affected by socioeconomic policies, and it generally tends to be in permanent swing, which, unlike other markets, requires special intervention from the government and other organizations to be regularized and stabilized. Megatrends such as globalization, urbanization, digitalization, sociodemographic, and sustainability changes are constantly shaping the real estate industry (Pfnür and Wagner 2020). The fluctuations in real estate investments are likely to have significant impacts on the creation of symbiosis between financial markets and real estate initiatives, growth in gross domestic income, increasing job opportunities in the construction sector, leasing and sales activities, decreasing unemployment rates, and enhancing the quality of life and economic growth (Anghel and Hristea 2015; Chen and Tongurai 2021).

The existing literature on the construction industry has been conducted from different perspectives, incorporating different approaches and investigating different dimensions. Using input–output (IO) tables, Bon and Pietroforte (1990) assessed the economic impact of the construction industry. Since then, several studies have been devoted to the application of IO analysis in the construction industry. In their seminal work, Zhu et al. (2020) summarized the application of IO analysis in the construction industry into five major groups—(1) the utilization of the direct and total resources of the construction industry, (2) the interindustry linkages of the construction industry and its impact on economic development, (3) the role of the construction industry in employment creation, (4) the productivity of the construction industry, and (5) the impact of technology on the construction industry (Ali et al. 2019; Bon 2018; Liu and He 2016; Song et al. 2006).

However, the IO analysis uses IO tables that do not include primary and secondary income distribution. This can be detrimental because it impacts interindustry connections, which can affect the findings of the impact analysis (Ahmed and Medabesh 2020; Harada 2015). As mentioned by Miyazawa (1976), this is because the production industry is linked to consumption structures, which depend on the structure of income distribution, as it regulates the expenditure behavior of different income groups of a social sector, which are referred to as households. The social accounting matrix (SAM) presents the generation, distribution, and redistribution of income along with industrial production, thereby providing an analytical framework for impact analysis with precise findings (Ahmed et al. 2021a, b). This study is different from existing works as it incorporates a SAM that allows us to study the aggregated and disaggregated impact of external shock on production and social sectors.

As a “rentier state,” Saudi economy is heavily dependent on its oil trade, and the whole economic wealth is mainly driven by oil resources. However, modern economies are facing massive efforts to start a profound change in the production system and use of energy sources to realize a green, ecological, and inclusive transition by encouraging the circular economy and the development of renewable energy sources (Zhang et al. 2019). In 2017, to free Saudi Arabia from oil reliance, the government implemented some economic policies and reforms under the umbrella of Saudi Vision 2030. They revolved around the diversification of income sources through a package of improved social and structural reforms based mainly on job creation, poverty alleviation, diversification, and balanced regional development.

Saudi Vision 2030 vision has implemented different policies to achieve these goals, which are divided into three stages. Finalizing the first edition of the program (2018–2020) that aims at preparing and transforming mindsets, increasing international performance, planning and implementation, the Saudi public investment fund, the main authority responsible for the implementation and accomplishment of the vision, started to realize the vision’s second pillar “Thriving Economy.” The main objectives of the vision’s second pillar “Thriving Economy” (2021–2025) are to diversify the economy, localize cutting-edge technology and knowledge, and develop strategic sectors and solid economic partnerships that increase Saudi regional and global impact. To support these goals and help accomplish the aspirations of Saudi Vision 2030, the public investment fund established eight strategic companies—NEOM, Qiddiya Investment Company, Amaala Company, the Red Sea Development Company, Roshn Real Estate Company, the Saudi Agriculture and Livestock Investment Company, the National Unified Procurement Company, and ACWA Power (SAMA 2021).

The Vision 2030’s ambitious objectives have been decrypted into 80 policies, including the improvement of infrastructure through public-funded projects, such as the Riyadh metro and Riyadh rapid bus transit system; incentives for Saudi investors to invest more inside than outside the country; the establishment of a Saudi tourism authority; the launch of the national program for information technology development; formation of the Supreme Committee for Energy Mix for Electricity Production and enforcing the renewable energy sector; and the creation of a Supreme Economic Council to strengthen private sectors by designing a regulatory framework for its activity and responsibility. As a result of these initiatives, the Saudi Central Bank has reported an improvement in finance, insurance, real estate, and business services; transport, storage, and communication; wholesale and retail trade and restaurants and hotels; manufacturing industries; and agriculture, forestry, and fishing (54th annual report, Saudi Arabian Monetary Authority). Most economic production activities (at constant prices) experienced a growing trend at different rates, and the non-oil sector GDP has recorded a positive year-on-year growth of 2.0% compared with the oil sector’s year-on-year growth of 1.4% (MEFIC Capital monthly report 2019).

One of the most important sectors that helped to diversify revenue resources and reduce the country’s reliance on oil is the tourism sector. Under its strategic Vision for 2030, the Kingdom of Saudi Arabia has undergone a remarkable cultural initiative to welcome international and national leisure tourists and support the growth of the tourism sector. By 2030, this sector is expected to contribute 10% to GDP and generate 1 million new jobs and 100 million visitations—45 M domestic and 55 M international visitations (Saudi tourism authority official website: https://sta.gov.sa/en/). To achieve this goal, the government is determined to expand the tourism sector by investing SAR 220 billion by 2023 and SAR 500 billion by 2030 to establish a huge line of construction and undertake key attractive projects, such as NEOM, Red Sea Project, Qiddiya, and Amaala (Durrani 2021). The existing and upcoming quality hotel supply in the main cities of Saudi Arabia, that is, Riyadh, Jeddah, and Dammam is expected to increase by 25%, 53%, and 23% by 2023, respectively. Saudi Arabia has the world’s highest hotel construction projects, with a room supply expansion rate of 61.1% by 2023, representing the highest rate among the most 50 populated countries in the world (Durrani 2021).

In line with its tourism-related construction growth rate, since 2015, the Kingdom has witnessed rapid urban growth, especially in its main cities, due to exceptional economic and social growth, increasing the number of cities to 285 (Balabel and Alwetaishi 2021). To encourage demand and enhance supply in the residential building sector, the Saudi government has implemented many regulations, imposing taxes on vacant lands, creating financial institutions to boost real estate development, exempting real estate transactions from 15% VAT, and implementing a lower property tax to reach the goal of 70% home ownership by 2030. The government has also projected the construction of 2.4 million square meters of housing located in the main cities of Riyadh, Jeddah, and Dammam (Krarti 2020). Moreover, the government launched the “Future Saudi Cities” program with the principal objective to “develop environmentally sustainable cities with adequate infrastructure and high quality of life” (Balabel and Alwetaishi 2021). Hence, the construction sector in Saudi Arabia is growing fast to support tourism demand in hotels and leisure infrastructure. Based on the above discussion, the following research questions arise:

RQ1: Do construction investments have a steady impact on aggregate GDP?

RQ2: What is the disaggregated impact of construction investments on the other sectors of the Saudi economy?

RQ3: How are the social sector and households affected by the construction sector?

To answer these research questions, this study investigates the aggregated and disaggregated impact of investments in the construction sector on the inclusive economic growth of the country. The study constructs a dynamic computable general equilibrium (DCGE) model using the SAM of the Kingdom of Saudi Arabia (KSA-SAM). The next section presents the method. "Policy simulation and findings of the analysis" section describes the findings of the analysis, and finally, "Conclusion" section concludes.

SAM and a DCGE model

This study employs the 2017 KSA-SAM. SAM is a very flexible accounting scheme and is particularly suitable for representing the social and economic situation of a country in its complexity. All economic flows recorded among the various actors are allocated according to their different origins and destinations, highlighting the logical links within the various stages of multisectoral and circular income flows (Socci et al. 2022), including production, value-added generation, primary income allocation, secondary income distribution, income utilization, and income accumulation. The KSA-SAM is presented in Table 1.

The current KSA-SAM characterizes 18 activities and 18 commodities with 2 primary factors (labor and capital), 3 private institutional sectors (nonfinancial corporations, financial corporations, and households), 1 public institutional sector (government), and the rest of the world. It also includes a capital account, direct and indirect taxes on commodities and activities, taxes on income, and import tariffs. The construction of the SAM started with the structure of the supply and use tables, and it is implemented along with the primary and secondary distribution of income through the National Accounts database, which affects the disposable income of institutional sectors. This allows for an analysis of the use of disposable income of each institutional sector, disaggregating it into consumption (exports to the rest of the world) and savings, and the sum of the latter coincides with the sum of investment by commodity made in the country. Therefore, a cycle is formed in which final demand leads to output through production, which generates primary income for institutional sectors, and, finally, disposable income induces final demand and thus closes the loop (Ahmed et al. 2018a, b). The SAM presents a structure based on the supply and use scheme, making it possible to analyze production in terms of commodities and activities, thus distinguishing between primary and secondary production for each industry.

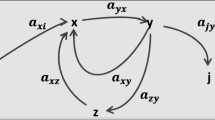

To evaluate the disaggregated effect of construction investments on the Saudi economy, a DCGE model based on the KSA-SAM is calibrated. The DCGE model presents a system of simultaneous linear and nonlinear equations, where the production function that generates the output in terms of commodities and activities follows a nested constant elasticity of substitution (CES) structure, as depicted in Fig. 1, and the output by commodity is allocated to demand. The purpose of the nested CES structure is to replicate the substitution and complementary relations across the various inputs of production.

Production function and allocation of total output

The structure of the model can be directly linked to the structure of the KSA-SAM, which then provides the flows for the initial calibration of the model. It follows the structuralist approach that considers income and wealth distribution, foreign trade, production chain density, and financial intermediaries (Taylor 1990). It is considered a powerful tool to estimate the economic impact of exogenous shocks on the demand and supply sides, revealing the direct and indirect effects of a public policy on an economic system (Pretaroli et al. 2018).

The dynamics of the model are characterized by the condition of capital accumulation. If the total value of the capital stock K in each period is obtained from the sum of the capital stock and total investment I generated in the previous period, then the equation is given as follows:

where t indicates the time, and \(\partial\) represents the capital depreciation rate. It is also considered a representative household that is rational and follows the maximum utility function (Lau et al. 2002).

where C indicates the total consumption; hh indicates households and \(\rho\) is the (exogenous) parameter of intertemporal preference (Paltsev 2004). The maximization process of the utility function takes place under the constraints on the total consumption expenditure that have to respect the following constraints:

Equation 3 states that the total consumption of households has to be equal to the difference between the total production by commodity Q, and the sum of the intermediate consumption b the public consumption pe, the investments I and the exports e. At the same time, Eq. 4 states that the total consumption of households has to be equal to the difference between the disposable income Y and the total saving S of households.. The disposable income is a function of the primary and secondary distribution.

where K represents capital endowment, L labor, a taxes on income, and tr net transfers.

The model is based on the complementarity approach in the approximation of infinite horizon choices within a finite horizon model that is presented in five years, and it assumes perfect competition in all markets and steady-state growth, wherein output, consumption, and capital grow at constant rates.

The other conditions of equilibrium—market clearing condition and zero profit condition—specify the quantities and prices in the market, although the model includes some behavioral rigidities of public administration and the rest of the world.

Policy simulation and findings of the analysis

In our simulation, we introduced a shock of SAR 317,616 million in the demand side to the construction commodity (it is customary to treat sectors/industries as commodities in SAM analysis). This amount is selected from the total injection of SAR 220 billion in investments for key projects, such as NEOM, Red Sea Project, Qiddiya, and Amaala, by 2023 and from the calculated amount of 61.1% increase in hotel construction by 2023. The corresponding amount relative to the GDP for 2017 was calculated as SAR 317,616 million. This will be distributed in five equal periods in the simulation, that is, each period has 20% of the total shock, and the total policy weight on GDP is 10.13%. The simulation results include direct and indirect policy impact on economic variables over time. In the CGE analysis, we construct and solve the SAM model first and record the benchmark values. Then, the shock is introduced, and the new values are recorded and compared with the benchmark to elaborate the variations. We record the policy effects in terms of GDP, household consumption, investments, exports, and imports. The disaggregated sector-wise value-added variation is also estimated. Table 2 presents the percentage change in the policy effect on the macroeconomic variables.

It is obvious from Table 2 that GDP appreciated significantly in the first two periods by 5.23% and 3.45%, while it started decreasing in the next three periods, albeit being a positive change. The total multiplier effect is significant, and this indicates that for each unit of SAR invested in the economic system, the total real system response (direct, indirect, and induced effects) is SAR 1.35. As this is a demand side policy, an increase in demand leads to an increase in the price level, as indicated by the GDP deflator. However, the increase in the price level is not far-reaching. This is because increased demand leads to increased production, which produces the opposite effect on the price level. Furthermore, the increase in prices tends to decline in the period.

The high increase in the first period can be explained from different perspectives. First, the CGE analysis allows the assessment of all the direct and indirect effects of an economic policy on the whole economic system. An increase in one commodity may also increase the demand and production of other commodities because of the presence of intersectoral linkages (Ahmed et. 2021; Ahmed and Medabesh 2020). The institutional sectors are also interconnected within the economic structure, and, hence, any shock to the economy may activate all the economic agents, which ultimately leads to an increase in investments (Ahmed et al. 2018a, b). These investments and production output of interconnected industries are high in the initial phases and are normalized and stabilized in the subsequent periods. This declining trend is consistent with the study by Ertugrul and Pirgaip (2021), who investigated the relationship between construction investments and economic growth in ten developing countries, including Saudi Arabia, from 1970 to 2019. The authors found an inverted U-shaped pattern, consistent with Bon’s proposition, implying that the contribution of construction investments starts diminishing at some point in time as economic growth reaches a certain brink. On the other hand, Zhu et al. (2020) studied the impact of the construction industry’s investments on the Australian economy using a hypothetical extraction method to analyze 15 IO tables from 2000 to 2014. Their findings confirm that the impact on other industries’ output was high in the first year and then experienced a stable declining trend.

Another explanation is inferred from the study by Erol and Unal (2015), who maintained that the temporary effect of GDP is attributed to the construction sector’s sensitivity to interest rates. Interest rates are relatively low at the beginning of any expansionary period, but they are expected to rise because of the expansionary, creating a feedback effect and decreasing construction activities as all construction sectors rely on financing costs. Table 3 presents the effect of an interest rate change on GDP. As this is an exogenous change in interest rate, the results can be presented as a sensitivity analysis of the model to changes in exogenous parameters.

A decrease in the interest rate is transferred into an increase in GDP from the second year. This leads to changes in households’ intertemporal choices in decisions between consumption and savings. An increase in the interest rate generates the opposite effect on GDP. In addition, the obtained results indicate that the model used does not generate biased effects for changes in exogenous variables.

Examining the statistical relationship between GDP growth and the construction sector in Europe, we found that, unlike investments in residential construction, public infrastructure investments have a short-term effect on economic growth and a weaker effect in the long term (Aali-Bujari and Venega-Martinez 2021). On the other hand, using longitudinal analysis, several seminal works have investigated the causal relationship between construction investments and economic growth in Hong Kong, Cape Verde, Sri Lanka, and Korea and concluded that the construction sector is a follower of economic fluctuations rather than a driver of GDP growth (Alhowaish 2015; Kim 2004; Lopes et al. 2011; Tse and Ganesan 1997). Based on the above discussion, the country should continue to monitor and update construction-induced growth policies and be ready to reconsider and reframe them with more innovative and environmentally friendly technologies to enhance the important role of construction in inclusive economic growth.

Table 2 indicates that investments have undergone a significant rise in the first two periods and then decreased in the following periods with steady growth. Moreover, household consumption did not experience a high appreciation because construction activities are capital intensive, requiring 74% of capital and 26% of labor, as presented by SAM. However, the distribution of capital among the institutional sectors reveals that households receive only 23% of capital as primary income. This implies that households’ disposable income is growing but not to a large extent, and, therefore, consumption growth is low. The findings indicate an increase in imports and a decrease in exports. This confirms that investment injections in the construction sector lead to an increase in imports, which can either be commodities related to the construction industry or other utility commodities. This phenomenon can be explained by the disaggregated value-added variations by activity, as mentioned in Table 4.

Table 4 presents the ranking of the value-added variations by activity. The ranking is constructed based on the results in the first period. It is possible to observe that the first place is “construction,” and it depends on existing policies because the construction sector is directly affected by policies.

When construction activities are stimulated, it indirectly increases the value-added of all other activities of the economic system. In particular, “mining and quarry” increased by 6.6% in the first year, placing second in the ranking for the entire period. This finding confirms that of Zhu et al. (2020), who found that the mining and quarry industry has a strong linkage with the construction sector in the structural analysis of inter-industrial linkages. Other activities such as “agriculture, hunting, and forestry”; “manufacturing”; and “wholesale and retail trade” had a significant increase, but after the first and second years, their growth decreased faster than that of other activities, falling in the ranking. In the second and third periods, the top positions in the ranking are filled by “transport”; “financial intermediation”; and “electricity, gas, and water supply.” This classification remained stable at the end of the period. For the other activities, the variations were significant but had lower values, without important effects on the ranking.

Conclusion

The construction sector is connected with several other sectors as it consumes various materials that are produced and supplied by other industries as inputs. Therefore, there is an economic pull effect toward these upstream industries. On the other hand, there is a demand for intermediate goods by all these industries for their production, which is an economic push effect created by the construction sector toward downstream industries. Hence, this sector has a strong backward and forward linkage with other economic sectors, and this linkage is reflected in income generation, employment creation, demand stimulation, and, ultimately, appreciation of the aggregated GDP. Therefore, the construction sector is a key sector for an economy not only for aggregated economic development but also for the disaggregated production growth of other industries. This study investigates the aggregated and disaggregated effect of construction investments on the Saudi economy using SAM and the DCGE model over a finite period of five years.

The findings revealed high GDP and investment growth in the first two periods, followed by a decreasing growth in the next three periods. This finding is consistent with those of existing studies, which suggested that the effects of the construction sector in promoting economic growth become weaker at a certain point. One of the reasons is the multiplying effect of the increase in one sector’s output on the output of other interconnected production sectors. These direct and indirect impacts are high in the initial phases until economic growth reaches a certain point. After that point, the impact experiences a declining trend unless construction-led growth policies are revisited and updated. A lack of environmentally friendly technologies in the construction industry may also inhibit further investments due to public policies and constraints. Another reason is the construction sector’s sensitivity to interest rates. Interest rates are low at the initial stage of any expansionary period and rise in the expansionary phase of the economy. This movement in interest rates creates a feedback effect that decreases construction activities as they are affected by financing costs.

Therefore, long term reliance on construction investments may not be a good idea; hence, periodic scrutinizing and embellishing of the construction sector with innovative technology-based and environmentally friendly policies will ensure sustainable and inclusive economic growth. Our findings present not only the aggregate impact on GDP and other macroeconomic variables but also a disaggregated impact on value-added generation by each economic sector in five periods. These findings help to understand the direct and indirect effects and the linkages of the construction sector with other sectors of the economy. However, a different linkage study is required to present the backward and forward interindustry connections.

Availability of data and materials

The SAM is not allowed to be public by the authors. However, the interested parties could contact the corresponding author to obtain it.

Abbreviations

- DCGE:

-

Dynamic computable general equilibrium model

- IO:

-

Input–Output

- KSA:

-

Kingdom of Saudi Arabia

- NUPCO:

-

National unified procurement company and ACWA power

- PIF:

-

Public investment fund

- SALIC:

-

Saudi agriculture and livestock investment company

- SAM:

-

Social accounting matrix

References

Aali-Bujari A, Venegas-Martínez F (2021) Impact of construction industry on economic growth in Africa: Granger causality and GMM estimation of dynamic panel models. Rev Econ Finance, vol 19

Ahmed I, Medabesh AM (2020) Role of income distribution and consumption expenditure in agricultural output: case of Nigeria. Int J Soc Econ 47(8):991–1001

Ahmed I, Socci C, Severini F, Yasser QR, Pretaroli R (2018a) Financial linkages in the Nigerian economy: an extended multisectorial model on the social accounting matrix. Rev Urban Region Dev Stud 30(2):89–113

Ahmed I, Socci C, Severini F, Yasser QR, Pretaroli R (2018b) Forecasting investment and consumption behavior of economic agents through dynamic computable general equilibrium model. Financ Innovat 4(7):01–21

Ahmed I, Socci C, Pretaroli R, Severini F, Deriu S (2021a) Socioeconomic spillovers of the 2016–2017 Italian earthquakes: a bi-regional inoperability model. Environ Dev Sustain 24:426–453

Ahmed I, Socci C, Medabesh A, Severini F, Zotti J (2021b) Economic impact of monetary policy: focus on real estate sector in Italy. Int J Financ Econ 26(1):1256–1269. https://doi.org/10.1002/ijfe.1848

Alhowaish AK (2015) Causality between the construction sector and economic growth: the case of Saudi Arabia. Int Real Estate Rev 18(1):131–147

Ali Y, Sabir M, Muhammad N (2019) A comparative input-output analysis of the construction sector in three developing economies of South Asia. Constr Manag Econ 37(11):643–658

Anghel I, Hristea AM (2015) Some considerations regarding the international real estate market—present and future predictions. Proc Econ Finance 32:1442–1452. https://doi.org/10.1016/S2212-5671(15)01520-8

Aveline-Dubach N (2008) Immobilier, l’Asie, la bulle et la mondialisation. 319

Balabel A, Alwetaishi M (2021) Towards sustainable residential buildings in Saudi Arabia according to the conceptual framework of “Mostadam” rating system and vision 2030. Undefined 13(2):1–16. https://doi.org/10.3390/SU13020793

Bon R, Pietroforte R (1990) Historical comparison of construction sectors in the United States, Japan, Italy and Finland using input-output tables. Constr Manag Econ 8(3):233–247

Chen X, Tongurai J (2021) The relationship between China’s Real Estate market and industrial metals futures market: evidence from non-price measures of the real estate market. Asia-Pacific Finan Markets 28(4):527–561. https://doi.org/10.1007/S10690-021-09334-8

Ciaschini M, Socci C (2007) Bi-regional sam linkages: a modified backward and forward dispersion approach. Rev Urban Region Dev Stud 19(3):233–254. https://doi.org/10.1111/J.1467-940X.2007.00138.X

David L, Halbert L (2014) Finance capital, actor-network theory and the struggle over calculative agencies in the business property markets of Mexico city metropolitan. Region 48(3):516–529. https://doi.org/10.1080/00343404.2012.756581

Diana M, Negescu O (2013) Effects of the financial crisis and of the evolution of real estate market on the construction field in Romania. Theoret Appl Econ vol XX

Doreen H (2016) Economic Diversification in Saudi Arabia. https://jpinyu.com/wp-content/uploads/2016/12/Fall2016_Saudi.pdf.

Durrani F (2021) Saudi Arabia real estate market review–Q1 2021. https://www.knightfrank.com/publications/saudi-arabia-real-estate-market-review-q1-2021-8016.aspx

Erol I, Unal U (2015) Role of construction sector in economic growth: new evidence from Turkey. https://mpra.ub.uni-muenchen.de/id/eprint/68263

Ertugrul HM, Pirgaip B (2021) The nexus between construction investment and economic development: evidence from MENA countries. Constr Manag Econ 39(11):932–947

Soummane S, Ghersi F (2019) Macroeconomic pathways of the Saudi economy: The challenge of global mitigation action versus the opportunity of national energy reforms. Ener Pol 130:263–282. https://doi.org/10.1016/j.enpol.2019.03.062

Harada T (2015) Changing productive relations, linkage effects, and industrialization. Econ Syst Res 27(3):374–390

Hu X, Liu C (2017) Slacks-based data envelopment analysis for eco-efficiency assessment in the Australian construction industry. Constr Manag Econ 35(11–12):693–706

Kim KH (2004) Housing and the Korean economy. J Hous Econ 13(4):321–341

Kou G, OlguAkdeniz Ö, Dinçer H, Yüksel S (2021) Fintech investments in European banks: a hybrid IT2 fuzzy multidimensional decision-making approach. Financ Innovat 7:39. https://doi.org/10.1186/s40854-021-00256-y

Kou G, Yüksel S, Dinçer H (2022) Inventive problem-solving map of innovative carbon emission strategies for solar energy-based transportation investment projects. Appl Energy. https://doi.org/10.1016/j.apenergy.2022.118680

Krarti M (2020) Evaluation of occupancy-based temperature controls on energy performance of KSA residential buildings. Ener Build. https://doi.org/10.1016/j.enbuild.2020.110047

Lau MI, Pahlke A, Rutherford TR (1997) Modeling economic adjustment: A primer in dynamic general equilibrium analysis. University of Colorado. Working Paper (available at: http://debreu.colorado.edu/primer/paper.htm)

Lau MI, Pahlke A, Rutherford TF (2002) Approximating infinite-horizon models in a complementarity format: a primer in dynamic general equilibrium analysis. J Econ Dyn Control 26:577–609

Li T, Kou G, Peng Y, Yu PS (2022) An integrated cluster detection, optimization, and interpretation approach for financial data. IEEE Trans Cybern 52(12):13848–13861. https://doi.org/10.1109/TCYB.2021.3109066

Lopes J, Nunes A, Balsa C (2011) The long-run relationship between the construction sector and the national economy in Cape Verde. Int J Strateg Prop Manag 15(1):48–59

MEFIC Capital monthly report 2019 (2019) Review of economic developments till end of December 2018 Monthly Macroeconomic Review-Saudi Arabia. www.mefic.com.sa.

Okunev J, Wilson P, Zurbruegg R. The causal relationship between real estate and stock markets. J Real Estate Fin Econ 2000:21:251-261

Paltsev S (2004) Moving from static to dynamic general equilibrium economic models. MIT Joint Program on the Science and Policy of Global Change, Technical Note No. 4

Pfnür A, Wagner B (2020) Transformation of the real estate and construction industry: empirical findings from Germany. J Bus Econ 90(7):975–1019. https://doi.org/10.1007/s11573-020-00972-4

Popescu AM, Cişmaşu ID (2013) Real estate market evolution trends in the context of the current economic crisis, integral part of the ecolonomic crisis. Theoret Appl Econ, vol XX

Pretaroli R, Severini F, Socci C (2018) Green and blue dividends and environmental tax reform: dynamic CGE model. In: Perali F, Scandizzo PL (eds) The new generation for computable general equilibrium models. Modeling the Economy. Springer International Publishing, pp 249–277

SAMA (2021) 57th Saudi Central Bank Annual Report 2021. https://www.sama.gov.sa/en-US/EconomicReports/AnnualReport/ANNUAL_Report_57th_2021.pdf

Sim S, Chang B-K (2006) Stock and real estate markets in Korea: wealth of credit-price effect. Undefined

Song Y, Liu C, Langston C (2006) A linkage analysis of the real estate sector using the hypothetical extraction method. J Appl Input-output Anal 11(12):25–47

Socci C, Ahmed I, Alfify MH, Deriu S, Ciaschini C, Sheikh RA (2020) COVID-19 and a trade-off between health and economics: an extended inoperability model for Italy. Kybernetes. https://doi.org/10.1108/K-03-2021-0222

Taylor L (1990) Structuralist CGE models. In: Taylor L (ed) Socially relevant policy analysis: structuralist computable general equilibrium models for the developing world. MIT Press, Cambridge, pp 1–70

Theurillat T, Crevoisier O (2014) Sustainability and the anchoring of capital: negotiations surrounding two major urban projects in Switzerland. Reg Stud 48(3):501–515

Theurillat T, Corpataux J, Crevoisier O (2010) Property sector financialization: the case of swiss pension funds (1992–2005). Eur Plan Stud 18(2):189–212. https://doi.org/10.1080/09654310903491507

Tse RYC, Ganesan S (1997) Causal relationship between construction flows and GDP: evidence from Hong Kong. Constr Manag Econ 15(4):371–376

Zhang H, Kou G, Peng Y (2019) Soft consensus cost models for group decision making and economic interpretations. Eur J Oper Res 277(3):964–980. https://doi.org/10.1016/j.ejor.2019.03.009

Zhu R, Hu X, Liu C (2020) Structural analysis of inter-industrial linkages: an application to the Australian construction industry. Constr Manag Econ. https://doi.org/10.1080/01446193.2020.1785627

Acknowledgements

Not Applicable.

Funding

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Author information

Authors and Affiliations

Contributions

Dr. Khadija conceptualized the idea and has written literature review. Dr. Irfan and Dr. Naif constructed the Social Accounting Matrix and has written methodology. Dr. Claudio and Dr. Stefano made analysis, and Dr. Ian has written results and discussion.

Corresponding author

Ethics declarations

Competing interests

Authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix A

Appendix A

A.1: Production by commodity

On the supply side, production is modelled through a nested production function by stages of aggregation, according to the scheme shown in Fig. 1. The aggregation also takes into account the presence of taxes on output that influence the price of the goods. The first stage aggregation is shown in Eq. 6

where \(P_{it}\) represents the price of goods, \(P_{dom,it}\) are prices of domestic goods, \(Pm_{it}\) are prices of imports from the rest of the world, \(\delta_{i}^{dom}\) represents the share of domestic goods in the total production by type of product and \(\sigma_{{Q_{dom} }}\) represents the elasticity of substitution between domestic and imported goods. \(Tax_{it}^{out}\) represents the level of taxes on output.

A.2: Production by activity

The second stage models the domestic production. To this end, it is necessary to consider the relationship between goods and industries. In fact, different types of industries can produce several type of goods and therefore the production can be seen from two different perspectives. Considering that for each industry the total value of production is equal to the value of primary factors used in the production process, the domestic production is obtained through the combination between intermediates goods and value added following a Leontief function in Eq. 7.

where \(Pbi_{jt}\) represents prices of intermediate goods, \(Pva_{jt}\) represents prices of value added, \(\delta_{ij}^{D}\) represents the share of intermediate activity in total production and \(\sigma_{a}\) is the elasticity of substitution between intermediate goods and value added. \(Tax_{jt}^{act}\) represents the level of taxes on activities.

A.3: Intermediate consumption of commodities

Value added and intermediate goods are modelled in the third nesting stage. The formation of the intermediate goods aggregate is obtained through the combination of individual types of intermediate goods

where \({P}_{jt}\) represents average price on goods market from the market clearing condition, \({\delta }_{ij}\) represents share of the cost by intermediate goods in the total cost and \({\sigma }_{BI}\) is the elasticity of substitution between intermediate goods.

A.4: Value added

Finally, the value added is obtained through the combination of the primary factors, labour and capital, and their price is formed according to the balance between supply and demand using an elasticity of substitution between capital and labour equal to 0.63 for KSA (see Soummane and Ghersi 2019). The Value Added formation also includes taxes on activities

where \({PL}_{t}\) is the price of labour and \({rk}_{t}\) is the return on capital, \({\delta }_{j}^{v}\) represents the share of labour in the total of primary factors and \({\sigma }_{v}\) is elasticity of substitution between labour and capital.

A.5: Households Consumptions

Household consumption derives from the maximisation of the intertemporal utility function, which establishes the level of consumption and savings in each period:

where \(U^{hh}\) is the intertemporal utility of households, \(C_{t}^{hh}\) is the total consumption of households in a given time, \(\rho\) is the exogenous parameter of intertemporal preference and where \(- \infty \le \rho \le 1\). To the \(\rho\) parameter is related the elasticity of substitution \(\sigma\) where \(\sigma = \left[ {1/\left( {1 - \rho } \right)} \right]\).the aggregate consumption by institutional sector is obtained as:

where \(cons_{it}^{hh}\) represents the level of consumption of households by commodity in a given time.

Then, the formation of household consumption is based on the combination of the quantity demanded and the consumption price index. This latter is obtained as:

where \(\delta_{i}^{C}\) is the share of each good consumption on the total consumption and \(\sigma_{C}\) is the elasticity of substitution between goods in the consumption aggregate. The total consumption is thus a function of the consumption price index and consumer utility, depending on consumption and savings. Thus, the demand for aggregate consumption by Institutional Sector is represented as follows:

The constraint is represented by present and future disposable income.

A.6: Public consumptions

The Public consumption expenditure is considered exogenous and represents an element of rigidity of the model. In fact, it is assumed that public expenditure does not vary endogenously because the government can finance expenditure from the deficit, and consequently, government choices are not linked to the utility function maximisation

where \(def_{t}^{g}\) is the government saving/indebtedness, and \(G_{t}^{g}\) is the total public expenditure for each public Institutional Sector, that is

where \(pe_{it}^{g}\) is the public expenditure by public Institutional Sector and by goods.

A.7: Corporations

Financial and non-financial corporations shift their disposable income to savings, being consumption equal to zero

A.8: Investments

The final demand for investment is generated through the combination of the goods demanded for investment according to the breakdown in the SAM, using a CES function:

where \({\delta }_{i}^{I}\) is the investment share of each goods in the total gross investment in the benchmark, and \({\sigma }_{I}\) is the elasticity of substitution between investment goods. Then, demand of each investment good is obtained as:

A.9: Exports

The demand of goods for export is a function of a number of exogenous parameters, namely the income of the Rest of the World, the nominal exchange rate, the level of foreign prices, and the rate of foreign inflation; it also depends on national prices, which, on the contrary, are formed endogenously

where \({\delta }_{i}^{E}\) is the export share of each goods in the total export in the benchmark, \({\sigma }_{E}\) is the elasticity of substitution between export goods, \({pmw}_{t}\) is the price of foreign goods, \(\pi\) is the level of foreign inflation and \({exr}_{t}\) is the nominal exchange rate.

A.10: Disposable income

With regard to the composition of income by Institutional Sector, in the first stage of income allocation, they receive income from primary factors (compensation of employees and gross operating surplus) according to their property share. From the formation of primary income, it is possible to move on to the disposable income by adding the net transfers from/to other Institutional Sectors minus taxes on income. The disposable income for private Institutional Sectors in each period is calculated as follows

where the income from primary factors in each period \(YF_{t}^{is} = L_{t}^{is} pl_{t} + K_{t}^{is} rk_{t}\), is net of income taxes and transfers to other Institutional Sectors, and adds transfers from other Institutional Sectors (\(tr_{tras}^{is} YF_{t}^{is}\)) as well as transfers from government (\(Tr_{t}^{g}\)) and from the rest of the world (\(Tr_{t}^{row}\)). Private Institutional Sectors’ gross disposable income at present value derives from the actualisation of disposable income in each period plus the stock of capital accumulated during the time horizon of the model, as follows:

Transfers from the Public Administration and the Rest of the World are considered exogenous, and therefore not depending on disposable income.

A.11: Closure rules

The closure rule of the model is generated by market balances, both of goods and of primary factors, through price adjustments as follows:

where \(Q_{it}\) is the total production by product in each period, \(bi_{ijt}\) are the intermediate goods, \(c_{it}^{hh}\) are households consumption, \(pe_{it}^{g}\) is the public expenditure, \(I_{it}\) are the investments, \(E_{it}^{ }\) are the exports to the Rest of the world.

Gross investment equals gross savings:

A ‘special treatment’ of capital in the last period of the model is needed, to approximate infinite horizon with model’s finite periods, following Lau et al. (1997). Capital level of terminal period is a variable, with endogenous capital accumulation. This allows to avoid that in the last period all capital would be consumed, and nothing would be invested. In this model, investment in the terminal period is constrained to grow at the same rate as saving

This has the advantage of imposing a balanced growth in the terminal period, without requiring that the model achieve the steady-state growth.

A.12: Dynamics of the model

Dynamism is governed through the condition of capital accumulation, that is the total value of the capital stock in each period is obtained from the sum of the capital stock and investments at the previous time.

where \(\partial\) represents the capital depreciation rate, and this rule guarantees the model dynamism.

The model follows the Ramsey analysis of optimal economic growth under certainty (Lau et al. 2002); economic growth is also expected to be in a steady state. In particular, the growth rate is fixed at 2.4% that is consistent with the statistical data of KSA. Moreover, the model is characterised by a finite time horizon (Paltsev 2004), set in 5 years for this work, and therefore it is considered a closing condition that allows the model to converge to a stable equilibrium in the last period, establishing the constraint that the level of growth of aggregate investment must equal the growth rate of savings in the last period.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Ahmed, I., Mehrez, K., Socci, C. et al. Disaggregated effect of construction investments on the Saudi economy: a dynamic computable general equilibrium model of Saudi Arabia. Financ Innov 10, 28 (2024). https://doi.org/10.1186/s40854-023-00530-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s40854-023-00530-1