Abstract

This paper examines how the difference in institutional environments constitutes differential IPO underpricing across countries. Using the Heritage Foundation’s Index of Economic Freedom (IEF) as a proxy for the heterogeneous institutional environment, and a sample of 3728 IPOs from 22 countries and regions over the period 1993–2014, we find that countries with higher economic freedom have significantly less serious IPO underpricing problems. Moreover, we find that among the 10 economic freedom factors covered by theIEF, financial freedom related factors play a more important role in reducing the IPO underpricing problem. Finally, consistent with the market sentiment hypothesis, we find strong evidence that pre-IPO market sentiment influences IPO first-day returns, and that the IPO underpricing problem is less severe when the market is bearish.

Similar content being viewed by others

Introduction

The IPO underpricing phenomenon has been a persistent and pervasive worldwide phenomenon (Loughran et al., 1994; Krigman et al., 1999; Ritter and Welch, 2002; Chambers and Dimson, 2009). Moreover, the level of IPO underpricing variesacross countries, and is generally more pronounced in emerging markets (Loughran et al., 1994).Footnote 1Why does the degree of IPO underpricing vary so dramatically across different countries, especially between developed and developing countries? This important and interesting issue has not received much attention in the literature, and it deserves a systematic investigation.

Many explanations for the underpricing phenomenon have been provided but the focus is within markets. To explain underpricing across markets, new perspectives are needed and one of these is the difference in institutional environments, the focus of our present study.

The institutional environment is generally defined as a combination of binding regulations, contractual mechanisms, the economic environment (e.g., Miller and Holmes, 2009, 2010), legal rights and enforcement mechanisms (La Porta et al., 1998, 2006). The focus of this study rests not on IPO underpricing per se, but rather on the cross-sectional difference in the extent of IPO underpricing in different countries. We propose that differences in institutional environments are important driving factors.

Existing studiesshow that a favorable institutional environment, with a well-developed financial market, legal system and degree of openness has a significant impact on economic development (Lau and Lam 2002; Henry, 2007), and sets the governance environment fora firm affecting its performance (LLSV, 2002; Shleifer and Wolfenzon, 2002). The standard international asset pricing model (ICAPM) and cross-listing literature specifically suggest that stock market liberalization could reduce the liberalizing country’s equity capital costs (Stapleton and Subrahmanyan, 1977; Errunza and Losq, 1989; Stulz, 1999; Henry, 2000a, 2000b). LLSV (1997, 1998) and Djankov et al. (2006) find that country-level investor protection and corporate governanceare important for firms to enjoy higher valuations and a lower cost of equity capital. More explicitly, Loughran et al. (1994) argue that lifting the binding economic contract and IPO mechanism helps to foster transparency, lower information asymmetry, and thus, alleviate IPO underpricing, although they do not formally test this assertion. Jones et al., 1999argue that governments that allow less economic freedom should find it necessary to offer greater underpricing to signal SIP commitment. We postulate that a better institutional environment helps to reduce the IPO underpricing problem after controlling for firm-specific factors such as information asymmetry and macro factors such as market sentiment and economic development.

Unlike some previous studies that focus only on a couple of particular institutional factors, such as legal liability, price stabilization or investor protection (Hopp and Dreher, 2011; Banerjee et al., 2011; Boulton et al., 2011), we use indices of economic freedom that measure the overall institutional environment to examine its relation to IPO underpricing. As such, our analysis looks at the impact of the general institutional environment rather than specific environmental features on IPO underpricing.

Economic freedom has been widely observed to be important for economic efficiency (Smith, 1776). In theory, a free economy is defined as the so-called “Arrow-Debreu world,” where economy efficiency is guaranteed in general equilibrium (Arrow and Debreu, 1954; McKenzie, 1959; Hart, 1980). In empirical studies, economic freedom has been investigated in other macroeconomic areas, especially those on economic growth (Gwartney et al., 1999; Haan and Sturm, 2000; Heckelman, 2000; Wu and Davis, 1999), income equality (Berggren, 1999; Scully, 2002) and employment (Feldmann, 2007, 2008).

The theoretical link between economic freedom and IPO underpricing, as implied by general equilibrium theory, is that an economically free country provides a free market for IPO firms and hence improves the economic efficiency of resource allocation. More specifically, a free market makes the burden of bureaucracy and corruption smaller and provides a steady and reliable monetary environment, a free and open investment environment, a transparent and open financial system with more protection and less likelihood of government confiscation. As a whole, a free economy could help reduce the severity of asymmetric information, agency problems and transaction costs for IPO firms, which in turn reduce IPO underpricing (Rock, 1986; Ritter, 1987; Allen and Faulhaber, 1989; Brennan and Franks, 1997; Mok and Hui, 1998; Aggarwal and Conroy, 2000; Ljungqvist, 2007; Boulton et al., 2011; Ghoul et al., 2011; Boulton et al., 2014.

On the other hand, economic freedom is perceived as a comprehensive proxy for institutional environment that is strongly associated with economic liberalization and property ownership protection (e.g., Henry, 2007). Miller and Holmes (2009, 2010) illustrate at least four channels through which a free economy might affect the equity costs in financial markets. First, economic freedom lowers the external regulatory burden and enables investors to make long-term plans more easily, thus lowering the uncertainty of the investment. Second, it encourages openness, brings more foreign investors to the domestic markets and facilitates risk-sharing activities. Third, by securing property protection and punishing corruption, a free economy gives investors the willingness and confidence to undertake more risks. Fourth, it encourages banking and financialintermediaries to provide information services independently, which helps lower the information asymmetry and identify the pricing of capital. In short, an economy’s economic freedom reflects how efficiently the market allocates economic resources and achieves the price of capital.

We follow previous studies (Claessens and Laeven, 2003; Santos-Paulino and Thirlwall, 2004; Henry, 2007; Miller and Holmes, 2009; Qi et al., 2010) and use the Heritage Foundation’s Index of Economic Freedom (hereafter the IEF) as the measure of economic freedom for the sample countries. The IEF has 10 sub-indexes that measure different aspects of a country’s economic freedom level. The aggregation of the 10 sub-indexes gives a comprehensive economic freedom index value. Specifically, we predict that the overall value of the index is negatively associated with the initial returns across countries.

Using a sample of 3728 IPO observations from 22countries between July 1993 and December 2014, we find a significant negative relation between economic freedom and IPO underpricing after controlling for other commonly used firm-specific and macro control variables. Moreover, we find that among the IEF’s 10 sub-indexes, financial freedomplays an influential role in explaining cross-country underpricing. That is, we provide direct evidence that lifting redundant financial regulatory restrictions lowers the underpricing.

Because U.S. and Chinese IPOs account for a great percentage of the total number of IPOs in the sample, we also conduct robustness tests on this potential data bias problem. The results support the main conclusion.

The remainder of this paper is organized as follows. Section 2 discusses the data, sample and model. Section 3 presents the empirical results. Section 4 provides the robustness tests and Section 5 concludes the paper.

Data, sample and the model

Data and the sample

Our sample period isfrom July 1993 to December2014.All relevant IPO data come from the SDC Platinum Global New Issue Database. Other data such as GDP per capita, global market returns and firm-specific information come fromBloomberg, DataStream, and WIND. After excluding private placements, non-original IPOs, and IPOs from countries that have less than 10 IPOs during the sample period, we obtain 14,343 IPOs from 63 economies. We further delete IPOs from nations that are missing analyst following, stock price synchronicity, home-country bias and democracy data, and obtain 10,029 IPOs from 24 countries. Finally, the IPO firm should have firm-level data such as IPO proceeds and underwriters. The final sample consists of 3728 IPOs from 22 economies.Table 1 provides the chronological distribution of IPO numbers for the sample countries.

We use the Heritage Foundation’s Index of Economic Freedom (IEF) to measure a country’s level of economic freedom. The IEF has been extensively used in studies of the relationship between economic freedom and capital market development (Lau and Lam, 2002; Miller and Holmes, 2009, 2010), trade policies and economic growth (Santos-Paulino and Thirlwall, 2004), corruption levels and capital costs (Claessens and Laeven, 2003; Qi et al., 2010 and capital market liberalization and economic growth (Henry, 2007). Jones et al. (1999) also apply the overall IEF rankings to measure governmental intervention levels in their cross-country SIP study.

The IEF has 10 sub-indexes, each of which measures a specific aspect of economic freedom: Financial freedom (Fin), Investment freedom (Ivst), Business freedom (Busi), Property rights (PPR), Freedom from corruption (Crup), Government expenditure size (FreeGov), Trade freedom (FreeTrd), Monetary freedom (Mny), Fiscal freedom (Fiscal) and Labor freedom (Labor). Each of the 10 freedom sub-indexes is graded using a scale from zero to 100, where a value of 100 represents the maximum level of freedom and signifies an economic environment or set of policies that is most conducive to economic freedom.The equally weighted average of the 10 sub-index scores gives an overall economic freedom score (TotV) for each economy. Countries are also classified into five groups by ranks determined using the overall IEF scores. Countries with higher overall scores or higher ranks are considered to have a higher level of overall economic freedom. In this study, we use both the overall score (TotV) and rank (Rank) to measure the economic freedom of the sample economies. A higher total score (TotV) or rank (Rank) for IEF implies a higher level of overall economic freedom.

Descriptive statistics

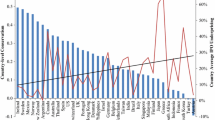

Table 2 reports the basic statistics for the IPO initial returns (IR) and the IEF index scores (IEF) for the sample countries over the sample period.Footnote 2

There are a few things worth pointing out. First, IPO underpricing exists in almost all the sample economies, and that the underpricing level varies significantly across countries. Consistent with previous studies (e.g., Loughran et al., 1994, Boulton et al., 2011, the sample IPO firms from less developed countries or emerging markets tend to have much higher first-day returns than those from developed markets. For example, the average initial returns in Indonesia, Poland and Thailand are 41.27, 33.95 and 53.17%, respectively, while the average initial returns in the U.S. and the U.K. are 18.65 and 10.76%, respectively.

Second, the magnitude of economic freedom is significantly different across countries. As expected, developed countries tend to have a higher level of economic freedom than developing countries. For example, the IEF index scores of developing countries such as China (52.78), India (54.11), Indonesia (52.95) and Philippines (56.24) are far below the overall IEF score average of 68.57; whereas the scores of developed countries such as the.

U.K. (78.35) and the U.S. (76.81) are far above the average.

More importantly, Table 2 shows that countries with higher initial returns (more IPO underpricing) tend to have lower IFE scores, and these countries tend to be developing countries. On the other hand, countries with higher IFE scores, which tend to be developed countries, tend to have lower initial returns (smaller IPO underpricing). This provides some initial evidence that economic development status may have a significant impact on underpricing levels.

To look deeper into the relationship between the total IEF score and the IPO underpricing level, we investigate the relationship between the IPO underpricing level and each of the 10 sub-scores of IEF. Although we expect that the total IEF score (TotV) is negatively associated with the underpricing level, each of the 10 sub-indexes might have different impacts on the initial return. Specifically, Miller and Holmes (2009) argue that financial freedom (Fin) can alleviate information asymmetry and help allocate resources to satisfy demand. Less information asymmetry leads to less risk premium. This predicts that a higher Fin would be associated with a lower IR. Investment freedom (Ivst) provides a free and open investment environment, which allows various financial instruments to be deployed to deal with a variety of investment issues such as risk sharing, asymmetric information and agency problems (Neher, 1999; Cornelli and Yosha, 2003; Wang and Zhou, 2004). This in turn leads to less severe IPO underpricing problems. For property rights (PPR), LLSV (2002) argue that investors accept higher valuations for firms in countries with better protection of minority shareholders, which also implies a negative relationship between PPR and IR.

In contrast, less trade freedom (FreeTrd), fiscal freedom (Fiscal), government freedom (FreeGov), and freedom from corruption (Crup) may reflect more government protection that may benefit the IPO firms and reduce the severity of information asymmetry and agency problems (Wang and Wang, 2012). However, what exactly the role of government plays in IPO underpricing has no consensus in the literature. Jones et al., 1999find that though governments generally tend to underprice their shares in the SIPs, governments with a larger expenditure size compared to their GDP level (i.e., a lower FreeGovscore) and stronger short-term revenue motivation would underprice less.

Therefore, there might be a positive association between IR and some of the economic freedom factors that reflect a transparent and open economic environment where issuers would be reluctant to underprice their shares, or consider such underpricing as unnecessary. On the other hand, factors reflecting less government protection may lead to more IPO underpricing.

Table 3 summarizes the correlation between the economic freedom variables and IR. The main testing variable TotV is significantly and negatively related to the IR. This confirms the trend revealed in the descriptive statistics in Table 2 that the overall IPO initial return is negatively associated with the degree of economic freedom. On the other hand, while the correlation between IR and the 10 IFE sub-indexes is significantly negative for six sub-indexes (Fin, PPR, Busi, Mny, Crup and Ivst), and it is also significantly positive for four sub-indexes (FreeTrd, Fiscal, FreeGovand Labor). Note also that among the 10 IFE sub-scores, the variables that reflect financial market freedom (Fin, Ivst) have the most negative correlations with IR.

It is clear that those factors that have significantly negative impacts on IPO underpricing ensure more transparent financial markets and provide more investor protection.

Testing models

To formally investigate how economic freedom contributes to the observed difference in IPO underpricing across economies, we run the following panel data regression:

where IR i, t is the average IPO initial returns of Country iin Yeart.Footnote 3 Our key testing variable, IEF is the economic freedom variable, proxied by either the total score (TotV) or the rank (Rank) of the index of economic freedomof Country iin Year t. We expect that the overall economic freedom level is negatively associated with the IPO initial returns.

We then put in two sets of control variables to control for general and IPO-specific factors. For the general factors, we first look atGDP, which is the GDP per capita of the country.We use it to control for the potential influence of the economic development status on initial returns. Vassalou (2003) argues that GDP growth plays an important role in explaining the cross-sectional equity returns. Ibbotson and Chen (2003) report that the long-term equity returns are in line with the growth of per capita GDP. Hopp and Dreher (2011) find that GDP is a significant variable in cross-country underpricing research, though such significance is sensitive to other included institutional variables.

IPO performance can be quite different across different years, due to different market conditions and investor sentiments (Ritter, 1984; Ibbotson et al., 1994; Lowry and Schwert, 2002; Lowry et al., 2010). Cornelli et al. (2006) find that the pre-IPO market sentiment is strongly and positively associated with first-day returns. Loughran and Ritter’s (2002) prospect theoryfurther predicts that such an association is asymmetric, although they do not formally test this assumption. Therefore, we include two global market sentiment dummy variables in our regression model.Bear and Bull are the pre-IPO market sentiment dummy variables, calculated based on the three-month holding period returns (R ACWI ) on the Morgan Stanley Country Index-All Country World Index (MSCI-ACWI index) prior to the IPO trading day.Footnote 4 Specifically,Bear = 1 if R ACWI ≤ − 10%; and 0 otherwise;andBull = 1 if R ACWI ≥ 10%; and 0 otherwise.Footnote 5

Ritter (1984) find that the average initial IPO return is higher in “hot market” periods compared to “cold market” periods. This finding is confirmed by later studies (Ibbotson et al., 1994; Lowry and Schwert, 2002; Dorn, 2009; Lowry et al., 2010. Recent studies further suggest that the underpricing magnitude is asymmetrically associated with market sentiments.Footnote 6 We expect that the regression coefficients of Bearand Bullwill benegative and positive, respectively.

Banerjee et al. (2011) find that IPO underpricing is higher in countries with higher levels of information asymmetry and lower home-country bias of the domestic investors. To control for the potential impacts of country-level information asymmetry, we put into the regressionAF(analyst following), SPS(stock price synchronicity) and HCB(home-country bias). AF is the median value of firm-year analyst following estimates in one country. SPS is a measure of the percentage of stocks moving in step, estimated by Morck et al. (2000). HCB is the ratio of home mutual fund investment weight in home stocks over the stock market capitalization weight in the world market estimated by Lau et al., 2010

Democ (Democracy) is an index defined by Marshall and Jaggers (2000). Higher democracy scores indicate a higher degree of institutional democracy. La Porta et al. (2006) argue that countries with a higher democracy index tend to be more responsive to minority shareholders. Boulton et al., 2010find that underpricing is higher in countries with higher democracy scores. Thus, we include the democracy index as an additional control variable.

Furthermore, Boulton et al., 2011find that in countries with higher IPO underpricing, the earnings information of their firms tend to be oflower quality. We therefore include EM (earnings management) as another control variable. Following their approach, we constructEM as the average countryiranking across the following four earnings management measures: EM 1,EM 2, EM 3 and EM 4. EM 1is the median ratio in countryiof the firm-level standard deviations of operating earnings over the cash flow from operations (both scaled bylagged total assets), multiplied by −1.EM 2is the cross-sectional correlation in country ibetween the change in accruals and change in cash flows from operations (both scaled bylagged total assets), multiplied by −1. EM 3is the median ratio in country iof the absolute value of accruals over the absolute value of cash flow from operations. EM 4is the ratioin countryiof the number of firms reporting small profits over the sum of the number of firms reporting small losses and small profits. A small profit (loss) is defined as a value ofnet earnings scaled by lagged total assets in the range[0, 0.01] ([−0.01, 0]).Footnote 7

After controlling for general factors, we then look into IPO-specific factors. Traditional single-country IPO studies suggest that underpricing can be attributed to several firm-specific financial factors (Baron, 1982; Beatty and Ritter, 1986; How and Howe, 2001; Michaely and Shaw, 1994; Ljungqvist, 2007). Specifically, we include four firm-specific IPO control variables: the IPO’s offering size (Proceeds), the demand for IPO (Oversold), an underwriter reputation dummy variable (Uwrt), and the prior-IPO firm performance proxied by the return of equity (ROE) 1 year before the IPO date. In previous single country IPO studies, these variables are the most popular control variables and are considered to be related with ex ante uncertainty in the information asymmetry literature (Ritter, 1984; Michaely and Shaw, 1994; Arugaslan et al., 2004; Loughran and Ritter, 2004; Ljungqvist, 2007).

Lastly, we control for time-series and industrial (or country) fixed effects. FEare the industry (Ind) and year (Year) fixed effect control variables. We use Petersen’s (2009) two-way clustering approach to estimate standard errors.

Empirical results

IPO first-day returns and economic freedom

In the regression model (1), the primary variable of interest is the economic freedom variable IEF. If a higher degree of economic freedom helps to lower the IPO underpricing level, we expect the estimated coefficienta1to be significantly negative; and that is precisely what we observein the regression results presented inTable 4.

Table 4 shows that the estimated coefficient of TotVand Rank are both significantly negative at the 1% level. Specifically, the significantly negative coefficient of TotV (−0.990) implies that one score improvement in a country’s IEF value is associated with a 0.990% reduction in that country’s IPO underpricing level. Similarly, the significantly negative coefficient of Rank (−10.445) indicates that for every one rank improvement in a sample country, the IPO underpricing of the firms in that country will be reduced by 10.445%. These results provide strong and direct evidence to our main hypothesis that overall economic freedom is negatively associated with IPO underpricing across countries.

Consistent with the market sentiment hypothesis, we find that initial returns are negatively associated with the bear market dummy variable and positively associated with the bull market dummy variable. These results lend support to the “hot market” arguments and the “prospect theory”: issuers will bargain harder over the offer price when the market is bad (Ritter, 1984; Loughran and Ritter, 2002). Moreover, similar to the finding of Cornelli et al., 2006and Dorn (2009) on the pre-IPO market, we find that the absolute value of the coefficient for Bear (−16.628) is more than double of that for Bull (7.918), showing an asymmetrical relationship between market sentiment and IPO initial returns.

The coefficient of the control variable GDP is positive and significant for the two regressions in Table 4. The positive coefficient of GDP suggests that average initial returns tend to be higher in wealthier economies.

The estimates of other control variablesare also broadly consistent with the expectations of the literature.The coefficients of AF (analyst followings) and SPS (stock price synchronicity) are positive and negative, respectively, but none of them are significant. Banerjee et al., 2011argue that in markets with serious home bias, domestic IPO issuers do not have to worry about outside competitors or lower their price too much to attract more investors, because domestic investors constitute a strong support. Consistent with Banerjee et al. (2011) home-bias argument, Table 4 shows that the estimated coefficients of HBare negative (−3.152 and −3.306). However, these two estimates are only marginally significant.

In contrast with the findings of Boulton et al. (2010), the estimate of Democ is negative and significant. This suggests that counties with a higher degree of democracy are associated with lower levels of IPO underpricing. In addition, we fail to find any significant effects for earnings quality.

For the IPO-specific control variables, IPO size (Proceeds)is often used as a proxy for large firms that are generally believed to have less severe information asymmetry problems and thus less underpricing problems (Ritter, 1984; Arugaslan et al., 2004; Boulton et al., 2011. Consistent with these studies, the coefficients of Proceedsare negative and significant at the 1% level in both regressions.

Similarly, Oversold and ROEentersignificantly negative into the regression, which is expected. However, the coefficients of ROE are insignificant in both regression models. Finally, the estimates of Uwrt (underwriter reputation) are positive but insignificant.

In summary, Table 4 provides strong evidence that overall economic freedom helps to reduce underpricing across countries,because a free economy is associated with a low external regulatory burden, enables investors to make long-term plans more easily, and lowers the uncertainty of investments (Miller and Holmes, 2009). In addition, by securing property protection and encouraging openness, a free economy provides the confidence to undertake risks and facilitate risk-sharing activities. In other words, economic liberalization has significant effects on real variables, such as economic growth, investments, and cost of capital (Henry, 2007).

Relationship between IPO initial returns and the sub-indexes of economic freedom

In addition to testing the overall relation between IR and the institutional environment, we also test the relation between IR and each of the 10 IEF sub-indexes. Columns 1–10 of Table 5 report the estimates for each of the 10 univariate regressions, respectively.

The results in Table 5show that different aspects of economic freedom have different impacts on initial returns. In the 10 univariate regressions, five sub-indexes (PPR, Crup, Busi, Ivst and Fin) show significantly negative coefficients; whileFreeGovshows a significantly positive coefficient.

The significantly negative coefficient for Fin indicates that an economy with more financial market freedom would suffer less from IPO underpricing. The role of financial freedom is generally accepted by previous empirical studies on financial deregulation (Errunza and Miller, 2000; Henry, 2007). Miller and Holmes (2009) argue that financial freedom is essential in allocating capital resources to their highest values and uses and encourages banking and financial intermediaries to provide information services independently with the goal of achieving the suitable pricing of capital and alleviating information asymmetry at the country level. Here, we provide new evidence that financial freedom also helps to alleviate the IPO underpricing problem.

Note that the only significantly positive sub-index (FreeGov) is a government related variable. As we discussed in Section 2, there are no generally accepted theories on the exact impact of the different government policies on economies in general, and IPO underpricing in particular, and the empirical evidence is mixed across different countries. Miller and Holmes (2009, 2010) argue that government spending is inefficient, which implies that a low level of government spending represents a high level of economic freedom. Jones et al. (1999) argue that different types of governments might have different economic and political ends, and that each would employ different IPO strategies, which would obscure the relation between initial returns and government variables. For example, they find that populist governments underprice less in SIP when they need more revenue for expenditure.

In summary, the results of Table 5 suggest that although IPO initial returns are negatively associated with overall economic freedom levels, the relation between IPO initial returns and each of the 10 individual sub-indexes is complicated.

Robustness tests

Robustness test without U.S. and Chinese IPOs

For historical reasons, the SDC database has more IPO data on some specific countries, such as the U.S. and China. In fact, the sum of US and Chinese IPOs in our sample is2,406, which almost coverstwo-third of our total sample, as shown in Table 1. To alleviate the impact of this possible data-selection bias, our first robustness test is conducted by estimating the model without U.S. and Chinese IPOs.

The results in Table 6 demonstrate that the main results still hold even without the U.S. and Chinese IPOsample. Specifically, the estimated coefficient of a1forTotV(Rank) is−1.035(−9.054)which is statistically significant at the 5%level.The estimates of the market sentiment variables, firm-specific control variables and the home-bias variable are also highly consistent with the results reported in Tables 4. Notice that the adjusted R 2is 0.147, which is actually higher than the adjusted R 2 of 0.122 in Table 4. Hence,a more balanced sample distribution after deleting the US and Chinese sample helps to better reflect the effect of cross-country economic freedom variations on the IPO initial returns.

To confirm the relation between IR and each of the 10 IEF sub-indexes, we also run the 10 univariate regressions by deleting the U.S. and Chinese sample.

Columns 1–10 of Table 7 report the estimates for each of the 10 regressions, respectively. The results in Table 7 are very consistent with that in Table 5, indicating that the relation between IR and each of the 10 IEF sub-indexes still holds after deleting the U.S. and Chinese IPOs. Specifically, Table 7 shows that the estimated coefficient of five sub-indexes (PPR, Crup and Ivst) are significant and negative.

Robustness test by including law origin

A number of previous studies suggest that the legal environment is an important institutional factor in influencing investments, and that relative to common law countries,civil law countries seem to suffer from higher cost of equity (LLSV, 1998, 2006; Eleswarapu and Venkataraman, 2006). In contrast with these traditional findings, Coffee (2001) finds that civil law countries also show dispersed ownership, and Sarkar (2011) observes that some civil law countries provide better minority shareholder protection than common law countries. Some recent studies even challenge the traditional methodology of using law origins as a basis for analysis, suggesting that most legal systems are hybrids in reality (Siems, 2007). Empirically, whether common law or civic law countries have lower levels of IPO underpricing, the empirical evidence is mixed (Boulton et al., 2010, 2012b).

Although the main task of this paper is to study the relation between IPO initial return and economic freedom, and notably that the economic freedom index used in this study has already reflected some aspects of the legal environment, such as property rights (PPR) and anti-corruption (Crup). To test whether the legal system has any impact on our main results, we conduct a robustness test that includes a common law dummy variable (LawSys).

The regression results in Table 8 are very consistent with that in Table 4, indicating that the main results are not sensitive to the inclusion of the legal system variable.LawSysis insignificantly and negatively associated with IR. As mentioned above, the economic freedom index may also be highly correlated with the legal condition of an economy.There is no consensus in the literature as to whether civic law or common law provides better investor protection either. Moreover, while the IEF is annually updated, LawSys has only 1 year of data from LLSV (1998), and this greatly limits its usage due to the critique of dynamic measurement bias.

Conclusion

In this paper we investigate whether economic freedom plays a role in explaining the IPO underpricing phenomenon across different countries. Unlike some previous studies that focus only on a couple of particular institutional factors, our analysis looks at the impact of the general institutional environment rather than specific environmental features on IPO underpricing.

Using a large sample of IPO initial returns across 22 countries over a 21-year period from July 1993 to December 2014, we find that firms in economies with higher levels of economic freedom have less severe underpricing problems.

In addition, to examine the overall relationship between the IPO initial returns and economic freedom, we investigate the relationship between the IPO initial returns and each of the ten economic freedom factors covered by the IEF. The result that financial market liberalization (Fin) is significantly and negatively associated with IPO underpricing is consistent with the ICAPM’s prediction that stock market liberation may reduce the liberalizing country’s costs of equity capital (Stapleton and Subrahmanyan, 1977; Errunza and Losq, 1989; Stulz, 1999; Henry, 2000b).

Consistent with the market sentiment literature, we find that IPO initial returns are negatively associated with the bear market dummy variable and positively associated with the bull market dummy variable. Moreover, similar to the finding of Cornelli et al. (2006) and Dorn (2009) for the pre-IPO market, we find that the impact of market sentiment on IPO underpricing is much stronger for bearish markets than that for bullish markets. These results lend support to the IPO “hot issue” markets literature (Ritter, 1984) and the “prospect theory.” (Loughran and Ritter, 2002). Among other control variables, we also find that IPO size is significantly and negatively associated with IPO initial returns.

This paper contributes to the IPO literature by providing country-level evidence that heterogeneous institutional environments help to explain the cross-country IPO underpricing anomaly. Specifically, we find strong and robust evidence that IPO firms from countries with higher economic freedom, especially higher financial freedom, have significantly less serious IPO underpricing problems.

Notes

Updated IPO initial return data can be found on Jay Ritter’s website: https://site.warrington.ufl.edu/ritter/ipo-data/.

The IPO initial return (IR) is the ratio of the difference between the first-day closing price and offering price to the offering price. We winsorize the initial returns at the 1st and the 99th percentiles.

Variable definitions are listed in Appendix.

The MSCI-ACWI index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of both developed and emerging markets. As of May 27, 2010 the MSCI-ACWI consisted of 45 country indexes comprising 24 developed and 21 emerging market country indexes.

In unreported robustness tests, we also construct the sentiment measures with cutting points of –20% and 20% for a 3-month MSCI-ACWI return, and the main results still hold.

From the issuer’s perspective, Loughran and Ritter’s (2002) prospect theory explains that issuers bargain hard in a bad state of the world to improve the offer price, whereas they are pushovers in a good state, resulting in an asymmetric relationship between pre-IPO market sentiment and initial returns. Cornelli et al. (2006) provide evidence of this by using Europe’s pre-IPO (grey markets) data.

For details, please refer to Boulton et al., 2011

Abbreviations

- AF:

-

Analyst following, defined as the median value of firm-year analyst following estimates

- Busi:

-

The business freedom sub-index score of the IEF

- Crup:

-

The corruption freedom sub-index score of the IEF

- Democ:

-

Democracy index defined by Marshall and Jaggers (2000)

- EM:

-

Aggregate earnings management

- Fin:

-

The financial freedom sub-index score of the IEF

- Fiscal:

-

The value of fiscal freedom sub-index score of the IEF

- FreeGov:

-

The value of government size sub-index score of the IEF

- FreeTrd:

-

The value of trade freedom sub-index score of the IEF

- HB:

-

Home bias

- IEF:

-

Heritage Foundation’s Index of Economic Freedom

- Ind:

-

Industry dummy variables

- IR:

-

IPO initial return

- Ivst:

-

The investment freedom sub-index score of the IEF

- Labor:

-

The value of labor freedom sub-index score of the IEF

- LawSys:

-

Common law system dummy variable

- Mny:

-

The value of monetary freedom sub-index score of the IEF

- PPR:

-

The property rights freedom sub-index score of the IEF

- Rank:

-

Rank of economic freedom

- SPS:

-

Stock price synchronicity

- TotV:

-

The total value of the IEF

- Uwrt:

-

Underwriter reputation dummy variable

References

Aggarwal, R., & Conroy, P. (2000). Price discovery in initial public offerings and the role of the lead underwriter. Journal of Finance, 55, 2903–2922.

Allen, F., & Faulhaber, G. R. (1989). Signaling by underpricing the IPO market. Journal of Financial Economics, 23, 303–323.

Arrow, K., & Debreu, G. (1954). Existence of equilibrium for a competitive economy. Econometrica, 22, 265–290.

Arugaslan, O., Cook, D. O., & Kieschnick, R. (2004). Monitoring as a motivation for IPO underpricing. Journal of Finance, 59, 2403–2420.

Banerjee, S., Dai, L., & Shrestha, K. (2011). Cross-country IPOs: What explains differences in underpricing? Journal of Corporate Finance, 17, 1289–1305.

Baron, D. P. (1982). A model of the demand for investment banking advising and distribution services for new issues. Journal of Finance, 37, 955–976.

Beatty, R. P., & Ritter, J. R. (1986). Investment banking, reputation, and the underpricing of initial public offerings. Journal of Financial Economics, 15, 213–232.

Berggren, N. (1999). Economic freedom and equality: Friends or foes? Public Choice, 100, 203–223.

Boulton, T. J., Smart, S. B., & Zutter, C. J. (2010). IPO underpricing and international corporate governance. Journal of International Business Studies, 41, 206–222.

Boulton, T. J., Smart, S. B., & Zutter, C. J. (2011). Earnings quality and international IPO underpricing. Accounting Review, 86, 483–505.

Boulton, T.J., Smart, S.B., Zutter, C.J. (2014). The impact of institutional quality on initial public offerings. Journal of Economics and Business, 73, 65-96.

Brennan, M. J., & Franks, J. (1997). Underpricing, ownership and control in initial public offerings of equity securities in the UK. Journal of Financial Economics, 45, 391–413.

Chambers, D., & Dimson, E. (2009). IPO underpricing over the very long run. Journal of Finance, 64, 1407–1443.

Claessens, S., & Laeven, L. (2003). Financial development, property rights, and growth. The Journal of Finance, 58, 2401–2436.

Coffee, J. (2001). The rise of dispersed ownership: The role of law in the separation of ownership and control. Yale Law Journal, 111, 1–82.

Cornelli, F., Goldreich, D., & Ljungqvist, A. (2006). Investor sentiment and pre-IPO markets. Journal of Finance, 61, 1187–1216.

Cornelli, F., & Yosha, O. (2003). Stage financing and the role of convertible securities. Review of Economic Studies, 70, 1–32.

Djankov, S., LaPorta, R., Lopez de Silanes, F., & Shleifer, A. (2006). The law and economics of self-dealing. Journal of Financial Economics, 88, 430–465.

Dorn, D. (2009). Does sentiment drive the retail demand for IPOs? Journal of Financial and Quantitative Analysis, 44, 85–108.

Eleswarapu, V. R., & Venkataraman, K. (2006). The impact of legal and political institutions on equity trading costs: A cross-country analysis. The Review of Financial Studies, 19, 1081–1111.

Errunza, V. R., & Miller, D. P. (2000). Market segmentation and the cost of capital in international equity markets. Journal of Financial and Quantitative Analysis, 35, 577–600.

Errunza, W., & Losq, E. (1989). Capital control, international asset pricing, and investors welfare: A multi-country framework. Journal of Finance, 44, 1025–1037.

Feldmann, H. (2007). Economic freedom and unemployment around the world. Southern Economic Journal, 74, 158–176.

Feldmann, H. (2008). Business regulation and labor market performance around the world. Journal of Regulatory Economics, 33, 201–235.

Ghoul, S. E., Guedhami, O., & Pittman, J. (2011). The role of IRS monitoring in equity pricing in public firms. Contemporary Accounting Research, 28, 643–674.

Gwartney, J., Lawson, R., & Holcombe, R. (1999). Economic freedom and environment for economic growth. Journal of Institutional and Theoretical Economics, 155, 1–21.

Haan, F., & Sturm, J. (2000). On the relationship between economic freedom and economic growth. European Journal of Political Economy, 16, 215–241.

Hart, O. (1980). Perfect competition and optimal product differentiation. Journal of Economic Theory, 22, 279–312.

Heckelman, J. (2000). Economic freedom and economic growth: A short-run causal investigation. Journal of Applied Economics, 3, 71–91.

Henry, P. B. (2000a). Do stock market liberalizations cause investment booms? Journal of Financial Economics, 58, 301–334.

Henry, P. B. (2000b). Stock market liberalization, economic reform, and emerging market equity prices. Journal of Finance, 55, 529–564.

Henry, P. B. (2007). Capital account liberalization: Theory evidence and speculation. Journal of Economic Literature, 45, 887–935.

Hopp, C., & Dreher, A. (2011). Do differences in institutional and legal environments explain cross-country variations in IPO underpricing? Applied Economics, 45(04), 435–454.

How, J. C. Y., & Howe, J. S. (2001). Warrants in initial public offerings: Empirical evidence. Journal of Business, 74, 433–457.

Ibbotson, R. G., & Chen, P. (2003). Long-run stock returns participating in the real economy. Financial Analysts Journal, 59, 88–98.

Ibbotson, R. G., Sindelar, J. L., & Ritter, J. R. (1994). The market’s problems with the pricing of initial public offerings. Journal of Applied Corporate Finance, 7, 66–74.

Jones, S. L., Megginson, W. L., Nash, R. C., & Netter, J. M. (1999). Share issue privatizations as financial means to political and economic ends. Journal of Financial Economics, 53, 217–253.

Krigman, L., Shaw, W. H., & Womack, K. L. (1999). The persistence of IPO mispricing and the predictive power of flipping. Journal of Finance, 54, 1015–1036.

La Porta, R., Lopez-de-Salinas, F., Shleifer, A., & Vishny, R. (1997). Legaldeterminants of external finance. Journal of Finance, 52, 1131–1150.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (1998). Law and finance. Journal of Political Economy, 106, 1113–1155.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2002). Investor protection and corporatevaluation. Journal of Finance, 57, 1147–1170.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2006). What works in securities laws? Journal of Finance, 61, 1–32.

Lau, K. N., & Lam, P. Y. (2002). Economic freedom ranking of 161 countries in year 2000: A minimum disagreement approach. Journal of the Operational Research Society, 53, 664–671.

Lau, S. T., Ng, L., & Zhang, B. (2010). The world price of home bias. Journal of Financial Economics, 97, 191–217.

Ljungqvist, A. (2007). IPO underpricing. In B. E. Eckbo (Ed.), (2007)Handbook of empirical corporate finance SET, volume 1.Amsterdam. North-Holland: Elsevier Chapter 7.

Loughran, T., & Ritter, J. R. (2002). Why don't issuers get upset about leaving money on the table in IPOs? The Review of Financial Studies, 15, 413–443.

Loughran, T., & Ritter, J. R. (2004). Why has IPO underpricing changed over time? Financial Management, 33, 5–37.

Loughran, T., Ritter, J. R., & Rydqvist, K. (1994). Initial public offerings: International insights. Pacific-Basin Finance Journal, 2, 165–199.

Lowry, M., Officer, M., & Schwert, G. W. (2010). The variability of IPO initial returns. Journal of Finance, 65, 425–465.

Lowry, M., & Schwert, G. W. (2002). IPO market cycles: Bubbles or sequential learning? Journal of Finance, 57, 1171–1200.

Marshall, M. G., and Jaggers, K., 2000. Polity IV project, political regime characteristics and transitions, 1800–2000, Center for International Development and Conflict Management, University of Maryland.

McKenzie, L. (1959). On the existence of general equilibrium for a competitive market. Econometrica, 27, 54–71.

Michaely, R., & Shaw, W. H. (1994). The pricing of initial public offerings: Tests of adverse selection and signaling theories. Review of Financial Studies, 7, 279–319.

Miller, K., & Holmes, K. R. (2009). Index of economic freedom. The Heritage Foundation &the Wall Street Journal. New York: Dow Jones & Co.

Miller, K., & Holmes, K. R. (2010). Index of economic freedom, the Heritage Foundation & the Wall Street Journal. New York: Dow Jones & Co.

Mok, M. K., & Hui, Y. V. (1998). Underpricing and aftermarket performance of IPOs in shanghai, China. Pacific-Basin Finance Journal, 6, 453–474.

Morck, R., Yeung, B., & Yu, W. (2000). The information content of stock markets: Why do emerging markets have synchronous stock price movements? Review of Financial Studies, 7, 279–319.

Neher, D. (1999). Staged financing: An angency prospective. Review of Economic Studies, 66, 255–274.

Petersen, M. A. (2009). Estimating standard errors in financial panel data sets: Comparing approaches. Review of Financial Studies, 22, 435–480.

Qi, Y., Roth, L., & Wald, J. K. (2010). Political rights and the cost of debt. Journal of Financial Economics, 95, 202–226.

Ritter, J. R. (1984). The hot issue market of 1980. Journal of Business, 57, 215–240.

Ritter, J. R. (1987). The cost of going public. Journal of Financial Economics, 19, 269–281.

Ritter, J. R., & Welch, I. (2002). A review of IPO activity, pricing, and allocations. Journal of Finance, 57, 1795–1828.

Rock, K. (1986). Why new issues are underpriced. Journal of Financial Economics, 15, 187–212.

Santos-Paulino, A., & Thirlwall, A. P. (2004). The impact of trade liberalisation on exports, imports and the balance of payments of developing countries. The Economic Journal, 114, 50–72.

Sarkar, P. (2011). Common law vs. civil law: Which system provides more protection to shareholders and creditors and promotes financial development. Working paper, University of Cambridge.

Scully, G. (2002). Economic freedom, government policy and the trade-off between equity and economic growth. Public Choice, 113, 77–96.

Shleifera, A., & Wolfenzon, D. (2002). Investor protection and equity markets. Journal of Financial Economics, 66, 3–27.

Siems, M. (2007). Reconciling law & finance and comparative law. McGill Law Journal, 52, 55–81.

Smith, A. (1776). An inquiry into the nature and causes of the wealth of nations. Chicago: University of Chicago Press.

Stapleton, R., & Subrahmanyan, M. (1977). Market imperfection, capital market equilibrium, and corporate finance. Journal of Finance, 32, 307–319.

Stulz, R. M. (1999). Globalization of equity markets and the cost of capital. Working Paper, National Bureau of Economic Research No. 7021.

Vassalou, M. (2003). News related to future GDP growth as a risk factor in equity returns. Journal of Financial Economics, 68, 47–73.

Wang, L., & Wang, S. (2012). Economic freedom and cross-border venture capital performance. Journal of Empirical Finance, 19, 26–50.

Wang, S., & Zhou, H. (2004). Staged financing in venture capital: Moral hazard and risks. Journal of Corporate Financing, 10, 131–155.

Wu, W., & Davis, O. (1999). The two freedoms, economic growth and development: An empirical study. Public Choice, 100, 39–64.

Acknowledgements

For helpful comments, the authors are grateful to the participants at the 2017 Frontiers of Business Research in China International Symposium.

Funding

Supported by Funding of Department of Education of Zhejiang Province (NO. Y201636546).

Availability of data and materials

The dataset supporting the conclusions of this article is available in the following link: http://www.heritage.org/index/

Author information

Authors and Affiliations

Contributions

All authors listed have contributed sufficiently to the project to be included as authors. Specifically, YC conducted all the tests in this paper. SW and WT participated in the conception and design of this research. HZ helped to draft the article and revise it critically for important intellectual content. All the authors listed have read and approved the manuscript that is enclosed.

Corresponding author

Ethics declarations

Competing interests

The authors declare that they have no competing interests.

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Chen, Y., Wang, S.S., Tong, W.H.S. et al. Economic freedom and IPO underpricing. Front. Bus. Res. China 11, 20 (2017). https://doi.org/10.1186/s11782-017-0019-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1186/s11782-017-0019-1