Abstract

At the beginning of factor investing research, the investment universe concentrated on developed markets and transaction costs were paid little attention. Expensive trading costs of factor investing in emerging equity markets influence optimal portfolio decisions. Based on a total costs estimate of factor-based portfolio tilts, a simple cost-mitigation approach increases net performance. Exploiting the structure of market impact, we indirectly control the costs by limiting order sizes relative to their underlying stocks’ short-term liquidity. This cost-efficient strategy yields better implementability and lower-priced turnover while a possible negative effect on gross performance is more than offset.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Investment decisions based on systematic risk premia and multi-factor asset pricing models provide a transparent alternative to active management that underlies high idiosyncratic risk. Foremost, Fama and French (1992) demonstrate the Arbitrage Pricing Theory and explain the stock market with a three-factor model extending the CAPM with the fundamental size and value risk factors, earlier investigated by Banz (1981) for size and Rosenberg et al. (1985) for value. Later, Carhart (1997) extents the Fama and French’s (1992) three-factor model, adding the prominent momentum factor. In Fama and French (2015), the two quality factors of investment and profitability are added as further systematic risk premia, which were rejected earlier concerning their robustness.

At the beginning of factor investing research, transaction costs were paid little attention. Contemporary research, still focusing on developed markets and mainly covering US stocks, presents several studies that identify the effect of transaction costs on factor-based equity portfolios with different out-comes. On the one hand, Lesmond et al. (2002), who investigate the transaction costs of momentum-based portfolios, find that net premia vanish for this strategy after trading costs. On the other hand, Korajzczyk and Sadka (2005), Novy-Marx and Velikov (2015), Ratcliffe et al. (2017) and Patton and Weller (2019), who also focus on net performance of momentum-based strategies, find different equilibrium sizes of the factor-based excess returns. Another disparity in the implementation cost literature is the shape of the underlying cost function that differs between concave, linear and even convex. The intentionally biased data selection can explain this disparity. Lesmond et al. (2002) report high-cost findings based on strong overweights in small- and micro-caps. This examination applies the study of Jegadeesh and Titman (1994), who do not consider implementation hurdles for large gross spread price momentum results. In contrast, Frazzini et al. (2018) limit their results to low-cost algorithmic trading approaches achieved in liquid developed markets. Extrapolating these findings to less efficient universes or average trading efforts might result in biased findings. However, most studies, including Frazzini et al. (2018), identify liquidity as the largest driver for market impact, and therefore, an important dimension for the successful implementation of factor-based strategies is observed. An active strategy’s total costs are composed of commission fees, bid-ask spreads and market impact. Various papers cover the modeling of market impact, including Loeb (1983), Kyle (1985), Hasbrouck (1991) and Keim and Madhavan (1996). Frazzini et al. (2018) report the impact of crucial model drivers (most importantly liquidity, followed by market capitalization, the idiosyncratic volatility of a firm’s equity return and finally, less crucial variables that represent the varying market environment) on the market impact in developed markets based on their large trading database. Several examinations covering market impact find this implementation hurdle increasing with a strategy’s investment size and liquidity demand. Empirical evidence agrees that the demand of trading large order sizes relative to the liquidity level increases market impact as invisible trading costs of adverse price movements. Further, Lesmond (2005) researches the costs of liquidity risk in emerging markets by explaining the lofty returns easily exceeding 75% p.a. with their bid-ask spread. Against this, illiquidity is an additional risk factor researched by Pastor and Stambaugh (2003), Acharya and Pedersen (2005) and Watanabe and Watanabe (2008) who develop asset pricing models that incorporate expected asset liquidity. Amihud (2002) finds that liquidity risk also significantly explains equity premia as especially the small firm effect. These studies identify the explanatory power of liquidity risk in the cross-section of stock returns and expose its uncertain effect on cost-efficient factor investing. Based on these findings, Donohue and Yip (2003), Garleanu and Pedersen (2013), Frazzini et al. (2018) and Novy-Marx and Velikov (2018) find optimal portfolio decisions in developed markets concerning transaction costs. Albeit the disparity of equilibrium portfolio sizes of factor-based excess returns and cost functions, the literature agrees on transaction costs distorting optimal portfolio decisions derived by factor investing strategies. Almgren and Chriss (2000) find cost-efficient strategies by identifying permanent and temporary market impact. Garleanu and Pedersen (2013) and Frazzini et al. (2018) find dynamic portfolio policies obtained by constrained optimizations and therefore improve net factor premia. Novy-Marx and Velikov (2018) resume three common cost mitigations in developed markets and compare their benefits. Despite the extensive cost modeling, studies on liquidity risk and recent investigations on cost-efficient implementations, the trade-off between risk premia and implementation costs in factor investing remains unclear. Especially the emerging equity markets, known as a less liquid stock universe with a large implementation hurdle, received little attention.

Our work is most closely related to Frazzini et al. (2018) but aims to understand emerging equity markets better. With recent progress regarding trading cost models and cost-efficient factor investing, most examinations focus on the liquid US stock market and other developed markets. This paper extends the existing literature in two ways. First, we investigate the net premia of factor investing in the less liquid emerging equity markets. Hence, we report the impact of a one-dimensionally dynamic cost model of three exemplary cost levels with respect to portfolio size. In this approach, we provide a sensitivity analysis of implementation costs by constructing portfolios that do not rely on a specific trading pattern nor result in overweights in small- or micro-caps. Second, we research the trade-off between risk premia and transaction costs of factor investing in emerging markets. In this approach, an active rebalancing strategy based on well-known risk factors to assess cost- and turnover efficiency is applied. In our investigation on the efficient implementation of fundamental and generic factors, we use a liquidity-driven market impact model based on Grinold and Kahn (1999) and Frazzini et al. (2018). Following and extending the ideas of Almgren and Chriss (2000), Frazzini et al. (2018) and Novy-Marx and Velikov (2018), a cost-efficient rebalancing strategy is presented. This cost-mitigation strategy seeks to limit the relative order sizes by a cap-parameter in each rebalancing step with respect to the underlying stocks’ short-term liquidity. Therefore, transaction costs are treated as another quantitative factor. This eventually leads to cost-efficient performance.

To transfer the results into asset management practice, we demonstrate the practical applicability explicitly from the aspect of illiquidity (which of course correlates strongly with size). Both market impact and the spread are driven by lower liquidity and make it more difficult to execute orders. This does not depend on size or stock market and is an effect that is primarily determined by the rel ative order size (order size relative to the observed liquidity) (see Frazzini et al. 2018). Other effects such as volatility and market environment also play a role, but size is overruled by liquidity. Given an increasing relative order size, the paper empirically demonstrates how the practical applicability suffers or becomes impossible according to transaction costs and in particular market impact.

The paper proceeds as follows. The next section describes the underlying market environment and reflects all applied methodologies. Here, the market impact as the cost model’s largest component is introduced and the methodologies for the multifactor mix and portfolio tilting are defined. The empirical results section outlines cost-inefficient portfolio performances concerning various investment horizons. Further, the cost-mitigation approach and its effect are presented. Moreover, we report sensitivity analyses and robustness checks to assess the return-to-cost trade-off. This section closes with the cost-mitigation’s implications on risk-adjusted performance. The last section concludes.

Data and methodology

The emerging markets universe

We research the emerging markets universeFootnote 1 in terms of the countries listed in the MSCI Emerging Markets IndexFootnote 2 over the last two decades ending in December 2019. Before the millennium, a small range of available data was omitted with respect to the quality and coverage of the liquidity data. In this study, data from MSCI is utilized to determine the underlying companies in emerging markets and their free-floating market capitalization. Besides M SCI, the Worldscope database from Refinitive is used for the fundamental value, profitability and investment factors. The generic momentum and low beta factors are calculated based on market data from Datastream (Refinitive). Further, Datastream is utilized for most market data such as return indices, liquidity and bid-ask spreads. Referring to the market closing of 2019 as today, this emerging markets universe consists of 26 countriesFootnote 3 across the five different sub-regions of Emerging Americas, Europe, Middle East, Africa and the Asia Pacific, of which the latter contributes to 79.35% of the emerging markets’ size.

In the following, the stocks associated with the MSCI Emerging Markets Index will be referred to as large caps. In contrast, remaining stocks larger than $10 million market capitalization are denoted as small caps. Large- and small-caps together complete the whole universe researched in this study. Today, this emerging markets universe consists of 3480 stocks summing up to $9.2 trillion free-floating market capitalization. These $9.2 trillion represent 15.1% of the developedFootnote 4 and emerging equity’s free-floating market capitalization with trending growth potentialFootnote 5. At year-end 1999, the free-floating market capitalization of the emerging markets stocks was summing up to $1.5 trillion, of which around

$1 trillion were related to large caps divided across 761 stocks. Back then, the universe consisted of 1209 assets and the 761 large caps aggregated to roughly two-thirds of the universe’s market capitalization. At year-end 2019, the number of emerging large caps grew to 1406 constituents, covering $7.2 trillion market capitalization measured in free-floating s tocks. Today, these 1406 emerging markets large caps grew in their share, summing up to 78.3% of the market capitalization. The remainder of 21.7% of the market capitalization is divided across 2074 small caps that sum up to around $2 trillion. This composition reflects the trends in the emerging markets environment. Although the number of small caps (quadrupled over the last two decades) significantly outnumbers large caps today, their relative market capitalization in the universe dropped by over 11 percentage points compared to the year-end 1999 level. In Fig. 1, the number of constituents in the emerging universe, also divided into large- and small-caps, is reported. This chart visualizes that large caps only just doubled over the last two decades while small caps quadrupled. Further, we compare the emerging markets environment with the developed world over the last two decades. The small caps of the developed world captured only just a fifth (while emerging markets’ small caps captured a third) of their universe’s market capitalization in year-end 1999. Today, the developed small caps market capitalization only aggregates to 13.5% (while emerging markets small caps still aggregate to 21.7%), unveiling the same trend of dominating large caps in the developed stock markets. Additionally, Fig. 2 provides the “lifetime” distribution of the stocks concerning their size class over the 240 observation months. This chart displays that, on average small caps keep in their size class less often than large caps for any given duration over the last two decades. Noting that stocks might change their size class during the observation months, this chart reports the fraction of stocks that survived a given time percentile with respect to their size class. The universe counts 7531 unique assets, of which 1053 (13.9%) persist less than a year on the stock market (5%-percentile). Only 223 (2.96%) of these stocks survive the full two decades, and only 22.8% of the universe is investable for at least 120 months (50% lifetime). From 6846 unique small caps, only four stocks stay in this size class over the full-time span and the remaining 6842 either left the market or are grown into large caps. Comparably, 124 of 2703 unique large caps keep their large-cap status over the 20 years. Another 95 size class shifting stocks survive the two decades on the EM stock market. From the 6846 unique small caps, more than a third (2018 stocks) have been downgraded from or upgraded to the large caps at least once in the two decades.

Time series of constituents in the emerging markets universe. This chart reports three time series based on monthly data of the number of constituents with respect to the whole universe, large- and small caps

Distribution of the lifetime of emerging markets stocks. As we find 7531 unique stocks in our analysis of the last two decades, this chart reports the relative lifetime distributions based on monthly data of the three size classifications. The relative fraction of the size class enduring this percentile is assigned over the percentiles of the stock lifetime (e.g., the 10% percentile denotes a lifetime of 24 months or less)

Transaction costs model

We need to apply a reasonable metric for the total transaction costs to calculate the trade-off between gross premia and implementation costs in emerging markets. The market impact model is the most important component of the total transaction costs and reflects the implementation hurdle of the illiquid emerging universeFootnote 6. Our study does not rely on a specific trading pattern by providing a sensitivity analysis on the market impact. We reflect the market impact costs with a simple square root cost model leaned on Grinold and Kahn (1999) and Frazzini et al. (2018):

ADV denotes the short-term liquidity calculated as average liquidity across primary and secondary stock exchanges over the last 20 trading days. Therefore, %ADV denotes the stock-wise order size relative to the monthly calculated ADV. We analyze the impact of three cost levels of market impact, specified by the cost parameter. Here, we reflect an efficient trading pattern of a larger institutional practitioner with a local trading desk, followed by a suggestion of average trading results. Lastly, we reflect an expensive cost level by the idea of incorporating issues with EM brokers and a potential time lag. In a recent study, Frazzini et al. (2018) apply a market impact model on their US trading data. In this paper, the reported relative trade size is limited below 15%. This low fraction occurs due to the liquid US stock market and an efficient trading pattern. Hence, no large relative order sizes that might occur from monthly portfolio decisions are included. Following the cost approach of this examination and transferring it to emerging markets, we understand the market impact of rebalancing equity to be mainly driven by liquidity demand (relative order size in %ADV). Finally, we define the total transaction costs as follows:

Execution feesFootnote 7 are comparably small, while the half bid-ask spread can also be expensive in emerging markets, albeit its general decline after the decimalization of the stock tickers. Referring to Fig. 4, we display the empirical spread data over the last two decades. A clearly declining trend over the last 20 years is observable. Figure 3 indicates the three cost parameters (low, medium, high costs) of variable market impact. However, the actual impact of transaction costs of each portfolio crucially depends on its size. Furthermore, Almgren and Chriss (2000) research this implementation hurdle of the stock markets by incorporating trading costs that eventually lead to a distorted but cost-efficient portfolio (Fig. 4).

Transaction costs square root model. This chart displays the three cost levels of market impact applied in this paper. The three parameters are scaling factors for the square root functionality of order sizes relative to liquidity

Time series statistics of spread data. This chart reports six time series statistics of the emerging markets positive spread data in bps based on daily data across all stocks

In this sense, many naive implementations of risk factors might result in high gross premia but fail a successful implementation as exemplary reported in Lesmond et al. (2002). We also researched more complex cost models concerning the effect of stock volatility and a perfectly passive trading model. This approach reflects the costs of waiting that arise by slowly trading toward the desired portfolio in small positions of 10% of the ADV per trading day. While the latter model mitigates the annualized transaction costs, no researched cost model distorts the results presented in this study. Therefore, we apply the one-dimensional market impact model with respect to simplicity as the most intuitive implementation. The next section presents a Z-scoring based on six risk factors and a portfolio tilting methodology.

Multifactor Z-scoring

Based on the asset pricing models of Carhart (1997), Frazzini and Pedersen (2014) and Fama and French (2015), we research tilt portfolios with respect to a mix of six well-known equity factorsFootnote 8. We include the generic effects of momentum and low beta and the four fundamental risk factors, value, size, profitability and investment. All these six factorsFootnote 9 are based on sound groundwork. We seek to diversify the factor premia and maintain a more persistent performance by equal-weighted mixing of the six signals. The empirical evidence presented in this examination is robust to alternative factor definitions, different mixes and also different weighting schemes. We decide to present this mix of six factors to cover fundamental factors and market effects and calculate the equal-weighted scheme with respect to simplicity.

Portfolio construction methodology

We apply a factor-tilt portfolio construction as a value-weighted method based on the market capitalization of free-floating stock. This value-weighted approach ensures that no strong overweights in small- and micro-caps arise. The stock positions in the initial portfolio (at t0) as well as all the following rebal- ancing weights (at t > t0) are constructed by screening the positive Z-scores (Z-scorei > 0) from the multi-factor mix. To calculate portfolio weights for each stock i, the universe weights weightuniverse,I are tilted under several constraintsFootnote 10 with respect to the following equation:

where the universe weights weightuniverse,i are determined by free-floating market capitalization. In every monthly rebalancing step, each stock i is assigned its factor-based return expectation Z-scorei, which is obtained by the equal-weighted mix of six Z-scores. After each rebalancing, the portfolio weights weighttilt,i are updated with empirical return indicesFootnote 11. This loop continues until the last rebalancing month of 2019-11-29. Later on, this tilting (denoted as “standard” or “uncapped” tilt) is further constrained with the cost-mitigation methodology.

Empirical results

Net performance

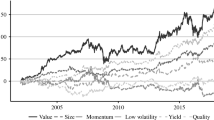

Before implementing the cost-mitigation, this subsection provides a net performance analysis of the tilting construction in emerging equity markets. The illustrations of factor premia in emerging markets achieved by this are displayed in the upper charts of Figs. 5, 6, 7 and 8. The setting in these four charts builds the foundation of our analysis and is split with respect to the investment horizon also roughly to investigate time trends. The initial portfolio size for these time spans is chosen heuristically with respect to the rising market liquidity and desired comparability. The upper chart of Fig. 5 displays the factor premia of the uncapped tilt over the full last two decades. While its gross performance is clearly higher than the universe’s or large caps’ return, most excess returns vanish with a medium cost level. The upper chart of Fig. 6 displays the returns over the last decade. Here, the factor-based tilts even underperform the universe net of costs. The upper chart of Fig. 7 shows similar results with even larger underperformance relative to the universe and large caps over the last 5 years. The factor premia clearly lost much of their magnitude in the trend of the last two decades. Hence, in the upper chart of Fig. 8 large factor premia in emerging markets persist over the first decade after the millennium. Finally, the tilt construction charts clearly display that the gross factor premia in emerging markets have been large in this century’s first decade but lost most of their potential in recent market environments. Especially with this decay in factor premia, the need for a cost-efficient implementation rises. Based on the findings of Almgren and Chriss (2000) and Novy-Marx and Velikov (2018), we present a cost-mitigation strategy to assess the trade-off between gross factor premia and transaction costs in the emerging stock markets. By applying this strategy to the above factor tilts, we report a thorough analysis of its effects.

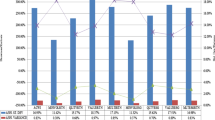

These charts report the performance (medium cost level applied) of the factor-based tilt portfolios with $2 billion initial portfolio size over the last two decades. The upper chart displays the uncapped tilt with 295.98% two-sided turnover p.a. The lower charts displays the cost-mitigated strategy with order size limiting parameter set to 100% of ADV (190.90% two-sided turnover p.a.)

These charts report the performance (medium cost level applied) of the factor-based tilt portfolios with $5 billion initial portfolio size over the last decade. The upper chart displays the uncapped tilt with 289.46% two-sided turnover p.a. The lower charts displays the cost-mitigated strategy with order size limiting parameter set to 100% of ADV (250.18% two-sided turnover p.a.)

These charts report the performance (medium cost level applied) of the factor-based tilt portfolios with $7.5 billion initial portfolio size over the five years. The upper chart displays the uncapped tilt with 215.12% two-sided turnover p.a. The lower charts displays the cost-mitigated strategy with order size limiting parameter set to 100% of ADV (202.23% two-sided turnover p.a.)

These charts report the performance (medium cost level applied) of the factor-based tilt portfolios with $2 billion initial portfolio size over the first decade only. The upper chart displays the uncapped tilt with 305.90% two-sided turnover p.a. The lower charts displays the cost-mitigated strategy with order size limiting parameter set to 100% of ADV (208.21% two-sided turnover p.a.)

Cost-mitigation strategy

This section reports the impact of the cost-mitigation strategy on the uncapped tilting portfolios. Based on gross and net factor premia insights, we examine the additional cost-mitigation constraint to improve its return-to-cost trade-off. We accomplish that by indirectly taking the transaction costs into account by adding a liquidity constraint to the tilt construction. While the trade execution is treated as fully exogenous to the monthly portfolio decisions, we implement the market impact function endogenously into the tilting construction. This constraint limits order sizes to exploit the near-term liquidity expectation. Therefore, the total transaction costs are mitigated while expensive turnover is re-distributed with respect to sufficiently liquid stocks. The portfolio objective is to maximize the net performance without distorting risk. Eventually, this comes at the cost of lowered return expectation (measured in average portfolio ex-ante Z-score) and, therefore, possibly lowered gross performance. This turns out to be cost-efficient, while the uncapped tilting maximizes the ex-ante return expectation without considering costs. Now, keeping all portfolio- and rebalancing constraints equal, various cost-mitigated portfolios are compared to their uncapped tilts and the universe with respect to (risk-adjusted) performance. The more recent study of Novy-Marx and Velikov (2018) claims that there is no arbitrage opportunity in harvesting factor premia in developed markets. The statistically significant net performance improvement of factor premia is based on higher risk exposure. Novy-Marx and Velikov (2018) report statistically equal Sharpe ratios for factor-based strategies against the universe. We also find mostly statistically insignificant Sharpe ratios of risk premia in recent years at best. Earlier initialized factor tilts, particularly cost-mitigated tilts and low-cost implementations, clearly show statistically significant (risk-adjusted) returns against the universe and uncapped tilts, respectively. Further, we display the cost-mitigated performances of the factor-tilts in the lower charts of Figs. 5, 6, 7 and 8. These four tilts are constructed by constraining the relative order size in each rebalancing to a limit of 100% of the near-term ADV (100%ADV). All these portfolios show increased net performance in comparison with the upper charts’ performance of uncapped tilts. Due to lowered turnover and efficiently lowered costs, the cost-mitigation offsets losses in gross performance. In Fig. 5 the cost-mitigation alone results in a significant excess return of around 2% annualized return after costs. Over the last 10-years, the net underperformance of over 1.5% relative to the large caps can almost be fully recovered in Fig. 6. Over the last five years, in Fig. 7, around 2.5% of the net underperformance is recovered by the cap-parameter of 100 %ADV. In the lower chart of Fig. 8, the cost-mitigation outperforms its uncapped tilt by almost 1.5% annualized return after costs (at medium cost level). We remark that the naive ADV expectation of predicting liquidity in the trade execution by its current level is a model assumption. Nonetheless, we apply the cost model with respect to the liquidity level after portfolio decisions with perfect foresight. The quality of the ADV expectation relies on this naive forecast. However, the monthly first-order auto-correlation of ADV (no overlap due to the ADV window size) is significantly large. Even in the cross section of different size classes, the Pearson auto-correlation ranges from close to 70 to over 90% with respect to the time horizons. Eventually, the cost-mitigation implicitly controls and mitigates expensive turnover. This results in more cost-efficient implementations by applying a suitable order size limit (100%ADV in the above scenarios) with respect to the investment size.

Sensitivity analysis

In this subsection, the effect of the cost-mitigation strategy is analyzed in more detail. The intended improvement in the return-to-cost trade-off seeks to determine net performance efficiency concerning portfolio size. We increase the (risk-adjusted) net premia of portfolios in emerging markets by applying the cost mitigation strategy. The charts of Figs. 9, 10, 11 and 12 report the gross and net performances of several cost-mitigations against their uncapped tilts with respect to ascending initial portfolio sizes (log-scaled x-axis). Figure 9 displays the performances over the last two decades and reveals a sorted picture. For small initial portfolio sizes, no gross performance is lost with cost-mitigated tilts. For initial portfolio sizes above $250 million, increasing parts of the gross performance are sacrificed for most cap parameters. This negative effect is more than offset for most strategies and cost levels. The loss in gross performance is larger for strict cap parameters (e.g., for limiting order sizes by 50% of the ADV, in the portfolios denoted as “TradeCap050”). The stricter cap parameters eventually outperform the uncapped tilt at smaller portfolio sizes at a large cost level. For larger portfolio sizes, more soft constraints like cap-parameter 200% of ADV clearly outperform the uncapped tilt with respect to the capacity limits of strict implementations. In Fig. 10, there is almost no negative effect on gross performance and almost every cap-parameter outperforms the uncapped tilt even with respect to the low-cost level. More strict cap parameters stand out over this horizon, especially for large portfolio sizes or high costs. With lower factor premia, the portfolios displayed in Fig. 11 are less sorted over the last five years. However, cost-mitigation strategies outperform the expensive uncapped tilt with rising cost levels and portfolio size. In the market environment with large factor premia as seen in Fig. 12 after the millennium, the uncapped tilt outperforms the cost-mitigated strategies with respect to gross performance. While the strict cap parameters cannot increase the net performance, more soft cap parameters can outperform the uncapped tilt at least at a medium cost level. Summing up these results, we often see a certain gross performance loss induced by the additional short-term liquidity constraint in many tilt portfolios. Nonetheless, with ascending portfolio size, cost level or both, a cost-mitigation strategy is found to outperform the uncapped tilt in each investment horizon. Eventually, determining a cross-sectional optimal strategy parameter is not possible but depends on investment size, cost level and market conditions. We can further conclude the empirical evidence that the cost-mitigation strategy shows increasing profitability with higher cost levels, portfolio sizes, or lower risk premia.

These charts report the gross and net performance of various cost-mitigation strategy limitings from 1999-12-31 to 2019-11-29 with respect to initial portfolio size and level of the trading cost model. The base case labeled as "Uncapped" is indicated with a dotted line and a ceased line indicates the reached capacity level of that strategy with respect to the market environment

These charts report the gross and net performance of various cost-mitigation strategy limitings from 2009-12-31 to 2019-11-29 with respect to initial portfolio size and level of the trading cost model. The base case labeled as “Uncapped” is indicated with a dotted line and a ceased line indicates the reached capacity level of that strategy with respect to the market environment

These charts report the gross and net performance of various cost-mitigation strategy limitings from 2014-12-31 to 2019-11-29 with respect to initial portfolio size and level of the trading cost model. The base case labeled as “Uncapped” is indicated with a dotted line and a ceased line indicates the reached capacity level of that strategy with respect to the market environment

These charts report the gross and net performance of various cost-mitigation strategy limitings from 1999-12-31 to 2009-11-23 with respect to initial portfolio size and level of the trading cost model. The base case labeled as “Uncapped” is indicated with a dotted line and a ceased line indicates the reached capacity level of that strategy with respect to the market environment

To research the effect of the cost-mitigation on further portfolio characteristics, Tables 1, 2 and 3 exemplary report a thorough performance analysis and descriptive statistics on the four environments. Table 1 shows that across all time spans, fractions of the excess return expectation (denoted as ex-ante factor Z-score) are sacrificed in the cost-mitigation. Therefore, this effect is in line with the extent of the cost reduction and is larger for strict cap parameters. Table 1 also reports the significance in (risk-adjusted) performance differences between any cost-mitigation against the uncapped tilt. In Appendix C, the applied hypothesis testing methodology is described to determine statistically significant differences in returns and Sharpe ratios. In general, we see that even small differences can easily be statistically significant due to the high serial correlation between the portfolio tilts. Table 1 confirms that for each declared investment horizon and cost level, at least one cost-mitigation significantly out performs the uncapped tilt’s (risk-adjusted) performance. In Table 2 further statistics are presented to understand the efficacy of the cap-parameters better. We see that more strict cap parameters lead to a broader diversification in terms of average holdings. This effect is mainly affecting small caps. With more strict cost mitigations, the two-sided turnover shrinks while limiting the expensive trades.

This effect, in general, is similar between large- and small-caps in the tilted portfolios. For the 20-year and the 10-year horizons after the millennium, strict cost mitigations improve the average position size held in the portfolio relative to its short-term ADV. This portfolio liquidity improvement is reversed for the latest 10- and 5-year horizon investments. Unfortunately, the average portfolio liquidity relative to the universe liquidity worsens for the strictest cap parameters. This negative effect peaks for the first 10-year horizon after the millennium between the uncapped tilt and cap-parameter 50 with 16 percentage points difference in portfolio liquidity. Nonetheless, the (risk-adjusted) net performance improvement is substantial for these tilts at each cost level. Finally, Table 2 reports the average order size of the cost-mitigations and uncapped tilt relative to the short-term liquidity and it is clear to see that the strict cost mitigations yield a certainly improved implementability. The “capped trades” statistic shows how many of the total trades in each portfolio are affected by the cost mitigations on average per rebalancing. Table 3 reports the return and Sharpe ratio significance of each cost-mitigation against the universe. While the portfolios over the last two decades and the portfolios over the first decade after the millennium outperform the universe significantly in terms of return and Sharpe ratio, the portfolios over the last 10 and 5 years perform much weaker. They often underperform with respect to the cost level. For the 5-year horizon, only the strictest cap-parameter outperforms the universe and the return differences are not significant for any cost level. This again reflects the observed decline in factor premia. The 10-year horizon portfolios have to be strictly cost-mitigated to outperform the universe significantly.

Robustness checks

To obtain robustness-checked results for the performance of the cost mitigation and to smooth the path dependencies of any initial portfolio, we provide robust statistics by constructing portfolios on a monthly rolling basis. Due to high serial correlations in the constructed portfolios and path dependency to their initial portfolio, geometric means over all possible portfolios (1-month rollings) of different initial dates confirm the overall efficiency of the cost-mitigation strategy. We do not want the results to be conditioned by the market environment or return expectations of the initial portfolio. Therefore, this robustness check corrects for all path dependencies. Hence, we update the monthly rolling initial portfolio sizes by the previous starting month’s performance. Table 4 reports the (risk-adjusted) excess return significance of cost-mitigated tilts against the uncapped tilts with respect to the rolling construction. All return and Sharpe ratio differences are statistically significant with respect to manysampled rebalancing months and often high serial correlations. Table 5 reports the (risk-adjusted) excess return significance of cost-mitigated portfolios against their universe with respect to the rolling construction. Cap-parameter 100%ADV emphasizes the statistically significant excess returns against uncapped tilts and the universe for various investment sizes. With the rolling portfolios over the last 20 years, 100% ADV outperforms the universe by 2.5% (the uncapped tilt by around 1%) p.a. with a significantly higher Sharpe ratio of .96 against 0.66 (.88) at only medium cost level.

Conclusion

While illiquidity can be understood as a long-term factor that causes cyclical near-term risk premia, it is also crucial for transaction costs. We studied this trade-off with respect to gross factor premia over various horizons. From our analysis, we can draw several conclusions. First, we find that it is possible to construct factor-based equity tilt portfolios with positive net premia in emerging markets over the last two decades and sub-periods. Second, we see that high risk premia of factor tilts in emerging equity markets have vanished in recent years. Therefore, a successful factor-based strategy is often determined by an efficient implementation (cost mitigation or low cost level). Third, with growing portfolio size increasing fractions of short-term portfolio liquidity and excess return expectation are sacrificed. Fortunately, the negative effect on the expected excess return and eventually often on gross performance is more than offset. Finally, we show that the cost-mitigation improves the (risk-adjusted) net performance of the factor tilts but can only partially preserve vanished risk premia. A cost-efficient implementation is often the critical component to outperform the market when the uncapped factor strategy solely does not.

To summarize these key findings, one core contribution of our analyses is that the cost-efficiency strategy generally works with different factor strategies. Of course, there are possible factor portfolios that have better risk-adjusted performance. However, the results work without much turnover, even with such simple factors/factor mixes. Nevertheless, the strategy has certain portfolio size limitations with respect to the market environment and cost-mitigation parameters. Before reaching this capacity limit, the efficacy of the cost-mitigation is increasing with respect to rising investment sizes and cost levels. Aiming to delay these limitations, further investigation will focus on the associations between factor investing, cost-mitigation strategies and macroeconomic influences. We researched that risk premia are cyclical in the near term and assume that a macro-adaptive approach might further increase cost-efficiency.

Notes

In the following, the emerging markets are denoted as “EM” and also referred to as “whole uni- verse”.

https://www.msci.com/emerging-markets, last visited: 2023-06-26.

The MSCI Emerging Markets Index consists of 26 emerging economies, including Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia,

Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates.

The developed world universe consists of all countries listed in the MSCI World Index, augmented with the small caps larger than $10 million market capitalization in each listed country. The developed universe, excluding frontier- and emerging markets, lists the following 23 countries: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, UK, USA.

Today, the equity market capitalization of emerging markets in the world’s investable stock markets (excluding frontier markets) aggregates to 15.1%. This share almost tripled and is constantly

growing from 5.4% at year-end 1999. The recent growth of the emerging stock markets is reported with 14.5% at year-end 2018, 13.9% at year-end 2017 and 12.7% of all non-frontier stock universes’ market capitalization at year-end 2016. For reference, less than 1 billion people, or approximately 15% of the world’s population, live in a developed markets country but developed stock markets still account for around 85% stock market capitalization (“http://www.ashmoregroup.com/sites/default/files/article-docs/MC_10%20May18_2.pdf, last visited: 2023-06-26).

Emerging markets stocks, in general, are considered to be executed more expensive than developed markets stocks. Besides the lower market liquidity, the time shift between emerging and developed regions can be an additional hurdle for institutional and individual investors.

Execution and commissions fees are negotiable and sum up to over 7bps in emerging markets. These fees cover all legal middle office activities of the sell-side and ensure the backup of all trade documentations through a global custodian. These electronic backups are by law completed by carbon copies in case of emergency.

A detailed description of the six factors and their calculations is reported in Appendix A.

9The fundamental value factor was researched in Basu (1977) and Rosenberg et al. (1985). The size factor is also a systematic risk premium and was discovered in Banz (1981). Jegadeesh and Titman (1994) and Hurst et al. (2017) researched the generic momentum factor. The operating profitability was researched by Haugen and Baker (1996) and Novy-Marx (2013) and is another systematic risk premium and the investment factor found in Titman et al. (2004), Cooper et al. (2008) and Watanabe et al. (2013). Ang et al. (2006) and Frazzini and Pedersen (2014) examined the generic low beta factor.

A detailed description of all (rebalancing) constraints is reported in Appendix B.

Thompson Reuters Datastream return indices for emerging equity represent the empirical stock returns as done by the Center for Research in Security Prices (CRSP) concerning dividend payments and stock splits.

References

Acharya, V.V., and L.H. Pedersen. 2005. Asset pricing with liquidity risk. Journal of Financial Economics 77 (2): 375–410.

Almgren, R., and N. Chriss. 2000. Optimal execution of portfolio transactions. Journal of Risk 3 (2): 5–39.

Amihud, Y. 2002. Illiquidity and stock returns: cross-section and time-series effects. Journal of Financial Markets 5 (1): 31–56.

Ang, A., R.J. Hodrick, Y. Xing, and X. Zhang. 2006. The cross-section of volatility and expected returns. Journal of Finance 61 (1): 259–299.

Banz, R.W. 1981. The relationship between return and market value of common stocks. Journal of Financial Economics 9 (1): 3–18.

Basu, S. 1977. Investment Performance of common stocks in relation to their price-earnings ratios: A test of the efficient market hypothesis. Journal of Finance 32 (3): 663–683.

Carhart, M.M. 1997. On persistence in mutual fund performance. Journal of Finance 52 (1): 57–82.

Cooper, M.J., H. Gulen, and M.J. Schill. 2008. Asset growth and the cross-section of stock returns. Journal of Finance 63 (4): 1609–1651.

Donohue, C., and K. Yip. 2003. Optimal portfolio rebalancing with transaction costs. Journal of Portfolio Management 29 (4): 49–63.

Efron, B., and R.J. Tibshirani. 1993. An introduction to the bootstrap. New York: Chapman & Hall/CRC.

Fama, E.F., and K.R. French. 1992. The cross-section of expected stock returns. Journal of Finance 47 (2): 427–465.

Fama, E.F., and K.R. French. 2015. A five-factor asset pricing model. Journal of Financial Economics 116 (1): 1–22.

Frazzini, A., and L.H. Pedersen. 2014. Betting against beta. Accounting Review 111 (1): 1–25.

Frazzini, A., Israel, R., and T.J. Moskowitz. 2018. Trading costs [working paper]. AQR Capital Management. https://papers.ssrn.com/sol3/papers.cfm?

Garleanu, N., and L.H. Pedersen. 2013. Dynamic trading with predictable returns and transaction costs. Journal of Finance 68 (6): 2309–2340.

Grinold, R.C., and R.N. Kahn. 1999. Active portfolio management: A quantitative approach for producing superior returns and selecting superior returns and controlling risk. New York: McGraw-Hill Library of Investment and Finance.

Hasbrouck, J. 1991. Measuring the information content of stock trades. Journal of Finance 46 (1): 179–207.

Haugen, R.A., and N.L. Baker. 1996. Commonality in the determinants of expected stock returns. Journal of Financial Economics 41 (3): 401–439.

Hurst, B., Y.H. Ooi, and L.H. Pedersen. 2017. A century of evidence on trend-following investing. Journal of Portfolio Management 44 (1): 15–29.

Jegadeesh, N., and S. Titman. 1994. Returns to buying winners and selling losers: Implications for stock market efficiency. Journal of Finance 48 (1): 65–91.

Keim, D.B., and A. Madhavan. 1996. The upstairs market for large-block transactions: Analysis and measurement of price effects. Review of Financial Studies 9 (1): 1–36.

Korajzczyk, R.A., and R. Sadka. 2005. Are momentum profits robust to trading costs?. Journal of Finance 59 (3): 1039–1082.

Kyle, A.S. 1985. Continuous auctions and insider trading. Econometrica 53 (6): 1315–1335.

Ledoit, O., and M. Wolf. 2008. Robust performance hypothesis testing with the sharpe ratio. Journal of Empirical Finance 15: 850–859.

Lesmond, D.A. 2005. Liquidity of emerging markets. Journal of Financial Economics 77 (2): 411–452.

Lesmond, D.A., M.J. Schill, and C. Zhou. 2002. The illusory nature of momentum profits. Journal of Financial Economics 71 (2): 349–380.

Loeb, T.F. 1983. Trading cost: The critical link between investment information and results. Financial Analysts Journal 39 (3): 39–44.

Novy-Marx, R. 2013. The other side of value: The gross profitability premium. Journal of Financial Economics 108 (1): 1–28.

Novy-Marx, R., and M. Velikov. 2015. A taxonomy of anomalies and their trading costs. Review of Financial Studies 29 (1): 104–147.

Novy-Marx, R., and M. Velikov. 2018. Comparing cost-mitigation techniques. Financial Analyst Journal 75 (1): 85–102.

Pastor, L., and R. Stambaugh. 2003. Liquidity risk and expected stock returns. Journal of Political Economy 111 (3): 642–685.

Patton, A.J., and B. Weller. 2019. What you see is not what you get: The costs of trading market anomalies. Journal of Financial Economics (Forthcoming).

Politis, D.N., and J.P. Romano. 1992. The stationary bootstrap. Journal of the American Statistical Association 89: 428.

Ratcliffe, R., P. Miranda, and A. Ang. 2017. Capacity of smart beta strategies from a transaction cost perspective. Journal of Index Investing 8 (3): 39–50.

Rosenberg, B., K. Reid, and R. Lanstein. 1985. Persuasive evidence of market inefficiency. Journal of Portfolio Management 11 (3): 9–16.

Titman, S., K.C.J. Wei, and F. Xie. 2004. Capital investments and stock returns. Journal of Financial Economics 39 (4): 677–700.

Watanabe, A., and M. Watanabe. 2008. Time-varying liquidity risk and the cross section of stock returns. Review of Financial Studies 21 (6): 2449–2486.

Watanabe, A., Y. Xu, T. Yao, and T. Yu. 2013. The asset growth effect: Insights from international equity markets. Journal of Financial Economics 108 (2): 529–563.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The reviews expressed in this paper are those of the authors and do not necessarily reflect the position of Quoniam Asset Management GmbH. Special thanks should be given to Thomas Kieselstein and Sascha Mergner for initiating this research and providing access to the company’s data center. We are particularly grateful for the discussions and helpful comments of Stefan Klein and Maximilian Stroh. The thoughts and opinions expressed in this study are those of the authors alone, and no other person or institution has any control over its content.

Appendices

Appendix A: Descriptions of factors

Factor | |

|---|---|

Momentum | Logarithmic price momentum is calculated as the sentiment of the stock price 12 months ago up to the previous months’ end price based on Jegadeesh and Titman (1994). The so-called 12X1 momentum omits the last month concerning the reversal effect for long-term investments. It is the supreme example of a generic market factor and a superior long-term alpha driver in the cross-section of sectors and regions. The persistence of this factor can be reasoned by behavioral traits of investors that follow strong performing stocks. These investors’ attention leads to a crowding effect that fosters the price sentiment until a macroeconomic event, earnings miss, or other incident stops the trend. In this paper, the price momentum is determined as |

\({\text{Mom12X}}1_{t} : = \log \left( {\frac{{{\text{pClose}}_{t - 12} }}{{{\text{pClose}}_{t - 1} }}} \right)\) (4) | |

Value | The value factor, as researched in Rosenberg et al. (1985), denotes a common book-to-price multiple that compares an asset’s book value to the actual market price. A large book-to-price value represents a cheap stock and therefore assigns a buy signal with respect to factor investing approaches. The origin of this fundamental risk premium dates back to the investigations of Benjamin Graham and David L. Dodd and has behavioral-based characteristics beneath its systematic and fundamental nature. A possible explanation of the persistence of this systematic risk premium lies in the investors’ optimism about bargains and pessimistic overreactions often resulting in bargains when poor financials are reported. |

Beta | The low beta factor investigated by Ang et al. (2006) and Frazzini and Pedersen (2014) describes how returns on a stock co-vary with returns on the market. Empirical research proves that low beta stocks explain cross-sectional premia in the long run and, by construction, serve as a cushion in drawdowns. In this study, \({\text{Beta}}: = \frac{{{\text{cov}}(r_{i} ,r_{{{\text{uni}}}} )}}{{\sigma^{2} (r_{{{\text{uni}}}} )}}\) (5) is calculated with weekly data over the last 250 business days and the cov() is exponentially weighted with a 125 business days half-life. |

Size | The size factor researched in Banz (1981) shows that smaller stocks in terms of market capitalization explain cross-sectional excess return as an investor’s compensation for taking additional risk. The efficacy of the size factor can be economically explained as a systematic risk premium based on the volatile nature and higher risk of bankruptcy of small caps. In this examination, the size factor is calculated as the logarithmic free-floating market capitalization |

Operating profit (profitability) | Operating profit (commonly known as EBIT) denotes the profitability of the company’s business before interest and taxes and is widely applied as another quality factor. To determine operating profit, the operating expenses are subtracted from the gross profit. Haugen and Baker (1996) and Novy-Marx (2013) find an additional risk premium with this factor. Financially healthy companies tend to continue their good business in the future, therefore economically justifies this risk factor |

Total assets growth (investment) | This risk factor measures the growth of the total assets to forecast future excess return as a second quality factor. Titman et al. (2004), Cooper et al. (2008) and Watanabe et al. (2013) find that stocks with lower recent total assets growth tend to outperform the market. In this paper, we compute the growth of the total assets over the last 500 business days |

Appendix B

Descriptions of rebalancing and tilting constraints (applied values in parentheses)

In the following table, all applied constraints are listed. The first constraint listed is the essential additional constraint that defines the cost-mitigation strategy. While all tilt-portfolios are equally initialized, all cost-mitigated portfolios hold this additional constraint in all time steps t > 0.

Constraint | |

|---|---|

Relative maximum order size cap (25–300% of ADV) | This parameter distinguishes cost-mitigated portfolios from their base case. This sets a limit for the relative order sizes in the rebalancing steps |

Initial threshold (Top 50%) | This threshold determines the lower bound for the mixed factor exposure at portfolio initialization. It controls the number of titles in the initial portfolio. This constraint represents the banding constraint from Novy-Marx and Velikov (2018) |

Rebalancing threshold (top 50%) | Alike the initial threshold constraint, a lower bound for the factor exposures is set for each rebalancing step. This banding constraint controls turnover and guides the number of holdings in the portfolio with respect to the trade-off of diversification and excess return expectation |

Relative minimum order size (10%) | This constraint manages the minimum size of position changes of already held assets in the rebalancing. It can be utilized to control turnover |

Absolute minimum order size (1 basis point of portfolio size) | Alike the relative minimum order size in absolute terms. This constraint prohibits the factor-tilt from generating economically insignificant orders that would artificially raise the average holdings |

Absolute Minimum Holding Size (5 basis points of portfolio size) | Declares the smallest permitted size of a weight in the constructed portfolio that a position might have |

Absolute maximum holding size (2% of portfolio size) | Concerning implementability and diversification, a maximum holding constraint limits portfolio weights to a certain fraction of the whole portfolio size. Each assets’ total market capitalization is additionally taken care of in this constraint |

Appendix C

Pairwise portfolio significance testing for differences in annualized (excess) returns and sharpe ratios

Due to strong serial correlations between portfolios and auto-correlation in the tiltings itself and a stochastic dependency in the portfolios, a common t-test cannot be applied. To test the statistical significance of our presented evidence, we apply the following test statistic Zµ as a two-sided t-test on the return differences for stochastically dependent, identically distributed portfolios:

With N degrees of freedom (#rebalancing months-2; because portfolio initialization is cost-mitigation independent) and µi, σi assigning the estimated annualized means and standard deviations of both observations.

We also report the statistical significance of the Sharpe Ratio (SR) difference between two stochastically dependent portfolios with the following test statistic from Ledoit and Wolf (2008):

Based on these test statistics all hypothesis tests check the alternatives: H0 : µ1 = µ2 (SR1 = SR2), H1 : µ1 I= µ2 (SR1 I= SR2) and report the p-value to the error levels p < 0.05, p < 0.01 and p < 0.001.

To account for the auto-correlation of the tilts, we do not just report the results of the above hypothesis tests. Still, we perform a bootstrap that is explained as follows.

Stationary circular block-bootstrapping

The hypothesis tests above are robustness-checked with a block-bootstrap to correct for auto- correlation as researched in Efron and Tibshirani (1993). Politis and Romano (1992) proved that randomization of the block-length in the circular block-bootstrapping maintains the stationarity of the observations in the bootstrapped samples. Therefore, the reported p-values are finally calculated as follows:

-

Calculate the Z-statistic as Z once for return- or Sharpe ratio testing

-

To apply the stationary circular block-bootstrap to test H0, transform the data so that H0 is true.

-

For Sharpe ratio testing it is \(\tilde{X}_{i} : = \left[ {\frac{{X_{i} - \hat{\mu }_{i} }}{{\hat{\sigma }_{i} }}\hat{\sigma } _{{{\text{combined}}\,{\text{sample}}}} } \right] + \hat{\mu }_{{{\text{combined}}\,{\text{sample}}}}\) for both time series.

-

For return testing this transformation is given by \(\tilde{X}i : = X_{i} - \hat{\mu }_{i} + \hat{\mu }_{{{\text{combined}}\,{\text{sample}}}}\) for both time series.

-

-

The robustness-checked hypothesis test works by simulating the distribution of the Z-statistic with block-bootstrapping under a true H0. We do that by generating M = 100,00 block-bootstrap samples for both time series of forced length N (circular) with uniformly randomized block-length \(b \in \left\{ {1,2,...,L\frac{N}{2}J} \right\}\) to maintain stationarity. The Z-statistic is calculated for each of the M bootstrap-samples as Z˜i.

-

Now we sum \(\frac{{\mathop {{\text{I}}:}\nolimits_{i = 1}^{{M = {1}0000 }} I(|\tilde{Z}_{i} \left| \ge \right|Z|)}}{M} = :p\) where (I) denotes the indicator function (that equals 1 if its argument is true and 0 otherwise) to get the p-value of our hypothesis test given H0 is true. This p value is the reported statistic for each hypothesis test in the results section.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Stankov, K., Schiereck, D. & Flögel, V. Cost mitigation of factor investing in emerging equity markets. J Asset Manag 25, 303–325 (2024). https://doi.org/10.1057/s41260-024-00353-4

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41260-024-00353-4