Abstract

Current account imbalances have increased steadily in rich countries over the past 20 years. While the U.S. current account deficit dominates the numbers and the news, other countries, especially within the euro area, are also running large deficits. These deficits are different from the Latin American deficits of the early 1980s, or the Mexican deficit of the early 1990s. They involve rich countries; they reflect mostly private saving and investment decisions, and fiscal deficits often play a marginal role; and the deficits are financed mostly through equity, FDI foreign direct investment, and own-currency bonds rather than through bank lending. Yet there appears to be a widely shared concern that these deficits are too large, and government intervention is required. My purpose is to examine the logic of this argument. I ask the following question: Assume that deficits reflect private saving and investment decisions. Assume also that people and firms have rational expectations. Should the government intervene, and, if so, how? To answer the question, I construct a simple benchmark. In the benchmark, the outcome is “first best” and there is no need nor justification for government intervention. I then introduce simple distortions in either goods, labor, or financial markets, and characterize the equilibrium in each case. I derive optimal policy and the implications for the current account. I show that optimal policy may or may not lead to smaller current account deficits. I see the model and the extensions very much as a first pass. Sharper conclusions require a better understanding of the exact nature and the extent of distortions, which we do not have yet. Such understanding is needed, however, to improve the quality of the current debate.

Similar content being viewed by others

Notes

For a review of facts and discussions, see Edwards (2002).

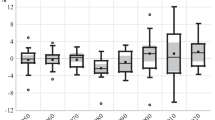

I have looked at it in more detail in Blanchard (2006)

A good survey of theories and facts is provided by Cline (2005). An insightful analysis of the relative roles of saving, investment, and portfolio flows in the United States and creditor countries is given by Brender and Pisani (2007).

For more discussion, see in particular Bernanke (2005); Blanchard, Giavazzi, and Sa (2005); and Caballero, Emmanuel, and Pierre-Olivier (2006).

I introduce a labor-leisure choice because when I later introduce distortions that imply employment is potentially off the labor supply, I want to be able to assess the welfare cost of such a deviation and derive the optimal policy.

See for example Obstfeld and Rogoff (1996, Chapter 4, Section 4, Equation 34); and Dornbusch (1983).

Under the alternative assumption of a decrease in the interest rate, dr<0, all the equations above would hold, with dr replacing dβ. The only difference is that, although the decrease in β has no effect on wealth A, the decrease in r increases wealth by dA=−2dr.

One of the many problems in mapping any model to the data is that the initial unemployment rate in Portugal (7 percent in 1995) was probably higher than the natural rate at the time. Thus, some of the employment increase in the 1990s was probably justified.

The usual rationalization would be to assume that monopolistic competitive price-setting firms in the non-tradables sector are willing to satisfy demand so long as price exceeds marginal cost. An explicit formalization would then have an additional distortion, namely, the presence of the monopolistic markup. This distortion, so long as the markup is constant, is irrelevant for my purposes.

This result is not robust to more general preferences, and may not hold if the intertemporal and intratemporal elasticities of substitution are different. But the point that the current account deficit need not be larger under such rigidities is general.

This is well-traveled ground in the research on optimal monetary policy in an open economy. See, for example, Devereux and Engel (2006).

The extreme form of some of these results depends again on the log-log restrictions. But the message about the relative effects of dg N and dg T is general.

The question has been explored, in a different but related context, by Caballero and Hammour (2005), who have looked at whether recessions lead to the disappearance of low-productivity vs. financially constrained firms.

This is, for example, a recurring theme in Nouriel Roubini's blog commentary on the U.S. current account deficit (www.rgemonitor.com/blog/roubini/).

The Asian crisis indeed shows that sudden stops can occur even in the absence of large current account deficits.

This is very well traveled ground. For a simple but formal discussion, see, for example, Caballero and Krishnamurthy (2002).

References

Bernanke, Ben, 2005, “The Global Saving Glut and the U.S. Current Account Deficit,” Sandridge Lecture, Virginia Association of Economics, Richmond, Virginia, March.

Blanchard, Olivier, 2006, “Adjustment within the Euro: The Difficult Case of Portugal,” MIT Economics Working Paper No. 06-04 (Cambridge, Massachusetts, Massachusetts Institute of Technology). Available via the Internet: http://econ-www.mit.edu/faculty/download_pdf.php?id=1295. Also published in Portuguese Economic Journal, February 2007.

Blanchard, Olivier, and Francesco Giavazzi, 2006, “Rebalancing Growth in China. A Three-Handed Approach.” China & the World Economy, Vol. 14, No. 4, pp. 1–20.

Blanchard, Olivier, and Francesco Giavazzi, and Filipa Sa, 2005, “International Investors, the U.S. Current Account, and the Dollar,” Brookings Papers on Economic Activity 1, Brookings Institution, pp. 1–65.

Brender, Anton, and Florence Pisani, 2007, Les Déséquilibres Financiers Internationaux, (Paris, La Découverte).

Caballero, Ricardo, Emmanuel, Farhi, and Pierre-Olivier, Gourinchas, 2006, “An Equilibrium Model of “Global Imbalances” and Low Interest Rates,” MIT Working Paper 06-02 (Cambridge, Massachusetts, Massachusetts Institute of Technology) Available via the Internet: http://econ.www.mit.edu/faculty/download_pdf.php?cd=1234.

Caballero, Ricardo and Mohamad Hammour, 2005, “The Cost of Recessions Revisited: A Reverse-Liquidationist View.” Review of Economic Studies, Vol. 72 (April), pp. 313–341.

Caballero, Ricardo, and Arvind Krishnamurthy, 2002, A Dual Liquidity Model for Emerging Markets. American Economic Review, Papers and Proceedings, Vol. 92 (May), pp. 33–37.

Caballero, Ricardo, and Guido Lorenzoni, 2006, “Persistent Appreciations, Overshooting, and Optimal Exchange Rate Interventions,” (unpublished; Cambridge, Massachusetts, Massachusetts Institute of Technology, October). Available via the Internet: http://www.mit.edu/centers/wel/conference/version3_112906_rc.pdf.

Calvo, Guillermo, Alejandro Izquierdo, and Ernesto Talvi, 2006, “Phoenix Miracles in Emerging Markets: Recovering Without Credit from Systemic Financial Crises,” NBER Working Paper 12101 (Cambridge, Massachusetts, National Bureau of Economic Research, March).

Cline, William, 2005, The United States as a Debtor Nation (Washington, Institute for International Economics).

Devereux, Michael, and Charles Engel, 2006, “Expenditure Switching Versus Real Exchange Rate Stabilization: Competing Objectives for Exchange Rate Policy,” NBER Working Paper No. 12215. (Cambridge, Massachusetts, National Bureau of Economic Research, May).

Dornbusch, Rudiger, 1983, Real Interest Rates, Home Goods, and Optimal External Borrowing. Journal of Political Economy Vol. 91 (February), pp. 141–153.

Edwards, Sebastian, 2002, “Does the Current Account Matter?” In: Sebastian Edwards and Jeffrey Frankel (eds). Preventing Currency Crises in Emerging Markets, (Chicago, University of Chicago Press), pp. 21–75.

Krugman, Paul, 1987, The Narrow Moving Band, the Dutch Disease and the Competitive Consequences of Mrs Thatcher. Journal of Development Economics, Vol. 27, pp. 41–55.

Obstfeld, Maurice and Kenneth Rogoff 1996, Foundations of International Macroeconomics. (Cambridge, Massachusetts, MIT Press).

Additional information

*Olivier Blanchard is the Class of 1941 Professor of Economics at the Massachusetts Institute of Technology and a research fellow at the National Bureau of Economic Research. This paper is adapted from the Mundell-Fleming lecture given at the IMF in November 2006. The author thanks Ricardo Caballero, Francesco Giavazzi, Guido Lorenzoni, Andrei Shleifer, Roberto Rigobon, and Jose Tessada for comments and discussions, and Tatiana Didier for excellent research assistance.