Abstract

This study examines the performance of equity market neutral (EMN) hedge funds by estimating alpha and beta, using monthly excess returns of the Fidelity Investments Spartan® US Bond Index Fund, the S&P 500 index and two indices of EMN strategies. The study investigates how much exposure to systematic risk is experienced by EMN hedge funds and hence by the investors in such funds. In addition, the article ascertains the stability of the estimated betas of EMN hedge fund indices. Results show that EMN fund indices had no systematic (stock and bond market) risk before the subprime mortgage crises of 2008. During the crises, the DJ Credit Suisse EMN index showed a positive beta in excess of 0.4, yet the Greenwich Van Hedge EMN index showed a beta less than 0.1. Similarly, the DJ Credit Suisse EMN index had no bond market beta up until November 2008. The Greenwich Van Hedge EMN index had almost no exposure to the market. The results were sensitive to market conditions and the EMN index. DJCS and GVH both had positive stock market alphas, which turned insignificant around October 2008. Similarly, both indices had positive bond market alphas, which turned insignificant around August–November 2008.

Similar content being viewed by others

INTRODUCTION

The objective of this study is to investigate the performance behavior characteristics of indices representing the equity market neutral (EMN) hedge fund strategy over the period January 1995 – January 2012. The focus is on analyzing the exposure that EMN hedge funds have to US equity and bond markets.Footnote 1

The EMN strategy is to have minimal and ideally no exposure to the risk generated by the market. Its objective is to provide returns that are neither aided nor hindered by movements in the market. This does not mean that EMN strategies are not volatile or without absolute risk, but rather that the volatility is not due to volatility in the market. In addition, EMN funds claim to produce returns that have less risk than the returns generated by the market, and in fact, in terms of risk, are more like bonds rather than equities.

Since the establishment of the first hedge fund, the industry has seen massive growth both in terms of number of funds available and assets under management. Table 1 shows the growth of EMN hedge funds from 1997 to the first quarter of 2012.

By using an EMN hedge fund index as a proxy for the performance of a ‘normal’ or ‘garden variety’ EMN hedge fund and the S&P 500 index as a proxy for the broad-based US equity markets, the beta for the EMN hedge fund is estimated using simple linear regression. The data cover the period January 1995 –October 2012, which encompasses periods of bull, bear and crises markets. The betas of two independent EMN hedge fund indices, Dow Jones Credit Suisse and Greenwich Van Hedge, are estimated by regressing each index's returns against the monthly returns of the S&P 500 index. If the beta for the EMN hedge fund indices is close to or equal to zero, then by definition we conclude that exposure to systematic risk is not present or is negligible. Linear regression on the data set over the entire period shows a static snapshot of the EMN indices’ beta estimate over a 17-year period. However, when beta is estimated for the indices using monthly returns for rolling 60-month periods, a more dynamic situation emerges. A critical outcome is the stability of betas of the indices over time.

This article also analyzes the claim that EMN hedge funds produce equity-like (level of) returns with bond-like risks (standard deviation). By using the Fidelity Investments Spartan® US Bond Index Fund1 as a proxy for the US bond market, comparison of the two indices highlights the similarities and differences.

The next section presents literature review. The hypotheses for market risk neutrality and performance are developed in the section after that. The subsequent section presents both the methodology and the data used for this research. The empirical results are discussed in the penultimate section. The final section discusses the conclusions drawn from the research.

LITERATURE REVIEW

Research focused on hedge fund performance generally falls into a few broad categories. The first category encompasses studies comparing and contrasting hedge fund performance to that of various indices, such as Ackermann et al (1999), Liang (1999) and Capocci and Hubner (2004). The second category offers comparisons of hedge fund performance to that of mutual funds, as studied by Ackermann et al (1999) and Liang (1999), who conclude that hedge funds, as a group, perform better than mutual funds on a risk-adjusted basis. Finally, research to analyze, define and categorize hedge fund investment styles and performance. Edwards and Caglayan (2001) find that market neutral hedge fund strategies as well as event-driven and macro hedge fund strategies are the only ones to provide protection to investors in down trending markets.Ennis and Sebastian (2003) find that after the stock market peaked in March of 2000 hedge funds in general did not provide protection to investors; rather it was the managers’ good timing of the market. Muhtaseb (2003 and 2006) discusses the merits of hedge funds like investing versus long only investing.

The strategy aims at balancing long and short positions to ensure zero or negligible market exposure and consequently a performance pattern that is independent of market movements (Lhabitant, 2002). As more factors are hedged away, the opportunity set for the manager to add value is reduced. In theory, a perfectly hedged portfolio should yield the risk-free rate minus transaction costs. In practice, as the portfolio is not hedged against some residual factors, the strategy could yield returns above the T-bills, but with much less risk than unhedged positions and with a potentially lower correlation to the market (Lhabitant, 2002). EMN hedge funds have provided returns approximately equal to those of broad indexes while assuming much less risk than a portfolio of common stocks (McCrary, 2005). Market neutral investing has a major disadvantage with respect to other long/short strategies. It requires an increased number of transactions to maintain the hedged (no exposure to the market) position. These transactions are costly, and they have potential consequences in terms of undesirable tax effects for hedge fund investors (Lhabitant, 2002).

There are several motivations for this research. First, several studies suggest that market neutral hedge funds represent a large percentage of the hedge funds operating in the industry. Capocci and Hubner (2004) and Capocci et al (2003) report that as much as 28.3 per cent of hedge funds employ a market neutral strategy. Second, most hedge funds in general do have exposure to the market. Results from several research articles that focus on all hedge funds as a group may not fully apply to EMN hedge funds or other individual strategies. EMN hedge funds have a specific objective, which is to deliver alpha while simultaneously hedging (removing) the fund's exposure to the general market. Capocci et al (2003) studied a database of 2894 individual funds and proposed that EMN hedge funds should be further studied due to their unique and interesting characteristics. A growing number of researchers are looking at individual hedge fund strategies for the focus of their research in order to understand the unique characteristics of the various individual strategies. Fung and Hsieh (2002) focus on fixed income arbitrage funds in their research, Mitchell and Pulvino (2001) concentrate their studies on risk arbitrage, and Gatev et al (1999) study relative value hedge funds on a stand-alone basis. Further investigation of the EMN hedge fund strategy on a stand-alone basis provides for a greater understanding of the strategy's individual particularities. Navone (2001) looked at the diversification benefits of the addition of EMN hedge funds to a portfolio of mutual funds and found that the inclusion of EMN hedge funds in a portfolio would significantly improve the risk-return tradeoff, but did not look into the neutrality of the funds. Finally, few researchers have studied the performance of hedge funds through bear markets. The 17-year period of data employed in this study includes the bear markets starting in March 2000 caused by the bursting of the Internet bubble, the post-9/11 market and the collapse of the sub-prime markets in the later part of 2007.

Brooks and Kat (2001) found that EMN hedge funds did not exhibit a high correlation with the equity markets. Other strategies showed a low and typically negative correlation to the bond markets, but EMN funds were an exception. They suggest that this could be due in part to the high degree of leverage employed in the EMN strategy. They also report that the correlations of all hedge fund strategies among each other are high in all but the EMN strategy, reasoning that other strategies share a high degree of similarity of exposure to systematic risk. In addition, EMN funds exhibit standard deviations that are lower than the bond markets but mean returns that are higher.

HYPOTHESES

This research tests three hypotheses regarding the performance of EMN hedge funds.

Hypothesis 1:

-

EMN hedge funds are market neutral, and the neutrality is stable

EMN hedge funds aim to produce returns that are independent of the returns of the market. The beta of a security is generally considered a measure of that security's exposure to the market risk. It is illustrated in the following equation:

where R EMN=rate of return from the EMN index; R Free=riskless rate of return proxied here by the T-bill rate; β=beta or systematic risk; R Index=rate of return from the S&P 500 index or bond market index; and α=alpha or the manager's value added; if β=0 then the excess returns will equal alpha plus an error term. R EMN=α+e; e=error term.

Therefore, EMN hedge funds would aim to have a beta that is as close to zero as possible. If the beta is zero, implying that the EMN funds do not earn returns by taking on market exposure, then the return that remains is alpha, which reflects the portfolio manager's ability to earn a return independent of the overall market movement.

Simple linear regression, run on the available monthly returns over the 17-year period of this study, shows a snapshot of the fund's beta over this time frame. The results (single regression model) of the entire 17-year period model are of limited value because they do not show how the beta of the strategy changes over time.

By examining beta using a rolling 60-month time frame we can observe the movement or shift in beta over time. The first 60-month period covers January 1995 through December 1999. Monitoring the strategy index beta in this way not only provides a much more dynamic full view of the monthly fluctuations of beta, but also allows us to observe the change in beta as the economic and market conditions change. The effects of a shift in market direction can be captured more precisely.

Hypothesis 2:

-

EMN hedge funds provide better returns than the broad-based US equity market indices

EMN hedge funds claim to provide returns that are better than the broad market indices. To evaluate this claim, the returns of the S&P 500 index and the Spartan US Bond Index Fund are compared on an absolute and risk-adjusted basis with those of the DJ Credit Suisse and Greenwich Van Hedge EMN indices.

Simply producing returns that are higher than the market index may be misleading. Consistency of returns is also important to investors in these investment vehicles. Many hedge funds are not as liquid an investment as purchasing an index fund. It is necessary to assume a longer-term holding period in order to better compare the returns. Periods of both bull and bear markets have occurred over the 17-year period studied, and provide a good environment to determine whether this claim can be supported.

Hypothesis 3:

-

EMN hedge funds exhibit risk characteristics that are closer to those of bonds than equities

EMN fund managers assert that the level of risk to which investors in their funds are exposed is comparable to that of the bond market more so than that of the stock market. By regressing the monthly returns of each of the two EMN indices against the monthly returns of the Spartan US Bond Index Fund, we estimate the bond market beta for each of the two EMN hedge fund indices. If EMN hedge funds were to have bond-like risk then this would be reflected in the significance of the beta estimate.

RESEARCH METHODS

The data Footnote 2

The EMN hedge fund index monthly returns are obtained from Greenwich Van Hedge Alternative Investments L.L.C. (www.greenwichai.com) and Dow Jones Credit Suisse (www.hedgeindex.com). The returns of both the Greenwich Van Hedge and Dow Jones Credit Suisse indices are updated and published monthly for the period January 1995 – January 2012. These indices are limited to hedge funds domiciled in the US and are reported ‘net of fees’. The EMN index returns are evaluated against the S&P 500 monthly returns and the Spartan US Bond Index Fund.

The S&P 500 index monthly returns for the period January 1995 – January 2012, the monthly returns of a 1-year T-bill, and the monthly returns of the Spartan US Bond Index Fund over the period July 1996 – October 2012 are used to observe the risk similarities with the EMN indices. These represent the returns of the broad US equity and bond markets and the risk-free rate of return. This time frame encompasses periods of both bull and bear markets, providing the opportunity to observe performance characteristics of the EMN strategy over the short-term, long-term, bear and bull markets.

This research uses the S&P 500 index as a proxy for the returns of the US stock market. The S&P 500 index and 1-year Treasury bill monthly rates of return are obtained from www.standardandpoors.com and the Federal Reserve (www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=billrates), respectively. The data for the Spartan US Bond Index Fund are available on www.Fidelity.com.

Risk exposure and measurement

Beta

This research estimates the beta of the EMN index using two simple linear regressions, one against the S&P 500 index and another against the Spartan US Bond Index Fund monthly returns. The slope of the regression is beta. Estimating beta using the 60-month periods shows the monthly changes in beta over rolling 5-year periods. The beta of a security is generally considered a measure of that security's exposure to the market risk. It is illustrated in the following equation:

Therefore, EMN hedge funds would aim to have a beta that is as close to zero as possible. If the beta is zero then the return that remains is alpha or the portfolio manager's ability to identify and exploit mispricing, timing and varying exposure opportunities.

Sharpe ratio

Developed by William F. Sharpe in 1964, the Sharpe ratio measures the level of excess reward per unit of total risk taken (Sharpe, 1964). Originally dubbed the reward-to-variability ratio by Sharpe, the ratio gained in popularity but the name did not, and it has since become known as the Sharpe ratio.

The definition of the Sharpe Ratio is as follows:

where: x is the index or fund; R x is the average monthly rate of return of x; R f is the best available rate of return of a ‘risk-free’ security (that is cash); and StdDev(x) is the standard deviation of r x

Therefore, using the Sharpe ratio we can standardize the reward to risk of the various indices to determine the level of risk involved. Generally, a Sharpe ratio over 1 is considered good.

Alpha

Alpha is a measure of an investment's performance on a risk-adjusted basis. Alpha is the return above and beyond the required return commensurate with the level of systematic risk of the asset. Alpha is considered to represent the value that the portfolio manager has added or subtracted from the security's return. The equation for computing alpha is as follows:

EMN hedge funds should produce positive alpha demonstrating the returns that are attributed to the manager's performance and not the market's influence.

Methodology

To test Hypothesis 1, the beta of EMN hedge funds are estimated against the monthly returns of the S&P 500 index over the 17-year period, January 1995 – January 2012. This research estimates the beta of the EMN hedge funds over rolling 60-month periods in order to determine how stable EMN funds are in terms of market risk exposure, as well as to observe the behavior in changing market conditions. Monthly returns are employed to calculate 60-month rolling betas.

Hypothesis 2 is tested by estimating the beta, alpha and standard deviation of the EMN hedge fund indices. This gives three different measures with which to evaluate the performance of EMN hedge funds against the broad market index to determine whether the funds in fact produce better returns than the broad stock market index.

Hypothesis 3 is tested by using the same regression methods as above, but instead the EMN indices risk measures are compared to those of the Spartan US Bond Index Fund. As the index fund used is the aggregate of all US bonds, there are investment grades, as well as high-yield or junk bonds, included in the index. Alpha and beta estimates over rolling 60-month periods as well as the returns of the EMN hedge funds are compared to those of a bonds index.

EMPIRICAL RESULTS

For the entire 17-year period January 1995 – October 2012, beta was 0.195 for the DJ Credit Suisse and 0.036 for the Greenwich Van Hedge Index when regressed against the S&P 500 index. These results are presented in Tables 2 and 3. This level of beta shows that the EMN strategy has a minimal yet statistically significant exposure to stock market risk.

These beta estimates are significant with a t-stat of 4.36 for DJ Credit Suisse and 2.03 for Greenwich Van Hedge. The R-squared is 8.5 per cent for DJCS and 2.0 per cent for GVH, indicating that more than 90 per cent of the risk of the equity market strategy index is not accounted for by the overall stock market movement. Over the long term, EMN as a strategy managed to deliver returns that have minute exposure to the stock market.

Tables 2 and 3 also illustrate alpha estimates for both the DJ Credit Suisse and the Greenwich Van Hedge indices. The alpha estimate for the DJ Credit Suisse index is not significant, yet the alpha of the Greenwich Van Hedge index is very significant. For the DJ Credit Suisse Index the estimated alpha is almost zero and the Greenwich Van Hedge index alpha is estimated at 0.45 per cent per month (t-stat is 5.62). This translates into an annualized alpha estimate of 5.4 per cent. On the basis of the results of Greenwich Van Hedge estimates, EMN hedge fund managers are producing positive annual returns to investors independent of the stock market's performance and in excess of the risk-free rate of return.

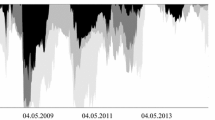

Figures 1 and 2 graphically illustrate the 60-month rolling betas for the two EMN indices. The shaded areas are bear market periods. When we look at the rolling beta over the period January 2000 – January 2012, we see that beta does in fact fluctuate but over a small range, up until the recent economic crises that started in 2008. Narrow ranges are used in order to capture the initial 60-month results, after which each month a new regression is run and the results are plotted to show any variation in the estimated value of beta. In the first two bear market periods, March 2000 – September 2001 and January 2002 – October 2002, the rolling beta estimates of both indices are significant yet very small. The static (long-term) beta is 0.195.

Graphic illustration of DJ Credit Suisse 60-month rolling beta versus the S&P 500 index compared to the estimated static beta over entire 17-year period. Bear market periods are shown by the shaded areas.1. March 2000 – September 2001,2. January 2002 – October 2002,3. August 2007 – February 2009.

Graphic illustration of Greenwich/Van Hedge index 60-month rolling beta versus the S&P 500 index compared to the estimated static beta over entire 17-year period. Bear market periods are shown by the shaded areas.1. March 2000 – September 2001,2. January 2002 – October 2002,3. August 2007 – February 2009.

Figure 3 shows a plot of the 60-month rolling beta estimates of the Greenwich Van Hedge and DJ Credit Suisse EMN hedge fund indices when regressed against the S&P 500 index. The exposures of the two indices to the market differ materially. The beta for the DJ Credit Suisse index spiked during the crises and remained at historically high levels (around 0.4), and did not decline afterwards, unlike the beta of the GVH index.

Comparison of rolling beta estimates of both the Greenwich Van Hedge and Credit Suisse Equity Market Neutral Hedge fund indices versus the S&P 500 index. Bear market periods are shown by the shaded areas. 1. March 2000 – September 2001, 2. January 2002 – October 2002, 3. August 2007 – February 2009.

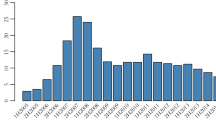

Examining the rolling alpha graphs more closely in Figures 4 and 5 we can see that on a long-term basis, alphas of both indices were trending downward. At the beginning of the millennium, DJ Credit Suisse's 60-month alpha estimate was approximately 0.7 per cent monthly or approximately 8.4 per cent annually and the Van Hedge Greenwich index was estimated at 1.24 per cent monthly or 14.88 per cent annually. Appendix A presents the alphas (versus the stock market) and betas of both indices for all rolling 60-month periods. As late as October 2008, the monthly alphas of DJ Credit Suisse and Greenwich Van Hedge were 0.3 per cent and 0.14 per cent, respectively. Around January 2009, the alphas of both indices were almost zero. In January 2012, monthly alpha decreased to −0.4 per cent monthly or −4.8 per cent annually for DJ Credit Suisse and zero for the Van Hedge Greenwich index.

Graph illustrating the movement in alpha for the DJ Credit Suisse Index over the period January 2000 – January 2012.

Graph illustrating the movement in alpha for the Greenwich Index over the period January 2000 –January 2012.

Return comparisons

Table 4 shows the average annual and monthly returns. The average annual total return for the EMN hedge funds is 9.68 per cent for the Van Hedge Greenwich Van Hedge index with an annualized standard deviation of 4.72 per cent. The annual return of the DJ Credit Suisse Index is 6.10 per cent with an annualized standard deviation estimate of 10.67 per cent. The S&P 500 or broad US market produced annual total returns of 7.45 per cent with a standard deviation of 15.93 per cent. The Spartan US Bond Index Fund had total average yearly returns of 6.04 per cent with a standard deviation of 3.51 per cent. The average annual risk-free rate of return was 3.97 per cent with a standard deviation of 0.45 per cent.

On a non-risk-adjusted basis, the GVH index outperformed the stock and bond markets. The DJCS index under-performed the stock market and performed as well as the bond market, over the period.

Table 5 shows the results for the excess returns. The average annual excess return for the EMN hedge funds is 5.58 per cent based the Greenwich Van Hedge index and a standard deviation of 4.02 per cent producing a Sharpe ratio of 1.39. The DJ Credit Suisse Index earned an excess return of 2.81 with a standard deviation equal to 10.57 per cent, yielding a Sharpe ratio of 0.27. The S&P 500 or broad US market produced annual excess returns of 4.17 per cent with a standard deviation of 15.89 per cent, offering a Sharpe ratio of 0.26. The Spartan US Bond Index Fund had average annualized excess returns of 3.54 per cent with a standard deviation of 3.55 per cent, delivering a Sharpe ratio of 1. At least one EMN index, Greenwich Van Hedge, outperformed the bond market and the stock market on a risk-adjusted basis. DJ Credit Suisse performed as well as the stock market but underperformed the bond market.

Table 6 shows correlation coefficients between the returns of each index. Both EMN indices show low positive correlations with the S&P 500 index. The DJCS correlation is 0.29 compared to 0.14 for GVH. Stock market correlations were higher than those of the bond market. The DJCS index correlation with the Spartan US Bond Index Fund is −0.22, different from that of the GVH index with the Spartan US Bond Index Fund, at 0.088. The fact that the correlations are different may reflect the different construction and index constitution methods of the two EMN indices.

Interestingly, both EMN indices enjoy higher correlations with the risk-free rate. This reflects the common practice of EMN hedge fund managers of targeting a return objective expressed as cash rate (risk-free rate) plus an incremental rate of return (risk premium).

Using average annual excess returns for all the indices as well as the standard deviations of those returns, a range of expected excess returns can be estimated. Table 7 displays the results of the 95 per cent confidence interval for the annual returns. The greatest range of monthly returns is, not surprisingly, that of the S&P 500 with excess returns ranging from 1.99 per cent to 6.34 per cent, a range of over 4.35 per cent. GVH returns range is 1.10 per cent, from 5.03 per cent to 6.13 per cent, whereas for the DJCS the range is greater at 2.90 per cent, from 1.37 per cent to 4.26 per cent. Over long holding periods, EMN hedge funds produce returns that are on average more stable than those the S&P 500 index. Average annual excess returns of 5.58 per cent and 2.81 per cent for the Greenwich Van Hedge and Credit Suisse indices, respectively, surround the average annual excess returns of the S&P 500 index of 4.17 per cent. The Spartan US Bond Index Fund shows that excess returns stretch from 2.96 per cent to 4.12 per cent with a range of 1.16 per cent.

The ranges of excess returns of EMN hedge fund indices are greater than those of the bond market index yet smaller than those of the stock market index. The return ranges present a similar picture to that of the Sharpe ratios. The excess returns show that in general EMN strategy delivers returns at least as high as those of the stock market but with significantly lower risk, more comparable to that of the bond market.

Neutrality to the bond market

Figure 6 shows the monthly excess returns for the Spartan US Bond Index Fund and the two EMN hedge fund indices. The excess returns of the two EMN indices displayed large swings before the dot com bubble burst in 2000 and during the recent economic crises of 2008–2009. Otherwise the EMN indices produced excess return ranges similar to those of the US bond market index.

Excess monthly returns of the Spartan US Bond Index Fund compared to the DJ Credit Suisse and Van Hedge Greenwich EMN Indices over the period July 1996 – January 2012.

Tables 8 and 9 show the estimated beta of the DJ Credit Suisse index against the Spartan US bond index to be −0.71 (t-stat −3.15), and for the Greenwich Van Hedge versus the Spartan US Bond Index Fund the beta estimate is 0.025 (t-stat 0.27). Obviously the results are not consistent across the two EMN indices. DJ Credit Suisse has a significant negative exposure to the bond market, yet Greenwich Van Hedge shows no exposure to the bond market. This brings up the issue of the different index construction methods. The stock market betas were 0.195 and 0.035 for DJCS and GVH, respectively. DJCS appears to have a relatively high negative bond market beta and a low positive stock market beta. Yet GVH index has no bond market exposure and very low and significant stock market beta.

Again, the alpha estimates of the two EMN indices are not consistent. For the entire period, the DJ Credit Suisse index produced a monthly alpha estimate of 0.0038 or 0.38 per cent (t-stat 1.6) versus the Spartan US Bond Index Fund. As reported in Appendix B, the 60-month rolling alphas were positive and significant through October 2008. Results for the Greenwich Van Hedge index against the Spartan US Bond Index Fund produced monthly alpha estimates of 0.44 per cent (t-stat 4.51) monthly or 5.28 per cent annually. The alpha is sensitive to the prevailing market conditions. As shown in Table B1, beginning in August 2008, the 60-month rolling alpha lost statistical significance. Before August 2008, all the alphas of both EMN indices were statistically significant and sizable, ranging from 0.5 per cent to 1.0 per cent per month.

SUMMARY AND CONCLUSIONS

The primary objective of this article is to determine whether hedge funds’ claim of market neutrality and independence from market movements is true. This study also investigates the ability of EMN hedge funds to produce returns that are higher than the (stock and bond) market index, along with risk characteristics similar to those of a bond market index. The time span of the study encompasses both bull and bear markets, including the bursting of the dot com bubble, the post-September 11, 2001 markets, and most recently and ongoing the sub-prime mortgage meltdown.

The forte of EMN hedge funds is to remain neutral and independent from broad market influences. Estimating rolling monthly betas allows for a better understanding of the effects of market changes on the funds and the exposure as the market changes. Examining the neutrality of EMN hedge funds reveals that the EMN hedge fund strategies, over the long term, maintain an independent exposure to the (bond and stock) market up until the beginning of the economic recession (September 2008) triggered by the subprime mortgage crises.

The exposure that is observed is in certain periods statistically significant, yet very small, as shown in Tables A1 and B1. Before the subprime mortgage crises, rarely was the estimated stock of DJCS beta greater than 0.10. In November 2008, the stock market beta went up from 0.08 to 0.42. DJCS stock market beta did not decline subsequently, yet the beta of GVH returned to almost zero within 6 months and eventually turned statistically insignificant. Similarly, the bond market betas demonstrated comparable shifts in exposure. Dow Jones Credit Suisse 60-month rolling bond market beta went up from an insignificant 0.0051 in November 2008 to a huge and very significant −1.96 and stayed at that level through January 2012. Interestingly, Greenwich Van Hedge bond market beta was insignificant throughout the period, except in September 2008 when the beta was 0.33 and significant.

These results send an alert to EMN strategy investors. Although the strategy maintains a neutral exposure to the stock market, the neutrality diminishes significantly during a crises market environment, based upon the DJCS index. EMN strategy exposure to the bond market is also sensitive to the EMN index selected. Investors must carefully vet an EMN fund and the EMN index selected to evaluate risk exposures. The results do vary across the two indices, DJCS and GVH. Investors are advised to carefully evaluate the construction and constitution methods of the available indices to make sure that the indices conform to the true structure of an EMN strategy.

Investors with portfolios consisting solely of EMN hedge funds have experienced returns that on average outperformed the S&P 500 index, over the period of the study, based on the results of the GVH index. The DJCS index did not outperform the S&P 500 index on an absolute basis. On a risk-adjusted basis, both indices performed as well as the S&P 500 index (DJCS) or better (GVH).

Using monthly and annual percentage returns, this study also shows that EMN hedge funds do in fact perform better than the broad market over the entire period of study. This does not necessarily mean that an investment in an EMN hedge fund will generate returns that beat the market in any single year. The overall advantage of EMN hedge funds is that in periods of bear markets they produce absolute returns that are less negative than the market index. It is for this reason that investment in these funds should be for longer holding periods. EMN hedge funds are better utilized as an addition to a diversified portfolio to aid in periods when the market conditions are unstable.

In conclusion, the EMN hedge fund strategy does maintain a neutral or negligible exposure to systematic risk during normal and economic crises-free periods. The neutrality fluctuates as the market conditions change and the exposure to market risk increases during bear market periods. Although fund managers are producing positive alpha, the alpha produced decreased over the period studied. Stock market alphas turned negative and insignificant for DJCS and small yet positive for GVH. These findings agree with those of Capocci et al (2003) that EMN funds produce alpha while simultaneously hedging the exposure to the general market. Standard deviations of the EMN indices’ monthly excess returns are split above and below that of the bond market, which contrasts with the findings of Brooks and Kat (2001) that EMN hedge funds have higher excess returns and lower standard deviations than the bond markets. The EMN monthly excess returns are higher than those of the bond index, in line with the findings of Brooks and Kat (2001). Our results confirm and extend those of Lo and Mueller (2010), which demonstrate large returns during the mid-1990s that significantly decline over time. The average returns and Sharpe ratios of statistical arbitrage decline steadily from 1995 through 2007.

Based on our results of the two EMN indices, GVH seems to be the more market neutral fund index. Table 10 shows for the entire period, GVH had lower stock and bond market betas. DJCS exhibited greater sensitivities to the stock market (0.2) and the bond market (−0.71). GVH also earned sizable and significant alphas against stock and bond market indices. DJCS alphas are essentially zero against stock and bond market indices, whereas GVH alphas exceed 40 basis points a month. These findings point toward the urgency of studying the different index construction methods utilized by the different index vendors.

Notes

Spartan US Bond Index Fund was ‘Formerly known as the Fidelity® US Bond Index Fund’.

The authors thank the providers of the data used in this research.

References

Ackermann, C., McEnally, R. and Ravenscraft, D. (1999) The performance of hedge funds: Risk, return, and incentives. Journal of Finance 54 (3): 833–874.

Brooks, C. and Kat, H.M. (2001) The statistical properties of hedge fund index returns and their implications for investors. Journal of Alternative Investments 5 (2): 26–44.

Capocci, D., Corhay, A. and Hubner, G. (2003) The Performance of Hedge Funds in Bull and Bear Markets. University of Liege. Working Papers.

Capocci, D. and Hubner, G. (2004) An analysis of hedge funds performance. Journal of Empirical Finance 11 (1): 55–89.

Edwards, F. and Caglayan, M. (2001) Hedge fund performance and manager skill. Journal of Futures Markets 21 (11): 1003–1028.

Ennis, R. and Sebastian, M. (2003) A critical look at the case for hedge funds. Journal of Portfolio Management 29 (4): 103–112.

Fung, W. and Hsieh, D.A. (2002) The risks in fixed income hedge fund styles. Journal of Fixed Income 12 (2): 6–27.

Gatev, E., Goetzmann, W. and Rouwenhorst, K. (1999) Pairs Trading: Performance of a Relative Value Rule. Yale School of Management. Working paper.

Lhabitant, F.-S. (2002) Hedge Funds: Myths and Limits. West Sussex, UK: John Wiley & Sons.

Liang, B. (1999) On the performance of hedge funds. Financial Analysts Journal 55 (4): 72–85.

Lo, A. and Mueller, M.T. (2010) Warning: Physics envy may be hazardous to your wealth! Journal of Investment Management 8 (2): 13–63.

McCrary, S.A. (2005) Hedge Fund Course. Hoboken, NJ: John Wiley & Sons.

Mitchell, M. and Pulvino, T. (2001) Characteristics of risk in risk arbitrage. Journal of Finance 56 (6): 2315–2375.

Muhtaseb, M. (2003) To outperform the market, get out of it! Journal of Wealth Management 5 (2): 66–74.

Muhtaseb, M. (2006) A thought or two for mutual funds. Journal of Investing 15 (1): 9–15.

Navone, M. (2001) Diversifying Market Risk through Market Neutral Strategies. IEIF Bocconi University. Working paper.

Sharpe, W.F. (1964) Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance 19 (3): 425–442.

Author information

Authors and Affiliations

Corresponding author

Appendices

Rights and permissions

About this article

Cite this article

Muhtaseb, M., Colborn, R. Neutrality of equity market neutral strategy to period and index. J Deriv Hedge Funds 18, 301–332 (2012). https://doi.org/10.1057/jdhf.2012.13

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jdhf.2012.13