Abstract

Long-term investments such as Private Equity (PE), present timing differences in cash inflows and outflows. When allocations in PE are not planned correctly, investors can suffer liquidity problems when paying for unexpected commitments. We present a multistage stochastic optimization model that includes PE assets as free cash flows projects. This model can determine PE allocations, in relation to public equity, under different market settings. Using a factor-based model to construct public and private equity markets, the major findings are: Liquidity problems can be avoided by planning PE allocations in advance and according to market conditions. Our tool reduces commitments taken for more volatile PE market or when investor target is lower. For target returns above 20 per cent, PE allocations enhance portfolio annual returns from 2 to 3 per cent (no volatility increase) only if PE net present value volatility is below 15 per cent. Beyond this point, higher returns comes with more risk. When PE investments are less correlated with public equity, the latter threshold extends to 45 per cent. PE allocation weight changes in time and according to its age. For favorable market conditions and high investors’ appetite, PE investment value can be greater than the entire wealth at some time periods. Leverage option for PE investments decreases performance, even in low PE volatility market. Potential PE gains are offset by debt interest payments and risk becomes higher.

Similar content being viewed by others

Notes

Societe Generale Index www.sgindex.com/Data since 2004.

References

Ang, A. and Sorensen, M. (2012) Risks, returns, and optimal holdings of private equity: A survey of existing approaches. The Quarterly Journal of Finance 2 (3): 1250011.

Bae, G.I., Kim, W.C. and Mulvey, J.M. (2014) Dynamic asset allocation for varied financial markets under regime switching framework. European Journal of Operational Research 234 (2): 450–458.

Ben-Tal, A., Margalit, T. and Nemirovski, A. (2000) Robust modeling of multistage portfolio problems. In: H. Frenk, K. Roos, T. Terlaky and S. Zhang (eds.). High Performance Optimization, Gewerbestrasse, Switzerland: Springer, pp. 303–328.

Birge, J.R. and Louveaux, F. (2011) Introduction to Stochastic Programming, New York: Springer.

Bygrave, W.D. and Timmons, J.A. (1992) Venture Capital at the Crossroads, Boston, Massachusetts: Harvard Business Press.

Chen, P., Baierl, G.T. and Kaplan, P.D. (2002) Venture capital and its role in strategic asset allocation. The Journal of Portfolio Management 28 (2): 83–89.

Cumming, D., Helge Hafi, L. and Schweizer, D. (2012) Strategic asset allocation and the role of alternative investments. European Financial Management 20 (3): 521–547.

Dantzig, G.B. and Infanger, G. (1993) Multi-stage stochastic linear programs for portfolio optimization. Annals of Operations Research 45 (1): 59–76.

Ennis, R.M. and Sebastian, M.D. (2005) Asset allocation with private equity. The Journal of Private Equity 8 (3): 81–87.

Gompers, P. and Lerner, J. (2001) The venture capital revolution. Journal of Economic Perspectives 15 (2): 145–168.

Harris, R.S., Jenkinson, T. and Kaplan, S.N. (2014) Private equity performance: What do we know. The Journal of Finance 69 (5): 1851–1882.

Hellmann, T. and Puri, M. (2002) Venture capital and the professionalization of start-up firms: Empirical evidence. The Journal of Finance 57 (1): 169–197.

Hilli, P., Koivu, M., Pennanen, T. and Ranne, A. (2007) A stochastic programming model for asset liability management of a Finnish pension company. Annals of Operations Research 152 (1): 115–139.

Kallberg, J.G. and Ziemba, W.T. (1983) Comparison of alternative utility functions in portfolio selection problems. Management Science 29 (11): 1257–1276.

Kaplan, S.N. and Schoar, A. (2005) Private equity performance: Returns, persistence, and capital flows. The Journal of Finance 60 (4): 1791–1823.

Klier, D.O. (2009) Introduction to the private equity industry and the role of diversification. In: Managing Diversified Portfolios, Heidelberg: Physica-Verlag, pp. 53–95.

Lamm, Jr R.M. and Ghaleb-Harter, T.E. (2001) Private equity as an asset class: Its role in investment portfolios. The Journal of Private Equity 4 (4): 68–79.

Ling, L. (2010) Portfolio Management for Private and Illiquid Investments, Princeton, NJ: Princeton University.

Ljungqvist, A. and Richardson, M. (2003) The cash flow, return and risk characteristics of private equity. National Bureau of Economic Research. Cambridge: Technical report.

Loos, N. (2006) Value Creation in Leveraged Buyouts, Deutscher Universitätsverlag.

Maranas, C., Androulakis, I., Floudas, C., Berger, A. and Mulvey, J. (1997) Solving long-term financial planning problems via global optimization. Journal of Economic Dynamics and Control 21 (8): 1405–1425.

Mulvey, J.M., Simsek, K.D., Zhang, Z., Fabozzi, F.J. and Pauling, W.R. (2008) Or practice-assisting defined-benefit pension plans. Operations Research 56 (5): 1066–1078.

Mulvey, J.M. and Vladimirou, H. (1992) Stochastic network programming for financial planning problems. Management Science 38 (11): 1642–1664.

Opler, T. and Titman, S. (1993) The determinants of leveraged buyout activity: Free cash flow vs. financial distress costs. The Journal of Finance 48 (5): 1985–1999.

Phalippou, L. and Gottschalg, O. (2009) The performance of private equity funds. Review of Financial Studies 22 (4): 1747–1776.

Welch, K.T. (2014) Private equity’s diversification illusion: Economic comove-ment and fair value reporting. Rochester, NY: Social Science Electronic Publishing location.

Ziemba, W.T. (2009) Use of stochastic and mathematical programming in portfolio theory and practice. Annals of Operations Research 166 (1): 5–22.

Ziemba, W.T. and Vickson, R.G. (2014) Stochastic Optimization Models in Finance, Singapore: World Scientific Publishing Co. Pte. Ltd.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix A

Problem size

The model has  nodes. There are 2N=2(MT+1−1)/(M−1) variables for Dn and Wn, MT variables for MDDn,

nodes. There are 2N=2(MT+1−1)/(M−1) variables for Dn and Wn, MT variables for MDDn,  variables for public assets (with cash) and only I variables for PE investments. So there is no difference in complexity when considering PE investment or not. Finally there are 2MT variables for the excess y and Z used to measure the utility function.

variables for public assets (with cash) and only I variables for PE investments. So there is no difference in complexity when considering PE investment or not. Finally there are 2MT variables for the excess y and Z used to measure the utility function.

To calculate the number of constraints, notice that each node has M childs. So the total number of constraints in (3) and (5) are  The number of constraints for (4) and (6) is L+1, while (7) is MT. The number of constraints in (8) and (9) is

The number of constraints for (4) and (6) is L+1, while (7) is MT. The number of constraints in (8) and (9) is  Finally, the number of constraints in (10) and (11) is (T+1)MT and

Finally, the number of constraints in (10) and (11) is (T+1)MT and

respectively. The constraints linked to the sign of the variables sum up to (3L+2)(MT−1)/(M−1)+I+2MT.

For the setting described in the section ‘Strategy construction, settings and measurements’ (M=2, L=10, I=1, T=10), the number of variables and constraints are 39 903 and 80 853, respectively:

Appendix B

Public equity market

Then:

Private equity market

Now:

Then:

Appendix C

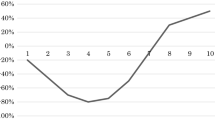

Using (14) and (15), Figure C1 shows the mean and volatility of public equity assets, for a particular factor matrix Ω with the setting given in the section ‘Rolling horizon procedure’. Table C1 shows the correlation between public equity returns and the single PE netflows, using different values of ρ1i given in (19).

Mean and volatility of public equity in factor-based model.

Rights and permissions

About this article

Cite this article

Reus, L., Mulvey, J. Multistage stochastic optimization for private equity investments. J Asset Manag 16, 342–362 (2015). https://doi.org/10.1057/jam.2015.20

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1057/jam.2015.20