Abstract

The underwriting cycle—the periodic swing in underwriting profitability in the insurance industry—has received considerable research attention. Studies have focused on causes of the cycle, whether there is truly a cycle, and the relationship between insurance company failure rates and the cycle. Little, if any, research, however, has focused on changes in underwriting practices over the course of the underwriting cycle. The current study considers three aspects of insurers’ underwriting strategy: (i) product concentration, (ii) geographic concentration, and (iii) focus on states with caps on general damages. Our analyses of the NAIC data show that all three aspects display trends that run opposite that of the combined ratio in medical malpractice insurance. During soft markets, which are characterised by low prices, low underwriting profitability and high loss ratios, insurers employ a looser underwriting strategy with lower product and geographic concentration, and less focus on safer states. We observe the use of a tighter underwriting strategy during hard markets, when loss ratios are low and prices and profitability are high. On the basis of observed associations between loss ratios and underwriting strategy, we also indirectly test the capital constraint theory and the risky debt theory. Our empirical results show that weakened capital bases at the firm level are associated with tighter underwriting.

Similar content being viewed by others

Notes

Boyer et al. (2012) and Boyer and Owadally (2015) argue that there is no evidence of predictability of cyclicality in insurers’ underwriting performance.

We follow the standard convention of referring to the periodic swings in underwriting profitability as the underwriting cycle, not because we contend that the swings are in fact cyclical, but because the terminology is widely used to refer to the ups and downs in underwriting profitability that occur over time.

One exception is Harrington et al. (2008), which reports excessive price-cutting in preceding soft markets may help explain subsequent hard markets.

The general liability (GL) insurance market has gone through similar cycles, but we focus on medical malpractice insurance for one major reason. The three measures of underwriting strategy we use in the paper are all line-specific, but GL is a combination of multiple lines. According to the NAIC categorisation of lines of business, product liability and other liability (including construction and alteration liability; contingent liability, contractual liability; elevators and escalators liability; errors and omissions liability, environmental pollution liability; excess stop loss, excess over insured or self-insured amounts and umbrella liability; liquor liability; personal injury liability; premises and operations liability; completed operations liability; and non-medical professional liability) together constitute general liability. Therefore, it is impossible to apply line-specific measures to the combination of multiple lines.

The underwriting cycle may be measured differently, but the majority of the literature focuses on underwriting profitability as an indication of the cyclical pattern. Therefore, we use the combined ratio, a commonly used measure of underwriting profitability, as a proxy to the underwriting cycle.

Whether the insurer is able to achieve its goal to limit loss exposures is a different matter, but here we focus on insurers’ choice, not realised outcomes, in our discussion of underwriting strategy.

Liebenberg and Sommer (2008) give a good summary of the competing hypotheses in the literature. The diversification discount hypothesis posits that diversification may increase operational and agency costs and thus reduces firm value. The conglomeration hypothesis holds that diversification can help enhance a firm’s financial performance through economies of scope and risk reduction.

See, for instance, Mayers and Smith (1994). The literature usually concludes that different organisational forms come with different comparative advantages that are suited for different lines of business. Stock insurers separate the functions of managers, owners (stockholders) and policyholders. Mutual companies on the other hand merge the owner and policyholder functions.

Such as lobbying for caps on general damages.

We recognise that underwriting strategy is a choice made by insurers. A tighter strategy does not necessarily lead to improved financial results, since each strategy has its benefits and costs. A greater product concentration may come with an informational advantage, but in the meantime, may lead to increased risk because of lack of diversification. However, such discussion is beyond the scope of this paper as we focus on how the underwriting strategy changes with the underwriting cycle.

Even when we consider all firms with positive premiums written in medical malpractice, half of the insurers write malpractice in less than four states.

Premium share is the firm’s malpractice premium in each state divided by its country-level total malpractice premiums.

Such firms’ premium shares also seem to move in opposite direction to the combined ratios, though not as closely as the percentage of the number of firms.

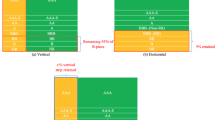

The correlations shown here reflect the relationships between annual median combined ratios and annual values of respective underwriting strategy proxies. For instance, from 1992 to 2010, we have 19 median combined ratios and annual median per cent values of malpractice premiums written. Table 5 shows the two categories of annual figures that have a correlation coefficient of −0.9022 with a P-value less than 0.0001.

Winter (1988, 1991, 1994); Gron (1994a, 1994b).

Gron (1994a, 1994b).

Firms with lower capacity tend to raise their prices over time (as predicted by the capital constraint theory), but given the same market conditions, firms in a stronger financial position charge higher prices (as predicted by the risky debt theory).

One may naturally ask how combined ratios and underwriting strategy affect each other. In this paper, we focus on their association and use it to derive our hypotheses. It is possible a two-way feedback exists. A looser underwriting strategy may increase loss ratios in the first place, which may then lead to tighten underwriting strategy in the next phase. However, such cause and effect is not what we set out to explore in this paper and remains a future research topic.

We also tried using year dummy variables in place of IndustrySurplus and found largely consistent results in terms of the sign and statistical significance of coefficients. Note that we cannot include IndustrySurplus and year dummies at the same time since it will then cause the model to be less-than-full rank.

For both industry capacity and firm-level capital, we use lagged variables to avoid a potential endogeneity problem.

Both absolute and relative capacity measures have been used in the literature. In addition to the absolute level of firm capital (FirmSurplus), we have also experimented with a relative capacity measure, premium-to-surplus ratio, which is a commonly used indicator of insurers’ capacity to underwrite new policies. A higher ratio signifies a lower level of capacity. When premiums increase without accompanying increases in surplus, an insurer’s capacity to write new policies is constrained. With the premium-to-surplus ratio replacing FirmSurplus and controlling for firm size (measured by the logarithm of admitted assets), we find largely similar results but worse fit for the data. The premium-to-surplus ratio does not show statistical significance in as many regression equations as FirmSurplus. When the ratio does exhibit statistical significance in certain scenarios, however, it displays the same effect on underwriting strategy variables as FirmSurplus. We chose to report results generated from FirmSurplus since it has the greatest explanatory power, but the results derived from the premium-to-surplus ratio are available from the authors upon request.

For instance, see Mayers and Smith (1994), and Fama and Jensen (1983a, 1983b).

For instance, we found several firms whose date of establishment is reported as a year that has not yet occurred, such as 2054.

We also ran pooled cross-sectional ordinary least squares (OLS) and the results are largely the same as those derived from fixed-effects models.

We cannot do fixed time effect models because one of our main independent variables, IndustrySurplus, is company-invariant. Its effect will be swept away by time-specific intercepts. The one-way fixed- and random-effects models allow intercepts to vary by company, with the latter also treating intercepts as random quantities. Frees (2004) points out that such company-varying intercepts can help account for potential heterogeneity.

SAS has a panel procedure specifically developed for modelling panel data, but it requires each cross-section to have at least two time points and each time point with at least two cross-section observations. Our data do not meet this condition, so we use two other different procedures (PROC GLIMMIX and PROC MIXED) to better fit our models.

See www.support.sas.com/documentation/cdl/en/statug/63033/HTML/default/viewer.htm#glimmix_toc.htm for more details of the GLIMMIX procedure. The Logistic procedure on the other hand is only good for running fixed-effects models.

See www.support.sas.com/documentation/cdl/en/statug/63033/HTML/default/viewer.htm#mixed_toc.htm for more details of the MIXED procedure. This procedure permits data that exhibit correlation and non-constant variability (or heteroscedasticity). It can handle both fixed- and random-effects models.

We tested for collinearity. All variance inflation factors (VIF) are smaller than 1.3. Since a VIF value greater than 10 is cause for concern, we can safely rule out collinearity concerns in our regression analyses. Results for intercepts are ignored in the table.

As one reviewer points out, Weiss (2007) states that the capital constraint theory does a better job explaining hard markets than soft markets. This might offer an insight into why we do not find supporting evidence for the sample period.

References

Boyer, M., Jacquier, E. and Van Norden, S. (2012) ‘Are underwriting cycles real and forecastable?’ Journal of Risk and Insurance 79(4): 995–1015.

Boyer, M. and Owadally, I. (2015) ‘Underwriting apophenia and cryptids: Are cycles statistical figments of our imagination?’ The Geneva Papers on Risk and Insurance—Issues and Practice 40(2): 232–255.

Cummins, J.D. and Danzon, P.M. (1997) ‘Price, financial quality, and capital flows in insurance markets’, Journal of Financial Intermediation 6(1): 3–38.

Cummins, J.D. and Outreville, J.F. (1987) ‘An international analysis of underwriting cycles in property-liability insurance’, Journal of Risk and Insurance 54(2): 246–262.

Doherty, N.A. and Kang, H.B. (1988) ‘Price instability for a financial intermediary: Interest rates and insurance price cycles’, Journal of Banking and Finance 12(2): 199–214.

Doherty, N.A. and Garven, J. (1995) ‘Insurance cycles: Interest rates and the capacity constraint model’, Journal of Business 68(3): 383–404.

Fama, E.F. and Jensen, M.C. (1983a) ‘Separation of ownership and control’, Journal of Law and Economics 26(2): 301–325.

Fama, E.F. and Jensen, M.C. (1983b) ‘Agency problems and residual claims’, Journal of Law and Economics 26(2): 327–349.

Frees, Edward W. (2004) Longitudinal and Panel Data: Analysis and Applications in the Social Sciences. Cambridge University Press, ISBN-13:978-0521535380ISBN-10: 0521535387.

Gron, A. (1994a) ‘Evidence of capacity constraints in insurance markets’, Journal of Law and Economics 37(2): 349–377.

Gron, A. (1994b) ‘Capacity constraints and cycles in property-casualty insurance markets’, Rand Journal of Economics 25(1): 110–127.

Harrington, S., Danzon, P.M. and Epstein, A.J. (2008) ‘“Crises” in medical malpractice insurance: Evidence of excessive price-cutting in the preceding soft market’, Journal of Banking and Finance 32(1): 157–169.

Lai, G.C., Witt, R.C., Fung, H.G., MacMinn, R.D. and Brockett, P.L. (2000) ‘Great (and not so great) expectations: An endogenous economic explication of insurance cycles and liability crises’, Journal of Risk and Insurance 67(4): 617–652.

Lei, Y. and Schmit, J. (2008) ‘Influences of organizational form on medical malpractice insurer operations’, Connecticut Insurance Law Journal 15(1): 53–84.

Liebenberg, A.P. and Sommer, D.W. (2008) ‘Effects of corporate diversification: Evidence from the property-liability insurance industry’, Journal of Risk and Insurance 75(4): 893–919.

Mayers, D. and Smith Jr. C.W. (1994) ‘Managerial discretion and stock insurance company ownership structure’, Journal of Risk and Insurance 61(4): 638–655.

Nordman, E., Cermak, D. and McDaniel, K. (2004) Medical Malpractice Insurance Report: A Study of Market Conditions and Potential Solutions to the Recent Crisis. Kansas City, MO: National Association of Insurance Commissioners.

Venezian, E. (1985) ‘Ratemaking methods and profit cycles in property and liability insurance’, Journal of Risk and Insurance 52(3): 477–500.

Viscusi, W.K. and Born, P.H. (2005) ‘Damages caps, insurability, and the performance of medical malpractice insurance’, Journal of Risk and Insurance 72(1): 23–43.

Weiss, M.A. (2007) ‘Underwriting cycles: A synthesis and further directions’, Journal of Insurance Issues 30(1): 31–45.

Weiss, M.A. and Chung, J. (2004) ‘U.S. reinsurance prices, financial quality, and global capacity’, Journal of Risk and Insurance 71(3): 437–467.

Winter, R.A. (1988) ‘The liability crisis and the dynamics of competitive insurance markets’, Yale Journal on Regulation 5(2): 455–500.

Winter, R.A. (1991) ‘Solvency regulation and the property-liability “insurance cycle”’, Economic Inquiry 29(3): 458–471.

Winter, R.A. (1994) ‘The dynamics of competitive insurance markets’, Journal of Financial Intermediation 3(4): 379–415.

Acknowledgements

The authors thank two anonymous reviewers for their insightful comments and suggestions, which helped greatly improve the article. Yu Lei gratefully acknowledges financial support from the Barney School of Business, University of Hartford.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Lei, Y., Browne, M. Underwriting Strategy and the Underwriting Cycle in Medical Malpractice Insurance. Geneva Pap Risk Insur Issues Pract 42, 152–175 (2017). https://doi.org/10.1057/gpp.2015.24

Published:

Issue Date:

DOI: https://doi.org/10.1057/gpp.2015.24