Abstract

This campaign demonstrates a core direct marketing principle. Citi International Personal Bank's Minimum Relationship Balance campaign acted on Pareto's principle to produce positive results in terms of both revenue and service delivery. The Bank conducted research on its client database and found that 60 per cent of its client base was contributing 96 per cent of its revenue; its problem was what to do with the remaining 40 per cent who were contributing only 4 per cent of revenue. One of the key issues for the Bank was that its less profitable clients were receiving the same top quality, and therefore expensive to the Bank, individual personal service as high-value clients. Addressing this issue meant that Citi International Personal Bank had to make some tough decisions about how to handle its less profitable client segments. The Minimum Relationship Balance campaign enabled the Bank to carefully divest itself of its unprofitable clients while maintaining its revenue. By aligning its client base, service proposition, acquisition target audience and brand, this campaign played a pivotal role in Citi International Personal Bank's long-term business strategy by creating a firm foundation for profitable growth in the future.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

illustrationCiti International Personal Bank is the offshore investment arm of Citi, one of the oldest and largest financial organizations in the world. Citi International Personal Bank offers international wealth management expertise to over two hundred million clients worldwide, and gives its clients access to investment products that may not be available to them in their home countries.

The Bank's clients are affluent people with diverse wealth management needs. To service each client's needs as effectively as possible, Citi International Personal Bank offers a high level of personal service; each client is allocated a dedicated Relationship Manager who speaks the client's language and shares their culture. All Relationship Managers are qualified to give investment advice.

In May 2008, as a result of a major brand repositioning exercise, in-depth database analysis and a customer-wide survey, Citi International Personal Bank realized that it couldn’t deliver on its high-quality brand and positioning. The crux of the problem was that a significant proportion of its client base didn’t correspond to its actual target market. Database analysis revealed that 40 per cent of its clients were worth only 4 per cent in terms of their total revenue contribution, yet these clients were receiving the same expensive Relationship Manager service as significantly higher-value clients.

Citi International Personal Bank had to find a way to focus its resources to enable it to deliver its high-quality one-to-one service proposition to its high-value client segment while simultaneously reducing its service costs to its comparatively low-value clients. It was clear that a comprehensive client value segmentation would need to be developed to drive campaign targeting and enable Citi International Personal Bank to manage its client relationships through clear effective communications tailored to each segment's needs.

Campaign background

Citi International Personal Bank's Relationship Managers are the channel through which it offers its wealthy international clients a dedicated investment service, unrivalled by any other competitor in its target market. Relationship Managers are recruited carefully and allocated to each client on the basis of a shared language, culture and geography. Citi International Personal Bank makes a sizeable financial investment in creating and delivering this unique one-to-one service, and, in order to maximize the profitability of this business model, the Bank's clients must be in the financial position to take advantage of a good proportion of the available investment services.

Early in 2008, Citi International Personal Bank launched its new business strategy, re-positioning its brand around its unique high-value Relationship Manager service proposition. In parallel with the process of clarifying and confirming its positioning, the Bank re-defined its target market. A high proportion of Citi International Personal Bank's 7,500 existing client base had the potential to make full use of the Relationship Manager service, including making the sizeable investments that create a win:win for the bank and its clients.

However, database analysis exposed a significant number of low-value client segments that simply didn’t require the Relationship Manager service; these clients had personal wealth management needs that could be well met by other departments within the Citi corporation. Clients in lower value segments were receiving the same levels of personal service as much higher-value clients (although clients with a balance below $25,000 were already being charged a $25 per month management fee). The Bank needed to match client value, service level and servicing cost with its brand positioning to ensure that its assets were being deployed most effectively, at the same time optimizing revenue by retaining as many profitable and potentially profitable clients as possible.

Following detailed analysis it was decided that, in order to qualify for the free Relationship Manager service, Citi International Personal clients would have to maintain a minimum balance of $100,000; clients with a lower balance would be charged a $50 per month ‘Relationship’ fee. The main challenge facing the Minimum Relationship Balance campaign was how to minimize the potentially massive negative impact on the Bank's revenue and brand of communicating these pragmatic business-based changes to affected clients.

Despite the inherently high and obvious risk of offending many of its wealthy clients, the Bank recognized that this campaign was a necessary stage in its long-term business strategy to achieve significant future growth in the high-tariff international investor target market. A renewed focus on high-value clients would allow Relationship Managers to concentrate on delivering a personal investment service to the high-value clients who most needed it and, thus, increase revenue.

Campaign objectives

The overall campaign objective was to reduce the number of low-value clients receiving the high-value Citi International Personal Bank Relationship Manager service by 75 per cent by end 2008 — without negatively impacting total business revenue.

The communication objectives for the campaign were:

-

to ensure that all existing clients were aware of the new minimum balance requirement and understood why Citi International Personal Bank was introducing it;

-

to clearly communicate the Bank's positioning to the target markets; and

-

to ensure that the project had, at worst, a neutral impact on business revenue.

An additional business objective was to increase each Relationship Manager's ability to deliver a sterling service, improving the longer-term capacity of Managers to maintain service levels after the planned expansion of its high-value client base. To support and drive its segment-driven campaign approach, the Bank also created segment-specific business and communication objectives.

Segmentation and targeting strategy

Citi International Personal Bank's sophisticated new segmentation approach, based on each client's actual and potential value, allowed the campaign's sometimes unwelcome messages to be communicated with great precision. Actual and potential value data, captured at the account opening stage, were used to create a profile for each segment:

-

Segment A — Affected clients who are likely to defect, some of whom may be able to increase their balances;

-

Segment B — Affected clients whom Citi International Personal Bank would like to stay and increase their balances;

-

Segment C — Unaffected clients with balances under $100,000 (see below); and

-

Segment D — Unaffected clients with balances over $100,000.

Segments A and B formed the most challenging and important target audiences for this campaign. How communication to these segments was handled would determine whether the campaign succeeded or failed in its goal of being, at worst, revenue neutral. The specific communication objectives for these two segments were:

-

to reduce the number of clients Citi International Personal Bank has in segment A, without damaging the wider Citi brand; and

-

to exploit the segment B opportunity to increase client balances.

Communication strategy

A profiling exercise gave Citi International Personal Bank valuable insight into each client segment's motivation. This insight, combined with clear segment-based communication objectives, enabled the Bank to create tailored messages that reflected client needs in each segment.

The Bank knew that many clients in Segments A and B who were currently holding a balance of less than $100,000 had the potential to increase their balance. Furthermore, limited numbers of clients in these segments were likely to prefer to retain the Relationship Manager service and pay the increased fee. Segment B, comprising clients with the potential to increase their balances, offered the best business opportunity for the campaign to achieve its objective of being, at worst, revenue neutral.

Segment A communications were carefully crafted to balance a clear statement of the Bank's intentions with encouragement to clients to transfer their account(s) to another part of Citi that offered services more suited to their financial management needs.

Segment B communications focused on convincing clients that it was worth their while transferring a higher proportion of their finances to Citi International Personal Bank. The Bank was aware that these clients held additional funds with competitors thanks to profiling activity. Segment B messages emphasized the Relationship Manager-based service commitment that Citi International Personal Bank were offering the client in the event that they decided to invest more money with Citi International Personal Bank.

Segment C comprised clients whose balances were less than $100,000, but who were exempt from minimum balance charges. These exemptions came about either as a result of the clients living in a country where local legislation prohibited balance restrictions or because the clients were Citi staff. Despite these clients’ exempt status, the Bank still felt it was important to communicate its proposition to this segment. These clients were asked to consider increasing their balance, despite the lack of financial penalty if they chose to maintain their funds at current levels.

Clients in segment D already fulfilled the minimum account balance requirements and, therefore, messages to these clients emphasized Citi International Personal Bank's continuing commitment to offering them a high-quality personal service. The communication objective to these important clients was to make them feel special and assure them that even more time and resources would be devoted to them as a result of the new minimum balance policy. The Bank also took this opportunity to inform these clients about Citi International Personal Bank's business strategy and positioning.

Campaign execution

A campaign communication schedule was presented to Citi International Personal Bank's Leadership Team in March 2008:

- April — June 2008 :

-

Create communications

- 13 June 2008 :

-

Communication ‘live’ date

- 31 August 2008 :

-

Communication end date

- 1 September 2008 :

-

Changes implemented

- 30 November 2008 :

-

Segment A and B deadline to either leave Citi International Personal Bank or increase bank balance or accept higher fees

- December 2008 :

-

Project review

The multi-stage campaign communications were carefully integrated and personalized. The campaign employed one-to-one media, including direct and email, supported by a dedicated microsite containing more detailed information on the minimum balance changes. All the campaign's communications used a clear, straightforward and honest tone.

The first wave of messages to all segments focused on the benefit to the client of retaining Citi International Personal Bank as their wealth management partner. The main challenge lay in how to handle Segments A and B. No matter how carefully this communication was worded, there was no avoiding the fact that these clients were being given an ultimatum — ‘increase your balance or face higher fees or leave’. The positioning of the first direct communications set the tone for the whole dialogue, and it was critical to the success of the campaign that these affected clients clearly understood why Citi International Personal Bank was taking this step and how Citi would be able better to serve them as a result of it (Figures 1 and 2).

Minimum Relationship Balance campaign — Direct mail

Minimum Relationship Balance campaign — Microsite

Personalized email was used for the first follow-up to each client; for example, the email to Segment A and B clients who indicated that they would prefer to maintain their balance between $50,000 to $100,000 offered them the full Relationship Manager service for $50 per month. After the email, every client received a phone call from their Relationship Manager. Direct mail and email communications were staggered between June and July to enable Relationship Managers to handle the responses and calls effectively, with calls continuing into August 2008.

All the Relationship Managers were given campaign specific training to enable them to handle these potentially difficult transition-period phone calls effectively. The Relationship Managers had the unenviable task of speaking with each affected Segment A and B client to try to persuade them to either invest more of their funds with Citi International Personal Bank to comply with the required minimum bank balance, or to close their account and transfer it within the Citi Corporation. The Relationship Managers explained what Citi International Personal Bank was doing, how the client was affected and what their choices were as clearly and straightforwardly as possible. Every campaign communication was consistent in tone and message, reiterating the added value and benefits of the proposition to the client.

Campaign results

The campaign's results soon met its business objectives and very quickly exceeded expectations. The campaign produced an overall revenue increase of 0.35 per cent revenue as a result of qualifying and loyal clients' balance increases. This equated to actual growth of over 200 per cent from the clients who remained with Citi International Personal Bank. Another benefit from the campaign was that the net reduction in client numbers improved the Relationship Managers’ ability to service the remaining high-value clients by 23 per cent per client.

This campaign resulted in improved revenue and services for the Bank and its clients. Both improvements helped to create a firm foundation to enable Citi International Personal Bank to fulfil its strategic goal of aggressively increasing its share of the high-value international investor market. The Bank can now be confident of delivering on its core service proposition, in part because it has substantially increased its understanding of its clients. This invaluable insight will inform product, pricing and communication development and targeting as the business moves forward.

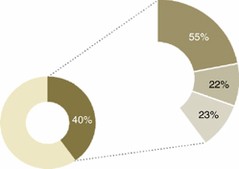

Of the original Segment A and B clients who made up 40 per cent of the client base but contributed only 4 per cent of the total revenue, 45 per cent stayed with Citi International Personal Bank on a new, more sustainable, basis:

-

55 per cent of the affected clients defected, taking 0.2 per cent of the total revenue with them;

-

22 per cent of affected clients stayed with Citi International Personal Bank and increased their balance to at least the minimum $100,000 requirement, increasing the revenue contribution from these clients by more 200 per cent; and

-

23 per cent of the affected clients maintained their balance under $100,000 but were happy to pay the fee in order to benefit from the Relationship Manager service (Figure 3).

Figure 3

Campaign response — 45 per cent of affected clients retained

The campaign succeeded in meeting all its objectives, and produced several significant additional benefits as well:

-

all existing clients had been made aware of the new minimum balance requirement and understood why it was being introduced;

-

Segment B balances increased by 222 per cent;

-

Citi International Personal Bank had clearly communicated its positioning to its clients and target market;

-

overall, the campaign had a positive impact on total revenue;

-

Citi International Personal Bank was now able to support its service-based added-value proposition to the clients who could take full advantage of it, producing increased revenue for the Bank and its clients;

-

the Relationship Managers were more satisfied in their roles as a result of their increased capacity to help their clients develop investment strategies; they felt empowered to deliver revenue growth; and

-

overall, Citi International Personal Bank clients are more satisfied with the Bank as a result of the campaign and the service improvements it heralded. Clients appreciate more rewarding experiences with the Bank, particularly the support they are now receiving from their Relationship Managers. As clients invest more of their assets, the Relationship Managers’ ability to help them with their personal investment strategies is increased. Relationship Managers can recommend targeted investments to improve each client's revenue. And, as investments generate more revenue for Citi International Personal Bank than static deposits, this creates a win:win situation for the Bank and its clients.

This campaign has changed the Bank's business culture to one that is driven by value-based segment management. This segment-based approach allows Citi International Personal Bank to identify and fully exploit business opportunities. For example, Citi International Personal Bank now has a much greater understanding of its clients’ behaviour in relation to price sensitivity. All new clients are made aware of the Bank's balance requirements at the first point of contact. Existing clients receive an automated monthly communication to ensure that balances are maintained in accordance with the minimum balance requirement.

The Bank is refining its value-driven segmentation strategy on an ongoing basis; for example, relationship pricing is being developed linked to value- and channel-based pricing — online services are free and personal services carry a charge. Channel-based pricing encourages clients to conduct their day-to-day banking business online, increasing the Relationship Managers’ capacity to deliver a premium investment advice service. Value-based segmentation is also informing highly targeted product and communication strategies. Client insight has led to improvements to the Bank's infrastructure to enable it to deliver a more personalized service. One example of this is a system enhancement that allows greater flexibility around the minimum balance so clients aren’t penalized for market movements in their investment value; a buffer zone can now be built around the minimum balance as a tangible good will gesture to loyal clients.

Lessons learned

This campaign was a brave one; it's never an easy business decision to deliberately offload clients, especially in current market conditions and such a wealthy target market. This campaign enabled Citi International Personal Bank to clarify its positioning and achieve complete consistency across its brand, product and service proposition, client base and acquisition target market. The campaign's execution was made easier by its clear campaign objectives. This clarity translated into honest, to-the-point and consistent campaign messages that emphasized Citi International Personal Bank's focus on its clients and its desire to deliver the best possible service to them. The Bank could tell its clients that the changes it was making would deliver a win:win situation that made complete business sense, paving the way for the Bank and its clients to move forward together profitably.

Sophisticated value-based segmentation and targeting was the vital element that delivered this campaign's success. Based on Pareto, the Bank constructed a sophisticated communication and product strategy for each segment, ultimately supported by one-to-one personal contact. Market and client insight, enhanced segmentation and targeting and staff training combined to ensure that the campaign exceeded its original objectives, improving existing clients’ loyalty to the brand and increasing revenue overall.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Boothby, K. Citi International Personal Bank: The IDM Business Performance Awards 2009: Award winner campaign: Minimum relationship balance. J Direct Data Digit Mark Pract 11, 332–340 (2010). https://doi.org/10.1057/dddmp.2010.13

Received:

Published:

Issue Date:

DOI: https://doi.org/10.1057/dddmp.2010.13