Abstract

In stable democratic countries the redistribution of power is institutionalized. Yet, there are periods of increased political uncertainty: During electoral campaigns there is uncertainty about who will win the election. And in multiparty parliamentary systems the uncertainty over who will actually govern usually continues throughout the coalition formation process. This article tries to contribute to answering the question whether and how financial markets react to such political uncertainty. Using a standard econometric tool, a GARCH (1,1) model, I find evidence for reactions of the AEX (Amsterdam Exchange Index) on periods of political uncertainty in the Netherlands. There is strong evidence that the political uncertainty during electoral campaigns is reflected in increased volatility of the AEX. The reactions during the coalition formation period seem to depend on the degree of uncertainty about the expected government coalition. The evidence for reactions on the ideological positions of government is mixed: Participation of left parties in governments seems to increase volatility, but the mean returns are not negatively affected in recent elections.

Similar content being viewed by others

Notes

Two points need further elaboration: On the same day the cabinet was sworn in, a secretary of state had to step back as she had lied about her membership in a militia. The point ‘statement of minister of economic affairs’ refers to minister Heinsbroek announcing that there should be short-term tax reductions. This statement was in direct opposition to the coalition treaty agreed upon two weeks earlier.

A comparison with the DAX in the same period shows indeed that the developments are mainly driven by developments of the world economy.

Compare for example Howells and Bain (2002, p. 538).

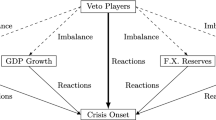

McGillivray (2003, p. 7) mentions another potential mechanism through which political uncertainty might trigger increased volatility: irrational reactions. In addition to the different expectations of which party participates in the coalition, the lack of a government might generate a general unease in the market. Referring to Shiller (1992) she hypothesizes that investors are more prone to irrational, herd-like behavior under such a cloud of confusion over the direction of the market.

Officially the AEX has been calculated on a daily basis since 1983. However, Thomson data service ‘Datastream’ provides a virtual AEX from 1965 onwards.

The composition of the AEX is reviewed annually. Every year in the month of March, the 25 most traded companies over the previous year are selected.

Other economic control variables such as trading volume or overnight interest rates are not available on a daily basis for the Netherlands over such a long time period. The results were robust to controlling for the US overnight interest rates.

I also tested more sophisticated variables like the positions of coalition agreements, or the policy positions of the leftmost veto player in the government coalition. Data from Debus (2007) who measured these positions using the Wordscores technique (Laver et al, 2003) based on policy positions from Benoit and Laver (2006) were used. However, none of these variables reached any conventional level of significance.

Also, in order to measure uncertainty during the coalition formation process, I tested variables that include measures of policy position. The uncertainty was supposed to be approximated either by the range between the most leftist and the most rightist economic policy offered by the potential minimal coalitions (calculated as the government center of gravity (Cusack, 2001)) or by the variance between the different policy offers. But these measures were not significant either.

These early elections took place because the government coalitions broke apart for political reasons. This excludes concerns about endogenous election timing for the Netherlands.

For a good overview on Dutch politics, see Andeweg and Irwin (2005).

Compare for example Chatfield (2004, p. 227).

In the statistical software package STATA, which I use in the following analyses, the independent variables enter the variance specification collectively as multiplicative heteroskedasticity. This leads to the following conditional variance equation for a GARCH (1,1) model: σ t 2=exp(λ0+λ1x t +λ2x t )+αɛt−12+δσt−12. This means that the variance is a linear function of the intercept λ0 and the independent variables (here x and w), the ARCH-term (ɛt−12) and the GARCH-term (σt−12). The ARCH-term can be understood as news about volatility in the last period. The GARCH-term is the variance from the previous period.

I also ran the regressions with an EGARCH (1,1) specification. The results were basically robust with the exception that the volatility-increasing effect of the participation of the PvdA in government could only be confirmed for the earlier period. However, the results of the diagnostic tests did not show any improvement compared to the more parsimonious GARCH (1,1) model. My choice of the GARCH (1,1) model is supported by the AIC. I experimented with including an ARCH-in-mean term in the models. Yet, the mean of the AEX return series does not depend on the conditional variance.

References

Alesina, A., Roubini, N. and Cohen, G.D. (1997) Political Cycles and the Macroeconomy. Cambridge, MA: MIT Press.

Andeweg, R.B. and Irwin, G.A. (2005) Governance and Politics of the Netherlands, 2nd edn. Hampshire, UK: Palgrave.

Benoit, K. and Laver, M. (2006) Party Policy in Modern Democracies. London: Routledge.

Bernhard, W. and Leblang, D. (2006) Democratic Processes and Financial Markets: Pricing Politics. Cambridge, UK: Cambridge University Press.

Bittlingmayer, G. (1998) Output, stock volatility, and political uncertainty in a natural experiment: Germany, 1880–1940. Journal of Finance 53 (6): 2243–2257.

Bollerslev, T. (1986) Generalized autoregressive conditional heteroscedasticity. Journal of Econometrics 31 (3): 307–327.

Bräuninger, T. (2005) A partisan model of government expenditure. Public Choice 125 (3–4): 409–429.

Chatfield, C. (2004) The Analysis of Time Series: An Introduction. Boca Raton, FL: Chapman & Hall.

Cusack, T.R. (1997) Partisan politics and public finance: Changes in public spending in the industrialized democracies, 1955–1989. Public Choice 91 (3–4): 375–395.

Cusack, T.R. (2001) Partisanship in the setting and coordination of fiscal and monetary policies. European Journal of Political Research 40 (1): 93–115.

Debus, M. (2007) Pre-Electoral Alliances, Coalition Rejections, and Multiparty Governments. Baden-Baden, Germany: Nomos.

Engle, R.F. (1982) Autoregressive conditional heteroskedasticity with estimates of the variance of UK inflation. Econometrica 50 (4): 987–1007.

Engle, R.F. (2001) GARCH 101: The use of ARCH/GARCH models in applied econometrics. Journal of Economic Perspectives 15 (4): 157–168.

Fama, E. (1970) Efficient capital markets: A review of theory and empirical work. Journal of Finance 25 (2): 383–417.

Fowler, J.H. (2006) Elections and markets: The effect of partisanship, policy risk, and electoral margins on the economy. The Journal of Politics 68 (1): 89–103.

Freeman, J.R., Hays, J.C. and Stix, H. (2000) Democracy and markets: The case of exchange rates. American Journal of Political Science 44 (3): 449–468.

Füss, R. and Bechtel, M.M. (2008) Partisan politics and stock market performance: The effect of expected government partisanship on stock returns in the 2002 German federal election. Public Choice 135 (3–4): 131–150.

Herron, M. (2000) Estimating the economic impact of political party competition in the 1992 British election. American Journal of Political Science 44 (2): 320–331.

Hibbs, D.A. (1977) Political parties and macroeconomic policy. American Political Science Review 71 (4): 1467–1487.

Howells, P. and Bain, K. (2002) The Economics of Money, Banking and Finance: A European Text. Harlow, UK: FT Prentice Hall.

Laver, M., Benoit, K. and Garry, J. (2003) Extracting policy positions from political texts using words as data. American Political Science Review 97 (2): 311–331.

Leblang, D. and Mukherjee, B. (2004) Presidential elections and the stock market: Comparing Markov-switching and fractionally integrated GARCH models of volatility. Political Analysis 12 (3): 296–322.

Leblang, D. and Mukherjee, B. (2005) Government partisanship, elections, and the stock market: Examining American and British stock returns, 1930–2000. American Journal of Political Science 49 (4): 780–802.

McGillivray, F. (2003) The coalition poker game and stock price volatility. Paper presented at the 2003 Midwest Political Science Association Meeting.

Moore, W.H. and Mukherjee, B. (2006) Coalition government formation and foreign exchange markets: Theory and evidence from Europe. International Studies Quarterly 50: 93–118.

Schneider, G. and Troeger, V. (2006) War and the world economy: Stock market reactions to international conflict. Journal of Conflict Resolution 50 (5): 623–645.

Shiller, R.J. (1992) Market Volatility. Cambridge, MA: MIT Press.

Tufte, E.R. (1978) Political Control of the Economy. Princeton, NJ: Princeton University Press.

von Neumann, J. and Morgenstern, O. (1944) Theory of Games and Economic Behavior. Princeton, NJ: Princeton University Press.

Vuchelen, J. (2003) Electoral systems and the effects of political events on the stock market: The Belgian case. Economics and Politics 15: 85–102.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Brunner, M. Does politics matter? The influence of elections and government formation in the Netherlands on the Amsterdam Exchange Index. Acta Polit 44, 150–170 (2009). https://doi.org/10.1057/ap.2008.37

Published:

Issue Date:

DOI: https://doi.org/10.1057/ap.2008.37