Abstract

Out-of-pocket (OOP) healthcare costs can impose a strain, their consequences are regressive, they may result into disaster and bankruptcy. These health expenses that surpass a certain percentage of total households income compelling the household to bear the cost of the illness is considered as catastrophic health expenditure (CHE). Using the national panel data collected in 2008/09, 2010/11 and 2012/13 waves in Tanzania, the study sampled a total of 1476 households with at least one member who had an experience of visiting a healthcare provider 4 weeks before the survey and she or he covered costs for treatment from own pocket. The logistic model was used to analyse the determinants of CHE in both rural and urban areas. The two most commonly thresholds were used, such as 10% and 40% of the overall income and non-food revenue, respectively. OOP healthcare costs are strongly and positively linked to catastrophic costs as well as household poverty. For both thresholds, income, household size, and age of the household's head above 60 years significantly influenced CHE at a 5% level. We support the literature pointed out that OOP healthcare expenses inflict financial catastrophe to the poor households and they even expose them to more hardship.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The primary objective of a healthcare system is to ensure that everyone has the opportunity to receive high-quality healthcare for better well-being and to exempt households from shouldering the costly burden of healthcare services. In developing nations, out-of-pocket (OOP) spending is the most common method of health financing [1], and its impact on household status, particularly among the impoverished, can be severe [2]. Direct payments for healthcare are an inappropriate method of financing because they disproportionately penalize vulnerable social groups, particularly the elderly and the poor [3]. The highest financial burdens fall on these families, and when the cost of healthcare surpasses their ability to pay, the likely response is to avoid or postpone seeking appropriate medical care. Families may be compelled to choose between providing healthcare for members and meeting other fundamental needs such as food, education, and housing [4]. Consequently, healthcare spending, especially catastrophic spending, can become a significant new source of poverty [2, 5].

Healthcare spending is considered catastrophic if direct payments for health services exceed a specific percentage of a household’s resources, thereby adversely affecting their standards of living. In countries like Tanzania, where mechanisms such as health insurance and taxation play a certain role in healthcare financing [6], households suffer from significant health expenses when one of their members becomes ill [7]. Catastrophic health expenditure (CHE) is defined as OOP healthcare spending that exceeds a certain percentage of a household's income, forcing the household to bear the cost of the illness [8]. When medical expenses push a household below the poverty line, it is said to be impoverished by medical expenses [9]. Even healthcare spending that seems manageable in relation to household income can be catastrophic for low-income families [3, 10].

Direct spending on healthcare increasingly causes policy distress for several reasons. First, OOP payments for healthcare services can push households into poverty or deeper poverty [11]. Second, households may be forced to cut back on other essential expenditures due to high health costs. For households already stretched to their financial limits, even a relatively small amount of healthcare spending can lead to financial catastrophe, forcing them to cut back on essentials like shelter, food, clothing, or children’s education. Similarly, excessive healthcare expenditures can cause financial hardship and impoverishment even for wealthy households [10]. Third, necessary healthcare services may be forgone by households to avoid extreme financial burdens, creating a harmful cycle of disability, poor health, and poverty [12].

Tanzania's OOP as a share of overall healthcare spending fell from 45 to 36% between 2002 and 2013. Despite this decline, the government’s per capita healthcare expenditure increased modestly, which is relatively better as compared to other countries in the region [13, 14]. For instance, in the fiscal year 2011/12, foreign donors accounted for 48% of Tanzania’s total healthcare expenditure (THE), while OOP spending constituted 33%. Excluding consolidated fund services, the total healthcare budget increased slightly from 9.1% to 11.3% of the gross domestic product (GDP), but this gain was largely due to a considerable increase in foreign aid. Compared to other low-income countries, Tanzania’s healthcare spending at 7.3% of GDP exceeds the global average of 5.3% for low-income countries (LICs). However, while 11.3% of the total government healthcare spending (including donor funding) is higher than the LIC average of 9.2%, it still falls short of the Abuja Declaration’s goal of allocating 15% of the national budget to healthcare [15, 16].

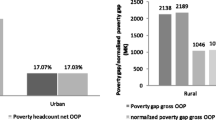

According to the 2022 Budget Brief Report and the Third National Five-Year Development Plan (FYDP III) 2021/22–2025/26, Tanzania has made significant progress in reducing reliance on OOP healthcare costs. In 2000, OOP spending accounted for 47% of overall healthcare expenditures, but due to various government efforts, this has been cut to 23% [17]. Despite this reduction, the percentage of OOP payments remains high, especially considering Tanzania’s poverty rate of 26%, with rural areas experiencing a rate of 31% and urban regions 16% [17]. There is subjective evidence of the welfare effects associated with OOP health costs (see, for example, [18, 19]), and in some cases, studies focus on specific populations such as adults, the elderly [20, 21], or child healthcare [22].

Research on the incidence of OOP healthcare costs on household welfare across different income groups and locations, is vital for planning and addressing prevailing debates [23]. Gendered analysis which were marginally featured in other studies are included in this paper to enhance comparisions [21, 23]. Moreover, precise estimates on determinants of catastrophic OOP healthcare expenses is crucial for both state and non-state stakeholders, though limited, in developing effective healthcare financial structures that promote equality and equity in access to healthcare services across socio-economic groups [24]. Therefore, the research questions are twofold: first, what is the incidence and intensity of CHE as a result of high OOP in Tanzania? Second, what are the determinants of catastrophic OOP healthcare expenditure on rural and urban households given their income differences in Tanzana?

2 Materials and methods

2.1 Study area, design and data sources

The study was based on the population dwelling in private households in Tanzania, using secondary data from the National Panel Survey (NPS) waves (I, II, and III) collected by the Tanzania National Bureau of Statistics. The dataset included individual and household socio-demographic, economic, and health-related data. The survey also captured additional details related to inpatient and outpatient care utilization over the last 12 months and four weeks, respectively, as well as health insurance coverage and a detailed breakdown of household spending.

The NPS employs a multi-stage, stratified cluster sampling design. Four distinct analytical strata are identified by the NPS sample design: Zanzibar, other Mainland metropolitan centers, Dar es Salaam, and Mainland rural areas. Within each stratum, clusters were selected at random, with the probability of selection proportional to the size of their respective populations. These clusters are similar to census enumeration areas in urban settings and villages in rural areas. In the final phase, 8 households from each cluster were selected at random.

The first round of the NPS in 2008/09 included a panel component from the 2007 Household Budget Survey (HBS). To create a panel of 1600 families for the 2008/09 NPS and HBS, 200 of the 350 clusters from the HBS sample were selected for the panel, a process that could only be done in Mainland Tanzania. Additionally, NPS rounds two and three employed the same sample design as the first round, resulting in an increase in the number of households due to the tracking of household splits. In this regard, the paper is based on households that reported having at least one member visiting a healthcare provider 4 weeks before the survey and using their own finances for treatment, as presented in Table 1.

2.2 Statistical analyses

Using STATA software, the data were analyzed to explore the frequency of health facility visits and the level of catastrophic health spending experienced by households. Descriptive analysis techniques and frequency tables were employed to present findings on both the prevalence and the severity of catastrophic health spending.

2.2.1 Measuring catastrophic expenditure on health

There are two main approaches for calculating CHE. The first, developed by Wagstaff and van Doorslaer [25], is the budget-sharing method, which defines CHE as OOP health expenses that exceed 10% of household income. The second, proposed by Xu et al. [26] is the financial-capacity method, defining CHE as health costs that account for 40% of non-food expenditures. These approaches, despite their limitations [27], offer valuable estimates of CHE and allow for comparisons across societies or countries.

According to the methodology of Wagstaff and van Doorslaer [25], to determine the catastrophic spending headcount ratio, Ti is defined as OOP healthcare expenses for household i, xi total spending for household i and f(x) food expenditure. If Ti/xi or Ti/[xi-f(x)] surpasses a given threshold, z, a household is said to have experienced catastrophic expenses. If the indicator Ei is defined as a dichotomous variable with a value of 1 if Ti/xi > Z and 0 else, the estimated prevalence of catastrophic spending at household (HC) is as follows:

whereby, N represents the sample size and Ei denotes 1 if Ti/xi (or Ti/[xi-f(x)]) > z and zero otherwise.

The main shortcoming of the headcount index is that it does not tell us much about the severity or intensity of catastrophic spending. It just shows what percentage of households are affected by the disaster. Then, the catastrophic overshoot was computed to quantify the magnitude of CHE. The intensity or catastrophic gap, also known as the catastrophic healthcare payment gap, is the average proportion of total consumption spending by which a household's payment exceeds the threshold. Similarly, if we establish an array Oi to represent the catastrophic gap as Oi = Ei ((Ti /xi)-Z), then the catastrophic medical payment overshoot (O) is as follows:

Although HC represents the occurrence of any disaster, O also determines the magnitude of the occurrence, and the two measures are linked by the mean positive overshoot (MPO), which is defined as follows:

In this regard, MPO index which is represented as mean positive gap (MPG) measures the average OOP healthcare spending for all households that surpass the criteria. Table 2 presents the variables used in measuring the CHE using Wagstaff and van Doorslaer [26] methods.

Moreover, basing on the Xu et al. [26] methodology, catastrophic health payments are estimated using the capacity to pay. The required data at the household level include monthly consumption expenditure (exph), food expenditure (foodh), the poverty line (pl), subsistence spending (seh) and capacity to pay (ctph).

OOP healthcare expenditures refer to direct payments made by households for healthcare services, including doctor consultation fees, medication purchases, and hospital bills, with insurance reimbursements deducted. Household consumption spending includes all monetary and in-kind payments for goods and services except healthcare, plus the value of homemade food consumed at home. Household expenditure on food covers all food purchases and home-produced food consumed, excluding alcoholic drinks, cigarettes, and meals eaten away from home.

To account for different food needs among household members, the adult-equivalent household size adjusts expenditures based on a scale that reflects economies of scale in food consumption. This study used an equivalence scale of 0.56, meaning that food needs increase with household size but at a decreasing rate [26].

To reduce measurement error, subsistence spending and the poverty threshold are calculated usingaverage food expenses of households with a food spending share of the overall expenditures in the 45–55 percentile, with the poorer the household, the greater the proportion of total income or consumption spent on food [26]. This is the poverty line, which is defined as subsistence expenditure per (equivalent) capita (Pl):

whereby, wh is the 45th to 55th percentile equivalized household size, and eqfoodh is the equivalized food expenditure. Each household's subsistence expenditure (seh) is calculated as follows:

A household is considered poor if its total household expenditure is less than its subsistence expenditure (poorh).

Non-subsistence spending of a household is defined as the amount of money available for non-essential expenses after covering basic needs such as food and shelter. This concept is also referred to as the capacity to pay. In some cases, a household’s food expenditure might be below the subsistence level, indicating that their food spending falls below the poverty line. This can happen because the survey’s reported food expenditure might not include factors such as food subsidies, self-production, or non-cash food consumption methods. When food spending is below subsistence needs, non-food expenditures are used to represent the household’s capacity to pay for additional expenses beyond basic necessities.

The OOP expenses as the percentage of a household's capacity to pay are referred to as the burden of health expenditures.

Catastrophic healthcare spending happens when a household's total OOP health expenses equal to or exceed 40% of the household's ability to pay or non-subsistence spending.

A dummy variable represents catastrophic health spending, with 1 representing a household with catastrophic spending and 0 indicating a household with no catastrophic spending.

A non-poor household is considered to be impoverished by health expenditures if it becomes poor after paying for healthcare costs. The poverty (impoorh) variable is a binary indicator defined as: 1: The household’s total expenditure, after out-of-pocket (OOP) healthcare costs, is equal to or less than the subsistence expenditure. 0: The household’s total expenditure, after OOP healthcare costs, is greater than the subsistence expenditure.

In this context, impoorh is 1 when the healthcare spending reduces the household’s total expenditure to a level that is below the subsistence threshold, reflecting a state of impoverishment due to health costs.

2.2.2 Measuring the determinants of catastrophic healthcare expenditures

The logistic regression model was used to analyse the determinants of catastrophic health spending using the household as a unit of analysis. Table 3 presents the variables used to measure the determinants of CHE. CHE is the dependent variable, defined as 1 if the household faces catastrophic healthcare costs and 0 if otherwise. The logistic distribution function is based on the logistic distribution function. The likelihood of a household incurring CHE is given by:

Also, its corresponding odd ratio was calculated as follows:

The odds ratios formulation is appropriate if the only available data for estimation is at the collective level rather than at the individual level. When dealing with individual-level data, an endogenous latent variable, y*, with a binary realization on the predictor variables, determines the likelihood of encountering catastrophic healthcare expenses. This is how the dependent variable data is assessed.

whereby,

\(\varepsilon\) is a random error term whose distribution is supposed to be logistic.

3 Results

3.1 People visiting a health facility

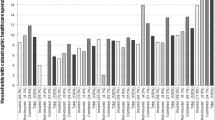

The proportion of households with at least one member who visited a healthcare service within 4 weeks before the survey is presented in Table 4. These proportions are broken down by income quintiles, location (rural and urban), and poverty status in each of the three waves of the survey. The results showed that the number of households in the poorest, poorer, and middle quintiles has been decreasing, while the number of households in the richer and richest quintiles has been increasing. This implies that the richest households are more likely to visit a health facility than their poorer counterparts. A similar trend was also observed for households headed by males (Table 4).

In terms of location, the results show that people living in rural areas are more likely to visit a healthcare facility than those in urban centers throughout all waves of the survey. Furthermore, when describing the tendency of visiting a healthcare facility in terms of poverty status across all waves, a related pattern was observed: non-poor households are more likely to seek treatment at a healthcare facility than poor households. The results reveal that less poor households report illness more frequently than poor households, indicating that these two groups have distinct perspectives on illness.

3.2 Household and OOP health expenditure

Monthly total health spending and OOP medical expenses in Tanzanian Shillings (TZS) for the sampled households are presented in Table 5. The ideal situation was to indicate how much of the total healthcare spending comes directly from the pockets of the households. Table 5 displays the results for all waves of the survey, as well as for different income quintiles, localities (rural/urban), and poverty status.

The results revealed that the average monthly healthcare spending for the poorest quintile decreased by 13.1% from 2008/2009 to 2010/2011, before rising by 25.1% in 2012/2013. On the other hand, the monthly OOP expenses for the poorer quintile increased by 3.4% from 2008/2009 to 2012/2013. The monthly OOP healthcare expenditure for the richest quintile also increased by 7.0% from 2008/2009 to 2012/2013. The associated trend has been observed in rural/urban localities and poverty status, where the OOP healthcare expenditure has been increasing across all waves (Table 5).

3.3 The incidence and intensity of CHE at 10% and 40% threshold

Indices of incidence and intensity of CHE across all waves of the survey were also estimated. Table 6 presents the level of CHE when overall consumption expenditure and non-food expenditure are used as the denominators. For the results to be comparable, a commonly established threshold was used. CHE for healthcare payments are calculated as a percentage of total household consumption expenditure and non-food expenditure using 10% and 40% thresholds, respectively.

The results show that, on average, 13.9%, 14.5% and 14.1% of all sampled households (at the 10% threshold) experienced CHE in 2008/09, 2010/11 and 2012/13, respectively. Relatively lower frequency and magnitude of CHE at the 40% threshold was revealed (Table 6).

In contrast, the catastrophic gap measures the severity of the incidence of CHE, whereas the MPG indicates those households which exceed the 10% threshold. This means that for the years 2008/09, 2010/11, and 2012/13, those who spent more than 10% of total health expenditure paid an average of 24.2% (i.e., 14.2% + 10%), 21.5% (i.e., 11.5% + 10%), and 21.4% (i.e., 11.4% + 10%), respectively. Moreover, the MPG at the 40% threshold is relatively higher (Table 6).

3.4 The incidence and intensity of CHE as a percentage of overall spending

The incidence of CHEs decreases as the expenditure thresholds increase, indicating an inverse relationship between the catastrophic headcount and the various thresholds (Table 7). For instance, as the threshold is raised from 10 to 25% of total expenditure, the incidence of catastrophic payments is estimated to decline at different levels in all waves. The average overshoot decreases as well, while the mean positive overshoot, on the other hand, increases as the threshold is raised.

3.5 Incidence and intensity of CHE as a share of non-food expenditure at various thresholds

The most widely used threshold in the literature to evaluate CHE when the capacity to pay is employed as the denominator is 40%. At this point, prior research has shown that households are compelled to compromise their basic needs [10]. The results at the 40% threshold are not significantly different from those of non-food expenditures. The incidence of CHE decreases as the expenditure thresholds increase, indicating an inverse relationship between the catastrophic headcount and the various thresholds. For example, as the threshold is raised from 10 to 25% of total non-food expenditure, the incidence of catastrophic payments is estimated to decline at different levels. The average overshoot drops as the thresholds are raised; however, the mean positive overshoot increases (Table 8).

3.6 Determinants of catastrophic healthcare expenditures

Both pre- and post-estimation diagnostic tests for variable reliability were used in the study as suggested by Lechner [28]. For instance, the Breusch-Pagan Lagrange multiplier (LM) test was performed to determine whether OLS could be used instead. It was found that no significant variables had been omitted from the logistic model of the given dataset. The probability value was 0.725, indicating that it is statistically insignificant at the 5% significance level. This revealed that no relevant variables had been omitted, and the model was correctly specified. Moreover, based on the Hausman test, the random effects model outperformed all other models, including fixed effects and pooled OLS. Thus, the sampled households were subjected to logistic regression to investigate the determinants of CHE at 10% and 40% thresholds. It was revealed that limited variables are associated with catastrophic healthcare spending at 10% or 40% thresholds (Table 9).

The results in Table 9 are based on threshold levels of 10% and 40%, depending on whether the denominator is overall consumption spending or non-food spending. The results reveal that household size is statistically significant at the 5% level for both 10% and 40% thresholds. This means that household size is related to the likelihood of causing CHE. The negative coefficient of household size implies that a household with fewer members is less likely to incur CHEs. A larger household entails a higher chance of someone being unwell. If the illness is communicable, a larger household size is more likely to have more sick members hence will likely to spend more on healthcare. Household size is expected to increase the likelihood of CHE because higher healthcare spending is more likely to lead to catastrophic healthcare costs.

Additionally, the 65+ years age group is significant at the 5% level for both 10% and 40% thresholds, meaning that the likelihood of incurring catastrophic spending is higher for heads of households aged 65 years or older compared to younger age groups, keeping other factors constant. Though the magnitude of the coefficients is nearly zero for household spending which also imply that households with higher income are less likely to be ill at both the 10% and 40% thresholds. This is because, unlike their poorer counterparts, better-off households can access resources such as clean water and better food for improving theier health.

Households living below the poverty line are unable to meet even their most basic needs and lack the financial means to cover any form of healthcare expenditure. In contrast, the healthcare expenditures of wealthy households often account for a smaller percentage of their income than those of impoverished households.

Education, particularly the household head's level of education, is another crucial component in understanding the magnitude of CHE [29]. In theory, if the household head has completed secondary school or higher education, the amount of healthcare spending is lower than in households where the head has not completed any formal schooling. Accordingly, the proportion of OOP expenditure in a household's budget may be reduced as a result of educational attainment. However, when defining the education of the household head as 1 if he or she has completed primary school or less, and 0 otherwise, the results show that all categories of education are statistically insignificant at the 5% level of significance given the 10% and 40% thresholds.

A narrow collection of variables, particularly environmental amenity variables such as safe drinking water in the rainy season, safe drinking water in the dry season, and sanitary toilets, appeared to have no significant impact on the probabilities of CHE across the threshold levels. The odds ratio of the logit model in favor of households falling into catastrophe is presented in Table 10.

4 Discussion and implications

The study indicates that household spending (proxy of real consumption expenditure), household size, and the age of the household head are significant factors influencing the occurrence of CHEs. Specifically, it has been observed that households headed by individuals in the age brackets of 36–60 years and those 60 years and older face higher risks of CHEs. This phenomenon is not entirely surprising given that both non-medical costs and a variety of related socioeconomic factors play a crucial role in determining OOP healthcare expenses [24].

Non-medical costs, which include expenditures on transportation, accommodation, and opportunity costs related to seeking medical care, often contribute significantly to the total financial burden of healthcare. For instance, individuals who live in remote areas might incur substantial travel expenses and may have to forego work to attend medical appointments, which compounds the financial strain of illness. Consequently, the socioeconomic status of households, including their income levels and the structure of the household, becomes a pivotal determinant of CHEs.

Moreover, there is a notable trend where educated individuals tend to migrate from rural to urban areas in search of better employment and other opportunities. This migration leaves behind predominantly less educated populations in remote areas, who are often employed in the agricultural sector. This trend corroborates the findings of Sirag and Mohamed Nor [18], which suggest that households led by individuals with only primary or secondary education are more likely to experience income poverty. This educational disparity and its impact on income levels reinforce the link between household education levels and the incidence of CHEs.

Beyond income and education, other factors such as healthcare utilization and health status have also emerged as important determinants of CHEs. Studies have shown that individuals with better access to healthcare services and better overall health status are less likely to face catastrophic health expenditures [30,31,32,33]. These findings underscore the critical need for effective health policies that not only reduce OOP costs but also foster collaborative efforts to ensure comprehensive healthcare coverage [34]. In Tanzania, OOP payments constitute a significant portion of healthcare funding, and there is an urgent need for reforms that address these costs to improve the equity and efficiency of the healthcare system.

Reforms aimed at alleviating the financial burden of healthcare are especially crucial for poorer households in developing countries [3]. Such reforms must consider gender disparities in healthcare access, as evidence suggests that male household heads visit health centers more frequently than their female counterparts [35]. Furthermore, Tanzania’s healthcare financing system, which heavily relies on user fees at the point of service delivery, reflects a broader issue where informal sector workers are largely excluded from health insurance coverage. This user-fee model, as noted in various studies, exacerbates financial hardships for the impoverished [36] and often results in the delay of necessary medical care, leading to more severe health conditions and higher costs [31, 37].

5 Conclusion

The incidence of CHE tends to decrease as the thresholds rise from 10 to 40%. Better-off households, though limited, may have the purchasing power to exceed these thresholds hence have less chances of being ill. However, the remaining portion of the income after CHE for relatively better-off households would not be sufficient to free them from the poverty trap. According to the methodology of this study, the OOP payments made by such households can be treated differently compared to those made by poor households, who are compelled to reduce their consumption of basic goods.

Consequently, high OOP expenses lead to catastrophic healthcare spending that ultimately hampers access to healthcare for households and individuals, potentially driving them into income poverty. Therefore, efforts should be made to increase health insurance coverage. While universal health insurance would be the most effective approach to shield people from the highly impoverishing consequences of OOP healthcare spending, financial protection mechanisms through health insurance schemes from both state and non-state actors should be strongly encouraged and promoted. Increased insurance coverage is particularly vital for the poor, elderly, most at-risk populations, and informal sector workers in both rural and urban areas.

Data availability

Data will be made available on request.

References

Koch SF, Setshegetso N. Catastrophic health expenditures arising from out-of-pocket payments: evidence from South African income and expenditure surveys. PLoS ONE. 2020;15(8): e0237217.

Somkotra T, Lagrada LP. Payments for health care and its effect on catastrophe and impoverishment: experience from the transition to universal coverage in Thailand. Soc Sci Med. 2008;67(12):2027–35.

Sarker AR, Sultana M, Alam K, Ali N, Sheikh N, Akram R, Morton A. Households’ out-of-pocket expenditure for healthcare in Bangladesh: a health financing incidence analysis. Int J Health Plann Mgmt. 2021;36:1–12.

Knaul FM, Arreola-Ornelas H, Mendez-Carniado O, Bryson-Cahn C, Barofsky J, Maguire R, Miranda M, Sesma S. Evidence is good for your health system: policy reform to remedy catastrophic and impoverishing health spending in Mexico. Lancet. 2006;368(9549):1828–41.

van Doorslaer E, O’Donnell O, Rannan-Eliya RP, Somanathan A, Adhikari SR, Garg CC, Harbianto D, Herrin AN, Huq MN, Ibragimova S, Karan A, Lee TJ, Leung GM, Lu JF, Ng CW, Pande BR, Racelis R, Tao S, Tin K, Tisayaticom K, Trisnantoro L, Vasavid C, Zhao Y. Catastrophic payments for health care in Asia. Health Econ. 2007;16(11):1159–84.

Dutta A. Prospects for Sustainable Health Financing in Tanzania: Baseline Report. Washington: Health Policy Project, Futures Group; 2015.

Embrey M, Vialle-Valentin C, Dillip A, Kihiyo B, Mbwasi R, Semali IA, Chalker JC, Liana J, Lieber R, Johnson K, Rutta E, Kimatta S, Shekalaghe E, Valimba R, Ross-Degnan D. Understanding the role of accredited drug dispensing outlets in Tanzania’s health system. PLoS ONE. 2016;11(11): e0164332.

Ekman B. Catastrophic health payments and health insurance: some counterintuitive evidence from one low-income country. Health Policy. 2007;83(2–3):304–13.

Xu K, Saksena P, Jowett M, Indikadahena C, Kutzin J, Evans DB. Exploring the thresholds of health expenditure for protection against financial risk. World Health Report. Background Paper, No 19. Geneva, Switzerland; 2010.

Xu K, Evans DB, Carrin G, Aguilar-Rivera AM, Musgrove P, Evans T. Protecting households from catastrophic health spending. Health Aff. 2007;26(4):972–83.

Elgazzar H, Raad F, Arfa C, Mataria A, Salti N, Chaaban J, Majbouri M. Who pays? Out-of-pocket health spending and equity implications in the Middle East and North Africa. Health, Nutrition and Population (HNP) discussion paper, World Bank, Washington, DC; 2010.

Nemati E, Khezri A, Nosratnejad S. The study of out-of-pocket payment and the exposure of households with catastrophic health expenditures following the health transformation plan in Iran. Risk Manag Healthc Policy. 2020;13:1677–85.

USAID. Tanzania health financing profile. Washington, DC; 2016.

Ally M, Piatti-Fünfkirchen M, 2020. Tanzania health financing policy notes: the role complementary financing mechanisms in Tanzania’s health finance architecture. World Bank. Washington, DC.. Components of out-of-pocket expenditure and their relative contribution to economic burden of diseases in India. JAMA Netw Open. 2020;5(5):e2210040.

WHO. Global status report on road safety 2018: summary. Geneva: World Health Organization (WHO/NMH/NVI/18.20); 2018.

World Bank. Tanzania public expenditure review 2020. Washington, DC; 2020.

Wagstaff A, Eozenou P, Smitz M. Out-of-pocket expenditures on health: a global stocktake. World Bank Res Obs. 2020;35(2):123–57.

Sirag A, Mohamed NN. Out-of-pocket health expenditure and poverty: evidence from a dynamic panel threshold analysis. Healthcare. 2021;9:536.

van Minh H, Kim Phuong NT, Saksena P, James CD, Xu K. The financial burden of household out-of-pocket health expenditure in Viet Nam: findings from the national living standard survey 2002–2010. Soc Sci Med. 2013;96:258–63.

Brinda EM, Andrés RA, Enemark U. Correlates of out-of-pocket and catastrophic health expenditures in Tanzania: results from a national household survey. BMC Int Health Hum Rights. 2014;14:5.

Brinda EM, Kowal P, Attermann J, Enemark U. Health service use, out-of-pocket payments and catastrophic health expenditure among older people in India: the WHO Study on global AGEing and adult health (SAGE). J Epidemiol Community Health. 2015;69(5):489–94.

Manzi F, Schellengerg JA, Adam T, Mshinda H, Victora CG, Bryce J. Out-of-pocket payments for under-five health care in rural southern Tanzania. Health Policy Plan. 2005;20:i85–93.

Al-Hanawi MK, Mwale ML, Qattan AMN. Health insurance and out-of-pocket expenditure on health and medicine: heterogeneities along income. Front Pharmacol. 2021;2021(12): 638035.

Bedado D, Kaso AW, Hailu A. Magnitude and determinants of out of pocket health expenditure among patients visiting outpatients in public hospitals in East Shoa Zone, Ethiopia. Clin Epidemiol Glob Health. 2022;15: 101066.

Wagstaff A, van Doorslaer E. Catastrophe and impoverishment in paying for health care: with applications to Vietnam 1993–98. Health Econ. 2003;12:921–34.

Xu K, Evans DB, Kawabata K, Zeramdini R, Klavus J, Murray CJ. Household catastrophic health expenditure: a multicountry analysis. Lancet. 2003;362(9378):111–7.

Flores G, Krishnakumar J, O’Donnell O, van Doorslaer E. Coping with health-care costs: implications for the measurement of catastrophic expenditures and poverty. Health Econ. 2008;17(12):1393–412.

Lechner M. Some specification tests for probit models estimated on panel data. J Bus Econ Stat. 1995;13(4):475–88.

Saito E, Gilmour S, Rahman MM, Gautam GS, Shrestha PK, Shibuya K. Catastrophic household expenditure on health in Nepal: a cross-sectional survey. Bull World Health Organ. 2014;92(10):760–7.

Boon H, Verhoef M, O’Hara D, Findla B. From parallel practice to integrative health care: a conceptual framework. BMC Health Serv Res. 2004;4:15.

Tungu M, Amani PJ, Hurtig A-K, Kiwara AD, Mwangu M, Lindholm L, Sebastian MS. Does health insurance contribute to improved utilization of health care services for the elderly in rural Tanzania? A cross-sectional study. Glob Health Action. 2020;13(1):1841962.

Godlonton S, Keswell M. The impact of health on poverty: evidence from the South African integrated family survey. S Afr J Econ. 2005;73(1):133–48.

Muhammad Malik A, Azam Syed SI. Socio-economic determinants of household out-of-pocket payments on healthcare in Pakistan. Int J Equity Health. 2012;11:51.

Ndomba T, Maluka S. Uptake of community health fund: why is Mtwara District lagging behind? J Glob Health Sci. 2019;1(2): e50.

Pan American Health Organization. Out-of-pocket expenditure: the need for a gender analysis. Washington, D.C; 2021.

Amu H, Dickson KS, Kumi-Kyereme A, Eugene Kofuor E, Darteh M. Understanding variations in health insurance coverage in Ghana, Kenya, Nigeria, and Tanzania: Evidence from demographic and health surveys. PLoS ONE. 2018;13(8): e0201833.

Su TT, Kouyaté B, Flessa S. Catastrophic household expenditure for health care in a low-income society: a study from Nouna District, Burkina Faso. Bull World Health Organ. 2006;84(1):21–7.

Acknowledgements

The authors wish to express their sincere gratitude to the Tanzania National Bureau of Statistics (NBS) for the technical support and making dataset accessible for this study. We appreciate all participants as well as the anonymous reviewers. The views expressed are those of the authors and cannot be considered to state the official position of any organization and partners.

Funding

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Author information

Authors and Affiliations

Contributions

Festo Anam Mwemutsi: Conceived and designed the study; Performed data reorganization; Analysed and interpreted the data; Contributed materials, analysis tools or data; Wrote the paper. Lutengano Mwinuka: Conceived and designed the study; Performed data reorganization; Analysed and interpreted the data; Contributed materials, analysis tools or data; Wrote the paper.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License, which permits any non-commercial use, sharing, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if you modified the licensed material. You do not have permission under this licence to share adapted material derived from this article or parts of it. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by-nc-nd/4.0/.

About this article

Cite this article

Mwinuka, L., Mwemutsi, F.A. Magnitude and determinants of the catastrophic out-of-pocket healthcare expenditure in rural and urban areas: lessons from Tanzania panel data survey. Discov Health Systems 3, 83 (2024). https://doi.org/10.1007/s44250-024-00151-0

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s44250-024-00151-0