Abstract

Industrial equipment/machinery is an important element of manufacturing. They are used for producing objects that people need for everyday use. Therefore, there is a challenge to adopt effective maintenance strategies to keep them well-functioning and well-maintained in production lines. This will save energy and materials and contribute genuinely to the circular economy and creating value. Remanufacturing or refurbishment is one of the strategies to extend life of such industrial equipment. The paper presents an initial framework of cost estimation model based on combination of activity-based costing (ABC) and human expertise to assist the decision-making on best life extension strategy (e.g. remanufacturing, refurbishment, repair) for industrial equipment. Firstly, ABC cost model is developed to calculate cost of life extension strategy to be used as a benchmark strategy. Next, expert opinions are employed to modify data of benchmark strategy, which is then used to estimate costs of other life extension strategies. The developed cost model has been implemented in VBA-based Excel® platform. A case study with application examples has been used to demonstrate the results of the initial cost model developed and its applicability in estimating and analysing cost of applying life extension strategy for industrial equipment. Finally, conclusions on the developed cost model have been reported.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The effectiveness and continuity of modern economy are highly affected by the availability of natural resources. This is significant because meeting the needs and desires of nowadays rapidly growing population requires vast amounts of natural resources that are gradually depleting. In such circumstances, circular economy (CE) is increasingly gaining attention of businesses and organisations as a new sustainable paradigm focusing on better use of natural resources, process efficiency and climate change [1,2,3,4].

The circular economy is defined as “a regenerative system in which resource input and waste, emission, and energy leakage are minimised by slowing, closing, and narrowing material and energy loops. This can be achieved through long-lasting design, maintenance, repair, reuse, remanufacturing, refurbishing, and recycling” [3, 5]. As can be seen in Fig. 1, the inner loops of reuse and remanufacturing seem the most appropriate end-of-life options for retaining product value in the CE model because they require less raw materials, energy, time, and cost than other conventional options (i.e. recycling and disposal). Accordingly, appropriate product life extension strategies should be adopted in order to maximise usage time within these inner loops options [6, 7].

Product life cycle stages in circular economy model [7]

The ambitious circular economy is therefore perceived by businesses and organisations as a positive opportunity [8] and an alternative to replace the traditional linear economy system “take-make-waste model”, that showed major effects on Earth’s ecosystem, with a more balanced business model that emphasises closed loops instead of continuous waste generation [4, 9, 10].

In the framework of circular economy, industrial equipment is a key factor in driving manufacturing industry. It represents about 25 percent of the manufacturing Gross Domestic Product (e.g. 21 percent of US GDP, 25 percent in Europe and 33 percent for Japan) [11]. The challenge is to keep them well-functioning and well-maintained in production lines because failure leads to significant financial and production losses. In addition, disposal of such failed equipment is both costly and environmentally unfriendly and does not recover any residual energy [12]. This necessitates the need to adopt maintenance strategies that extend the life of the equipment and reduce waste of material.

Therefore, remanufacturing or refurbishment is one of the options that can be made to restore industrial equipment to a level of quality and functionality that competes with the new one and contributes effectively towards developing the circular economy and achieve sustainable development [10, 13, 14]. The concept of remanufacturing is spreading throughout the world, especially in Europe. For example, the European Remanufacturing Network has reported that the remanufacturing industry in Europe is assessed to reach a total turnover of about €30 billion with 190,000 employees. This could be triple up to about €100 billion by 2030 with possibility to employ over half a million people [15].

In this context, researchers (from universities and research centres) and industry representatives from nine European countries launched RECLAIM (RE manufaC turing and refurbishment LA rge I ndustrial equipM ent) project to establish solutions for the sake of helping European industry to improve productivity and performance by overcoming failure problem of ageing machines. The project intending to formularise ground rules and tools that enable manufacturers to monitor the health conditions of machines and implement the appropriate life extension strategy (i.e. remanufacturing, refurbishment, upgrade, maintenance, repair, recycle, etc.).

RECLAIM solutions concept is based on developing a Decision Support Framework (DSF) for the timely and accurate machine’s health prediction and the selection of best recovery action. The DSF will accumulate knowledge of machinery status and aid manufacturers to understand the feasibility of restoring the machine, the best time to perform restoration at the least possible cost, and the best restoration strategy that needs to be implemented for the machine. This can be accomplished through integration of the following technologies and strategies (see Fig. 2) [16,17,18,19].

-

Cost Modelling and Financial Analysis Toolkit: using a combination of parametric costing and activity-based costing (ABC) methods to develop the cost model that will carry out cost estimation and analysis of life extension strategies and activities within RECLAIM. Monte-Carlo simulation will also be implemented to help estimate the propagation of uncertainty of cost outputs and perform sensitivity analysis.

-

Prognostic and Health Management Toolkit: using shop floor data to calculate overall equipment efficiency and extract other meaningful information by analysing sensory and system level data to enable prediction and prevention capabilities as well as trace asset status.

-

Fault Diagnosis and Predictive Maintenance Simulation Engine using Digital Twin: monitoring and predicting of the performance and status of factory assets in order to provide the user with all the necessary features to schedule maintenance work on the machines and prevent the failures being predicted by “Prognostic and Health Management” component.

-

Optimization Toolkit for Refurbishment and Remanufacturing Planning: optimising planning by multi-variable monitoring of the operating parameters of the machine, where the effects of variable changes can be determined and combined with known best practice methodologies for model-based shop floor control.

-

Refurbishment and Remanufacturing Process: deploying novel tools and methodologies to be used for the refurbishment or remanufacturing process. Also, the Augmented Reality enabled multimodal interaction mechanisms will be developed to enhance the process of refurbishment and remanufacturing.

Conceptual framework of RECLAIM DSF [19]

These technologies and solutions developed in RECLAIM will be applied and validated through five case studies (pilots) selected from different European industrial sectors (i.e. footwear manufacturer, white goods manufacturer, wood manufacturing, friction welding machines and textile manufacturer) in order to demonstrate their general applicability to other industrial sectors. For more details on the RECLAIM project, the reader is referred to [16, 20].

The cost model is a key component in RECLAIM solution. Its main purpose is to estimate and understand the costs to be incurred when applying particular life extension strategy. It will be integrated with other tools and methodologies (as illustrated in Fig. 2) to enable end-users perform optimal decision-making regarding which life extension strategy (e.g. remanufacturing, refurbishment, repair) to implement for large industrial equipment that is towards its end-of-life, taking into account variables such as cost, machine performance, and energy consumption. This paper focuses on introducing an initial framework for cost model estimation in the RECLAIM solution.

Therefore, the relevant research question would be revolved around developing simple and tractable methodology that employs human expertise within cost model framework to estimate and analyse total cost of applying life extension strategy for large industrial equipment and thus support informed decision-making. Accordingly, the following research question has been formulated:

How can expert knowledge be integrated within cost modelling framework to estimate and analyse cost of applying different life extension strategies for industrial equipment?

To reach a conclusion regarding this research question, the following objectives have been set up.

-

Develop ABC cost model to calculate cost of life extension strategy that has more available data to be used as a benchmark strategy.

-

Use expert opinion to modify data of benchmark strategy.

-

Use modified data to estimate costs of other life extension strategies.

-

Apply the developed cost estimation methodology on a case study to demonstrate its applicability.

The rest of the paper is organised as follows: “Cost Estimation Methods” provides a literature review on the cost estimation methods used for developing cost models for supporting life extension strategy selection. Advantages and disadvantages of these methods are also reported. “Proposed Cost Estimation Framework” details the initial framework of the cost model presented in this paper. Cost model requirements, architecture and methodology used are described. “Cost Model Implementation” demonstrates the implementation of cost model through a case study of estimating cots for different life extension strategies applied to friction welding machine. Analyses of cost outcomes are also presented, including graphical representation of results. “Discussion” discusses the contributions of the article to the circular economy. And “Conclusion” draws conclusion from this work.

Cost Estimation Methods

There is a variety of approaches used in engineering domain for developing models to estimate the cost of manufacturing/remanufacturing products. These approaches can generally be classified into three basic methods, analogy, parametric and activity-based costing, or a combination of them. Selecting the best cost estimating method is based largely on the data availability for conducting the estimate [21,22,23,24]. The fundamental principles for cost estimation methods and examples of their application in manufacturing/remanufacturing products are discussed next.

Analogy Cost Estimation

Analogy cost estimation is a qualitative method that depends on expert judgement. It involves comparing the similarities among the product needs to be estimated and the products that have been previously manufactured/remanufactured. Therefore, costs of the past similar cases are needed to generate cost estimates for the new product [22, 24,25,26].

Analogy cost estimating is mostly applied using Case-Based Reasoning (CBR). A typical CBR system involves retrieving the most relevant case(s), reusing the case(s) for solving the problem, revising the proposed solution, and then adopting/retaining the solution into the case repository [27, 28]. Goodall et al. [29], Ficko et al. [30], Qin et al. [31] and Ghazalli & Murata [32] are examples of applying CBR approach in predicting manufacturing/remanufacturing costs.

Parametric Cost Estimation

Parametric cost estimation is a quantitative method that uses mathematical equations, referred to as Cost Estimation Relationships (CERs), to integrate cost with one or more cost driver variables that affect cost. The CERs can range from simple equations to complex relationships involving multiple variables. Generally, the CERs can be developed by applying statistical analysis, such as linear regression modelling to relate historical data to the cost being estimated. However, when historical data is scarce, the CERs logic can be determined through expert knowledge so that the causal relationship of cost drivers and the estimated cost is identified [33,34,35].

Examples of applying parametric cost estimation include [36, 37] in which a linear regression model was compared with neural networks to examine the performance and ease of cost estimation modelling to develop cost estimating relationships (CERs). Camargo et.al. [21] studied the possibilities of applying parametric cost estimation methods in the textile and garment industries. The application of parametric method for cost estimation in the design phase was also examined by Duverlie and Castelain [38] and compared with the CBR method. They concluded that the combination of the two methods, parametric and CBR, is reasonable.

Activity-Based Costing Estimation

Activity-Based Costing (ABC) is a costing method that identifies activities performed and assigns the cost of each activity according to the actual consumption by each. It is also called “engineering build up costing” or “bottom-up costing”. ABC approach has been described by many authors [22, 24,25,26, 39]. While the two cost estimation methods described above rely on the availability of historical data/knowledge, activity-based costing, on the other hand, depends on breaking-down the whole manufacturing/remanufacturing process into smaller work activities for easy estimating. Once individual estimates are calculated for each activity, they are added up to generate the overall estimate of the cost. This is not restricted by historical data availability as data can be directly collected from users and other available sources. ABC can also account for indirect costs more accurately by costing the time and resources spent on each activity in the process. In addition, it facilitates cost tracking so that detailed cost analysis can be performed to identify the most influential variables on the overall cost.

The ABC method has been broadly applied in manufacturing/remanufacturing domain. Life cycle cost model and manufacturing cost model for aircraft wing are developed based on activity-based costing. Object-oriented system engineering has also been used in modelling [40,41,42]. Qian and Ben-Arieh [33] presented a cost estimation model that links ABC with parametric cost estimations of the design and development phases of machined rotational parts. Ardiansyah et al. [23] also introduced a hybrid approach of parametric cost estimation and ABC to generate the cost information of the whole process from the design stage up to development stage. It has been applied to the development of an electric vehicle prototype. Another integrated parametric cost estimation model with ABC approach has been presented by Susanti et al. [43] to estimate production costs of a Li-ion battery pack for e-motorcycle conversion. Each activity’s cost of the production process was put into a parametric cost estimation model to calculate the cost of each activity into the total cost of production. ABC has also been used to analyse economic benefit of remanufacturing a slat track in aircraft wing [44] and support the selection of optimum End-of-Life recovery alternative [45] through developing a cost estimation model based on using detailed recovering process information.

Comparison of Cost Estimation Methods

Further to the literature review provided in the previous subsections, Table 1 presents a summary of the advantages and disadvantages for each of the three methods [21, 25, 26]. It can be seen that Analogy and Parametric estimation methods are more suitable for fast and easy estimations where enough amount of historical data and knowledge is available and detailed estimation is not required. Otherwise, ABC approach is the best option as it is not restricted by historical cost data, but good knowledge about the process and activities is required.

From the literature review, we can notice that there is a need for cost estimation approach that uses less amount of data to produce acceptable results. The cost estimation methodology presented in this paper addresses this issue by integrates expert knowledge within ABC costing method so that fast, accurate and detailed cost estimations can be obtained using minimum amount of data required.

Proposed Cost Estimation Framework

The cost model in RECLAIM is built based on customer requirements and expectations. It will carry out cost estimation and analysis for every selected life extension strategy of the industrial equipment. This is done through developing ABC cost model for calculating cost of benchmark strategy. Then, cost model data related to benchmark strategy are adjusted to estimate cost of other life extension strategy.

Cost Model Requirements

The framework for cost estimation model presented in this paper is built based on initial end-user requirements that include estimating the total cost for single life extension strategy, e.g. remanufacturing/refurbishment, and providing breakdown analysis of the total cost estimated, for comparison and decision-making concerning which the most suitable and cost-effective life extension strategy is for a given condition of equipment. These requirements captured from pilot partners are considered initial and subject to update. For example, there are some factors that might affect cost outputs such as variations in labour time due to type of technology used to perform the activity, learning curve of the staff, etc., will be considered in the updated version of this cost model framework. Therefore, activity-based costing (ABC) method is appropriate to meet these requirements because it gives accurate results based on cost breakdown structure which will allow for analysing the distribution of total cost and comparison between different life extension strategies.

Cost Model Architecture

The cost model will be integrated within the Decision Support Framework (DSF) so that the output of the cost model is used as an input to the DSF through RECLAIM database to provide decision support to pilot partners (end-users) in RECLAIM. As seen in Fig. 3, the cost model will collect data such as machine/component to estimate cost for, strategy to estimate cost for as inputs and return the cost estimate of applying the strategy and its cost breakdown as an output. The cost output is calculated based on data and knowledge stored in the cost model.

Cost model architecture

Cost Estimation Methodology

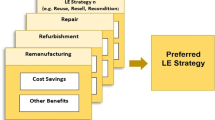

Selecting an appropriate cost estimating methodology is a key factor in constructing cost model. Parametric cost estimation methodology requires availability of sufficient historical cost data to generate correct cost equations using statistic, while analogy cost estimation methodology requires cost cases from similar past projects and relies on expert judgement in adjusting costs. Activity-based costing (ABC) methodology gives accurate results based on cost breakdown structure, but also requires data and information about resources consumed during activities. The initial framework of cost estimation presented in this paper adopts a combination of ABC method and expert knowledge, as shown in Fig. 4. This includes using ABC method to calculate cost of life extension strategy that has more data availability. Then, data used in calculating life extension strategy cost are adjusted by expert to estimate cost of other life extension strategies identified by pilot partners for their machines. Using such approach of cost estimation method is somewhat easy and fast to implement because it needs to collect only one set of cost model data (i.e. data for one life extension strategy), which will then be modified by expert to estimate cost of other life extension strategies. It will also allow for detailed analysis into estimated total cost to understand the cost difference between different life extension strategies for industrial equipment, which is a key requirement for the cost model in RECLAIM.

Cost estimation process in proposed framework

Cost Breakdown Structure

Figure 5 shows cost breakdown structure (CBS) used in the initial framework of cost estimation methodology. It has been developed based on identifying activities of life extension strategy process. Then, the main cost elements have been determined for each activity, which include labour cost, machine cost and consumables cost.

Cost breakdown structure for life extension strategy

Cost Drivers and Cost Estimation Relationships

Having defined the CBS, the next step is to generate mathematical equations for each cost element based on cost driver. Cost drivers are those factors of life extension strategy process that directly explain the cost incurred by the activities in the process. An example of the main cost drivers for each activity of the proposed life extension strategy process is shown in Table 2.

The cost drivers rate and quantity consumed by each activity are determined (e.g. Rl is the labour rate (€/hour) and Tl is the labour time (hour)).

Then, for benchmark strategy, the cost of each activity is computed based on cost drivers rate and quantity as shown in Eq. 1.

where Cj is the cost of jth activity, k is the number of cost elements in activity j and Oj is the consumables cost during activity j.

The cost estimate process is continued in the same way for all activities, and the total cost of benchmark life extension strategy is then calculated by aggregating all costs of activities as per Eq. 2.

where Ctotal is the total cost for benchmark life extension strategy, Cj is the cost of activity j and n is the number of activities.

The cost of other life extension strategies can be estimated based on adjusting cost drivers quantities in respect to benchmark strategy. For example, values of machine time, labour time and consumables cost for type s of life extension strategy are modified as percentages of the corresponding values of benchmark life extension strategy. Accordingly, we rewrite Eq. 1 to estimate cost of each activity of strategy s as shown below.

where αs is the adjustment factor for strategy s, which is for simplicity independent of activities j.

Cost Model Implementation

The cost model to be developed in the RECLAIM project will be used by pilots end-users participating in the project. Five case studies have been selected from distinct industrial sectors to be used in validating technologies and solutions developed in the project: footwear manufacturer, white goods (cookers, dishwashers, etc.) manufacturer, wood manufacturing, friction welding machines and textile manufacturer. The initial cost model presented in this paper has been demonstrated on one of these five industrial case studies (i.e. Friction Welding Machinery). An Excel® Visual Basic for Application (VBA) tool was developed to implement the developed cost model. Figure 6 shows a sample of cost model interface including inputs form.

Cost model interface

Case Study and Application Examples

The case study presented in this paper is built around a friction welding machine (as shown in Fig. 7) to demonstrate the application of the developed cost model, i.e. to evaluate the cost of applying life extension strategy which will be used for the selection of optimised life extension strategy options by the DSF. The machine was manufactured by Harms&Wende (HWH), Friction Welding Machinery, Germany, one of the pilots participating in the RECLAIM project. Such welding machines are used for joining of welded metal parts and for a huge variety of materials like steel, aluminium, ceramics, brass, and copper. Friction welding machines include a variety of electrical (motor, convertor, controller, etc.) and mechanical (welding head, spindle, gear, clamping unit, frame, etc.) components which are relevant for maintenance tasks.

Friction welding system

In this case study, four components (motor, spindle, sample-holder and sample-detector) have been identified as core components because they are the most degradable of the machine. They will be indicated as “movable components” where they can either be repaired or replaced. The other components of the machine have not significant contribution to degradation of the machine, and accordingly they will be indicated as “static components”.

In addition, four life extension strategies have been identified in this case study to calculate the cost for: Refurbishment and three types of Corrective Maintenance. The Refurbishment strategy includes restoring the machine and bringing it up to date with satisfactory working conditions [7]. This is done by replacing movable components and repairing other static components of the machine. Corrective Maintenance strategies include performing set of activities after a failure or fault detected on the machine/component, so that it can be restored to perform the required function [7]. Here, Type-I Corrective Maintenance includes replacing the two main movable components (Motor and Spindle). Type-II Corrective Maintenance includes replacing only one main movable component (Motor or Spindle), whereas Type-III Corrective Maintenance includes replacing the other two movable components (sample-holder and sample-detector). It has been assumed that there will not be any repair activities being carried out for the static components during application of the Corrective Maintenance. This is due to that those components have negligible contribution to the degradation of the machine.

The initial cost model presented in this paper has been experimented on data collected from HWH pilot partner. The data and results were normalised because cost outputs will be varied when more requirements are incorporated into the cost model (see “5 5”). The normalisation of results will also be useful in comparing relative cost between different life extension strategies.

As a first step in case study application, cost of applying the Refurbishment strategy (benchmark strategy) was calculated based on resources consumption data shown in Fig. 8. Then, the cost of applying other types of Corrective Maintenance strategies were calculated by modifying activity resources consumed in the Refurbishment strategy (as described in “Cost Drivers and Cost Estimation Relationships”). Details of adjustment factors and type of work being done for each life extension strategy are listed in Table 3.

Cost model data for estimating Refurbishment cost

As can be seen in Table 3, the Refurbishment strategy includes replacing all movable components. Costs related to the application of the Refurbishment strategy are calculated based on resources consumed for each activity and price of new parts (as shown in Fig. 8). The repair cost of other machine components (static components) was estimated as 20% of the total Refurbishment cost. The cost of type-I Corrective Maintenance is estimated by considering 70% of the resources consumed during Refurbishment. Similarly, for type-II and Type-III Corrective Maintenance it has been considered that 50% and 5% of the Refurbishment resources will be consumed during application of these strategies, respectively. Also, during application of type-III Corrective Maintenance, both Sample-holder and Sample-detector will be changed because they degrade rapidly and have almost the same Mean Time To Failure (MTTF). It can also be noticed that the resources consumed during application of the strategy are very low compared to other strategies.

The assumptions and data used in developing and implementing the cost model have been confirmed by experts from RECLAIM partners as being within the reasonable ranges. This can be considered as initial validation of the cost model as more validation process will be needed when the model incorporates more requirements, such as variations of cost model data (see “Cost Model Requirements”). The cost model will also be implemented to more case studies of different pilots in the RECLAIM to investigate its generic applicability to as many industrial sectors as possible.

Cost Estimation Results

Figure 9 shows the normalised cost of different life extension strategies resulted from the case study in respect to the Refurbishment strategy cost.

Comparison of life extension strategy costs

Analysing total cost is an essential task to identify the main cost contributors to total cost. The pie charts in Fig. 10 show the cost breakdown as percentages for the different life extension strategies obtained from the developed cost model. It can be noticed that the Repair/Replacement activity cost represents the majority of the total cost. They are about 83%, 84%, 78% and 45%, for Refurbishment, Corrective Maintenance (I), Corrective Maintenance (II) and Corrective Maintenance (III), respectively. The following two big contributors for these four life extension strategies were Disassembly and Assembly activities, respectively.

Cost distribution for different life extension strategies

These results are considered preliminary as the developed cost model will be subject to further updates based on specific requirements, but they are appropriate for demonstrating the applicability of the cost model.

Discussion

A circular economy is based on restorative and regenerative approach in which products, components and materials are retained after use and put back into the value chain at their highest utility. In this context, the RECLAIM solution introduces innovative methods and tools that substantially allow ageing equipment that is near to its end-of-life to be brought back to operation through exploring and evaluating different forms of recovery strategies (e.g. remanufacturing, refurbishment, repair and reuse). Implementing such Circular Economy-driven actions can significantly extend the useful life of large industrial equipment, eliminate, or limit, high cost of replacement of such equipment and then improve the return on investment.

The cost model introduced in this paper constitutes one of the major tools that RECLAIM will deliver for heavy industrial equipment, in line with the circular economy. The cost modelling tool will be deployed to suggest cost-effective solutions (i.e. refurbishment, remanufacturing, etc.). It will also feed the decision support framework that is based on circular economy principles and standardised processes with the aim of improving the durability, flexibility and sustainability of heavy machinery in the industrial sector.

Conclusion

This paper described a framework for cost estimation methodology based on end-user requirements specifications to estimate and analyse the total cost for applying life extension strategy, e.g. remanufacturing/refurbishment, which will be used for comparison and decision-making concerning the most suitable life extension strategy for the industrial equipment. The proposed cost estimation framework integrates expert knowledge with activity-based costing method. It has been implemented in VBA-based Excel® platform and used through a case study to show its feasibility to evaluate and analyse the cost of different life extension strategies applied to friction welding machine.

Among the advantages of the developed cost model is that it uses less data for cost estimation. It requires to collect data for only one life extension strategy that will then be modified by expert to estimate cost of other life extension strategies. This allows for fast cost estimation results based on cost breakdown structure which enables to analyse the distribution of total cost and comparison between different life extension strategies.

The developed cost model will slightly be updated in terms of requirements and architecture. For example, to incorporate factors that might affect cost outputs such as variations in labour time due to type of technology used to perform the activity, variations in cost drivers rates, learning curve of the staff, type/quality of new parts installed, etc. Also, indirect costs such as “downtime cost”, i.e. the cost incurred due to the downtime resulting from the application of the life extension strategy, might be considered in the updated version of cost model. The developed cost model will also be demonstrated on other case studies of different pilots participating in the RECLAIM to investigate its generic applicability to as many industrial sectors as possible.

References

Bakker CA, Mugge R, Boks C, Oguchi M (2021) Understanding and managing product lifetimes in support of a circular economy. J Clean Prod 279:123764. https://doi.org/10.1016/j.jclepro.2020.123764

Patwa N, Sivarajah U, Seetharaman A, Sarkar S, Maiti K, Hingorani K (2021) Towards a circular economy: an emerging economies context. J Bus Res 122:725–735. https://doi.org/10.1016/j.jbusres.2020.05.015

Nikolaou IE, Jones N, Stefanakis A (2021) Circular economy and sustainability: the past, the present and the future directions. Circular Economy and Sustainability, 1–20. https://doi.org/10.1007/s43615-021-00030-3

Oliveira M, Miguel M, van Langen SK, Ncube A, Zucaro A, Fiorentino G, Passaro R, Santagata R, Coleman N, Lowe BH et al (2021) Circular economy and the transition to a sustainable society: integrated assessment methods for a new paradigm. Circular Economy and Sustainability, 1–15. https://doi.org/10.1007/s43615-021-00019-y

Geissdoerfer M, Savaget P, Bocken NMP, Hultink EJ (2017) The circular economy – a new sustainability paradigm? J Clean Prod 143:757–768. https://doi.org/10.1016/j.jclepro.2016.12.048

Mihelcic JR, Crittenden JC, Small MJ, Shonnard DR, Hokanson DR, Zhang Q, Chen H, Sorby SA, James VU, Sutherland JW (2003) Sustainability science and engineering: the emergence of a new metadiscipline. Environ Sci Technol 37(23):5314–5324

Fontana A, Barni A, Leone D, Spirito M, Tringale A, Ferraris M, Reis J, Goncalves G (2021) Circular economy strategies for equipment lifetime extension: a systematic review. Sustainability 13 (3):1117. https://www.mdpi.com/2071-1050/13/3/1117

van Dam K, Simeone L, Keskin D, Baldassarre B, Niero M, Morelli N (2020) Circular economy in industrial design research: a review. Sustainability 12 (24):10279. https://www.mdpi.com/2071-1050/12/24/10279

EMF (2021) Circular economy in industrial design research: a review. https://www.ellenmacarthurfoundation.org/circular-economy/what-is-the-circular-economyhttps://www.ellenmacarthurfoundation.org/circular-economy/what-is-the-circular-economy

Milios L (2018) Advancing to a circular economy: three essential ingredients for a comprehensive policy mix. Sustain Sci 13(3):861–878. https://doi.org/10.1007/s11625-017-0502-9

Accenture (2021) From survival to revival: Industrial post covid-19. https://www.accenture.com/gb-en/insights/industrial/coronavirus-industrial-post-covid19#::text=Industrial

Dissanayake D, Weerasinghe D (2021) Towards circular economy in fashion: review of strategies, barriers and enablers. Circular Economy and Sustainability, 1–21. https://doi.org/10.1007/s43615-021-00090-5

Wang Y, Zhu Q, Krikke H, Hazen B (2020) How product and process knowledge enable consumer switching to remanufactured laptop computers in circular economy. Technol Forecast Soc Chang 161:120275. https://doi.org/10.1016/j.techfore.2020.120275

Yuan X, Liu M, Yuan Q, Fan X, Teng Y, Fu J, Ma Q, Wang Q, Zuo J (2020) Transitioning China to a circular economy through remanufacturing: a comprehensive review of the management institutions and policy system. Resour Conserv Recycl 161:104920. https://doi.org/10.1016/j.resconrec.2020.104920

ERN (2015) Remanufacturing market study. Report, European Remanufacturing Network. http://www.remanufacturing.eu/assets/pdfs/remanufacturing-market-study.pdf

RECLAIM: (2021). https://www.reclaim-project.eu/

RECLAIM (2019) Reclaim: Communication and dissemination master plan. Report. https://www.reclaim-project.eu/resources/

RECLAIM (2020) Reclaim: Initial requirements specification. Report. https://www.reclaim-project.eu/resources/

RECLAIM (2020) The reclaim architecture specification – period 1. Report. https://www.reclaim-project.eu/resources/

Zacharaki A, Vafeiadis T, Kolokas N, Vaxevani A, Xu Y, Peschl M, Ioannidis D, Tzovaras D (2021) Reclaim: toward a new era of refurbishment and remanufacturing of industrial equipment. Frontiers in Artificial Intelligence 3(101). https://doi.org/10.3389/frai.2020.570562, https://www.frontiersin.org/article/10.3389/frai.2020.570562

Camargo M, Rabenasolo B, Jolly-Desodt A, Castelain J (2003) Application of the parametric cost estimation in the textile supply chain. Journal of Textile and Apparel, Technology and management 3(1):1–12

Masel DT, Judd RP (2007) Using bottoms-up cost estimating relationships in a parametric cost estimation system. In: 2007 ISPA-SCEA annual conference, pp 1–9

Ardiansyah R, Sutopo W, Nizam M (2013) A parametric cost estimation model to develop prototype of electric vehicle based on activity-based costing. In: 2013 IEEE International conference on industrial engineering and engineering management, pp 385–389. IEEE

NASA (2015) Nasa cost estimating handbook. Report, The National Aeronautics and Space Administration (NASA). https://www.nasa.gov/sites/default/files/files/01_CEH_Main_Body_0227_15.pdf

Curran R, Raghunathan S, Price M (2004) Review of aerospace engineering cost modelling: the genetic causal approach. Progress Aerosp Sci 40(8):487–534

Niazi A, Dai JS, Balabani S, Seneviratne L (2006) Product cost estimation: technique classification and methodology review. J Manuf Sci Eng 128:563–575

Aamodt A, Plaza E (1994) Case-based reasoning: foundational issues, methodological variations, and system approaches. AI Commun 7(1):39–59

Watson I (1999) Case-based reasoning is a methodology not a technology, pp 213–223 Springer

Goodall P, Graham I, Harding J, Conway P, Schleyer S, West A (2015) Cost estimation for remanufacture with limited and uncertain information using case based reasoning. J Remanufact 5(1):1–10

Ficko M, Drstvenšek I, Brezočnik M, Balič J, Vaupotic B (2005) Prediction of total manufacturing costs for stamping tool on the basis of cad-model of finished product. J Mater Process Technol 164-165:1327–1335. https://doi.org/10.1016/j.jmatprotec.2005.02.013

Qin PP, Liu CJ, Shu JW, Yan LY (2016) A case-based reasoning cost estimating model of hydraulic cylinder remanufacturing, pp 232–238. World Scientific. https://doi.org/10.1142/9789813208322∖_0027

Ghazalli Z, Murata A (2011) Development of an ahp–cbr evaluation system for remanufacturing: end-of-life selection strategy. Int J Sustain Eng 4 (1):2–15. https://doi.org/10.1080/19397038.2010.528848

Qian L, Ben-Arieh D (2008) Parametric cost estimation based on activity-based costing: a case study for design and development of rotational parts. Int J Prod Econ 113(2):805–818. https://doi.org/10.1016/j.ijpe.2007.08.010

Xu Y, Elgh F, Erkoyuncu JA, Bankole O, Goh Y, Cheung WM, Baguley P, Wang Q, Arundachawat P, Shehab E (2012) Cost engineering for manufacturing: current and future research. Int J Comput Integr Manuf 25(4-5):300–314

Langmaak S, Wiseall S, Bru C, Adkins R, Scanlan J, Sóbester A (2013) An activity-based-parametric hybrid cost model to estimate the unit cost of a novel gas turbine component. Int J Product Econ 142(1):74–88. https://eprints.soton.ac.uk/193725/

Smith AE, Mason AK (1997) Cost estimation predictive modeling: regression versus neural network. Eng Econ 42(2):137–161

Cavalieri S, Maccarrone P, Pinto R (2004) Parametric vs. neural network models for the estimation of production costs: a case study in the automotive industry. Int J Prod Econ 91(2):165–177

Duverlie P, Castelain JM (1999) Cost estimation during design step: parametric method versus case based reasoning method. Int J Adv Manuf Technol 15 (12):895–906. https://doi.org/10.1007/s001700050147

Almeida A, Cunha J (2017) The implementation of an activity-based costing (abc) system in a manufacturing company. Procedia Manuf 13:932–939. https://doi.org/10.1016/j.promfg.2017.09.162

Xu Y, Wang J, Tan X, Curran R, Raghunathan S, Doherty J, Gore D (2008) A generic life cycle cost modeling approach for aircraft system, pp 251–258. Springer

Yuchun Xu Jian Wang XTRCSRJDDG (2008) Manufacturing cost modeling for aircraft wing. In: The 6th International conference on manufacturing research (ICMR08). Brunel University, London, pp 817–824

Xu Y, Wang J, Tan X, Early J, Curran R, Raghunathan S, Doherty J, Gore D Life cycle cost modeling for aircraft wing using object-oriented systems engineering approach. https://doi.org/10.2514/6.2008-1118, https://arc.aiaa.org/doi/abs/10.2514/6.2008-1118

Susanti S, Yuniaristanto Y, Sutopo W, Astuti R (2020) Parametric cost estimation model for li-ion battery pack of e-motorcycle conversion based on activity based costing. https://doi.org/10.20944/preprints202007.0684.v1

Xu Y, Feng W (2014) Develop a cost model to evaluate the economic benefit of remanufacturing based on specific technique. J Remanuf 4(1):4. https://doi.org/10.1186/2210-4690-4-4

Xu Y, Fernandez Sanchez J, Njuguna J (2014) Cost modelling to support optimised selection of end-of-life options for automotive components. Int J Adv Manuf Technol 73(1):399–407. https://doi.org/10.1007/s00170-014-5804-9

Acknowledgements

The authors acknowledge all RECLAIM project partners for their support of the work.

Funding

The work described in this paper is part of the RECLAIM project “REmanufaCturing and Refurbishment LArge Industrial equipMent” and received funding from the European Union’s Horizon 2020 research and innovation programme under grant agreement No 869884.

Author information

Authors and Affiliations

Contributions

Nasser Amaitik: writing-original draft, methodology, conceptualisation; Ming Zhang: writing, methodology, conceptualisation; Zezhong Wang: methodology, conceptualisation; Yuchun Xu: methodology, conceptualisation, review and editing, supervision; Gareth Thomson: review and editing; Yiyong Xiao: conceptualisation; Nikolaos Kolokas: review and editing, conceptualisation, resources; Alexander Maisuradze: review and editing, methodology, resources; Oscar Garcia: resources; Michael Peschl: review; Dimitrios Tzovaras: review.

Corresponding authors

Ethics declarations

Consent for Publication

The authors declare their consent to publish this article in “The Circular Economy and Sustainability journal”.

Conflict of Interest

The authors declare no competing interests.

Additional information

Consent to Participate

The authors declare their consent to participate in this article and correctness of authors group, corresponding author, and the order of authors.

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Amaitik, N., Zhang, M., Wang, Z. et al. Cost Modelling to Support Optimum Selection of Life Extension Strategy for Industrial Equipment in Smart Manufacturing. Circ.Econ.Sust. 2, 1425–1444 (2022). https://doi.org/10.1007/s43615-022-00154-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s43615-022-00154-0